Executive Summary

Many readers of this blog contact me directly with questions and comments. While often the responses are very specific to a particular circumstance, occasionally the subject matter is general enough that it might be of interest to others as well. Accordingly, I will occasionally post a new "MailBag" article, presenting the question or comment (on a strictly anonymous basis!) and my response, in the hopes that the discussion may be useful food for thought.

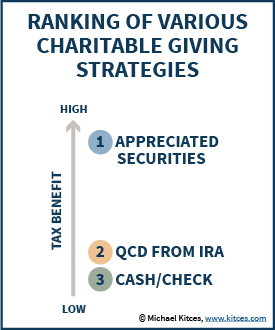

In this week's MailBag, we look at a recent inquiry regarding whether it's still a good deal to donate appreciated securities to a charity, now that the rules are back allowing Qualified Charitable Distributions (QCDs) directly from an IRA to a charity.

Donating Appreciated Securities Vs Qualified Charitable Distributions (QCDs)

Question/Comment: With the new rules allowing you to donate money from an IRA to a charity, is it ever appropriate to donate stock anymore? Wouldn't not paying up to 39.6% on an IRA distribution be better than not paying 20% on capital gains given the new rates for 2013?

In terms of tax benefits, it is true that with the return of Qualified Charitable Distributions (QCDs) in 2013, it is a better deal to donate from an IRA than to just donate cash. Nonetheless, it's actually still inferior to donating appreciated securities.

The issue is that while a QCD avoids an ordinary income tax rate of up to 39.6%, a donation of appreciated securities also gives a tax deduction that avoids a tax up to 39.6%; however, donating the appreciated securities also avoids a long-term capital gains tax, too!

An example may help to illustrate:

Client has $100,000 in three accounts: a checking account, an IRA, and some zero-basis securities. Assume a 20% tax rate on capital gains, 40% on ordinary income (makes the math easier, although technically a high income client would also face a 3.8% Medicare surtax as well). With respect to these three accounts, the client has a total net worth of $300,000, although some of it is pre-tax and some of it is after-tax.

- Scenario 1. If the client writes a check, that account is gone. The $100,000 donation by check gives a $100,000 charitable deduction, so if the client were to withdraw the IRA to spend it, the two would offset each other. In practice, the offset is never quite perfect; the income increases AGI and may impact certain phaseouts and credits, while the deduction may not be fully utilized in a single year and may have to be carried forward to a subsequent year. To account for the fact that the deduction may not perfectly offset the income, we can assume that the client ends out being able to spend about $98,000 of the IRA, losing the last $2,000 to the "tax slippage" of income and deductions. In the meantime, the client still has $100,000 of appreciated securities, which are worth $80,000 on an after-tax basis. The net result of this donation: the client's true after-tax net wealth remaining is $98,000 + $80,000 = $178,000 after doing a $100,000 donation.

- Scenario 2. Client does a $100,000 QCD from the IRA, eliminating the account entirely. The $100,000 in the checking account is all after-tax and can be spent anytime. The $100,000 of securities are still worth $80,000 after capital gains taxes. The net result: The client has $180,000 of after-tax wealth remaining after a $100,000 QCD, slightly better than Scenario 1, because there was no $2,000 "tax slippage" from trying to match above-the-line income and below-the-line charitable deductions.

- Scenario 3. Client donates appreciated securities. This produces a $100,000 charitable deduction, which can be applied against the $100,000 IRA, and with tax slippage once again the net value of the IRA would be about $98,000. The checking account is still worth $100,000 after tax. Net result: The Client donated $100,000 of appreciated securities, and has $198,000 of after-tax wealth remaining.

Not surprisingly, Scenario 1 - with no donation of appreciated securities, nor using the QCD rules - is the worst. Notably, this is also the result that would occur if the QCD rules didn't exist and someone just tried to do a direct distribution from an IRA to a charity anyway (taxed as a normal distribution from the IRA, mostly-but-not-fully offset by a charitable contribution of the proceeds).

Not surprisingly, Scenario 1 - with no donation of appreciated securities, nor using the QCD rules - is the worst. Notably, this is also the result that would occur if the QCD rules didn't exist and someone just tried to do a direct distribution from an IRA to a charity anyway (taxed as a normal distribution from the IRA, mostly-but-not-fully offset by a charitable contribution of the proceeds).

On the other hand, as the examples illustrate, Scenario 2 (using QCDs) is an improvement but it's ultimately Scenario 3 that wins by a healthy margin. In fact, the difference is attributable almost entirely to the capital gains taxes that were permanently avoided with the donation of appreciated securities, which applies in addition to the fact that there's a charitable deduction for the full fair market value of the stock. Certainly, the greatest caveat here is that the client needs to be able to use the charitable deduction over some reasonable time period; if donations are too high relative to income, the charitable deduction carryforward is lost after 5 years, and if deductions are too low and the client can't itemize the value is lost in the first place. And of course, in some cases the state tax treatment of charitable deductions can impact the outcome. But in the overwhelming majority of scenarios, the appreciated securities are the best outcome, and the results improve as either the capital gains tax rate or the magnitude of the capital gain increases.

It's also worth noting that donating appreciated securities also has greater flexibility, as they can be used to fund split-interest trusts (e.g., a Charitable Remainder Trust {CRT} or Charitable Lead Trust {CLT}), private foundations, or donor-advised funds, while QCDs can only be done to public charities.

This analysis is very clear in its outcome based on the stated assuptions in a vacuum. However, some other factors must be weighed for many clients; first, many affluent clients in pay mode still have massive capital loss carryforwards. Second, this removes any step-up potential for long positions not necessarily ready to be harvested. And lastly and most importantly, clients with the wherewithall to take advantage of QCDs to the tune of 100,000 are likely clients for whom generational Roth IRA planning would make sense. I think that outside of this vacuum if you run the numbers a Roth conversion would significantly outperform any QCD that is beyond a client’s RMD.

Michael,

Understood, but hear me out if you would. If the RMD is less than 100,000 you’re reducing the retirement account more rapidly than required. Regardless, a Roth would remove future RMDs for the IRA owner and hence, enhance family wealth from a generational perspective. I find clients engaged in QCD planning are affluent taxpayers who would be receptive to Roth planning. If you have a 100,000 RMD you likely have a sizable IRA and net worth. There’s my 2 cents, otherwise in a vacuum I agree with your thinking as laid out above.

Mike

Mike,

I don’t disagree with the value of Roth conversions. I’ve written about them extensively.

In point of fact, what you’re saying here supports what I wrote. Doing large QCDs is inferior to just donating appreciated securities, while donating appreciated securities also leaves the IRA available to be converted into a Roth (if that otherwise makes sense based on tax rates on other factors).

– Michael

Heya. I was contemplating adding a website link

back to your website since both of our web sites are based mostly around the same niche.

Would you prefer I link to you using your website address: https://www.kitces.com/blog/mailbag-is-a-qualified-charitable-distribution-qcd-from-an-ira-better-than-donating-appreciated-securities/ or blog title: MailBag: Is A Qualified Charitable Distribution (QCD) From

An IRA Better Than Donating Appreciated Securities?

. Please make sure to let me know at your earliest convenience.

Thank you

Michael,

Great info again. I agree with you on your replies to the other posters. I am not sure why Roth conversions are even part of this particular conversation. The question was in regards to donating money to charity, not intra-family wealth transfer. The mere gifting of the appreciated assets was a pseudo-conversion of the IRA. Yes, is an actual conversion a smart thing to do after the donation, probably, but in the end, the question was specifically about which assets to donate, not tax plays for the next decade or two or three.

Hi are using WordPress for your blog platform?

I’m new to the blog world but I’m trying to get started and set up

my own. Do you require any coding expertise to make your own

blog? Any help would be greatly appreciated!

Michael-

You lost me here. Don’t all of your scenarios assume that the #100,000 of appreciated securities have a basis of $0? You state that your assumption is that after paying 20 percent capital gains tax rate on $100,000 of appreciated securities that you will net $80,000. That would only happen if you had zero basis in the appreciated securities, which almost never happens.

Am I missing something here?

It also should be noted when you’re donating appreciated securities you’re limited to 30 percent of AGI if you’re claiming the current value of the securities on Schedule A. Carryforwards apply as you state.

Plus appreciated securities can be gifted to people with a lower effective capital gains tax rate. Heirs also get a step up in basis if you plan to leave the securities to them upon your death.

Dave

I really like what you guys tend to be up too. This sort of clever work and exposure!

Keep up the excellent works guys I’ve included you guys to my personal blogroll.

Michael,

You made a passing reference to it, but it seems that the new Medicare surtaxes (as well as income/means testing for Medicare premiums) factor into this for higher income individuals. Depending on how much gain the appreciated securities have, reducing the surtaxes using a QCD seems like it could be the better deal in some instances.

Corey

I’ve gone ahead and included a backlink back to your internet site from one of my clientele requesting it. I have used your webpage URL: https://www.kitces.com/blog/mailbag-is-a-qualified-charitable-distribution-qcd-from-an-ira-better-than-donating-appreciated-securities/ and blog title: MailBag: Is A Qualified Charitable Distribution (QCD) From An IRA Better Than Donating Appreciated Securities? to be sure you get the proper anchor text. If you woud like to see where your website link has been placed, please e mail me at: [email protected]. Appreciate it

If a retiree has no other itemized deductions, then the QDC could certainly be more beneficial than donating appreciated stock. The client can take advantage of their full standard deduction and receive a full tax benefit in the form of lower taxable income. The lower taxable income may also help the client write off more medical expenses and qualify for other 2% Misc deductions.

This scenario works well with people with less than 3million net worth with decent pension income with social security and a charitable mindset.

Michael, I just now read your 2013 post about QCD’s from IRA’s.

You compared the tax treatment of QCD versus charitably giving highly appreciated stock. I would find enlightening a similar comparison of (a) annually giving x dollars market value of a highly appreciated stock to a charity while holding the IRA for the children’s inheritance versus (b) annually giving x dollars QCD to the charity and holding the highly appreciated stock for the children’s inheritance when the children would receive a step-up in basis.

Dan,

Thanks for the suggestion! I’ve added this to the prospective topic list for consideration in the future! 🙂

– Michael