Executive Summary

A popular feature of permanent life insurance is that it accumulates cash value that can grow over time – ensuring that if the policy is surrendered, the policyowner will still have something to show for it that cannot be forfeited. However, this “non-forfeiture value” of a life insurance policy has an important secondary benefit as well – it gives an insurance company the means to provide policyowners a personal loan at favorable interest rates, because the cash value provides collateral for the loan.

Yet even as cash value life insurance operates as collateral for a life insurance policy loan, it also remains invested, earning a rate of return that slows the erosion of the net equity in the policy and allows a policy loan to remain in place for an extended period of time. And with some insurance policy loan strategies – such as the popular “Bank On Yourself” approach, there’s even a possibility that the cash value can out-earn the stated interest rate of the loan, allowing the loan to compound ‘indefinitely’.

The caveat, however, is that in the end a life insurance policy loan is still really nothing more than a personal loan from an insurance company, using the life insurance cash value as collateral. Which means even if the net borrowing cost is low because the cash value continues to appreciate, that’s still growth that the investor might have enjoyed for personal use, if the loan was never taken out in the first place. Or viewed another way, trying to bank on yourself doesn’t work very well when ultimately the loan interest isn’t actually something you pay back to yourself, it simply repays the life insurance company instead!

Life Insurance Cash Value: A Non-Forfeiture Benefit

When an individual simply pays for annual term insurance, the consequences of cancelling a policy are rather straightforward: the policyowner stops paying the premium, and the insurance company is relieved of its commitment to pay a death benefit if the insured passes away. The relationship is akin to a renter and a landlord – as long as the rent is paid, the renter lives in the property, and if the renter decides to move out, he/she simply stops paying the rent, and the two part ways.

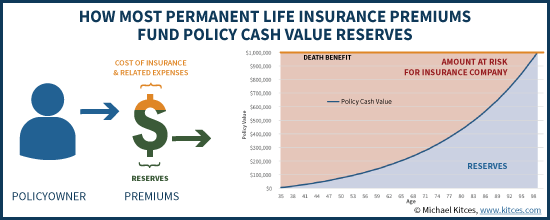

In the case of permanent insurance, however, the situation is more complicated. The insurance company offering permanent insurance is collecting far more in annual premiums than is necessary to “just” cover the annual cost of death benefit coverage, because the policy is designed to endow at its face value (i.e., have the cash value compound to the policy’s face value) at age 100. In turn, this means the insurance company holds an increasing amount of reserves, necessary to pay that fully endowed face value at the policy’s maturity date, should the insured actually “outlive” the policy. (Notably, policies issued for the past 10 years use more recent 2001 CSO mortality tables that extend the maximum life span of the policy to age 121.)

The significance of these reserves is that while with term insurance, if the policyowner stops paying the premiums the coverage is simply forfeited, with permanent insurance state regulators require insurance companies to provide some kind of benefits that cannot be forfeited even if the policyowner allows the policy to lapse. This non-forfeiture benefit, to return a (large) portion of the reserves associated with the insurance policy, is what we typically call the “cash value” of permanent life insurance.

The Life Insurance Policy Loan – A Cash-Value-Backed Personal Loan

While the origin of the “cash value” of permanent life insurance was as a non-forfeiture value for the policyowner – a share of the insurance company reserves associated with the policy that couldn’t be forfeited even if the policy lapsed – the existence of this “asset” is also what makes it possible to obtain a life insurance policy loan.

In fact, the reality is that a life insurance policy loan is really nothing more than a personal loan from the insurance company to the policyowner… for which the cash value of the life insurance policy serves as collateral. And the insurance company can confidently make the loan to the policyowner, at a relatively ‘favorable’ rate of interest, because it knows that if the loan is unpaid the collateral can be foreclosed upon and liquidated to repay the loan. Because the life insurance company controls the cash value that is serving as collateral to the loan in the first place!

In turn, the reality that the cash value of life insurance serves as collateral for the (personal) loan also explains why a growing loan can cause a life insurance policy to lapse – because ultimately, the insurance company doesn’t want to take any risk that the loan could ever be “underwater” (where the balance of the loan is greater than the collateral backing the loan). Thus, as the value of the loan approaches the cash value of the life insurance policy, the insurance company does in fact compel the liquidation of the collateral to repay the loan… even if that unfortunately causes the life insurance policy to lapse in the process!

Understanding Net Borrowing Rates And Insurance Policy Loan Spread

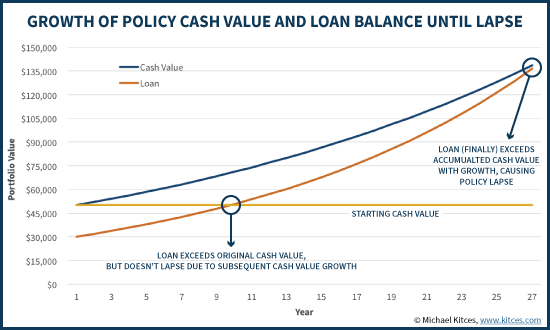

An important caveat to the dynamics of life insurance policy loans – and the fact that if the value of the loan reaches the total cash value of a policy it can cause the life insurance to lapse – is that even if no payments are being made on the loan and its balance compounds (or technically, negatively amortizes), the cash value as the underlying collateral of the loan continues to grow as well.

After all, the life insurance policy loan is still nothing more than a personal loan from the insurance company, using the asset value of the life insurance as collateral. Which means the cash value itself is still an asset of the policyowner, and remains invested with the potential to grow – just as the value of the underlying real estate can continue to grow, even though there’s a mortgage against the property.

But in the context of life insurance – where the value of the asset can grow almost in line with the balance of the loan, even when no payments are made on a life insurance policy loan – it can take a significant amount of time for the compounding loan balance to erode the net equity of the policy and ever trigger a lapse of the coverage. Or viewed another way, determining how long it will be until a life insurance loan causes the policy to lapse is based on the net borrowing cost (how quickly the loan is outcompounding the cash value asset), not just the stated borrowing rate on the loan.

For example, imagine a situation where a life insurance policyowner has a whole life policy with a $50,000 cash value, and takes out a $30,000 loan at a 6% interest rate, which means the policy has a net equity value of $20,000. With 6% compounding loan interest, the policy would lapse within nine years as the loan compounds to $50,684, eroding the net equity down to $0. However, if the underlying cash value continues to earn a 4% crediting rate, then the policy won’t actually lapse after nine years. Because by then, the loan balance may be up to $50,684, but the cash value itself would be up to $71,116 (which means the net equity has actually grown to $20,432!)!

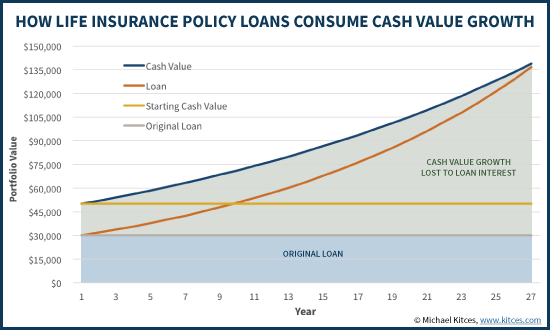

In fact, at these rates – where the loan compounds at 6% but the cash value (as collateral) compounds at 4% as well – even with no payments on the loan, it would actually take 27 years for the original $20,000 of equity in the policy to be eroded down to $0, causing the policy to lapse! (And in reality, it would take even longer, because subsequent premium payments into the life insurance would add even more cash value, increasing the size of the collateral and reducing the danger of policy lapse).

Notably, though, if the policy were to actually lapse at the end of this time period, the policyowner will be required to report gains and pay taxes based on the gross value of the policy ($144,000)! While the net value of the policy may be zero, as far as the IRS is concerned, the lapse of the policy is still the surrender of a policy worth $144,000 – even if the policyowner is required to use all $144,000 to repay the outstanding personal loan!

The Problem With Trying To Bank On Yourself With Life Insurance Policy Loans

Recently popular life insurance loan strategies like “Bank On Yourself” and “Infinite Banking” rely heavily on the idea that when an insurance policyowner borrows from a life insurance policy, they are “borrowing from themselves”, often at a very low net loan spread. Some even have the potential that the underlying cash value may outearn the borrowing cost anyway (between the growth in cash value and potential dividends from a non-direct recognition whole life policies, or the upside potential from the crediting methods of equity-indexed universal life policies).

And while Bank On Yourself is "legit" in that borrowing and repaying life insurance loans is a way to tap the cash value of a life insurance policy without surrendering it, the big caveat to these scenarios, as discussed earlier, is that ultimately someone who takes out a life insurance policy loan isn’t actually “banking on yourself” at all. The reality is that it’s just simply taking out a personal loan, not unlike a credit card loan, a mortgage, or a P2P loan, for which loan interest will be paid. The difference is simply that the loan happens to come from a life insurance company, and can be done at a relatively appealing rate of interest thanks to the cash value of the life insurance serving as collateral for the loan. Still, the borrower is really doing nothing more than taking out a personal loan and racking up loan interest while using their cash value life insurance as loan collateral! In other words, a life insurance policy loan isn't "banking on yourself" any more than taking out a home equity line of credit is "banking on your house".

Similarly, while it might be appealing to have a low net borrowing rate like 2% (and for some policies, the net borrowing rate can be as low as a 0.25% loan spread!) the reality is that the key driver of borrowing from a life insurance policy is not actually the “net” borrowing cost (the difference between the loan interest rate and the crediting rate), but simply the loan interest rate itself! A small net borrowing cost may ensure that a loan can remain in force and negatively compound for a longer period of time before the equity is eroded… but that simply means more money is “lost” to the insurance company in the form of cumulative loan interest paid over time! Because the policyowner is still ultimately paying the entire cost of the loan interest rate!

For instance, continuing the earlier example, where a 2% net borrowing rate meant a $30,000 loan against a $50,000 policy wouldn’t actually lapse for a whopping 27 years… when the policy does lapse, it terminates with a $144,000 loan (and a $144,000 cash value to repay that loan). However, in the long run, this means the policyowner only got to use $30,000 of the cash value (via the loan), and never got the benefit of the $114,000 of growth over the subsequent 29 years! Because all of that growth was consumed by compounding loan interest! (Which the IRS recognizes in taxing the policy surrender based on the $144,000 of gross cash value – even if it’s all used to repay the loan, the policy itself was still worth $144,000 when it lapsed, producing a significant taxable gain!)

Notably, even if the growth rate of the cash value is better, and manages to exceed the borrowing rate, this may allow the life insurance policy to remain in force for a longer period of time, but it still means when the policy lapses that the policyowner pays the tax bill for all the upside growth of the cash value even though he/she never got to use it (beyond having it be consumed in covering the interest on the policy loan)! Again, the policyowner “uses” only $30,000, and never sees the $114,000 of growth (beyond the tax bill that’s due on it!).

As noted earlier, the appeal of some “Bank On Yourself” strategies is that the policy may actually earn a positive loan spread, where the growth of the cash value actually exceeds the loan interest rate. However, the challenge in today’s environment is that arguably the risks are far greater that a policy will underperform its borrowing cost, rather than outperform. In fact, the concerns about “excessive” and overstated return assumptions in equity-indexed UL policies (and the unrealistically favorable loan projections that result) has become so problematic, the National Association of Insurance Commissioners (NAIC) recently enacted Actuarial Guideline 49, specifically to crack down on the return assumptions in EIUL policies. The new rules are expected to result in a maximum projected crediting rate for loan illustrations of only about 7%, and some commentators have suggested that even 7% is still unrealistically high in today’s environment. (To put it in context, restrictions on variable universal life illustrations first adopted by FINRA in 1994 required that VUL policies “only” illustrated a 12% average annual growth rate for equities, which as we now know in retrospect was still far too aggressive as well, because regulators still tend to err to the high side!)

The bottom line, though, is simply this: in the end, a life insurance policy loan is really nothing more than a personal loan from a life insurance company, for which the cash value of the life insurance serves as collateral for the loan. This may allow for relatively favorable loan interest rates (thanks to the collateral), and the loan may be able to negatively amortize and still sustain for a long time (as the small net loan spread means it can take a very long time for the long to be underwater). Nonetheless, even if the policy loan takes decades to eventually compound and trigger a lapse – or be repaid from the death benefit if the insured passes away – the fact remains that a life insurance policy loan is not really a way to “Bank On Yourself” at all, it’s simply a strategy for taking out a loan and paying loan interest, which as with any borrowing should be used prudently to avoid accumulating significant loan interest over time!

So what do you think? Do you view life insurance loans as a viable cash flow strategy? Are you thinking about life insurance loans differently by recognizing they're simply a personal interest-bearing loan using life insurance cash value as collateral?

If your a HIGH INCOME EARNER and need a tax deffered vehicle above your Employer Plan, IRAs, Roth IRAs – Cash Value Life Insurance Can be a decent way to accumulate another next egg. You could also buy Muni Bonds. Depends what you are looking to do, many ways to skin a cat. Life insurance for Estate Planning over the 5MIl. Single and 10Mil Married is an excellent Strategy. With the Tax Bills looking at reducing Estate Taxable values it will be even more important for Affluent clients to consider ILITS.

Question is can you be a Fee+Commission advisor and give this advice in the best interest of the client or should you have to refer the business out?

Excellent article. I have been battling this in my practice in recent weeks. I have come in competition with many “Be Your Own Banker” guys. Having a background in insurance, I knew the concept didn’t smell right but haven’t done the math to prove my points. Thanks for taking the load off of my shoulders!

This article only proves an unrelated point that unserviced loans are not good for clients. Unfortunately, if you are trying to disprove the “banking” strategy’s validity, you have an uphill battle against the facts. That said, if you are uninterested in the facts and just want your client to yourself, there are actually myriads of opinions out there to back you.

If you want to keep your clients in house and you are licensed to sell insurance or have a trusted ally who can, you may have better luck proving the following: Many agents promoting this strategy use inferior carriers (that pay higher significantly higher commission rates than the best of breed carriers) and/or design the policy in a way that it pays more commission and therefore credits less to the policyholder.

-Hutch

Thank you for this interesting article Michael. I think it will be helpful for a lot of people to get into the nuts and bolts of how this strategy works.

As you know, the life insurance books don’t deal with an example like you detailed above, and I doubt many agents would deem this an ideal strategy either.

The true “Be Your Own Banker / Bank on Yourself” strategy is to pay back the loan to yourself, including the additional interest that you would have paid under traditional financing. (The traditional example is to show how it works for financing a car every X years.)

The results for this are far different than those illustrated above, especially when repeated over and over in the course of 20, 30, or 40 years.

I illustrated just this morning, taking a retirement income tax free cash flow stream to a long-time Surgeon client of mine of $200,000 each year, for a duration of 15 years, or $3,000,000 of cumulative cash flow. The order and elements of the tax free cash flow were first a tax-free surrender of dividends down to cost basis, followed by policy loans taken against the policy thereafter, with no payment of current or accrued interest for the life of the contract. I’m also able to include the cash value rate of return, and in a zero percent tax bracket, we consistently net a 5% cash value ROR during the entire loan period and for the duration of the client’s lifetime (until his age 100). If the male Insured dies at his age 92, there is still a net income tax free death benefit of an approximate $1.4mm and the loan is repaid at the time of his death.

The loan illustration is with a top mutual carrier, and is based upon their general portfolio rate of return dividend scale including current expenses and mortality. The dividend crediting rate has slowly declined over time, and the $200,000 in annual policy loans is based upon the static dividend illustration projection, so we are cognizant of the fact that we will need to monitor and perhaps reduce the $200k if dividend rates continue their slow decline. Nevertheless, in the client’s 40% retirement tax bracket, $200,000 of net cash flow, is the pre-tax equivalent of $333,000 per year, or, $5,000,000 of pre-tax cumulative income over the 15 year time span. This cash flow also pays for his long term care policy premium (income tax free), and can also be used as a cash buffer in the event of poor or bear equity markets. The cash values also substitute for an emergency fund, so instead of earning 0% on Money Market or short term bonds, we instead capture 5% tax deferred, and once accrued within the policy cash value, the cash value cannot decrease, it is impervious to market declines. Finally, the cash values replace the bond element within my client’s overall investment portfolio, allowing for higher equity allocation percentage. What’s not to like, or love, actually? PS We also took advantage of QLAC’s using this approach for both he and his wife, because with this enormous tax free cash flow for 15 years, we don’t need the projected IRA RMD’s at age 70.5. Even more advantages, but this is sufficent for now.

Wow! What was the commission on that policy? 🙂

Inconsequential compared to the millions of dollars derived for the Client, plus 25 years of quality service and advice.

Very interesting discussion as I have a run-away loan in a single premium whole life policy that I bought 28 years ago. The company’s illustrations show the cash surrender value will exceed the loan value up to age 100 provided the guaranteed interest rates and current cost of insurance remain the same. But if I cash it out now I understand I would pay heavy taxes on both the cash value and the loan value! Does one just wait till death and let heirs recoup whatever is left of the tax-free cash value…and risk an increase in the cost of insurance that wipes out the policy? Or are there other alternatives?

If you’re still insurable, 1035 into a new policy, carry the loan. After 6 months (or 1 year…wishy washy IRS guidence) withdraw from policy to repay loan. Product design/assumpion will determine if there will be any sustainable death benefit or CV.

This concept is commonly, referred to as loan rescue. Whole life policies are dangerous. Especially with loans.

Be VERY careful with this approach so as not to generate taxable event if policy loan exceeds policy cost basis at time of exchange. Many carriers will not permit the exchange when this is the case, Hancock will, and they may even help finance the policy rescue. If your SPL is pre-1988 issue? That’s a whole additional question and potential problem for you perhaps.

28 years ago brings you to 1988, which is the pivotal year. I would check with the carrier to confirm your policy is not a MEC. Either way, the safest way to play it would be to spend down other assets and leave behind the full tax free death benefit. If the cash value has hit corridor and is causing the death benefit to increase you probably have less risk than you think of the policy lapsing due to increasing rate of insurance inherent in universal life. Although your cost per unit of insurance increases with age, you are only charged for the net amount at risk. If the policy has indeed hit corridor you can probably take a tax free withdrawal to basis without risking lapse. Since this older policy has no overloan protection rider, you will have to be careful managing tax-exempt loans after that, but it is possible. It can even be quite useful during market downturns to supplement income and let your stocks heal. However, excessive loans should be paid back to avoid the problem Michael discussed. This reply is meant to be educational only. Please verify, test, and measure everything for yourself with the carrier and your servicing agent.

Execute a policy change to reduce policy loan down to policy cost basis (your cumulative premiums). See if that helps. Next, ascertain minimum amount of interest payment you need to pay each year to avoid policy implosion. Both of these approaches should help you mitigate policy lapse in the future. Finally, how old are you today, and, how’s your health? Actuarially, very few men live to age 100.

All three of you are really terrific! I’ve taken this policy to two “experts” who had no idea what could be done. To answer some of your questions…I am 70 years old and in excellent health – I do expect to hit that 100 mark! My policy was purchased on 5/12/88 – a whole 39 days before the 6/20/88 MEC effective date. (I had no idea what MEC was so I did some homework.) One thing I read was that if you 1035 to another policy it will likely be impacted by the MEC ruling. I certainly would like to tap into the cash value if needed. My policy does say that it will terminate on the policy anniversary on which the insured is age 100. Does that mean it would no longer be tax free? Another concern is that I recently found out the insurance company (Fidelity & Guaranty) was purchased by Anbang, a Chinese conglomerate and they have made no attempt to even inform their policy holders of this change – not very friendly, but I assume they must still comply with all U.S. laws. Don’t know if all this changes your recommendations, but I certainly do appreciate your professional advice..

Will your policy terminate at your age 100? or, endow at your age 100. These are two very different definitions with two very different results for you.

The Policy’s Termination statement is “This policy will terminate at the earlier of:

* The effective date of its surrender to us.

* The expiration of 31 days after notice of written termination has been mailed advising that the policy loan and interest equal or exceed the policy’s cash value without any payment being made.

* The Insured’s death.

*The policy anniversary on which the Insured is age 100.”

Does that mean I would be required to take cash value prior to age 100 and lose its tax-free status? What a great health incentive that would be!

Excellent article. What if the policy holder paid back the loan over a 4 to 6 year period of time just as they would with a normal loan? How would that affect thing’s?

They’d pay loan interest for the time they took out a loan, and their collateral would continue as it otherwise does. Again, it’s just a personal loan, for which the life insurance happens to serve as collateral…

– Michael

But my understanding is unlike a bank loan, you wouldn’t have to “qualify”, it’s no questions asked. You can take out your money even up to your bases like with a Roth, but the nice thing is you can put it back “anytime” unlike a Roth you have 60 days. It also works well for people who can’t contribute to Roths due to income max and for businesses who have large cash-flow on their books for several years and want to get a better long term return than the .01% in the bank. You can over fund the policy up to MEC level and have access to that cash but it still can earn dividends will it’s just sitting their in the bank.

If you put the money into the life insurance policy, you still have to PAY LOAN INTEREST to borrow your own money.

If you put it in the bank (or invest it elsewhere if you prefer), you don’t have to borrow it and pay loan interest at all. It’s your money. You can just withdraw it. All of it. At any time.

Ultimately, the fundamental problem if that tying up the money in a life insurance policy means you often HAVE TO borrow it to get it back. It’s akin to putting all your money into real estate and then borrowing it back with a mortgage if you need the cash. Yes, you can get a mortgage at a low fixed rate. But it’s still a loan to access your own capital once you make yourself illiquid. The same is true with a life insurance loan.

– Michael

You always do have the option of removing the money from you cash value as a distribution (withdrawal), which is tax free up to basis.

When you borrow against the cash value of a life insurance policy you aren’t withdrawing your own funds. They stay in the policy and continue to compound. When you take a policy loan you borrow the insurance companies money on which you pay interest. If your funds were in stocks or a bank account as you suggest, you don’t get the advantage of the continual compounding of your money because you’ve either had to cash in the stock or spend the savings.

Mike, I think the real story here is not economic but one of ease. Your future ability to obtain a quick loan can be tremendously compromised by all kinds of events. A loss of wage income, assets that lost value or maybe undesirable given current events, expensive drawn-out loan processes dealing with appraisals and high loan costs (fees & interest) all may affect your ability to obtain a quick loan when you need one. And let’s face getting a policy loan at a 6%- 7% rate, is pretty quick, no questions asked.

Certain carriers allow you to contractually lock in your cost to borrow at 5%-6‰ for the life of the policy.

John,

Have you seen any data on the percentage of carriers/policies still offering fixed rate loans for NEWLY issued policies?

These were routine in the past, and my impression is that they’re “less common” now, but I have no idea what the real ratio is of newly-available policies today that offer fixed rate vs floating rate loans?

– Michael

No I have not seen a comprehensive list. I just keep my pulse on the marketplace. We have certain criteria where we classify carriers by tiers or tranches. And to be clear some have fixed rates, but then will offer suppressed crediting on loaned money. A small subset of carriers will lock in the cost to borrow or at least have a reasonable top-end cap on the loan interest rate and still offer unchanged index crediting on loaned money. There are 7 that I would consider putting a client’s money with. Four I like a lot and three others not as much, but still may be worthy if say any of those 3 were going to be more forgiving underwriting a particular client.

There are still other levers the carrier can pull to recoup that opportunity cost in a high interest rate environment (raise COI, lower caps), but if a client plans to use a policy mostly for BYOB or take tax-exempt loans in retirement, it’s comforting to at least peg the loan rate by choosing one of these carriers.

-Hutch

Which four do you like a lot, and which three not so much?

Sorry, Lucas. We are carrier agnostic and constantly gravitate to best of breed in an ever-changing market. For a post that may live forever, I’m not going to go on record touting any one carrier over another. Your favorite IMO/FMO should be able to help with this. However, some of them will probably have an agenda since they usually concentrate business to one or two carriers who give them sweetheart overrides. If they’re a good operation they should be able to help with the fairly straightforward question of, “Which carriers offer contractually locked or capped loan rates where loaned money still participates in full index crediting.” If you don’t get to at least 5, find another FMO.

-Hutch

Wow, what an awful article that really misses the point entirely. No one should own Cash Value life insurance – ever. It has many flaws, but the fact that you specifically taught the merits of this “personal loan” is deceiving. It is not a personal loan – you are borrowing your own money! Cash value policy companies overcharge premiums in order to provide several benefits. The first problem is that you can only get ONE of these benefits at any time(unless you can figure out a way to live and die at the same time). Another problem is when you borrow from a cash value policy, you are borrowing your OWN money. And they will never let you borrow more than the surrender value and the future premiums can support. If I had bought a tem policy and invested the difference in premiums, I would have much MORE money that I could access at no cost…. So let’s say I have this great investment for you. Invest with me & I’ll pay you 4% interest to use your money. If you want it back, I’m going to charge you 7% interest, and if you die, I keep your money. Still want to do business with me? Hell no! But that is exactly what cash value life insurance is !

CV Life has so many other uses than this, Bob – you’re painting with quite the broad brush. I do not sell insurance (fee-only), but I still recommend its uses. Most of my older clients (past the years that people typically buy term) still have insurance needs, whether to pay off the mortgage on the retirement house, to replace a single life pension on spouse, estate equalization for siblings, etc. Those that don’t have it almost always wish they had gotten a little.

I can’t say that I would recommend this BYOBanker concept as the primary reason for purchasing CV Life, but it does provide other important benefits to some.

Bob, please read my enlightening comment below. Why is it my Harvard MBA and CPA clients are the biggest buyers of permanent whole life insurance? These guys put in $100,000-200,000 of annual premium into their permanent life programs. My only regret is that my current cash value (currently $1.44mm) is not more. My tax free cash flow during retirement is going to be pretty remarkable. Plus, I recapture all my premiums back income tax free-and this includes the premium allocated to the death benefit or term element of my premiums too. My cash values also replace the bond element of my investment portfolio 100%. I don’t own a bond or a bond fund or ETF anywhere. And I enjoy a current cash value ROR (5%) far superior to any current new money rates. Plus I can take taxable gains from my cash values-income tax free via 1035 exchange to pay my long term care policy premiums for life. Plus my cash values act as a retirement buffer against down equity markets-adverse sequence of return risk will never ever apply to either me or my wife. Plus I don’t need a 0% Emergency find of Money Markets or short term bonds at all because my 5% tax deferred growth liquid cash values replace that 0%, which means my overall portfolio ROR just received a nice boost. Plus when I die, the death benefit of my permanent life insurance will replace my spouse’s lost SS check, because she’ll opt for mine as her widow’s SS benefit, and lose hers, won’t she. No term policy accomplishes replacement of that lost SS check, does it Bob. Plus my permanent cash value life insurance is excellent bank collateral, I’ve negotiated loans in the past with 200 basis point reductions because Bankers love it when I assign a cash value life insurance policy to collateralize the loan. I call it “credit credibility”. I could go on…but I suspect you now recognize and appreciate the myriad, countless and unique advantages my permanent life insurance fortress has and will accomplish as a portion of my overall wealth accumulation strategy. My life insurance defense, enables me to be far more aggressive on investment risk offense. because I own and enjoy a fantastic base to my financial pyramid.

Lots of “highly educated” people gave Bernie Madoff Billions so I’m not sure that is a good indication of a strategy’s merits. This is not to say that life insurance isn’t a great tool in some situations, especially for ultra high net worth, but most people being sold on the “bank on yourself” strategy could benefit from this article.

Actually, the examples Michael used focus more on unserviced loans and don’t really illustrate what’s being recommended with the “banking” strategy. I do agree with you that the higher your net worth is or moreover the higher your current and anticipated income tax bracket is, the more powerful the strategy becomes. It can still pencil out for above-average joe’s and even average joe’s, especially if they have conservative risk tolerances.

Ditto…

Bob,

I’m really not certain how you interpreted this article was “teaching the merits” of life insurance loans…

That aside, your statement that “you are borrowing your OWN money” is simply factually incorrect. Read the contract. A life insurance policy is a personal loan for which the policy simply serves as collateral. And as with any lender, the company doesn’t loan you more than the value of the policy because they’re not willing to extend credit above the amount of the loan collateral…

– Michael

Nothing more than a clever way of selling life insurance.

Actually it is more than that, but it does entail substantial education in a realm you’re probably not familiar or comfortable with.

fantastic post. I really never understood how the loans actually worked, they sound earily similar to reverse mortgages.

i’ve never seen the “tax free” life insurance argument for retirement cash flow pencil. it’s an argument to sell insurance but mathematically makes no sense. this article touches on just one aspect. arguably more important is the fact that you can never “borrow” the full amount of the cash value or the policy will lapse causing a taxable event. so your access to liquidity is extremely limited. life insurance salesmen will often quote the cash value growth as tax free but neglect to say that only a small portion is actually available without a lapse.

Your uses of the phrases “your access to liquidity is extremely limited” and “only a small portion is actually available without a lapse” actually bolsters your earlier contention that you personally have never seen the tax-exempt component of life insurance pencil out, but that only speaks to your lack of exposure and knowledge on the subject. – Hutch

On the contrary hutch. Your contention that a client has access to the full cash value for any amount of time without causing a taxable lapse reflects your limited knowledge. The description you use, 90% year one or 100% year 5 are sales tacticts. You neglect to add that the client must put the cash back quickly to avoid a taxable lapse. So if the client has a real need for cash that is longer term i.e. theyre retired, the taxes will eat them up. I’m happy to take this offline if you have an illustration that proves otherwise

Tim, I’m not selling anything here. I’ll be respectful of Michael’s wishes, but one could even argue that your sensationalized comments are sales tactics that you’re employing to keep more AUM. Uniformed and incorrect blanket statements like that, especially using the words “never” and “extremely” when it’s so far from reality, really bother me.

By 100% year 5, I meant of the client’s basis in the policy and this can be achieved (not always) by overfunding to the MEC limits certain products designed for high early cash value. It could happen in year 4 or 3, maybe in year 6 or possibly later depending on how actually crediting goes, but that would be an extreme case. Even staying within the constraints of AG-49, year 5 was being conservative with certain policy designs. I’m not going to waste any more time splitting hairs, but I think it’s safe to say that your prior comments (4 posts up) saying how only “a small potion is available” and access is “extremely limited” are both WAY OFF BASE. They are not even close to the truth whether or not you have “never seen it pencil,” which is obviously true.

If you reread Michael’s article you will see that your more recent comment (1 post up) that a “client must put the cash back QUICKLY to avoid a taxable lapse” is also incorrect and way off base. Read the part of Michael’s post by the pictures and you will see the flaw in your statement.

Most clients don’t want to liquidate or borrow against their entire cash surrender value because they don’t want to lapse the policy for multiple reasons. Although that may be a big concern for you, I have never had a client find that to be even close to a deal-breaker.

I am happy to spend time with you citing specific illustrations, but I will need to collect a “fee only” retainer for my time. In lieu of getting educated on the specifics, I suggest not using such extreme language on subjects where you are clearly out of your element. If we were in a competitive situation with a client, you would have discredited yourself many times over by now.

-Hutch

Hutch,

the ability to withdraw 100% of basis in 5-7 years is not a benefit worth mentioning. I can get 100 % of my basis out of a checking account in 1 day. I’m very specific in saying that the ability to borrow against the Cash Value is limited without risking a future lapse.

Michael’s article shows that “borrowing from yourself” is misleading. I’m arguing that “tax free” retirement income is also misleading because you can only access a fraction of the cash value (unless you plan to pay it back to the insurance company). I’m going to avoid personal attacks like “discredited yourself” and stick with facts.

Tim,

I’m glad that you’re now deciding to start focusing on facts. The one you’re harping on however isn’t why people do the strategy nor why it’s promoted. I’m not mentioning that having access to your full basis as any of the main benefits. I was doing so to refute your prior outlandish claims about having “extremely limited” access.

If not having access to all of your cash value at anytime is your main concern you should indeed stick with your checking account. Although I retain “sufficient” access to capital, the benefits that I get for sacrificing some access is a permanent death benefit, a significantly better rate of return on my risk-off assets, tax deferred growth, and yes tax-exempt distributions. And yes I do give back some of these benefits when I utilize the loan feature, but still come out ahead of the checking account. Last time I checked more is still better when it comes to money.

It’s true that I shouldn’t access every dollar of it ever and must leave at least a small fraction behind at death to preserve the tax sanctuary. However, since I earned a better rate of return than someone who left their risk-off money in a checking account, I will have a much bigger number to draw from (when isolating this pool of funds). So I don’t need to take ALL of it to create more net after tax income from this pool of funds than someone who opts to have full access from the jump in a checking account. Nor do I want to. I actually have some legacy goals, and I’ve found that the best clients to work with do as well.

So showing clients a properly structured “tax-free retirement” scenario is not misleading at all. It’s the same thing we all teach regardless of your financial product(s) of choice – delayed gratification to acquire a certain set of benefits. If the benefits that this strategy offers don’t appeal to you or your clients then we’re in totally different markets. Go forth and prosper, but there’s no reason to sensationalize and bash a perfectly viable strategy just because you’ve chosen to have a personal problem with it.

-Hutch

I don’t have a personal problem with anything Hutch. I agree, it’s better than a checking account. I disagree, that you only have to leave a “small fraction” to keep the policy in force over ones lifetime. a client will have access to more capital for retirement from a diversified portfolio net of all tax, that’s a fact. so if retirement income is the primary goal, life insurance is not the right vehicle. If the primary goal is legacy planning, life insurance is a great vehicle. I’ve made my points and moving on.

Actually you can probably verify with your compliance department that the following statement you made is not a fact as you have claimed, “A client will have access to more capital for retirement from a diversified portfolio net of all tax.” If you can produce a client agreement backing that statement up, an ADV, and proof of sufficient E&O coverage I will sign on as a client on Monday with funds I currently have allocated in insurance products with contractual guarantees and tax deferral.

Let’s be clear that your other statements about which are the right vehicles for various goals are also your opinions, not facts. As an American you are entitled to your opinions as well as the freedom to share them on any forums you like. So I am happy to move on too.

-Hutch

Well said. How can the statement “a client will have access to more capital in diversified portfolio…” be a fact, when IN FACT, none of us know what the markets will do in the future, especially for an individual portfolio?

assuming the same underlying gross investment returns, the statement is correct. one has an insurance cost, the other doesn’t. one has income tax on growth to access all capital, the other capital gains. one is better for retirement income, the other is better for legacy planning. there’s nothing sensationalized about it.

Tim,

I’m sure your simplistic classifications suit you well. Unfortunately I know too much, so I can’t just blindly accept those types of blanket statements or assumptions. You can do what you want with the following information, including turn a blind eye to it:

Did you know that once an overfunded insurance contract hits corridor the all-in annual costs of the policy will be in the range of ETFs? You may have to do some research on the “corridor” thing before you fully grasp some of this information.

Did you know that the aggregate all-in lifetime expenses of an overfunded life insurance policy will often be far less than managed money (not even including the ongoing taxation of AUM)?

Did you know that since an agent receives the bulk of their compensation on the smallest balance a life insurance policy will ever have, they often stand to make far less than the investment advisors accusing them of making insurance recommendations based on compensation?

Did you know that low basis stocks and funds can often be much more powerful legacy tools than leaving behind a life insurance policy that has already hit corridor?

I actually consider the word problem of distribution and legacy planning to be much more complex than your prior statement on the matter. I therefore don’t attach such remedial qualifiers to asset classes when analyzing fact patterns. We could go on for days, but it’s not a good use of either of our time.

I sincerely hope that someday I meet one of your very best clients and then we can resurrect this discussion. At that time the only opinion that will matter will be there’s.

Did you know that a client who draws from a 3% yielding muni portfolio in equal installments over 30 years until the value is $0 will have received more after tax capital during their lifetime than the index UL policy you describe? I already have plenty of life insurance salesman after my clients.

More “factual” financial planning advice on the internet by some guy named Tim with no last name.

John,

I have followed your thoughts through your running “scrimage” with Tim and I must congratulate you on the sophisticated cogency of your knowledge. You write well (grammar and syntax, ignored, get me “turned off”) but your flowing thoughts managed to elicit a “page turner”) label from me. I am impressed.

Best regards…

G. Jerry Nwosu, MBA

Ex-planner/Advisor

P/S: The recent overkill (DOL) has soured my enthusiasm for these matters.

Guys,

Just a friendly reminder to keep the conversation civil and away from personal attacks.

Respectful disagreements and constructive discourse remain open and welcome here, as always.

– Michael

I’ve looked at hundreds of projections for these life insurance strategies and it always seemed like you had to squint at them to make the numbers work. It’s nice to see that it wasn’t just me.

Are there people/situations for whom cash value life insurance makes sense? Certainly. Would most people be better off buying term and investing/saving the difference? Probably. Do the large and undisclosed commissions play a role in recommending these strategies? You decide.

As a side note, the biggest red flag for me with these strategies is that they always used projections of what COULD happen and were never able to produce examples of what REALLY happened (which is especially true of VUL and EIUL policies).

It’s tough for an analytical person like me to accept, but people’s behavior isn’t always the best numerical answer. In the 11+ years I’ve been in this business, I have NEVER seen someone “invest the difference”. It’s used as an excuse for a lower monthly premium, but they never even know what “the difference” is!

I still recommend whole life insurance in some situations, I don’t sell them (fee-only), so I get $0 extra for my recommendation. When you combine the cash value accumulation (w/o ongoing taxation), the ability for the policy to self-complete in the case of disability (basically a DI policy in the amount of the premium), the value of the underlying “term” insurance, etc., often the WL policy can serve as a pretty good substitute for a portion of their fixed income/bond allocation. It depends on age, health, other resources, etc. but I have seen it work quite well.

11 years in the business and never seen or helped anyone “invest the difference”?? AND you are fee-only? Wow. I’d be interested in learning how you get your lower to middle income clients out of the financial basement and on to a higher level. I know Michael, I’ve gotten way off track from the focus of your original article! But , while we might have differences of opinion, I do enjoy the thought process of other advisors. Keep it up!

I’ve helped many people do it; I’ve never seen someone do it on their own.

Your “always” and “never” statements are far from true. Although IUL is a relatively young product, Pacific Life has a piece showing what they illustrated and what actually happened in the last 10 years. Also Mass Mutual has some great “compliant historical” pieces showing what actually happened that go back decades for various WL products at much older less efficient actuarial tables used. You can ask you local wholesalers for each.

About your BTID comment, you’ll easily win for a risk-on asset class vs. a risk-off asset class. But what about your best bond solutions vs. overfunded insurance? Would most people be better off with your bonds? Probably not, even if they didn’t have to pay you a fee for your advice. Does your firm offer double-digit crediting in great years and contractually-guaranteed floors in bad years?

Check your own biases, sir. It’s OK to have preferences, but do your research before making blanket statements like this. I’ve done actual studies on the total projected expenses for max funded IUL policies compared to aggregated AUM fees over the years. Guess who often makes more money? As long as you’re disclosing everything, perhaps you should aggregate the projected cost of your investment advice over the years on an increasing balance using the most compliant growth projections when signing initial client agreements.

Hutch – Just found this. I’d love to see your “detailed studies on the total projected expenses for max funded IUL policies compared to aggregated AUM fees over the years” Writing a book on financial literacy and that info could be enlightening. Contact me at [email protected].

John, you can get a sense for expenses in an IUL by reading Bobby Samuelson’s articles. He’s published an IUL benchmark table and also goes into more detail about costs in IULs, especially max overfunded IULs (since most are designed to be overfunded):

https://lifeproductreview.com/indexed-ul-cap-par-rate-benchmark-index/

Expenses are generally pretty high on the new IUL due to the charge-funded ICMs and bonuses. Could be good, but could also result in losses due to the additional charges.

Commissions are only contingent on how you design the contract. Has nothing to do with the benefits of what an EIUL or IUL provide, but the person you’re entrusting to know what they’re doing and doing it within the best interest of the client. We make more in the mid and long term from equities based clients. The industries as a whole are full of fees, in fact, the only transparent programs out there are insurance backed contracts, the numbers are right there in front of a clients face. If an advisor or agent doesn’t understand them, or present them ethically, that’s a personally character issue, which is a problem industry wide well beyond insurance contracts. Just last year the big wire houses got called-out for not divulging the real fees and hidden costs they reap off account holders, which now they are mandated to do so in the plans prospectus. Plus, where else can you make a vacation home payment, while your clients are losing their shirts and half of their life savings. It’s all a matter of perspective.

Hello Michael, this is an insightful article and for the most part true. Most agents do sell the sizzle by saying that you’re borrowing “FROM” your policy and paying “YOURSELF” back with interest, which is absolutely not true. It only appears to have that effect as you are indeed taking a personal loan from the insurance company while allowing another asset (your cash value) to compound in your favor.

The uninformed masses will say it can’t work because of the outrageous commissions life insurance agents receive. If they were educated on the strategy they would know that a policy designed for “banking” is funded to the MEC limits and often includes a term rider, both of which substantially reduce commissions. This allows the policy holder to achieve robust and early tax-deferred compounding of an asset class that has contractual parameters keeping it immune from market risk whether you’re talking Whole Life or Indexed Universal Life. It’s also worth mentioning that quite a few companies these days offer “over-loan protection riders” that function somewhat like a non-forfeiture option after significant policy loans have been taken. If the rider is triggered then some nominal amount of death benefit would be set aside by the carrier, no more loans/withdrawals allowed, and the delivery of a death check would nullify the embedded tax liability for lifetime distributions exceeding basis. They did this because of all the bad press they got from the retroactive tax you described when policies lapse long after loans have been taken.

Enough about the product, let’s address strategy. Both the books you referenced actually recommend that policyholders service the loans regularly. What you illustrated by not paying the loan for decades proves policyholders have enough time and flexibility to right the ship if they can’t service the loan for some reason liked they have been advised to. There’s other things they can do as well like reduce face amount or surrender cash value to satisfy the loan to name a couple. The strategy actually works best for people who intend to be fiscally conservative or “an honest banker” and pay the loans back as soon as possible. Even if you pay cash for everything, once you make a purchase, you still make regular payments to fill up your cash account so you can make your next purchase using cash. The “banking” strategy simply has you funnel those cash flows through a very lean permanent life insurance policy to produce a better long term result.

In most cases it will outperform the cash-payor for 3 reasons, with the third being the most powerful:

1. A better risk-free rate of return

2. Tax-deferred growth

3. Continuous compounding of the asset.

You see, every time you pay back the loan the policy brings you to higher place in line on that compounding curve. On the other hand even if you could get a higher after tax rate of return on your cash account, once you spend the asset to make a purchase, you killed the compounding. You then have to replenish the account with whatever periodic payments you would be paying down the life insurance loan with and earn incremental compounding as you refill your account. In most circumstances, a properly designed “banking” policy will destroy paying cash over time for purchases even if you had a savings account where the interest rate didn’t start with a dot.

I like the approach of this article how it attempted to be unbiased and objective. Now some people (including many investment advisors) have a strong bias against life insurance. I fault both the investment and insurance industries for that. They have both been bashing each other for ages since they’re often competing for the same dollars, and neither have done a good job of educating the public of how products from each realm can actually compliment each other. The very best advisors take the opinion out of it and learn the merits of how various products and strategies can actually be interwoven to achieve the results that clients want. Do you know any who want a better rate of return on their risk-off assets? Anyone worried about future higher taxes? What if you could harness the power of compounding from not only your savings, but also some of your purchases as well? It doesn’t mean you get to keep it all, but what if you could benefit from it? So if you’re out there blindly parroting the talking heads that blindly bash life insurance, maybe it’s worth spending time to actually get educated. Any number of IMOs or FMOs would be happy to help.

This strategy is not competing with stocks. It is however competing with cash and other fixed income products. If the products are structured properly by a knowledgeable and ethical agent, and the client understands how to utilize the strategy as an “honest banker,” being as fiscally responsible as they would be if they paid cash for everything, then the strategy actually can actually work quite well in most cases.

Respectfully,

-Hutch

This is a very thoughtful message, Hutch. Thank you.

You’re welcome. Glad you enjoyed it.

John or “Hutch”, I’ve read through Michael’s article and all these comments. I must say you are an expert at this! I’m impressed with your analysis and thinking. So much so I thought “I’ve got to Google this guy and see what he does for a living”. Glad I did. Hope to be in touch soon.

Hi John, just have to, have to connect with you.

Could you please add me on linkedin (my profile link below)

linkedin.com/in/mehtab-singh-bandesha-5053439a

I wish you had discussed this article prior to release with someone who is a life insurance expert. While your argument against cash value life insurance is full of industry terminology, it lacks deep understanding. It also took me years to understand it myself. The issue you raised in this article is well known in the life insurance industry and they have come up with riders that offset the issue you have raised so that there is no phantom income in case a life insurance policy lapsing in the manner you described. Your article assumes that whole life, indexed universal life and Variable universal Life are all the same product with different names and similar risk profile. Since most of your readers are investment people, this is like me saying the risk of investing in a pink sheet stock is the exactly same risk as investing in a government bond.

I have seen many stock brokers compare whole life to a private equity fund or emerging markets fund and claim whole life is a ripoff. Now if we are looking at extreme scenarios, which is fair, we should look at what happens to some other tail events that could happen. What if fed keeps the interest rates at zero for the next 50 years, what if the SP500 remains flat year after year for the next 30 years.

that is not what AG49 is about at all and I think you know that. Intentionally misleading readers…I was really liking this blog until I saw that.

what is the point of this article anyways? Your policy will lapse! taxable event! (in 30 years) who would let their policy lapse? A dead person? Who couldn’t pay back the 50k in 30 years? You neglect to talk about the value of that 50k over 30 years, this is just garbage and you clearly have an agenda here. This looks more like politics than advice.

Money is an excellent replacement for life insurance(and visa, versa). For you older planners/insurance salesman that are still touting the benefit of holding on to policies until death, you have all taken an “end run” to get to the same place that smarter people get to directly. By saving/investing that $100,000 – $200,00 per year that MR WISE OWL suggests clients should put into cash value policies, me (and my clients) have more money. We don’t need life insurance anymore because those who depend on us can live very comfortably off the income generated from that larger principal amount. We don’t need to borrow somebody else’s money because we have our own. We don’t need Long-term care insurance because the monthly cost for such can be easily handled with income from pensions, social security and invested MONEY! We are SELF-INSURED and enjoy a MUCH simpler life without all the potential tax issues involved with CV life insurance and without having to deal with insurance company’s rules and restrictions. And when I do need to use some of my principal, I don’t have to borrow it and pay interest to some company just for the benefit of using my own money. Being self insured is really the best way to describe financial independence, don’t you think??

Bob, I would be in agreement with you that self-insurance is the way to go. However, you know as well as I, that only 2% of the population can claim this status at any particular time in their lives. Unless you were born into such wealth, a different matter, many of this class had to earn it along the way over the course of long and also successful careers. I say successful because wealth can be transitory highly dependent on personal circumstances void of significant financial setbacks permitting this class to not only accumulate wealth but avoid wealth loss or dissipation events over the same time period. Even now, their great wealth doesn’t insulate them from future dissipation events.

I would say it’s a fair statement that; many of your wealthy clients weren’t always so wealthy. Not knowing their present economic conditions 30 years ago, many would have had to purchase life insurance and possible other coverage: annuity, automobile liability, homeowners, etc. along the way to becoming able to self-insure today. After all, if you are truly wealthy, you wouldn’t need any insurance of any kind unless of course you lost your wealth, then only in hindsight, you may wish you weren’t so hasty to have discarded insurance based solutions.

Certain life insurance policies and annuity contracts (predominantly non-cash value designs) were not only designed to accumulate/provide an economic value over time but to also permit policy and contract holders to better exercise control of their property via their mere design features that are for practical purposes, superior to other financial products that may accumulate wealth but have weak long-term property control features. While you may never have needed such features because you successfully avoided circumstances over the last 30 years or so that would have damaged your wealth accumulation prospects you cannot have foreseen such fortunate events at earlier times. Any reasonable person with a young family to provide for would have taken interim measures by purchasing insurance just in case their future wealth accumulation efforts to get where they are today didn’t materialize.

After working as a litigation economist and in insurance company home offices, I have plenty of anecdotes to share of very wealthy people suddenly becoming un-wealthy. What to hear some?

I’d like to hear some.

David, going back to a several cases I worked on in the mid-1990s the first; a prominent LA anesthesiologist (mid age 40’s) was brought to his knees financially after an automobile accident severally injured a little girl leaving her permanently injured. Her life care plan called for an $8.50 million settlement. Unfortunately for the doctor, he had no automobile insurance or blanket liabilities coverage. He was going through a divorce and moved out of his home leaving the payment of his policy premiums to his soon to be ex-wife. Unbeknownst to him, she dropped his auto coverage (and therefore his blanket liability) because she didn’t want to pay the premiums on his corvette. The good Doctor was immediately bankrupted.

In a second case, a wealthy LA philanthropist, on the advice of his agent, “financial planners” purchase a $10 million life-only annuity following a purchase of a Jumbo size pref+ UL policy. The philanthropist was an A++ risk and also a tri-athlete. About 4 months after purchasing the coverage’s he was in a head on collision with a drunk driver. The philanthropist didn’t die. He was declared “permanent and stationary” after about 8 months of rehab. However, he was burned significantly and had no use of his legs or left arm. His family secured his release from rehab and took him home under private nursing care in Beverly Hills. Once home, he somehow managed to locale a revolver hidden in a bedroom end table by rolling out of bed, onto the floor and crawling to the location. He took his life. You can imagine what happened. The kids wanted to know what happened to Dad’s $10 million! The annuity terminated and the life carrier didn’t pay the claim due to suicide so they returned the premium. The family sued the agent and financial planners bankrupting them in the process. Several years later I handled the agent’s divorce. As my firm was hired by the agent and financial planners, my job was to evaluate the annuity value at the time of death.

Some of the most wealthy sophisticated investors in the world were taken by Berine Madoff and others like him. As we all know this a tremendous and very prestigious list. Joe and Linda Stewart had no knowledge of Bernie Madoff but still lost $1.150 million in the Agile Funds (a Madoff feeder fund). So, stuff happens.

Wow. That’s crazy. Thanks for the share. Very interesting indeed.

Bob. No, it’s not.

I think that’s the key statement there: you are self-insured. The nature of dividend-paying whole life insurance prevents you from spending more money on premiums than you receive, assuming you keep the policy in-force. So, it’s mathematically impossible for you to do better (financially) by “self-insuring” if what you want is a large estate. That’s true of most other types of insurance too. They allow you to purchase $1 of insurance for a specific purpose for a fraction of a dollar. When you self-fund, you are spending $1 for $1, which means it’s inherently more expensive if or when you need money for that otherwise insured event.

Maybe you think self-insurance/self-pay is simpler, but it’s more expensive in most cases. The only time it would be cheaper to self-fund is if your insurance is not really insurance but, in fact, some kind of “prepaid” plan, like we see with healthcare plans.

Regarding the complexity: Have you read the average whole life insurance policy contract? It’s about 100 pages, give or take, with much of that being numerical values. Most of them are written in “plain English.” Compare this to the language contained in IRS publication 590 alone for just a handful of retirement plans.

Regarding policy loans: You think you don’t need to borrow money from someone else because you have your own. But, if you’re generating income from that principal, then you DO need to borrow money from someone else or accept a lower income from that principal amount. Like insurance, there are only two ways to finance something: you either borrow money from someone else, or use your own cash. When you use your own cash, you eat the opportunity cost if you do not add more back to your cash fund than you withdrew.

Now, there’s nothing inherently or morally wrong with self-insuring. But, if you want to be self-insured because you like the idea of being your own insurance company, that’s a different matter apart from which is a better or more efficient approach to financial planning.

David,

Your statement about self-insurance is mathematically incorrect.

Insurance death benefits are purchased for a fraction of the death benefit because the death benefit is paid in the future and the premiums are paid today. That’s a simple time value of money calculation.

You can self-insure the exact equivalent amount of death benefit at your life expectancy by simply keeping the premiums yourself and buying the same investments the insurance company would. Technically, you’ll end out with MORE money, because the insurance company has to set aside a portion of premiums for expenses and its own profit margins. See https://www.kitces.com/blog/why-you-should-only-buy-insurance-protection-and-annuity-guarantees-expected-to-lose-you-money-on-average/

For those who don’t live until life expectancy, the life insurance will have a superior internal rate of return to this, in exchange for the fact that if you live beyond life expectancy, it becomes even more inferior. Some (though sadly too few) life insurance policy illustrations actually show this IRR calculation, specifically to illustrate the implied time value of money of the insurance.

Yet ON AVERAGE, the policy shouldn’t come out to be any better than the IRR at life expectancy. If you expect it to be better, that means the client knows of a health condition reducing life expectancy that the insurance company hasn’t priced into the premiums… which would be insurance fraud. With fair disclosure for underwriting, the insurance policy is designed to be actuarially fair, which means its IRR is equal to the expected return of the insurance company’s (mostly bond) portfolio, less expenses and margins.

The reason to purchase insurance is for those who can’t possible afford to have the low-probability bad outcome (i.e., an early death) occur. Not because they EXPECT it to occur, but because they can’t afford to have an ‘unlucky’/unfavorable outcome because it’s so extreme.

– Michael

You said: Your statement about self-insurance is mathematically incorrect.

My reply: No it’s not. I think you misunderstood my claim. I wrote you cannot pay in more to a dividend-paying whole life policy than you receive and that most of the time it’s more expensive to self-insure. Still, maybe I should adjust my statement to just say that it’s unlikely you will do as well as the insurer.

You said: “You can self-insure the exact equivalent amount of death benefit at your life expectancy by simply keeping the premiums yourself and buying the same investments the insurance company would.”

My reply: There is a sense in which you’re right. If you became the insurance company, you could replicate an insurer’s results (kind of circular reasoning, but true nonetheless). But I think it’s not possible in the sense that most people mean when they say “self insure.”

For example, term insurance is a huge money-maker for insurance companies because so few of them pay out. Obviously, they price them such that, even with death claims, the insurer still profits. Are clients going to sell term insurance policies to collect a profit on those premiums? Are they going to be able to purchase investments at the same cost as the insurer? Will they have the same yield on cost starting out? Can they get access to the same investments as institutional investors? If so, they would be insurers.

As a practical matter, let’s say a man’s life expectancy is 76 years. Run a simple illustration for a male at an older age, say 60 or 70, or near his life expectancy. The death benefit will always be higher than the premium outlay. Even if you self-insured up to that point, you could buy life insurance and get a death benefit amount that exceeds your self-insurance fund. Based on what you wrote, there should not be a positive IRR at life expectancy (unless I somehow misunderstood you).

But, you could also try self-insuring starting at a younger age, and still not match the insurance death benefit, even when you buy the same exact investments as the insurer. First of all, when you’re first starting out as an investor, you don’t have the position size an insurer does, which puts you at a serious disadvantage and makes it difficult to “catch up” to what an insurer can do with its money. You have to start small, with small sums of money — most likely monthly savings contributions.

This will cause a secondary problem you spelled out in an unrelated post here on your blog. Namely, the cash flow going into investments over time significantly affects your rate of return, almost always negatively (because you are dollar-cost averaging over many years). Perhaps you could do value investing, like an insurer does. But, you probably don’t have a 100-year time horizon like an insurer does, which means you may not be willing or even able to wait for the best available investment with your excess cash.

But, setting aside position size and assuming you start self-insuring by saving monthly, let’s say you started out saving $1,000 per month at age 35 to try to self insure. At near your life expectancy (age 76), you would have $1,606,460.79 in death benefit assuming the industry average net total return on invested assets of 4.71% (net of fees, but not net of taxes).

Now, take that same amount ($1,000/mo) and buy a dividend paying whole life policy. I ran one quote and came up with $2,216,204 of DB at age 76 with a life paid up at age 100. This is a 6.20% IRR on death benefit. Much higher than your self-insurance fund.

Here’s where you come up with slightly more money: the cash value. At age 76, the whole life insurance policy has $1,485,817 in cash values compared to the $1.6 million through self-insurance. The IRR on CSV is 4.69%, slightly lower than your self-insurance fund.

At age 100, your self-insurance fund is: $5,256,807.77 (gross). After tax would depend on what you invested in. In the insurance policy, the death benefit is: $4,948,073, net of taxes.

Perhaps this is what you meant by the idea you could do better self-insuring (not including taxes)?

That works for some who have a high risk tolerance, but not everyone does. What happens if your in the withdrawal phase and another 2008 happens, 2001, etc. and you “need” income, you will start to eat away at your principle. Also you have to account for the tax on your gain that you have paid, not just look at the average return. I agree that all products serve a purpose for the appropriate client. Everyone should stop generalizing. I’ve seen people who thought they were self insured deplete all their funds when a spouse was diagnosed with Alzheimer’s and the market crashed during that time. I’ve seen parents loose their retirement paying for Adult children’s cancer treatment after they lost their health insurance once their FMLA ran out. If you have Bonds in your portfolio CV Life with a good mutual company I’ve seen can definitely bet the average Muni Bond. Big Banks have the majority of the money you guys have in the bank invested in CV Life policies. Agents are paid trail commissions from what I’ve heard on those policies and a good company that has a good rating will do annual reviews with their clients. Choose an agent that has integrity.

Wow, this comment section is full of Insurance Nerds! There is no Right or Wrong Answer! It’s all about “Client Suitability”. I’m thinking Permanent Life Insurance is the perfect product for a very small number of wealthy people that want to pay their agent a very high commission, and access a long term tax free death benefit for their heirs. For most Americans that are functionally poor, they need a low cost term policy to protect their kids. If they are disciplined, they are saving money consistently via retirement plans and other tax-free or deferred products, but again we see most people are not doing this, just like they can’t keep a workout plan or diet in place. If you are an agent talking poor people into an overly expensive life insurance policy, you already know you are doing wrong, all the hypothetical projections in the world will not change this. Just hook people up with the right policy for their needs, write good business and sleep easy.

I have spent a lot of time trying to get to the bottom of these participating whole life policies as there is a lot of noise out there. While some of the marketing is definitely hyped up and the “paying yourself back” and “recapturing interest” can be misleading, it is hard to argue with the cash-flow that these policies can produce. I do not sell these as the company I work for is not a mutual, but I own policies. I am looking at an illustration from Ohio National (paid dividends for over 100 yrs) at current dividend levels that are much lower than what a lot of the materials state, and here is what comes out.

Age 35, male: Inital face amount: $500,000 with Paid up additions rider

Premiums: $5,100 base and $13,300 of PUA for a total of $18,400 for 7 years. Remaining years the premium is $5,100.

First year cash value: $12,943

total premium outlay thru age 70: $271,600

Age 70 cash value: $837,488

Age 70 death benefit: $1,461,649

With these scenario, client can draw an income-tax free cash flow of $42,491 from age 70 through age 100. This is about a 5% withdrawal rate that is tax-free with a death benefit along the way. Yes it is decreasing due to the loan amount increasing, but even if the insured lives to age 100, there is a residual death benefit of $458,379 with a cumulative premium outlay of -$1,003,130. That means he would have received $1,274,730 income-tax free after only paying $271,600. And that is not counting the death benefit. Add the death benefit to that number and you are still ahead of the death benefit at age 70 ($1,733,109 vs. $1,461,649). You are basically just accessing the benefit early.

Most of these policies are going to earn a long-term rate of 4-4.5% based on current assumptions. The YOY grown is closer to 5% in “retirement” years.

If insured passes at age 85, the death benefit $1,184,191.

If we wanted to take income only to age 90, the amount jumps to $54,156. Now we are at a 6.46% withdrawal rate with a death benefit of $646,012 at age 90. These cash flow rates are better than a lifetime SPIA with refund.($52,421.01) or a 20-yr period certain annuity ($53,663.33) with a better residual benefit. I know you will say you can do better with a diversified portfolio, and yes, you maybe can.

Now this asset can certainly replace any cash holding or bond-type of investment as it will generate conservative but competitive returns that are un-correlated to the market. Owning this asset will allow their advisor to remain more aggressive with the rest of the portfolio and have a reserve of available cash to draw upon in down years, so you aren’t selling low. Just another option on the flexibility of participating whole life.

Just like any product, it is the few reps/agents that over-sell the benefits and make it “too good to be true” that ruin an otherwise great asset to own. One example of this is when they say you can be in a better position by borrowing from the policy and paying back “extra” interest. The extra interest is merely premium, so of course the values will be higher, there is no magic there. And yes, it is a personal loan from the insurance company but it is one that is paid back on your own terms and is usually a favorable rate. If you can get access to quick cash at a lower rate and are ok with the repayment terms, then by all means get the money elsewhere.

It isn’t the be-all end-all solution, but there is certainly nothing inherently bad about owning a policy that is structured this way. I have seen policies with available loan balances close to 90% of first year premium. The commission on these policies is significantly reduced for the agent, as they are not being paid the higher up-front commission on the whole life contract for the whole amount. They are paid on base usually at 50-90% and then on the PUA about 3-4% depending on carrier and product. It is still a nice payday for the agent but most people assuming they are getting 100% of the first year premium, which is certainly not the case. One case I was looking at with an agent would have paid him about 10% of first year premium, big difference.

—Michael—

Maybe you could run some Monte Carlo simulations with a 5% after-tax

static withdrawal rate on different portfolios to see how it compares?

It is apples to oranges but at least a benchmark.