Executive Summary

The ongoing commoditization of investment products is driving a fundamental shift in today’s financial advisor platforms, as broker-dealers and custodians transition from being primarily about financial services products, to instead trying to operate as the technology hubs around which financial advisors build their businesses.

The transition is appealing because ultimately broker-dealers and custodians are a form of platform business model, which takes a small slice of all the assets and transactions that flow across the platform. Which means in the end, the more successful the financial advisors on the platform are, the more successful the platform itself will be.

The challenge, however, is that the rising demand from financial advisors for better technology is driving a number of advisor FinTech software providers to build increasingly comprehensive solutions, aiming to compete directly with the often-proprietary platforms of today’s broker-dealers and custodians. From the growing portal platforms of Orion Advisor Services and eMoney (before it was acquired by Fidelity), to the launch of Salesforce Financial Services Cloud and Black Diamond’s acquisition of Salentica, it’s “game on” for independent FinTech providers to build comprehensive solutions for financial advisors.

Unfortunately, though, this transition has set financial advisor software companies on a collision course with broker-dealer and custodian platforms themselves, and it’s a collision that many of the independent FinTech companies cannot survive. Because the reality is that in the end, financial advisors will only pay “so much” for a software solution, and independent software proivders simply cannot compete with the size and scale of a true platform business – as companies like Garmin navigation quickly learned when Google Maps showed up, or the entire CD music business learned when iTunes showed up.

Notably, this doesn’t mean that all financial advisor technology will inevitably consolidate around broker-dealer and custodian platforms. Because those platforms really only need to “control” the technology that is integral to their platform itself. But it does mean that the most successful advisor tech companies in the future may not be the ones that are the most comprehensive - unless they can truly pivot to not just platform software, but a platform business model - and instead will be the ones that stay focused in their core competency, and are most effective at building flexible APIs to integrate most easily with other real platforms (and their often-legacy existing technology infrastructure).

Or viewed another way, the future of independent financial advisor FinTech software companies is to become the best “Apps” in the App Store of custodian and broker-dealer platforms. Not to try to become App Stores themselves… a transition that most will inevitably lose, because they cannot outcompete and replace the true platforms that advisors still need to invest their clients' actual portfolio dollars.

How Financial Advisor Platforms Are Evolving Into Technology Platforms

When it comes to financial advisors, in the past our various technology platforms co-existed peacefully, because they ultimately served different marketplaces and fulfilled different "matching" functions.

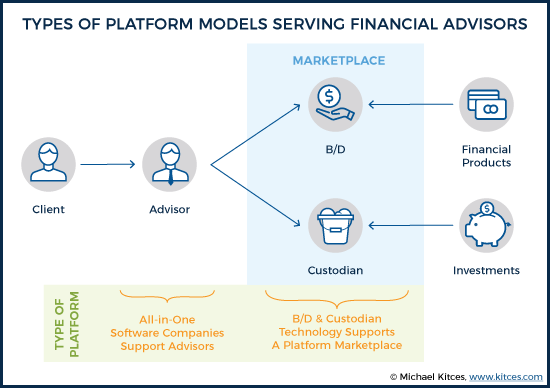

For instance, broker-dealers matched brokers to (commission-based) securities products (to be subsequently sold to clients). RIA custodians matched advisors to an array of investment solutions they could implement for a fee with their own clients. In essence, one was a platform for securities salespeople selling financial services products, and the other was a platform for (largely discretionary) investment advisers. And the legal and regulatory differences between selling products for a commission, and managing portfolios for a fee, meant that advisors generally chose one or the other, but not both.

In the “early” days of financial advice, these broker-dealer and RIA platforms competed primarily by the quality of the marketplace they created – their tools and support to sell securities products or implement investment portfolios, and the breadth of their marketplace of products or investment choices. However, over time the focus has increasingly turned to the “platform” itself – the tools and technology used to support and implement the financial advisor’s business on that platform. Especially as the availability of the products and solutions themselves become commoditized.

In other words, early on it was about whether the platform offered a particular ETF or mutual fund or annuity or third-party manager. But now, when any financial advisor can buy virtually any mutual fund or ETF or manager from any custodian, and can implement almost any commission-based mutual fund or annuity at any broker-dealer, the platforms themselves have to come up with some other way to differentiate. Because when everyone has access to the same final information or products, it's the effectiveness of the platform itself that dictates the "winner". Thus, while everyone had access to the same World Wide Web pages to index and categorize, and Google was actually the 21st search engine to enter a crowded marketplace, it ultimately differentiated and was victorious by the quality of its platform solution, taking the same end information that everyone else had, but better matching it to consumers and their needs.

Accordingly, broker-dealers have increasingly been pressured to provide a full technology platform to financial advisors, and RIA custodians have become more and more like tech companies over time as well. The shift is on from product selection and investment choices, to the technology of the advisor platform itself.

The good news of this shift is that it is driving new investments into advisor FinTech solutions, amplified further by the rise of the robo-advisors, who aren’t taking market share, but did shine a bright light on the lagging tech solutions at existing financial advisor platforms today. The bad news, however, is that competition to serve the full breadth of a financial advisor’s needs, as products themselves are commoditized and all channels converge on comprehensive financial advice, is potentially spurring too many financial advisor platforms, and not all of them can and will survive!

Growing Competition To Be THE Financial Advisor Platform

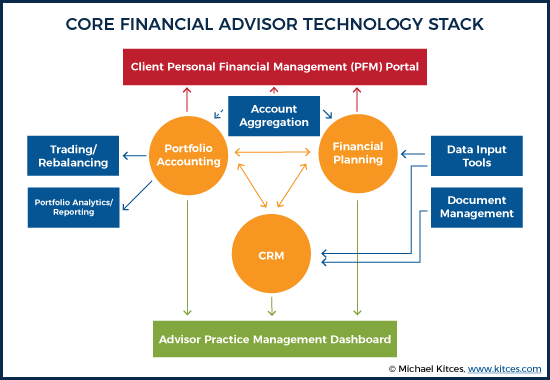

For most financial advisors (at least those who in some way provide investment advice or implement investment products), the “core technology stack” is comprised of CRM, financial planning software, and a portfolio accounting solution (supported by trading/rebalancing software).

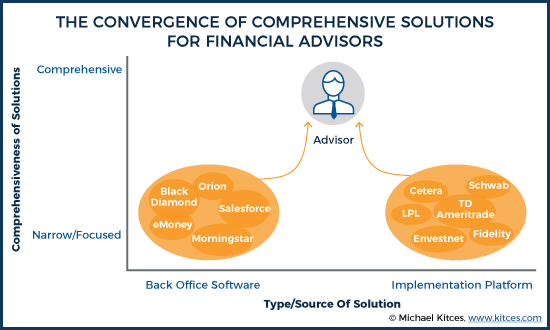

Accordingly, major financial advisor platforms have increasingly been shifting to provide comprehensive solutions that cover most or all of these components. From Envestnet buying Tamarac and more recently FinanceLogix and Fidelity acquiring eMoney Advisor, to announcements that Schwab is working on a new version of PortfolioCenter called Portfolio Connect and Fidelity is building its own portfolio accounting solution into the new Wealthscape platform, and major deals between Cetera and MoneyGuidePro and LPL and FutureAdvisor (while Commonwealth and Raymond James build their own proprietary CRM). Whether it’s an approach to buy, build, or partner, major advisor platforms are moving aggressively to round out their full suite of advisor technology.

However, the notable trend in recent years is that advisor platforms themselves are not the only ones trying to build comprehensive advisor technology solutions. Advisor FinTech companies themselves are beginning to acquire and build across a wider range of solutions, morphing towards a more comprehensive platform.

Thus, for instance, Salesforce has announced its Financial Services Cloud, eMoney was building its eMx portal to be the advisor’s daily dashboard (a strategy that Fidelity’s acquisition seems to simply double down on), Orion open-sourced a big slice of its code to become a more central platform hub, Morningstar bought TRX rebalancing software, and most recently Black Diamond’s portfolio accounting solution bought Salentica CRM.

The relatively straightforward strategy seems to be the idea that if advisors already use a piece of technology, and want everything to be integrated and interconnected, the opportunity for any software company is to expand its offering to those other integrated components. By acquiring or integrating more components of the stack, the software company can “expand wallet share” and make it harder for any advisor to leave, improving its appeal for those advisors seeking fully integrated solutions, and tying them into an (independent FinTech) ecosystem that improves long-term retention for the software company.

However, the challenge of this shift is that while in the past, advisor technology companies were partners to existing financial advisor platforms – solutions that the advisor (or platform) could plug into its existing ecosystem – as advisor software solutions expand to become their own platforms, they are increasingly on a collision course with RIA custodians and broker-dealers trying to accomplish the same thing. In other words, companies like Orion, Black Diamond, or even Morningstar used to simply partner with and integrate with RIA custodians and broker-dealers... but now, they're increasingly finding themselves in head-to-head competition to control the core of the advisor's tech stack.

Why Most Independent Software Companies Will Fail As Financial Advisor Platforms

This collision course is significant, because I believe that ultimately most financial advisor FinTech companies will fail in their efforts to become holistic financial advisor platforms.

The reason is that while their software may be important, and ultimately all of those software tools together may constitute a “platform” on which the advisor operates, the software company itself is not actually a true platform business model.

The key distinction is that in order to be a true platform business model, the participants on the platform must come together for an exchange… where the platform itself can financially benefit from or monetize some portion of the exchange. For instance, eBay brings together buyers and sellers, and takes a slice of each transaction. Amazon brings together consumers and merchants, and takes a slice of each transaction. Google brings together people searching for information and advertisers who want to reach them, and takes a slice of each transaction (through getting paid for advertising).

But even a holistic and standalone financial advisor technology stack is not actually part of a value exchange transaction between the advisor and another party. In the end, it’s a back-office solution for the advisor’s own (pipeline) business. In other words, the advisor buys the software to use to deliver his/her own services, but the software company’s “platform” isn’t actually part of the client transaction. It only powers the advisor's own business behind the scenes. And must be paid for directly out of the advisor's overhead expenses.

By contrast, consider the broker-dealer platform model. Advisors who use the technology of a broker-dealer to become more successful don’t just pay the broker-dealer for the technology. Instead, the broker-dealer’s technology ultimately facilitates the advisor doing more business with the financial services product manufacturers, who distribute products through that broker-dealer (and ultimately to the end client). And the broker-dealer takes a slice (through the grid). Which means the broker-dealer doesn't actually need to make money on its software solutions; it just needs them to make the advisor's own business more successful, and benefit from the increased volume of platform transactions.

Similarly, the RIA custodian platform model provides technology, but it’s to facilitate financial advisors who are deploying client assets in the investment marketplace. And whether it’s putting money into a money market fund, or paying the ticket charge on a stock trade, the RIA custodian gets a slice of every transaction. Which, again, means that RIA custodians don't actually need to profit from the software to monetize the software. Thus why TD Ameritrade purchased iRebal, and ultimately turned its $50,000/year licensing fee into a free solution for any/all advisors on its platform.

In other words, the software company gets paid for the software; the true platform business model provides the technology to help the participant in the marketplace engage in more transactions, and earns its profits from the increased activity that occurs as a result. Without any need to be paid directly (either as much, or at all) by the advisor themselves.

And in the aggregate, the distinction is significant. Because software companies are ultimately limited by the amount of money they can charge any particular advisor, based on the advisor’s business needs, ability to afford the solution, and the available alternatives for the advisor to solve his/her business problems elsewhere. It's a brutal competition to get a slice of the advisory firm's overhead expense allocation. By contrast, true platform marketplaces have the opportunity to profit based on the volume of transactions and ‘value exchanges’ that pass through the marketplace, a more indirect but potentially much larger profit opportunity. Especially because the revenue often comes directly from the value exchange transaction itself, which means it's borne jointly by the advisor and their client (e.g., a ticket charge, or the scrape of a 12b-1 fee), rather than forcing the advisor to write a check.

For instance, Schwab’s technology ultimately facilitates over 7,000,000 revenue-producing trades in a year (from commissionable trades to bonds with markups, OneSource funds, fee-based wrap accounts, and more), for which it generated a whopping $825 million of trading revenue in 2016. In fact, Schwab’s platform is so large, with over $2.5 trillion of retail and institutional assets, that if interest rates just rise enough for Schwab to earn a profit on its money market funds, it’s estimated the company can earn $650 million in additional revenue.

Consider that for a moment. Schwab can generate $650M of revenue based on just earning a few basis points on a few percent of the trillions of client assets attracted to its marketplace, through its technology that advisors use… even without charging a dime for the technology itself.

That, ultimately, is why it’s virtually impossible for pipeline companies (solutions that fit into the advisor's delivery pipeline) to compete with true marketplaces. Because the marketplace can scale drastically beyond what pipeline competitors can, which in turn makes it possible to generate revenue that is an order of magnitude larger, even if the technology itself couldn’t be sold to an advisor for a fraction of that price.

This is why Uber is bigger than any individual taxi company, AirBnB is bigger than any hotel chain, and Amazon may ultimately be dragging down the entire retail industry. Similarly, Google largely obliterated the GPS navigation industry, simply because it was so profitable to be a successful search engine and mapping tool (because it supported Google’s advertising business), that they could afford to give away the technology for free and put their competitors out of business with a better platform business model.

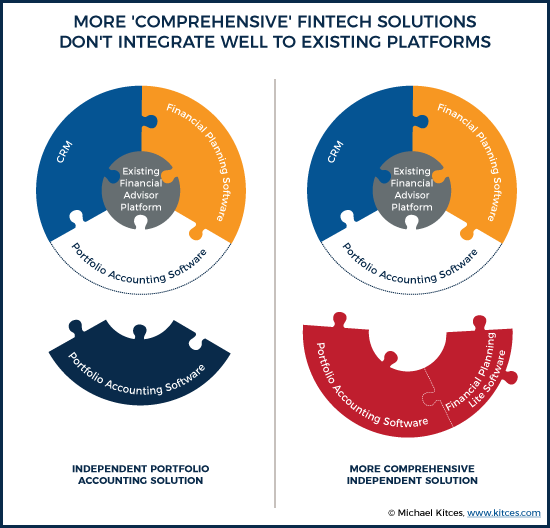

Ultimately, I fear that this may be the demise of many of today’s CRM, financial planning, and portfolio accounting software solutions that are trying to evolve into holistic platforms. As single standalone solutions, they could “plug in” to an existing platform, solving a particular problem better and more efficiently than the platform could itself. Not every platform wants to have to buy or build every component of the solution; just the ones that are central to their platform value proposition. But the more independent FinTech software for advisors expands, the less that can fit into an existing broker-dealer or RIA custodian platform, and the more the software provider competes with the platform directly. Yet independent software companies for advisors are not true platforms, because in the end they’re simply solving the back-office challenges of an advisor’s pipeline business model, rather than actually facilitating (and getting paid to facilitate) a true marketplace exchange.

The distinction matters, because eventually, true platform companies that can ‘cross subsidize’ the technology with the actual profitability of the marketplace will be more successful, precisely because they don’t have to just rely on the economics of advisors buying the software alone. In fact, this helps to explain exactly why Schwab is building its next generation portfolio accounting, why Fidelity is building its own next generation portfolio accounting, and why Envestnet is expanding its tech platform (as even though it’s a heavily tech-centric company, it’s important to note that the company’s core is still facilitating a platform marketplace between advisors and third party asset managers who want to work with them!). Expect to see Schwab buy or build its own financial planning software soon as well. And as Morningstar tries to pivot from a data company to a platform business, with the growth of its Managed Portfolios and newly announced Model Marketplace, expect to see them continue rounding out their holistic advisor technology stack as well (presaged by their acquisition of tRx last year).

In other words, if you were a financial advisor platform that actually did facilitate a marketplace and could ‘infinitely’ scale profitability simply by attracting more advisors and clients to the platform, why wouldn’t you “give away” quality software at a below-market (or potentially, entirely free) price point, since the successful growth of the platform marketplace can ultimately be far more profitable than the software alone anyway?

Succeeding As Financial Advisor FinTech – Be The Best App In The (Custodian or Broker-Dealer) App Store

Notably, these dynamics do not mean that all financial advisor tech companies are dead or doomed. Because some marketplaces may choose to work with outside providers, rather than building everything themselves. In fact, the whole point of a platform is that it becomes a nexus point for multiple producers and consumers/users to come together for solutions.

Perhaps the best case-in-point example is TD Ameritrade, which has differentiated itself amongst the custodians by making one of its advisor benefits an advisor tech platform marketplace of its own – Veo, which facilitates a marketplace between advisors and other FinTech solutions. Similarly, Pershing Advisor Solutions has previously announced its own open API and integration strategy to become a marketplace for advisor technology. And even somewhat more “captive” proprietary platforms like Schwab still facilitate open access (e.g., via Schwab OpenView Gateway) to parts of the technology stack they don’t actually want to build themselves. Because the reality is that even for a financial advisor platform, it’s not necessarily (nor even desirable) to try to build all of the technology solutions for advisors; it’s just necessary to build the technology that is integral to the platform itself, and the ability of advisors to conduct business there.

In other words, there’s a difference between building an App store, and trying to produce all the Apps in the store. While companies like Apple and Google do populate certain key apps in their own stores (e.g. iMessage and iTunes, Gmail and Google Docs), in the end the overwhelming majority of the marketplace is comprised of other, third-party technology solutions (i.e., app makers) who produce apps that consumers can purchase and use. And RIA custodians and broker-dealers can and do operate similarly.

In this context, the key for most financial advisor FinTech solutions to survive and thrive in the future is to focus on what they do best, and be the “top App in the [custodian or B/D] App store” in their category, the best-in-class solution for whatever it is they do. Don’t try to grow the app to the point of replacing the app store, because an app – even an amazing one – will eventually be trounced by a true platform business model that will inevitably out-develop it (i.e., no advisor software company can iterate new best-in-class solutions in every category at once), or be out-competed by a superior business model (because platform marketplaces that take a slice of every transaction will always be superior to software businesses that simply require users to buy licenses). In other words, unless the company has a business model that goes beyond just charging advisors a price for their software - and can convert to a true marketplace platform themselves - don’t try to outcompete real platforms in their own core competencies, as if the platform can monetize the solution better than the software company, the platform will inevitably win (a lesson that Garmin navigation learned the hard way as Google Maps came to dominate the marketplace).

In turn, this means the software strategy is not to true to compete against true platforms for wallet share, but to become so best-in-class that any and every platform would rather use your solution than ever consider building their own inevitably-inferior one (or perhaps, even, buy your company entirely, as has happened in recent years to eMoney, Finance Logix, tRx, TradeWarrior, and more). Integrations should focus not on the depth of integrations with a select other independent software partners, but the flexibility of the API for true platforms to integrate as deeply as they can. Because as Apps from Candy Crush and Angry Birds, to WhatsApp and Skype and more have shown, it’s possible to have an incredibly financially successful software company built entirely on someone else’s platform. Those software solutions never would have achieved a fraction of their scale by trying to market and distribute directly to consumers as independent software solutions outside the App Store.

Yet again, as recent industry FinTech trends have shown, an increasing number of software companies are trying to expand outside of their core competencies, in an effort to create a more holistic solution, and pitting themselves increasingly head-to-head against true financial advisor platforms (custodians and broker-dealers). But they're expanding the scope of their technology, without pivoting the underlying business model, a dangerous shift when the "real" platforms have an arguably superior business model and an unwillingness to cede so much territory.

In fact, one of the most common complaints I hear today in the world of so many broker-dealer and other advisor platforms is that today’s independent FinTech solutions do “too much” beyond their scope, and haven’t worked hard enough at being flexible to integrate into existing platform technology – leading more and more, from Schwab and Fidelity to Commonwealth and Raymond James – to buy or build their own proprietary solutions instead. A trend I expect to continue and even accelerate, leaving fewer and fewer independent FinTech solutions available outside of existing platforms. And once a platform buys or builds its own solution, the advisors on that platform are usually permanently lost as potential customers for other independent software company (at least until/unless the advisor leaves the platform themselves), which means the pool of available advisors for independent solutions will get smaller and smaller.

For instance, in the independent RIA space, soon the only major truly "open" platform left may be TD Ameritrade (as Schwab builds Portfolio Connect and Fidelity builds out Wealthscape), yet even TDA has acquired key components (e.g., iRebal) for its platform, and at the point that there's only one major platform hub for independent RIA FinTech to plug in to, they're not really independent anymore anyway, they're simply indirect captives of their only active integration partner, TD Ameritrade!

Which means if independent financial advisor software solutions continue to expand their scope instead of figuring out how to become more flexible to integrate more easily to existing platforms - and lose more and more access as the real platforms buy or build their own truly holistic solutions - they risk being the most comprehensive financial advisor software solutions with too few platforms willing to work with them to actually survive!

So what do you think? Should financial advisor software solutions try to operate more like Apps in the RIA custodian and broker-dealer “App Store” platforms? Independent advisors often prefer independent solutions, but if you were running a custodian or broker-dealer, would you be willing to cede that territory? Please share your thoughts in the comments below!

Focusing on doing one thing and doing it well is definitely the way to go. Not only will the big custodians not appreciate you taking on the role of an all-inclusive “platform”, but vendors who even attempt to be an all-in-one will (and have) find that that they are jacks of all trades, masters of none. Focus, focus, focus.

The term “best of breed” exists for a reason.

Best,

Don Whalen, PreciseFP

You used “platform” over 100 times in this post, yet the word is not defined.

As a basic analogy, Lego bricks are a platform. Anyone can create anything from Lego bricks without obtaining permission or authorization from Lego. The instructions in the box simply guide the builder to build the set that’s pictured on the box, but an infinite number of alternate creations can be built from the same pieces.

Lego supports the platform by enforcing its own standards of interoperability so that any brick in one set is compatible with bricks from other sets. The platform is so popular that even knock-off toys disclaim on the box “compatible with other leading brands.” In addition, other businesses have been created on top of the Lego platform, such as Pley, which will rent out Lego sets for a monthly subscription, with no intervention or permission from Lego required.

Programming languages are also platforms. Any developer can write code, successfully compile it, and execute it within a supported environment (hardware or software) without any intervention or permission from the working group that maintains the programming language standards.

Platforms, therefore, are only as successful as the people who build on top of them (e.g. developers). The more the platform supports developers, the more successful the platform will be, leading to mass adoption.

I cannot identify an equivalent platform in financial services technology today.

Companies including the broker-dealers and institutional custodians you mention, are solution providers, but they are not platforms. Some of them even provide APIs to their solution to manage trading, alerts, or perform data inquiries (such as TD Ameritrade Institutional that you cited), but I know of no provider that has defined and standardized a framework upon which developers can build freely and with no supervision.

Broker-dealers, institutional custodians, and even independent solution providers that offer multiple technology solutions for the financial advisor technology “stack” are bundled solution providers, but the offering of bundled solutions does not make the company a platform provider.

Bill,

Broker-dealers and custodians are platforms between INVESTORS and the various financial services products they want to purchase (whether that’s stocks, bonds, mutual funds, ETFs, third-party managers, advisor-managed portfolios, etc.). It’s a classic platform model; they facilitate the platform, and take a scrape of every transaction (trading fees).

Their platform is connecting consumers with investment solutions. That’s their business model, for which they literally hold and custody the money. They’re “solution-providers” for advisors, inasmuch as the advisors use their solutions to help more consumers conduct investment transactions and custody money on their platform. An important point to recognize, about where the advisor does (and does NOT) actually fit into the equation from the perspective of the custodian’s own business model. That’s what you get when you use a “free” custodian! 🙂

For further definitions of platform models, see https://www.kitces.com/blog/financial-advisor-matchmaking-platform-business-model-of-the-future-fintech/

– Michael

As Dermot noted, I’m afraid we’re speaking past one another, as we often do, getting caught up in the semantics of fabulously ambiguous words like “platform.”

My software engineering roots are showing, as I consider broker-dealers and custodians to be marketplaces for investors and products to facilitate exchanges between investors and product providers, not “platforms” in the vernacular of software engineering.

The subject is a platform business model. See https://hbr.org/2016/04/pipelines-platforms-and-the-new-rules-of-strategy for further discussion, or http://amzn.to/2pGkMdL for the full book version. 🙂

If you prefer to use your wording, remove 100% of the instances of the word “platform” and substitute “marketplace”, and re-read accordingly. 🙂

– Michael

print blogpost.replace(“platform”, “marketplace”)

Whew, that’s better!

I think there is a difference between a platform as a technology stack and a platform orientated business model which involve cross-subsidization. What Bill describes is the former while I think that the article is more about the latter. With a platform orientated model you can monetize your service using non-direct means (Google & Facebook give you free stuff so they can learn about you and sell that learning to advertisers) thus subsidizing the service the end user is receiving.

In the wealth management space the custodians have the most obvious means to indirectly monetize given how they make money on both trading and the float. This gives them the ability to subsidize any software they build on top of the custodian service. Given the imminent increase in interest rates I would think it’s only a matter of time until you see “free” custodian services. You saw something similar play out in the 401(k) world where the traditional record keepers were hit hard by verticalized players who worked out there was more money to be made in own-brand investments and rollovers than in software.

If this were a normal market then things would play out as article suggests. However I think that the advisor market has complexities that the consumer market does not. Firstly RIAs, and possibly soon bd advisors, have a defined fiduciary duty to their clients. So going for a “free” software solution which passes costs to the client through indirect means may lead to issues.

Secondly then the average custodian is not Google, Amazon, Facebook et al. Building and maintaining a best of breed software stack is a difficult undertaking for the best software companies out there. Assuming any of the current players in the wealth management space can do this on an ongoing basis is a stretch.

Finally how many advisors will agree to rely on one custodiansoftware provider to run their business? The majority of RIAs use multiple custodians today. Given how this whole business model is based on indirect monetization of custodian assets it’s difficult to see how the average custodiansoftware provider would be cool with an advisor using their software for free and then putting assets elsewhere. So the RIA would have to give up their independence to save a few dollars. Granted the average BD CEO may have a different set of criteria they are managing against.

Bill (and Michael),

As part of a life planning advisory firm, one thing I’ve noticed as we’ve adopted some fantastic technology solutions the last several years (eMoney, Orion, SalesForce, etc.) is the increasing number of websites and logins for our clients. Are either of you aware of a single client dashboard solution that can be integrated with multiple technologies like that? Or a developer that might be up for that? We are interested in having a single client dashboard on our own company website that would be a one-stop shop for viewing not only financial items like their portfolio value, net worth, and cashflow summary, but also some elements of their “life plan”– their goals, family tree, current concerns and decisions, etc.

I would love any input you have on that concept and how we might be able to get it off the ground.

Thanks in advance!

Nick Stebner, CFP(R), CPWA(R)

LifePlan Financial Group, Inc.

Nick,

The first option that comes to mind is using your Orion Advisor Services client portal as the platf…. no, WAIT, foundation for your online client portal.

Several years ago Orion published source code for their client portal on GitHub and allows other developers to build whatever they want for the client portal (which was the impetus for creating the Fuse Hackathon, now entering its fourth year this September).

Here’s my suggestion: Watch my videos from the 2015 and 2016 Fuse Hackathons, especially the final day videos where all the companies who participated are identified. If you see companies that you already use (eMoney comes to mind), reach out to them and ask what components of eMoney you are able to embed in the Orion client portal.

2015 Day 3: https://youtu.be/yiN6D6l5Gw0

2016 Day 3: https://youtu.be/47_hMT9unCE

Thanks, Bill. I appreciate the reply, and will run those down.

Nick

Thank you for your comments Nick, you have a some great options available to implement what you are wanting to accomplish.

We will reach out to provide you an updated demo of our Orion client portal. I want to make sure you have an opportunity to see how Orion’s portal with the help of our integration partners can support your vision. Based on your vision, you may be interested in an integration we recently rolled out with Everplans:

http://www.prnewswire.com/news-releases/everplans-professional-and-orion-advisor-services-announce-integration-to-enhance-advisors-referral-networks-300420498.html

To the extent you want to leverage eMoney’s client portal, no problem! We integrate Orion’s portfolio values, performance calcs, and statements directly into eMoney’s portal.

In addition, if you decide you want to build a completely customized client portal experience, you can literally use the Orion client portal source code that we publish out on GitHub to provide a great start. We can pair you with a development partner that has experience building customized client portals using our API and will be familiar with other industry APIs as well.

At Orion, we are open architecture and are big believers that a one-size-fits-all approach to independent advisor technology is not the future. We are supporters of choice, especially when it comes time to implementing the client portal that best accentuates your firm’s value proposition. We will be in touch soon!

EC

Eric–

Thanks for the post! Eddie Sempek reached out to me yesterday, so we’ll be taking a look at the open architecture capability next week. I’ll start working on Ty… 😉

Thanks.

Nick

Personally, for planning-centric firms, I would lean more towards a central portal like eMoney Advisor, and using the eMx dashboard integrations to try to connect with other tools (to the extent possible).

The challenge with Orion is simply that it’s very investment-centric. Which is fine for firms centered on AUM and investment management. If Nick is focused on life planning, the idea that clients always see investment accounts and investment performance as the center of the client portal login experience may not be ideal… :/

More generally, yes I have lamented for a while that there’s a battle underway for control of the client portal and advisor dashboard experience, leading to a (problematic) proliferation of duplicative portals for clients and advisors. See https://www.kitces.com/blog/the-battle-of-advisor-dashboards-and-client-pfm-portals-advisor-technology-as-the-engine-or-the-interface/ from 2014 on this. I think it’s only gotten worse since then. 🙁 Too many platforms want to be all things to all advisors, and view it all from THEIR perspective, and not the advisor and client use cases. :/

– Michael

I’d be curious to know if you guys have any opinions of eMoney’s announcement for “An open API strategy to enable greater freedom and flexibility for firms to customize their own technology solution” in Q3 2017. Between this and Orion’s API could this pave the way for someone to swoop in with a best-of-both-worlds customizable client portal?

Laura

http://www.prnewswire.com/news-releases/emoney-advisor-launches-enterprise-division-to-support-the-wealth-management-needs-of-firms-at-scale-300428323.html

Platform companies like Uber, AirBnB, Amazon, and Apple have all claimed a dominant position in their respective industries. Is there a player in fintech who can claim dominance? Is it fair to say that establishing dominance as a platform in today’s world would require a company to function on top of all major custodians? Envestnet’s Tamarac Advisor XI might boast the largest market share as a true multi-custodial solution, and if I’m not mistaken, they charge BPS on AUM. If Tamarac created a model marketplace, and charged additional BPS for the distribution of those models would they successfully place themselves in between the investor and product manufacturer? If this is the case, could new competitors emerge to take on platform dominance by duplicating Tamarac Advisor XI’s functionality? While it would not be cheap or easy, it seems a nimble and young fintech firm could emerge as a winning platform.

There’s not a requirement that 1 platform control all the market share for platform business models to exist. Even amongst the companies you list, most have competitors (some larger than others). And those are far less regulated industries than financial services – where regulation (amongst other factors) leads to a more fractured market share environment.

I would view Envestnet’s business model as more akin to a platform model than a pure technology model, though. It’s not a coincidence that in the second graphic, they’re listed amongst broker-dealers and custodians. Their roots are as a marketplace (platform business model) between advisors and third-party managers, for which their technology forms the hub of that marketplace. Which is quite different than “just” selling software (though they now have a foot in each camp).

Bear in mind that one of the key aspects of platform models is the network effects that form around them. The more people who are on the platform, the more who are attracted to the platform. Merely replicating Tamarac Advisor Xi doesn’t make the asset managers show up (because there are no advisors there), nor the advisors show up (because there are no investment managers there). Just as Jet.com has ‘replicated’ most of Amazon’s actually website capabilities – you go to the website, look stuff up, and buy it – but isn’t able to steal away their market share at this point.

– Michael

Michael,

I found this article extremely educational and interesting. Your non-financial examples helped explain your concepts very well. I am immersed in the “FinTech” space (first in San Francisco and now in Sydney, with start-ups asking for advice on their marketing) and I can’t tell you how many times I have heard the “pitch” that “our new software will solve advisors problems..it will be able to do everything….” I worry for the number of players in the space, and I want them all to read this post. To your point I believe that FinTech Entrepreneurs can build the superior apps that plug into the true platforms as long as they focus on a single problem to solve. Plenty of hurdles exist for independent advisors and they still seek solutions, but they can’t pile on the expenses.

Thanks for what I imagine will be an eye-opening read for many FinTech players.

~Kristin

Michael,

Thank you for sharing this article. This resonated to us on many levels at AdvisorBid as our vision is to become the next Uber, AirBnB, or LinkedIn for the financial services industry. We know this is a bold statement and we have the early adopters, technology, and success stories to share. We’ve invested years into developing our technology and would be thrilled to receive feedback, suggestions, and/or ideas from advisors (and Michael) on how we can help everyone uncover more opportunities?

AdvisorBid Inc., the first patent-pending social marketplace to streamline financial advisors’ transitions, buying, selling, and merging of advisor businesses, and has revolutionized how advisors build relationships in a way the industry has never seen before.

Advisors in transition can weigh offers from leading broker-dealers (BDs), registered independent advisors (RIAs), and offices of supervisory jurisdiction (OSJs) in one secure, confidential marketplace. The marketplace provides easy step-by-step walkthroughs, tailored weekly snapshots, live dashboards for recruiters and advisors, and a messaging panel to communicate in real time, allowing advisors to conduct due diligence on new opportunities, and recruiters to bid on advisors in motion simultaneously.

“Calling 1-800 numbers at broker-dealers, RIAs and OSJs was the ‘old-school’ method. Why should an advisor go through the tedious process of filling out mountains of redundant paperwork for each company, one at a time, just to find out the portability of their business and how much that company is willing to compensate advisor to partner with their company? Advisors crave transparency. Helping them save time and maximize money making potential for them and their clients by leveraging the power of technology is the foundation of our vision.” says AdvisorBid founder and CEO, Brandon Spottswood.

A process that used to take weeks, months, and even years to endure, has now been chiseled down to a matter of minutes by providing advisors with all the information they need to make the most informed transition decision possible. AdvisorBid protects the anonymity of advisors during a move or selling their book of business, and enables advisors in motion to place themselves front and center with companies they’re interested in. AdvisorBid helps advisors lock-in higher payouts, lower advisory platform fees and expenses, gain access to world class marketing, practice management and technology, locate amazing cultures to plug into, and receive highly competitive upfront compensations to make the move.

“We believe that when leading financial services companies compete, everyone wins!” says Spottswood.

AdvisorBid is the only social marketplace where advisors can buy or sell a book of business, receive top offers to transition to leading BDs, RIAs and OSJs simultaneously, locate resources to propel their practice, and provides a new way for leading companies to showcase their opportunity, office space, post events and bid on advisors in motion. The marketplace has more than 1,200 active advisors throughout all 50 states and U.S. territories, created over 10,000 relationships, is partnered with more than 75 leading companies in financial services, and has facilitated over 32 transitions since its inception. AdvisorBid consists of a rapidly growing 10-person team, accredited investors, and welcomes more top talent.

The marketplace requires no membership fee, and is the only free solution for advisors to adhere to the Securities and Exchange Commission (SEC)’s proposed rule in 2016 — Adviser Business Continuity and Transition Plans, Release No. IA-4439. This proposed rule received strong industry feedback since it was released, and AdvisorBid is ready to accommodate demand upon approval. The marketplace provides the most advanced technology to bring advisors and financial services companies together like never before.

“AdvisorBid has provided so many opportunities for us. We have an electronic marketplace of prospective advisors, businesses for sale, and potential acquirers. It has not only become our first, but often our only one stop shop for business development.” says Chris Holloway, CEO at Investor Securities Group, a Super-OSJ at Securities America with over 100 advisors nationwide.

Next Steps: Please reply to this article, check out AdvisorBid at http://www.advisorbid.com, e-mail us at [email protected], or call us at 1-877-MKT-PLCE. We are eager to receive your feedback, ideas and suggestions.