Executive Summary

While the first safe withdrawal rate research originated nearly 20 years ago, it was simply based on an analysis of the sustainable cash flows that could be drawn from a portfolio over a 30-year time horizon based on various historical scenarios, ignoring the impact of fees and taxes. Of course, in the real world clients must bear the cost and impact of both, which reduce not only the amount of growth that the portfolio enjoys over time, but also the level of sustainable cash flows.

In reality, though, extensive research has been done over the past two decades to model the impact of taxes (and fees) on safe withdrawal rates. The impact is not as severe as some might fear - it's not as though the safe withdrawal rate must be chopped by 25% for a client in the 25% tax bracket - due to the fact that taxes have a natural self-mitigating effect, as they are only due when the portfolio has appreciated (which is when it has the most money available to pay those taxes). Of course, if the account actually is a pre-tax IRA, though, the net spending really does have to be reduced for the entire marginal tax rate!

Although the application of these adjustments can become complex when combining taxable accounts, pre-tax retirement accounts, and tax-free Roth IRAs, the fact remains that a proper application of the safe withdrawal rate research should reduce a client's recommended spending to account for the future drag of taxes, along with investment expenses and advisory fees. On the other hand, the good news is that other factors can help to boost the safe withdrawal rate as well, including a client's greater diversification (i.e., more diversified than the original research assumptions), spending flexibility, and varying time horizon. Ultimately, all of these adjustments can be incorporated to arrive at an appropriate safe withdrawal rate recommendation for a client.

How Taxes Can Impact Retirement Cash Flows

It's no great surprise to recognize that if clients must pay taxes from their portfolios, that there will be less available to fund their retirement cash flows.

However, the extent to which taxation reduces sustainable retirement income is less clear. For instance, if a client's marginal tax rate will be 25% and the safe withdrawal rate is 4%, does that mean the withdrawal rate has to be reduced by 25% of 4% (or about 1%), dropping it down to 4% - 1% = 3%? Or alternatively, if the average annual growth rate of a balanced portfolio is 8% and one quarter of that (or about 2%) will be consumed by taxes, does that mean the safe withdrawal rate actually falls to 4% - 2% = 2%? As it turns out, the impact of taxation is not nearly as severe as might be feared, for several reasons.

The first is that while taxes do drag on the growth of a portfolio, safe withdrawal rate research also assumes that in the worst case scenarios, clients will dip into their starting principal as well, rather than leave over a giant legacy to the next generation at the end; as a result, the impact of taxes is limited, as principal liquidations remain a tax-free return of basis.

Second, the reality is that in the case of taxes, in down years for the portfolio the tax consequences are limited (and may even result in a refund for deductible losses), and the bulk of the taxes are only due in years when the portfolio is up anyway (or where the portfolio was up in prior years and the gains that were deferred are finally coming due); this favorable timing effect helps to further ameliorate the adverse impact of taxes on the safe withdrawal rate.

Third, the reality is simply that in scenarios where the safe withdrawal rate must be relied upon - where either long-term returns were poor, or unfavorable sequencing meant that by the time good returns arrived the portfolio was largely depleted - there is often little tax impact, for the simple reason that there aren't many (or any) big gains on the portfolio in the first place! After all, for a retiree who gets underway on the eve of the next Great Depression, there simply aren't going to be a lot of gains to pay taxes on at all. If the retiree starts out in the midst of a significant bull market, the drag of taxation will be much higher... but then again, in such scenarios, the safe withdrawal rate would have been significantly higher to begin with, and a retiree following a 4% rule would likely be safe regardless of the tax drag.

Adjusting Safe Withdrawal Rates For Taxes

So given all of these dynamics, how should the safe withdrawal rate be adjusted to account for the impact of taxation?

Not surprisingly, the result depends on the underlying tax rate assumptions. After all, clients who are subject to relatively low levels of taxation - for instance, Federal tax rates of only 15% on ordinary income and 0% on long-term capital gains and qualified dividends - the drag of taxes on safe withdrawal rates is rather modest. For those facing higher levels of taxation - for instance, those with a significant pension and Social Security benefits whose portfolios will be taxed at least 25% on ordinary income and 15% on long-term capital gains - will be more severely impacted by tax drag. In turn, those at the top tax brackets will drag even further.

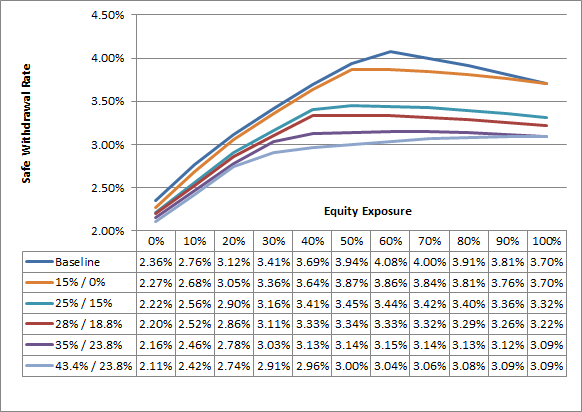

The chart below, adapted from the February 2010 issue of The Kitces Report and updated for 2013 tax rates, shows the "baseline" safe withdrawal rate (with no taxation) at varying equity exposures, and how the safe withdrawal rate shifts downwards as taxes are introduced. (The research assumes the fixed portion of the portfolio is invested in intermediate government bonds and is taxed as ordinary income, and the equity exposure is invested in large cap US equities and is taxed at preferential long-term capital gains and dividend rates. Taxes are applied annually to growth, but only to the growth that actually occurs from year to year, and losses are harvested if available, and used or carried forward as eligible. Results are tested through historical scenarios going back to 1871 and use the available data from Shiller. The portfolio is assumed to pay its own way for all tax obligations, and the post-tax safe withdrawal rate is the one that succeeds even after taxes have been netted against all growth through the time horizon.)

As the results reveal, taxation does indeed have a significant drag on a client portfolio. With a baseline peak in the safe withdrawal rate of just over 4%, the introduction of a modest level of ordinary income taxation trims the withdrawal rate by about 0.2%; however, rising to a moderate level of taxation (e.g., 25%-28% ordinary income and 15% - 18.8% long-term capital gains and qualified dividends) pushes up the drag to approximately 0.6% to 0.7%. Those facing the top tax rates find a tax drag as high as 0.9% to 1.0%. (Notably, those in the middle tax brackets would also find the optimal portfolio shifts to become more conservative, as the taxes on equities reduce the benefits of an equity-centric portfolio, until the client reaches the top tax rates where the spread between ordinary income and capital gains is so high that the optimal portfolios again become the more aggressive ones.)

Of course, these tax analyses all assume that the client's balance sheet is comprised exclusively of taxable accounts, which will generate taxes from time to time as the accounts grow. In the case of clients who have pre-tax retirement accounts (e.g., IRAs and 401(k)s), it's not merely the growth in the account that's taxed but the entire withdrawal, and all at ordinary income tax rates. Accordingly, in the retirement accounts, the impact is both harsher and simpler: if the withdrawal rate is 4%, and the client faces a 25% marginal tax rate, then the net safe withdrawal rate really is a full 25% haircut down to a net of 3%. On the other hand, if the account is a tax-free Roth, then a safe withdrawal rate of 4% really does produce net cash flows of... 4%.

Applications In A Client's Retirement Plan

In practice, most clients will have a combination of taxable and pre-tax retirement accounts (and perhaps some Roth accounts as well). To determine a sustainable safe withdrawal rate, each of the account types can be adjusted for the impact of taxation, and then combined back together, once a reasonable estimate of the future marginal tax rate has been made (i.e., what tax rate will the investment accounts face, after the bottom brackets are already filled by Social Security benefits, pensions, etc.). For example:

Harry and Mary have a $700,000 taxable account, a $500,000 IRA, and a $100,000 Roth IRA. Given their Social Security benefits and Harry's modest pension, a portion of their income will fall in the 15% tax bracket but most of it will fall in the 25% ordinary income (and 15% long-term capital gains) brackets. As a result, their safe withdrawal rate from the taxable account falls to approximately 3.5%, which would produce an available after-tax cash flow of 3.5% x $700,000 = $24,500 (again, this assumes the account will separately pay any taxes attributable to the account). The IRA's net safe withdrawal rate would be 3% (reduced by 25% for taxes), which means the account will provide annual withdrawals of 4% x $500,000 = $20,000/year but it is assumed that Harry and Mary can only spend $15,000 (the remaining $5,000 is allocated for taxes). The Roth IRA provides a 4% x $100,000 = $4,000/year after-tax cash flow (since it is all tax-free and ready to spend). Thus, in the end, Harry and Mary can generate sustainable after-tax cash flows of $24,500 + $15,000 + $4,000 = $43,500 from their portfolio, in addition to the available after-tax income from their Social Security and pension payments.

Of course, in practice it's worth bearing in mind that taxes aren't the only thing that reduces the safe withdrawal rate; investment costs have a further impact. However, the irony is that at higher levels of taxation, the impact of fees is reduced, for the simple reason that the portfolio does not grow as much and therefore the drag of fees is diminished (or conversely, the impact of taxes is reduced as fees take a bite out of growth). Thus, while the safe withdrawal rate should be adjusted downwards based on taxes and fees, the combined effect is slightly less severe than just adding the two.

On the other hand, it's also worth bearing in mind that there are factors that increase the safe withdrawal rate as well. For instance, as discussed extensively in the March 2012 issue of The Kitces Report, safe withdrawal rates can also be adjusted upwards for the benefits of diversification (the original research all relied on two-asset-class portfolios of large-cap US stocks and intermediate government bonds, though today's portfolios are clearly more diversified!), as well as the positive benefits of spending flexibility, greater risk tolerance, the impact of market valuation on safe withdrawal rates, and varying time horizons (which can increase or decrease the safe withdrawal rate). The safe withdrawal rate is also higher for clients whose spending is anticipated to decline in their later years, especially those for whom discretionary expenses compromise a significant portion of their retirement cash flows. Thus, while it's important to adjust the safe withdrawal rate for the impact of taxes, it's crucial that it be balanced against (or compounded by!) adjustments for other relevant factors that apply to the client's goals and circumstances as well!