Executive Summary

An independent financial advisory firm can have significant value, even if the business doesn’t have any physical or intellectual property to yield profits. Because the reality is that with annually recurring revenue and 95%+ client retention rates, there really is income-producing value in an advisory firm, even if it’s mostly based on the “goodwill” of clients to stick around year after year.

However, valuing a business whose primary assets is intangible goodwill can be challenging, especially given that the overwhelming majority of independent advisory firms are small/solo practices that generate little net profit beyond the healthy income paid to the advisor-owner to operate the business. As a result, the traditional Discounted Cash Flow (DCF) approach to valuing most businesses tends to break down (and undervalue) a “small” advisory firm (e.g., those with <$1M of revenue).

For such hard-to-value assets, an alternative approach to valuation is simply to look at the prices being set by buyers and sellers in the actual marketplace, and to simply value the business relative to its marketplace comparables. In fact, sometimes digging further into the piecemeal value of the business isn’t even relevant, just as no one values a car by disassembling it to value and then add up all the component parts; instead, for nearly 100 years, they’ve just looked up the going market value in the Kelley Blue Book instead.

In the context of advisory firms, the leading “Kelley Blue Book” solution for valuation is FP Transitions and its “Comprehensive Valuation Report” (CVR), which uses their comparables database of more than 1,500 advisory firms bought and sold in the past 20 years to estimate the value, after making reasonable adjustments for transition risk, cash flow quality, market demand, and the payment terms of the transaction itself.

Unfortunately, the FP Transitions CVR valuation estimate isn’t quite as cheap and accessible as buying the Kelley Blue Book – due to the harder-to-value aspects like transition risk and cash flow quality that must still be considered – but nonetheless, at $1,200, it makes getting a reasonable valuation accessible for the vast majority of independent advisory firms. In fact, a growing number of firms get regular valuation updates every year or two, just to understand how the value of their firm is changing, and whether/how they should make changes to further enhance the value.

Ultimately, the largest advisory firms that have greater complexity may still want to rely on custom valuations using the DCF approach, and a growing number of online valuation tools for advisory firms are starting to crop up to compete as well. Nonetheless, it’s hard to argue with going right to the source, and getting a valuation from FP Transitions using their actual (albeit proprietary) database of over 1,500 completed advisory firm transactions.

The Challenge In Valuing A Financial Advisory Firm

A financial advisory firm can be incredibly valuable, even though unlike most “traditional” businesses, it has no equipment or other physical income-producing assets, nor any intellectual property that can be licensed. Nonetheless, advisory firms have a client base, that pays regular annually recurring revenue, and has an astonishing lifetime client value given 95%+ retention rates for those clients year after year. Which means if a buyer can step in, and merely continue to service those existing relationships, there’s a profitable cash flow ready and waiting.

And as a result, advisory firms can be sold for substantial sums, even though the overwhelming majority of the sale price is based on nothing more than the “goodwill” of the clients to stick around.

Except the question arises: how much, exactly, should a buyer pay for an advisory firm whose primary value is just the goodwill of clients? Especially if there’s a risk that goodwill may be overly attached to the advisor who is about to walk out the door, as an estimated 95% of advisory “firms” are really just a book of business or a small practice served solely by an advisor and perhaps a handful of support staff (who may or may not be loyal to a new owner/buyer).

Valuation Methodologies For Financial Advice Businesses

The classic measure for income-producing businesses that don’t have physical assets able to be sold/liquidated is to just value the income stream itself, either by capitalizing the cash flows at an risk-appropriate cap rate, or for smaller and potentially-more-rapidly-growing businesses, to calculate the discounted present value of future cash flows (more simply known as the “Discounted Cash Flow” [DCF] methodology).

The problem, however, is that the DCF methodology doesn’t align very well to solo-owner independent advisory firms. After all, the DCF method is generally predicated on calculating the free cash flow of the acquired business, after replacing the key employees. Except in a solo advisory firm, almost all of the “profits” of the business are simply the compensation OF that owner-advisor. And so, to a third-party buyer, the present value of the free cash flows would be relatively modest.

In January 2000, we listed our first practice for sale, a fee-based sole proprietorship. We used a multiple of about 1.4 × TTMR (trailing 12 months revenue), an opinion extrapolated from the results of the discounted cash flow analyses that many at the time insisted held the right answer.

In other words, the DCF model seemed to have priced the business far too low – in what appears to have been a combination of both a sheer understatement of the value of a solo advisory firm based on the DCF methodology, and also the fact that, in the early days, appraisals were typically tied to all-cash transactions, despite the fact that virtually all advisory firm acquisitions today use some kind of shared-risk shared-reward structure (which ultimately allows for higher valuations, at least if/when the client base transitions successfully).

But if the DCF model doesn’t work for smaller advisory firms, how should you determine the appropriate price for a buyer and seller (and not let it become a major point of dispute and contention)?

Valuing An Advisory Firm From Direct Market Data Comparables

One of the most straightforward ways to value a hard-to-value asset is simply to look at what other similar assets are selling for in the marketplace, and just make adjustments along the way for known-to-be-relevant features of the particular asset.

In point of fact, automobiles are commonly priced this way, a practice first established by Les Kelley when he created the Kelley Blue Book, that “simply” estimated the value of a car by looking at the market prices of other cars being bought and sold in the marketplace (with reasonable adjustments for everything from wear-and-tear condition, to upgraded features).

Similarly, this kind of market data approach is also how most home-buyers estimate the value of a piece of real estate (first with the help of a real estate agent, and now often with online tools like Zillow), starting with the base going rate of comparable properties in the area, and then making adjustments for known differences (e.g., upgraded appliances, kitchen and bathroom remodeling, and a recent roof reshingling).

Of course, the challenge in the advisory firm context is that pricing an advisory firm based on comparables requires a large database of comparables in the first place! Though this was a challenge in the past – FP Transitions, which has been facilitating advisory firm Mergers & Acquisitions for nearly 20 years – actually does have a database now, of more than 1,500 completed transactions!

The FP Transitions Comprehensive Valuation Report (CVR)

The FP Transitions Comprehensive Valuation Report (CVR) aims to provide a “most probable selling price” estimate of value by looking at comparable market data from its proprietary database, and then adjusting the valuation based on relevant market factors.

In the context of advisory firms, the three primary adjustment factors used to estimate a price in the CVR are: Transition Risk, Cash Flow Quality, and Market Demand.

Transition Risk

Transition risk is arguably the biggest and most material issue to consider. After all, if the clients don’t transition to the new owner-advisor, and their recurring revenue doesn’t stick around, the entire value proposition collapses.

And notably, there are a lot of issues to consider when assessing transition risk, including how long the clients have been involved with the firm in the first place (and therefore how likely they are to remain ‘loyal’ and stick around), the availability and willingness of the departing advisor to stick around after closing to help with the transition, whether clients will continue at the same broker-dealer/custodian or have to be transitioned to a new platform (as a requirement to re-paper accounts isn’t fatal, but at least increases the risk that fewer will transition), and whether there’s already any established relationship between the buyer and the clients (for instance, an internal transition or intra-family transaction usually has lower transition risk than a third-party buyer).

Of course, it will never be perfect – FP Transitions notes that even in a typical well-executed acquisition, only 90% to 95% of clients stick around after a year. But obviously, it could be better, or could be far worse… which matters, a lot, to the value of the advisory firm.

Cash Flow Quality

In addition to the transition risk of clients, it’s also important to recognize the “quality” of the cash flows that the clients are paying – in other words, what are the risks and underlying trends of the cash flows themselves.

For instance, the demographics of the clients who are paying the advisory fees is a big deal when it comes to cash flow quality of the business. After all, there’s a huge difference between generating $500k/year of revenue from a bunch of 75-year-old clients who are spending/withdrawing, versus a group of 50-year-olds who are still accumulating and mostly past the stage of paying for college (where there should be a lot of substantial ongoing contributions).

Similarly, there’s a big difference between a firm where half that $500k of revenue is a handful of key clients, versus one where the revenue is evenly spread amongst 50 clients (which in turn is different than a firm where there’s 500 clients, and such a high volume of small clients could actually be a challenge unto itself).

In situations where there actually are multiple advisors, the “cash flow quality” also involves the question of how likely it is for those other advisors who support the clients (and their cash flows) to stick around, or whether they may break away, and take clients with them, potentially severely undermining the cash flows for the buyer.

Market Demand

Last but not least, there’s the sheer market demand itself, which is driven by the size of the firm and the structure of the practice (for instance, sellers on a large custodial platform may have more demand than those currently at a small broker-dealer), its location (as the buyer may or may not want to expand to clients in that location), and whether the practice has a niche or other unique characteristics that would add strategic value.

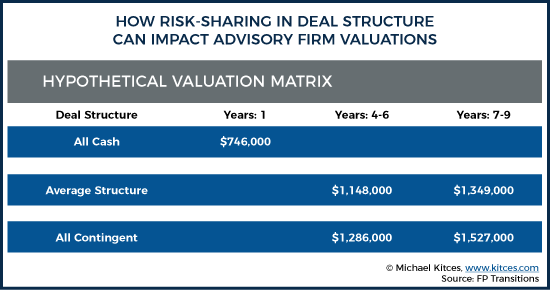

Payment Terms

Of course, it’s also important to note that Payment Terms matter, too. Because how the payments are classified and structured can impact the taxation of the transaction for the seller, and also the buyer. Which matters, because whether a buyer can deduct or amortize the purchase price has a real impact on what he/she may be willing to pay in the first place.

In addition, the reality is that the more risk-sharing there is in the terms of the deal, the easier it is for the buyer to pay more (at least if the deal works out well, because the buyer is protected if the transition goes poorly).

In practice, Grau notes that deals typically include some cash at closing – e.g., 30% – because the seller usually won’t tolerate “nothing down” (although pure revenue-sharing transitions do occur sometimes within broker-dealers), but the buyer won’t accept the risk of an all-cash deal that might not turn out well. And Grau advocates for a performance-based promissory note that reduces the remaining amount owed after a year or two if there’s been a substantial “miss” on anticipated retention.

The Importance Of Getting A (Regular, Independent) Valuation

One of the reasons that the Kelley Blue Book (KBB) became so popular as a means to figure out the price to buy or sell a used car was because it was so simple and easy to use. It made reasonable pricing information easily accessible, and potential buyers or sellers could simply look up the car in question, make a few reasonable adjustments, and get a good estimate of the appropriate price (from an independent source they could mutually agree upon). Of course, an especially unique car with specialized features might require a more formal appraisal process. But for the overwhelming majority of transactions, the KBB got the job done efficiently.

And arguably, the same may be true for what FP Transitions has created with its CVR valuation solution. As while there are advisory firm valuation experts who can assist in applying the DCF model to large and complex advisory firms, the reality is that for most practices, simply looking at comparable market data, and making reasonable adjustments for known-to-be-relevant factors (e.g., transition risk, cash flow quality, etc.) are more than sufficient to get a good estimate of a reasonable price for a buyer and seller. In some cases, more detail doesn’t even help, just as disassembling an entire car and valuing each component from the bottom up won’t actually give a better valuation than just looking at what price buyers and sellers are valuing the car in the actual marketplace.

Especially since for “smaller” practices as opposed to businesses (e.g., most of those under $1M of revenue), it’s not even clear that the more granular DCF methodology is effective to value the firm, as it appears to under-rate the value for buyers who aren’t just looking to invest capital for profits, but want to “buy a job” that will pay them well to service the clients, too.

The relevance of this for the individual financial advisor is that it tools like the FP Transitions CVR make “regular” valuations of an advisory firm more feasible because the straightforward market data approach brings the cost down substantially. While “complex” firm valuations can run $6,000 to $16,000, advisors can get a CVR from FP Transitions for just $1,200/year. (Michael’s Note: Nerd's Eye View readers interested in purchasing an FP Transitions CVR can receive a $200 discount through March 31, 2017, when using the KITCES200 discount code.)

Notably, that’s still significantly more expensive than the automobile equivalent of just buying the Kelley Blue Book – ostensibly because it’s still a more manual (and somewhat subjective) process to “score” or index an advisory firm’s transition risk and cash flow quality and assess market demand. Nonetheless, the price point is low enough that even solo advisory firms could get “regular” valuations every year or few.

This can be especially important for those who are considering a sale in the coming years – even if not imminent – because it provides clear feedback on what the firm is really worth, and indicators of what can be changed or improved to enhance the value by the time it’s really time to sell. In other words, it gives you (the advisor-owner) an understanding of the levers you can move that materially maximize value.

And of course, getting an (independent) valuation is also important for those who really are getting ready to sell their advisory firms, especially if they’re “smaller” advisors. Because the reality is that even a “small” advisory firm still has real value to a buyer. In fact, Grau emphasizes in his book that just getting indications of interest from the “closed market” platform of an advisor’s existing custodian or broker-dealer may substantially undervalue the business – a fact that the custodian or B/D itself may not disclose or emphasize, since it’s in their interests to see the assets retain on their platform, not to necessarily maximize the value for the selling advisor. And an advisor who doesn’t get an independent valuation may never realize what he/she missed.

Of course, it’s worth noting that FP Transitions is not the only company offering valuations for financial advisory firms. Other ‘competitors’ include Echelon Partners and DeVoe & Company for very large advisory firms, along with Succession Resource Group, and Advisor Growth Strategies. Another player is Gladstone Associates, which initially developed and then separately spun out an online eAnalytics platform called Truelytics to facilitate and ease the (annually recurring) valuation process, along with more recent newcomer 3X Equity (at an even lower price point). And firms like Succession Link and RIA Match are trying to operate as competing marketplaces to FP Transitions.

Nonetheless, FP Transitions appears to be unique in having real-world market data of more than 1,500 transactions that they’ve facilitated over the past 15+ years, giving them unique insight into the factors that are actually driving the valuation process, and what buyers and sellers are actually agreeing to (as opposed to just what a DCF model would predict).

For the truly large and complex advisory firms (e.g., $500M+ and especially $1B+), it may still be appealing to get an even more customized valuation using the DCF model. But for the overwhelming majority of practices, where the owners (and the DCF model) seem to actually underestimate the value of the practice, the FP Transitions Comprehensive Valuation Report appears to be a good fit to fill the void.

So what do you think? Would you pay for a Kelley Blue Book valuation of your firm? Have you used the FP Transitions Comprehensive Valuation Report? Do you think all firms should get regular valuation updates? Please share your thoughts in the comments below!

(Michael’s Note: Nerd's Eye View readers interested in purchasing an FP Transitions CVR can receive a $200 discount through March 31, 2017, when using the KITCES200 discount code.)

Probably a good idea to pay for a valuation every three years or so. Or subscribe to the $1200 annual tool. Overall, not a bad price for tracking biz metrics and valuation.

Not a very helpful article. How about a better example of a lifestyle practice with say $3-400,000 in revenue – the reason planners don’t retire is that most of the revenue is pretty dependable ongoing…. What’s that worth to be bought out. If buyout over 7 years what is a typical split?

Brad,

I’m not quite sure what you were expecting here. The whole point is if you want to know what a lifestyle practice with $3-400,000 in revenue is… get a professional valuation to find out.

If you’re looking for a rule-of-thumb valuation, there are plenty out there. 2X revenue says the practice is worth $600,000 to $800,000. But that doesn’t mean it’s what a willing buyer will actually pay you when the time comes, if you don’t adjust the valuation for all the other relevant factors…

– Michael

A couple of major differences between valuing a practice and a car are the presence of cash flows in the business and uniformity of the good being valued.

The best indicator of value for an income producing asset is the discounted, future value of said cash flows. I would suggest a superior way of assessing value would be to model the cash flows of the business under a number of different scenarios (e.g. realistic risk associated with loss of clients/revenue upon departure of key employee) and obtain a range of values based on those outcomes. This stilll leaves some discretion to appraiser for discount rate to apply but would be more specific to each firm.

Unlike using KBB to value a relatively uniform good (I.e., car) the challenge with using a multiple to value a financial services firm is that no two are exactly alike. Differences in cost structure, level of services provided, and key advisor loyalty are extremely difficult variables to control for by merely applying an adjustment to a market multiple of revenue and generating an opinion of value.

Great topic to cover and excellent points, as always. The question I keep asking myself is at what point does KBB stop tracking the valuation of vehicles based on what they are selling for and start declaring the valuation of vehicles because everybody uses them to start the negotiations?

I suppose FPT could find themselves in the same position given their market share. Having a database of 1,500 deals is fantastic, but how many of those deals began by using FPT’s valuation estimates?

A book of business, just like a car, is going to be worth what someone is willing to pay for it. The market itself naturally discovers the true value of a book of business based on an advisor’s visibility of that book of business. Advisors simply want to know what’s out there and want to know how to find it.

At http://www.AdvisorBid.com – we offer the FIRST and only FREE patent-pending platform with NO subscription fee for advisors to bid on books of business for sale, sell your business for top dollar, transition to a new broker-dealer, breakaway and start or join an existing RIA, or recruit advisors to your broker-dealer, RIA, or OSJ by bidding on advisors in motion. We’ve transitioned over 35+ advisors in the past couple months, including nearly a billion of assets transitioned. Our vision is to connect our industry together like never before.

At AdvisorBid, advisors do not have to pay $1,200 for a valuation, and/or $800-1,000 for an annual subscription fee, just to find out what an advisor is willing to offer or pay for it. AdvisorBid is the only FREE marketplace to connect to other advisors near you and discover what your practice is worth. Valuations are only as good as what the buyer is willing to pay for it. Demographics, timing of the year, product/investment type, and various valuation methods are some of many factors that go into account for what a book will be sold. They key is, getting noticed. The more advisors that simply know what you’re looking for, the more you’ll be able to maximize your money making potential.

Schedule a conversation with us to learn more at: http://advi.so/speakwithus

Watch our Welcome to AdvisorBid video at: http://advi.so/welcometoadvisorbid

Sign up for FREE today at: https://advisorbid.com

Cheers to your successes this year!

Brandon Spottswood

Founder & CEO at AdvisorBid

As a small firm that has provided valuations and transition consulting since 2009, I can say FP Transitions does some things very well and you have hit on them.

The biggest problem I see with literally everything FPT delivers is they operate with an overwhelming seller bias. As a result their valuations are too high. (BTW, I think Truelytics is almost always on the low side). Even more important factors than the price, how the deal is structured, who carries the risk, and how the risks are balanced, all lean heavily in the buyer’s favor if they follow FPT’s advice.

As an example directly from their CVR, FPT claims that a deal structure where the buyer pays a large down payment and the entire remaining balance under a fixed note is a deal where risk is borne equally between the parties. Not true!

If the deal is 100% based on fixed payments, whether in a lump sum or over time, the risk is borne by the buyer because they have no way to adjust the payments based upon revenue retention. This is far from a balanced deal.

A truly balanced deal is one where, other than a down payment, payments are made over time and are revenue based, that way both parties participate in growth or declines together. But in their CVR they claim this type of deal loads all the risk onto the Seller which is illogical.

From day one I have committed to never allowing a buyer and seller to ink a deal that was not a fair and balanced deal, regardless of which party hired me. That is the way to do this work.