Executive Summary

With health insurance premiums continuing to rise every year – in some areas, compounding at double-digit rates – more and more consumers are questioning whether it’s even worthwhile to have health insurance at all. Especially now that the Tax Cuts and Jobs Act of 2017 has repealed the Individual Mandate (effective in 2019) that would have applied a tax penalty for those who decline to enroll in health insurance through an individual exchange.

At the same time, though, rising health insurance premiums have also increased the popularity of alternatives to traditional health insurance, including so-called healthcare sharing programs. Typically organized under ministries or other religious organizations, healthcare sharing programs operate outside of traditional health insurance, and in some cases may be more restrictive with their benefits… but are also operating at a cost that is substantially less than traditional health insurance.

In this guest post, Jake Thorkildsen provides an in-depth explanation of what healthcare sharing programs are, a review of the most popular healthcare sharing programs and ministries, why healthcare sharing programs are not for everyone, and the kinds of situations where they might at least be considered.

So whether you’re simply curious to better understand an increasingly popular alternative to traditional health insurance – now covering more than 1,000,000 people – or are actually trying to evaluate and compare programs for a particular client situation, I hope this comparison and review of the various healthcare sharing programs is helpful!

As health insurance premiums continue their trajectory into outer space, the subject of healthcare sharing programs as an alternative to insurance is becoming more common. On the XYPN Radio VIP Community Facebook group, which is increasingly becoming a ‘brain trust’ of sorts for advisors to ask questions and share insights, several advisors have put out questions in the forum around how these programs work and how/if they should be discussing them with clients. Michael Kitces, intrigued and noting the relevance of this topic, posted in the group that someone should write a guest post to discuss healthcare sharing in more depth – thus the birth of this post.

What are healthcare sharing programs? Are they a viable alternative to health insurance? How do they work? What are the risks? And how should financial advisors communicate about these programs with clients? I’ll address each of these questions in this post, providing those who are not familiar with these healthcare sharing programs a ‘lay of the land’ and my opinion on how financial advisors should approach the subject with clients. In full disclosure, my family has been using a healthcare sharing program for a few years and we’ve had a favorable experience – so I may have some inherent bias, but also real-world perspective as a participant, and have attempted to write an objective summary.

What Is A Healthcare Sharing Program Or Ministry?

Let’s begin with an overview of what a healthcare sharing program actually is. These are faith-based programs (of varying degrees with options for different religious denominations) which facilitate voluntary sharing among members for eligible medical expenses. Specifically, members send in monthly ‘shares’ (i.e., premiums) which are distributed to or on behalf of other members with medical expenses (i.e., benefits payments) in accordance with program guidelines. They are built upon the principle of people with similar beliefs and values coming together to share each other’s burdens, not unlike the risk-pooling nature of health insurance.

However, a large part of the appeal of healthcare sharing programs is that in practice, they are much less expensive than health insurance. As a result, families can become members in healthcare sharing programs for $300 to $500 per month, compared to the average unsubsidized cost of family traditional health insurance coverage at $1,564 per month, and its easy to see the savings appeal for those who lack generous employer coverage or do not qualify for government premium assistance. In addition, healthcare sharing programs typically have lower out-of-pocket expense limits than typical high-deductible health insurance plans as well.

Notably, though, healthcare sharing programs are not actually health insurance (as discussed further below). In fact, part of the reason that they’re less expensive than traditional health insurance is that their coverage may be more limited (than Affordable Care Act mandates for essential health benefits). And their limitations of coverage are based not only on managing potential costs and claims, but also the faith-based nature of the programs in the first place.

Accordingly, while healthcare sharing programs do cover many typical medical expenses that health insurance covers, they typically do not cover many health-related costs deemed to be ‘unbiblical’ – which the programs define in their guidelines – and may exclude payments for birth control, abortions, injuries related to alcohol or drugs, and injuries from certain hazardous activities (or even failure to wear helmets or seat belts in some situations).

Nonetheless, participating members are exempt from the Affordable Care Act’s individual mandate to purchase health insurance, even though healthcare sharing programs do not meet the ACA’s essential health benefits requirements (an ACA exemption soon to be a moot point, courtesy of the recent tax reform legislation’s repeal of the individual mandate starting in 2019), and complete IRS Form 8965 at tax time which attests to membership in a qualifying program (in lieu of traditional health insurance).

To become a member, healthcare sharing programs may require agreement with a statement of faith, and in some cases even have a process to verify regular church attendance, although each has a different policy (and one of them is known for its more inclusive member qualifications).

How Healthcare Sharing Programs Differ From Health Insurance

Even though it may seem like a group of people pooling risk and sharing expenses is the definition of insurance, it isn't. There are some key features of health insurance which healthcare sharing programs lack, including:

- Insurance is broadly defined as "a practice or arrangement by which a company or government agency provides a guarantee of compensation for specified loss, damage, illness, or death in return for payment of a premium." As stated in healthcare sharing program disclaimers, no such guarantee exists.

- Insurance is a legally binding contract between an insurer and the insured. As each program will make clear, everything in these programs is ‘voluntary’, and there is no actual binding contract between a member and the program or between members to receive payment.

Nonetheless, while healthcare sharing programs are not health insurance (you will notice in their literature and on calls that they are adamant about not using any traditional insurance lingo), they rely on a similar framework, albeit with different terminology. Here are some common health insurance terms, and their health sharing program equivalents:

- Deductible = personal responsibility, annual household portion (AHP), or Annual Unshared Amount (AUA)

- Premium = monthly "share"

- Claim = eligible event, incident, or illness

- Explanation of Benefits (EoB) = Explanation of Sharing (EoS)

More generally, a fundamental premise of insurance is a group of people pooling high-impact / low-probability risks which are more easily borne by a group instead of an individual… and in this regard, health sharing programs are designed to mimic insurance, and thus far have successfully done so for decades to the tune of billions of dollars of facilitated sharing payments. Speaking from personal experience, our only major medical event (birth of my daughter – which turned into a longer than expected stay at the hospital) was handled by our program with a high level of professionalism, expediency of payouts, and ease of communication – it far exceeded my expectations.

Adoption Of Healthcare Sharing Programs In Lieu Of Traditional Health Insurance

In a time of rapidly increasing health insurance costs, people are turning to this alternative option more frequently. All of the major healthcare sharing groups have seen dramatic increases in membership over the last few years – with total membership now over one million people between the four major programs (Christian Healthcare Ministries, Liberty HealthShare, Medi-Share, and Samaritan). For reference, total membership in 2010 when the ACA was passed into law was reportedly around 200,000.

There's a lot of material available on the web discussing these plans – some of the information is good, and some not so much. But for advisors, there is an increasing need to be well-informed and objective, whether or not you agree with the religious principles they are based upon. The percentage of Americans who identify as 'Christian' may be declining, but it's still over 70% of the country and, therefore, still highly relevant.

Arguments abound about how well each of these programs actually fulfills their objective of people with a shared value system supporting one another’s needs. As with even well-intentioned large and growing non-profit organizations, the programs have all implemented policies and procedures which critics suggest are designed more around keeping costs low than sharing every need. However, the core of healthcare sharing program guidelines are generally clear about what is covered and is not – even if what they do and don’t cover isn’t always the same as traditional health insurance. Accordingly, the important thing for current and prospective program members is that they understand what’s in the program guidelines (and that the programs will follow their own guidelines to a T). Of course, each program works differently from insurance and, to make it more complicated (like most planning subjects!), they all have their own unique approaches, pros, cons, and quirks.

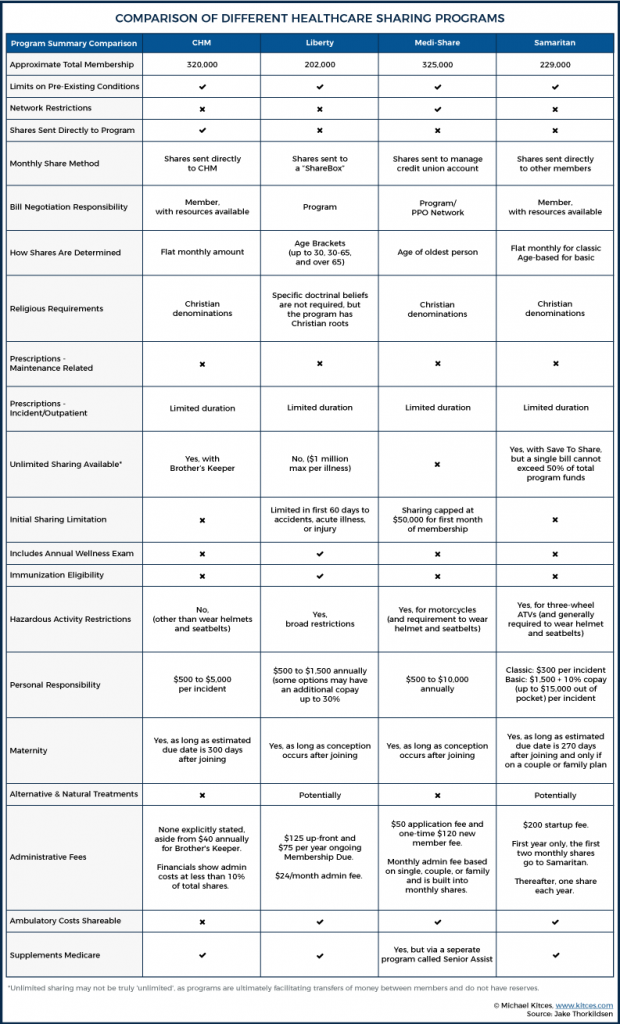

Comparison And Review Of Most Popular Healthcare Sharing Programs

Even in a Nerd’s Eye View post, there isn’t enough space to give a thorough explanation of all the ins-and-outs of each player in this field. However, what follows is a summary and comparison of each of the four major programs, followed by a discussion of their risks, and then my thoughts on how advisors should approach the subject. As you’ll see, given the differences amongst each, there generally isn’t one best healthcare sharing plan, as different programs or ministries are better for some needs than others.

Nonetheless, the most popular healthcare sharing programs reviewed here include:

Christian Healthcare Ministries (CHM) Review And Pricing

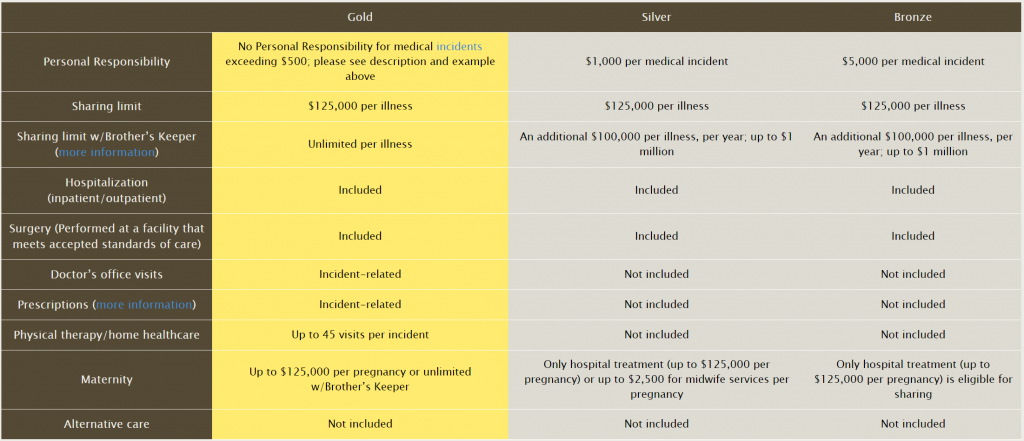

Christian Healthcare Ministries was founded in 1981 and was the original medical expense sharing platform. As with other healthcare sharing programs, it operates as a 501(c)(3) tax-exempt organization (although the 'premiums' paid across all of these programs are not considered charitable contributions because benefits are received, which means they are not tax deductible). According to their website, members have shared over $2.5 billion in medical bills. Total membership currently stands at approximately 320,000. CHM has Gold, Silver, and Bronze options (not to be confused with ACA plans of the same name!) with varying benefits and costs.

Who can be a member? Per the CHM website:

To be CHM members, participating adults must be Christians living by biblical principles, including abstaining from the use of tobacco and the illegal use of drugs (1 Corinthians 6:19-20), following biblical teaching on the use of alcohol, and attending group worship regularly if health permits (Hebrews 10:25). There are no restrictions based on age, weight, geographic location or health history.

That last point notwithstanding, there are some stipulations on pre-existing conditions as discussed later.

Patients are essentially cash payers with their doctors, and are responsible for negotiating the best deal they can on medical expenses (with some resources available from CHM to provide coaching or even negotiate on a members behalf). Members receive the bills and interact directly with the medical provider's billing department and pay the provider directly. Once a medical bill is received and negotiated, the bill is then submitted to CHM for processing (in practice, bills are often submitted before final pricing has been agreed upon so CHM can be looped into the process), at which point it can take "up to 120 days" before the member receives a check from CHM which they will then use to pay the provider. (Notably, this means that, in theory, a member could receive a check from CHM and then not actually pay their provider, although doing so would be grounds for termination of membership going forward.)

Ironically, while healthcare sharing members do not have access to an insurer’s negotiated costs on healthcare services, most medical providers are so happy to not deal with insurance companies and their claims process that large discounts are often available for cash-pay customers who are willing to ask (often even after services are rendered, as the billing department is typically separate from the medical service providers anyway). Sometimes telling the provider upfront that you’re a self-paying customer is all it takes, although in other cases it can take a fair amount of work. Nonetheless, obtaining a discount in line with “usual, customary, and reasonable” pricing is often not that hard, although it may require more than one call and more than little patience. In situations where pricing isn’t established initially (like an emergency), members will get the care they need and handle billing later – even if the resulting bill is higher or not as discounted as CHM would like to see, 100% of the eligible bill will still be shared regardless of the discount amount. Per CHM’s website, “Most CHM members are successful in getting discounts. If you have trouble getting a large discount (at least 40%), the CHM Member Advocate department has patient advocates who can coach you or even negotiate with your providers on your behalf.” And if it’s any indication of how effective CHM and its members are in obtaining discounts, their pricing has not increased for a decade.

The CHM deductible-equivalent is referred as the ‘personal responsibility’ and is per incident – which means there is no set annual deductible. Twenty events could equal 20 incident 'deductibles' in a single year, where the amount the member is responsible for varies from $500 to $5,000 per incident depending on the chosen option (Gold, Silver, or Bronze). On the other hand, if someone only has a single incident that spans multiple years and needs no other health care services, the per-incident personal responsibility limit could eliminate any costs in subsequent years (other than monthly shares). An 'incident' is defined at length in CHM’s guidelines, but essentially is all care related to the same medical event – for example, maternity is a single incident all the way from the original doctor visit through delivery and follow-up.

Interestingly, any discount the member obtains can be applied towards their per-incident personal responsibility (deductible) amount. For example, a $10,000 expense for an eligible incident is negotiated down to $6,000 for someone on the ‘Gold’ plan which features a $500 per incident personal responsibility. The member would receive $6,000 from CHM, and turn that over to the provider, without being responsible for the $500 ‘personal responsibility’ because it was more-than-covered by the $4,000 discount. This is an incentive for members to aggressively negotiate for discounts. However, members are not responsible for any portion of an eligible medical expense which CHM feels is not appropriately discounted, and, of course, the discounts themselves need to be documented (shown on the bill or proven by another iteration of the bill).

The base plans do have maximum sharing limits for any given incident (i.e., a maximum amount of “claims” that will be paid, beyond which members are responsible for their own costs again), but members can opt into CHM’s “Brother's Keeper” program, which provides for catastrophic coverage above those limits (for an additional, albeit small ‘share’). Brother’s Keeper is simply a name for a separate fund held at CHM – it is not a third-party program or an actual form of insurance. Only the Gold program with Brother's Keeper provides "unlimited financial assistance… for eligible medical bills". Silver and Bronze plans are capped at a maximum sharing limit of $125,000 per illness, which increases to a million dollars with Brother's Keeper.

CHM does not have (or require) a provider network, and members are free to receive treatment from the doctor or hospital of their choice. In this regard, members have a remarkable amount of flexibility and control over their healthcare. However, a common member complaint is the length of time it can take to receive reimbursement for medical expenses (given a wide range of providers whose expenses must be reviewed). I asked CHM about this, and was given a response that it has a lot to do with how much growth they've experienced and they are working to improve processes, add and train staff, and reduce the time it takes to process bills for sharing. They also reminded me that, even at 90 to 120 days, they are often still faster than insurance. Still, when payments are pushed toward the outer edge of this timeframe, it can sometimes result in members having to set up payment plans with the medical provider while they wait for full reimbursement.

Plan prices are quoted in terms of “units”, where a single person is one unit, their spouse is another, and all dependent children combined are one more unit – for a maximum of three possible units for any family. Monthly shares are $150 for the Gold plan per unit, $85 for Silver per unit, and $45 for Bronze per unit. So, a family of three (or ten!) would pay $450 per month for the Gold plan. Separately, the Brother's Keeper program costs $25 per quarter per unit plus a $40 per membership fee annually. Thus, a family of three units would have about $28/month added to their base plan share, resulting in a total monthly Gold share of $478 if they also want Brother’s Keeper. The prices change only across plans but do not change with age (a 25-year-old in the Gold program shares the same amount as a 60-year-old in the Gold program). Monthly shares are sent directly to CHM, which makes it unique among the programs reviewed in this article – this feature will be discussed in more detail further below.

Liberty HealthShare Review And Pricing

In 2014 there was a merging of three different healthcare sharing groups, some of which had roots going back to the mid-90s, to form what is known today as Liberty HealthShare (“LHS”). Currently, LHS has approximately 202,000 members.

LHS has the reputation of being one the most 'inclusive' healthcare sharing programs, because they allow a wider latitude of religious belief among members. On their website, they state “It's a mission that many people can get behind, whether they are Protestant, Catholic, Mormon, Jewish, or don't identify with any of those groups.” In fact, while the other programs require prospective members to sign statements of faith, and may even obtain verification that one regularly attends church, Liberty merely requires that, among other points, you agree "everyone has a fundamental religious right to worship the God of the Bible in his or her own way" and that it is our "spiritual duty to God and our ethical duty to others to maintain a healthy lifestyle and avoid foods, behaviors, or habits that produce sickness or disease." This would seem to include anyone who respects religious freedom, understands the need for healthy living, and believes in God (which, in this context, could be open to a wide latitude of interpretation). Specific doctrinal beliefs are not required. For those who are not involved in a church, and/or do not fully agree with the detailed theological positions of some of the other programs, LHS could be a fit where the others are not.

In terms of how billing works, Members have a card with their Member ID #, providers submit bills directly to LHS, LHS verifies them for eligibility and obtains/negotiates discounts, and then coordinates payment directly to the provider. LHS seeks to obtain ‘Fair and Reasonable’ pricing for medical services, which it defines as at or below 150% to 170% of Medicare allowable rates – if fair and reasonable pricing cannot be obtained, it appears that Liberty will still fully share the expense as long as the incident is eligible under their guidelines (although they may notify the member that future bills from that provider may not be fully shared). Once a final price is negotiated on behalf of a member, LHS will send an Explanation of Sharing (EoS) to the member and the medical provider. This is a very different process than CHM, in which members are reimbursed directly and trusted to pay the provider.

Members send their monthly shares to a "Sharebox" – which is a separate account over which LHS will have a limited power of attorney. The Sharebox seems to serve a similar purpose as an RIA using a 3rd party custodian. As noted on the LHS website, "Money designated by members for cost sharing is never owned or invested by Liberty HealthShare℠. The money in your Sharebox is sent directly to another member's Sharebox who has a medical expense need." LHS moves money between the members’ Sharebox accounts according to need and will then issue payment directly to a provider from a Member’s Sharebox.

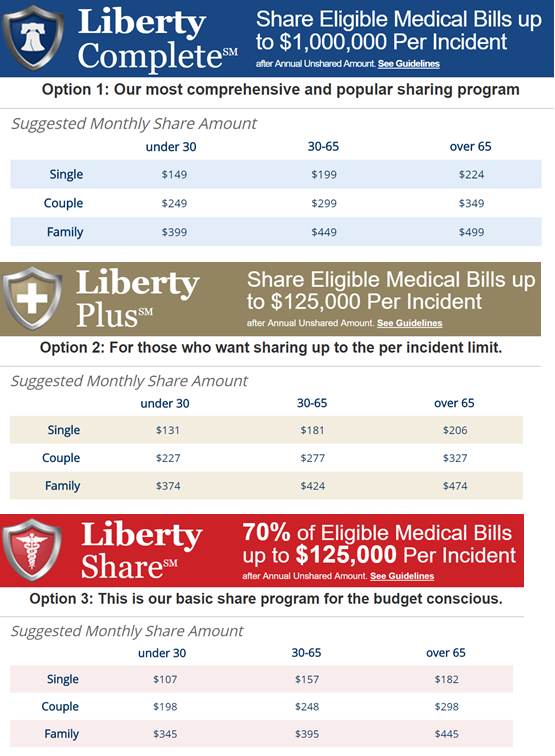

Like CHM, there are three options, and each has its own per incident maximum limits – Liberty Complete, Liberty Plus, and Liberty Share. Their top tier option, Liberty Complete, shares eligible medical bills up to $1,000,000 per incident. Also, like CHM, members are free to choose their own providers, and do not have to worry about in/out-of-network concerns.

All LHS options have a deductible-like feature called an Annual Unshared Amount (AUA), which is $500 for an individual, $1,000 for a couple, and $1,500 for family – it is the same across all three options. LHS also has a 60-day waiting period after initial enrollment where medical expenses “for any reason, other than accidents, acute illness or injury, are not eligible for sharing.” Also, monthly shares do increase with age. Members with certain health issues which LHS deems correctable (like high cholesterol) will be assigned a personal health coach and assessed an additional monthly share of $80 until the condition is no longer present.

In addition to its less exclusive membership requirements, Liberty is unique in four other areas:

- Membership includes an annual wellness visit including lab tests and other associated routine services up to $400 per year. This is not subject to the AUA.

- Immunizations are eligible for sharing (and not subject to the AUA for the first year of birth). The three other programs discussed do not consider immunizations to be an eligible expense.

- It is the only health sharing program discussed which does not have an option for ‘unlimited’ sharing. However, the $1 million maximum is per incident and not a ‘lifetime’ limit.

- Of the four major programs, it appears to be the only one which would cover an extramarital or teen pregnancy.

The “suggested share amount” pricing for LHS is comparable to CHM, but with age-based premiums is a bit more expensive for those aged 65 and older. Generally, LHS members receive more comprehensive benefits than other programs, though LHS is actually more restrictive when it comes to hazardous activities (as discussed later), and LHS lacks an unlimited sharing option. Also, despite being labeled as a “suggested” share amount, LHS pricing is still mandatory, to the extent that sending in less can result in loss of membership or a denial of sharing for medical expenses (though since it is not insurance, the payments are not technically contractual).

Medi-Share Review And Pricing

Medi-Share began in 1993, serves more than 325,000 members, and has facilitated the sharing of more than $2 billion dollars in medical bills.

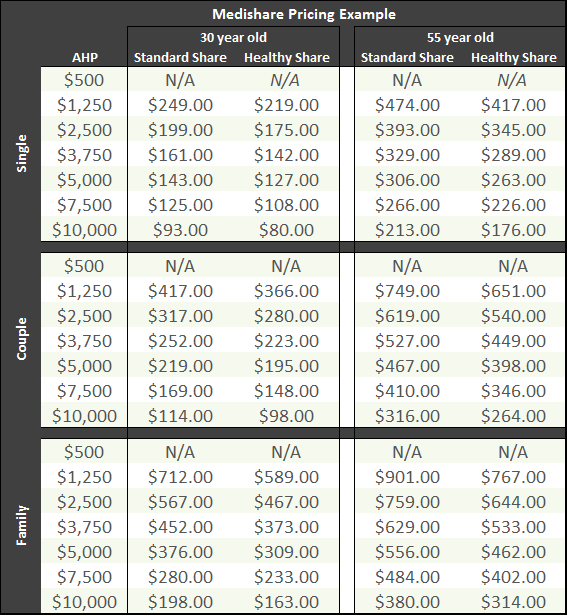

Medi-Share looks the most like traditional insurance out of the four programs reviewed here. Out of the box, it has no lifetime or per illness/incident maximums, which makes it unique among all four programs. Members do have an Annual Household Portion (AHP, the equivalent of a family deductible) which must be used up before the sharing kicks in, though, and there are options for the AHP ranging from $500 up to $10,000 (similar to selecting a deductible level, as a way to individuals manage their cost for participating in the program).

Medi-Share also has a separate Senior Assist program, which is meant for seniors over age 65 to supplement Medicare Part A and Part B (i.e., a healthcare sharing version of Medigap supplemental insurance). While the other healthcare sharing programs can supplement Medicare, they are priced no differently. Senior Assist, however, can be had for as little as $70 per month, and has a set $1,250 AHP.

To become a member of Medi-Share, applicants must agree to a detailed statement of faith and “attest to a personal relationship with the Lord Jesus Christ. A church leader may be interviewed to verify [applicant] testimony”.

Medi-Share members have access to the PHCS nationwide PPO network (PHCS is part of MultiPlan, a large provider of PPO networks), through which members benefit from similar discounting and bargaining power as other insurance companies. In this manner, it operates more closely to traditional insurance, as members are strongly incentivized to use in-network providers, and generally will pay more (i.e., have a higher personal responsibility amount) for going outside the network. When members need care, they go to the network provider, the provider submits bills to Medi-Share directly, Medi-Share then reviews and discounts the bills, and submits an Explanation of Sharing detailing the resulting price for the service(s) rendered. If the member has not yet met the AHP, the member will then pay the provider directly. If the AHP has been met, Medi-Share coordinates sharing of the bill through a similar mechanism as Liberty’s Sharebox. Medi-Share members have individual sharing accounts at an independent financial institution (America’s Christian Credit Union) where a limited power of attorney has been given to allow Medi-Share to move money between member accounts for direct member-to-member sharing (i.e. Medi-Share facilitates the sharing and sending of money from a member’s account to the medical provider).

As far as plan options go, Medi-Share allows members to choose from 7 different AHP levels between $500 and $10,000, and monthly share amount pricing is based on the age of the oldest person going on the membership (which then increases each year as that person ages). Pricing levels are for single, married, or family. Similar to the other programs, pricing for families is the same whether there is one child or ten. Medi-Share also includes a free telemedicine program for members, which members can utilize for a myriad of purposes without incurring the time or expense of actually traveling to a doctor’s office.

Because Medi-Share has multiple AHP levels and also varies pricing with age, its pricing grid (with every possible combination) would be quite large. For context, though, the table bellows shows pricing at the various AHP levels for single, couple, and family options for a hypothetical 30 and 55 year old (again, pricing is based on oldest member). Pricing quotes for other ages and AHPs can be obtained directly on their website using their ‘Share Calculator’ - https://mychristiancare.org/prices/.

Similar to Liberty, Medi-Share also assesses an $80 per month additional share for their mandatory Health Partner program for members with certain correctable health conditions such as high cholesterol. This is notable because health insurance companies cannot legally adjust pricing this way based on health conditions under the Affordable Care Act – they may only discriminate (price differently) based on age and tobacco use.

Samaritan Ministries Review And Pricing

Samaritan Ministries started in 1991. Today, they have 229,000 members.

Samaritan is closest in form to CHM out of the programs reviewed thus far. One of the key differences, though, is that rather than submitting medical bills and monthly shares to a centralized hub or managed 3rd party account where funds are distributed to the member with the medical need, members actually send checks each month to specific other people (i.e., other members who have “claims”).

For example, you might send a check to Joe in Montana for $250 and Mary in Missouri for $150 if your monthly share amount totals $400. In practice, members usually only need to send one check per month. And if you have a medical expense being shared, you may get several checks in the mail from people across the country. Often times, members send the checks with get-well cards or other notes with kind words and well wishes. This level of personal-ness (I know, not a word!) draws many to the program, while perhaps turning others away who are not comfortable with it or don’t want to deal with physically sending checks each month. At 229,000 members, plenty of folks seem to be perfectly okay with it. And they are currently rolling out a PayPal integration to facilitate electronic member-to-member sharing.

Samaritan appears to have the most exclusive membership eligibility requirements of all four groups. While Medi-Share may verify regular church attendance, Samaritan always requires a church leader verification which states the member regularly attends church at least three out of four weeks per month (health and weather permitting). Members are required to re-certify annually.

Like CHM and LHS, Samaritan members are free to use the providers of their choice, and are not bound by any in-network restrictions as with Medi-Share. Members get care, receive the bill as a cash-paying customer, negotiate it, and submit it for sharing, at which point the ministry staff will evaluate it for eligibility and then (assuming it’s a shareable expense) assign the need to members – who then write and mail checks directly to the Member with the need. In cases where Samaritan feels the price has not been appropriately discounted to a usual and customary rate, they outsource (at no additional cost) to a 3rd party called the Karis Group who will contact the medical provider and negotiate further on the member’s behalf. Even if their ideal pricing cannot be achieved, the expense will still be shared. However, the member may be asked to use a different provider in the future (or else be responsible for the excess amount in future bills from that provider).

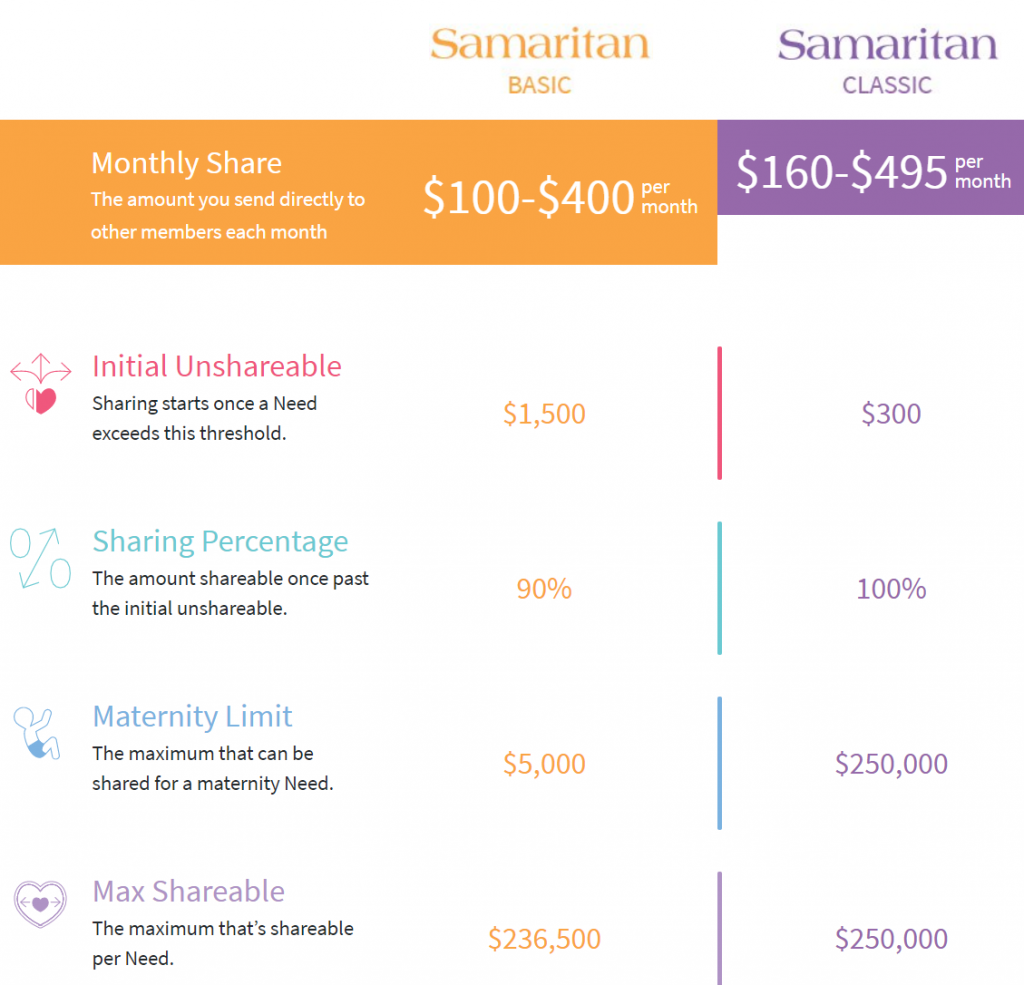

Samaritan has two options to choose from, Basic and Classic, with prices varying depending on whether the member is single, married, or a family, with limits as shown below. The pricing for the Basic option is further adjusted by age. Similar to CHM, members can reduce or eliminate their ‘personal responsibility’ for eligible medical bills by obtaining discounts.

Out of the box, there is a maximum shareable limit per need (similar to CHM’s definition of an ‘incident’, Samaritan defines a ‘need’ as “an illness or injury resulting in visits to medical doctors, emergency rooms, testing facilities, or hospitals” – which means something like maternity is a single need) of either $236,500 or $250,000.

However, there is an optional "Save to Share" program members can enroll in for an additional $150 to $415 per year, which can help with medical expenses over $250,000 (there is no maximum limit with Save to Share, although exceedingly large bills which are more than 50% of the total amount in the Save to Share program theoretically may not be fully shared – since 1994, their largest single bill under Save to Share was $3.5 million which was discounted to under $2 million and then fully shared. Reportedly, there is currently about $20 million in Save to Share, which means in the unlikely event a bill over $10 million was received, full sharing may not be available). Notably, members merely promise to set aside this money in a personal account – it is not sent to Samaritan (although Samaritan keeps a record of how much should be there so it can call up to that amount when needed).

Samaritan’s Basic plan covers only 90% of eligible expenses, effectively leaving the individual participant with a 10% co-insurance obligation. The maximum out of pocket for this plan is $15,000 ($1,500 personal responsibility + 10% share of the first $135,000). Additionally, the basic plan only shares up to $5,000 in eligible maternity costs.

Healthcare Sharing Programs Comparison Summary:

Below is a table which summarizes some of the salient data points (and differences) of each program. (For a larger PDF version of the table below, click here.)

Because the various benefits and limitations may be more relevant for some individuals and less for others (depending on their personal circumstances), there is not any one program that can be called a ‘clear winner’ above the others. For anyone interested in joining, I’d highly recommend reading the guidelines thoroughly – and more than once.

Nonetheless, some notable observations and additional differentiators include:

- CHM has demonstrated significant pricing stability, having gone a decade without increasing prices. Aside from minor areas like excluding ambulance expenses, I did not see any glaring instance of a major coverage they lack when comparing to the other programs.

- Liberty is more inclusive as it pertains to membership eligibility. They also put a high emphasis on ongoing health maintenance, which is reflected in the inclusion of free annual wellness exams and in the health coach program.

- Medi-Share has great pricing, and handles bill negotiation for members, but is the only program discussed with in-network restrictions. For those in large cities, this is probably fine and members may enjoy not having to negotiate their own bills. But some small towns or rural areas may have few in-network options (which may or may not be fully offset by the inclusion of the free telemedicine service). Members also automatically receive a savings card for dental, vision, and prescriptions.

- Samaritan generally seems to have less ‘quirks’ than the other programs, with broader coverage in some areas (such as naturopathic or chiropractic care). Sending checks directly to other members may be appealing to some people more than others, though.

The Fine Print on Healthcare Sharing Programs

At this point, you may be thinking "wow that all sounds pretty reasonable and very affordable". Maybe you like the way these programs allow for greater control over personal health decisions, or are drawn by the pricing for clients struggling to afford traditional health insurance premiums.

But these programs are not without their catches and disclaimers. Here's a list (not all-encompassing) of some types of people who may not want to enroll, or situations that should cause some to think twice before enrolling:

- People with pre-existing conditions. The terms around and definitions of pre-existing conditions vary with each program. In general, there is some time limit applied, and sharing around subsequent events related to the condition are either not shared, or shared at a lower level. Medi-Share does not decline membership due to pre-existing conditions (nor do the others). However, there are limitations on sharing for bills related to any pre-existing condition, which is defined as “signs/symptoms, diagnosis, treatment or medication for a condition prior to membership”. Sharing for pre-existing conditions is as follows:

- For a pre-existing condition that has gone 36 consecutive months without signs, symptoms, treatment, or medication (or if the member has been faithfully sharing for 36 consecutive months), sharing is eligible for up to $100,000 per year (even if the patient has only been a member for a few months they would have access to the $100,000 – it’s the time from last symptom/treatment that counts). But no sharing would be eligible for a condition that has occurred within the previous 36 months until 36 consecutive symptom-free months have passed or until the member has been faithfully sharing for 36 consecutive months.

- Once a pre-existing condition has gone 60 months without signs, symptoms, treatment, or medication (or if the member has been faithfully sharing for 60 consecutive months), sharing is eligible for $500,000 per year going forward.

- Therefore, there are no instances with Medi-Share where a pre-existing condition is treated as though it had never occurred. The most a member will ever be able to have shared for a pre-existing condition is $500,000 per year for as long as they are a member.

Samaritan distinguishes between 'cured' pre-existing conditions and ones that are merely 'stabilized'. If a medical issue was cured and has not had symptoms, treatment, or medication of any kind in the last 12 months, the issue would be eligible for sharing in the future if it re-appears (just as if had never occurred before). If a condition has been 'stabilized' for five years (defined in detail in the guidelines), it can be eligible for sharing, as well.

CHM only allows sharing related to pre-existing conditions under its Gold option, and there is a tiered schedule where expenses related to that condition would be shared, but only at lower amounts until after the third year (at which point, the condition is no longer considered pre-existing). Most conditions are not considered pre-existing if more than one year has gone by without signs, symptoms, or treatment. For cancer, this extends to five years.

Liberty does a 36 month look back as part of the application process, and anything found to have presented signs, symptoms or treatment in that period, is a pre-existing condition, and sharing for any such condition would be prohibited in the first year of membership. Sharing in years two and three is limited to $50,000 per year and afterward (years four and beyond) the condition is no longer considered pre-existing.

Some of the programs even have language in the guidelines saying a change between plans (within an existing healthcare sharing program) could result in conditions being considered 'pre-existing', even if the condition originally occurred while a person was already a member. This is meant to prevent someone from waiting until a condition is discovered and then trying to get on an 'unlimited' or higher cap plan.

- People who use tobacco or other drugs, or have a habit of drinking and driving. These can all result in otherwise eligible expenses being rejected for sharing. Tobacco use is prohibited across the board in all healthcare sharing programs. In addition, recreational marijuana use (even in legalized states) would not be consistent with program guidelines (at least as long as marijuana use is not Federally legal).

- People who participate in ‘hazardous’ activities. Each program is different about what exactly constitutes “hazardous” though. With Medi-Share, you might want to think twice about riding motorcycles. No helmet = no sharing. Even with a helmet, medical expenses which result from a motorcycle accident are capped at $100,000 and limited to a 12-month period after the accident. Samaritan is fine with motorcycles, quads, go-karts, etc., but will not share any expenses related to accidents involving three-wheel ATVs or any expenses for other on-road or off-road vehicles if the accident was the result of reckless behavior, alcohol, or drugs. And be sure to wear a helmet! Liberty has the most robust section in its guidelines on hazardous activities, going so far as to leave the classification of a ‘hazardous’ activity as open to their interpretation and potentially not eligible for sharing at all. Examples of hazardous activities “include, but not are limited to, rock/cliff climbing, spelunking, skydiving, or bungee jumping.” CHM is the most lenient in this area, only requiring that safety gear such as helmets be worn when riding ATVs, motorcycles, etc. Their guidelines do not specifically reference hazardous activities which would not be shared.

- People who receive some other Federal or state assistance. Each healthcare sharing program has at least some caveats with respect to being a ‘secondary’ payment source for those also eligible for Federal or state assistance.

For example, my interpretation of CHM guidelines is that members are required to pursue any available governmental assistance like Medicaid. Liberty has similar language. Samaritan, however, explicitly states in their guidelines that although sharing is secondary to other eligible sources (like Medicare, Workers Comp, or other insurance), “seeking assistance from government aid programs is never required.”

Medi-Share’s guidelines state “members may qualify for public assistance or private benevolence programs. Those who use programs such as these will receive an incentive in the form of a share credit.” They also make it clear that eligible sharing is secondary to alternative sources such as Workers Comp and Fraternal benefits.

- Anyone planning to adopt children with medical conditions will want to think very carefully before joining a healthcare sharing program. Even though some of the programs will actually help pay for adoption costs, the adopted children are subject to "the same eligibility requirements as other new members" – which means adopted children who have pre-existing conditions will still be subject to the pre-existing conditions clause. This is one example where the practical constraints of the programs may be in opposition to the stated mission. Right or wrong, the presumption of the programs is that people who choose to adopt children with pre-existing conditions (thank you to everyone who does this – you are a saint!) can obtain traditional insurance or other forms of assistance for those children.

- People who require ongoing expensive prescriptions. Each healthcare sharing program has its own prescription drug policies, but generally prescriptions are only shared related to a specific medical need, and only for a short duration. Such prescriptions would generally fall under the same per-incident limits or personal responsibility, AHP, or AUA, as applicable (the labels vary among each program). Maintenance prescriptions are not eligible for sharing at all. Members are encouraged to participate in prescription discount programs such as NeedyMeds, GoodRx, OneRX, and LowestMed. Medi-Share, for example, allows sharing of prescriptions related to an eligible incident/illness for only 6 months with "some exceptions for cancer and transplant recipients". Samaritan covers 120 days, with similar exceptions. This means that someone who developed a condition like Type I Diabetes after becoming a Member would only have insulin considered a shareable expense for a very short duration.

- People who want to "be sure" their medical bills will be paid if and when they are incurred. While all of the healthcare sharing programs have strong histories of success, there is no guarantee of payment because, remember, these are voluntary programs and not an actual contract for health insurance benefits. In fact, each group makes it abundantly clear they are not insurance and membership is not a contract. Typical disclaimers read …

The organization facilitating the sharing of medical expenses is not an insurance company and the ministry’s guidelines and plan of operation are not an insurance policy. Whether anyone chooses to assist you with your medical bills will be completely voluntary because participants are not compelled by law to contribute toward your medical bills. Therefore, participation in the ministry or a subscription to any of its documents should not be considered to be insurance. Regardless of whether you receive any payment for medical expenses or whether this ministry continues to operate, you are always personally responsible for the payment of your own medical bills.

Ultimately, members are placing a great amount of faith in these programs, which do not receive the state regulatory oversight and protection afforded to traditional insurance. That said, to-date these programs appear to have adhered to their guidelines and shared billions of dollars of eligible medical expenses. There are certainly some articles on the internet which paint a less than glamorous picture in some cases. But, to be fair, there are a lot of success stories, as well. The success of healthcare sharing depends on upholding and dutifully administering the member guidelines – on the whole, they seem to have done this so far.

It should also be noted that healthcare sharing groups do not carry reserves as traditional insurance companies would. This is because funds are not truly pooled, but merely ‘shared’. Additionally, actuaries are not used – monthly shares are based on experience and set at levels which meet member sharing needs, thus making them susceptible to under or oversharing from time to time. Each program has different policies to manage this process. For example, Samaritan has a proration policy where if less than 100% of the need is met in a given month, they prorate that across all members with needs and then make up the difference in the following month(s) – the reverse also applies (sometimes there’s less need and so members don’t share as much). In months where there was a shortfall, the need has historically been met the next month through needs balancing and/or special gifts. After three consecutive months of shortfall, there would be a mandatory vote to raise the monthly share amount.

Liberty and Medi-Share are a little different, in that money can accrue in the separate accounts in lower need months so that it is available in higher need months. Readers might be interested to learn Liberty has not increased rates since they rebranded in 2014 and, actually, rates have gone down.

CHM is considerably different in that monthly shares are actually sent to a central account at CHM. I asked about their policies and procedures to ensure that funds are only used for their intended purpose and received an impressively long (entire page) list of bullet points describing the many safety protocols they have in place – including external audits, voluntary SOX compliance, and extensive checks and balances on check writing. Their 2016 financials show a cash position of $57 million with shares and gifts totaling $220 million and member medical needs payments totaling $175 million. Total expenses were $190 million, which indicates that the organization operates with a high level of administrative efficiency (less than 10% of member shares). If we assume all cash is available to pay member expenses, this implies roughly four months of reserves on hand (at least as of the date of the statements) – of course, I was reminded that while insurance companies keep reserves, CHM does not. As previously mentioned, CHM has not raised their price for 10 years – and the last time they raised prices it was only $15 per month (i.e. a Gold plan unit went from $135 to $150). Purportedly, they have never in their 37-year history run into a scenario where funds were not sufficient to meet members’ medical needs.

- People who have less than monogamous relationships. Medical expenses related to maternity and STDs which result from extramarital activities are not eligible for sharing in most of the programs (although I'm not sure how they would know!). Even a teen pregnancy or STD treatment may not be covered.

- People who want to keep funding their Health Savings Accounts. As of the time of this writing, healthcare sharing programs do not satisfy the requirement to have a High Deductible Health Plan in order to be eligible for contributions to an HSA. Of course, if you already had an HSA, you can keep withdrawing from it for medical expenses at your discretion – including to cover the personal responsibility out-of-pocket amounts under a healthcare sharing program, though no further contributions to the HSA will be permitted.

However, there is legislation in the works that could allow HSA use with healthcare sharing programs: S. 403 - Health Savings Act of 2017, which would be a great leap forward for members. The applicable text simply reads: "For purposes of this section, membership in a healthcare sharing ministry (as defined in section 5000A(d)(2)(B)(ii)) shall be treated as coverage under an HSA-qualified health plan." You can read the full text here.

- Individuals who enjoy taking the deduction for their health insurance premiums. As these programs are not insurance, the 'premiums' are not deductible. Consequently, self-employed individuals cannot claim the above-the-line deduction for health insurance premiums, nor can other individuals count the monthly share amount “premiums” as medical expense itemized deductions.

- People who appreciate the "free" annual wellness exams the law currently requires insurance companies to provide. Of course, the reality is the cost of wellness visits are built into standard insurance premiums, and are not truly “free”. But the cost of an annual wellness visit, especially when labs for bloodwork are included, is not trivial, and many people prefer to have the cost bundled into their premiums so the visit itself has no cost at the time. Currently, only LHS covers annual wellness exams without an out of pocket cost (up to $400).

Beyond these caveats, there are certainly some other quirks – one example is that ambulance transportation is not eligible for sharing with CHM, even when it could be deemed medically necessary (except for between hospitals if necessary to receive adequate care). In addition, all the programs deny coverage for self-inflicted injuries, although some do cover this for children under a certain age.

At this point, I'll refer you to the member guidelines if you want to learn more about the possible exclusions for specific healthcare sharing programs. Hopefully you see the importance of reading the Guidelines in excruciating detail before enrolling!

Other Considerations And Risks

As we can see, there is plenty to like with healthcare sharing programs, while at the same time there are numerous potential coverage gaps and possible surprises for people who may not have fully read and comprehended the program guidelines. Whereas at least with health insurance, coverage is more standardized and consistent, especially given the Affordable Care Act’s “essential health benefits” requirements.

However, while healthcare is a highly politicized topic right now, few would argue that health insurance premiums aren’t getting out of hand. As Mr. Money Mustache noted in a recent article (warning, strong language ahead if you read it), there will be a point where more people will say enough is enough and stop paying for insurance because the pricing is no longer an accurate representation of their risk of incurring a catastrophic medical bill. In the meantime, many healthy people are finding they have another option to insurance – healthcare sharing programs – that comes with a very enticing price tag.

And Medi-Share and Liberty actually operate somewhat closely to traditional insurance, though the others have taken a very different approach. Still, there is much to be said for empowering individual consumers to shop around, compare prices, and be responsible for their own care. I would argue that the low pricing of these programs is, at least in part, a result of members having greater responsibility and taking the time to ‘shop around’ – for an example, understanding that MRI prices can greatly vary between two nearby locations. Although premium savings is also likely facilitated by the fact that the programs’ limitations screen out a lot of unhealthy lifestyles, including all tobacco users, which means those who can and do qualify are likely already healthier than the “average” person covered by health insurance.

In fact, it would seem that what's happening is these programs, which were grandfathered into the ACA, is that generally healthy people who are currently subsidizing higher-risk individuals in traditional insurance plans are instead joining a lower cost pool of like-minded folks. I have to wonder if at some point this movement of lower-risk people out of the general population risk pool for traditional health insurance is going to draw unwanted political attention. It is certainly a possibility, however unlikely, that Congress could disallow these programs altogether, and force participants back into traditional health insurance – what the lawman giveth, the lawman can taketh away. Although at least if they are forced back into traditional health insurance, the loss of healthcare sharing programs will not mean a total loss of coverage.

As it stands, members of these programs realize they can return to the traditional insurance realm if they encounter something that isn't covered (at least during an eligible open enrollment period, and as long as the law continues to require insurers to accept those with pre-existing conditions). Which also means another future possibility is Congress might make it more difficult to return to traditional insurance once someone opts into a health sharing program. This would certainly make people think twice about the lack of a guarantee and test their 'faith' in these programs. Although at the same time, many members appreciate knowing the funds they pay every month in a healthcare sharing program are not paying for services they find morally objectionable, and thus would choose to stay anyway.

Another risk to consider is what may happen if meaningful healthcare reform actually occurs (and let us hope it does!). If health insurance costs declined to more affordable levels (though probably not happening anytime soon?), it's not inconceivable there could be some migration out of the healthcare sharing programs. It's difficult to forecast to what extent this may occur and, if it did, how it would impact the sustainability of the programs. But without a doubt, healthcare sharing programs are easier to administer – and maintain costs – when new healthy individuals are regularly joining, as has been happening in the years since ACA was implemented.

Impact Of Eliminating The Individual Mandate

I’m not in the habit of making predictions, but writing this article and the recent tax reform which eliminates the ACA’s individual mandate effective in 2019 has me thinking a lot about the problems in healthcare, and the likely direction things may take. My expectation is that, without significant healthcare reform, insurance costs will most likely continue their upward trajectory.

With no penalty for not having insurance beginning 2019, more people are going to stop paying for it, thus increasing the cost for those who stay in (perhaps by necessity due to poor health). As this happens with greater frequency, I foresee healthcare providers, at least at the general/family practice level, responding with new business models catering to self-pay customers featuring transparent and competitive pricing – or even monthly memberships with ‘unlimited access’.

In such a world, low cost catastrophic-only private insurance, along with healthcare sharing programs, could then fill the void between routine care and coverage for major events like cancer, while we wait for further reform. In other words, a shift to more cash payers outside the traditional insurance system would likely be a continued boon to the growth of healthcare sharing programs.

In essence, until the medical industry in the United States is comprehensively reformed, it seems that membership in healthcare sharing programs is likely to continue growing at a solid clip.

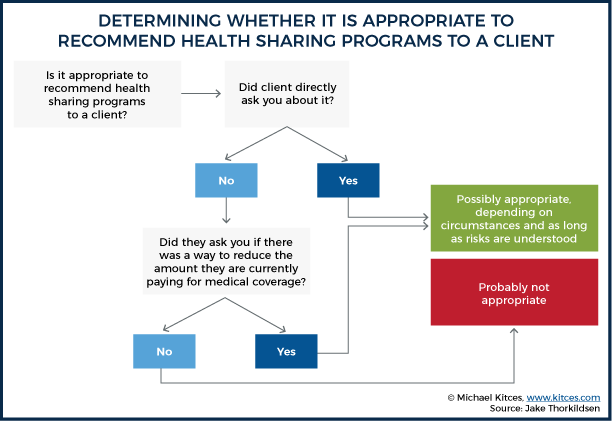

How Should Advisors Approach Healthcare Sharing Programs With Clients?

With an understanding of what these programs are, how they work, and some of the risks they face, the issue for financial planners becomes how they ought to discuss this option for handling healthcare costs with clients.

On one hand, there is considerable risk in joining these programs. It’s not like we are talking about insuring a boat here – this is about the cost of healthcare, and people do get hurt, become sick, or get cancer, for which the costs can be enormous. It’s a BIG deal! What if, as an example of a worst-case scenario, a client had a teenage daughter who became pregnant and the baby needed care in the NICU? If the family was under a health sharing program like CHM, Medi-Share, or Samaritan, which found the expense to be ineligible, this could quite easily result in severe financial hardship unless the family was able to obtain other assistance. There’s also the religious aspect of the programs to which some may object. It is easy to see how this can be a prickly issue for many in the profession.

On the other hand, the cash savings of monthly share amounts, versus traditional health insurance premiums, can be significant, and go a long way in helping people meet their financial goals (or to simply be covered when they might not even be able to afford traditional coverage). There are many people for whom these healthcare sharing options are working very well. Their needs are covered, and they are saving hundreds of dollars (or more) every month. My family was saving more than $1,000 per month compared to our traditional insurance options available when we joined a program, and we benefited from a lower ‘deductible’, as well. When we had our daughter, our experience with the sharing process far exceeded my expectations. As we all know, the ability to save several hundred dollars or more every month can make a huge difference in one’s financial plan and overall financial position. For that reason alone, these programs are worth understanding and may have merit for certain clients.

According to NCSL (National Conference of State Legislators), annual premiums for average family insurance coverage reached $18,764 for 2017 ($1,564/month). NCSL found the average worker contributes $5,714 annually ($476/month) towards the cost of their coverage. Compare these stats to healthcare sharing programs, which can have family coverage at $300 to $500 per month, and may have much lower ‘deductibles’, too. So for those who work for employers which don’t heavily subsidize coverage, the self-employed, or individuals who aren’t able to obtain government premium assistance tax credit subsidies, there is tremendous savings potential with healthcare sharing programs.

Financial planners should remember that their job is not to make decisions for clients in a paternalistic fashion – but rather to educate, lay out the available options, and help clients understand the risks so they can make an informed decision. This notwithstanding, clients place an enormous amount of trust in their financial advisor. Which is why it’s concerning that some financial planners reportedly are outright rejecting the idea of these programs. Whatever the reason may be – whether ideological differences or lack of knowledge – this does a disservice to interested clients.

So, should planners recommend that clients enroll in these programs? As usual, the answer is – it depends! As we’ve discussed, the aforementioned savings come with additional and unique risks. Like so many other financial tools, one must evaluate the risk against the return or benefit being offered. I decided to go for it with my family but, personally, I would definitely not recommend this to everyone. Aside from eligibility, the decision for an individual to enroll will come down to price, moral appeal, and acceptance of the various coverage gaps and risks.

Let’s look at some examples. When doing a cash flow analysis, I am not inclined to think a planner should look at the amount someone is paying for health insurance and suggest out of the blue they can reduce it by joining a healthcare sharing program, even if those savings would be significant. If they were highly confident a client’s faith/value system aligned, then maybe there are some cases where it could be brought up. At the risk of sounding hypocritical (since I have participated in a health sharing program!), as a rule of thumb, I don’t think it’s appropriate to bring up this subject in this type of situation.

After all, it’s one thing to recommend an investment or compare different insurance plans, but it’s another to recommend someone discontinue health insurance altogether and venture into the realm of unregulated healthcare sharing programs. I’m not ashamed of my own participation in a healthcare sharing program, but I think these programs may have more risk and coverage gaps than many people are probably aware, and even with awareness it’s not always easy to judge the risks. Being willing to accept those risks is a very personal decision – much more so than other investment other insurance choices. Financial planners take on many responsibilities, but a decision of this magnitude is not one of them. So for these reasons, I think planners should be hesitant to say to a client out of the blue – “Hey client, I really think you could benefit from a healthcare sharing program – it looks like you could save hundreds per month, and I suggest that you sign up as soon as possible.”

However, what if a client directly asked about this topic? Or came to their planner frustrated with another year of huge insurance premium increases and asked if there is ANYTHING that could lower the amount they pay? In these cases, I believe it is appropriate for a financial planner to provide some information and explain how it works (basically a summary of everything written in this article). These instances, which are occurring with greater frequency, are exactly when advisors should know about the programs. Their client is asking directly about it, and healthcare sharing could truly help meet their need.

Any client who is considering a healthcare sharing program should be strongly reminded (multiple times!) that these programs are not insurance, and go over what this really means. Talk about the risks involved, and then it is up to the client to thoroughly read the program guidelines and make a choice as to whether or not they are comfortable with it. There is no free lunch, and there is definitely a reason for the savings (including that they aren’t covering a lot of expenses which insurance companies are required by law to cover). If clients are ok with this, then… great! A planner has done their job in informing them and the client decided it was best to move forward.

What’s not acceptable, in my opinion, is a client who shares the value system of these programs coming to an advisor and the advisor telling them the program is awful, shady, etc… To do so, you have to ignore a lot of evidence to the contrary – a million people (and counting) and decades of successful operations with billions of dollars in expense sharing are not something to write-off without due consideration. But again, I also think it’s generally not appropriate for a financial planner to recommend membership in one of these programs without some prompting or expression of interest initiated by the client.

To summarize, I’ve put together one of those fun flowcharts:

We’ve only scratched the surface here, but my hope is this information will prove useful to you as clients approach you for advice on this nuanced subject – or if you just happened to come across this article because you are researching healthcare sharing options. I’ve found that all the programs are easily reachable and happy to answer questions. As non-profits, they are not trying to maintain a certain margin or worried about their stock price – they exist to help their members share medical expenses within the parameters of the program guidelines.

One last point which I did not address in this post – some of the programs also offer group coverage for churches and businesses. This is a more complex matter, and those interested are encouraged to contact the programs to learn more.

If you’d like to do a little more digging, here are links to each website where you can find their guidelines and learn more:

- Christian Healthcare Ministries: http://www.chministries.org

- Liberty HealthShare: https://www.libertyhealthshare.org/

- Medi-Share: https://www.mychristiancare.org/

- Samaritan: https://www.samaritanministries.org

- Though I’ve written about the four largest programs, there are actually several other programs (some newer) which include:

-

- Solidarity HealthShare, which markets specifically to Catholics. https://www.solidarityhealthshare.org/

- Christ Medicus Foundation (CMF CURO) which is operated under Samaritan and specifically for Catholics: https://cmfcuro.com/

- Altrua HealthShare which, like Medi-Share, participates in the PHCS PPO network. Their website indicates this program may be more inclusive than Liberty. https://altruahealthshare.org/

- Medical Cost Sharing, Inc. This program appears to include Rx benefits and a ‘Vanishing Personal Responsibility’ (i.e. declining deductible). There is an interesting comparison chart on their website - http://www.medicalcostsharing.com

Cheers!

So what do you think? Have you had clients ask you about healthcare sharing programs? Would you ever recommend a healthcare sharing program to a client? When is it appropriate for an advisor to recommend healthcare sharing programs? Please share your thoughts in the comments below!

I am glad to read your amazing blog and your given information is useful for everyone. Thanks for sharing your knowledge with us!

Thanks for the comprehensive article.

My family joined HIPNATION, a concierge medical practice based on 5 states (we’re in Georgia) that charges $100/month per person for unlimited medical care by a PCP, with no further co-pays. It’s not for hospital care and not for specialists, although they have a bunch of affiliate specialists with whom they’ve negotiated cash deals. HipNation is part of a growing trend of direct-pay concierge medical practices that promise to provide more traditional, in depth medical care that you just don’t find with major HMOs like Kaiser and Blue Cross. They cap the number of patients and do not shuffle you off to specialists when you have a wart or a stuff nose.

HipNation recommends signing up for a the share ministries described in this article OR signing up with an indemnity program. We signed up with Sedera Health, one of the smaller non-Christian health shares. We are paying $450 / month (with a $5000 per incident deductible) for the three of us; compared to the $2800 / month offered by the government Health Exchange (Kaiser), it’s very reasonable. There’s lots of other options popping up, so it pays to shop around.

On a somewhat political note, it is interesting to observe that the two areas that have had the most government intervention — healthcare and education – have experienced far and away the most cost increases, along with abysmal outcomes. The free market, as exemplified by these health shares (they are far less regulated than the insurance industry), provides price transparency and real efficiency and innovation.

Would like to see an indepth review of newbies SideCar and Knew health insurance. thanks

Thanks for your valuable suggestions, I glad to inform you that I have decided to take your advice and implement it.

Affordable life USA

Of course, Evan. This is really amazing post.

yes Thank you for you feedback.

Do these substitute for Medicare Supplement Plans? would one be penalized should they choose to go back onto Medicare Supplement?

This article is a little dated, but seems to give a good overview of how each handles a little differently… https://soundmindinvesting.com/articles/view/healthcare-sharing-ministries-and-medicare

Solid comparison of the different CHSMs. My family and I have been happy Medi-Share members for years now and I agree that it’s probably the option most similar to traditional insurance in terms of how it works.

One small change that people may want to be aware of is that the AHP options have changed recently. They now range from $500 to $10,500 and the monthly share amount also depends now on where you’re located within the US. A more detailed look at the current prices is: https://www.medisharereviews.com/price-comparison.html

I’ll be sharing this article with those looking for a detailed comparison of their Christian healthcare sharing options, thanks for posting it.

Ive had Liberty Healrhshare for almost 3 years. The monthly is about 350 for my wife and I. The annual share went from 1000 to 1750 in this time. My wife and I are healthy. No smoking, no drinking, no hazardous lifestyle. I did however require emergency services a couple times which resulted in minor, non life threatening incidents. I have been bombarded with calls and emails from doctors, hospitals, and collection companies continuously! Eventually, maybe in

5-6 months and following much effort on my part (phone calls, faxes,

emails, waiting on hold) they will get paid. They apparently have attorneys they use to help clear up your credit report. Good thing for that! You are instructed not to pay during their negotiations eventhough you may go to collections. Your medical team will know you because of the coverage you have!

This is NOT your typical insurance! Be prepared to be frustrated!

The rates are pretty good compared to insurance companies but the hassle makes you wonder if its worth it! The people are very nice and understanding but are at the mercy of their processing dept which no one can talk to. We cannot afford any insurance company so we are left with shopping health share companies this year! Hopefully, we can find one that is capable of honoring their financial obligation in a more timely and reasonable time!

There is another option for cost-sharing that is not based off religion: Knew Health! I’ve been a member since August 2019 & so far so good. Their staff has been really helpful in answering my questions & explaining their services (what is/isn’t shared). They also offer discounts for labs, supplements, free health coaching & free telemedicine. They didn’t require a letter from a church & no recent health physical either. Oh & no hidden fees!!! All of these christian costshare groups charge you extra $$ for processing plus a lot more $ if you don’t fit into their BMI so you are required to use their health coach + pay about a hundred bucks each month. http://www.KnewHealth.com

I want to know if my employer is allowed to deny me the ability to use a cost sharing program, instead of the insurance they provide? Because as of now, that is what they are telling me is that I can’t use “cost sharing”.

Really need more information to help, Andrew. Was it a condition of employment? Are you under a union? etc. Generally-speaking, you should have option to decline insurance coverage – especially if you are paying towards it. But by the same token, employer is generally under no obligation to direct funds they would have spent toward insurance for you to a cost sharing program you choose.

These sharing schemes are the way forward if your not bound by law. https://www.helpfulhealthinsurance.com

Wow! This Is Good Post Thank You….https://curable.care/online-appointment-in-coimbatore

Hi, I would say this is an amazing article on health plans. You’ve covered everything that everyone is love to read. Please add me to your subscriber list so if next time you publish an article I would get notify of it.

Securepharmacare is the Best place to Buy oxycodone Online and to also buy other medicines online with overnight delivery. This medication is utilized to help assuage moderate to extreme agony

buy oxycodone acetaminophen 10-325 en español

Excellent blog. This is very informative; thank you for sharing. Very useful and helpful; I hope I can get a chance to see this. I also want to share that Aynjil is innovative cancer insurance that supports patients through every stage of the recovery process.

<a href=" https://wyldcbngummies.com/ " rel=“dofollow”>get wyld gummies</a>

<a href=" https://wyldcbngummies.com/ " rel=“dofollow”>order wyld gummies online</a>

<a href=" https://wyldcbngummies.com/ " rel=“dofollow”>real fruit thc gummies</a>

<a href=" https://wyldcbngummies.com/ " rel=“dofollow”>thc gummies</a>

<a href=" https://wholemeltsshop.com/ " rel=“dofollow”>How to Dab Whole Melt Extract for Maximum Flavor and Effect

</a>

<a href=" https://wholemeltsshop.com/ " rel=“dofollow”>Whole Melt vs Live Rosin</a>

<a href=" https://wholemeltsshop.com/ " rel=“dofollow”>Top 6-Star Whole Melt Extract Strains You Need to Try

</a>

<a href=" https://wholemeltsshop.com/ " rel=“dofollow”>How Whole Melt Extract Is Made</a>

<a href=" https://wholemeltsshop.com/ " rel=“dofollow”>Where to Buy Verified Whole Melt Extract Online in the USA

</a>

<a href=" https://wholemeltsshop.com/ " rel=“dofollow”>Whole Melt for Medical Use</a>