Executive Summary

In theory, the whole point of having a “product illustration” is to show how the product is anticipated to work… whether it’s a mechanical device, or an intangible like a life insurance policy. Except the caveat is that, ironically, intangible assets like life insurance policies sometimes have even more “moving parts” than a mechanical device, making it remarkably difficult to understand how it actually works. Or even to determine the underlying “mechanical” assumptions that are driving the outcomes of the illustration in the first place.

In this guest post, life insurance expert Barry Flagg, founder of Veralytic (a company that produces life insurance due diligence tools), highlights the challenges of effectively identifying and understanding the moving parts in a typical life insurance policy illustration. Which over the years have become so problematic, that recently issued regulations from the New York Department of Financial Services (NY DFS Regulation 187) have suggested that life insurance illustrations should no longer be permitted as a means to compare life insurance policies… because, in essence, they’re too vague and uncertain for fiduciaries to actually rely upon!

For instance, while the core of any life insurance policy (or any other) illustration is its projected earnings or growth, after being reduced by its projected Cost Of Insurance (COI) charges and other expenses, the reality is that not all life insurance companies illustrate these costs and expected returns in the same manner. For instance, sometimes COI charges are “pure” and include only the raw Cost Of Insurance expenses, but in other times COIs are “loaded” with distribution or other costs. Certain “premium loads” may apply charges based on the premiums paid, but use an underlying “target premium” calculation to determine those charges, rather than uniformly applying them to all premiums. And while life insurance policies do typically get projected at a specified rate of return, insurance companies can and sometimes do add additional – but not necessarily guaranteed – return assumptions on top, which means even insurance policies with the same projected return input are not necessarily being projected at the same rate of return!

The challenge of these dynamics in life insurance policy illustrations is not only that it’s sometimes difficult to call what costs are or are not being included, and what the “real” projected rate of return is, but that the potential to not have results that align with (non-guaranteed) assumptions means that two otherwise-identical life insurance policy illustrations may have a substantively different level of risk about whether the assumptions will actually be fulfilled. A risk that, itself, is not typically reflected in a life insurance policy illustration.

As a result, the reality is that “best practices” in doing due diligence on a life insurance policy illustration entails far more than just looking at the illustration to see which policy is projected to maintain the death benefit the longest, or accumulate the highest (not-necessarily-guaranteed-or-even-likely) cash flow. Instead, effective due diligence for life insurance policies must dig deeper, or use third-party support tools, to truly understand the costs and risks underlying the projected opportunity.

Comparing hypothetical illustrations as supposed due diligence or product recommendations never made sense to me. I grew up in the financial services business – literally. I’m the son of an actuary and Certified Financial Planner™, started my career as an analyst in the Pension Investment Advisory department of his financial planning practice while still in college, and became the youngest CFP® in the history of the College for Financial Planning. My first job involved providing the partners in the firm with due diligence on mutual funds to document that product recommendations were in the client’s best interest.

I used Morningstar to research and document that costs were justified and performance expectations were reasonable. When I graduated from college, I took a position in a life insurance agency to diversify my experience and build my resume. That experience – where due diligence for product recommendations didn’t consider costs, performance, or risk, and instead consisted of comparing illustrations of hypothetical values for some limited number of products – could not have been more different than my earlier experience in a fiduciary environment.

So I spent the next/last 30 years searching for and/or developing tools and techniques for analyzing internal policy costs and evaluating the reasonableness of performance expectations based on my experience with same analysis on other financial products. Along the way, I invented and founded Veralytic Research as a tool for fiduciary-oriented advisors to measure the competitiveness of internal policy costs and the reasonableness of performance expectations (among other things) against the universe of peer-group alternatives as follows.

Understanding Life Insurance Cost Competitiveness

The pricing and performance of all cash value life insurance products is a function of just a few factors, namely:

- Cost of insurance charges (COI) for death benefit claims

- Policy Expenses (E) for policy design, underwriting, distribution and administration

- Investment gains and/or interest income (i%) credited to policy cash values in excess of COIs and E

In other words, premiums are always based on the following formula in minimum‑premium defined‑death‑benefit policy designs, and policy performance is always based on the following formula in maximum‑accumulation defined‑contribution policy designs:

| Premiums/Performance | = | Cost‑of‑Insurance Charges (COI) |

+ | Policy Expenses (E) |

- | Policy Interest/Earnings (i%) |

This simple formula can, therefore, be used to evaluate the pricing of either proposed coverages, and/or in-force policies, by first separating policy costs into either cost of insurance charges (COIs), and policy expenses (E), and then grouping expenses by their nature into the only three ways that insurers calculate and collect policy expenses, namely 1) fixed administration charges (FAEs), 2) cash‑value‑based “wrap fees” (e.g., M&Es), and 3) premium loads.

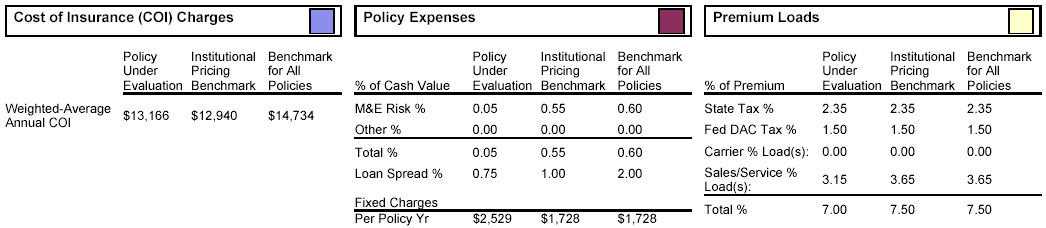

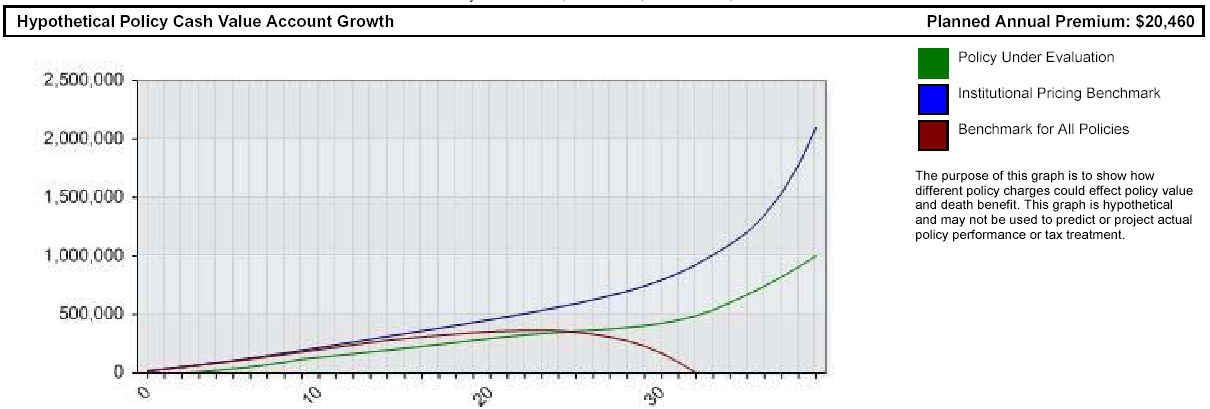

Because these costs vary from year-to-year resulting in hundreds of cost figures that are difficult to evaluate or compare, evaluation and comparison of costs become much more practical when “normalized” to account for differences in amounts and timing of the different charges in different policies. This “normalizing” of varying policy charges computes a single value for each pricing component by adjusting for differences in timing at the rate of interest/earnings at which the policy cash values would otherwise grow, but for the deduction of the given charge(s). These normalized values can then easily be compared with industry benchmarks for each pricing component (see below for example table of “normalized” costs below, courtesy of Veralytic).

The practice of benchmarking is well-established and common in the financial services industry, where the performance of a financial product is frequently compared to a standard, independent point of reference. For instance, to determine the appropriateness of a given mutual fund selection, the performance of that mutual fund is often compared with the Dow Jones Industrial Average, the S&P 500, the NASDAQ, or the Wilshire 5000 depending on the fund’s investment objective.

Likewise, comparing COIs and expenses for a given life insurance product to industry standard mortality tables (e.g., Society of Actuaries 75-80 Basic Select & Ultimate Gender Distinct Mortality Tables at www.soa.org) and industry aggregate expense ratios (see Society of Actuaries Generally Recognized Expense Table for 2001 also at www.soa.org), reveals actual cost competitiveness. This practice of comparing costs to benchmarks is consistent with prevailing practices in most all other segments of the financial services business, is compliant with FINRA Rules, and addresses the requirements of NY DFS Regulation 187.

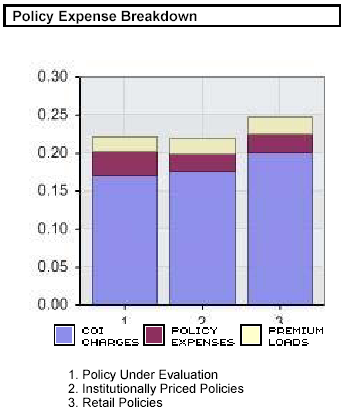

To understand the competitiveness of total costs relative to the universe of peer-group alternatives, “normalized” costs are calculated relative to death benefits (which can fluctuate over time and/or be different between different products), and are again compared to industry benchmarks (See example Policy Expense Breakdown in the graphic below for showing the present value of all policy costs per $1.00 of death benefit over the expected policy holding period, courtesy of Veralytic).

To understand the competitiveness of total costs relative to the universe of peer-group alternatives, “normalized” costs are calculated relative to death benefits (which can fluctuate over time and/or be different between different products), and are again compared to industry benchmarks (See example Policy Expense Breakdown in the graphic below for showing the present value of all policy costs per $1.00 of death benefit over the expected policy holding period, courtesy of Veralytic).

Measuring aggregate costs per $1.00 of death benefit relative to benchmarks also provides insights as to the relative impact and fairness of individual pricing components on overall policy pricing. As shown above, cost of insurance charges (COIs) typically comprise 85% of total costs, whereas fixed administration expenses (FAEs), premium loads, and cash-value-based “wrap fees” (e.g., M&Es) make up 15% of total costs as explained below.

Cost of Insurance Charges (COIs) – Whether disclosed or not, all policy types are priced for expected cost of insurance charges or COIs. COIs are deductions from permanent life insurance policy cash values to cover anticipated payments by the insurer for death claims. As with most types of insurance, claims are, and arguably should be, the largest single cost factor of any insurance policy (If claims are not the largest single cost factor, then is the product really insurance against the risk of death, or something else?). With life insurance, COIs typically account for about 85% of total costs, but can themselves vary by as much as 80% between different insurers and different products (even different products from the same insurer). At the risk of stating the obvious, the higher the COIs, the higher the premiums required to pay higher COIs.

COI charges are calculated year-by-year on the Net-At-Risk policy death benefit (i.e., the NAR, or the difference between the death benefit less policy account cash values that would already be available to pay the death benefit) multiplied times a COI rate provided by the insurance company for each age corresponding to each policy year for each product. Thus, for instance, if the current cash value was $300,000 and the death benefit was $1,000,000, and the COI at the insured’s current age was $5.00 per $1,000, then the COI charge in the current year would be $1,000,000 - $300,000 = $700,000 / $1,000 = 700 x $5.00 = $3,500.

These COI deductions are much like term life insurance premiums, in that they are predominantly for claims paid during a given period (typically 1 year). For this reason, COIs are frequently referred to as the pure "risk" portion of the premium, reimbursing the insurance company for the risk associated with paying the death benefit. And because the risk of death increases with age, so do the COIs over time.

In addition, some insurers "load" the COIs to cover other policy expenses that are not disclosed elsewhere. For instance, some policies are marketed as "no-load" or "low-load" policies, and as such do not disclose certain policy expenses or loads. The expenses or loads that are typically "hidden" are sales loads, and other premium-based loads, which can be appealing for the insurer because it can reduce the appearance of state premium taxes or Federal deferred acquisition costs (DAC) taxes. Or as noted earlier, give them a way to "hide" their distribution costs inside "loaded" COIs to market being a no-load or low-load policy, even though those distribution load costs are really still there (just in another form, as loaded COIs).

Because COIs are calculated on the NAR (i.e., net amount at risk difference between the death benefit less policy account values), and because COIs increase geometrically with age as discussed above, the NAR itself is a significant factor in the determination of COIs. For instance, COIs are minimalized when cash values are nearly equal to the policy death benefit, even at the older ages when COI rates are at their highest. However, because policy cash values are “collected” by the insurer upon death in addition to COIs collected in prior years, cash values in the policy account on death are also a cost of maintaining the death benefit that must be considered.

Fixed Administration Expense (FAE) – FAEs are typically charged for expenses related to actuarial design, underwriting and new business processing, and service and administration, and are calculated as some fixed amount set at the time of policy issued, either as a flat monthly charge (e.g. $10.00 a month), or in relation to the originally issued policy face amount (e.g. $1.00 per $1,000 of policy face amount). While this charge is fixed in amount at the time of policy issued, it can vary from year to year by a predetermined schedule (e.g. $10.00 a month and $1.00 per $1,000 of policy face amount during the first 10 policy years, and $5.00 a month and $0.00 per $1,000 of policy face amount thereafter).

In addition, FAEs can also include contingent or back-end policy surrender charges that are deducted from the policy cash account value upon surrender or cancellation/termination of the policy. These surrender charges are calculated in relation to the initially issued policy face amount and can be as much as 100% or more of the planned annual premium for policy types available to the general public at large (i.e. policies commonly referred to as "Retail Policies"), or can be less or even 0% for policies purchased in larger volumes (i.e. frequently referred to as "Institutionally Priced Policies”) or fee-only-type products. In either case, this surrender charge typically remains level for an initial period of years (e.g. 5 years), then reduces to $0 over a following period of years (e.g. policy years 6 through 10 or 6 through 15).

Premium Loads – Premium loads are calculated as a percent of premiums paid in a given year, and typically range between 0% and 35%. Premium‑based charges customarily cover state premium taxes that average 2.50%, DAC taxes averaging 1.5%, and Sales Loads/Expenses ranging between 0% and 30%. In addition, while state premium taxes and DAC taxes are generally calculated by the respective government agencies as a percent of premium, and while insurance companies must certainly pay these taxes, insurance companies are not required to assess the charge as a percent of premium. As such, some insurance companies charge no (i.e. 0%) premium charges, and collect state and federal taxes from other charges within the policy (usually COIs).

Premium-based charges can also vary depending on either the policy year in which a premium is paid, or the level of the premium paid into a given policy. For instance, a higher premium load may be assessed in the early policy years to recover up-front expenses related to underwriting, issue, and distribution of a given policy. After these up-front expenses have been amortized (frequently over a period of ten policy years), premium loads are then often reduced in recognition of the relatively lower policy owner service and policy administration expenses.

In addition, a higher premium load may be charged on premiums paid up to a "Base Policy Premium" or "Target Premium" level, while a lower premium load may be charged on premiums in excess of the Base/Target Premium amounts. This Base/Target Premium is set by actuaries and is generally calculated using conservative assumptions as the amount necessary to cover COIs and expenses required to maintain life insurance death benefit. As such, this Base/Target Premium can be thought of as the true "insurance premium" (i.e. the premium necessary or likely necessary to be paid to maintain life insurance coverage in an otherwise-flexible-premium policy).

Premium amounts paid into the policy in excess of this Base/Target Premium can, therefore, be viewed as "excess premium" above and beyond that required to cover the costs of maintain the death benefit. "Excess premiums" are typically intended to either create a cash value reserve as “pre‑payment” of what would otherwise be future premiums and/or to grow the policy account for wealth accumulation, retirement planning, and/or asset protection.

As such, premiums paid up to the "insurance premium" are typically subjected to higher "insurance loads" to cover policy expenses unique to the insurance component of the policy, while “excess premiums” are typically subjected to a lower “investment‑like loads” on those monies contributed toward cash values accumulations. In either case, Veralytic Reports calculate the blended premium load for easy comparison to industry benchmarks and/or peer group products.

Cash‑Value‑Based “Wrap Fees” – Cash-value-based “wrap fees” are insurance fees charged as a percent of policy account values (e.g., M&Es found in variable products) similar to Fund Management Fees (FMEs) that are also charged as a percent of assets under management. However, these cash-value-based insurance fees are specific to the policy, separate from and in addition to FME investment fees, can vary over time (e.g. 1.00% of cash values during the first 10 policy years, and 0.5% of cash values thereafter), and/or the amount of the cash value (e.g. 1.00% of cash values up to $25,000, and 0.5% of cash values above $25,000), and in either case typically range from 0% to 100 bps (1.00%).

These cash-value-based insurance fees are specific to each policy, without regard to the underlying general account investment portfolio or mutual‑fund‑like separate account funds, and are therefore a cost that needs to be considered in any analysis of policy costs. On the other hand, investment fees are specific to the respective separate accounts within a policy, and as such are a function of the underlying separate account fund selection, which usually change within the same policy over time with changes in asset allocations of invested assets underlying policy cash values. As such, investment fees are more logically addressed in the evaluation of cash value investment performance (see further discussion of fund-specific investment expenses under Historical Performance section).

Some products disclose cash-value-based insurance expenses in both dollar amount and percentage rate (i.e., when deducted at the policy level), whereas other products disclose cash-value-based insurance expenses only in a percentage rate (i.e., when deducted at the separate account level). For uniformity of cost analysis across all products, “normalization” of policy costs for differences in amounts and timing of charges should use the expected policy interest/earnings rate less the percentage rate of cash-value-based insurance charges (i.e., the rate at which policy cash values would otherwise grow, but for the deduction of the costs).

Evaluating Reasonableness of Life Insurance Performance Expectations

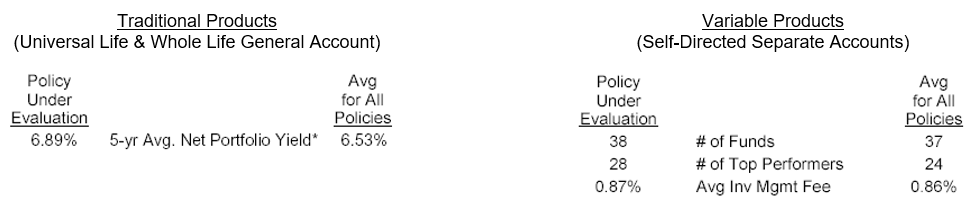

While past performance is no guarantee of future results, measuring past performance against relevant benchmarks is a generally-accepted measure for the reasonableness of performance expectations. The reasonableness of performance expectations is, therefore, generally a function of historical performance of cash value investment options appropriate for acceptable risk, the expense ratios for invested assets underlying policy cash values, and number and diversity of cash value investment options (see Figure 8 for an example of performance expectations factors below, courtesy of Veralytic).

Policy account values in traditional life insurance products are invested in the insurer’s general account managed by the insurer, and required by regulation as a practical matter to invest predominantly in fixed income securities like high-grade corporate bonds and government-backed mortgages. Traditional products include all forms of universal life (i.e., even indexed universal life) and generally do not disclose such investment expenses.

Policy account values in variable products are directed by the policy owner among a family of mutual‑fund‑like separate accounts typically offering a wide range of asset classes including an assortment of domestic and foreign stock funds, an array of domestic and foreign bond funds, a money market account, and usually a fixed account (typically the same as the insurer’s general account).

Also, because neither cash-value-based investment expenses (i.e., Fund Management Expenses or FMEs), cash-value-based insurance expenses (e.g., M&Es), nor life insurance policy earnings, are generally illustrated in a consistent or standardized manner, care is needed in understanding differences between the rate of return shown in illustrations, versus the actual rate of return that is reasonable to expect.

- Gross Rate Of Return – The gross policy interest/earnings rate is that rate of return credited to policy cash values reported before deduction of investment‑related fund management expenses (FMEs) and before deduction of cash-value-based insurance. The gross rate is typically disclosed in variable life products but not typically disclosed in traditional universal life or whole life products. The reporting of the gross policy earnings rate is also somewhat unique to life insurance products as rates of returns for investment products are most often reported net of FMEs.

- Net Rate (Investment Rate Of Return) – The net policy interest/earnings rate is that rate of return credited to policy cash values reported after deduction of investment‑related FMEs, but before deduction of cash-value-based insurance. In other words, this “Net Rate” is equal to the Gross Rate minus FMEs, and as such is most closely analogous to the “investment rate of return” on policy cash values (e.g., universal life policy interest crediting rates and whole life dividend interest crediting rates are generally reported after deduction investment expenses). This “Net Rate” is also consistent with mutual funds reporting of earnings after deduction of related investment expenses (i.e., their FMEs) and is, therefore, most useful in comparing performance outcomes for different life insurance or other financial products.

- Net-Net Rate (Policy Rate Of Return) – The net-net policy interest/earnings rate is that rate of return credited to policy cash values reported after deduction of both investment FMEs and cash-value-based insurance “wrap fees” (e.g., M&Es). In other words, this “Net‑Net Rate” is equal to the Net Rate minus insurance Mortality & Expense (M&E) charges, and because this Net‑Net Rate reflects the rate of return reported on policy cash values after all cash-value-based fees, it can also be referred to as the “policy rate of return” (i.e., the rate of return on policy cash values after deduction of both investment and insurance “wrap fees”). This “Net‑Net Rate” is the rate of return at which cash values would otherwise grow but for the deduction of all other policy expenses COIs, FAEs and premium loads, and is thus most useful in accounting for differences in the timing and amount of different charges in different policies for easy comparison.

While certain practitioners may disagree with the use of a consistent Net Rate when comparing different products and calculation policy expenses and instead suggest that using a consistent Gross Rate produces a more accurate means of policy comparison, the use of a consistent Gross Rate for the purposes of such comparisons is only valid when the appropriate cash value allocation is known, and also made consistent in all products under evaluation. For instance, advisors should be cautious not to assume each policy will return 8% if one policy invests in all stocks and another invests in a balanced fund, such that the policies aren’t invested in the same funds that would be reasonably expected to produce matching 8%/year returns in the first place! (Similarly, it’s important to ultimately still compare the policies on a net basis after fund expenses as well, especially since not all life insurance policies, particularly variable policies, use the same sub-accounts with the same underlying expense ratios.)

The availability of cash value is also an element of suitability (i.e., specifically mentioned in NY DFS Regulation 187). Cash value, or cash surrender value (CSV), is a defining characteristic of permanent life insurance. In simple terms, CSV is the value available to the policyholder for withdrawal or upon policy termination and is equal to the policy account value minus the surrender charge. All other factors being equal, the higher the accessible cash value after deduction of cost of insurance charges, policy expenses, and contingent surrender charges, the more suitable the policy. As such, once again measuring cash value accessibility against benchmark average cash values is useful in determining which products are in the client’s best interest (see Figure 10 for an example measurement of accessible cash values, courtesy of Veralytic).

Life Insurance Risk Considerations

Risk is also an element of suitability, both generally speaking, and specifically mentioned in NY DFS Regulation 187. While the premium is often misconstrued as the price/cost of a life insurance policy, the premium is not the price/cost of the life insurance policy (e.g., like a contribution to an Individual Retirement Account is not the price/cost of the IRA). In both cases, the price/cost is the sum of the expenses deducted from the premium/contribution. As such, the stability of the planned premium payments in a minimum premium defined‑death‑benefit policy designs, and/or the reliability of projected benefits in a maximum accumulation defined-contribution policy is always a function of the following formula: Premiums/Benefits = COIs + E – i%.

If costs (either in terms of COIs or other policy expenses) are greater than expected, or interest/earnings are less than expected, the additional premiums will be required to maintain expected benefits or expected benefits will be reduced or lost, resulting in client disappointment (and possible complaint) in either case. As such, to be suitable over the long term (versus just attractive in sales illustrations), cost of insurance charges must be adequate to meet the insurer’s expected death benefit claims, and policy expenses must be adequate to meet the insurer’s and servicing organization’s service and administration commitments, and expected interest/earnings must be reasonable.

Due diligence for product recommendations should, therefore, consider whether expected cost of insurance charges are consistent with mortality experience, whether expected policy expenses are consistent with operating experience, and whether expected policy interest/earnings are consistent with historical performance of both invested assets underlying policy cash values and corresponding asset class benchmarks. NAIC Illustrations Model Regulation generally ignores these risks, instead permitting both changing assumptions over time (e.g., mortality improvements and operating gains, albeit with disclosures in footnotes not often read by advisors or clients), as well as a wide range of interest/earnings assumptions that have too often proved to be unreasonable.

For example, traditional “fixed products” (i.e., universal life and whole life) are required by regulation to invest assets underlying policy cash values predominantly in high-grade corporate bonds and government-backed mortgages as a practical matter. As such, the policy interest crediting rate for universal life products and the dividend interest crediting rate for whole life products will generally correlate over time with the 5.0% historical rate of return on high-grade corporate bonds and government-backed mortgages (higher for insurers with superior investment performance and perhaps for indexed products and lower for insurers with inferior investment performance).

However, NAIC Model Regulations permitted illustrations to assume interest crediting rates as high as 14.0%, and required illustrations to reflect assumed interest crediting rates as low as 3.0%, and continue to allow illustrations to reflect assumed interest crediting rates that vary significantly from the rate of return reasonable to expect based on historical return for invested assets underlying policy cash values. Because these assumed rates are generally guaranteed for one year or less (considerably less than the typically-multi-decade expected holding period for permanent policies), and because insurers routinely change declared interest rates, proper due diligence requires looking beneath the current policy crediting rate to consider both historical performances of both invested assets underlying policy cash values and corresponding asset class benchmarks.

Likewise, NAIC Illustration Model Regulations allows for an even wider range of earnings assumptions for “variable products” (i.e., variable universal life and variable life). In addition, performance expectations are not generally set by the insurer in “variable products,” and instead are set by the agent/broker, and too often, are not correlated with the actual rates of return for the asset allocation appropriate to the risk profile of the client. For instance, NAIC-compliant illustrations permit any policy earnings assumption between 0.0% and 12.0% without regard to the actual asset allocation appropriate to the risk profile of the client. Again, proper due diligence requires looking beneath the illustrated policy earnings assumption to consider the rate of return that’s reasonable to expect from the asset allocation appropriate to acceptable risk.

Best Practices In Life Insurance Policy Due Diligence

On July 18th, 2018, the New York State Department of Financial Services (NY DFS) issued a Best Interest Rule for life insurance (Regulation 187). This new Rule re-defines the meaning of “clients’ best interests” for product recommendations to be more consistent with other fiduciary rules, requiring life insurance producers to "act in the best interests of the consumer … based on an evaluation of relevant suitability information … and the care, skill, prudence, and diligence [of] a prudent person … considering only the interests of the consumer in making recommendations." In other words, to actually delve into all the details discussed in this article.

From a practical perspective, whenever presented with life insurance policy illustrations containing hypothetical premiums, hypothetical cash values, and/or hypothetical death benefits as supposed decision support for some product recommendation, advisors need to insist that all illustrations include those pages commonly referred to as “policy accounting pages” or “detailed expense pages”, and which show year-by-year disclosure of cost of insurance charges (COIs), policy expenses, and the interest/earnings underlying hypothetical premiums, cash values, and death benefits. With these “detailed expense pages”, advisors should have enough information to begin using NY DFS Regulation 187 as a “checklist” for careful, skilled, prudent, and diligent evaluation of the key issues fiduciary advisors should be focused on: 1) costs; 2) performance; and 3) risks relative to benefits.

Different advisors will use NY DFS Regulation 187 in different ways. Some will use it as criteria for seeking out life insurance professionals who have evolved beyond just looking at comparisons of policy illustrations and who instead really do consider the (unbundled) costs, performance, and risks in their product recommendations. Others will use the NY Rule to ensure that search results from a Brokerage General Agency (BGA) or Insurance Marketing Organization (IMO) are based on those costs, performance, and risks. Other still will use Regulation 187 as a more detailed guide for comparing costs among products being recommended, assessing the reasonableness of expected interest/earnings relative to asset class benchmarks, and evaluate the risk of not achieving interest/earnings assumptions.

Either way, NY DFS Regulation 187 provides a “checklist” for determining when an in-force policy or product recommendation is in the clients’ best interest, namely, when a) costs that can be justified, (i.e., cost of insurance charges, mortality and expense fees, investment advisory fees, surrender charges, charges for riders, etc.), b) performance that is reasonable to expect (i.e., availability of cash value, equity-index features, limitations on interest returns, etc.), and c) the risk that is appropriate for the circumstances (i.e., market risk, guaranteed interest rates, etc.) “based upon all products, services, and transactions available to the producer.”

Alternatively, our purpose in creating Veralytic was, from the start, to make such life insurance product due diligence as easy, fast, and reliable… as when I used Morningstar to research and document that mutual fund costs were justified and performance expectations were reasonable early in my own career. Accordingly, many life insurance professionals already include a Veralytic report on their life insurance product recommendations (akin to requesting a Morningstar report to substantiate the due diligence for a mutual fund or ETF recommendation). Or advisors who want to delve deeper themselves can get a complementary Veralytic report on a policy of your choosing via http://www.veralytic.com/complementary-veralytic-report.aspx (and note #Kitces2019 in your submission as a Nerd’s Eye View reader).

What is the standard procedure for finding out everything about my policy? What if I have lost some of my documents?

And here you have it:

“Because COIs are calculated on the NAR (i.e., net amount at risk difference between the death benefit less policy account values), and because COIs increase geometrically with age as discussed above, the NAR itself is a significant factor in the determination of COIs. For instance, COIs are minimalized when cash values are nearly equal to the policy death benefit, even at the older ages when COI rates are at their highest.”

Yet, I hardly ever see a policy with cash value near the DB. Even though the insured was told the policy is paying 5.5 or 6%.

Uh huh.

Does DPL conduct due diligence to this extent?

How timely! I just left Barry a voicemail and referenced this article as to how I found him/ his company- so, thanks Michael! Curious about the details of what partnering with Barry/ Veralytic looks like, to use them as a resource for my firm to analyze some ‘old’ large UL policies for some high net worth clients.

@disqus_uH03zkaWpP:disqus When considering ‘old’ policies how do you evaluate insured-specific current mortality risks? Do you pull APS, rx histories, public records or other data sources? What tools or processes work for you?

Well first, goes without saying, never replace anything until you have a formal offer with a carrier and the numbers make sense for replacement. I am a broker and not a underwriter, but all of the above is used for carriers to evaluate risk and potentially make an offer. Depending on situation, I’ll gather everything health/ personal history related first, contact 4-6 carriers who I think might be the best fit (determined by my experience and knowledge with their different underwriting ‘sweet-spots’) and then receive responses from those underwriting teams. At this point, they provide ball park informal offers, which we then take into account prior to formally applying. There is another route you can go with an informal application, too. But in all cases, make sure you’re working with someone who is truly independent and not formally engaged with any carrier on a w2 basis.

How often do you look at options and current value then? Seems like a great deal of work to do on an frequent basis. How do determine its worth the time investment to spending talking to 4-6 carriers? Experience or any external analysis?