Executive Summary

As the financial advisory industry continues to move away from being primarily product-driven (where client ‘relationships’ were primarily transactional sales interactions, and advisors could go months or even years without interacting with some of their clients after the sale was closed) and towards a recurring-revenue ongoing relationship model (where advisors provide continuous, ongoing advisory services to their clients), the total number of clients that any one advisor can handle at any given time has decreased dramatically. Because, not only are there significant time constraints around actually doing the work necessary to serve those clients well (not to mention the time needed to actually find new clients and convince them to work with you), but there are cognitive constraints as well, given that physiologically our brains (as humans) can only keep track of a limited number of interpersonal relationships to begin with!

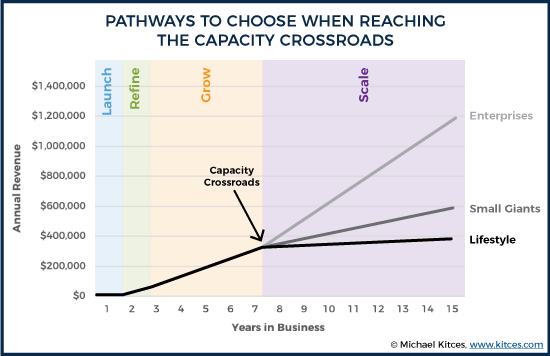

Traditionally, having ‘too many’ clients was rarely a problem – as advisors just focused on their best clients for repeat business opportunities – but in the modern relationship-driven model, all advisors will eventually reach a point where they simply don’t have the capacity to take on more of those ongoing relationship clients and continue to grow the firm. In other words, the advisor has reached a ‘Capacity Crossroads’, and must make a conscious decision about the path to pursue next - either stop growing, or increase the firm’s capacity by bringing on additional staff (and possibly another advisor) in order to continue growing the firm. The problem, however, is that even for those who choose the path of continued growth, once an advisor crosses that capacity threshold, not only are any additional clients less profitable (due to the higher overhead costs incurred by increasing staff), but the advisor also has to manage that growing number of team members… which is rarely a goal for advisors who decided to strike out on their own to serve clients (and not manage employees)!

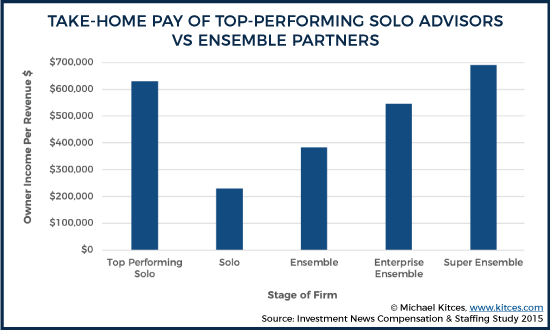

For most financial advisors, the choice at the Capacity Crossroads becomes a decision about long-term income potential, where the advisor has to decide whether to become a ‘lifestyle practice’ and stop growing (flat-lining their growth and income), or to hop on the eternal hamster wheel of growth and work towards building an enterprise business to continue to grow their income. Yet the reality is that, for those who do decide to go down the enterprise path, there is little evidence to suggest that there are any economies of scale growing down the road from being a ‘small’ solo practice to a multi-billion-dollar firm. And, in fact, top-performing solo advisors often have the same take-home pay as the average partner at a $1B+ ensemble anyway!

In addition, the reality is that the choice at the Capacity Crossroads isn’t just between Lifestyle or a ‘go-big’ enterprise to maximize shareholder value in the first place; there is another choice, which is to become a “Small Giant” advisory firm, which doesn’t grow just for the sake of growing, but rather is built intentionally to be ‘great’ instead of ‘big’. In essence, Small Giants seek to be a purpose-driven business, typically one that is able to serve not only the clients/customers, but also the employees, vendors, and the community. In other words, the point isn’t to maximize just shareholder value, but rather to simply be excellent at what they do, while focusing on serving all of their stakeholders, including owners, employees, vendors, clients, and communities. Fortunately, it also turns out that small giants also happen to be steady growers, and are able to be rather profitable to boot!

Ultimately, though, the key point is simply that, if there isn’t that much difference in the long-term wealth-building potential between a lifestyle practice, small giant, or enterprise firm (especially given the time, effort, and reinvestment cost required to build a multi-billion-dollar business), then the answer to the question of the best path to take when you reach the Capacity Crossroads simply comes down to personal choice. Which is important, because in the end, the best way to build a practice that maximizes your own happiness as an advisor isn’t by allowing growth to dictate the role you fill in the business, but by intentionally setting a vision for the type of business you want to build in the first place!

Reaching The Capacity Crossroads In An Independent Advisory Firm

In the early days of building an advisory firm, the formula is pretty simple: go out and get clients. Because in the early days, a newer financial advisor has a lot of time, and not a lot of clients – i.e., a lot of ‘excess’ capacity – and the best way to grow the business (and the advisor’s income) is simply to add clients and turn that idle capacity into more productive time. The more clients the advisor can add, the more income they can generate.

Until, at some point, the advisor reaches the Capacity Crossroads… that moment where suddenly, there’s no more remaining time left in the day that isn’t spoken for by a meeting or service issue for a sizable number of existing clients. And the advisory firm literally runs out of time capacity to grow anymore.

In the past, financial advisors rarely ever had to consider the overall capacity of the business, because the advisory business itself was more transactional. When the focus every year was going out to find new opportunities to do business with someone, and existing ‘clients’ were simply people that the advisor had once sold a product to in the past and had minimal ongoing service needs, there wasn’t much of a capacity limitation for advisors. Thus why the financial advisors of old – brokers or insurance agents – often had hundreds of ‘clients’ (many of whom the advisor might not have actually met with in 1, 3, or even 5+ years!).

But as the business of financial advice shifts to a recurring-revenue truly-relationship-based model – one that necessitates more ongoing service and ongoing meetings with clients, to retain more lucrative ongoing advisory fees, and sets an expectation that the advisor will actually truly know the client and their needs – suddenly a real capacity limitation emerges. As there are just only so many hours in the week, month, and year, for an advisor to do all those meetings and service work. And ultimately, the human brain itself can only handle ‘so many’ relationships with other human beings… which researchers have estimated at approximately 150 people, often leaving advisors with room for no more than 75-100 clients (after leaving some ‘brain room’ for family and friends!).

The most straightforward way for a financial advisor to navigate past the Capacity Crossroads is simply to hire more staff to handle the growing load of clients. Which often means first hiring an administrative assistant to handle more of the servicing work, then adding a paraplanner to help with the financial planning support work, and eventually taking on a servicing advisor to be the lead relationship manager for at least a portion of those client relationships.

The caveat, however, is that adding staff to increase capacity then means, as an advisory firm owner, that the advisor now has to manage them! Which often results in a material amount of additional work… for an advisor who often started the business to serve clients and not to manage people… and generating what is often remarkably little additional income (since the early clients generate substantial income for the advisor-owner doing the work, but for additional clients the owner only generates the profit margin remaining after other advisors do the work!).

Example: Celia started her practice with the goal of simply earning a good and healthy income as a financial advisor, and after her first year in business was happily advising 25 clients with an annual gross revenue of $50k and a net revenue of $35k. She loved spending time with her clients, having lengthy discussions about their lives and goals, and creating very thoughtful, detailed financial plans for them. However, she did such a good job for them that they quickly began referring several of their friends to her. She didn’t want to refuse her clients’ referrals, but without a clear vision of what she wanted to grow to (or who her ideal target client was), the firm quickly blossomed to over 100 clients… and Celia didn’t know how to handle them all.

With an increase of gross revenue to $250k across those 100 clients, Celia had to hire an assistant ($40k/year), and a paraplanner ($55k/year), to help her keep up with the work. Now that she has employees, and a much larger client base, however, she also needs a larger office space, and has a lot of new overhead expenses (e.g., insurance, payroll services and tax, new office equipment, supplies, etc.).

Once Celia’s employees and overhead expenses were paid, her net revenue was only $105k. Despite the fact that her firm had grown, quadrupling her client base, adding more than $200k of additional revenue, her net take-home income was ‘only’ up $70k! In addition, Celia found herself very stressed out and unhappy, because a substantial fraction of her time was now spent managing her staff and overseeing a larger operation, which she did not enjoy at all. Also, because she had so many more clients, she couldn’t spend the focused time on plans that she once enjoyed so much, there was very little opportunity to catch up with her favorite clients over lunch or drinks, and she was frustrated that she had to stick to a strict meeting schedule and decrease the frequency of meetings just so that she could make sure she gave all of her clients at least some attention.

The fact that some advisors don’t want to hire and have to manage people – or end out very unhappy advisors by growing too far and being ‘stuck’ managing more people than they ever wanted to – has led to a dichotomy in the advisory industry between ‘lifestyle’ firms (that choose not to hire and remain founder-centric, limited to the number of clients the founder can personally handle, often with little subsequent growth once capacity is reached), or choosing to become an ‘enterprise’ that grows beyond the advisory firm founder and begins walking down the never-ending treadmill of adding more and more team to support more and more growth.

The Small Giant As An Alternative To Building A Lifestyle Or Enterprise Firm

The one big challenge of the Lifestyle versus Enterprise dichotomy of advisory firms is that many or even most firms don’t appear to clearly fit either definition. As while there are clearly some firms that are focused on being high-income solo advisors, and others who truly seem to have the growth-minded obsession of the classic entrepreneur who seeks to rapidly grow and scale a very large enterprise… there is a substantial subset of advisory firms that do eventually grow beyond their founders, adding in associate advisors, service advisors, and sometimes even adding partners, in a desire to serve more clients, but don’t have the mentality of being ‘enterprise’ builders by any classic definition of entrepreneurism.

The distinction is that these firms between Lifestyle and Enterprise may continue to grow past the capacity of their founders, but still aren’t necessarily being built with the focus to just ‘grow’ for the sake of growing, getting big for the sake of getting big, in a model that’s groomed for an eventual sale and liquidity event for the founders, and a focus on maximizing shareholder returns. Instead, it’s more about simply trying to continuously get better, and deliver whatever unique service the firm has created to more people who would benefit from that service (beyond just what the founder themselves can deliver).

In 2006, the former Executive Editor of Inc. magazine, Bo Burlingham, published a book called “Small Giants”, about a similarly unique subset of companies that “choose to be Great instead of Big”. The core thesis of the book was that these “Small Giant” companies are purpose-driven companies that don’t just make decisions to maximize the value or growth of the business alone, but instead choose a path that aims to be the best at whatever they do, balancing the interests of all their stakeholders, including owners, employees, vendors, customers/clients, and their communities. It’s the craft beer brewing company that chooses to use pure ingredients and eschews modern brewing technology to create a higher quality and more ‘authentically’ brewed best-in-class beer; it’s the independent record label that chooses not to sell out to the record industry and instead stays focused on supporting emerging artists by putting “music before rock stardom and ideology before profit”; it’s the local delicatessen that puts the quality of its food and its deep connection to the local community over expanding and franchising across the country.

In 2006, the former Executive Editor of Inc. magazine, Bo Burlingham, published a book called “Small Giants”, about a similarly unique subset of companies that “choose to be Great instead of Big”. The core thesis of the book was that these “Small Giant” companies are purpose-driven companies that don’t just make decisions to maximize the value or growth of the business alone, but instead choose a path that aims to be the best at whatever they do, balancing the interests of all their stakeholders, including owners, employees, vendors, customers/clients, and their communities. It’s the craft beer brewing company that chooses to use pure ingredients and eschews modern brewing technology to create a higher quality and more ‘authentically’ brewed best-in-class beer; it’s the independent record label that chooses not to sell out to the record industry and instead stays focused on supporting emerging artists by putting “music before rock stardom and ideology before profit”; it’s the local delicatessen that puts the quality of its food and its deep connection to the local community over expanding and franchising across the country.

Notably, a key distinction of Small Giants is that not only are they ‘not huge’ like the publicly traded companies that most people are familiar with, but also that they’re not publicly traded (i.e., owned by outside investors) in the first place, and instead are privately held by their founders. (Or at least, carefully guarded in the hands of shared owners all committed to the same company vision and goals.)

The benefit of maintaining closely held ownership is that it allows the advisory firm to maintain its own control and freedom. Which means the owners really have the ‘luxury’ of choosing to balance a wider range of needs and stakeholders than ‘just’ maximizing profit and shareholder value, and likewise have the luxury of choosing not to pursue major growth opportunities simply for the sake of growing and expanding… particularly if there’s a concern that doing so may come at the cost of sacrificing the quality of their greatness in the first place.

In fact, one of the key essences that Burlingham discovered with Small Giants is that they don’t necessarily have to grow very much at all… because, again, the focus isn’t necessarily on just maximizing the value of the company, but also on being excellent at whatever it is the company does, providing a great work environment for its employees, and often having a deep involvement in its local community. (Even though in practice, doing so often results in a company that both grows steadily and is very profitable as well!) Or as business guru Tom Peters put it in his book “In Search of Excellence”, “great organizations originate from people who have ‘not totally stupid obsessions’ around which they build.”

In turn, part of what makes Small Giants so successful is precisely that their focus is not on just being bigger and more profitable; rather, their focus is on being ‘better’ and prioritizing service not only to customers/clients but also to their employees, vendors/suppliers, and communities. Which is what develops higher-quality relationships with their employees, vendors, and communities in the first place, attracting them to the business purpose (and the culture it creates). All of which creates what Burlingham calls the “mojo” of Small Giants: the business equivalent of a leader’s charisma, that makes people want to be a part of the company.

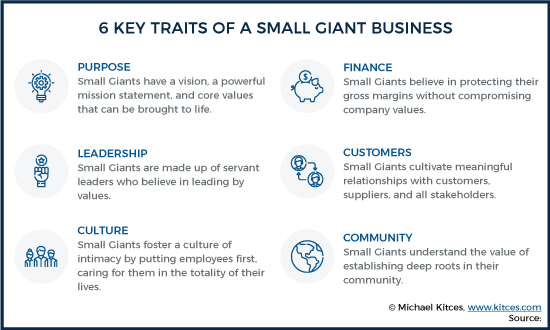

Ultimately, Burlingham finds that the defining characteristics of Small Giants are their (mission-driven) purpose, their (service) leadership, their (intimate employee-first) culture, their relationship-centric approach to customers (and suppliers/vendors), their deep roots in their community, and a focus on not necessarily maximizing profits but being certain to protect their gross margins to remain financially stable (without compromising company values). Which, again, goes beyond the Lifestyle firm that reaches its capacity and stops growing, but isn’t necessarily the same as a classic entrepreneurial Enterprise that pursues growth and maximizing shareholder value at all times (with whatever outside capital and potential loss of control it takes).

The (Similar) Upside Potential Of Lifestyle, Small Giant, And Enterprise Advisory Firms

The conventional view of most businesses is that it’s a ‘grow or die’ world, and that all business owners should always and only want to keep growing and maximizing profits… or be accused of being ‘irresponsible’ to the needs and interests of the business and its shareholders.

This grow-or-die view is only accentuated by the celebration of ‘fastest-growing business’ lists in various industries (including standalone lists just for the fastest-growing advisory firms), media coverage on the sometimes-eye-popping liquidity events of advisory firm founders, and a steady drumbeat of ‘thou shalt grow’ pressure from our own broker-dealer and RIA custodian platforms (as in the end, the primary way their platforms grow is by increasing the size of the advisory firms on their platforms).

Yet in recent years, industry benchmarking studies have revealed that the connection between advisory firm growth, and its anticipated benefits, are not so straightforward. As in practice, it appears that there are virtually no economies of scale to be found in the operation of an advisory firm as it grows from $50M to $250M to $1B to $3B+, as overhead expense ratios and profit margins remain remarkably steady up to a multi-billion-dollar size that exceeds what the overwhelming majority of advisory firms ever grow to in a lifetime. In other words, there’s no discernible growth-leads-to-efficiencies link to be found amongst 99%+ of all advisory firms.

In addition, ongoing growth in a service- and client-intensive business like financial planning often necessitates introducing new partners to the business who have a stake in what is being built (or else they’ll ‘walk’ with their clients and revenue), resulting in a dilutive effect to equity and profits even as the firm grows.

More generally, the mere fact that for the first 100 clients, the advisor earns virtually all of the net revenue (minus just a small allocation for overhead expenses) which can be as high as $0.70 to $0.80 on the dollar, but earns ‘just’ the profit margin (which may be no more than $0.20 to $0.30 on the dollar) beyond that point, means in practice actual take-home income growth ends out being far slower than revenue growth as advisory firms grow past their founder’s capacity. Even more so for firms that are reinvesting heavily to produce that growth, such that they can’t even enjoy 20% to 30% profit margins (because of all the additional capacity hiring they must do). On the other hand, the growing availability of technology in recent years has made solo advisory firms more efficient and profitable than ever.

In fact, industry benchmarking studies have shown that the top-performing solo advisory firms can actually generate the same take-home pay as the average partner at a $1B+ AUM Super-Ensemble advisory firm! (And some high-producing solo advisors can be even more profitable!)

Of course, advisory firm founders who build larger ensemble firms do build the value of their equity, in addition to the income stream. Except, because of the necessary burden of reinvestment of profits to fuel that growth, owners of ensemble firms growing up to that point typically take home even less in income for years or decades… such that often the value of the equity in the end may not actually materially enrich the founder of an ensemble firm, and instead merely makes up for the foregone profits along the way (except for perhaps a small subset of the very largest enterprise advisory firms)!

Visioning An Advisory Firm Past The Capacity Crossroads If The Money Didn’t Matter?

The fact that the long-time wealth-building potential of advisory firms can actually be remarkably similar for Lifestyle, Small Giant, and most Enterprise firms, raises an interesting question – if continuing to grow an advisory firm towards an enterprise doesn’t necessarily result in greater wealth in the long run, what is the best path for an advisory firm owner to take when approaching the Capacity Crossroads?

In essence, the choice comes down to not what is financially best – as they can all be very rewarding – but literally a matter of what the advisors themselves want to build.

A Lifestyle firm (advisor) becomes the preference for those who would rather work to live, than live to work. This includes those advisors who not only want to balance the demands of the business against their non-business goals and desires, but specifically want to avoid the burdens of managing a substantial number of people, and wish to remain primarily client-facing. Lifestyle firms are simply firms where advisors remain first and foremost advisors, paid for the advisory work they do. Notably, lifestyle firms in practice are rarely sold; instead, the most profitable path for them is simply to remain working in the business (and making the income) as long as they can, which is more remunerative than selling it anyway.

A Small Giant (advisor/owner) becomes the preference for those who don’t want to just make a good income, but feel a fundamental drive and desire to have their business deliver a better and better solution to more and more clients. Not to grow for the sake of growth, or for the sake of financial remuneration, but simply in pursuit of continuing to expand the reach of a purpose-driven business to serve… recognizing that such a path will inevitably mean the advisory business must grow beyond its founder, and the founder themselves will ultimately wear the shared hats of advisor (still serving clients) and advisory firm business owner (managing a growing team). Small Giants tend to pursue internal succession plans (and/or heavily utilize Employee Stock Ownership Plans), recognizing that when a unique purpose-driven business is built, it’s extremely difficult to find external buyers who will honor the original vision and purpose of the business, compared to internally developed talent that has been steeped in the culture of the firm and can carry on the legacy and vision of the business in the future.

An Enterprise (advisory-firm owner) becomes the preference for those who truly feel driven and motivated to build ‘a business’, and transform themselves from being ‘a financial advisor’ to fully becoming ‘an advisory firm business owner’. For enterprise builders, it’s common and even likely that the founder will eventually move away from client relationships altogether, and instead will invest themselves primarily into the growth and development of their people and their culture instead, and building and maximizing the shareholder value of the business by whatever path it takes (from organic to inorganic growth, self-funded or strategically taking outside investor capital), often with an eventual goal of a liquidity event at the end (whether selling to a larger firm, a strategic acquirer, a private equity firm, or as an IPO in the public markets).

The key point, though, is simply recognizing that the decision to ‘keep growing’ past the Capacity Crossroads doesn’t have to be an all-in-or-all-out decision of either trying to grow a ‘huge’ Enterprise (that eventually must manage a large number of people), or remaining a Lifestyle firm instead out of a lack of desire to manage people at all.

There is a middle ground: the Small Giant, the purpose-driven business that may happen to grow longer along the way, but isn’t necessarily motivated by the money and financial benefits to keep growing, rather than a desire to blend together financial and non-financial goals in pursuit of simply delivering the business’ purpose-driven value to more clients beyond those the firm currently serves (and doing the necessary hiring and expansionary growth along the way).

So what kind of advisory firm do you really want to build?

Excellent article, Michael! I love your take on the Small Giants philosophies through the lens of financial firms. Bo Burlingham, the author of the Small Giants book, also co-founded the Small Giants Community, an organization dedicated to identifying, connecting, and developing purpose-driven leaders. I work for the organization as its Chief Storyteller.

There are more resources on how to build a Small Giants business and other learning opportunities at http://www.smallgiants.org. Thanks again for your valuable contribution to the Small Giants conversation!

Thank you for such a wonderful article! I have felt neither a desire to plateau with a lifestyle practice nor a goal to build a huge ensemble firm and didn’t have the words to describe it and haven’t met anyone else with a similar goal and thought I was the only one. Now I know I am not and look forward to reading Small Giants!

Interesting article. How many clients do you think a solo advisor (lifestyle practice) can handle completely by themselves? (No virtual paraplanner or assistant). Assuming real financial planning is being done.

Out here in India, we feel ‘occupied’ and busy once an advisor has around 45-50 relationships to handle. Unlike in US, there is lot of administrative work involved here as data is not easily available and has to be manually ‘worked’ upon to get the consolidated view. My personal guess is that with the adviser tech available in US and the access and automation of data with it, one should be able to handle around 80 odd relationships.

Of course, Michael would be able to give a far better view.

Hi Michael, everything here is so true and I can fully relate to it. ‘Small Giants’ is a great read. If you’re at the capacity crossroads it will help you to decide next steps. Continue with the great work and podcasts. Thanks.

Very insightful piece, Michael. Every firm (and its founders) come on this ‘Crossroad’ event sooner or later and have this dilemma of what to do, how to approach things going forward. Your article comes so very handy and shows a clear direction. Thanks for this.

Interesting Article. After listening to Dan Goldie, he gave ample evidence that with his book of business, that a TAMP might be a “less stress, more economical” way to go… Your thoughts…

Excellent article Michael. I’ve given this a good bit of thought, listened to others, and reached some conclusions from my experience as a solo. I’m now partially retired, have a practice of about 30 clients for whom I have about $15 million AUM and $30 million under advisement. I think Mukul’s number of 60 is easily done IF (and it is a big IF) one uses a third party for investments. I learned that my clients all wanted investment management, but had a variety of needs and situations that created a requirement for different investment strategies. As a solo I couldn’t craft and manage a wide range of strategies so I found a reasonably priced company that could do that for me while I was still in charge. I could easily do 60 clients and I do pretty full service high touch planning. A great presentation I heard from a Fidelity executive on artificial intelligence at last year’s FPA conference gave me the sense that in the future one could double that and still have the same level of personal connection and service. I think Mark Tibergian’s number of an upper limit of 90 for real relationship planning is about right and with new technology that could go to about 150 clients. If you run the same numbers you used one could have a very rewarding practice without the hassles of growth.

Trusted financial advisor LifeLong Wealth Management Group

#LifeLong Wealth Management Group

One of Canada’s greatest assortment of high-quality adult incontinence products is provided by Gladwell Care, which sources its goods from well-known and reliable manufacturers.

#Gladwell Care

Together, we will navigate the intricacies of the financial landscape and craft a tailored roadmap for your financial future.

https://www.creativelive.com/student/llwmg?via=accounts-freeform_4