Executive Summary

When purchasing a product or service, it’s only natural to want to know what it will cost. But in the context of paying for professional services in particular, “what you pay” isn’t only a matter of measuring the value (relative to what you get), but also of understanding the incentives of the person providing the service and their conflicts of interest. From the person selling new clothes on commission (and who tells everyone they ”look great” in whatever they’re wearing coming out of the dressing room) to the surgeon who thinks ‘every’ health issue may require surgery to resolve, it’s crucial to understand when advice is at least at risk of being compromised.

However, when conflicts of interest become too widespread and of concern to consumers, businesses can differentiate specifically by highlighting their efforts to mitigate or entirely avoid such conflicts. Which, in practice, is what has happened with financial advisors over the past 20 years as the “Fee-Only” label has shifted from a descriptive label of how an advisor is compensated into an increasingly mainstream marketing label. And leading to a growing number of disciplinary actions from the CFP Board in response to CFP certificants that misused the label in a manner that was misleading to clients.

Accordingly, in its recently enacted new Standards of Conduct, the CFP Board has further updated and refined its compensation disclosure definitions, particularly as it relates to the “Fee-Only” label. At its core, the requirement to be “Fee-Only” is still that the advisor receives only fees – now more broadly labeled as not receiving any “Sales-Related Compensation” that might include commissions, trails, revenue-sharing solicitation fees, or the like – and emphasizes the importance that neither the CFP professional nor their firm nor any Related Party receives such compensation either.

On the other hand, the CFP Board also refined the scope of Related Parties that have to be considered in a CFP professional’s compensation disclosures, recognizing that there’s no need for compensation to be ‘disclosed’ from a Related Party that had no connection to the services provided by the CFP professional in the first place. Thus, for instance, the mere fact that a family member or separately owned business happens to generate commissions is not ‘fatal’ to the Fee-Only label, as long as the CFP professional isn’t actually directing clients there (such that the compensation would be “in connection with” their financial planning services).

Ultimately, the key point to recognize is that the CFP Board does not actually require CFP professionals to be “Fee-Only” and not accept commissions, nor does the organization specifically endorse one type of compensation model over another. However, to the extent that “Fee-Only” is becoming more popular in the marketplace, and financial advisors may feel a financial incentive to use the label, the CFP Board does require that CFP professionals use the label accurately. Which means it’s up to the advisor about whether they wish to use the Fee-Only label or not… but if they do, it is incumbent upon them as CFP professionals to do so in an accurate manner that reflects the full scope of the advisor-client relationship!

The Problematic Popularity Of Marketing As “Fee-Only”

In order for a fiduciary to obtain informed consent from a Client for a prospective conflict of interest, the advisor must first disclose the nature of the conflict in the first place. Accordingly, fiduciary rules for financial advisors have long required Registered Investment Advisers to disclose (via Form ADV Part 2) the nature of their compensation – for instance, whether they receive AUM fees, performance-based fees, or even commissions as an RIA through a related entity – and explain any conflicts of interest that may ensue from their compensation.

In the past decade, such compensation disclosures have taken on additional focus given the success of organizations like NAPFA (and more recently, also Garrett Planning Network and XY Planning Network) in promoting “Fee-Only” as a way to describe the compensation of advisors who receive only advisory fees (in the form of AUM fees, hourly fees, or subscription or retainer fees) and no commissions. The significance of the Fee-Only label is that, by definition, it espouses that such advisors do not have conflicts of interest that commissions entail.

In practice, though, this message about the consumer benefits of “Fee-Only” advice has been widely adopted by the media… and in the process, turned “Fee-Only” from a descriptive explanation of compensation practices into a (very desirable) marketing label, to the point that advisors have an economic interest to describe their compensation as “Fee-Only” for the marketing benefits it creates… and therefore necessitating specific Standards of Conduct around how such compensation descriptions and labels should be used (properly). As in practice, one of the most common functions of regulations is to ensure ’truth in advertising’, and that descriptive marketing labels are an accurate reflection of what the consumer will actually get.

Prior (2008) Standards Of Conduct On Use Of “Fee-Only” Compensation Description

Under the CFP Board’s 2008 Standards of Conduct, CFP certificants who were providing financial planning or material elements of financial planning were required to provide upfront disclosure (written or oral) of any compensation they (or a Related Party) may receive through the course of the Client Engagement.

Rule 1.2. If the certificant’s services include financial planning or material elements of the financial planning process, prior to entering into an agreement, the certificant shall provide written information and/or discuss with the prospective client…

…[c]ompensation that any part to the agreement or any legal affiliate to a party to the agreement will or could receive under the terms of the agreement; the factors or terms that determine costs; [and] how decisions benefit the certificant and the relative benefit to the certificant.

Rule 2.2. A certificant shall disclose to a prospective client or client the following information:

- An accurate and understandable description of the compensation arrangements being offered. This description must include:

- Information related to costs and compensation to the certificant and/or the certificant’s employer, and

- Terms under which the certificant and/or the certificant’s employer may receive any other sources of compensation, and if so, what the sources of these payments are and on what they are based.

In addition, the prior Standards of Conduct also required that CFP professionals not engage in any form of ‘misleading advertising’ about their services:

Rule 2.1. A certificant shall not communicate, directly or indirectly, to clients or prospective clients any false or misleading information directly or indirectly related to the certificant’s professional qualifications or services. A certificant shall not mislead any parties about the potential benefits of the certificant’s service. A certificant shall not fail to disclose or otherwise omit facts where that disclosure is necessary to avoid misleading clients.

While these rules didn’t necessarily require that advisors provide detailed descriptions of the exact amounts of compensation they would receive, it did inherently require both providing a description of how the advisor is compensated, and that the description be an accurate reflection of reality.

In fact, to help ensure that advisors use such labels properly, the “Terminology” section of the prior Standards of Conduct also included an explicit definition of what it meant to be “Fee-Only”, stating:

Fee-Only. A certificant may describe his or her practice as “fee-only” if, and only if, all of the certificant’s compensation from all of his or her client work comes exclusively from the clients in the form of fixed, flat, hourly, percentage or performance-based fees. [Emphasis added.]

In other words, “Fee-Only” meant compensation that came solely from various types of fees – flat, hourly, or AUM – and not of any other type (e.g., commissions).

Notably, though, the word “Compensation” itself in the definition of Fee-Only was also explicitly defined further in Terminology, as:

“Compensation” is any non-trivial economic benefit, whether monetary or non-monetary, that a certificant or related party receives or is entitled to receive for providing professional activities. [Emphasis added.]

The key aspect of the “Compensation” definition – as an extension of Fee-Only – was that not only were advisors required to receive only fees and not commissions to use the Fee-Only label, but also that any Related Parties (e.g., the financial advisor’s firm, or another business entity that the financial advisor owns) had to receive only fees and not commissions as well. Any commission compensation received by a Related Party would ‘taint’ the Fee-Only status of the CFP certificant.

And in point of fact, the treatment of commissions received by Related Parties became a major issue over the past decade when it came to the use of the “Fee-Only” label (and the enforcement of compensation disclosure rules against CFP certificants).

Key Fee-Only Compensation Disclosure Case History: Goldfarb And Camarda

In early 2011, a local competitor in Florida filed a complaint against Jeffrey and Kimberly Camarda, alleging improper use of the “Fee-Only” label by the CFP certificants, who provided both “Fee-Only” financial planning from their RIA (Camarda Advisors) and also implemented insurance products for their clients through a commission-based insurance agency they also owned (Camarda Consultants).

The Camardas claimed that “Fee-Only” was an accurate description of the compensation received for services provided by Camarda Advisors, and was in accordance with the SEC’s rules and required Form ADV disclosures (where the relationship to Camarda Consultants was disclosed). However, the CFP Board noted that its rules pertained to the Camardas as CFP certificants, and not specifically their RIA entity (which by definition was ‘Fee-Only’ since the RIA itself had no brokerage or insurance product affiliates), such that all of the related entities must be considered when evaluating how they held themselves out to the public.

Accordingly, under the CFP Board’s “Related Party” rules, the Camardas were similarly found to be in violation of the compensation disclosure rules for describing themselves as “Fee-Only” with respect to their financial planning services as CFP certificant under Camarda Advisors when in practice clients were also paying insurance commissions to a Related Party (Camarda Consultants, which the CFP certificants owned).

However, the Camardas also noted that the existence of dual-registration (with an RIA and a broker-dealer) was not uncommon in the world of financial advisors, including amongst the CFP Board’s own volunteer leadership and committees. And sure enough, in November of 2012, then-chair of the CFP Board’s Board of Directors, Alan Goldfarb, announced his resignation from the Board after an allegation that Goldfarb (and two other members of the CFP Board’s Disciplinary and Ethics Commission) had misrepresented their compensation in their marketing and communications to clients.

The issue in Goldfarb’s case was that he had represented to the public that he was a “Fee-Only” CFP certificant (on FPA’s PlannerSearch website for consumers) while working at an RIA that was owned by an accounting firm which also owned a broker-dealer subsidiary (where Goldfarb also had both an employment relationship and an ownership interest). Accordingly, similar to the Camarda case, Goldfarb had a relationship with both an RIA and a broker-dealer, and his clients could potentially pay a commission to the related broker-dealer while also being engaged with Goldfarb’s RIA for financial planning services. As a result, Goldfarb was similarly deemed not to be “Fee-Only”, and therefore Goldfarb was issued a Public Letter of Admonition from the CFP Board.

Notably, though, unlike in the Camarda case, Goldfarb maintained that his role in the broker-dealer was purely a supervisory/oversight function and not as a ‘producing’ registered representative, and noted that his ownership was a mere 1% interest. Perhaps even more significant, though, Goldfarb noted that not one of his clients had ever actually paid a commission to the related broker-dealer, and in practice that his clients really had only ever paid fees for his services.

Nonetheless, the CFP Board determined that Goldfarb’s Related Party was still “entitled to” earn commissions from Goldfarb’s clients (given the presence of the broker-dealer itself) and that Goldfarb’s employment and ownership interests still triggered “Related-Party” status (i.e., there was no ‘de minimis’ rule for a ‘negligible’ interest in a Related Party; any ownership interest in a Related Party could trigger the rules).

In an attempt to create further clarity around the issue, the CFP Board issued a Notice To Members in August of 2013, in which it further emphasized that CFP professionals must provide accurate descriptions of their compensation based on compensation they, or a Related Party, received or are entitled to receive, including:

- Compensation that the CFP professional receives or is entitled to receive from a Client or prospective Client for providing professional activities;

- Compensation that Related Parties, such as the CFP professional’s employer, receives or is entitled to receive from a Client, prospective Client, or other source for providing professional activities; and

- Compensation the CFP professional receives or is entitled to receive from Related Parties, such as the CFP professional’s employer or other sources, for providing professional activities.

A key aspect of the CFP Board’s “entitled to” framework, where compensation that a CFP professional or their firm either received or could (i.e., was “entitled to”) receive must be disclosed, was that even just being affiliated with a broker-dealer – whether by registration (in an employment context) or ownership – was enough to disqualify a CFP professional from being a CFP certificant.

In other words, simply being a registered representative of a broker-dealer would automatically disqualify the CFP professional from claiming they were “Fee-Only”, for which even being able to prove that 100% of clients had only ever paid 100% in fees was not sufficient to demonstrate otherwise (as there was still nothing to stop the next client from being charged a commission if the CFP professional was affiliated with a broker-dealer that was entitled to do so).

Similarly, the CFP Board’s August 2013 Notice To Members also emphasized that because compensation disclosures, in the end, were about what the CFP professional or their firm received as compensation from clients for services rendered, it would no longer be valid for CFP professionals to simply disclose their compensation as “salary”, as even if the CFP professional were compensated by salary, that salary would only be earned based on the compensation the CFP professional’s firm generates (as revenue) in the form of fees or commissions from the Client.

Thus, as CFP professionals who received a salary from a firm that generates its revenue from commissions for product sales must still disclose their compensation as “commissions” and not “salary” (and in point of fact, Goldfarb was also disciplined in part because, after being questioned about his Fee-Only status, he subsequently altered his compensation description on the FPA PlannerSearch website to “salary”, but the CFP Board found that because his salary came in part from a firm that had a related broker-dealer, the potential commission compensation still had to be disclosed).

The end result of these compensation disclosure concerns was that, after the 2013 Notice to Members was issued, CFP professionals were required to explain their compensation as Fee-Only (if applicable), Commission-Only (if applicable), or fall in between in the broad category of “Commission and Fee” (for all those who were neither Fee-Only nor Commission-Only).

Still, though, the ongoing desire and marketplace pressure to use the Fee-Only label resulted in ongoing improprieties, including a Financial Planning magazine article (and subsequent Wall Street Journal follow-up) finding 486 CFP professionals at wirehouse broker-dealers who were improperly using the Fee-Only label (despite, by definition of their employment at a broker-dealer, being ineligible to do so), and more than 30 disciplinary actions in the past 5 years, including Private Censures, Public Letters of Admonition, and even suspensions of the CFP marks, related to improper use of the “Fee-Only” label.

New Duties When Representing Compensation Methods Under CFP Board New Standards Of Conduct

The increasingly high profile of compensation descriptions (and especially the “Fee-Only” label) in recent years, combined with the rising number of disciplinary actions for improper use of those compensation labels, led the CFP Board’s Commission on Standards to revisit and ultimately revise the rules for Compensation Disclosures going forward. New compensation disclosure rules that took effect in October of 2019 will be enforced starting after June 30th of 2020.

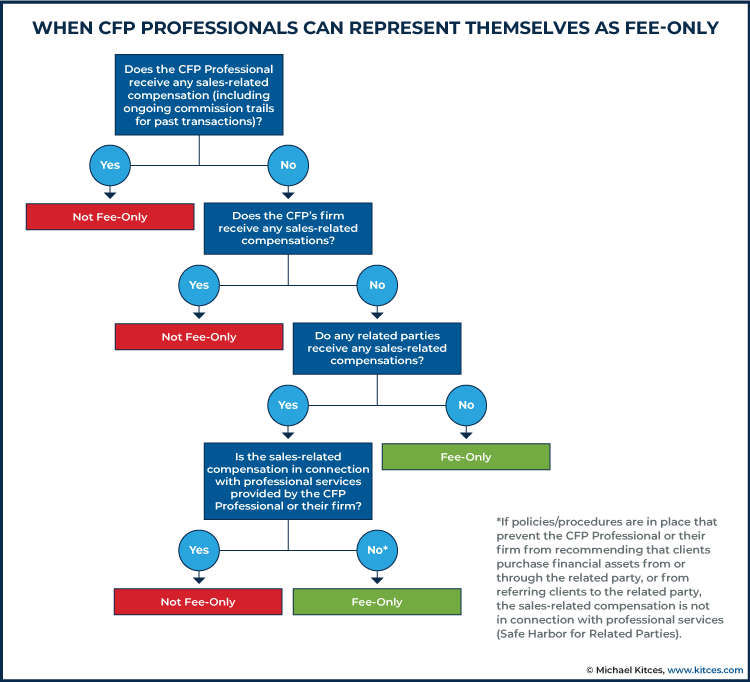

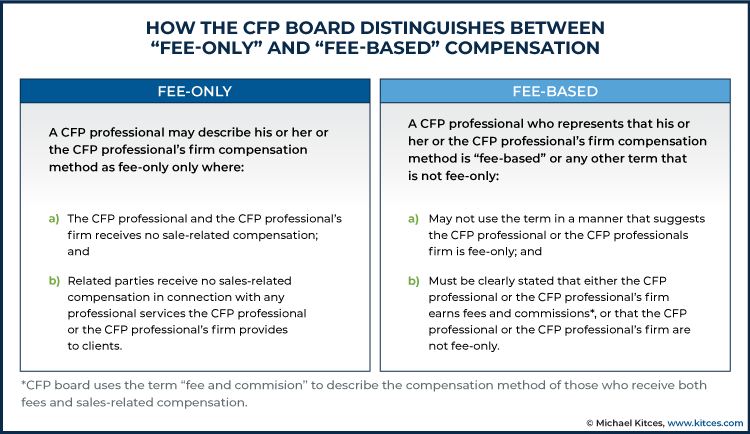

At their core, the CFP Board’s new Standards of Conduct, and specifically the establishment of new “Duties When Representing Compensation Method” to clients and prospects as a part of the 15 Duties of CFP professionals to their clients, still require that CFP professionals only use the “Fee-Only” label if their compensation is in fact only from fees and not commissions, stating that:

Fee-Only. A CFP® professional may represent his or her or the CFP Professional’s Firm’s compensation method as “Fee-Only” only if:

- The CFP professional and the CFP Professional’s Firm receive no Sales-Related Compensation; and

- Related Parties receive no Sales-Related Compensation in connection with any Professional Services the CFP professional or the CFP Professional’s Firm provides to Clients.

Notably, in the new “Fee-Only” compensation definition, the key requirement is not that the advisor only received compensation from a series of specified types of fees (e.g., AUM fees, hourly or flat project fees, monthly subscription or retainer fees, etc.), but instead that the CFP professional does not receive any “Sales-Related” (i.e., commission) Compensation.

Defining Sales-Related Compensation Rendering CFP Professionals Ineligible For Fee-Only

Under the new Standards of Conduct and Duties to Clients, Sales-Related Compensation, for the purposes of compensation disclosures, is defined as:

Sales-Related Compensation. Sales-Related Compensation is more than a de minimis economic benefit, including any bonus or portion of compensation, resulting from a Client purchasing or selling Financial Assets, from a Client holding Financial Assets for purposes other than receiving Financial Advice, or from the referral of a Client to any person or entity other than the CFP Professional’s Firm. Sales-Related Compensation includes, for example, commissions, trailing commissions, 12b-1 fees, spreads, transaction fees, revenue sharing, referral or solicitor fees, or similar consideration.

Not surprisingly, the core of the definition of “Sales-Related Compensation” is around commissions that are generated from a client purchasing or selling financial assets (e.g., the traditional sales or transaction-related commission) or similar payments on an ongoing basis for continuing to hold such assets (e.g., levelized commissions that continue to be paid after the original sale). As the CFP Board’s own definition notes, this may include (upfront) commissions, trailing commissions such as 12b-1 fees, spreads (e.g., for individual bond transactions), and other transaction fees.

In this context, it is important to note that the receipt of ongoing commission trails, even for transactions that may have occurred in the distant past, still run afoul of the CFP Board rules on the receipt of Sales-Related Compensation for CFP professionals who want to use the Fee-Only label.

Similarly, even receiving ’just’ the shareholder servicing portion of a 12b-1 fee is still deemed to be Sales-Related Compensation, such that even advisors working at Vanguard may not characterize themselves as “Fee-Only” (as Vanguard’s brokerage platform receives 12b-1 servicing fees to support investors using the technology platform).

In fact, because FINRA defines mutual funds that pay only the 0.25% shareholder servicing portion of a 12b-1 fee as “no-load” (no sales-charge), but the CFP Board treats all 12b-1 fees as a commission, it is even possible for a CFP professional or his/her firm exclusively using “no-load” funds to still be ineligible for Fee-Only treatment.

Nerd Note: For financial advisors who may be considering a switch to “Fee-Only” status, the requirement to cease the receipt of any Sales-Related Compensation, including 12b-1 fees and commission trails, can sometimes present a challenge unto itself. In the case of 12b-1 fees, it is often (though not always) feasible to engage in an internal Share Class external to an institutional/advisory share class that excludes such costs and revenue to the advisor. However, in the case of many types of insurance and annuity products, the CFP professional may have to terminate their relationship with the insurance company altogether and convert the Client to a “House/Orphaned Account”, or cede the Client to another broker or agent, to fully cease their receipt of Sales-Related Compensation. There is no exclusion under CFP Board rules for CFP professionals whose only Sales-Related Compensation pertains to trails from prior sales that occurred in the past.

In addition, the new “Sales-Related Compensation” rules also explicitly note that payments for the referral of a Client to any person or entity will also be deemed Sales-Related Compensation. This does not include the CFP professional’s own firm (thus, revenue-based compensation that the firm pays to its advisors upfront or on an ongoing basis for business development and client servicing will not run afoul of the rules), but advisors who are paid solicitor fees to refer to other advisory firms (e.g., serving as a solicitor for another RIA) would be treated as Sales-Related Compensation.

Similarly, serving as a solicitor for a TAMP would also be treated as Sales-Related Compensation (though a TAMP that collects the advisor’s own fees, keeps a portion to cover the TAMP’s expenses, and remits the remainder of the advisor’s own revenue will not be treated as receiving Sales-Related Compensation).

On the other hand, these Sales-Related Compensation rules would not prohibit a Fee-Only CFP professional from paying solicitor fees to get clients and remain Fee-Only (even/including fees to a Related Party that it owns); it’s only Sales-Related Compensation to receive such compensation from an external/third party in exchange for an introduction to/referral of the Client.

Other exceptions to what may otherwise constitute Sales-Related Compensation include:

- Soft dollars (any research or other benefits received in connection with Client brokerage that qualifies for the “safe harbor” of Section 28(e) of the Securities Exchange Act of 1934);

- Reasonable and customary fees for custodial or similar administrative services if the fee or amount of the fee is not determined based on the amount or value of Client transactions; or

- Non-monetary benefits provided by another service provider, including a custodian, that benefit the CFP professional’s Clients by improving the CFP professional’s delivery of Professional Services, and that are not determined based on the amount or value of Client transactions.

In other words, compensation that is received by RIA custodians or other service providers to an advisory firm, that is specifically allocated back to benefit clients (e.g., soft dollars), or that is reasonable and customary and not specifically tied to the amount or value of Client transactions or that otherwise benefit Clients (e.g., dollars or no-cost services for a custodian’s technology, practice management consulting, conferences, etc.), is not treated as Sales-Related Compensation.

Ultimately, though, the key point is simply that if the CFP professional, or the CFP professional’s firm, receives any kind of Sales-Related Compensation, the CFP professional may not hold themselves out as being “Fee-Only”. And the fact that the CFP Board’s rules encompass both the CFP professional and their firm means that, even if the firm itself is compliant with other regulators (e.g., an RIA that properly discloses an outside business activity relationship with an affiliated brokerage firm or insurance agency in its Form ADV), the CFP professional would still run afoul of their duties under the CFP Board’s Standards of Conduct. Similarly, the fact that a CFP professional complies with NAPFA’s definition of “Fee-Only” does not necessarily or automatically mean that they qualify under the CFP Board rules as a Fee-Only CFP professional (especially given that the two organizations have diverged in the past regarding the definition of Fee-Only).

The Receipt Of “In Connection With” Sales-Related Compensation By Related Parties

The idea that a CFP professional should only hold out as “Fee-Only” if, in fact, the CFP professional (and their firm) only receives fees and not commissions is relatively straightforward. In practice, the more complicated scenarios – and the ones that ultimately resulted in disciplinary action for both Goldfarb and Camarda – emerge when “Related Parties” to the CFP professional are also considered.

In an effort to provide further clarity, the new Standards of Conduct provide an explicit definition of what constitutes a “Related Party”:

Related Party. A person or business entity (including a trust) whose receipt of Sales-Related Compensation a reasonable CFP professional would view as directly or indirectly benefiting the CFP professional or the CFP Professional’s Firm.

In turn, the new rules state that there is a rebuttable presumption (i.e., presumed to be the case unless proven otherwise) that a “Related Party” will include a member of the CFP professional’s family, a business entity that the CFP professional (or their firm) controls, is controlled by, or is under common control with, or any business entity that is controlled by members of the CFP professional’s family.

Notably, though, in theory, any ownership stake by a CFP professional in a business entity that receives Sales-Related Compensation would be a Related Party (as was the case with both Goldfarb and Camarda). The CFP Board does not provide any de minimis exception to such rules. Consequently, even ‘just’ a 1%-or-less stake in an entity that receives commissions may count, if a “reasonable CFP professional would view [the receipt of that Sales-Related Compensation] as directly or indirectly benefitting the CFP professional or the CFP Professional’s Firm”.

On the other hand, the fact that the CFP professional must actually benefit (directly or indirectly) from the Related Party’s receipt of Sales-Related Compensation still allows some room for a truly negligible interest – thus, for instance, if the CFP professional suggests the Client open a bank account for their new business at Bank of America, and also happens to own shares in Bank of America through an S&P 500 index fund in the advisor’s own retirement portfolio, should not run afoul of the rules… as a “reasonable CFP professional” would not interpret any real measurable “benefit” to the CFP professional for having referred one Client to open one account at one branch of a national publicly-traded bank!

In addition, it’s also important to recognize that with respect to Sales-Related Compensation to Related Parties, it’s not simply a matter of whether the Related Party receives such compensation, but what that compensation is received for:

Fee-Only. A CFP professional may represent his or her or the CFP Professional’s Firm’s compensation method as “Fee-Only” only if… Related Parties receive no Sales-Related Compensation in connection with any Professional Services the CFP professional or the CFP Professional’s Firm provides to Clients.

In Connection with any Professional Services. Sales-Related Compensation received by a Related Party is “in connection with any Professional Services” if it results, directly or indirectly, from Client transactions referred or facilitated by the CFP professional or the CFP Professional’s Firm.

In other words, the mere fact that a Related Party earns/generates Sales-Related Compensation (e.g., commissions) is not enough alone to run afoul of the rules. Otherwise – especially given the Related Party rules for family members – a CFP professional might lose their eligibility to claim “Fee-Only” status because their brother happens to be a health insurance agent, or their spouse is a real estate agent, or the family owns a mortgage business… all scenarios where family members are receiving “Sales-Related Compensation” (in their respective jobs/businesses).

Instead, when it comes to Related Parties, the receipt of Sales-Related Compensation only counts when it is received “in connection with any Professional Services” that the CFP professional (or their firm) actually provides to Clients. Thus, for instance, if the advisor recommends insurance in the financial plan and implements it in a related business (as occurred in the Camarda case), it would still be Sales-Related Compensation.

However, if the CFP professional has a relationship to a business receiving Sales-Related Compensation that has no actual connection to the CFP professional’s own clients and the services they received (as was the case with Goldfarb, or more generally in any scenario where family members happen to be in commission-related businesses, but the CFP professional doesn’t actually refer clients to them), the CFP professional could still qualify as providing “Fee-Only” services.

In fact, to help more clearly separate out situations where family members or other related businesses may earn commissions in their own roles not actually connected at all to the CFP professional’s clients and services provided, the CFP Board provides a “safe harbor” exception:

Safe Harbor for Related Parties. Sales-Related Compensation received by a Related Party is not “in connection with any Professional Services” if the CFP professional or the CFP Professional’s Firm adopts and implements policies and procedures reasonably designed to prevent the CFP professional or the CFP Professional’s Firm from recommending that any Client purchase Financial Assets from or through, or refer any Clients to, the Related Party.

Thus, for instance, if the CFP professional establishes and implements a policy that explicitly states “Clients will not be referred to the spouse/family member/family business/related business” (such that even if Clients do end out doing business there, it occurs only naturally and not as a result of the CFP professional’s referral), then the Related Party’s Sales-Related Compensation would not eliminate the ability of the CFP professional to call themselves “Fee-Only”.

Again, though, any Related Party compensation that is connected to the CFP professional’s financial advice and/or an intentional referral recommendation would be treated as (not-Fee-Only) Sales-Related Compensation to the CFP professional.

Avoiding Misleading Representations About Compensation: Fee-Based And Other Labels

In addition to the specific rules around the use of the “Fee-Only” compensation label, the CFP Board’s “Duties When Representing Compensation Method” obligation also includes a general requirement that “A CFP professional may not make false or misleading representations regarding the CFP professional’s or the CFP Professional’s Firm’s method(s) of compensation”. Accordingly, CFP professionals have not only an obligation to use the “Fee-Only” label accurately only as prescribed, but also not to use other labels in a manner that may be misleading.

For instance, as part of a fiduciary exemption for broker-dealers first proposed in 1999 and finalized in 2005, the SEC first established the concept of a “fee-based brokerage account” – a type of brokerage relationship where investors could engage in ongoing trading and the broker could provide ongoing (non-discretionary) advice recommendations to the investor for an ongoing fee calculated as a percentage of the account balance (similar to an Assets-Under-Management fee) in lieu of paying traditional brokerage commissions. Investors, in turn, might have a fee-based brokerage account and conduct other ‘traditional’ commission-based business with the broker.

Ultimately, this Broker-Dealer Exemption was vacated in the lawsuit of Financial Planning Association vs SEC in 2007, but the concept of having a “fee-based” brokerage relationship remained, but causing some confusion for investors about the difference between a “fee-based” engagement (which pertained to a particular account that was compensated by fees) and a “Fee-Only” engagement (which pertains to the entire advisor-client relationship).

Accordingly, as a part of the CFP Board’s new “Duties When Representing Compensation Method”, CFP professionals are explicitly prohibited from using “’fee-based’ or any other similar term that is not Fee-Only… in a manner that suggests the CFP professional or the CFP professional’s firm is Fee-Only”. Instead, regardless of whether the firm is utilizing a fee-based engagement for at least a subset of accounts with clients, if the CFP professional is not Fee-Only, they “must clearly state that either the CFP professional or the CFP Professional’s Firm earns fees and commissions, or that the CFP professional or the CFP Professional’s Firm are not Fee-Only”.

In addition, in situations where a CFP professional controls their own firm, the Standards of Conduct explicitly require that the CFP professional “not allow the CFP Professional’s Firm to make a representation of compensation method that would be false or misleading if made by the CFP professional”.

Of course, in many situations (particularly with larger firms, or more generally where the CFP professional is in an employee and not an independent model), the CFP professional does not actually control their firm and the way it markets itself. Nonetheless, the new Standards of Conduct still require in such situations that the CFP professional “must correct a CFP Professional’s Firm’s misrepresentations of compensation method by accurately representing the CFP professional’s compensation method to the CFP professional’s Clients”.

In other words, the CFP professional will not be held liable for inappropriate marketing that their firm engages in beyond the CFP professional’s control but will still be expected to clarify their compensation with their own clients.

In the end, though, it’s important to recognize that the CFP Board does not specifically advocate for one type of advisor compensation model over another, does not direct CFP professionals to operate on a Fee-Only basis to meet their fiduciary obligations to clients (as long as the resulting Conflicts of Interest are properly disclosed, receive informed consent, and are mitigated to the extent possible), and does permit fiduciary CFP professionals to earn commissions as well as fees.

However, the Standards of Conduct nonetheless do require that if a CFP professional is going to use the Fee-Only label (or other marketing language that implies a similar compensation methodology with clients), it must be an accurate representation of their actual compensation (including to themselves, their firms, and Related Parties in connection with the delivery of their professional services as CFP certificants).

Ultimately, it’s up to CFP professionals about whether they will operate on a fee-and-commission basis or as Fee-Only, and whether it’s worthwhile from a business and/or marketing perspective to adopt the Fee-Only approach. The CFP Board’s only concern is that compensation disclosures, and compensation labels in general, must be an accurate reflection of the (entire) advisor-client relationship.

Disclosure: Michael Kitces is a co-founder of XY Planning Network, which was mentioned in this article.

Nice job Michael of giving the background and explaining the new standards as to fee disclosures.

Based on what you said “However, if the CFP professional has a relationship to a business receiving Sales-Related Compensation that has no actual connection to the CFP professional’s own clients and the services they received (as was the case with Goldfarb, or more generally in any scenario where family members happen to be in commission-related businesses, but the CFP professional doesn’t actually refer clients to them), the CFP professional could still qualify as providing “Fee-Only” services.” perhaps the CFP Board might consider rescinding or expunging my censure since Fee-Only would have been correct.

Again, keep up the good work as a trusted industry observer.

Alan Goldfarb

I think the CFP board made a good decision here. Consumer clarity should be key; the consumer should understand the compensation and service model so he/she can make an informed decision.

The (mis)perception that the CFP Board is striving to create that “fee-only” is somehow less conflicted than other advisor compensation models is complete and utter nonsense and reflects a total lack of understanding of the basic principles of economics and incentives. I dropped hourly billing from my compensation platform two years ago because I found it to be the MOST conflicted compensation model. Aside from the well documented hourly billing conflicts in the legal profession of “heavy pencils” and “value billing,” the uniquely awful problem with hourly billing in financial planning is that it creates a powerful disincentive for clients to take the time to share the important detailed financial information necessary for establishing a holistic financial plan.

I still do flat-fee planning through my RIA, but am always aware of the incentive I have to do as little work as possible to get the job done. I am sure some readers will smirk at reading this. I encourage you to get in touch with your inner utility-maximizing economist self. To borrow a quote from Freakonomics, “Morality reflects the way we would like society to work. Economics reflects the way it actually does work.”

It is also completely moronic for the Board to fail to understand that there are many instances in which the client’s interests are best served by applying multiple compensation models. As a simple example, while most of my revenue comes from AUM business (which has its own set of dastardly conflicts that must be disclosed), my clients’ interests with respect to their fixed income portfolios and/or corporate cash are sometimes best met through standard brokerage accounts that are not subject to AUM fees. In most cases, these accounts are free to the clients (save for the occasional ticket charge). Why pay an AUM fee on assets that require no management or where the AUM fee is greater than the interest earned on the account?

As with the CFP Board’s ridiculous faux fiduciary standard, the Board’s flexing over its new fee-only rule is more about creating the appearance of good ethics than the reality. It unequivocally fosters confusion among consumers. I can attest that it is truly refreshing/liberating as a non-CFP financial planner to be able to truly put the interests of the consumers first and to embrace true transparency through the disclosure of all MATERIAL FACTS, instead of being bound by the CFPB’s feckless new standard of conduct and by its authoritarian rule over its 87,000 CFP members. As industry ethics thought leader Don Trone once said, no organization has done more harm to the fiduciary standard [and to consumers] than the CFP Board. Don also stated, “If the CFP Board was a country, it would be North Korea.”

And this is the organization that Michael wants to be the standard bearer for the profession???

Maybe its time stand up and push back against the Board. #consumersfirst #moralcompasssearch

Well, what happens if a fee only advisor whose been in business for 30 years and marketed themselves as fee only all this time decides to get married to a mortgage broker. They will simply choose to live together and never get married. How about the same scenario again and his 2nd cousin child becomes an insurance agent and the whole family wants to help the the cousin’s child. You can’t divorce your family. So the fee only advisor has to remove their fee only marketing because someone in the distance family took a commission based job. I can see this rule being amended many more times before it eventually gets discarded. We need a simple broad fiduciary standard and compensation should be tied to the level of fiduciary advice given.

I can’t wrap my head around how the CFP Board (or whoever makes these rules) is essentially saying it’s unethical for Fee-Only advisors to have solicitors agreements with other Fee-Only advisors. This I almost seems like a logical fallacy.

Also, does the CFP actually have the ability to enforce the use of the words “Fee-Only.” I wasn’t aware that they had a trademark including the words “Fee-Only.” What’s next? Are we not going to be allowed to call ourselves “Investment Advisors” if we take an AUM fee? Where did CFP participants agree to be bound by future seemingly arbitrary rules? Are firms who were receiving compensation for referring clients to other fee-only firms now going to be stripped of their CFP marks? Or, are they grandfathered in?