Executive Summary

Over the past couple of decades, Congress has passed several laws impacting the Federal estate tax exemption, resulting in a significant increase from $675,000 in 2001 to $11.58 million today. As a result, under the current rules, most taxpayers will not be subject to a Federal estate tax liability, and thus, the current focus of tax planning for one’s estate should generally focus on reducing Federal income tax liability. Basis management is a critical part of this process and includes strategies to both maximize the step-up in basis, as well as to minimize the loss of any unrealized and/or carryforward capital losses.

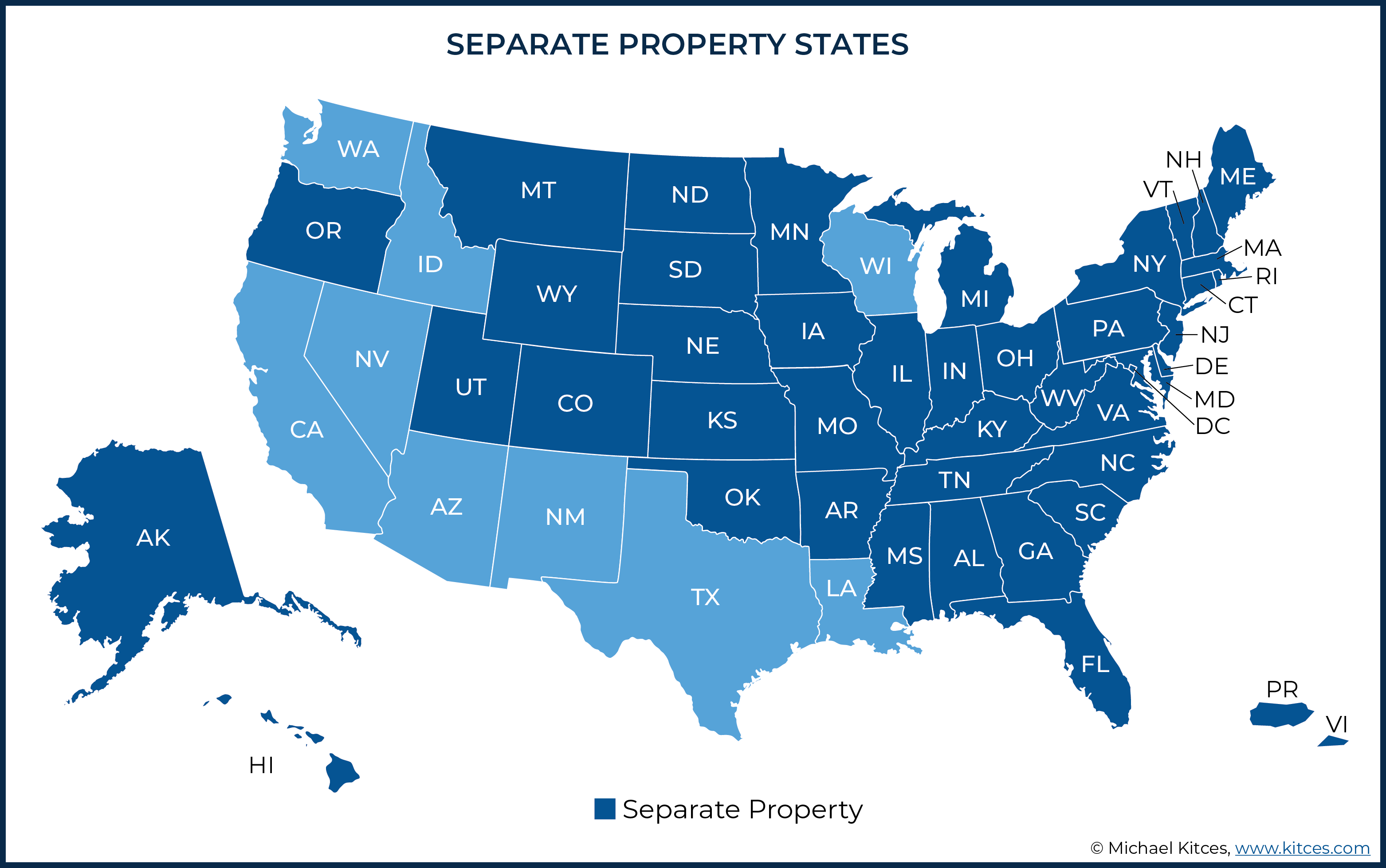

For spouses, two questions are important in determining adjustments to the basis of inherited (non-IRD) assets: 1) who owns the asset, and 2) whether the state of residence is a community property or separate property state. In separate property states, property ownership is generally determined by common law, which generally dictates that property is owned as it is actually titled. Thus, if an asset is in an account that belongs solely to the deceased spouse, then 100% of the asset is subject to a step-up (or step-down) basis adjustment; however, for assets held jointly (typically either as joint tenants with rights of survivorship or tenants by the entirety), the surviving spouse will typically receive a step-up/step-down basis adjustment on only one-half of the assets (the half of assets considered to have been owned by the deceased spouse).

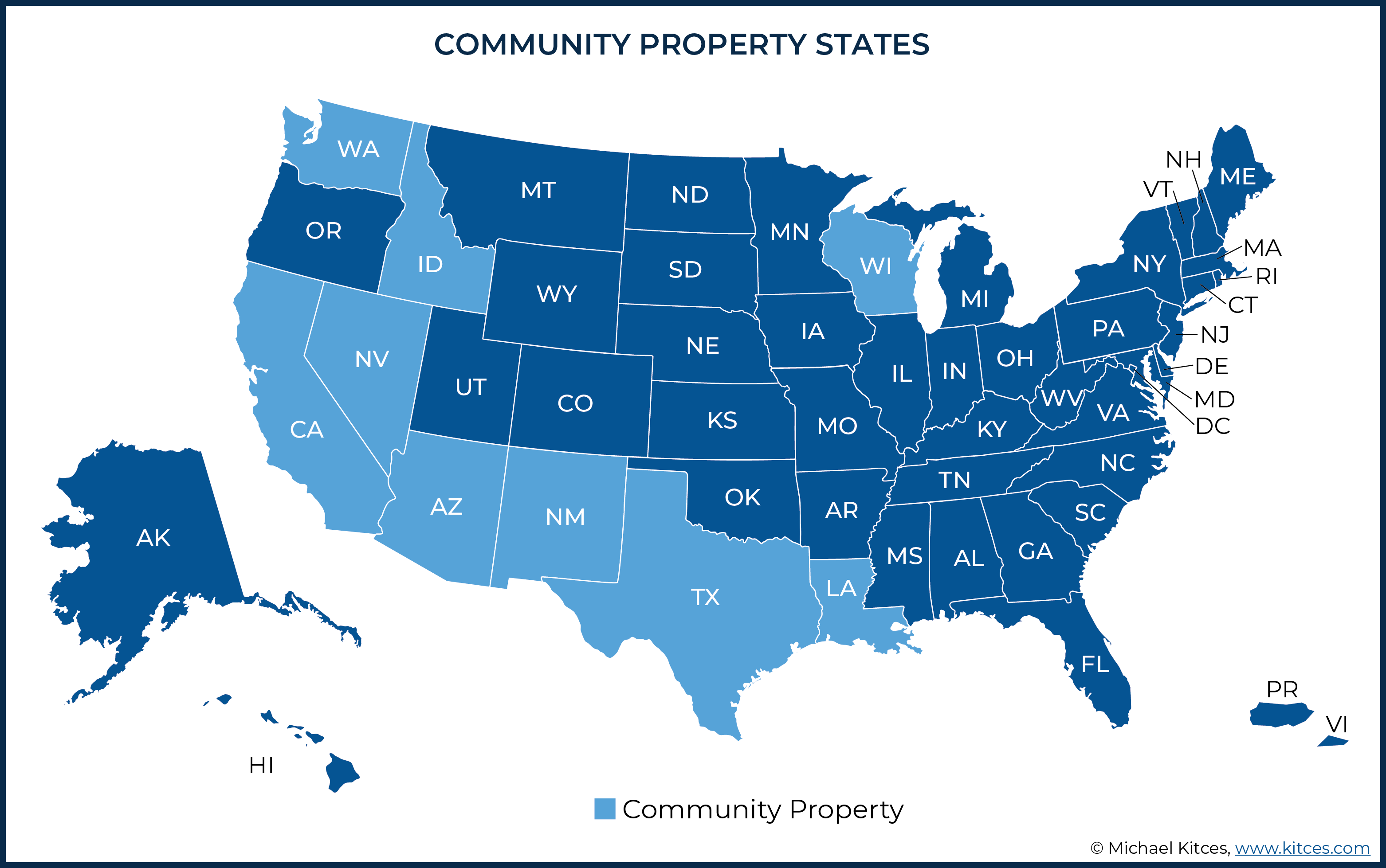

By contrast, in states that follow the “community property” rules (AZ, CA, ID, LA, NV, NM, TX, WA, and WI; with AK also allowing couples to opt-in to community property treatment), most assets acquired during marriage, as well as those assets which are mutually agreed upon to be jointly owned or that can’t clearly be identified as either spouse’s separate property, are essentially treated as being simultaneously owned 100% by each spouse. Accordingly, these assets will automatically receive a full step-up/step-down adjustment on the entire value of the property upon the death of either spouse.

This basis adjustment of inherited assets at death can potentially result in losing out on the opportunity to benefit from realized capital losses, which can be used to offset capital gains and up to $3,000 ordinary income each year. However, by gifting assets prior to death, the original owner’s basis can be retained, and unrealized capital losses preserved!

For non-spouse beneficiaries, the benefits of gifting assets with potential capital losses are not quite as favorable as those for spouse beneficiaries but remain valuable, nonetheless. More specifically, when a non-spouse receives an asset with unrealized capital losses, the so-called ‘double basis’ rules apply. These rules use the value of a gifted asset on the date of the gift to calculate the amount of any capital loss. On the other hand, the donor’s basis at the time of the gift is used to calculate the amount of any capital gain.

Application of the ‘double basis’ rules results in three potential consequences for non-spouses who are gifted with assets that have unrealized capital losses: 1) If the sale price of the asset is less than the fair market value on the date of the gift, then the recipient of the gift can claim a loss equal to the difference between those two values; 2) If the sale price of the asset is more than the original owner’s basis on the gift date, then the recipient of the gift has a capital gain equal to the difference between those two values; and 3) If the sale price of the gifted asset is in between the fair market value on the gift date and the original owner’s basis, the recipient has neither a capital gain nor a capital loss.

Ultimately, the key point is that gifting assets is a simple yet effective strategy to preserve the economic value of unrealized capital losses that can be used to reduce future capital gains (and up to $3,000 of ordinary income, annually). As while the basis of inherited assets will generally receive a step-up (or step-down, depending on the FMV) adjustment at death, unrealized capital losses from inherited assets are essentially useless after the original owner’s death since they will no longer be available for use to offset any gains in tax years after death.

In the not-so-distant past, the primary estate planning concern for many mass-affluent, and most high-net-worth families, was avoiding the Federal estate tax. Over the past 20 years, though, the estate tax exemption has repeatedly and dramatically increased, starting with President Bush’s Economic Growth and Tax Relief Reconciliation Act of 2001, and most recently under the Tax Cuts and Jobs Act of 2017. Cumulatively, these changes have increased that estate tax exemption by more than 1,700% over the last two decades, from just $675,000 in 2001 to $11.58 million in 2020.

Thanks to these increases, as well as other generous estate tax rule changes made since 2001 (such as portability of the estate tax exemption), the number of decedents exposed to Federal estate taxes has decreased by nearly 98%, to less than one in every one-thousand families is likely to end up owing estate tax under the current system. In other words, only about 2,000 to 3,000 estates in the entire country will have to contend with a Federal estate tax in 2020.

Accordingly, “tax planning” for one’s estate at death in the current environment has become a lot less about estate tax planning, and far more about the income tax planning opportunities at death… particularly with respect to opportunities to maximize the cost basis of assets inherited at death.

IRD (Non-Step-Up) Assets Vs. Step-Up-In-Basis Assets

When an individual dies and leaves assets to an heir, those assets fall into one of two categories.

The first group of assets can be categorized as Income in Respect of a Decedent (IRD), while the other group of assets consists of essentially everything other than IRD items that are included in the first group. The primary difference between the two groups of assets, from a beneficiary’s point of view, is that only assets in the second group receive a step-up in basis, while IRD assets do not.

Income-In-Respect-Of-A-Decedent (IRD) Assets Get No Step-Up In Basis

IRC Section 691 outlines the rules for Income in Respect of a Decedent, which, in essence, is any type of “pre-tax” asset whose ordinary income tax consequences were not already recognized before the decedent passed away.

IRD assets include a deceased sole proprietor’s or pass-through business owner’s outstanding accounts receivables, embedded gains on U.S. savings bonds, other accrued but unpaid bond interest, embedded gains of non-qualified annuities, the gain associated with outstanding installment sales payments, net unrealized appreciation, final employment bonuses and paychecks that weren’t paid before death… and most commonly, all pre-tax retirement accounts (e.g., IRAs, 401(k) plans, etc.). These IRD-type assets receive no step-up in basis, which essentially means that beneficiaries of the assets step into the decedent’s tax shoes after their death.

Step-Up-In-Basis Assets

By contrast to the select group of assets that fall into the IRD category upon the death of an owner, any and all other (non-IRD) assets receive a step-up in basis.

The “step-up in basis rule”, as outlined in IRC Section 1014, essentially treats the beneficiary of an asset received due to the owner’s death as though they purchased the inherited asset for its fair market value on the date of the decedent’s death (or on the alternate valuation date as described in IRC Section 2032, if such an option is elected by the executor of an estate).

Thus, the beneficiary of such assets is generally free to sell such assets immediately without any income tax consequences (assuming no gain/loss since the decedent’s death). Plus, from a sheer convenience perspective, this means the beneficiary can sell the asset and know what the cost basis is (fair market value on the date it was inherited), without needing to try to retroactively reconstruct cost basis from historical purchase and transaction information that may no longer be available after the original owner has passed away.

Step-Down In Basis And The ‘Step-Up-In-Basis’ Misnomer

While the phrase “step-up in basis” has become the colloquial way of describing the tax treatment that a beneficiary’s non-IRD assets receive upon inheritance, the reality is that the phrase does not always ring true.

Instead, as noted above, IRC Section 1014 treats the beneficiary as though they purchased the assets in question for the fair market value on the decedent’s date of death… whether that amount is higher, or lower, than the decedent’s basis in the property prior to death.

Of course, one would certainly hope that this amount is greater than the decedent’s own basis, especially if they’ve owned the asset for a long period of time. But the reality is that’s not always going to be the case. Sometimes investments lose value between their date of purchase and when their owner passes away. Thus, in situations where the value of an asset has declined since a decedent’s original purchase, a beneficiary will generally have to step down the basis of the inherited property to its value on the date of death.

Example #1: In 2015, Marsha purchased 500 shares of Beverly Hillbillies Oil stock in her taxable brokerage account for a total of $400,000. Recently, Marsha passed away and, on the date of her death, owing to a steep decline in energy prices since their purchase, her Beverly Hillbillies Oil shares were valued at only $70,000. (As far as we know, her death was not a result of losing $330,000 in her portfolio, but a mere coincidence!)

The heir to Marsha’s Beverly Hillbillies Oil shares will be treated as though they purchased those shares on her date of death. As such, their cost basis in the acquired-by-inheritance Beverly Hillbillies Oil stock will be decreased from the original $400,000 down to $70,000, its fair market value on Marsha’s date of death.

Accordingly, if Beverly Hillbillies Oil stock were to have a dramatic turnaround and Marsha’s heir were to sell the stock two years later for $400,000 – the same amount Marsha initially paid for her shares in 2015 – her heir would owe long-term capital gains tax on the $330,000 gain that occurred after Marsha’s death (even though neither Marsha nor her heir ever got a tax deduction for the prior $330,000 loss!).

How The Step-Down In Basis Impacts Spouses’ Joint Accounts In Separate Property States

The step-down-in-basis rules apply to non-IRD assets transferred to a beneficiary by reason of the owner’s death, which can include both ‘traditional’ inheritances (e.g., from the original owner to their children), but also include bequests to a beneficiary who is a spouse of the original owner.

However, in order to apply the rules for the step-up (or step-down) of basis for property transferred between spouses at the death of the first spouse, it’s necessary to first determine which spouse actually owned the property for income tax (including step-up/step-down in basis) purposes in the first place.

And notably, the rules to determine ownership of property in the first place – getting to the answer of the “Who actually owns what?” question – is generally a matter of state law… not Federal law. In essence, the Federal Tax Code provides the “how” (as in “How should property be treated upon passing to a beneficiary?”), but it’s state law that provides the “what” (as in “What property is treated as having belonged to the decedent?”).

Thus, in order to understand the tax treatment of assets after death, including which assets will be stepped-down in basis, an understanding of both state property laws and the Federal income tax laws is necessary.

When it comes to the ownership of property by spouses, the vast majority of states use a “separate property” regime, where common law is used to determine property ownership. Under common law, ownership is determined by how property is actually titled, and property in one spouse’s name is generally treated as belonging solely to that spouse.

Accordingly, the beneficiary of property owned entirely by one spouse will get a full step-up/step-down in basis upon that spouse’s death… even if the beneficiary of the decedent-spouse is the other spouse!

For a variety of reasons, though, many married couples prefer to hold most, if not all, of their taxable investments in joint accounts. And more specifically, those accounts tend to be joint accounts with rights of survivorship.

Under IRC Section 2040, in situations where spouses have a “qualified” joint interest in property – property held by spouses as either joint tenants with rights of survivorship, or as tenants by the entirety – upon the death of the first spouse, the surviving spouse will generally and automatically receive a step-up/step-down in basis on one-half (but only one-half) of the assets. In other words, the deceased spouse is presumed to have owned 50% of (and therefore, get a step-up/step-down in basis for 50% of) the assets, regardless of how much each spouse actually contributed to the purchase.

That stepped-up/stepped-down basis amount (50% of the fair market value) is then added to the basis already attributed to the surviving spouse via the 50% of the assets that they were deemed to have owned prior to the deceased spouse’s passing.

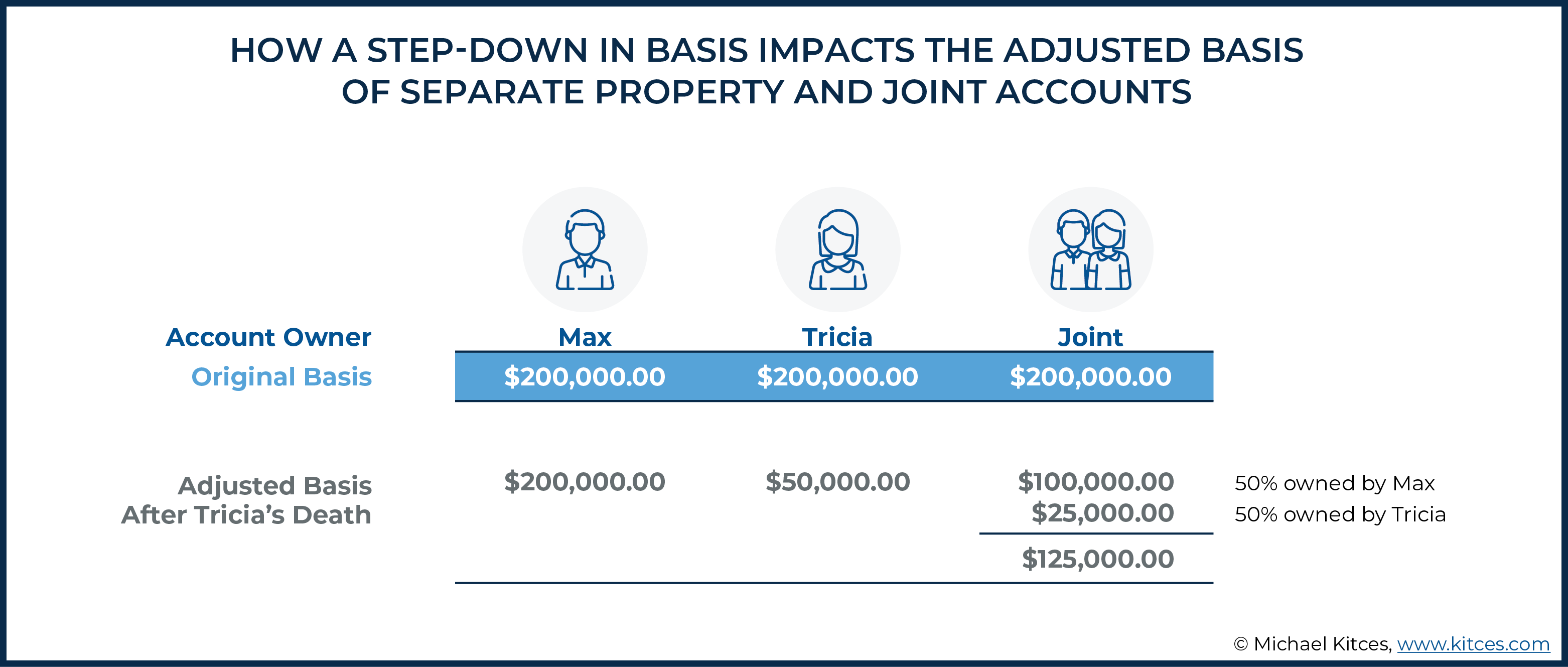

Example #2: Max and Tricia are married and live in Virginia, a separate property state. They have three taxable brokerage accounts: one that is titled only in Max’s name, one that is titled only in Tricia’s name, and one that titled as a joint account. Each of the accounts contains CPR stock that was purchased for $200,000 (each).

Unfortunately, Tricia has just passed, and on Tricia’s date of death, the CPR stock in each of the three brokerage accounts noted above was worth $50,000. Thus, the couple had a total of $150,000 of CPR stock as of Tricia’s passing, which had been collectively purchased for $600,000 (original cost basis). Notably, however, because of the three different ways in which the stock accounts were owned (titled), there will be three different basis treatments for the stock owned in the accounts when received by the spousal beneficiary.

The stock owned in Tricia’s name only will receive a full step-down in basis. Thus, the basis of the stock in that account will drop to $50,000, its fair market value on the date of Tricia’s death.

Similarly, half of the joint account will receive a step-down in basis (since it is deemed to be owned 50% by Tricia as a joint account held between a married couple), resulting in a total of $125,000 of basis ($25,000 step-down in basis equal to the value of Tricia’s half of the account upon her death + $100,000 of Max’s own existing basis on his half of the account upon Tricia’s passing).

Finally, the stock owned in Max’s name only will receive no step-down in basis at all because it was fully owned by Max, leaving Max’s original basis of $200,000 intact. Thus, after Tricia’s death, Max will have a total of $50,000 + $125,000 + $200,000 = $375,000 of basis on the $150,000 total value of the CPR shares.

Accordingly, as a result of Tricia’s death, the ownership of the couple’s cumulative CPR shares at that time, and the step-down in basis rules, Max loses a cumulative $600,000 - $375,000 = $225,000 of basis upon Tricia’s passing.

Nerd Note:

The result of the above example does NOT produce $150,000 of CPR shares with a uniform cost basis of 250% ($150,000/375,000) of the share price at Tricia’s death. Rather, there are truly three separate share lots – the one-third of the shares that were owned by Tricia have a basis of $50,000, which match their (Tricia’s) date-of-death value, the one-third of the shares that were in Max’s individual account retain their cumulative $200,000 price-at-purchase basis, and the remaining one-third of the shares that were owned jointly are allocated the remaining $125,000 of basis.

Selling An Investment That’s Down To Lock In A Realized Capital Loss Prior To Death Is Often NOT A Viable Solution

Many times, the knee-jerk reaction of advisors to the “The Disappearing Capital Loss At Death” problem is to sell the asset with the capital loss prior to death, to ‘lock in’ the realized loss on the couple’s tax return. Alas, this is often not a viable solution.

More specifically, while couples filing joint tax returns tend to think that everything on their tax return is theirs – as in “it belongs to both of them” – the reality is that while a joint tax return reports a couple’s combined income, deduction, credits, etc., on a common return, the building blocks of that return still largely belong to the respective individuals making up the couple, themselves.

Take, for instance, carryforward capital losses, which are losses that have already been ‘locked in’ by the sale of “loser investments”, but which have not yet been used up in previous tax years.

In general, taxpayers are allowed to use capital losses to offset any capital gains, plus an additional $3,000 of ordinary income. Any losses in excess of those amounts (net capital gains plus $3,000 of ordinary income) cannot be deducted in the current year but may be carried forward to future years, up to and including the year of death.

Capital loss carryforwards are reported on Schedule D, Capital Gains and Losses, which, like the Form 1040 that most people are familiar with, records the combined amounts of a couple (and not the gain and losses of each member of the couple separately). However, the “building blocks of gain and loss” that are used to complete that form still belong to each member of the couple separately.

Thus, and as Revenue Ruling 1974-175 made clear over 40 years ago, the capital loss associated with one individual from a couple ‘dies’ with the death of that person who owned the asset producing the loss, and not upon the “death of the couple”.

In the absence of any express statutory language, only the taxpayer who sustains a loss is entitled to take the deduction. See Calvin v. United States, 354 F. 2d 202 (10th Cir. 1965). Therefore, the business loss and the capital loss sustained by the decedent for the period ending with the date of his death are deductible only on his final income tax return. Thus, no part of such net operating loss or capital loss is deductible by the decedent's estate or carried over to subsequent years. (emphasis added)

It is, therefore, a well-settled matter that while a married couple can use each other’s income and deductions to offset one another when electing to file a joint return, the actual items of income and deductions (and credits, etc.) remain the ‘property’, of the person (or persons) generating them (or of the assets that person held). And since a joint return can only be filed up to the year in which a spouse passes away, after that, any unused deductions, credits, or other tax benefits attributable to the deceased spouse will, unfortunately, generally die with them.

Example #3: Bruce and Pearl are married and have filed a joint income tax return for each year since their wedding. Sadly, Bruce died on January 15, 2020. At the time, there had been no trades (realized gains or losses) in any of the couple’s taxable accounts in 2020, nor has Pearl made any since Bruce’s death.

In 2000, Bruce and Pearl met with a broker and purchased $250,000 worth of RonEn stock in their joint brokerage account. Unfortunately, as luck would have it, in 2008, RonEn went bankrupt while Bruce and Pearl still owned the stock in their joint brokerage account. Thus, the couple became the not-so-proud owner of a combined long-term capital loss of $250,000.

Over the course of the following decade and until Bruce’s death, via both the sale of some investments with capital gains and the $3,000 annual capital loss amount allowed to be written off against ordinary income, the long-term carryforward capital loss on the couple’s joint tax return was whittled down to ‘just’ $123,000.

If Pearl takes no action with respect to investments in her own taxable account(s) before the end of 2020 (e.g., sells some investments with a capital gain to be offset by the existing carryforward capital loss), another $3,000 of the $123,000 capital loss carryforward will be used to offset ordinary income on the couple’s final joint income tax return. The remaining $120,000 of carryforward capital loss, however, will be cut in half.

More specifically, since 50% of the RonEn shares sold at a loss were deemed to be owned by Bruce, 50% of the carryforward capital loss was Bruce’s as well. Therefore, any amount of his loss not used up by the last year ‘he’ files an income tax return is irrevocably lost, along with its tax-saving power.

If a surviving spouse is able to sell assets with enough gain in the same year as the capital-loss-“owning” deceased spouse’s death, then the decedent’s realized capital loss can be fully ‘used up’ on the year the tax return was filed for the year of death (the final joint tax return).

But what if the surviving spouse doesn’t have enough taxable assets with a gain? There’s no way to make use of that now-realized capital loss!

Nerd Note:

It’s entirely possible that, with good tax planning, a surviving spouse would have little to no gain in a taxable account after the first spouses death, as appreciated assets could have been transferred to the deceased spouse’s ownership (for at least one year) and then left (bequeathed) back to the surviving spouse with a full step-up in basis, eliminating any gains!

Community Property Twists To The Step-Up/Down-In-Basis Rules For Marital Property

While most states employ a separate property regime based on common law, a number of states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin) use a different system, called community property, to determine ownership of property for married couples. Which, again, is important, because state-determined ownership of property defines the Federal income tax treatment of which of the couples’ joint assets get a step-up (or step-down) in basis!

A complete discussion of community property is beyond the scope of this article, but in general, community property for married couples includes assets that are acquired during marriage while living within a community property state (with some exceptions, such as assets acquired during the marriage but received via gift or inheritance), assets that are ‘converted’ to community property via mutual agreement, and any other property that otherwise clearly can’t be identified as an individual spouse’s separate (i.e., non-community) property.

But what exactly is community property? Conceptually, for post-death basis planning purposes, you might think about community property as property that is simultaneously owned 100% by both spouses, regardless of whose name(s) is/are actually on the account. Thus, community property of spouses will generally receive a full step-up/down in basis on the entire value of the property, at both deaths… automatically!

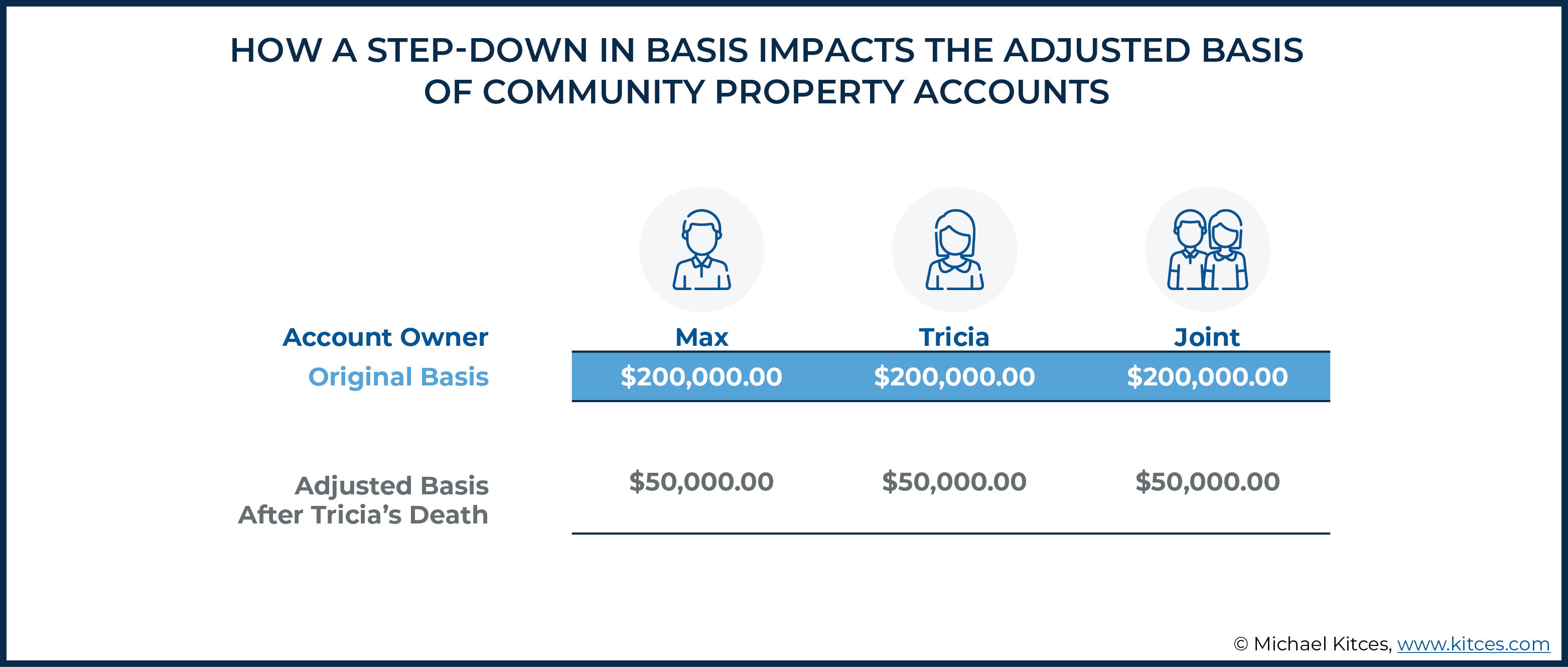

Example #3: Recall Max and Tricia, the married couple from Example #2. Suppose that, instead of living in Virginia, a separate property state, they instead chose to marry and live in a community property state.

Further recall that Max and Tricia have three taxable brokerage accounts: one that is titled only in Max’s name; one that is titled only in Tricia’s name; and one that titled as a joint account. Now imagine that each of the accounts again contains CPR stock that was purchased for $200,000 (each) with income the couple earned while married (i.e., “community property” funds). Thus, although all three accounts have different registrations, they are all considered to be community property.

On Tricia’s date of death, the CPR stock in each of the three brokerage accounts noted above was worth $50,000. Thus, the couple had a total of $150,000 of CPR stock as of Tricia’s passing. Oddly – at least to the majority of people who are more familiar with common-law-state rules – since each of the accounts was considered community property, Max will be subject to a full step-down in basis on all three accounts (i.e., the basis of the stock will decrease to $50,000 in each account, for a total basis of $150,000)... even the account that was only in Max’s name to begin with!

Compared to Example #2, in which all the facts were the same except for the fact that Max and Tricia’s assets were considered separate property in a common-law state, there is an additional step down of $225,000 (on top of the $125,000 that was already lost in Example #2) because of the community property rules!

Planning To Minimize Step-Down-In Basis Reductions For Investments With Unrealized Capital Losses

Clearly, the result in each of the three examples above is wholly unsatisfying (albeit some even worse than others). Investment losses are certainly not desirable, but once they exist, they do have real economic value in the form of a tax deduction for the loss. Thus, if a loss is, well… lost upon death, so is the economic value associated with it. Planning to minimize such outcomes is an important and valuable part of estate planning… and especially when Federal estate tax planning has been so greatly diminished in recent years (due to the increases in the Federal estate tax exemption).

Notably, when planning to minimize the impact of a step-down in basis for an investment with an unrealized capital loss, it’s important to determine to whom the loss-laden assets are intended to be bequeathed upon the death of the owner, as there are key differences that apply when the intended recipient of assets is a spouse as opposed to a non-spouse.

More specifically, while the same strategy – gifting – can be used in both cases, the ultimate outcome of the strategy will be different depending upon whether the recipient of the asset is a spouse or non-spouse.

Mitigating The Impact Of The Step-Down In Basis For Property Of Married Couples Intended For The Surviving Spouse: Separate Property States

When evaluating near-death basis-planning strategies, it’s important to maximize any potential unrealized losses that a soon-to-be-deceased spouse may own as they approach the end of life. Because, as noted earlier, upon the death of that spouse, the basis of the assets that they transfer to heirs steps to the value at the date of their death… regardless of whether that value is a step higher or a step lower than their own pre-death basis, and the unrealized capital loss, along with its economic value, is generally lost via a step-down in basis.

When it comes to mitigating the potential impact such a step-down in basis may have, the easiest, and often the best approach is to simply gift the loss assets to the intended beneficiary prior to death.

This pre-death gifting strategy works well in a variety of situations but is particularly effective in scenarios where the goal for the surviving spouse in a separate property state is to retain assets upon the death of the first-to-die spouse.

As notably, IRC Section 1015(e), entitled “Gifts between spouses”, states:

In the case of any property acquired by gift in a transfer described in section 1041(a), the basis of such property in the hands of the transferee shall be determined under section 1041(b)(2) and not this section.

And IRC Section 1041(b)(2) plainly states:

The basis of the transferee in the property shall be the adjusted basis of the transferor.

Thus, if one spouse transfers an asset with an unrealized loss to the other spouse, the receiving spouse has only one basis – the original spouse’s basis – and the full unrealized capital loss can be preserved.

Example #4: Earnest, who has chronic health problems, is married to Ida, who is in excellent health. The couple has lived in a separate property state throughout their marriage.

Earnest has an individual brokerage account, and the couple has a joint brokerage account as well. Each account holds a number of different investments, some of which have unrealized gains, and some of which have unrealized losses. The unrealized losses in Earnest’s individual account equal $70,000, while the unrealized losses in the joint account equal $100,000.

If Earnest dies without taking any action, the $70,000 unrealized capital loss in his individual account will disappear as the assets receive a step-down in basis. Similarly, half ($50,000) of the $100,000 unrealized loss in the couple’s joint account would be eliminated via a step-down in basis.

Accordingly, it’s likely advisable for Earnest to consider a more proactive approach. One straight-forward, yet highly effective strategy, is for Earnest to transfer (gift) the positions in the accounts (both his individual account and the joint account) with the unrealized losses to an account in Ida’s own name, while he’s still alive.

In doing so, Ida (the transferee spouse) will retain Earnest’s (the transferor spouse) basis in the investments. Thus, by making such a gift, Earnest can avoid the step-down in basis (i.e., the loss) of $70,000 + $50,000 = $120,000 of unrealized capital losses upon his death, allowing Ida to ‘hang on’ to them for future use by avoiding that step-down in basis.

Notably, it’s important to examine investment accounts granularly to identify potential assets to gift to preserve losses from a step-down in basis. Thanks to the historic bull market run following the financial crisis of 2008, cumulative built-in capital gains are more common than capital losses. However, it’s not the cumulative total of these amounts that matters. It’s the individual positions in the investment accounts.

Any position with an unrealized loss in the taxable account of a terminally ill spouse living in a separate property state should be earmarked for possible transfer to the healthy spouse in order to preserve the potential loss for that position! And despite the market’s good fortune of the past dozen years, most diversified portfolios are likely to have at least some positions at a loss (not to mention losses incurred during the ongoing COVID-19 crisis).

Nerd Note:

While this section of the article focuses on separate property states, the same rules generally apply to the separate property of married couples in community property states. Such separate property typically includes property that was owned separately before marriage, as well as property received separately as a gift or inheritance during marriage. Planning for such separate property (of couples living in community property states) mirrors planning for couples in separate property states.

Critically, while certain basis planning strategies require action well in advance of a person’s death (oftentimes more than a year in advance), the ability to gift assets ‘burdened’ with losses to a ‘healthy’ (likely-to-live-longer) individual, including a spouse, can be done at any time. It can even be done just prior to death (which if not feasible by the individual themselves, can still be done by a competent and legally authorized individual on their behalf, such as the individual’s Attorney-in-Fact, if their Power of Attorney document grants such gifting powers).

Finally, it should be noted that while the strategy of moving loss-laden assets into the healthy spouse’s name can be particularly effective from a tax planning point of view, by doing so, the ill spouse does give up control over those assets. And once the assets are transferred, there may be nothing to prevent the receiving spouse from later transferring those assets (via gift or by bequest upon death) to someone or some entity of which the ill-spouse would not have approved (e.g., a future/second spouse, children from a future marriage, etc.). Thus, when choosing to implement such a strategy, trust is a critical component.

Mitigating The Impact Of The Step-Down In Basis For Property Of Married Couples Intended For The Surviving Spouse: Community Property States

Generally speaking, assets tend to appreciate over time. That makes the community property rules – where a full step-up in basis is received on any community property, regardless of titling – preferential to the separate property rules as a default for post-death basis treatment. But for proactive individuals who wish to try and preserve the full unrealized capital loss of an investment, the community property rules can actually work against them (by forcing a full step-down in basis upon the death of either spouse!).

Accordingly, when it comes to trying to avoid losing the unrealized loss of a community property asset, additional steps may need to be considered. For instance, it may be beneficial to convert the community property to separate property by mutual agreement of the spouses (and under whatever additional procedures are required to do so under state law) should one spouse become seriously ill.

Once such a ‘conversion’ has taken place, the planning for the formerly-community-property-asset-with-a-loss can proceed forward as if it had been separate property to begin with. Of course, by doing so, the ill spouse would again be relinquishing control over their portion of the community assets, which needs to be considered.

Mitigating The Impact Of The Step-Down In Basis For Property Intended For A Non-Spouse Under The Double-Basis Rules

When it comes to preserving the benefits of unrealized capital losses, the tax treatment afforded to spouses is unmatched. But not everyone is married!

Some individuals never get married. Others are married and are later divorced or widowed. And in some cases, married individuals may simply wish to give assets-with-an-unrealized-loss away to persons other than their spouse (e.g., their children, grandchildren, or other heirs).

In such situations, the good news is that there is still a benefit to giving away loss-laden assets (to non-spouse persons) prior to death. The bad news is that the benefits are not as great as when a spouse is the recipient of the same gift.

More specifically, the general rule is that when an asset is gifted, the recipient of the gift takes the previous owner’s basis as their own (i.e., basis is “carried over” from the donor to the recipient). This is the case when an asset with an unrealized gain is given to another individual, regardless of whether the recipient is a spouse or a non-spouse person. In addition, as discussed above, basis is also carried over from one spouse to another when an asset with an unrealized loss is gifted between spouses as separate property.

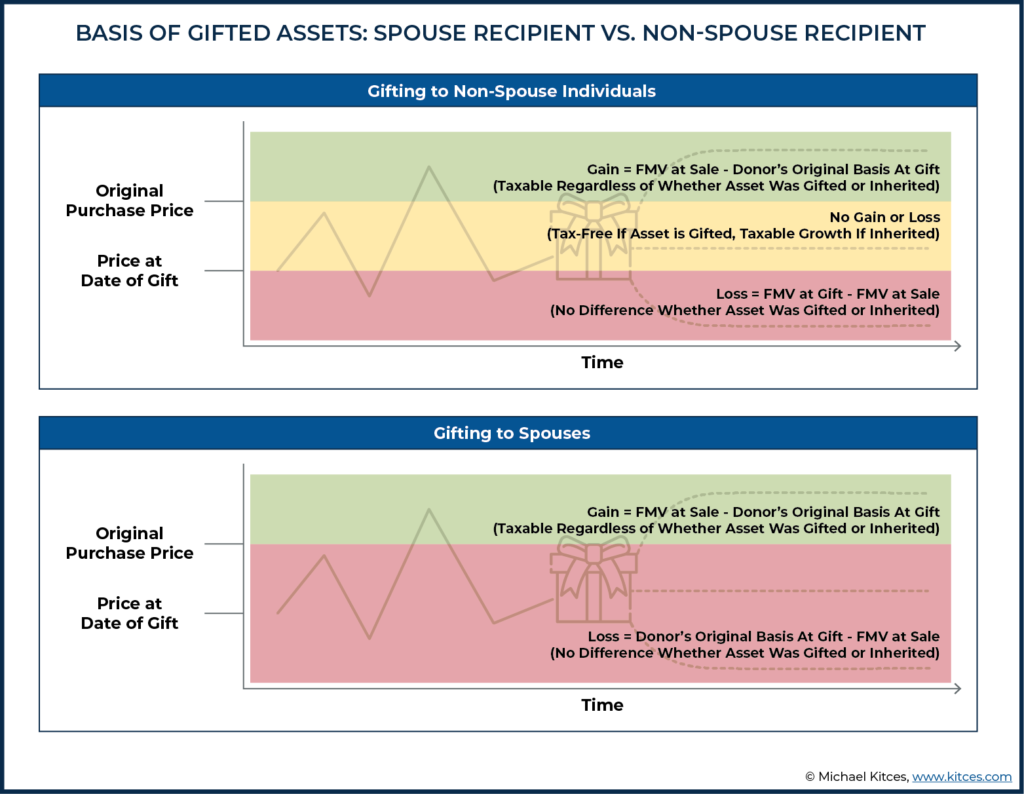

There is, however, an exception to the general carryover basis rule, when an individual transfers property that has a fair market value below its adjusted cost basis (i.e., an unrealized loss) to a non-spouse.

In such situations, under IRC Section 1015(a), the non-spouse recipient of the property is treated as though they have two different basis amounts: one for determining whether there is a capital gain upon the sale of the gifted investment and another for determining whether there is a capital loss upon the same sale!

Under these so-called “double basis” or “split basis” rules, the recipient of the property uses the value on the date of the gift as the basis amount to determine a potential capital loss. By contrast, for purposes of determining a potential capital gain, the recipient of the property uses the donor’s higher original (carried-over) basis.

The ultimate result of these double basis rules is that there are actually three potential tax outcomes for the recipient of property gifted with an unrealized loss when (if) they eventually sell the gifted investment. It all depends upon the value of the gifted asset at the time of the sale.

The three potential consequences for the recipient of the gift can be summarized as follows:

- Scenario # 1: Sale Price Of Gifted Asset Is Less Than The Fair Market Value On The Date Of The Gift – The recipient of the gift is entitled to claim a capital loss equal to the difference between the fair market value on the date of the gift and the sale price (but not the loss from the owner’s original basis).

- Scenario # 2: Sale Price Of Gifted Asset Is More Than The Original Owner’s Basis On The Date Of The Gift (Carryover Basis) – The recipient of the gift will have a capital gain equal to the difference between the sales price of the asset and the original owner’s carried over basis.

- Scenario # 3: Sales Price Of Gifted Asset Is Between The Fair Market Value On Date Of The Gift And Original Owner’s Basis – The recipient of the gift will not owe any capital gains tax (because the value is not higher than owner’s original basis), nor will the recipient be able to claim a capital loss (because the value is not lower than the fair market value on the date of the gift).

As the graphic below shows, the treatment afforded to non-spouse individuals gifted investments with a capital loss is not nearly as strong as the treatment when the same asset is gifted as separate property to a spouse. More specifically, for purposes of claiming a future capital loss, it makes no difference to a non-spouse individual whether they receive an asset with an unrealized loss as a gift or as a bequest upon the death of the owner. In either case, they will ‘only’ be able to claim a capital loss for additional losses incurred after their receipt of the asset.

But on the capital gains side of things, it’s a different story. In essence, by gifting an asset with an unrealized loss to a non-spouse individual, the recipient is able to earn back the original owner’s unrealized loss tax-free (because for capital gains purposes, the recipient’s basis remains the owner’s initial basis). By contrast, if the same individual were to die and leave the same asset to the same non-spouse individual, the asset would be stepped down in basis, and all future gain would be subject to capital gains tax!

Example #5: Rhonda is 70 years old and is terminally ill. As part of her ongoing tax planning, Rhonda transfers $100,000 of HereUGo stock to her son, Max. Rhonda had purchased HereUGo stock several years ago for $180,000, and consequently that was still her basis in the stock at the time of its transfer to Max.

If HereUGo stock continues to decline in value and Max sells it when it is worth “only” $80,000, Max will be entitled to a $20,000 capital loss; the difference between the $100,000 value of the stock on the date of transfer and its ultimate sale price. This is precisely the same outcome had Max inherited the same shares at the same $100,000 fair market value.

If, however, HereUGo has a mild recovery, and Max sells it for $150,000, he can walk away with the full amount. There is no capital gain owed because the sales price is less than the $180,000 Rhonda initially paid for the investment (Max cannot, however, claim any capital loss, because the sales price is more than the $100,000 value of the HereUGo stock on the date of its transfer).

Consider, now, what would have happened if Max had inherited the same shares at the same $100,000 fair market value. Instead of a ‘wash’ of no gain/no loss, the basis would have been stepped-down to the $100,000 fair market value, and Max would have incurred a capital gain of $50,000.

Finally, if HereUGo stock has a tremendous recovery, and Max sold it when it had increased in value to $200,000, he would owe capital gains tax on $30,000 of gain; the difference between the sales price of $210,000 and Rhonda’s original, carried over basis of $180,000.

By contrast, if the shares had been inherited, the basis would have been stepped-down to the $100,000 fair market value, and Max would have incurred a capital gain of $110,000 (as opposed to the $30,000 of gain he’d have by receiving the same shares via gift). Thus, by gifting the asset to Max instead of dying and leaving it to him, Rhonda allows Max to earn up to her $80,000 unrealized capital loss on HereUGo stock back, tax-free!

No one likes to see their investments go down in value, but if an individual has a diversified portfolio and rebalances with any sort of regularity, they are almost guaranteed to have positions with a loss at most, if not all, times. When such positions are held within retirement accounts, such losses are of no concern (at least from a tax-planning point-of-view), as the tax-deferred nature of retirement accounts eliminates any tax benefit that would otherwise be associated with the loss.

But if the same loss-burdened position is held in a taxable account, it becomes a different story. All of a sudden, that loss has real economic value, which should be preserved to the extent possible. There are a variety of ways in which planners may choose to do so, but one of the simplest and most effective solutions is to engage in a little Red Hot Chili Peppers planning and…

Give it away, give it away, give it away, give it away now!

It’s that simple. By ‘giving it away now’, instead of dying with an asset with an unrealized capital loss, some economic value related to the loss can be preserved.

In the case of one spouse gifting separate property to the other spouse, gifting the asset allows maximum economic value to be retained as the recipient-spouse picks up the donor-spouse’s basis for purposes of calculating future gains and losses (upon the sale of the asset).

And while the treatment for non-spouse recipients of similar gifts isn’t as strong, the double-basis rules still allow such individuals to earn back the donor’s capital loss on the position tax-free.

Ultimately, the key point is that even though the Federal estate tax is no longer an issue for most individuals, income taxes, including taxes on capital gains, remain a real problem. Accordingly, planning to mitigate such taxes is an important part of any estate plan. Doing so not only requires trying to maximize the step-up in basis for assets of an individual that have an unrealized gain, but also minimizing the step-down in basis of assets of the same individual by preserving the economic value of such losses to the extent possible under the law.