Executive Summary

For many financial advisors, helping affluent clients with charitable planning strategies is a common objective, particularly those who have more than enough to satisfy their own retirement and family goals and also wish to make substantial charitable contributions that will help others in need. Which in recent years has become even more flexible, as the Tax Cuts and Jobs Act increased the percentage-of-AGI limit on cash contributions from 50% to 60%, and the CARES Act (as extended by the Coronavirus Stimulus Act) further increased the limit from 60% to 100%(!) of AGI, making it possible for the most charitable inclined clients to fully offset their income and reduce their tax bill to zero! Yet as it turns out, reducing one’s tax bill all the way to nothing actually produces tax savings at the lowest tax brackets… such that in the end, the new 100%-of-AGI charitable giving limit actually is not such a great deal after all!

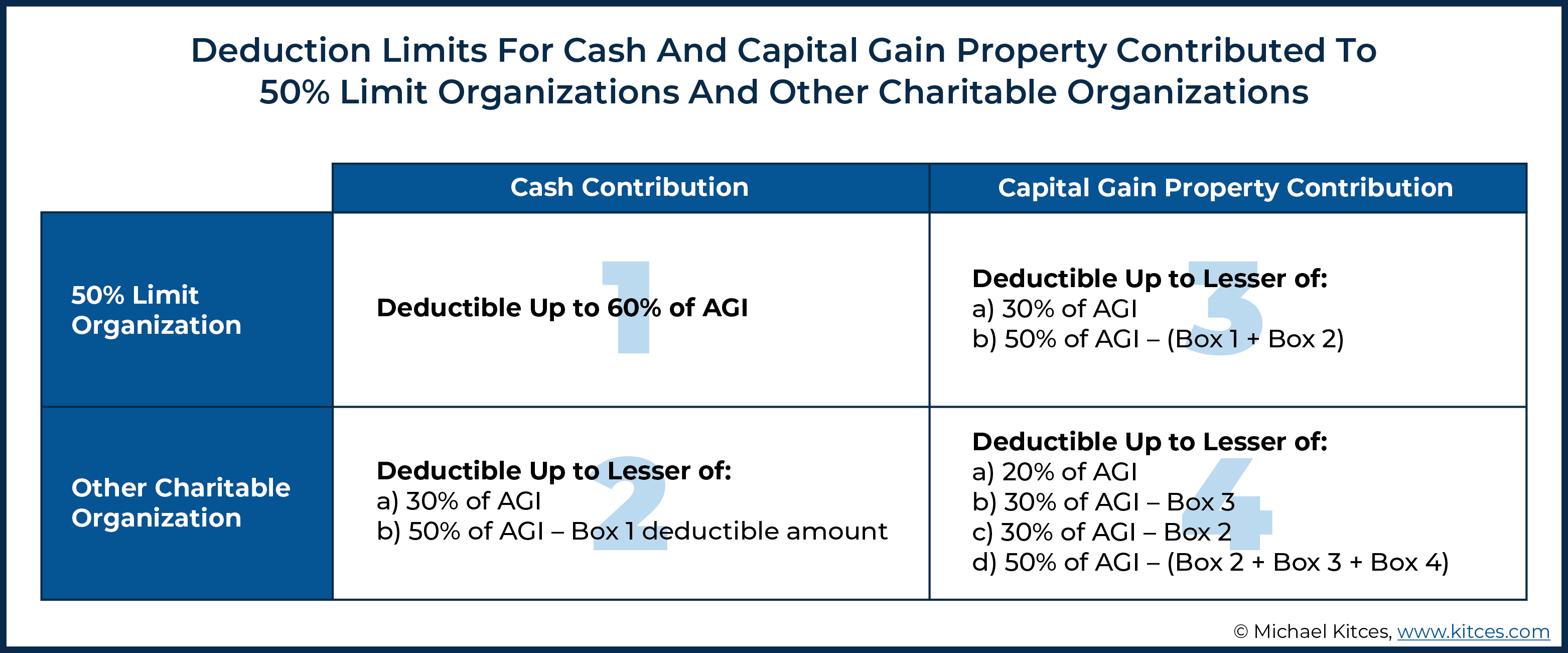

Taxpayers who itemize deductions on their Federal income tax return can generally deduct contributions made to qualifying charitable organizations up to some percentage of their Adjusted Gross Income (AGI), traditionally ranging from 20% to 50% of AGI, and is dictated by such factors as the nature of the asset donated (e.g., cash gifts vs Capital Gain property) and the type of charitable organization receiving the gift (e.g., “50% Limit Organizations”, which include churches, educational institutions, hospitals, government entities, and public charities; and “Other Charitable Organizations” which include any charity not considered a 50% Limit Organization).

As a result, charitable contributions can be categorized into four primary groups: 1) cash contributions to 50% Limit Organizations, 2) cash contributions to Other Charitable Organizations, 3) Capital Gain property contributions to 50% Limit Organizations, and 4) Capital Gain property contributions to Other Charitable Organizations. And when contributions in a given year overlap between multiple categories, there is a specific order of operations to be employed, which first prioritizes cash over Capital Gain property contributions, and then 50% Limit Organizations over Other Charitable Organizations.

With the CARES Act of 2020, though, a new 100%-of-AGI limit on deductions for category 1 – certain “qualified” cash contributions to charities – was implemented (and extended through 2021 with the passage of the Consolidated Appropriations Act) to provide some additional incentives for charitable giving in the face of the financial impact that COVID-19 has had on Americans. Which means that taxpayers can technically offset all of their taxable income with charitable contribution deductions, resulting in a tax bill of $0!

Still, though, the fact that one can take charitable contribution deductions up to 100% of their income doesn’t necessarily mean it’s a good deal to actually do so. Because it is often simply be better for a taxpayer who normally finds themselves in a higher ordinary income tax bracket to go ahead and actually pay taxes on a portion of their gross income at lower tax rates (and not offset it with a charitable deduction), thereby preserving their charitable giving (or at least their charitable deduction) for future years when their rates may be higher again. And by spreading charitable contributions out over multiple tax years (and leveraging the five-year carryforward allowances for unused charitable contribution deductions), they can effectively offset income in years when they would be subject to higher tax rates, thereby producing a greater total tax benefit.

Ultimately, the key point is that while the new CARES Act (now extended by the Coronavirus Stimulus legislation) makes it possible to claim Qualified Contribution deductions (with 100%-of-AGI limits) and zero out one’s tax bill, in practice it is rarely a good idea to do so. As while there is a small group of ultra-high-income individuals who can occasionally still benefit from using the increased deduction limits they provide, in most cases, high income donors are better served to stretch out or carry over a portion of their charitable giving (and charitable deductions) across multiple high income years instead. Though for financial advisors who have clients who won’t necessarily benefit from the provision, simply being able to explain why the better option would be not to take potential deductions as soon as possible can be a valuable service, in and of itself!

Charitable planning is a major goal for many affluent clients, who have accumulated enough financial assets that they have satisfied retirement and family goals… and have enough left over to contribute to others as well.

And while many individuals looking to make significant charitable contributions may do so primarily for altruistic purposes, maximizing the potential tax benefits of such contributions is often an important secondary objective… to the point that Congress actually limits the tax benefits available for charitable giving in any particular year through various percentage-of-AGI limitations on charitable tax deductions.

These limits on the tax benefits of charitable giving were temporarily lifted last year, though, with the introduction of a new 100%-of-AGI limit on certain “qualified” cash contributions to charities. Except as it turns out, just because one can donate up to 100% of their income for a tax deduction doesn’t necessarily mean it’s a good deal to do so!

Limitations On Charitable Contribution Tax Deductions Based On Type Of Charity And Type Of Asset

In general, taxpayers who itemize deductions on their Federal income tax returns are able to claim a deduction for contributions made to qualifying charitable organizations. However, while such deductions are typically allowed, they are generally limited to no more than a specified percentage of a taxpayer’s Adjusted Gross Income (AGI).

In fact, there are actually multiple percentage-of-AGI limitations that apply to charitable giving tax benefits, which are generally based on two key factors: 1) the type of charity (as discussed further, below) to which contributions are made, and 2) the type of asset that is donated to the charity (e.g., cash or Capital Gain property).

And notably, because donors may give more than one type of property to more than one type of charity in any particular year, a series of ‘ordering’ rules apply to determine the priority order in which deductions are taken and applied to their respective AGI limits across different categories.

Cash Contributions Made To 50% Limit Organizations

The first category of common charitable contributions includes cash gifts made to aptly named “First Category Organizations,” as described in IRC Section 170(b)(1)(A), which are more commonly known as “50% Limit Organizations.”

Common examples of 50% Limit Organizations include churches and other houses of worship, educational institutions, hospitals, the Federal and/or state and local governments, and publicly supported charities organized for charitable, religious, scientific, literary, or educational purposes, or for the prevention of cruelty to children or animals.

So why are these organizations called ‘50% Limit Organizations’? It’s simple.

In general, per IRC Section 170(b)(1)(A), cash contributions made to 50% Limit Organizations are deductible to the extent that they do not exceed 50% of a taxpayer’s AGI.

Nerd Note:

IRC Section 170(b)(1)(G), created by the Tax Cuts and Jobs Act of 2017, temporarily increases the AGI limit from 50% to 60% for such contributions, effective through 2025. However, even though the limit to such charities is currently 60%-of-AGI, they are still referred to as “50% limit” (and not “60% limit”) organizations.

Charitable contributions in excess of their respective deduction limits can generally be carried forward and deducted for up to five years.

Example #1: Alice is a single taxpayer who has $200,000 of AGI for 2021. In June of 2021, Alice makes a cash contribution of $150,000 to her donor-advised fund, a 50% Limit Organization.

Here, Alice will be allowed to deduct up to 60% of her 2021 AGI, which will be equal to 60% x $200,000 = $120,000.

Since Alice’s $150,000 donation was greater than this amount, the excess $150,000 (Alice’s contribution) – $120,000 (60% of her AGI) = $30,000 of Alice’s 2021 cash contribution will be disallowed as a 2021 deduction (but will be eligible to be carried forward for up to five years for future use).

Cash Contributions To Other Charitable Organizations

The second category of charitable contributions includes cash gifts made to any charitable organization not included in the list described under IRC Section 170(b)(1)(A). In other words, any charity that is not a 50%-limit organization. Deductions to these organizations for cash contributions are generally limited to 30% of a taxpayer’s AGI instead.

Example #2a: Harry is a single taxpayer who has $300,000 of AGI for 2021. He makes a contribution of $100,000 to his favorite charity, though that charity does not qualify as a 50% Limit Organization.

Accordingly, Harry will be able to claim a deduction for a charitable contribution of his $300,000 AGI × 30% limit = $90,000 for the current year.

Since Harry donated $100,000, but his 30%-of-AGI limit was only $90,000, he will also have a carryforward deduction of $100,000 (his total contribution) – $90,000 (30% of Harry’s AGI) = $10,000 that he can use for up to the next five years.

If a taxpayer makes cash contributions to both a 50% Limit Organization and a non-50% Limit Organization in the same calendar year, an additional rule applies.

More specifically, the deduction taken for the cash contribution made to the non-50% Limit Organization is further limited to no more than 50% of the taxpayer’s AGI, when added to the already-allowed cash contribution to the 50% Limit Organization (as unlike the 60%-of-AGI cash contribution limit under the Tax Cuts and Jobs Act, this coordinated contribution limit remains a 50%-of-AGI limitation!).

Example #2b: Matt is a single taxpayer who has $300,000 of AGI for 2021. During the year, he makes a cash contribution of $100,000 to a charitable organization that qualifies as a 50% Limit Organization. Additionally, Matt makes a cash $75,000 contribution to a charitable organization that does not qualify as a 50% Limit Organization.

While Matt’s $75,000 cash contribution to the non-50% Limit Organization is less than 30% × $300,000 = $90,000 of his AGI, and collectively, his $100,000 + $75,000 = $175,000 of cash contributions are less than 60% × $300,000 = $180,000 of his AGI, he cannot claim a deduction for the $175,000 total cash contributions.

Notably, 50% of Matt’s AGI is 50% x $300,000 = $150,000. Therefore, when added to the $100,000 of cash contributions Matt made to the 50% Limit Organization, the $75,000 of cash contributions he made to the non-50% Limit Organization will only be deductible to the extent they do not exceed that $150,000 amount.

Accordingly, after using the first $100,000 of his charitable contribution limit for the donation to a 50% Limit organization, Matt will only be able to take a deduction for $150,000 – $100,000 = $50,000 of his cash contributions to the non-50% Limit Organization this year. Since Matt actually donated $75,000 to the latter, he will have a carryforward deduction for the excess $75,000 - $50,000 = $25,000 that can be used over the next five years.

A key takeaway from Example 2b, above, is that, in terms of the order of operations, cash contributions to 50% Limit Organizations get counted first. After that, cash contributions to other charitable organizations get counted (subject to their own 30% limitation) and are only allowed as limited by either the 30% deduction limit, or to the extent that there is still ‘room’ left below 50% of a taxpayer’s AGI, whichever is lower.

Contribution Of Capital Gain Property To 50% Limit Organizations

While cash may be the easiest way for taxpayers to make contributions to support the charitable causes that are most important to them, it’s certainly not the only way that such contributions can be made (and, as a matter of practice, is rarely the most tax-efficient way). More specifically, taxpayers have the option of donating Capital Gain property to charitable organizations as well.

Such property can consist of anything from a work of art to a piece of real estate. Nevertheless, the most common type of Capital Gain property contributed to charitable organizations is appreciated securities (i.e., investment holdings), such as stocks, bonds, mutual funds, and ETFs.

Accordingly, the third category of charitable contributions includes these various Capital Gain assets – defined, essentially, as assets for which a long-term capital gain would be generated upon a sale of those assets – that are contributed to a 50% Limit Organization. For these contributions of Capital Gain property to a 50% Limit organization, the maximum deductible amount for a single year is equal to 30% of a taxpayer’s AGI.

Example #3a: Helen is a single taxpayer who has $400,000 of AGI in 2021. She makes a Capital Gain property contribution of appreciated securities of $200,000 to her favorite charity, which qualifies as a 50% Limit Organization.

Accordingly, Helen will be able to claim a deduction for a charitable contribution of up to $400,000 (AGI) × 30% = $120,000 for the current year.

Because she donated more than the available AGI limit, Helen will only be able to deduct up to the $120,000 threshold, and will thus also have a carryforward deduction of $200,000 (total contribution) – $120,000 (deduction limit) = $80,000 that can be used over the next five years.

It’s important to distinguish Capital Gain property contributed to a charitable organization from the broader category of non-cash contributions. Notably, Capital Gain property generally does not include clothing, furniture, and other household goods, as these items tend to depreciate in value after purchase. Thus, if sold at Fair Market Value, such property would not result in a long-term capital gain. Accordingly, contributions of such items to 50% Limit Organizations are subject to the ‘regular’ 50% limit (as the TCJA only temporarily increased the limit to 60% for cash contributions made to such organizations) In situations where assets have a fair value lower than their basis (e.g., a sale would not produce a long-term capital gain), the AGI limit for such contributions made to 50% Limit Organizations is no longer 30%-of-AGI but reverts back to 50% of a taxpayer’s AGI instead. Additionally, a taxpayer may make an election to treat contributions of Capital Gain property as non-Capital Gain property. In such instances, the gross amount of the deduction is equal to ‘only’ the cost basis of the contributed assets (i.e., appreciation is ignored) instead of its market value (as would be the case for Capital Gain property contributions), and the AGI limit is again increased from 30% of the taxpayer’s AGI to 50% of the taxpayer’s AGI.

Nerd Note:

If a taxpayer makes both cash and Capital Gain property contributions to a 50% Limit Organization in the same calendar year, an additional limitation applies.

More specifically, the deduction for the Capital Gain property contributions, when added to the cash contributions, cannot exceed 50% of the taxpayer’s AGI (or 30% of their AGI, if less, as noted above).

Example #3b: Mike is a single taxpayer who has $400,000 of AGI in 2021. During the year, he makes a cash contribution of $110,000 to a charitable organization that qualifies as a 50% Limit Organization. Additionally, Mike makes a $150,000 Capital Gain property contribution to the same charitable organization.

If Mike made only a Capital Gain property contribution, then the maximum potential deduction for his contribution for which he would be eligible would be 30% × $400,000 (Mike’s AGI) = $120,000 (and the last $30,000 of his $150,000 contribution would be carried forward).

However, Mike cannot claim a charitable deduction for Capital Gain property contributions of $120,000 because his cash contributions, in effect, reduce the amount that he can deduct for his Capital Gain property contribution.

Notably, 50% x $400,000 (Mike’s AGI) = $200,000. Therefore, when added to the $110,000 cash contribution Mike made in the same calendar year, the Capital Gain property contribution of $200,000 will only be deductible to the extent that they do not exceed the 50% limit amount remaining after taking into account the cash contribution.

Accordingly, Mike will only be able to take a deduction for $200,000 (50% limit) – $110,000 (cash contribution amount) = $90,000 of his Capital Gain property contributions this year.

He will have a carryforward deduction of $150,000 (original Capital Gain property donation) – $90,000 (Capital Gain property contribution deduction used this year) = $60,000 that can be used over the next five years.

A key takeaway from Example 3b, above, is that, in terms of the order of operations, cash contributions to 50% Limit Organizations again get counted first. After that, Capital Gain property contributions to 50% Limit Organizations get counted (subject to their own 30% limitation) and are only allowed to the extent that there is still ‘room’ left below 50% of a taxpayer’s AGI.

Contribution Of Capital Gain Property To Other Charitable Organizations

Of course, Capital Gain property can also be contributed to charitable organizations that do not qualify as 50% Limit Organizations, which are the fourth category of charitable contributions. In such cases, the maximum amount that can be deducted as a charitable contribution in any single tax year is limited to 20% of a taxpayer’s AGI.

And, as it might not surprise you to learn, Capital Gain property contributions made to non-50% Limit Organizations are at the back of the pack when it comes to the ordering rules of what’s deductible as a charitable contribution, as can be seen in the graphic below. Which means such charitable deductions are not only subject to the 20%-of-AGI limit but also subject to a slew of other limits as well when those donations are stacked on top of any/all other charitable giving for that tax year.

Qualified (Cash) Contributions Allow 100%-of-AGI Deductions For Charitable Contributions Through 2021

While the deduction limits for charitable contributions discussed above are the general limits that apply to taxpayers’ contributions to qualifying charitable organizations, the CARES Act of 2020 created “Qualified Contributions,” which permit certain cash contributions to certain charities to be deducted up to 100% of a taxpayer’s AGI.

Thus, a taxpayer who makes enough contributions that are eligible to be treated as Qualified Contributions can completely offset their entire taxable income with charitable contribution deductions for the year, resulting in a $0 tax bill!

And while initially, the CARES Act authorized Qualified Contributions for 2020 only, in December of 2020, the Consolidated Appropriations Act extended this 100%-of-AGI tax break through 2021. Thus, clients can still take advantage of this tax benefit.

In order to qualify, though, per Section 2105(a)(3) of the CARES Act, Qualified Contributions must be made in cash and must be made only to qualifying 50% Limit Organizations during 2020 or 2021 (per the extension provided by the Consolidations Appropriations Act).

Qualifying 50% Limit Organizations for the purpose of these rules are all such 50% Limit organizations except so-called Supporting Organizations (organized under IRC Section 509(a)(3)) and Donor Advised Funds. Provided a taxpayer’s contribution meets these requirements, they may elect (but are not required) to treat the contribution as a Qualified Contribution, which is deductible up to 100% of the taxpayer’s AGI (less any other charitable contribution deductions that have already been calculated).

Example #4a: Shai is a single taxpayer with $400,000 of AGI for 2021. He decides to make a $400,000 contribution, in cash, to his local house of worship.

Because Shai made a cash contribution to a 50% Limit Organization, he may elect to treat the contribution as a Qualified Contribution and take the entire amount as a deduction, leaving him with $400,000 (AGI) – $400,000 (Qualified Contribution Deduction) = $0 of taxable income, and thus a $0 tax bill!

However, as noted earlier, these 100%-of-AGI deductions are “less any other charitable contribution deductions that have already been calculated.” Essentially, cash contributions to 50% Limit Organizations come first in the charitable contribution deduction order of operations, and Qualified Contributions actually come last. Though in practice, this is actually favorable and means these Qualified Contributions can be added on top of any other charitable contribution deductions allowed under the ‘normal’ rules.

Example #4b: Jolene was a single taxpayer with $300,000 of AGI for 2021. She decides to make a cash contribution of $150,000 to a local healthcare clinic and a $50,000 Capital Gain property contribution to a local food bank. Both entities qualify as 50% Limit Organizations.

Normally, despite making $200,000 of total charitable contributions, Jolene would be eligible for a deduction of 50% × $300,000 (Jolene’s AGI) = $150,000, which, under the charitable contribution deduction ordering rules, would be completely filled up by Jolene’s $150,000 cash contribution. Thus, Jolene’s $50,000 Capital Gain property contribution would have to be carried over for use in future years.

But, in 2021, thanks to the extension of the CARES Act Qualifying Contribution allowance, Jolene could receive a charitable contribution deduction for the full $150,000 (cash) + $50,000 (Capital Gain property) = $200,000 value of her contributions. This is because Jolene’s $150,000 cash contributions were made to qualifying 50% Limit Organizations, and the contribution was made in 2021, which means she can treat the contributions as Qualifying Contributions.

Accordingly, deductions attributable to her other contributions (i.e., her Capital Gain property contributions) would be calculated first, with the deduction attributable to the Qualifying Contributions added on top.

Thus, Jolene can claim a deduction for the $50,000 of Capital Gain property contributions (because the $50,000 total is less than 30% × $300,000 (AGI) = $90,000) under the ‘normal’ rules.

Then, via her election to treat the remaining $150,000 of cash contributions as Qualifying Contributions, Jolene would be eligible to take a deduction for that amount as well, because her total deduction limit would be $300,000 (100% of AGI) - $50,000 (prior contribution to Capital Gain property) = $210,000, which is more than enough to accommodate her $150,000 cash contribution.

The end result… A combined charitable contribution deduction of $50,000 (Capital Gain property) + $150,000 (cash) = $200,000 for 2021!

When it comes to the technical terminology used for various tax breaks for contributions to charities, Congress likely could not have been more confusing if they had tried! Notably, Qualified Charitable Distributions (QCDs) have been around since the Pension Protection Act of 2006 and allow IRA owners (and IRA beneficiaries) who are 70½ or older to transfer funds directly from their IRA (or inherited IRA) to qualifying charitable organizations without including the distribution in their AGI. Meanwhile, Qualified Charitable Contributions are the technical name for charitable contributions eligible for the CARES Act-created above-the-line deduction of $300 (applicable in 2020 and 2021), which can be used by individuals who donate to charity and don’t itemize their deductions. Finally, ‘plain old’ Qualified Contributions are the official name for cash contributions to qualifying charities in 2020 or 2021 that are subject to the special up-to-100%-of-AGI limit when reported as itemized deductions.

Nerd Note:

The Misplaced Allure Of A $0 Tax Bill

On the surface, for those individuals who are very charitably inclined, the ability to make (cash-based) charitable contributions in 2021 that, along with other deductions, are large enough to completely eliminate a 2021 tax liability (i.e., produce a $0 tax bill) sounds pretty enticing.

Indeed, for an affluent taxpayer who, year after year, has a tax bill in the tens or even hundreds of thousands of dollars (or more), a $0 tax bill sure may look especially nice and appealing.

But looks can be deceiving…

The reason is that if a high-income individual makes enough charitable contributions to reduce their taxable income (and thus, their tax bill, as well) to $0, they will be using their charitable contributions to offset income that would be taxed at each potentially applicable income tax rate. From the top tax bracket… all the way down to the bottom.

For instance, if the taxpayer would normally find themselves in the 35% ordinary income tax bracket (absent the charitable contribution deductions), then using the special charitable contribution options for 2021 and reducing their taxable income to $0 (using qualified contributions) would mean not only offsetting income that would have otherwise been taxed at the 35% marginal rate, but also offsetting the income that would have been taxed at the 32% rate, 24% rate, 22% rate, and even the 12% and 10% lowest ordinary income tax brackets. Which effectively diminishes the value of the charitable donation by the end, when it is ‘only’ producing savings at a 10% tax rate!

For individuals interested in maximizing the tax benefits of charitable contributions, an alternative approach would almost undoubtedly produce greater tax savings. Because in the end, it’s often better for a taxpayer who normally finds themselves in the 35% ordinary income tax bracket to go ahead and actually pay taxes on a portion of their gross income at a tax rate of only 10% or 12%, and preserve their charitable giving (or at least their charitable deduction) for future years when their rates may be higher again (e.g., revert back to their ‘normal’ 35% rate).

This doesn’t necessarily mean a taxpayer should, or needs to, reduce their total giving to charitable organizations. Rather, it might simply benefit them to spread such charitable contributions over multiple years.

By doing so, the total amount of charitable contributions can be used to offset income… but stretched out to offset income in the years that it would be subject to higher tax rates, thereby producing a greater total tax benefit!

Example #5: Beth and Benny are a married couple in their 50s who, after accounting for itemized deductions (e.g., their State And Local Tax deduction) other than those for charitable contributions, have projected taxable income for 2021 of $500,000. Thus, they find themselves squarely in the 35% ordinary income tax bracket.

Beth and Benny have done a good job saving for their goals and, in light of both their personal good fortunes and understanding of the significant challenges many families are currently dealing with, they have decided to make a substantial contribution to their local food bank. After some discussion, the couple settles on donating one year’s worth of income, a $500,000 total contribution.

However, in light of the size of their contribution, Beth and Benny would like to try and maximize their tax savings in order to minimize the after-tax cost of the contribution.

In 2021, a married couple who file a joint return with $500,000 of ordinary taxable income will have an income tax bill of $124,089 (after applying the various graduated income tax brackets… or just take my word on this calculation, okay?).

Accordingly, a charitable contribution of $500,000 that reduces taxable income to $0 in 2021 will result in Federal income tax savings of $124,089.

Thus, if Beth and Benny decided to make their charitable contribution in such a fashion, the total after-tax ‘cost’ of the contribution would be $500,000 (total charitable contribution amount) – $124,089 (total tax liability) = $375,911.

In 2021, the 12% ordinary income tax bracket for joint filers ends at $80,250. Suppose, then, that instead of making one $500,000 charitable contribution in 2021, Beth and Benny made a charitable contribution that would be sufficient to leave them in the 12% tax bracket. This would entail making a $500,000 (current taxable income, before charitable contributions) - $80,250 (12% tax bracket threshold) = $419,750 charitable contribution in 2021, and a subsequent $80,250 charitable contribution in 2022 (to add up to their total giving goal of $500,000).

In making a $419,750 charitable contribution in 2021, the couple would have $80,250 of taxable ordinary income in 2021, resulting in a $9,232 tax bill (a blend of the 10% and 12% tax brackets). Accordingly, the 2021 charitable contribution of $419,750 will save the couple $124,089 (original tax liability with $500K taxable income) – $9,232 (new tax liability with $80,250 taxable income) = $114,857.

Meanwhile, the remaining $500,000 (total contribution amount target) - $419,750 (2021 contribution) = $80,250 charitable contribution that they can make in 2022 will reduce the couple’s taxable income next year from $500,000 to $419,750. At $419,750 of taxable ordinary income, Beth and Benny would have a Federal income tax bill of $96,001 in 2022. Thus, the $80,250 charitable contribution would produce a $124,089 (tax liability on $500K taxable income) – $96,001 (tax liability on 419,750 taxable income) = $28,088 tax savings.

The end result is that by ‘pushing’ $80,250 of Beth and Benny’s charitable contribution from 2021 to 2022 (and deliberately keeping themselves in the 12% tax bracket in 2021), the couple’s combined tax savings goes from $124,089 (tax savings with $0 taxable income in 2021) to $114,857 (tax savings with $80,250 taxable income in 2021) + $28,088 (tax savings with $419,750 income in 2022)= $142,945!

That’s $142,945 – $124,089 = $18,856 of additional tax savings! And all by simply shifting about 16% of the total charitable contribution to the next tax year and not taking their income and 2021 tax bill all the way down to $0!

Treatment As A Qualified Contribution Is A Taxpayer Election (It’s Optional!)

While using the Charitable Contribution provision to take income all the way down to $0 may not make much sense from a tax planning point of view for most clients, it generally shouldn’t discourage them from making substantial charitable contributions either.

Fortunately, though, charitable contributions – even (and especially!) those that are made in cash to qualifying 50% Limit Organizations and are eligible for the 100%-of-AGI limit – don’t have to be treated as Qualified Contributions. Instead, as noted earlier, an election must be made to treat those otherwise-not-deductible ‘excess contributions’ as such.

Accordingly, taxpayers who want to make substantial cash charitable contributions in 2021 (because they want to make those contributions this year) can simply avoid treating some or all of those amounts as Qualified Contributions by not making the election to do so.

Absent such an election, the ‘regular’ charitable contribution deduction rules will apply, reducing the ability of the taxpayer to fully offset their income for the year, and thereby increasing the likelihood of carryover deductions for future years (which may offset income tax at higher income tax rates in those future years).

For instance, recall Beth and Benny from Example #5, who had $500,000 of AGI, and who made $500,000 of cash contributions to qualifying 50% Limit Organizations. Further recall that, as illustrated, from a tax-planning point of view, it did not make sense for the couple to offset income at lower brackets, such as the 10% and 12% rate, by contributing the full $500,000.

Instead, it was suggested that, rather than making the full contribution of $500,000 in 2021, Beth and Benny might want to split their contributions over two years, thereby allowing them to receive a greater net tax benefit (because by splitting the contribution over two years, they would be able to offset income that would collectively be taxed at higher rates).

Suppose, however, that Beth and Benny really want to make the $500,000 contribution in 2021, but they still want a bigger bang for their buck when it comes to their taxes.

Well… No problem!

Instead of using the Qualified Contribution provision for the 100%-of-AGI limit, Beth and Benny can simply treat their cash contribution as a ‘regular’ cash contribution subject to the currently standard 60%-of-AGI limit. Accordingly, they would be allowed a charitable deduction of ‘only’ 60% × $500,000 = $300,000. The remaining $500,000 – $300,000 = $200,000 of charitable contributions would have to be carried forward and (potentially) deducted in (up to five of the next) future years. (And a $300,000-in-2021-and-$200,000-in-2022 split is even more tax-efficient than their prior $419,750-in-2021-and-$80,250-in-2022 approach.)

Alternatively, Beth and Benny could elect to treat only a specified amount of their charitable contributions as Qualified Contributions. In other words, the decision to claim “excess” cash contributions above the 60%-of-AGI threshold as Qualified Contributions is not an all-or-none requirement; it can be in any amount desired.

Furthermore, this election does not need to be made at the time of contribution but, rather, on the tax return. Thus, Beth and Benny can work with their CPA or other tax professional to make the best decision once they know the exact amount of all their other income, deductions, credits, etc., to fit themselves precisely into the tax bracket they wish to remain in (and carry forward the rest).

A word of warning for those advisors who also prepare tax returns (and those advisors who work closely with the client tax professionals): upon a cursory review of some of the most common professional tax filing software programs, it appears that most of them designate any and all cash contributions made to 50% Limit Organizations as Qualified Contributions by default. Accordingly, it appears that tax professionals will have to actively indicate how much of a client’s eligible cash contributions are not supposed to be treated as Qualified Contributions. In the craziness of a normal tax season, things like this are often missed… and this is not going to be a normal tax season... and this is a brand new provision. In short, if you’re preparing tax returns, make sure you carefully review how clients’ cash contributions are deducted. And if you’re not preparing tax returns, but you know that your client intends to deduct cash contributions, make sure that you emphasize to the client (or to their tax professional) that they carefully review their charitable contribution deductions before signing off on the return.

Nerd Note:

(Limited) Scenarios Where 100%-of-AGI Qualified Contributions Can Still Make Tax-Planning Sense

While, in general, the Qualified Contribution provision won’t give clients the biggest tax bang for their buck, there are, as always, exceptions to the rule.

For instance, clients with ultra-high-income may be able to benefit substantially from this provision. And while the exact income figure can vary based on what type of asset – besides cash – are being contributed to which type of charitable organizations, the most obvious group of ultra-high-income clients who can benefit from this provision are single clients with income in excess of about $1.3 million, and married couples who file joint returns with income in excess of about $1.55 million.

Why these clients? Why those dollar amounts? In short, the answer is explained by little more than a rudimentary math exercise.

As we know, the general rule is that taxpayers can deduct cash contributions made to 50% Limit Organizations up to 60% of their AGI. Furthermore, in 2021, the top 37% Federal income tax bracket ‘kicks in’ at $518,401 for single filers and $622,051 for married couples filing joint returns.

Accordingly, single filers can have up to $518,401 (37% income tax bracket threshold for single filers) ÷ 40% (1 – 60%, the 50% Limit Organization deduction limit) = $1,296,003 of income before they are unable to offset all of their income tax at the highest 37% tax bracket using the ‘regular’ term contribution rules.

Similarly, married taxpayers who file a joint return can have up to $622,051 (37% income tax bracket threshold for married filers) ÷ 40% (1 – 60%) = $1,555,125 before the same would be true.

Example #6: Graham is a single taxpayer with $2 million of AGI who is extremely charitably inclined.

Under the ‘normal’ rules, Graham would be eligible to take a maximum deduction of 60% × $2 million = $1.2 million for cash contributions to 50% Limit Organizations.

If Graham were to make contributions sufficient to fill up this ‘allowable’ bucket, it would still leave him with $2 million (his AGI) – $1.2 million (allowed deductions for cash gifted to 50% Limit Organizations) = $800,000 of taxable income.

Thus, $800,000 (total taxable income) – $518,401 (single filer threshold for the 37% tax bracket) = $281,599 of his income would still be taxed at the highest 37% marginal income tax rate for 2021.

However, if Graham wanted to, he could contribute an additional $281,599 of cash to qualifying 50% Limit Organizations in 2021 and elect for only those contributions to be treated as Qualifying Contributions. By doing so, Graham would reduce his taxable income to $518,401, the 37% income tax bracket threshold for single filers, thereby preventing any of his income from being taxed at the highest 37% rate. (And any remaining charitable carryforward would also still be available to apply against 37% tax rates in the future, too.)

Ultra-high-income clients are not the only ones who should think about making use of Qualifying Contributions, though. Other potential benefactors include business owners who can utilize the Qualified Contribution provision to lower taxable income enough in order to be able to receive a (larger) Qualified Business Income (QBI) deduction.

Critically, unlike all other deductions, which are keyed to a taxpayer’s AGI, the QBI deduction phaseouts are instead based on taxable income. Thus, a larger charitable contribution can reduce taxable income to the point where a bigger QBI deduction may be possible!

How The Biden Administration May Impact Tax Planning With Charitable Deductions Caps

For individuals like Graham in Example 6, giving in such a manner (i.e., leveraging deductions for Qualifying Contributions in conjunction with deductions for ‘normal’ contributions) in 2021 may make even more sense given the incoming Biden Administration.

Notably, President-elect Biden has proposed capping the value of itemized deductions at a maximum of 28%. While it is possible that tax legislation could be passed later this year to retroactively impose such a restriction for 2021, it’s more likely that any such changes (if they do actually happen in the first place) would be effective in future years starting in 2022.

Accordingly, individuals concerned about this potential limitation on the benefits of future itemized deductions may wish to front-load deductions in 2021, when their full value will most likely be received.

For most individuals, the ability to deduct up to 60% of AGI for cash contributions made to 50% Limit Organizations is more than enough to ensure that any contributions made during the year will be fully deductible on the individual’s return.

However, from time to time, individuals may be generous to the point where such limits no longer capture all of their contributions.

In such instances, Qualified Contributions can help such individuals get around the ‘normal’ limits on deductions for charitable contributions. However, just because something can be done doesn’t mean that it should be done.

Indeed, most taxpayers making charitable contributions substantial enough to require the use of Qualified Contributions in the first place are likely better off spreading their deductions over multiple years in order to offset income tax at the highest possible rate, rather than maximizing their charitable deductions to take their income (and tax bill!) all the way down to $0… and applying their charitable deductions against the lowest and least valuable tax brackets.

Nevertheless, there is a small group of taxpayers who may still benefit from the Qualified Contribution provision. And for financial advisors who have clients who won’t necessarily benefit from the provision, simply being able to explain to their client why the best option would be to not take a potential deduction as soon as possible can be a valuable service, in and of itself!