Executive Summary

Improvements in worker productivity over time are one of the biggest drivers for increasing an entire country’s standard of living. In the context of an individual business, productivity becomes the driver for growing revenue faster than the associated costs to support that revenue – otherwise known as “scaling” the business. For most businesses, investments in technology are one of the factors – if not the single greatest factor – that brings productivity improvements.

Except, perhaps, when it comes to the business of financial advice. As despite an incredible boom in advisor technology over the past decade, advisor productivity – whether measured by the average number of clients served by each professional in the firm, or the average revenue generated by each professional – has remained entirely flat for nearly 10 years. Instead, technology improvements have shown up in the back-office efficiency of advisory firms – where productivity ratios have improved significantly.

Yet in practice, the stagnation of advisor productivity – or at least, the apparent inability of technology improvements to have measurable increases in advisor productivity – isn’t entirely surprising, once it’s recognized that clients ultimately hire a (human) financial advisor precisely to gain expertise and support beyond what technology alone can provide. (Or else the client would simply solve their challenges themselves using the internet!)

Fortunately, though, this doesn’t mean that advisor productivity cannot be improved. Instead, recent Kitces Research into “How Financial Advisors Actually Do Financial Planning” finds that enhancements in advisor productivity are driven by three (non-technology) factors: client variability, advisor expertise, and (professional) staff support.

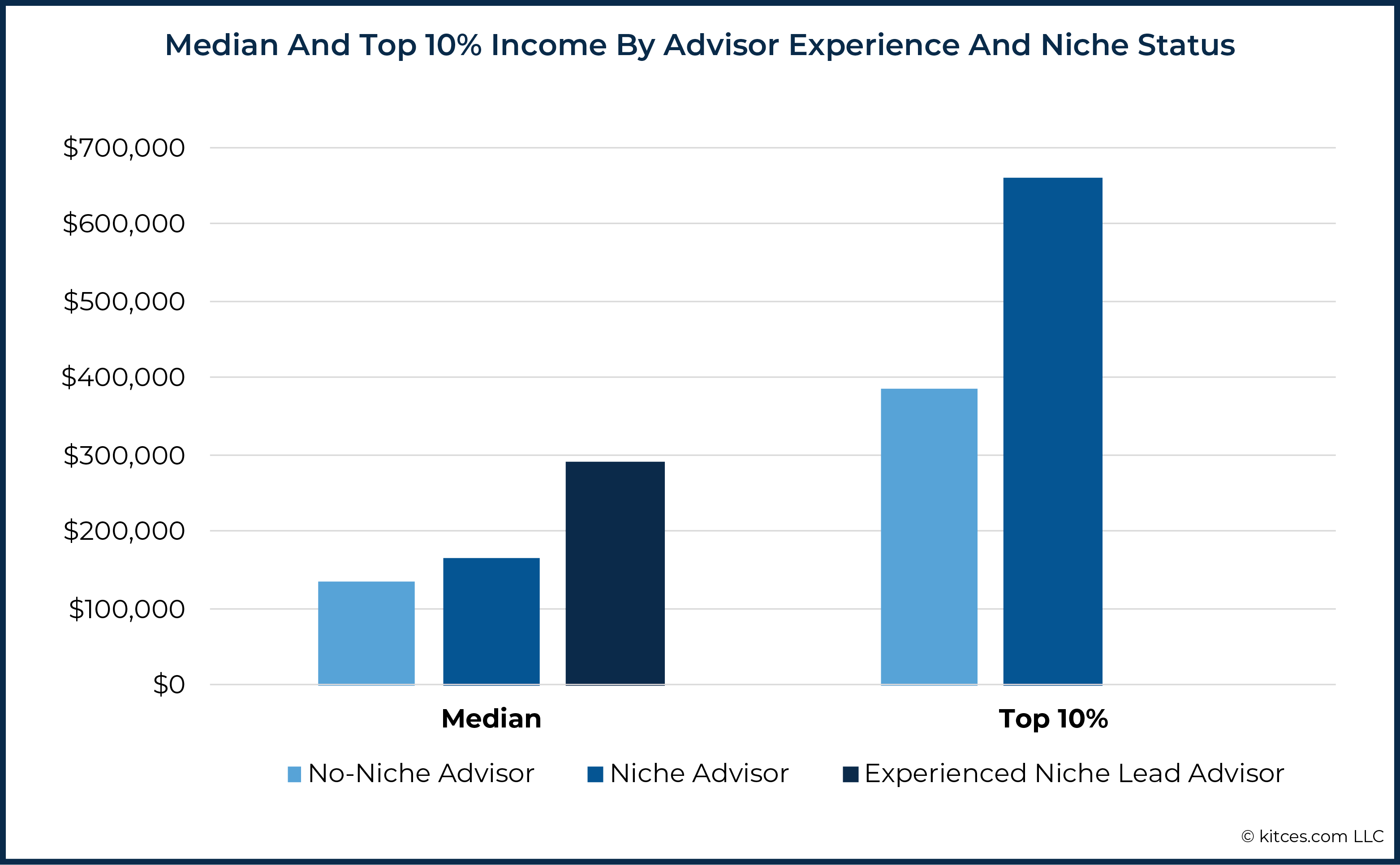

When it comes to client variability, the challenging reality is that because most financial advisors build their businesses in the early years by taking nearly anyone who will just agree to be a client (and compensate the advisor for their advice), the typical advisory firm ends out with an extremely wide range of clientele. Yet in practice, when advisors get more focused into a particular niche or specialization, enabling them to develop more ‘repeatable expertise’ simply by targeting a more consistent group of clients who have more consistent needs to be serviced in the first place, the average advisor ends out spending 13% less time doing middle- and back-office support work, can service 14% more clients, and is able to attract more affluent clients (who pay higher fees), such that the top 10% niche/specialized advisors earn nearly 67% more than the top 10% non-niche advisors (earning $660,000 versus $395,000, respectively).

Similarly, because of the complexities involved in giving advice to clients (who almost by definition tend to have more complex issues and needs… or else they wouldn’t be seeking out and willing to pay a professional financial advisor for support), advisors who invest in their own expertise are able to complete the financial planning process with clients in significantly less time. Specifically, CFP professionals complete the financial planning process in nearly 22% less time on average than non-CFP advisors. And for experienced advisors – who tend to attract even more complex clients – the differences expand further, with experienced non-CFP advisors averaging 52 hours in the first year to complete the financial planning process, compared to only 29 hours for CFP professionals (a 44% improvement in time efficiency!).

And because of the time-intensiveness of client meetings themselves – where advisors typically spend at least as much time preparing for and following up after the client meeting as the time in the meeting itself – one of the greatest improvements in advisor efficiency comes from leveraging professional support staff (i.e., paraplanners and associate advisors) to aid in the planning process. In fact, the cumulative difference in how the top 25% of advisors spend their time compared to the bottom 25% advisors amounts to as little as 1 hour per day in additional client meetings by leveraging paraplanners to aid in the meeting preparation… which results in a 64% increase in the average number of clients serviced, and a whopping 80% increase in advisor take-home pay!

Ultimately, technology may still provide incremental improvements in advisor efficiency along the way as well, especially as more technology tools arrive specifically to aid in the efficiency of the most time-consuming areas of the advisor’s day like meeting preparation and follow-up time. Nonetheless, the research shows that in the end, the greatest differences in advisor productivity are not actually driven by their technology adoption, but instead by the variability of their clientele, the expertise of the advisor themselves, and how the firm leverages professional (not ‘just’ administrative) staff support to focus the advisor’s time where it has the most impact: in meetings with clients!

The rise of the robo-advisors, and their promise to ‘democratize’ advice through the scalability of technology, stoked nearly a decade of fears that advisory firms would inevitably face fee compression, and must better leverage technology themselves to survive and thrive.

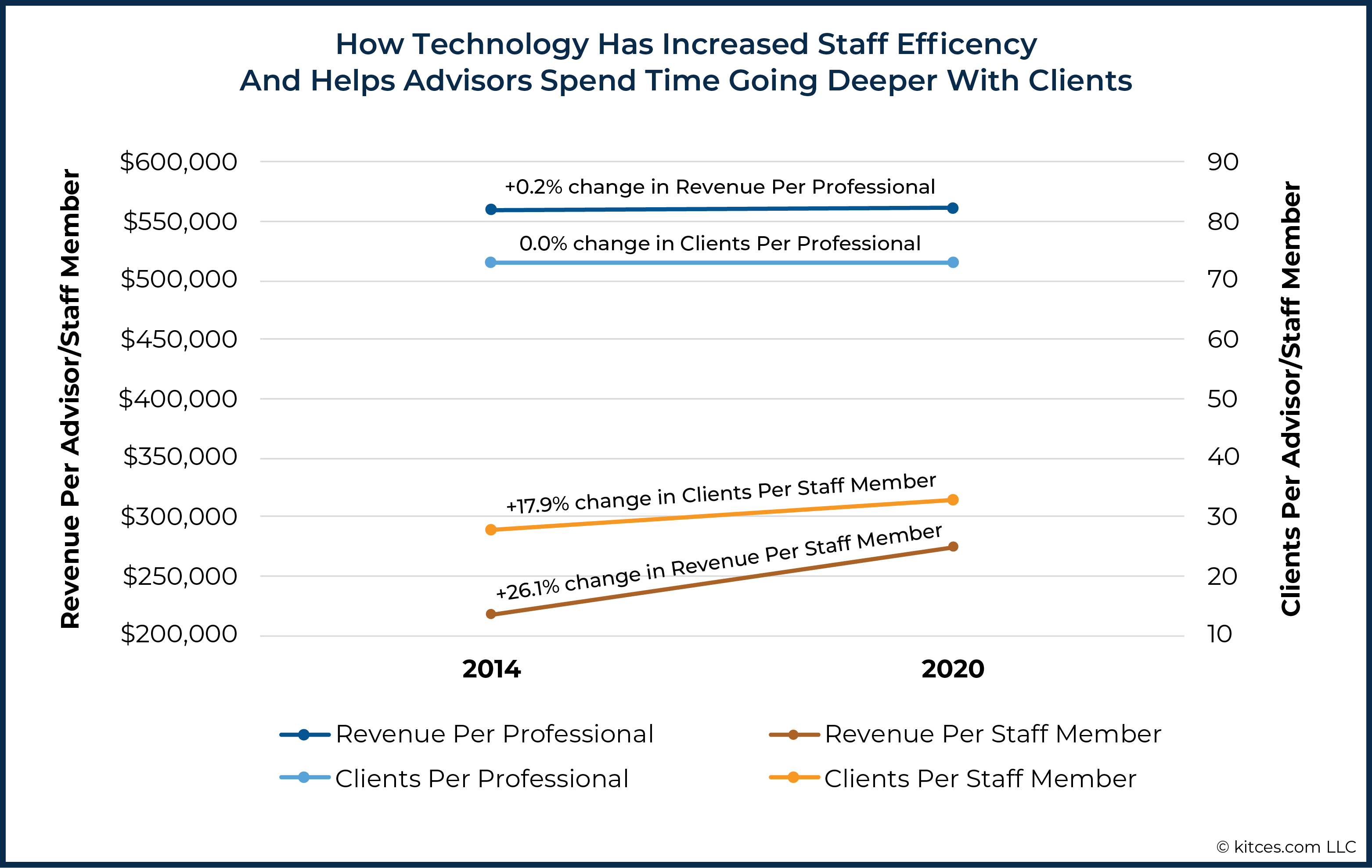

Yet nearly a decade later, perhaps the most remarkable outcome of the robo-advisor movement is how much didn’t actually change at all. For instance, back in 2014, the Investment News benchmarking study of the financial performance of advisory firms found that the average financial advisor (including lead and service advisors) supported 73 active clients and generated $561,000 of revenue. In the 2020 version of the same study, there was very little difference – the average lead or service advisor supported the same number of active clients (73) and generated only $1,000 of additional revenue ($562,000).

Notably, though, that’s not to say that technology is having no impact on the efficiency of advisory firms. For instance, the same Investment News benchmarking studies also show that the average advisory firm was able to support $275,000 of revenue per staff member in the aggregate in 2020 – up from just $218,000 of revenue/staff back in 2014 – and the average number of clients per staff member rose from 28 to 33.

In other words, technology doesn’t appear to be impacting the efficiency of the ‘front-office’ advisor themselves, but it is steadily beginning to automate and improve efficiencies in back-office staff. In fact, Kitces Research shows that even when advisors leverage more third-party technology tools in their financial planning process, the time to construct a financial plan actually remains the same or even rises. Because in practice, when technology makes the financial planning process more efficient, the typical advisor doesn’t use the time savings to do less for the client… instead, they ‘reinvest’ the time to do even more for the client, leveraging technology to go deeper (not faster).

The fact that technology helps the back-office be faster and the front-office go deeper is still a plus for the overall efficiency of the advisory firm. But it also raises the question: why aren’t advisors themselves benefitting from the efficiency potential of technology, and what does it take to make advice itself more scalable?

The primary driver, in a word, appears to be Meetings. As meetings between advisors and clients – whether held in-person or virtually via Zoom – have long been an anchor of the financial advice relationship. Additionally, meetings are a part of the advisor-client interaction that is difficult to accelerate with technology because they are largely about delivering information to clients (at the pace they can absorb it), and providing them the guidance and support they need to take action (at the pace they are ready to do so). After all, if clients could resolve all of their advice needs with some information and automated technology, they wouldn’t have needed to hire a financial advisor in the first place!

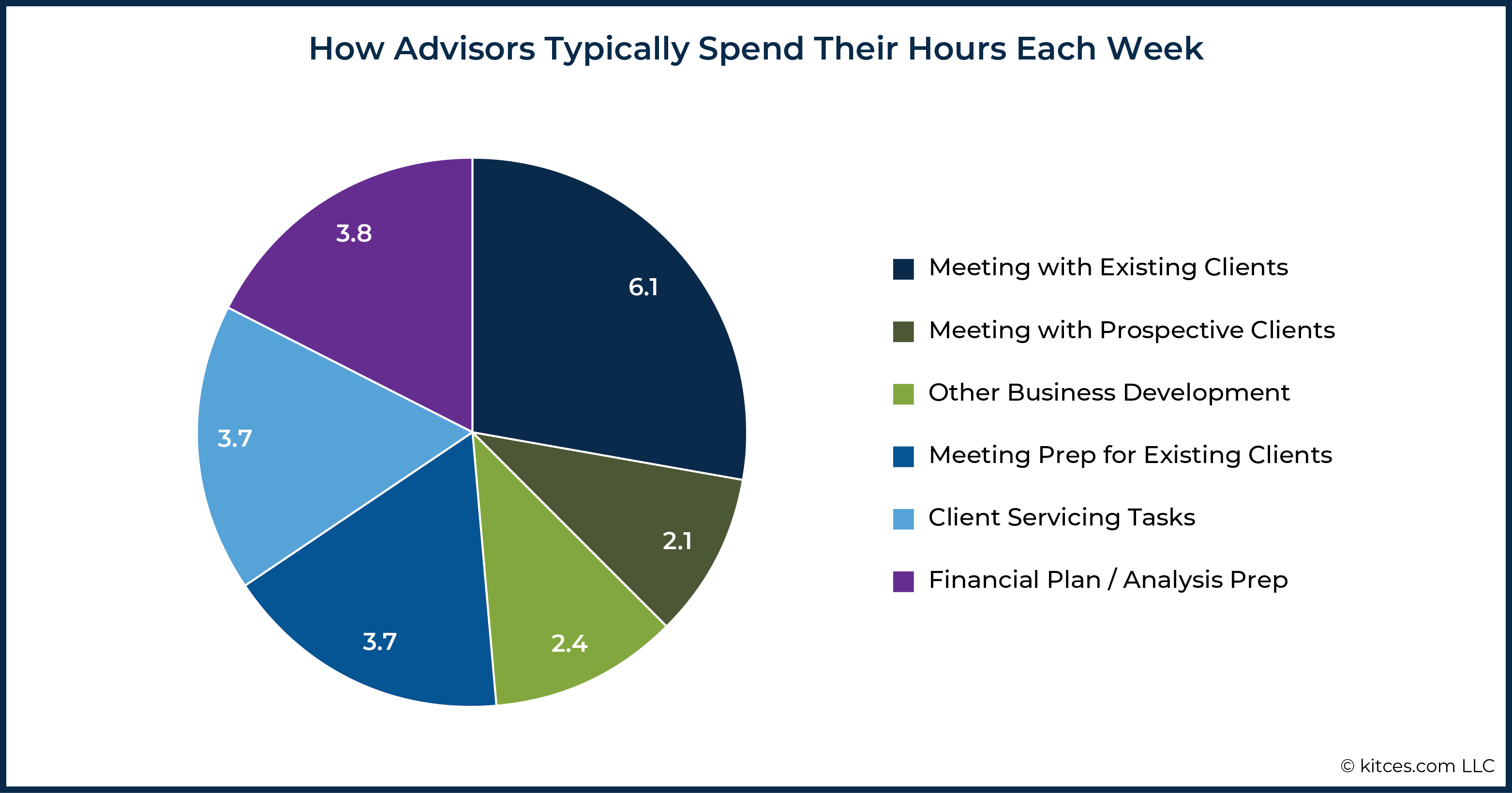

Furthermore, the time-consuming nature of client meetings is amplified by the fact that every meeting entails not only the time for the meeting itself, but the time to prepare for the meeting (from analyzing client issues to preparing agendas and meeting reports) and the time to follow-up afterward (on whatever action items came from the meeting itself). In fact, Kitces Research on How Financial Advisors Really Do Financial Planning shows that the typical advisor spends slightly more time preparing for client meetings and doing the servicing after client meetings as they spend in meetings themselves!

Which means, simply put, that making client meetings more efficient – including and especially the time it takes to analyze financial planning issues, prepare for, and follow-up on client meetings – can actually be the biggest driver of financial advisor efficiency!

Reducing Client Variability To Increase Advisor Efficiency

Most advisory firms grow, especially in the early years, by taking anyone and everyone who is willing to become a client in the first place. In this context, the only factors that determine whether a prospect becomes a client are their financial wherewithal and their willingness to buy whatever product or portfolio or ad-hoc advice the advisor is offering.

The end result of this approach is that clients may end out with a common portfolio or suite of products they’ve implemented, even though they may have very different service needs and expectations. Some may expect occasional meetings but in person, while others may expect more frequent check-ins but virtually. Some may want to simply tap the advisor’s expertise as needed and then follow through themselves, while others may expect the advisor to engage a more hands-on approach. Some may expect the advisor to simply support whatever product or advice was originally offered, while others may be looking for the advisor to help address whatever financial advice questions they have.

Consequently, it’s very difficult for most advisory firms to create more scalable systems and processes because their clients – and the breadth of their client needs – don’t fit a more standardized approach in the first place. In other words, scalability is prevented by the high variability of the clients themselves.

So what’s the alternative? Simply put: having less client variability by getting more specific about what the firm offers, who it best serves, and seeking to attract clients who specifically want that particular offering. This is otherwise known as having a niche or specialization.

In fact, Kitces Research shows that financial advisors who focus on niches or specializations operate substantially more efficient and scalable advisory firms, spending 13% less time doing middle- and back-office support work for clients, 28% more time with clients and prospects, serving an average of 14% more clients, who in turn have an average of 25% more in investable assets and net worth.

In other words, advisory firms that focus into niches end out serving more clients and being able to charge higher fees… despite, ironically, providing financial plans that are actually less comprehensive by breadth (but more in-depth for greater client value). Such that the top 10% of advisors with niches generate $660,000/year in take-home income (compared to ‘just’ $395,000 for the top 10% of non-niche advisors).

In other words, scalability in financial advice is achieved by creating a more “repeatable expertise” via a niche or specialization, and then refining the firm’s marketing and sales processes to attract clients who are seeking that particular expertise (and find it valuable and worth paying for).

By reducing the variability of client demands, the firm can operate in an environment where it’s easier to systemize the firm’s value to clients in the first place (while also being able to attract clients who pay higher fees for that more unique and specialized advice!).

Expanding Expertise To Expedite The Financial Planning Process

When clients have questions for which there is a readily apparent answer, there usually isn’t much need to hire an advisor; simply asking Uncle Google or Aunt Siri is usually enough to get the requisite information to make a decision. Instead, almost by definition, clients seek out financial advisors to help with problems that are too complex to answer with information alone, and require a deeper level of expertise to understand and apply the knowledge.

Yet the sad irony is that the requirements to become a financial advisor are quite low – typically no more than a Series 6 and 63, a Series 65, or a state life-and-health insurance license – all of which test the rules to which advisors will be subject, and the nature of the products they may sell… but none of which actually require expertise in the topics of financial advice itself.

The end result of this dynamic is that as advisors take on clients to whom they will give advice, the advisor often has to do a great deal of their own analysis and research to figure out the answer to the questions in the first place. And as advisors gain experience and build their brand/reputation and gain more clients with more complex needs over time, they end out needing to spend more and more time analyzing their clients’ financial planning challenges and crafting appropriate recommendations.

Which means that by deepening the advisor’s expertise in the first place – to reduce the amount of per-client analysis – there is an opportunity to gain additional time efficiency and scale in financial advice. This is exactly what Kitces Research shows.

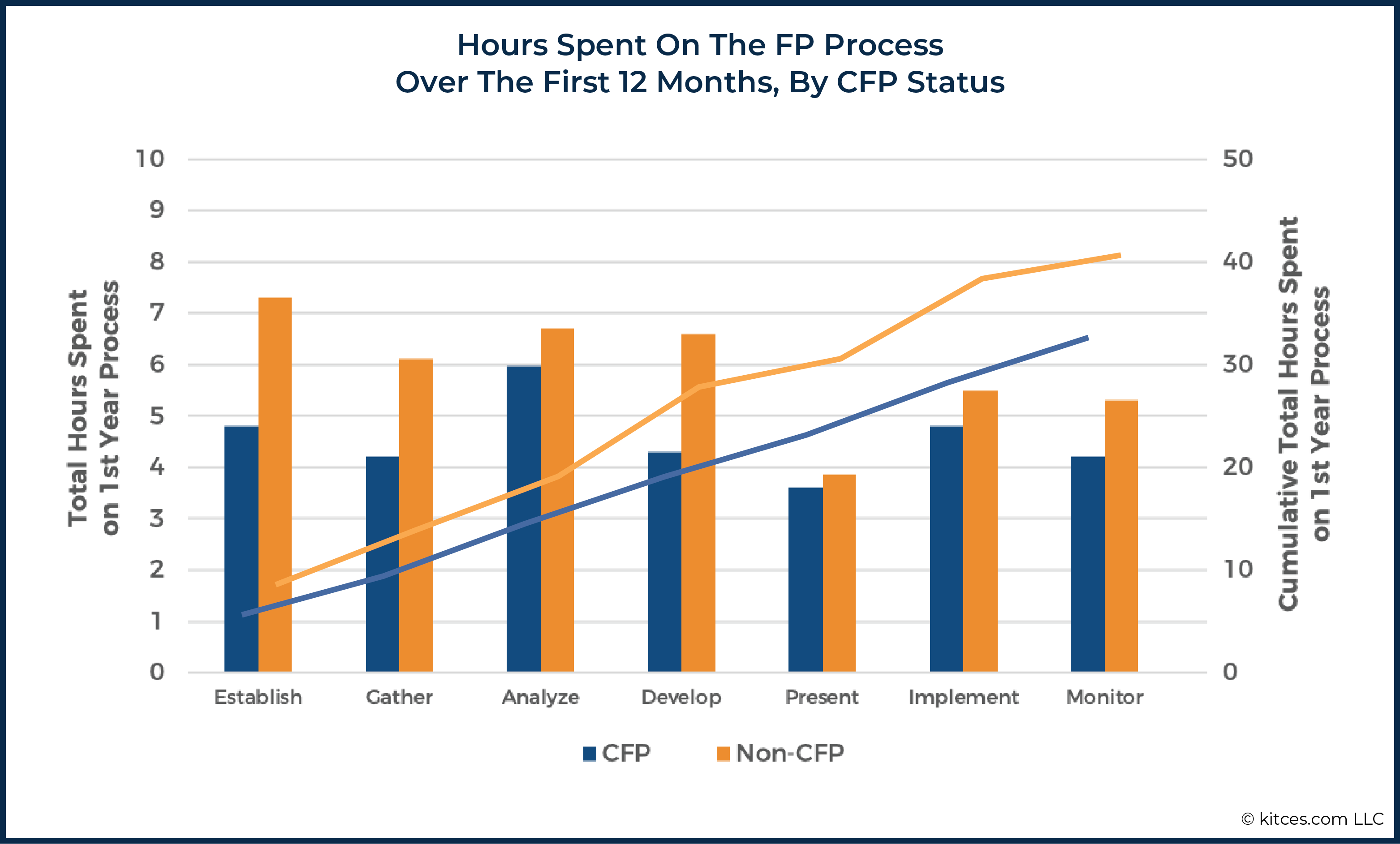

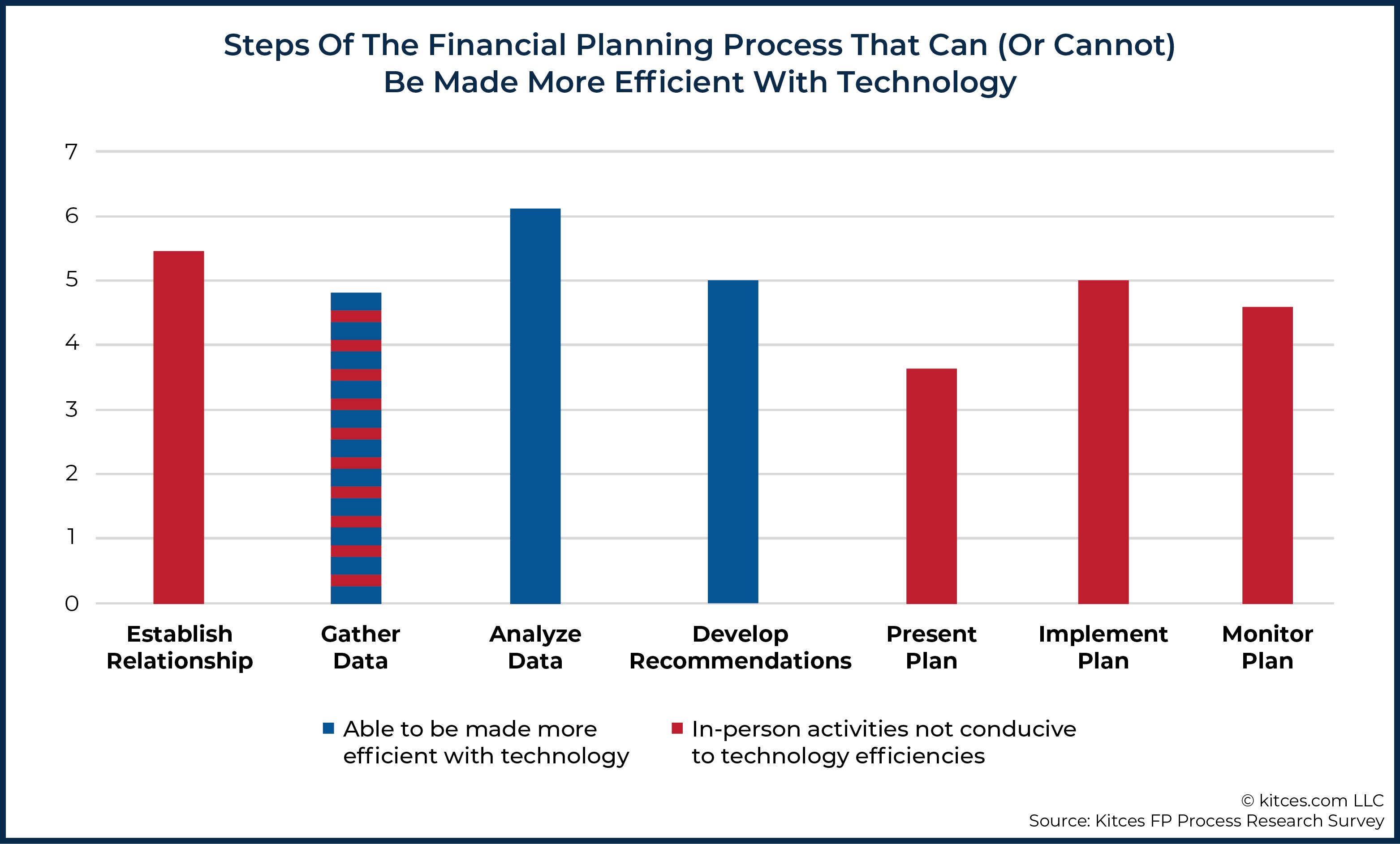

The average financial advisor spends nearly 35 hours engaging in the entire comprehensive financial planning process over the first year of the engagement, from establishing the relationship and gathering data upfront, to doing the analysis and crafting recommendations, delivering the plan and implementing the recommendations, and then beginning the subsequent ongoing monitoring process.

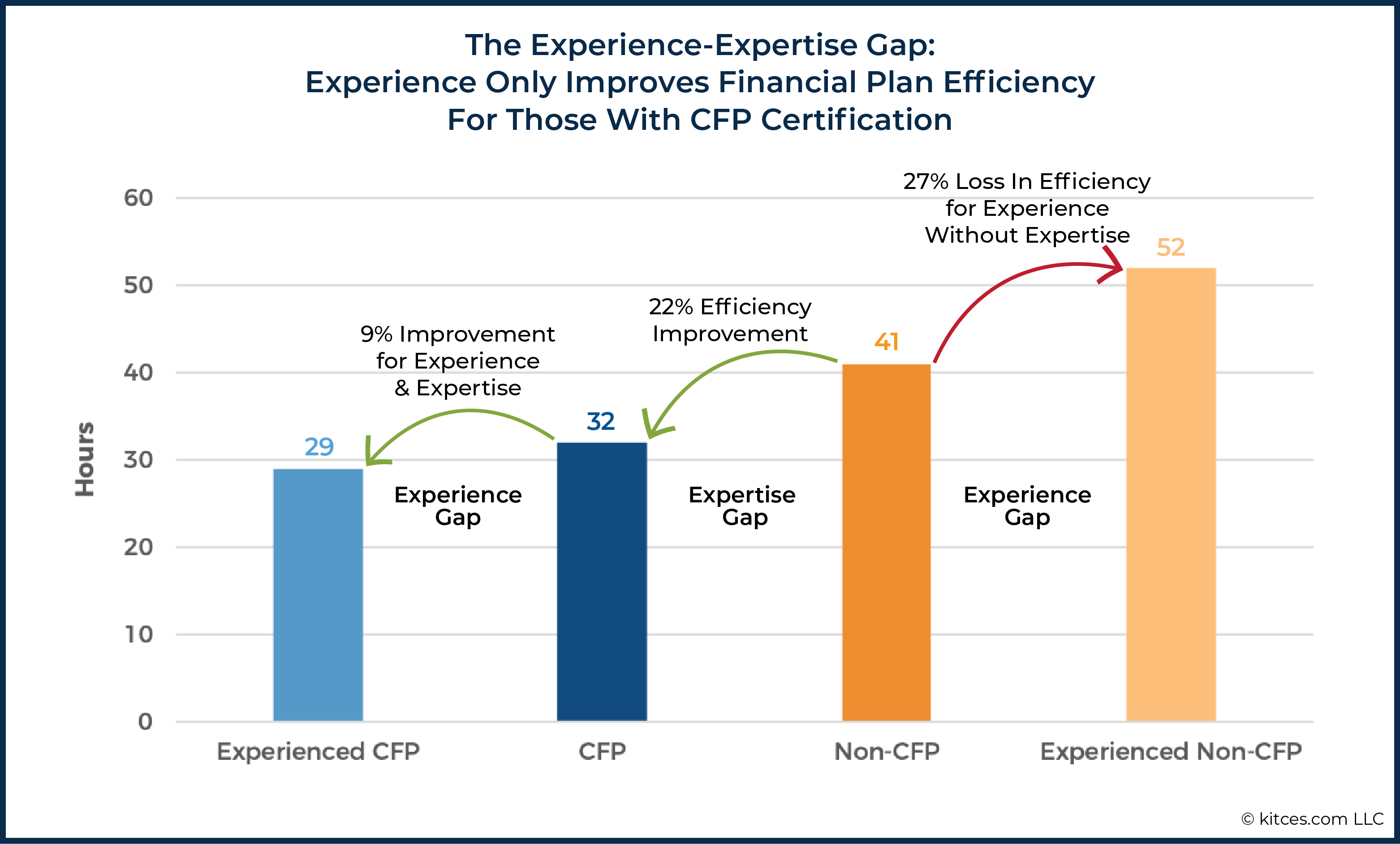

However, when separated between those with and without CFP certification, the time to construct a plan diverges significantly: the average CFP professional gets through the process in 32 hours, while the average non-CFP advisor takes 41 hours in the first year to engage in the same financial planning process!

Notably, there is little substantive difference between CFP professionals and non-CFPs when it comes to the time to present a financial plan itself. Instead, the difference in time emerges in all the other stages of the planning process, and especially when it comes to the time it takes to establish the relationship (where greater perceived expertise can accelerate credibility and therefore trust), to gather data (with better knowledge of the questions to ask upfront, with fewer follow-up questions), and to develop recommendations (decreasing the time it takes to do the background research to formulate the right recommendation).

In turn, as CFP professionals gain more experience – coupled with the expertise gleaned from their CFP certification – their time to construct financial plans decreases further, to 29 hours. However, as non-CFP advisors become more experienced – and generally attract more sophisticated clientele with more complex needs – their time to deliver a financial plan increases to an average of 52 hours. In other words, gaining experience (and the more sophisticated clients that come from greater experience) makes CFP professionals more efficient, but makes non-CFP advisors less efficient!

The end result is that for the most experienced financial advisors, there is a whopping 44% improvement in the time it takes to complete the entire financial planning process as a CFP professional versus a non-CFP advisor. Or viewed another way, expertise that is learned once, definitively, provides ongoing time savings for every client thereafter!

Leveraging Staff Support To Focus Time On Client Meetings

One of the biggest reasons that technology has a very limited impact on the efficiency of the financial planning process is that so much of the process is meetings with clients… which isn’t very conducive to technology efficiencies, as clients are still ultimately human beings who will only ever take in information and make a decision ‘so’ quickly.

And meetings themselves are time intensive. Not only when it comes to the time for meetings themselves, but as noted earlier, because of the preparation for the meeting, along with the follow-up thereafter. Which may not be conducive to technology automation – because, again, clients tend to hire advisors for the tasks that can’t already be automated and require another human with expertise to give conscious thought and analysis, but that can often be delegated.

In fact, Kitces Research on How Advisors Actually Do Financial Planning shows that advisors who leverage support staff (whether as a solo advisor hiring support or as an advisor working within a larger firm) drive significantly more revenue and client efficiency. This entails not just administrative support staff, but specifically paraplanners and associate planners (who themselves typically have CFP certification) and can take on some of the most complex and time-consuming parts of the advice process.

Specifically, Kitces Research shows that advisors who leverage paraplanners or associate advisors service an average of 120 clients (compared to only 73 clients per advisor for ‘pure’ solo advisors) and generate an average of $279,000 in take-home compensation (compared to only $155,000 for pure solo advisors). Which is accomplished by being able to spend 30% less time per client, including a cut of almost 40% of the follow-up servicing time after meetings (which is delegated to the paraplanner to follow up on).

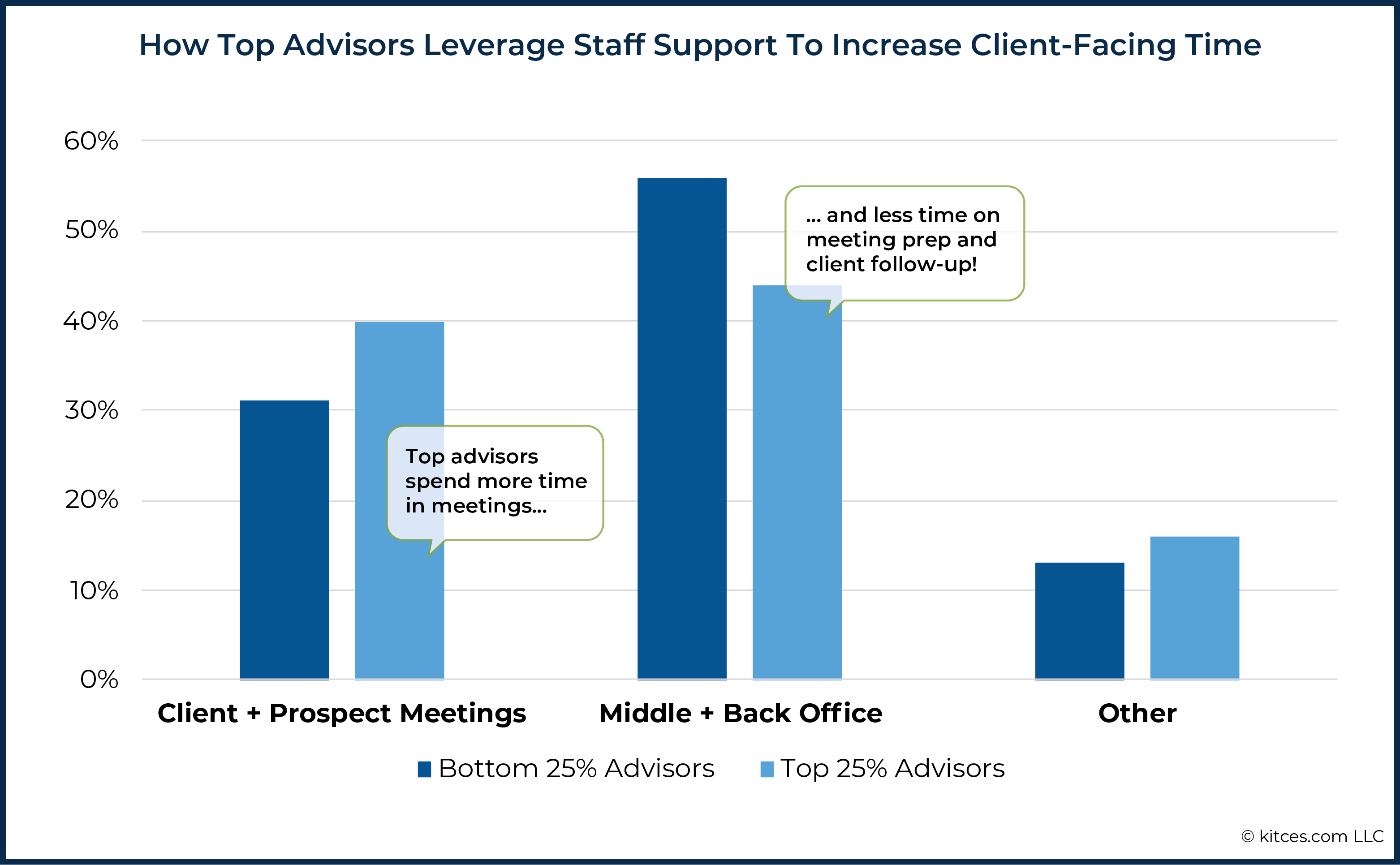

Overall, Kitces Research shows that the difference between the top 25% of advisors and the bottom 25% actually just comes down to a 10% difference in how time is spent: specifically, that top advisors spend about 10% more of their time in meetings with clients and prospects, and about 10% less on meeting preparation and client follow-up. Which amounts to nearly 1 hour per day of additional meetings, or an average of about 4 meetings per week, which adds up to 200+ additional client and prospect meetings per year.

In other words, executing more efficient advice processes to service more clients is more a game of inches than drastic automation. Advisors who engage paraplanners or associate advisors can cumulatively support 64% more clients by taking what is typically 2 client meetings per day plus 2 hours of meeting prep and follow-up, and turning it into 3 client meetings but only 1 hour of preparation (which, notably, means the meeting preparation and follow-up time per meeting is cut rather drastically, from an average of 1 hour per meeting to only about 20 minutes per meeting).

The key, though, is that the aforementioned efficiencies are specifically for advisors that leverage not ‘just’ administrative staff support, but specifically paraplanners or associate advisors… those who often have the CFP marks themselves (or at least have passed the CFP exam and are working towards their experience requirement). These support resources are those who can help address not just the back-office tasks that are increasingly being automated anyway but, specifically, the more complex client work that can’t be delegated and instead needs to be done by a human being... recognizing that the human being doesn’t have to be the lead advisor doing all the meeting preparation and follow-up work, and that it can be an associate advisor instead.

In turn, this also means that even if the paraplanner or associate advisor ‘just’ supports the advisor for half the day – 3 meetings and 1 hour of preparation – and only cumulatively shifts 1 hour per day of the advisor’s time, that’s still enough to cumulatively add up to a 64% increase in client capacity and an 80% increase in take-home pay over time!

Ultimately, the very essence of “scaling” is about the ability to grow revenue faster than expenses – by either doing more with less, or at least doing a lot more in business revenue while adding relatively less in additional business costs to get there.

The most straightforward way to achieve such results is through technology, which often has a fixed or more limited increase in cost while being able to service far more clients. Yet, in practice, while technology is automating more and more of the advisor’s back office, it appears to be doing relatively little for middle- and front-office tasks related directly to client advice.

As a result, the path to scalability for the delivery of financial advice itself may not necessarily be about technology. Instead, it’s about narrowing the variability of the clients being served, deepening the advisor’s expertise to be able to give advice more quickly and efficiently (with less back-and-forth, better questions upfront, and faster analysis and recommendations), and leveraging planning support staff in a manner that reduces meeting preparation and follow-up time and allows the advisor to have more time to meet with more clients and prospects in the first place.

Of course, this doesn’t mean that technology won’t be able to drive additional efficiencies as well, especially with tools like Pulse360 emerging specifically to make the meeting preparation and follow-up aspects of the financial planner’s day more efficient. But in the end, advisor efficiency appears to be driven far more by who the advisor chooses to serve, the expertise they bring to the table, and how they leverage their time to be as focused on client meetings as possible. Which, fortunately, are all under the advisor’s control!

Leave a Reply