Executive Summary

From the moment they were introduced nearly 25 years ago in the Taxpayer Relief Act of 1997, the Roth IRA has been an incredibly popular retirement vehicle, thanks to its ‘unlimited’ potential for generating tax-free growth. Of course, the caveat is that Roth-style accounts are only tax free because the contributions into the account are made on an after-tax basis – unlike traditional retirement accounts, which enjoy a tax deduction on the initial contribution. Which means in practice, households must make a decision whether to contribute to a pre-tax traditional IRA or a tax-free Roth, based on whether the upfront tax deduction (on the traditional IRA contribution) will be more or less valuable than tax-free growth at the end (on the Roth IRA distribution).

Mathematically, the Roth-versus-traditional IRA decision will actually be the same, regardless of growth rates and time horizon, as long as both accounts remain intact and tax rates don’t change. If future tax rates do change, though, the Roth IRA will result in more wealth when tax rates rise in the future, while the traditional IRA will benefit when tax rates are lower in the future. Though in practice, because the tax burden for a Roth IRA is paid upfront – when the (after-tax) contribution is made – there is no future uncertainty with respect to its future tax rate; instead, changes in tax rates primarily impact the future value of a traditional IRA, in particular, making it better or worse off depending on whether or how tax rates change.

To cope with this uncertainty, one popular approach is to ‘tax-diversify’ between the two types of accounts, splitting contributions between traditional and Roth IRAs so that there is at least ‘some’ benefit regardless of which direction tax rates go (as higher tax rates benefit the portion of dollars in the Roth, and lower tax rates would benefit the traditional IRA dollars instead). However, the reality is that splitting dollars between traditional and Roth retirement accounts isn’t just a form of diversification; because the outcomes are correlated to each other (as a change in tax rates that benefits one type of account adversely impacts the other type by the same amount), the net result is that tax diversification doesn’t actually diversify the risk, it simply neutralizes the opportunity altogether. Or viewed another way, splitting between traditional and Roth IRAs is not akin to the diversification of owning different types of stocks; it’s more akin to just bailing out of stocks altogether and owning zero-return cash.

So what’s the alternative? Instead of trying to tax-diversify between traditional and Roth retirement accounts, taxpayers can consider trying to ‘Roth optimize’ exactly when to add dollars to tax-free Roth accounts. After all, a household’s tax rates typically vary throughout life – often by a wide range as careers start and stop and change, family and health needs impact our time in the workforce and what we earn, businesses are started and subsequently fail or succeed, and eventually retirement comes (with its own tax complications of Social Security benefits and Required Minimum Distributions). Which means there will be years where a household can ‘time’ its tax situation, by contributing to traditional IRAs in years when income and tax rates are high, and tactically switching to Roth contributions (or even engaging in Roth conversions) when tax rates are unusually low.

Of course, there’s always a risk that tax rates will change in the future, not because of the household’s change in income, wealth, or circumstances, but simply because Congress itself ‘changes the rules’ by altering tax rates. Although, in reality, while tax brackets have varied significantly throughout history, tax deductions have often changed alongside the brackets, such that changes in effective tax rates have actually been remarkably narrow throughout history. In other words, the variability of tax rates due to Congress (which we can’t control) is actually dwarfed by changes in tax rates within the household over time (which can be planned for!).

Ultimately, though, the key point is simply to understand that arbitrarily splitting dollars between traditional and Roth-style retirement accounts isn’t actually a positive wealth-creating strategy; instead, it is more akin to ‘going to cash’ and eliminating the opportunity altogether. For those who want to actually maximize wealth with the traditional-vs-Roth decision, the better approach is to try to Roth-optimize by timing when to shift between traditional and Roth accounts. Which, in practice, is easier than most realize, as while a household’s future is never certain, the Roth-vs-traditional decision has the most impact in years that are especially high or low in income… which are actually the years that are most easy to identify in the moment for a Roth optimization timing decision!

To Roth Or Not To Roth: Evaluating Roth Versus Traditional Retirement Accounts

The Taxpayer Relief Act of 1997 introduced, for the first time, the opportunity for individuals to contribute to a tax-free Roth IRA for retirement. Up until that point, retirement accounts – in the form of both IRAs and 401(k) plans – provided a tax deduction when contributions were made to the account, in exchange for the fact that subsequent distributions at retirement would be taxable (in essence, allowing not only growth to compound on a tax-deferred basis, but the original contribution to be tax-deferred as well). Roth-style accounts were unique, though, in that contributions would no longer be tax-deductible… but growth within the account would still be tax-deferred, and could ultimately be withdrawn tax-free (at least if certain requirements were met).

From nearly the moment of their inception, the promise of a lifetime of tax-free growth made Roth accounts popular, especially amongst higher-income households that faced top tax brackets. However, to limit their use by high-income households, Roth accounts were established with income limitations, both on contributions themselves (with the ‘maximum’ contribution reduced to $0 for those above specified income thresholds), and on Roth conversions (which were prohibited for households with more than $100,000 of AGI, although the Roth conversion income limitation was subsequently removed starting in 2010 by the Taxpayer Increase Prevention Act of 2005 [TIPRA]). As a result, the highest-income households that faced the highest tax rates – for which tax-free growth would ostensibly be most valuable – were the ones that were least able to actually utilize Roth accounts!

Yet the irony is that, in reality, the tax-free growth of a Roth-style account is not necessarily more valuable than the pre-tax contribution to a traditional IRA in the first place. As while a tax-free Roth account is clearly more valuable than simply investing in a ‘normal’ taxable investment account, traditional IRAs do have a significant additional benefit: the upfront tax deduction on the contribution in the first place. Which substantively changes the comparison beyond a simple rule of thumb that “tax-free Roth accounts are always better”.

The Tax Equivalency Principle Of Roth Versus Traditional Retirement Accounts

Imagine for a moment that you learn you are going to receive a $5,000 bonus from your employer – funds that you wouldn’t need to cover your current household spending – and are suddenly faced with the decision of where to save this additional income.

On the one hand, you could contribute the full $5,000 to a traditional IRA and receive the associated upfront $5,000 tax deduction. On the other hand, you could contribute to a Roth IRA, but doing so will mean that you would have to hold aside some of the money for taxes (presuming that the rest of your wealth is already invested, so you don’t have extra cash lying around), such that if your Federal-plus-state marginal tax rate is 25%, only $3,750 will actually end out in the Roth account (with the other $1,250 going to taxes).

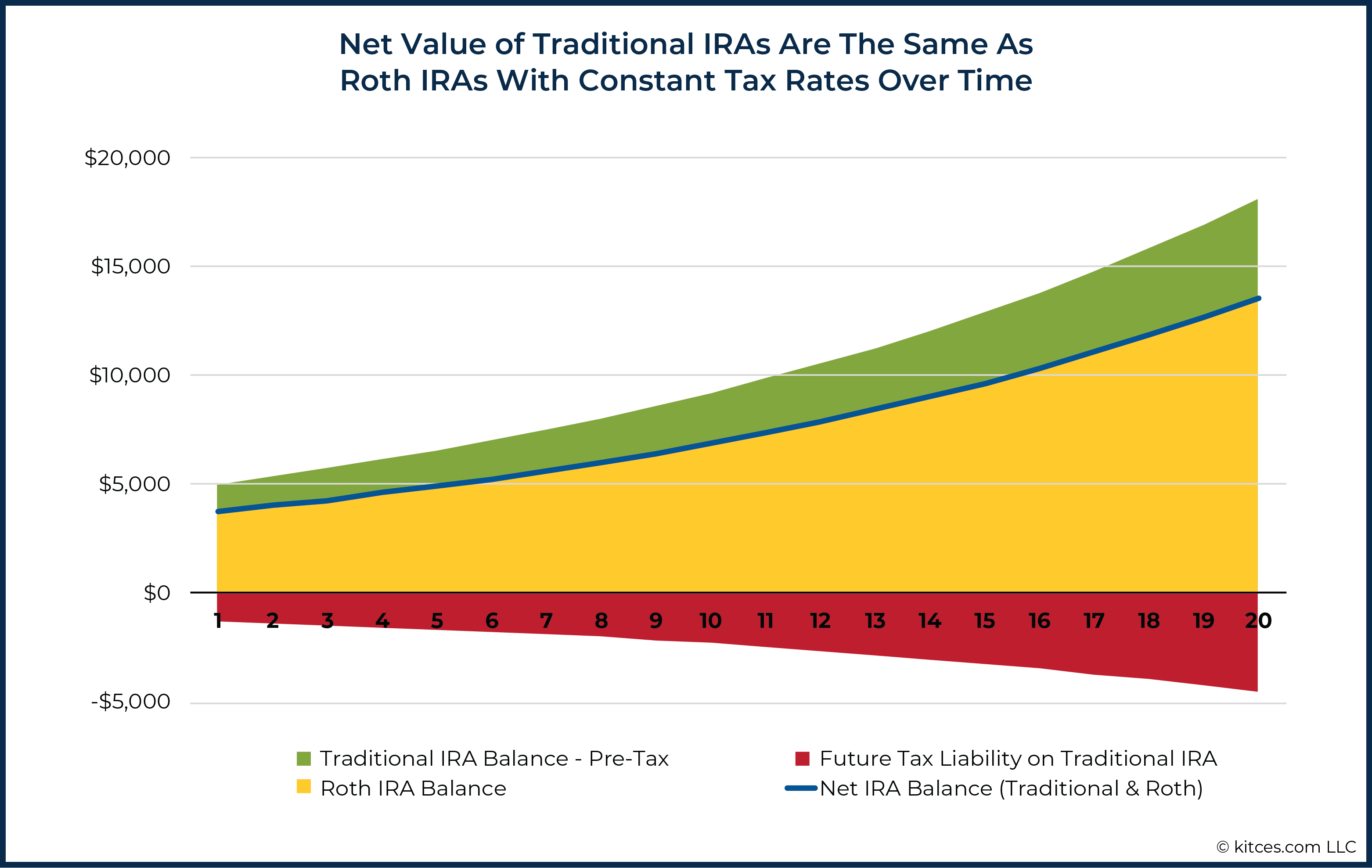

Assume that you leave the dollars in the retirement account long enough for its value to double (whether that’s compounding 7% per year for 10 years, or 4% per year for 18 years). At the end of the time period, the Roth account will grow from $3,750 to $7,500, while the Traditional account will grow from $5,000 to $10,000. However, the Traditional account is still a pre-tax account, and being able to spend the money will require withdrawing it and paying the associated taxes… which, if tax rates haven’t changed, will reduce its value by 25%, to a net value of $10,000 – (25% x $10,000) = $7,500 of after-tax value.

The end result is that the Roth account produces neither a dollar more nor a dollar less than the traditional retirement account! Because in practice, when Uncle Sam has ‘earmarked’ 25% of a growing retirement account, the value of the account grows to the upside at the exact same rate that the tax liability grows to the downside. As a result, regardless of the time horizon or the growth rate, the after-tax value of a traditional retirement account is always exactly the same as the value of the Roth account (as long as the tax rates remain the same).

Roth Versus Traditional When Tax Rates Change

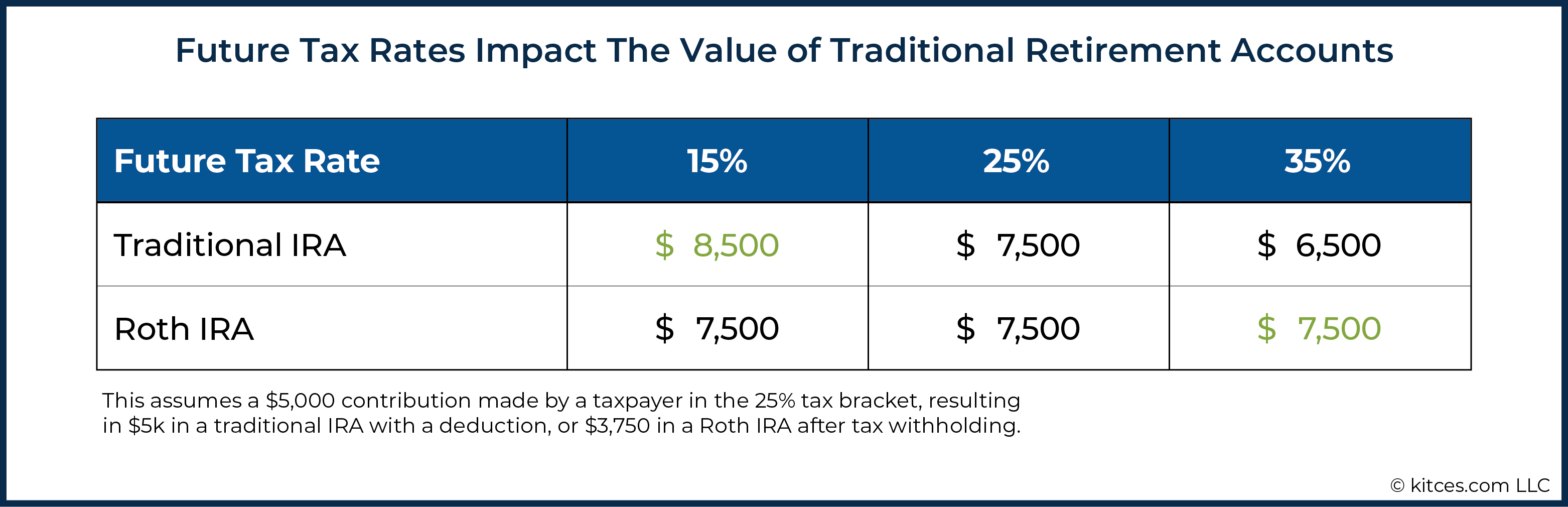

The ‘tax equivalency’ of Roth versus Traditional retirement accounts exists because, in the long run, the additional value of tax-free growth in a Roth is the same as the additional value of the upfront tax deduction for the traditional retirement account. With the caveat that in the end, the value of the upfront tax deduction on a traditional retirement account is not just a function of the marginal tax rate when the deduction occurs. The value of a traditional IRA will also be impacted by what the final tax rate turns out to be when the dollars are actually withdrawn in the future.

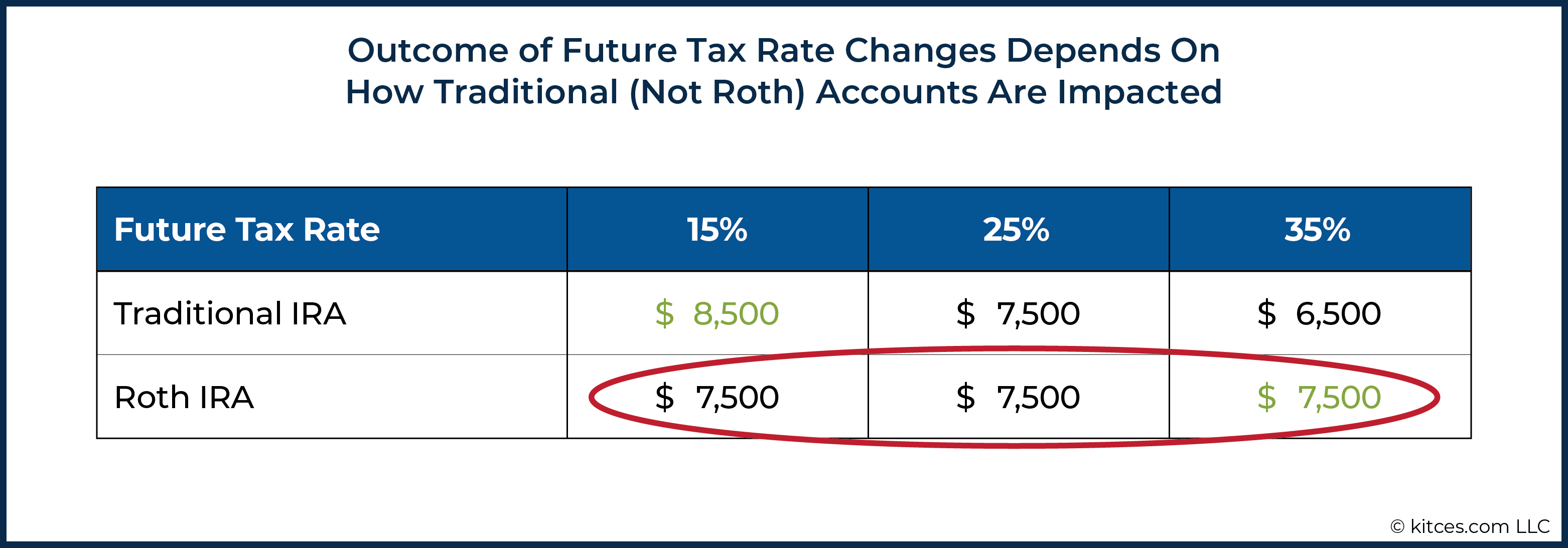

After all, the $3,750 Roth IRA that doubles in value with growth to $7,500 will ‘always’ be worth $7,500, because the tax impact was ‘locked-in’ upfront (at the assumed 25% tax rate), while the final value of the $5,000 pre-tax Traditional IRA contribution is not actually determined until the end. If the future tax rate turns out to be 35% (and not 25%), the traditional IRA will grow to $10,000 but only be worth $6,500 after taxes. If the future tax rate declines and is only 15% in the end, the traditional IRA that grew to $10,000 will be worth $8,500 on an after-tax basis.

As the chart above shows, for any given upfront tax rate (that is ‘locked in’ with the after-tax Roth contribution), if future tax rates are higher than that initial tax rate, then the Traditional IRA’s value will fall behind the Roth account. If future tax rates are lower, though, then the Traditional IRA’s value ends out being ahead of the Roth account. Which means it’s the change in tax rates – between the upfront contribution and the final distribution – that ultimately determines whether a Traditional IRA ends out being better, or worse, than a Roth-style account.

How Tax Diversification Minimizes Tax Alpha Opportunities

When it comes to investing, there is significant uncertainty about what the future price of any particular stock (or the overall stock market) will be, such that one of the most common investment strategies to manage this uncertainty is to diversify into a wide range of investments. And for many individuals and households, there is also significant uncertainty about what their ‘tax future’ will look like, given both the potential for job and income changes, sudden wealth events (for better or for worse), and the potential that Congress itself will change the rules of the game. Such that some people look not only to diversify the investments in their portfolio (to manage investment uncertainty) but also to diversify their investments across their traditional and Roth retirement accounts (to manage tax uncertainty).

In other words, recognizing that a traditional retirement account will fare better if the individual’s tax rates are lower in the future, but the Roth will turn out to have been preferable if the individual’s tax rates end out higher, having some dollars in each type of account – Roth and traditional – is a way to diversify against this uncertainty. Which might mean contributing evenly to traditional and Roth retirement accounts every year (whether via an IRA or 401(k) plan). Or it could mean taking what were historically accumulations in traditional retirement accounts (especially since many 401(k) plans still only offer a traditional and not Roth-style option) and doing a partial Roth conversion to turn half of the traditional account into a Roth.

The end result, though, is simply that by having some dollars in a traditional account (which benefits if tax rates go down) alongside some money in a Roth account (which benefits if tax rates go up), the household can ‘ensure’ at least some benefit, regardless of which direction tax rates actually go. As with traditional diversification, by holding some exposure to each, there is an opportunity to benefit as long as either does well in the future. The household has ‘tax diversified’ its retirement accounts in the face of tax uncertainty.

Why Tax Diversification Doesn’t Actually Diversify

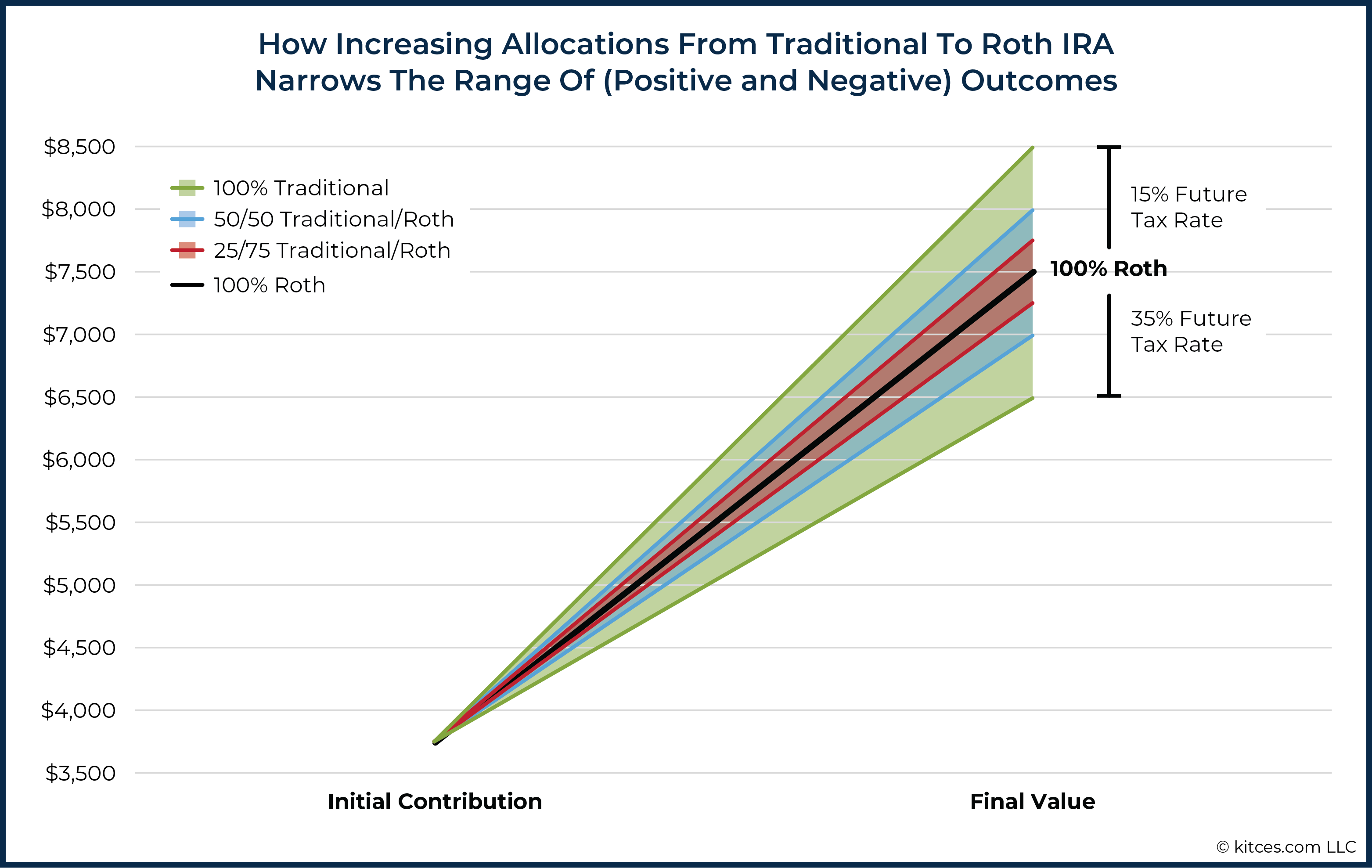

While there is a clear, intuitive appeal to the concept of ‘tax diversification’, the caveat is that, in practice, the outcomes are not really consistent with the traditional benefits of diversification. Because with traditional diversification – in the investment context – the outcomes of each investment are (at least ideally) independent of each other (i.e., not correlated to one another). Whereas when it comes to tax diversification, the outcomes are directly related to each other; every 1% tax rate increase that benefits the portion that was allocated to the Roth impairs the funds that remained in a traditional account, and vice versa when tax rates decrease (where the traditional account benefits but the Roth does not).

Although in reality, because the tax rate on a Roth account is effectively ‘locked-in’ at the time of contribution or conversion, the outcomes of tax rate changes – for better or worse – are driven entirely by whether the traditional retirement account fares better or worse. As the Roth account is always worth the same after-tax value in the future, regardless of what actually happens to future tax rates. Whether that Roth outcome is better than what the traditional IRA would have been is determined by future tax rates (which reveal what the traditional IRA might have been worth on an after-tax basis).

As a result, the decision to put dollars into Roth versus traditional accounts effectively just ‘takes money off the table altogether’ from a tax-planning perspective. With a traditional account, future outcomes could be better or worse (depending on what future tax rates turn out to be), while increasing the percentage of dollars in the Roth account simply narrows the range of outcomes altogether (to the point that with a full Roth conversion, there is no upside or downside from future tax rate changes).

Or viewed another way, splitting dollars between traditional and Roth accounts is not akin to ‘investment diversification’ (e.g., between large- and small-cap stocks); instead, it’s more analogous to taking money out of the markets altogether (eliminating both the downside and upside opportunity) and just holding zero-risk-zero-opportunity cash instead.

How Tax Timing Beats Tax Diversification

Investment diversification is popular because markets are incredibly efficient, and, at best, most investors will struggle greatly in their efforts to time the markets to determine when to buy or sell individual stocks (or the overall stock market). However, when it comes to our tax situation, there is no aggregate market trading in and out of our individual tax futures to arbitrage away opportunities to generate alpha. Instead, we are uniquely privy to our own tax situation and our own plans and expectations for the future… which creates unique opportunities to engage in 'tax timing' that tactically navigate our changing tax situation over time.

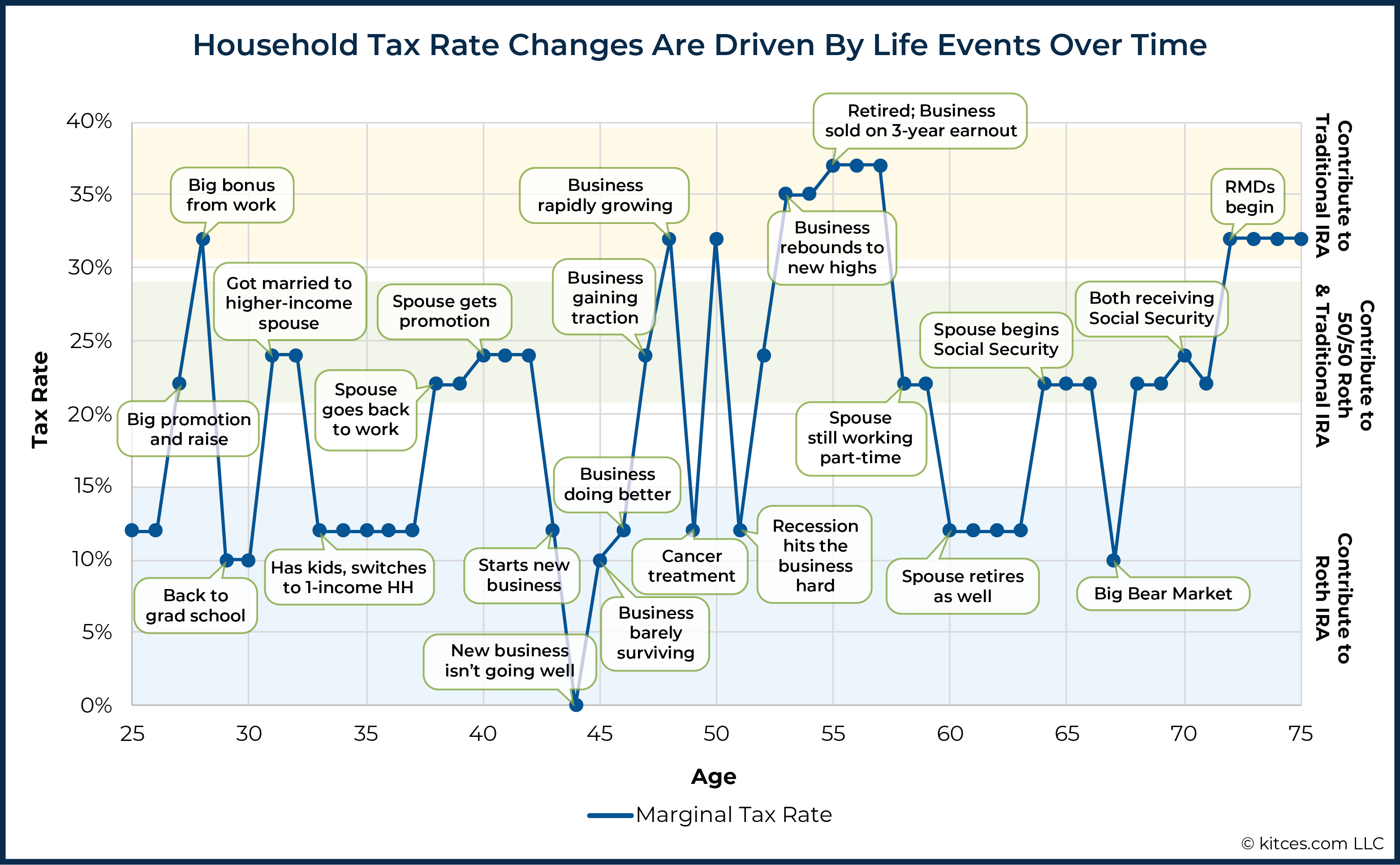

After all, our tax picture can and does change – sometimes quite significantly – over time. In some cases, this is a function of our growing careers (e.g., tax rates tend to rise during our working years as our careers build) or growing net worth (e.g., the more wealth that is accumulated, the more passive investment income that tends to be generated, filling lower tax brackets and crowding marginal income into higher tax brackets).

In other situations, it’s any number of ‘one-time’ events that occur with ‘surprising’ regularity, from being laid off in a recession or taking time out from the workforce to go back to school, taking leave for a health event, launching of a new business that drags our income down, or, conversely, a big bonus at work, a home-run investment, a business that takes off, or a major liquidity event that boosts our income higher.

Accordingly, rather than simply having an arbitrary strategy of ‘tax diversification’ (e.g., always contributing 50% to a traditional account and 50% to a Roth account), a Roth-optimized ‘tax timing’ strategy would aim to more opportunistically determine when to contribute to traditional accounts, and when to contribute to (or convert into) Roth-style accounts.

For instance, consider an approach where instead of arbitrarily diversifying 50/50 between a Roth and Traditional IRA, the aforementioned household over their lifetime contributed to Roth-style accounts any time their tax bracket was 10% or 12% (or Roth-converted 1/10th of their existing IRA once retired, and no new contributions can be made), went 50/50 between the two account types only when their tax rates were 22% or 24%, and contributed to a traditional account (to get the upfront tax deduction) anytime their tax rates are 32%+.

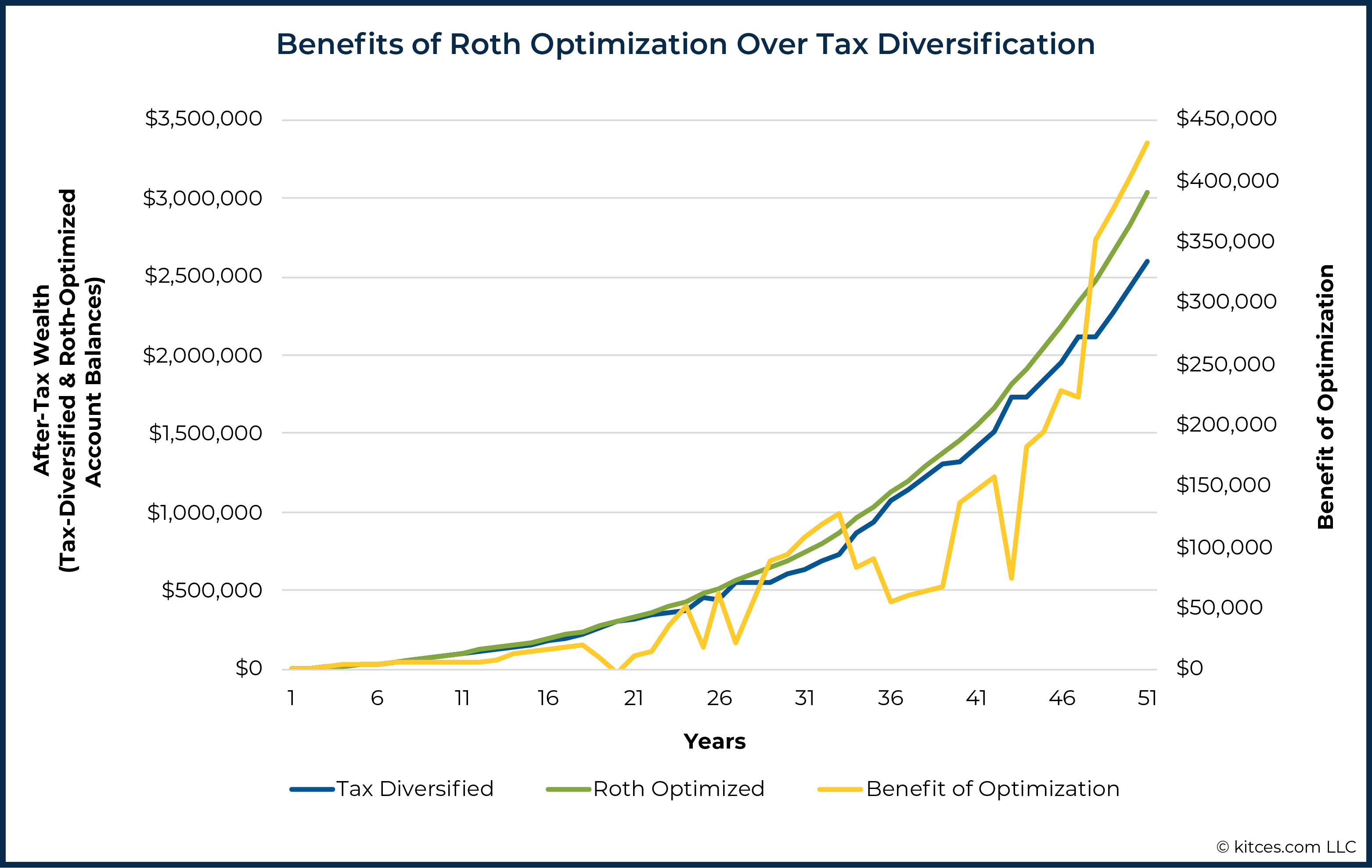

As the results reveal, engaging in Roth accounts more opportunistically (rather than consistently tax diversifying) produces a nearly 10% lift in cumulative lifetime after-tax wealth… amounting to more than $400,000 in additional wealth for optimizing ‘just’ $10,000/year annual contributions ($5,000 per person) for the couple during their working years!

Finding The Equilibrium Point In Roth Optimization

The good news is that, while trying to ‘time’ the markets is challenging at best, ‘timing’ one’s own tax circumstances is far more practical. After all, we know with reasonable certainty our current tax bracket as it exists in the current year, which provides a helpful initial baseline. And through the financial planning process itself, we typically will already be formulating a plan for at least what we’re trying to achieve in the future… which is generally associated with some level of expected future wealth and future income. And from this, our future tax brackets can also be projected!

Of course, the reality is that in some cases – particularly for those that are in the ‘middle’ tax brackets already – the path forward may not be as clear. A married couple earning a strong joint income of $200,000/year and building wealth is already in the 24% tax bracket, and while they may believe they can stay in a 24% bracket even in retirement (by keeping their income to ‘just’ $329,000 or less!) and not creep into higher tax brackets, they may be skeptical about ever getting to lower tax brackets (e.g., it may be difficult for them to get below $81,000 of income given their portfolio wealth and its passive income, Social Security benefits, required minimum distributions, etc.).

Yet, because the potential wealth that can be gained from Roth optimization relative to tax diversification is only created by changes in tax brackets, the truth is that for a household whose tax bracket isn’t likely to change in the future – higher or lower – it doesn’t actually matter which type of account they choose because both will have the same wealth outcome anyway!

But in some cases, tax brackets do move to an extreme, in one direction or another. The otherwise higher-income household has an unusually low-income year (perhaps due to a layoff, an illness, or some other event), or alternatively has an especially high-income year (due to a big bonus, liquidity event, or some other moment of financial serendipity).

And those ‘extreme’ years – with especially high or low tax brackets – are the ones that actually create the most wealth from a Roth optimization strategy… which means in the end, the years that are obviously high- or low-income years are the only ones that matter anyway (for which the decision to contribute to a traditional retirement account or convert/contribute to a Roth account will likely be readily apparent!).

Finding The Tax Equilibrium Point For Current Versus Future Tax Brackets

While tax brackets are graduated based on income, what constitutes a ‘high’ income year for some households may actually be a ‘low’ income year for another. For instance, a household that typically earns $100,000/year would find a $300,000 income year to be ‘huge’, but a household that earns $1M every year would treat it as a very low-income year. Consequently, it’s important to recognize that ‘high’ income years (for traditional IRA contributions) and ‘low’ income years (for Roth contributions or conversions) must be evaluated relative to the household itself.

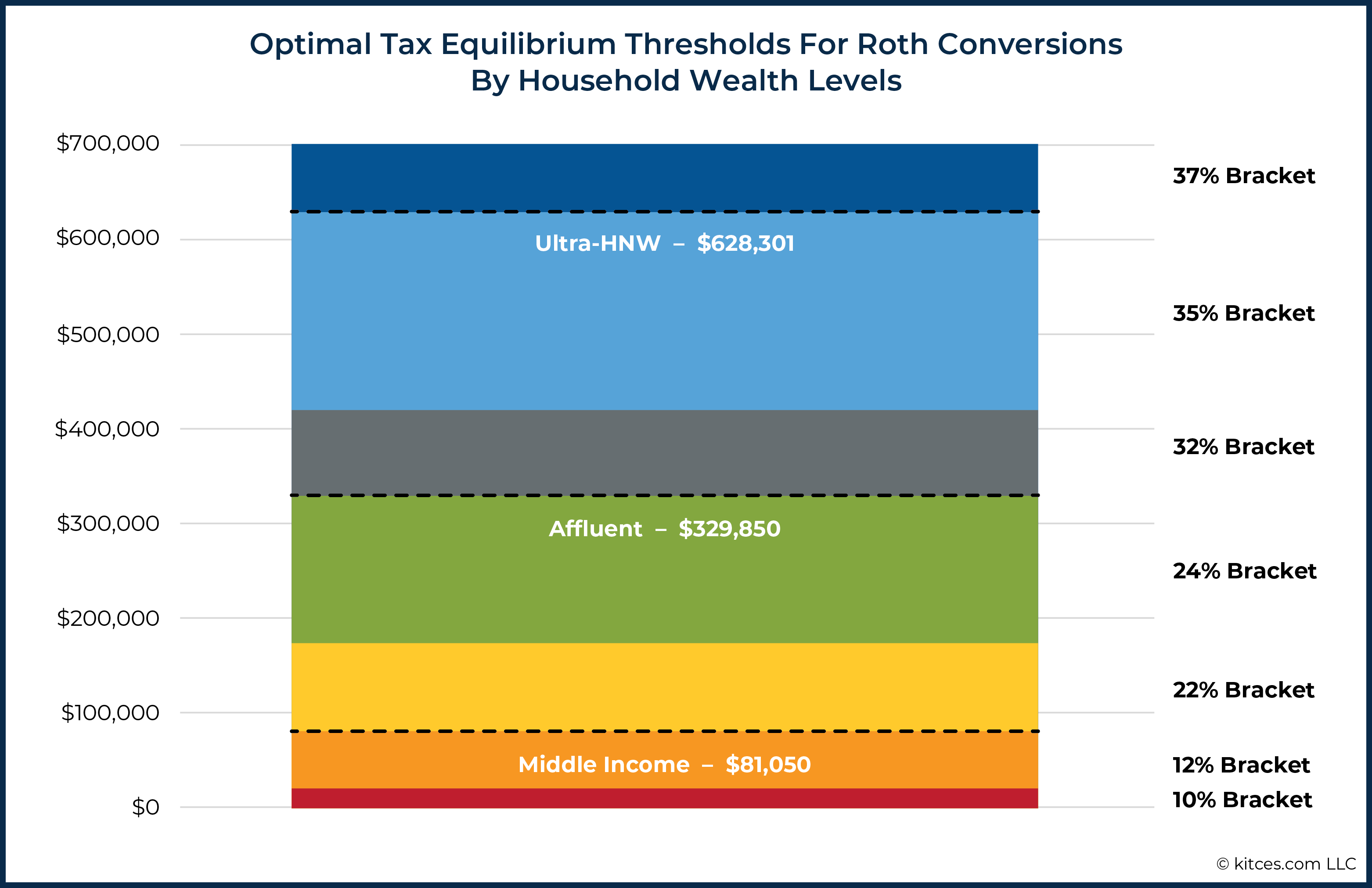

Fortunately, though, the progression of tax brackets lends itself to natural transition points around which Roth decisions can be optimized. In particular, with the seven income tax brackets – 10%, 12%, 22%, 24%, 32%, 35%, and 37% – progressing from one tax bracket to the next is ‘only’ a 2% or 3% increase, with two exceptions: from the 12% to the 22% bracket (a 10% increase), and from the 24% to 32% bracket (an 8% increase). Accordingly, Roth optimizations will largely focus on keeping households that can stay within those 12% and 24% thresholds, to try as best they can to stay within those thresholds… and of course, for anyone whose income is significantly higher, at some point, any tax bracket that is not the top 37% tax bracket will be a ‘good deal’.

Accordingly, the ‘middle-income’ households who are able to remain under $81,050 of taxable income as a married couple in 2021 (eligible for the 12% income tax bracket and 0% long-term capital gains and qualified dividends) will generally want to contribute to Roth accounts as long as they remain under 12%, but use traditional retirement accounts when their income exceeds these levels (to get the deduction at higher rates, in the hopes of withdrawing or converting in the future back at 12%-or-lower rates).

More ‘affluent’ households (e.g., those with one or several hundred thousand dollars of income and/or up to a few million dollars in wealth) who can stay under $329,850 of income as a married couple in 2021 (and thus remain in the 24% tax bracket) may want to more aggressively Roth convert if they are able to leverage the 12%-or-lower brackets, and will want to focus on traditional (deductible) contributions at higher (32%+) brackets.

And ultra-high-net-worth households, for whom any tax bracket that is not the top 37% bracket (at $628,301 of income or higher for a married couple in 2021) would be a ‘good deal’, will likely want to Roth-convert right up to the threshold of crossing from the 35% back into the 37% bracket (and continue to use pre-tax traditional accounts to reduce their income in years when they are in the top tax brackets).

Tax Diversification Versus Roth Optimization To Navigate Future Changes In Tax Law

While many households can maximize Roth optimization strategies by simply focusing on the select number of years where their tax brackets are clearly higher or lower than usual (which, by definition, are the years that matter the most, because they are associated with the biggest difference between current and future tax rates that create Roth value), in some cases the driving concern is not that an individual’s tax rates will be higher in the future (such that a Roth contribution or conversion would be appealing now), but that ‘tax rates’ in the aggregate (i.e., as set by Congress) may be higher in the future. After all, if Congress enacts broad changes to the tax law that increases future tax brackets across the board, then tax rates may be higher for everyone down the road. Which would make Roth accounts the preferred approach for everyone.

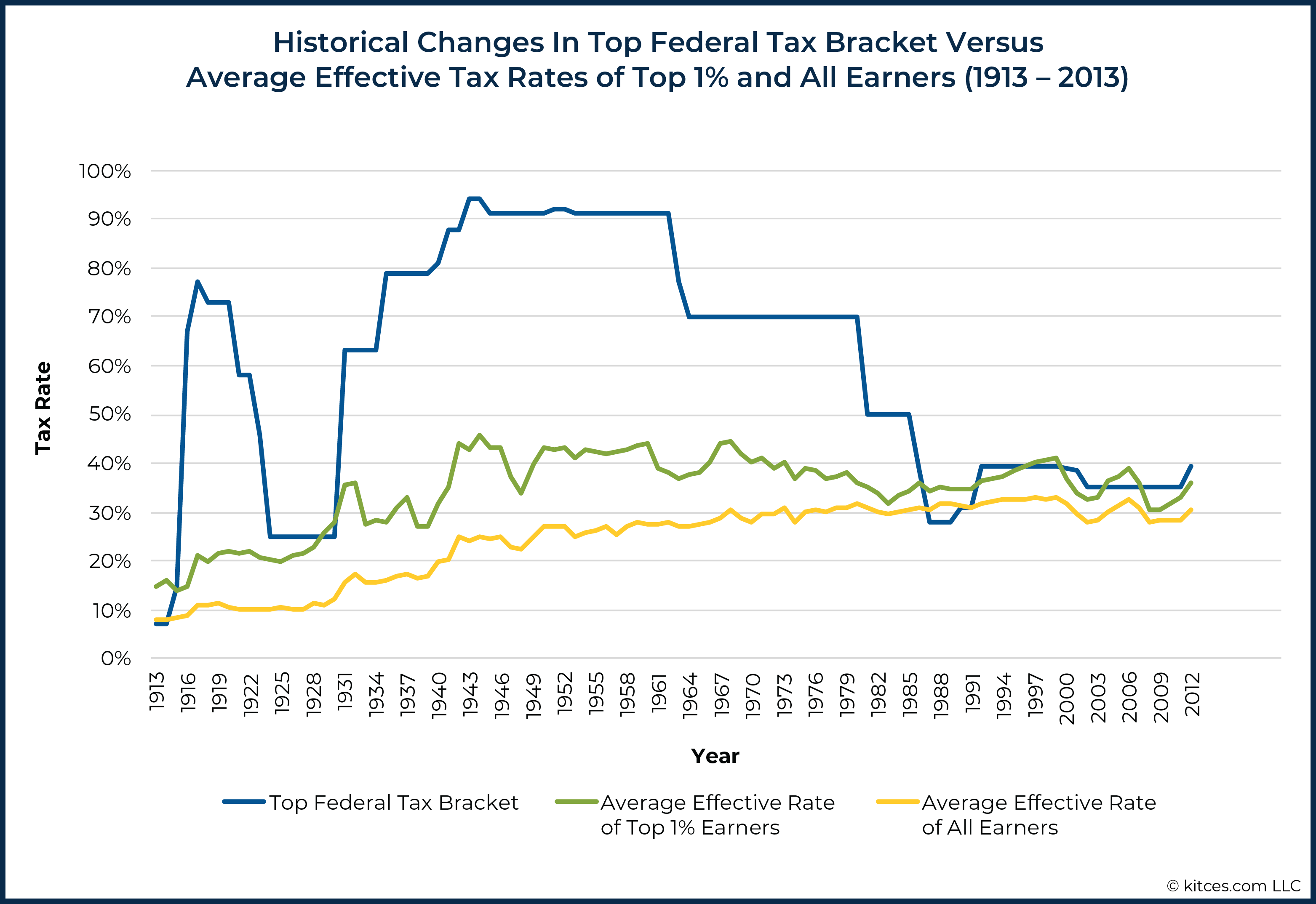

Yet, in the end, while marginal tax rates have changed significantly over the years as tax policy has changed, the actual average (i.e., effective) tax rate that households pay has been relatively stable for decades. In fact, while the top marginal tax bracket has varied as high as 90% to a low of 28% since World War II, the average tax rate of the top 1% has remained in a far tighter range from 30% to 45% over that time period. And the average tax rate of households overall has hovered even more narrowly between 23% and 33% (with much of that increase the result of expanding payroll taxes, not changes in income taxes).

In other words, because Congress tends to change deductions and other rules at the same time they change the tax brackets (adding deductions that mitigate the impact of increased tax rates, and curtailing deductions alongside decreases in tax rates), in practice, the tax system is more stable than most realize, and the variability of a household’s individual tax circumstances is much wider – and therefore presents a greater planning opportunity – than trying to figure out the net effect of future tax law changes. Especially when recognizing that even if overall tax burdens go up in the future, it may not be in the form of an income tax bracket increase (e.g., Congress might implement a wealth tax, or a consumption tax, or some other approach that would not benefit the decision to use a Roth account!).

Whereas a household that typically is in the 22% tax bracket is experiencing an off-year in either the 12% or 32% tax bracket has a known 10%+ swing that can be capitalized upon immediately (or alternatively, the household that plans to retire in a different state, which could entail a 10%+ change in marginal tax rates simply by moving!).

Ultimately, while the uncertainty tied to the tax system – both with respect to a household’s own tax rates as income rises and falls over time, and the potential for Congress to change the laws themselves – introduces a non-trivial amount of tax uncertainty, engaging in ‘tax diversification’ by splitting dollars between Roth and traditional retirement accounts doesn’t necessarily improve the situation. Instead, choosing to pursue Roth accounts simply narrows the range of future outcomes, eliminating the ‘downside’ risk of tax brackets moving the wrong way… and also eliminating all of the upside potential of making good tax planning decisions. Which means in practice, tax diversification doesn’t diversify the opportunity; it takes the opportunity off the table altogether.

The alternative instead is to focus on opportunistically utilizing Roth accounts – whether in the form of a contribution or a conversion – specifically to leverage the Roth benefits in low-income years, while capitalizing on the good ‘old-fashioned’ benefits of traditional retirement accounts to defer taxes in high-income years (when, by definition, tax deferral is most valuable because the tax rate is higher!). As while in most years, households may not have a clear view on which direction their tax rates are going to go, but if their tax rates don’t change much, it doesn’t actually matter which account is chosen anyway! Instead, the Roth-versus-traditional decision matters the most when there is a significant difference between current and future tax brackets… which means that most of the tax planning opportunity really can be captured by ‘just’ focusing on the few years when income has clearly moved to an extreme for that household (to the upside or the downside).

Fortunately, though, significant changes in income often are clear at the time, whether due to imminent plans for a change (e.g., retiring to a state with a materially different tax rate), a major challenge that reduces income for the year (e.g., laid off, an illness, or a business loss), or an ‘upside surprise’ that makes it an especially good year to capitalize on traditional deductions (e.g., a big bonus, or a business liquidity event). Which provides the opening to consciously contribute fully to a traditional retirement account (in high-income years) or to a Roth account (via contribution or conversion) in low-income years. Because splitting dollars between Roth and traditional accounts may be fine in years where income is ‘in the middle’ and there is no clear direction, but a broad policy of tax diversification will, on average, lag a more proactive approach of Roth optimization, even if it only gives taxpayers something to ‘do’ once every few years!

In the situation of tax rates staying level for life, would Roth accounts edge out Traditional by the ability to contribute more? While both have the $6(7)k/yr cap, $6k after tax is worth more than $6k before tax. If someone has a 20% tax rate then is maxing their Roth really like getting $7,200 into an account that will grow tax free? Even if you put $6,000 into a Traditional and an additional $1,200 into a taxable account the Roth should still win, right? Thanks for the article, very interesting as always!

Jared,

Yes, for those who can cap out contributions to a Roth account, there is a slight positive tailwind for the Roth account, all else being equal on tax rates.

Notably, though, the tailwind is only fairly slight, though, and it takes only a modest shift in tax rates at ANY point in the future to more-than-offset it. (Even just moving to a lower tax rate state in retirement can be enough.) See https://www.kitces.com/to-roth-or-not-to-roth-may-2009-issue-of-the-kitces-report/ for a more detailed analysis of this. (Numbers there are a little dated, but the relative effect size for the benefit of maximizing Roth contributions is still similar today.)

– Michael

I always appreciate your insights but Jared’s point is critical. Your being atypically inconsistent by both claiming the Roth and pre-tax IRA are identical when tax rates don’t change and then saying the Roth advantage, highlighted by Jared, is not significant if tax rates change. The Roth has an advantage. It may not be significant but with an unknown future it could be larger or smaller than estimated now.

Also, the flexibility of having both may also be more significant than your article and comments suggest. The impact on Medicare premiums could be significant for lower income individuals. Some NY City housing subsidies are tied to taxable income and so the Roth could allow other government support too. The ability to make charitable donations from pre-tax accounts during lifetime or at death provides additional advantages for more wealthy clients.

Roth and pre-tax are not negatively correlated like negatively correlated investments which cancel out each other. They are both tax deferred and the combination allows some possibility of control of income and tax rate. The combination simply takes advantage of the unknown nature of future tax rules and income and allow the taxpayer the potential opportunity to take advantage of opportunities when they arise.

For most people (anyone with a retirement plan at their job or their spouse’s job), traditional IRA contributions are not tax-deductible if you are in a high tax bracket. Your only option at that income level is to contribute to a traditional IRA without getting the deduction. You can immediately roll it over to a Roth IRA so that the earnings will be tax free, or you can leave it and pay taxes on the earnings later, but you can’t deduct the contribution either way. The tax-optimized strategy is simplified for IRAs to always contribute to a Roth IRA when you are below the income limit, and do a backdoor Roth IRA contribution if your income is above the Roth limit. The backdoor Roth is only optimal if you don’t have significant assets in a traditional IRA, because you will have to pay taxes on the conversion amount in proportion to the percentage of the assets that have not already been taxed.

Additionally, many people in upper tax brackets can max out their contributions and still pay the tax on the Roth contribution, so the tax payment now will come out of a taxable account, rather than reducing the contribution to the retirement account. Growth will generally be lower in fully taxable accounts, from a combination of using tax-avoidance strategies and paying taxes on some portion of the earnings every year, but could be higher if it is held long-term in an index fund. This further complicates the analysis.

401k contributions are tax-deductible at any tax bracket. This includes a self-employed 401k. So this tax avoidance strategy mostly only applies to people who have the option of choosing between a traditional 401k and a Roth 401k. Although it also applies for timing conversions of assets from traditional accounts to Roth accounts. It can also apply for timing which account to withdraw money from, as you should withdraw from a Roth account in years with unusually high income (possibly from sale of a house or large amounts of long-held stock in a fully taxable account) and a traditional account in most other years.

The strategy could also apply to people with low or moderate income that is highly variable, but that is an uncommon situation. Most people with income below $100k don’t have significant income variations except for periods of unemployment, when contributing to retirement accounts probably isn’t feasible anyway.

Excellent article Michael! Below are a few additional, somewhat predictable changes, that taxpayers may want to address via ROTH vs. traditional arbitrage:

1. Married couples may die in the same tax year, but not usually/always, especially if their ages are significantly different. Once the survivor must file as a single taxpayer their brackets shift dramatically. If their income does not decline commensurately, their marginal tax rate will increase. This may be a consideration for some couples.

2. Taxpayers who are likely to leave a significant legacy to their heirs, should consider the impact of inheriting significant tax deferred assets. Projecting the tax bracket, career state, etc., of heirs, over a likely demise timeframe, may point to greater ROTH vs. traditional contributions and/or ROTH conversions. The SECURE Act has likely increased the number of affected taxpayers.

3. In a similar vein, those with charitable intent may not want to lean towards ROTH accounts, if they intend to benefit favored charities, upon their demise. To the extent they intend for charities to be beneficiaries of their retirement accounts, they should avoid ever paying taxes on those amounts.

In addition, some taxpayers need to consider situations beyond federal and state marginal tax rates, e.g., ACA subsidies, Social Security taxation, EITC, CTC, etc. Taxpayers who may qualify in those low income years for credits need to carefully analyze the tax implications of choosing ROTH vs. traditional retirement savings accounts.

Thanks for all you invest in educating us all!

While theoretically correct (not sure why it took 5 pages and 7 graphs), this article misses an important practical point in favor of having some substantial portion of your wealth in Roth or after-tax account. Having those accounts actually provides one with optionality to withdraw or not to withdraw from the traditional IRA or 401K accounts. Otherwise, how else will one cover its living expenses?

If your future tax rates are lower, the optionality value is negative… if your future tax rates are higher because you’re accumulating so much wealth that you anticipate you’ll “need” tax-free income to cover living expense, it’s not optionality, it’s simply a projection of higher tax rates that drives more Roth dollars. Which is precisely the framework we set here. If you project higher future tax rates (due to wealth creation or other reasons), you need to be able to withdraw from Roth IRA accounts to avoid taking traditional IRA withdrawals at those high tax rates. But it’s not actually optionality that drives the outcome. It’s outright future tax rates (and/or projected wealth/income that will lead to future tax rates). 🙂

– Michael

What about the flexibility to cover large one-off expenses while controlling tax the tax bracket for qualified withdrawals?

One additional thing to consider for retirees is Medicare plan B costs which rise significantly at higher income levels. I’m running into this due to RMDs. Hindsight, it would have been better if I had overweighted ROTH or converted more traditional IRA-ROTH earlier.

Yes, IRMAA surcharges on Medicare Part B (and Part D) does matter. Though in the grand scheme, it’s actually not a major impact, as it amounts to little more than a roughly-1% marginal tax rate increase overall. (See https://www.kitces.com/blog/income-thresholds-for-medicare-part-b-and-part-d-premiums-an-indirect-marginal-tax/ )

For someone who is close to an IRMAA threshold in any particular year, it matters a lot. (Since just $1 over the line incurs the whole next tier of surcharges.) But from the ‘full lifetime’ perspective, changes in tax rates on the WHOLE retirement account is still an order of magnitude higher than the incremental IRMAA savings. (e.g., if you convert IRAs at 32%+ to get Roth dollars at 22% or 24% to stay under IRMAA thresholds, the 8% – 10% change in tax rates is far more impactful on a sizable IRA than the Medicare surcharges would have saved).

– Michael

The article to which you link indicates a 1.5% marginal cost impact. This goes higher as you pass IRMMA thresholds. And for a married couple that both pay for Medicare the marginal rate become 3%. So isn’t it worthwhile to do Roth conversions at 24% if you can push future MAGI down below $176,000 where IRMMA kicks in.

I don’t think we give enough credit to tax deferred accounts. I love Roth IRA’s for people in the 12% or lower. For people in the 22% and 24%, I think it depends on how their situation. I don’t think it’s a level playing field for anyone on the 22% marginal tax bracket and beyond though. Many states give a tax deduction for tax-deferred contributions, then turn around and never tax those accounts. Also, I think it’s important to note that tax deduction for retirement accounts provides a benefit at marginal tax rates. At withdrawal, especially now that pensions are more rare, much of the IRA distributions could (and probably would) be taxed at lower tax brackets even when an individual is in the same marginal tax bracket. For example, someone contributing at the 22% federal tax bracket and withdrawing at the same tax bracket but has no other income (or at least not enough to fully fill in the 10% and 12% brackets – most people probably fall in this category) would have some of their IRA distributions taxed at 0% (standard deduction), 10% and 12%. Therefore, their tax-deferred distribution would effectively be taxed at a lower rate even though marginal rates are unchanged. With some planning this can be even more prevalent. Any thoughts on this?

Indeed, here in NY, $20K/person/year of the withdrawals from a pre-tax retirement account are not taxed by NY after age 59.5. This favors doing roth conversions in early retirement versus saving in roth accounts prior to retirement.

Yet another nuance here is that typically by the time we are laid off in September of any given year, making that year a lower income year, we have already contributed on a pre or post tax basis to our employer’s 401K.

In the end, we will never be able to know what the optimal retirement savings strategy would have been until once the saver is dead! But I found this article very helpful even if it couldn’t possibly cover all the variables that impact taxation.

Kay

There is an overlooked angle on marginal versus average tax rates between the two.

The IRA gets its original deduction at the marginal tax rate, but pays back an average rate when withdrawn as income, taxed across 0 (standard deduction), 10%, 12%, 22%, etc and paying an average tax rate overall. There’s not a flat 15-25% tax on the future withdrawals as illustrated.

The Roth pays taxes up front at the highest marginal rate (same place the IRA gets the deduction). So unless those future average rates on the IRA withdrawals are equal to the top marginal rate the Roth paid initially, it’s not a simple wash on the taxes.

While I agree with you there is not a significant difference in Roth vs traditional or the 50-50 approach, there are 2 reasons why Roth IRA could make a big difference. Roth IRA allows you to withdraw principal amounts anytime so for a 25 year old, there may not be much benefit traditional versus Roth at age 65, but there is a big difference in liquidity at age 40 if the person faces unemployment. All the contributions in principal amount can be withdrawn tax free and as you explain if the person really finds another job later on in the year, you can always convert from traditional back to Roth to replenish the account in a low tax year. I can’t exactly give figures but folks who have Roth IRA’s overtime will need less in emergency savings amounts because of the liquidity Roth IRA’s provide. The other part is that lets say you have 1 million in Traditional and 1 Million in Roth IRA at age 65. If you need a large amount to help your kids buy a house, lets say like 300K, Roth IRA is so flexible because the large one time withdrawal wont tip you into a higher bracket.

Have you perhaps overlooked the ultimate impact that these decisions have on taxes later on in life – post age 72 when RMD’s are mandated? What about the net inheritance for the heirs since the Secure Act has so drastically altered (unfavorably) the prior ability to stretch the IRA withdrawals over the single life expectancy of the heirs (vs. now over a 10 year period and therefore large IRA inheritances may well be distributed more quickly, thereby causing higher taxes due to a more condensed distribution period (and possibly on top of other income the heirs have during what could statistically be their own highest earning years. Lastly, if the converted amount in the Roth is invested more for growth (equities for a long-term goal plus the government no longer will share in the future growth) then counter balanced by a more conservative allocation for the still traditional (unconverted funds) since these funds will likely fund the retirement expenses since the Roth money is now basically being managed as the future inheritance for the next generation(s).

I feel like your discussion, was clinical and mathematically sound, but missing some obvious opportunity’s to manage a tax burden for the current and future generations and ignoring the possibilities of compounding being pushed to the Roth for a more efficient and superior outcome for the family comprehensively (especially with the extra 10 years available post death for the Roth funds to grow without any tax dilution to yield a notably higher net outcome to generation number 2 (even without tax rates going up… and to an even greater advantage if tax rate increase further.

Great article and great points Gary. On a similar note, for individuals that may have enough pension and social security income to cover most retirement expenses, Traditional IRA & Roth IRA funds may largely be left to grow in sheltered/tax free accounts as long as possible and then passed to heirs upon death. Isn’t the fact that there are no RMDs for Roth accounts a very significant Roth advantage for individuals in this situation? Even perhaps enough of an advantage if the retirement tax bracket is the same as the bracket when the funds were put into the Roth?

For us in states with an estate tax, especially one with a low threshold, Roth conversions can be useful, even if it is not a big issue with federal income taxes.

Exactly. Now that my family is facing that threshold, we are maxing out Roth conversions as fast as our present income tax bracket will allow.

Nice article. Might you elaborate on this article versus your fantastic article several years ago, “Tax-Efficient Spending Strategies From Retirement Portfolios”. In that article, doing strategic Roth conversions seemed to have a major impact on how long savings lasted. Yet this article and other more recent ones I have read seem to indicate the impact of conversions is very small. What is your opinion, Roth conversions can have large impact or only small on overall money available in retirement. This question is focused only on the post retirement period.

This article is great, but leaves out two important factors. The first is that one can always convert more to a Roth, but can’t recharacterize back anymore. This creates a strong nudge in the middle-bracket (22-24%) years to choose traditional, since as Michael points out it’s a wash if one retires in middle brackets as well, but any low income year provides an opportunity for a conversion and significant rate arbitrage. You always want some surplus pre-tax to be able to use those opportunities.

The other is IRMAA. That’s a good reason to convert to Roths and fill the 22-24% near the last few years before IRMAA/Medicare look backs start becoming relevant to lower the effect of RMDs on IRMAA rates. And also the 2.8% net investment tax.

Fantastic as usual, but two more points to consider. Behavior and large one time needs.

Behavior – Let’s say we have an average clients who lives in the 22%-24% tax brackets. Most of my clients live their life out of habit. If they get a bonus, the money finds a use, if they have some big expenses, then they tighten the belt. When it come to Roth vs Traditional, this behavior favors the Roth. The tax savings of the traditional contributions is just white noise to the client and will be absorbed by “life”. However the power of tax free compounding on a tax free account over 10-40 years is incredible. So score 2 points for house Roth.

One time needs – I’ll never forget when a 70+ client whose taxes I was preparing (I’m and EA not a financial planner.. yet) came to me with a $30,000 additional IRA distribution because they needed a new roof. They told me they new that they took out a lot and that they extra withholding to cover. When we were wrapping up I told them their taxable income was up over $50k. “Oh Matt, you must have made a mistake, we only took out an extra $30k…”. But there was no mistake. They had previously had only a couple of dollars of taxable social security and now it was almost full taxable. They owed a pile of money and cried at my desk. I felt horrible because with some planning we could have really minimized the problem. One of the strategies that would have solved this would have been simply having access to a Roth IRA. If they had done split contributions over the years and taken some or all of that lump sum distribution form a Roth, then the problem would have been small or gone.

So even for an unsophisticated everyman I am a huge advocate of having at least one “roof’s” worth of money in a Roth IRA, and then talking with your accountant (or planner) before taking out chunks. Score 2 more point for house Roth.

Michael, I’m confused by this assertion:

I thought the marginal tax bracket was all/mostly what we cared about when making this pre-tax vs Roth decision? Because these $s come off the top. So, don’t we very much care that the top tax bracket has varied between 28% and 90%?

I’m not sure I follow this:

It seems like what we really care about is what would have happened had we contributed to traditional vs. Roth. So the variable of interest is the relative difference between the two approaches (in ending wealth) under different tax rate change scenarios. And a 50/50 split would seem like a reasonable starting point for helping mute the variance of this variable.

By the way, I don’t think this takes away from your argument for optimization.

Loved this article.

A factor for me was that I could effectively put more into tax advantages accounts by electing Roth over the years (maxed out various options). And, very importantly, since I was in a volatile and somewhat risky industry with personal guarantees for my business obligations, the more money I had put away in such accounts, the safer I was should the worst occur. Especially true of 401k and similar accounts, and the segregated rollovers to IRAs and Roth IRAs from such sources.

While not all may benefit from this protection, and I never had to test this due to a guarantee call, it was always possible and could have been devastating financially to me. Helping bring me peace of mind as well. Totally worth it for me.

Thanks again for your excellent work and thought provoking articles.

Michael, thanks for your excellent analysis and Roth optimization strategies. The take-home message for me (and additional optimization strategy) is that if investors aren’t fully invested, they could choose to pay some/all of the Roth conversion-related taxes with non-retirement funds. In the pay-all scenario, the full $5,000 could be converted, making the Roth option the better choice.

All of this leads me to question how many investors are fully invested. And, if being fully invested is the right strategy for Roth conversion candidates given the uncertainty of conversion opportunities.

I see your point but I wouldn’t call that a fair equivalency. If they’re willing to let go of those funds to pay the tax bill on the Roth contribution it would only be fair to say those funds could also be put into the tax deferred account.

Michael,

Have you read the recent paper (June 2021) by Ed McQuarrie “When and for Whom are Roth Conversions Most Beneficial? A New Set of Guidelines, Cautions and Caveats”?

Notwithstanding your invaluable contributions to the advancement of knowledge in Financial Planning — and on this subject in particular—it is the most thorough analysis of Roth conversions I have come across so far.

It would be great to hear your take on it.

Available at SSRN: https://ssrn.com/abstract=3860359 or http://dx.doi.org/10.2139/ssrn.3860359

Similar to several posts below, I found that not focusing on future RMD’s is a big hole in the article. Let’s say that via “Roth optimization” you end up with a large amount in traditional IRA. Come RMD time, you will have a very large forced withdrawal which will be taxed at some future rate. Whereas if you had put a larger amount in the Roth IRA, you would have a smaller forced withdrawal and therefore better able to manage future taxes.

My strategy has been to convert my 401k to Roth IRA subject to two constraints: 1) never go above the tax bracket threshold I’m in. 2) convert such that the RMD’s associated with the amount left in the 401k and traditional IRA’s is about equal to or less than what I will need to withdrawal in the future years. That way if tax rates drop, I can withdraw more from my 401k and if tax rates increase, I can withdraw from my Roth. Is this wrong?

I notice there are many people who believe Ed McQuarrie’s article on Roth Conversions being not really very beneficial. However, I believe there is one factor that was omitted in the McQuarrie article that make it invalid. The consequences of RMD’s. While it is true the non-Roth account can grow at a fast enough pace to equalize the after tax net value, this truth is only valid for accounts which are not (yet) subject to RMD’s. Once the RMD’s kick in the non-Roth must suffer a diminishing principle, yet the Roth account can continue to grow tax free. Those returns enable the Roth account to surpass the non-Roth account. Even more significant: The RMD’s can often force the investor into a higher and higher tax bracket as the investor ages and RMD’s unrelentingly climb. (Contrary to the McQuarrie case study where he claims Rob and Sue mostly stay in the 24% marginal rate, it actually is easy for someone in the Rob and Sue situation to have their RMD’s grow substantially. In fact, I think McQuarrie made a mathematical error in his case study. I’m not certain of his error, but I can only get his results if I presume no growth on the basic IRA account from which the RMD’s are calculated and extracted. Presuming an average growth, and likewise presuming an average growth in Social Security, Rob and Sue are quickly found in the 32% and then 35% tax brackets. With this calculation, the McQuarrie results are completely nulified.) Getting money out a non-Roth IRA account is always a good idea IMHO. This tax equivalency argument may be true, but it is a red herring…. (a valid distraction, but not probably the deciding point.) There is yet one more factor ignored in the article and that is the payment of capital gains tax. As RMD’s go up, so too will the vulnerability to higher brackets for capital gains. The “outside IRA/Roth-IRA account” in which the RMD’s might be saved or from which tax obligations on the conversion are paid (probably) have capital gains associated. In other words, the Roth-IRA account can accumulate gains without vulnerability to this tax, but the funds that are in taxable accounts will potentially be liable for up to 43% CG tax (presuming the RMD’s force the investor above $1M/year MAGI)… which it turns out is surprisingly easy given a relatively long life….

Good points…what portfolio would you lean to for conversions vs. charity? Yes, you will say it depends but I do both – convert and want to give to charities. ,,,,$5M, $10M, $20M?

I look at the roth for tax free income in the future 70s and 80s. Heirs are not apparent presently.

Since it’s end of year crunch time, of course I found this article now. It is wonderfully thorough on the topic, considering a variety of perspectives/income levels. One criticism: I don’t see where Mr Kitces took into account the beneficial arbitrage of tax rates when your trad IRA is your primary income source in retirement. If you save at a 35% bracket going in, then pull out to pay tax later, even if marginal rates are higher later, you will fill lower brackets in all cases first. Mr Kitces portrayed diversification as essentially meaningless but it seems at least some trad IRA money is going to be useful.

IRA distributions exceeding $34,000 triggers income tax on 85% of Social Security benefits, and $91,000 triggers the Medicare IRMAA surcharge.

If a person expects to be in the same marginal bracket both now and in retirement (e.g. 22%), would it make sense to do as high a Roth conversion as possible each year before retirement without exceeding that marginal rate, until the IRA balance is low enough that the annual IRA distribution in retirement would be less than $34,000 (or $91,000)?

In other words, if paying 22% income tax on Roth conversions before retirement is no different than paying 22% income tax on IRA distributions during retirement, why not do the conversions, in order to avoid the SS benefits income tax and/or the IRMAA surcharge?

Very late to the party here, but I wanted to thank you for articulating so many important points so well, Michael (on this and all your articles).

My 2 cents is that debating these rules of thumb is helpful, but I feel that you really have to do comprehensive financial planning software projections that capture the unique situations of the clients you serve (and add 10 years of xls after surviving spouse’s death for the beneficiary IRAs…unless there’s software that does that now) to know for sure what approach each year makes sense. Then you can capture all the moving pieces, potential stealth taxes (social security, cap gains increase, NIIT, IRMAA, etc.), etc. and provide the best recommendation possible each year.