Executive Summary

As we begin another new year, a fresh set of challenges and opportunities await the world of financial advisors. The themes remain the same as years past – technology, regulation, and practice management – but the landscape is shifting and changing.

In terms of technology, 2014 seems to have been the year of the “robo-advisor”, but I anticipate that 2015 will be the year of “robo-advisors for advisors”, with a looming explosion of financial technology (or “FinTech”) for advisors. While the robo trend has not actually picked up much in the way of client assets, it has clearly highlighted the lack of competitive technology solutions for advisors, and that’s a business opportunity a number of new businesses are aiming to solve. After years of having few and poor choices for technology, 2015 may be the first year of a new trend, where the challenge for advisors is making a decision in a sea of overwhelming (though not necessarily all good) choices instead.

With respect to regulation, we face yet another year of potential proposals on a new fiduciary rule, but with the Department of Labor set to announce their fiduciary redraft as early as this month, we may finally be about to move on to the next stage of the debate. In the meantime, regulators are poised to make mandatory succession planning (or at least, business continuity planning in the event of death, disability, or retirement of the advisor) as the surprise “hot” issue of the year, and the first half of 2015 will also witness an outcome to the case of Camarda vs CFP Board – which, win or lose, will have significant ramifications for the role of the CFP Board and its marks in the future of the financial planning profession.

The third big trend for advisors in 2015 is the ongoing slow-motion “crisis of differentiation” unfolding amongst advisors. As organic growth rates slow for the entire industry, there simply aren’t as many “unattached” clients as there once were, and as more and more advisors step up to deliver financial planning and wealth management, being an experienced and credentialed advisor just isn’t the differentiator it once was. In the coming year, I anticipate we’ll see a lot of advisory firm taking a hard look at their current marketing approach, sowing the seeds of a future niche or specialization to reignite their growth in the future, and/or making a commitment that it’s no longer enough for the average firm to spend a mere 2% of revenues on marketing anymore.

Robo-Advisors For Advisors – An Explosion of Advisor FinTech

As predicted in last year’s Top Issues article, the robo-advisors vs (human) advisors discussion dominated the industry news cycle in 2014, even though the reality is that the true robo-advisor platforms have little more than about $3B of AUM collectively, in what’s estimated to be a $33.5 trillion marketplace for investable assets. Notwithstanding their paltry assets and 0.01% market share, though, the real impact of the robo-advisor trend on advisors is not taking clients from them, but casting a bright light on the poor quality of technology solutions available to them, especially for their use as a “front office” interface with clients. From an entirely digital onboarding process, to a nice web portal and app for clients, the robo-advisors built from scratch what many of today’s (human) advisors haven’t been able to buy even if they wanted to. Expect that to change in 2015.

In the coming year - starting with next month's T3 Advisor Technology conference - I anticipate that we will witness an onslaught of new companies seeking to serve advisors, providing them tools that allow them to “compete” with robo-advisors (though in truth it’s more about serving their own clients better than any actual head-to-head competition). The emerging trend actually began in late 2014, with some early robo-advisor incumbents that have had slow revenue growth in the direct-to-consumer market pivoting towards advisors, including the launch of Betterment Institutional, Jemstep Advisor Pro, and Motif Advisor. In 2015, expect to see even more new startups that attract (modest) venture capital funding to pursue advisors right out of the gate and try to turn them into “cyborg” (or “bionic” tech-augmented) advisors; Upside Advisor started down this road in late 2014, and more will follow. And of course, some of the large-firm incumbents (custodians and/or broker-dealers) will build their own solutions as well, like Schwab Intelligent Portfolios, while the rest feel significant pressure to either create their own, too, or partner with new providers to bring similar solutions to their advisors.

What will change as these robo-advisor-for-advisors platforms come forth is a recognition that robo-advisors were really just nice technology for a paperless onboarding process and ongoing interfacing with clients, built on top of a relatively simple passive TAMP solution with automated rebalancing software. In the first stage, robo-advisors began the process of turning passive strategic asset allocation into a commodity at a low price point of 0.25%, justifying their value with a technology-augmented superior client experience. In the next stage, human advisors will get access to the same “robo” technology, offer it to clients as a free giveaway while they layer additional value-added (e.g., financial planning) services from (human) advisors on top, and raise the question of why consumers should pay a robo-advisor anything at all.

The caveat to the prospective explosion of Advisor FinTech in 2015, though, is that it may create more confusion than really solve problems, at least for now. An emerging plethora of choices will actually make it difficult for advisors to decide which vendors to adopt (or even find the time to analyze and compare them all), further complicated by the fact that many will be startups that don’t survive (forcing the advisor to vet the company’s management and business model for survivability, or risk being forced to change software again in a year or two). The lack of clear industry data standards will require software integrations to be an ever-expanding and unmanageable (for most vendors) volume of point-to-point integrations, making it a struggle for advisors to patch together which software and tools will work with which other software and platforms. And many custodians and broker-dealers may use this technology fractionalization as an opportunity to launch a fresh wave of proprietary solutions for “their” advisors, creating a new form of “technology handcuffs” that will make it harder for advisors to change platforms in the future (after what had been a trend towards greater advisor flexibility across platforms in the past few years).

Notably, the coming wave of new advisor FinTech may also finally solve some of the biggest gaps in the advisor technology stack – the lack of a centralized Personal Financial Management (PFM) portal for clients, and also a centralized practice management dashboard for advisors. And expect to see some new FinTech categories emerge as well, such as the next generation of trading and rebalancing software to create “Indexing 2.0” solutions that threaten to make mutual funds and ETFs irrelevant (the robo trend’s biggest true disruptive threat to the existing financial services industry).

Regulation – Camarda vs CFP Board, the DOL on Fiduciary, and Succession Planning for RIAs

While the CFP Board is not technically a regulator (at least from a legal perspective), its enforcement actions as a quasi-regulator for financial planners have landed the CFP Board in a lawsuit with CFP certificants Jeff and Kim Camarda, who have sued the CFP Board to block it from publicly disciplining them over their use of the “fee-only” term in their compensation disclosures. The stakes in the Camarda case are significant for the CFP Board, both financially, and as a validation (or repudiation) of their legitimacy to be an enforcer of professional standards for financial planners. With depositions done and still no settlement in sight, the case will likely go to trial and come to a conclusion in the first half of 2015. Win or lose, the outcome will have significant ramifications for the future role of the CFP marks, and the CFP Board itself, in the regulation of financial planning as a profession.

In the meantime, the second (and final?) draft of the Department of Labor’s proposed fiduciary rule (including, most controversially, the potential expansion of the fiduciary duty to advisors who recommend rollover IRAs) is still scheduled for release to the Office of Management and Budget (OMB) in January; assuming the rule really does come forth, expect to see a great deal of debate in the first quarter of 2015 as OMB has 90 days to review the rule for potential adoption. And of course, if the rule is ultimately implemented, 2015 will just be the first of a multi-year transition process into a new fiduciary framework that will impact many advisors who are not currently subject to a fiduciary duty under FINRA. And win or lose for the DOL, the outcome of the fiduciary rule may ultimately be an indicator of whether or what action the SEC takes on a potential uniform fiduciary standard for all advisors, which matters whether you're a FINRA registered representative, or an SEC- or state-registered investment adviser.

The other notable regulatory event that may be coming in 2015 is a series of new requirements for investment advisers to have (documented) succession plans in place. The North American Securities Administrators Association (NASAA) has proposed a model rule that would require all state-registered investment advisers to establish a succession plan to handle the potential departure of the advisor (especially founder/sole proprietor) from the business, which after an extended comment period this past fall is expected to be implemented in the coming months. And the SEC recently announced that it may consider a similar succession planning rule for Federally-registered investment advisers in the fall. In truth, the rule proposals are really more about business continuity in the event an advisor dies or becomes disabled, and facilitating a smooth exit transition, than requiring “true” succession planning; nonetheless, expect to see regulators putting a lot more focus on requiring a plan for what happens to an advisor’s firm and his/her clients, in the event that something happens to the advisor.

Slowing Growth Rates And The Growing Crisis of Advisor Differentiation

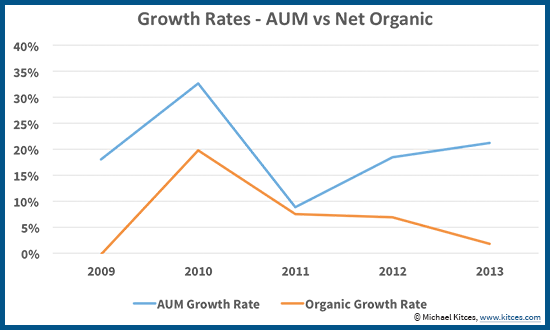

The past 5 years have been marked by a raging bull market that has dramatically lifted the AUM and revenues for virtually all advisory firms; according to the latest Investment News benchmarking study, the average advisory firm has nearly doubled over that time period, now up to over $200M of AUM with 2 partners and a staff of 7. Yet buried within those numbers is a concerning trend; while AUM (and revenues) are up, the “growth” is increasingly coming from just the tailwind of market returns, and once market returns are backed out the underlying net organic growth rates are rapidly approaching 0%.

Slowing growth rates in the aggregate suggest that the landscape for advisors has changed from what it once was, and that there simply aren’t as many new client opportunities as there were in the past. In a sign of maturation for the advisory industry overall, there just don’t seem to be as many “un-attached” clients (those without an advisor at all) as there once were. For better or worse, the majority of people who will work with an advisor may already be working with one now, and most of the rest are purely self-directed and likely never will; at the margin, there are only so many prospective clients on the table for everyone to compete for, and there just aren’t many referrals to get from existing clients when everyone they know either already has an advisor of their own or doesn’t want one at all!

In turn, this slowing of advisor growth rates means the competition is fiercer than ever for the few new clients that are available, and for many firms their growth will only come at the direct “expense” of taking clients from competing firms. Which is difficult, as most advisors define their “differentiators” in a substantively identical way; give or take a little, it’s virtually always: “We provide customized, individualized financial advice to our clients, delivered from well-educated highly-credentialed advisors who have several decades of experience.”

The fact that actually doing customized financial planning as an experienced and educated advisor is no longer enough to be compelling to a prospective client (especially when trying to draw a client away from an existing advisor with similar experience and credentials) is putting pressure on advisors like never before to truly differentiate themselves from the competition, amidst a sea of other advisors who all say the same thing. Advisors are inevitably being pushed towards niches and specialization to compete, are seeking out post-CFP certifications and designations to establish such expertise, and may soon face profit margin compression as they are forced to budget more than the paltry 2%-of-revenues that the average advisory firm spends on marketing. On the other hand, given the incredibly high lifetime value of a client for an advisory firm, perhaps this will be the impetus necessary for firms to recognize the value of spending marketing dollars to get new clients. Though without a doubt, this will be easier for larger firms that have free cash flow to reinvest and the ability to scale their marketing, potentially widening the gap between the largest firms that get larger and the smaller firms that remain stuck small.

The crisis of differentiation is also driving advisors to seek out new markets, hoping to expand the pie of potential clientele rather than struggle to compete for the “typical” advisor’s baby boomer clientele. This is leading to an exploration of working with younger clients, lowering asset minimums to expand further into the mass affluent, testing new business models (e.g., monthly retainers), and more. Though many firms will struggle to compete in this space in the near term, as their service model and infrastructure are so squarely dedicated to their existing core clientele that they’re simply not appealing in new/different markets. In the long-run, expect to see the rise of the "Turnkey Financial Planning Platform" (TFPP) that will give the advisor all the tools, templates, business model, and a community of like-minded advisors to collectively succeed targeting a particular type of clientele or service model (e.g., Garrett Planning Network, Alliance of Comprehensive Planners, and the XY Planning Network).

The struggle to grow organically – along with record profit margins thanks to the market boom, an increasing availability of lenders, and firms that have systemized enough to want to scale by tucking in a smaller firm – is also fueling firms to seek out inorganic growth through mergers and acquisitions, leading to a reported 50:1 imbalance of buyers outnumbering sellers. After all, why seek out clients one or two at a time, when the firm can acquire 50, 100, or 500 at once? Thus far, the imbalance has been a surprise to many, with the expected wave of retiring advisors turning out to be a mirage, but in 2015 the pace of M&A may increase, not necessarily because a lot more advisors suddenly start to retire, but simply because they decide it’s more advantageous to try to grow by leveraging the platform and resources of a larger firm. The fact that a larger size provides greater potential scale to expand profit margins and defend against the next bear market doesn’t hurt, either.

The bottom line, though, is that 2015 may turn out to be a "surprisingly" challenging year for growth for most advisors, with the ongoing bull market masking an increasingly difficult competitive environment signified by slowing organic growth rates. The best firms will use the currently favorable market backdrop as an opportunity to shore up their profit margins to defend against the next bear market, and sow the seeds for future differentiation by crafting their new (or first) marketing plan. The worst firms will allow complacency and the market tailwind to continue to mask the problem until it’s too late. When we look back on the firms that have been successful – or not – by the end of this decade, I strongly suspect we’ll find a dramatic gap between the firms that proactively invested into a marketing plan at this transition point, and those who continued to rely solely on passive referrals from existing clients only to discover that growth by referrals is not actually a best practice in marketing, but the slow-growth outcome that occurs from not having a marketing plan at all.

So what do you think? What do you see as the top issues facing advisors in 2015? Do you have new/different plans for your own advisory firm? Do you agree with the issues cited here, or do you see new/different challenges and opportunities on the horizon?

In addition to the issues mentioned, something I’m seeing more advising shifting their thinking about how they are running their practice.

From advisors who have been happily looking at their practice as two separate sections — a) being an advisor b) owning a business ….to that of an advisor owner (sometimes taking the role as business manager, sometimes hiring a manager… other times choosing to continue with the advising or planning role).

Especially seeing this in advisors who are 20-25 years away from full retirement.

I wonder if this is due to younger advisors watching what is/has been happening to advisors who remained solo until retirement and didn’t end up with the investment they thought they’d get from their firms.

I’m a little late to the discussion but take a look at July 2015 CFP Board changes to the case study/experience requirement. No details yet but it looks like someone challenging the exam (ChfC, Phd, CPA, etc) may get a pass on taking a case class and complete a case directly for CFP Board instead.

Craig,

Indeed, I’m afraid that is the case. I covered it separately on the blog two weeks ago when the CFP Board announced – see https://www.kitces.com/blog/cfp-board-softens-experience-requirements-for-new-cfp-certificants-reduces-capstone-requirement-for-challenge-status/

– Michael

Information provided in this page is very informative.These days digital technology is developing rapidly.It is implementing in all sectors.In today’s life this Financial technology taking one step forward and providing good results.Here some top 5 “FinTech” startups to watch in 2015.