Executive Summary

The ‘popular’ view of the world of financial advisors these days is that we’re all in a collective race for size and economies of scale, because only the largest can survive and everyone else is doomed to a world of declining profit margins as the overhead costs of running an advisory firm grind their income down to nothing.

Yet the latest industry benchmarking research for RIAs, including both the 2015 FA Insight “People And Pay” and the 2015 Investment News “Compensation And Staffing” studies, found that just the opposite may be occurring – by operating with lean staff overhead and leveraging technology, standout solo financial advisors supported by just 1-3 staff members are actually some of the most financially successful and profitable advisory firms out there, taking home more in owner income than any advisors but the partners of the largest super ensemble firms!

And perhaps most notable is that not only is the typical successful solo advisor practice doing exceptionally well financially, but it is succeeding not by serving an exclusive set of high-net-worth clients with $1M+ minimums, but by serving a mass affluent clientele often claimed (incorrectly!?) to be ignored by the RIA community! In fact, the latest benchmarking data reveals that the common stereotype that RIAs serve "only" the high-net-worth is entirely wrong, as it's really only a small subset of the largest (albeit also the most visible) advisory firms who are focused on those clientele, while the mass of solo financial advisors serve the broader mass affluent!

Profitability Of Solo Proprietor Financial Advisors Vs Ensemble Firms

In the ‘normal’ analysis of a company’s profitability – for an advisory firm or any other business – the process is relatively straightforward: add up all the revenue, subtract the direct expenses of delivering the financial advice (or other product/service), then subtract the overhead expenses of operating the business, and you arrive at an operating profit margin for the firm. An employee receives the salary and other compensation paid for working in the business (part of the direct expenses or overhead depending on the role), and the owners/shareholders receive the profits remaining at the end.

Measuring the profit margins of a financial advisor is a challenge when it’s a sole proprietorship, though, because there is rarely a distinction between the salary/compensation the financial advisor claims for working in the business, versus the profits that are received from the bottom line of the business. From a buyer’s perspective, the separation of the two is important because a buyer would have to replace the work the financial advisor does in the business with another advisor, and would then only enjoy the profits remaining thereafter. Thus, a firm that generates $300,000 in “total take-home pay” for the advisor might appear from the buyer’s perspective as $200,000 that would have to be paid to a replacement financial advisor and “only” an actual take-home profit of $100,000. Which means the buyer (seeing only $100,000/year of profits) would pay far less than the seller (seeing $300,000/year of take-home pay) may expect; nonetheless, in the context of a solo advisor – particularly one organized as a sole proprietorship – this distinction is often lost (at least until the time of sale), beacuse there is not a financial nor tax reason to make a distinction between salary and profits in the first place.

Accordingly, then, one of the easiest and most straightforward ways to measure the “profitability” of an advisory firm is simply to look at the total take-home compensation of the owner-advisors, a combination of what they might be paid in salary/bonuses for working in the business (as it commonly done for larger ensemble firms) and what they are taking home as bottom-line profits from the business. And, as the latest research shows, by this measure the top solo financial advisors are doing remarkably well!

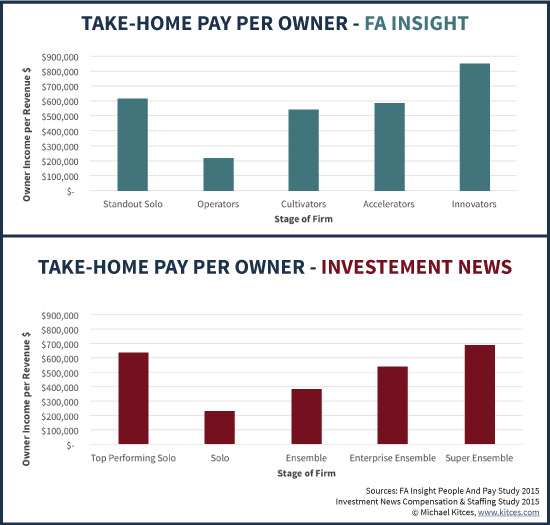

For instance, the latest 2015 Investment News Compensation And Staffing Study (sponsored by Pershing and produced by Philip Palaveev and his team at The Ensemble Practice), finds that the top performing solo advisors are taking home a whopping $631,116 of income on a base of $936,565 of revenue, which means $0.67 of every dollar of revenue is going home with the advisor!

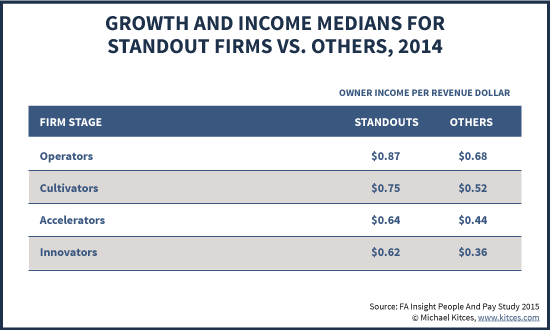

The newest 2015 FA Insight “People And Pay” study finds a similar phenomenon; standout “Cultivator” firms (solo owners with $500k to $1.5M of revenue) are taking home an average of $0.75 of income per dollar of revenue. And the standout “Operators” – solo advisors with less than $500k of revenue but highly profitable practices – are generating $230,000 of revenue and taking home $193,000 of it, which amounts to over $0.80 on the dollar! By contrast, the typical larger firms (“Accelerators” with $1.5M to $4M of revenue and “Innovators” with $4M+) generate barely half that amount of owner income relative to revenue (and even the standout firms can’t get close).

Of course, the ‘caveat’ of larger firms is that they may be taking home less in income per dollar of revenue, but they are much larger firms with far more in total revenue in the first place. So "just" $0.62 of owner take-home pay for every $1 of revenue is still a lot more money when Innovators have $4M+ of revenue to begin with. On the other hand, they also split that revenue amongst a larger number of partner/owners in the first place, which means the take-home pay per owner still isn't necessary much better after all!

In fact, according to both the FA Insight and Investment News studies, an advisory firm actually has to grow all the way to the top echelons of size (an “Innovator” with $4M+ in revenue for FA Insight, or a “Super Ensemble” with $10M+ in revenue under Investment News) for the take-home pay per partner of the multi-partner firm to exceed that of a standout/top-performing solo advisor!

Notably, the take-home pay of the categories above are broad-based averages; the standout/top performing firms in each of the categories are capable of generating better take-home pay for owner/advisors. But to say the least, growing a firm significantly larger is not a ‘free pass’ to better total take-home compensation as an advisor simply due to having more staff, resources, and any anticipated ‘economies of scale’. Instead, the data suggests that unless the firm is especially lean and well-run at larger sizes, a solo advisor who grows the firm larger just earns less money until the firm scales to at least $500M of AUM (or at least $1B+ by the Investment News study) with four partners who finally get a slightly larger take-home from their slice of a much larger (and more complex) pie! (Though notably, the large-firm owner also has an advisory firm asset that may be worth more than a solo advisor’s practice.)

The Value Of Hiring And Leveraging Staff In A Solo Advisory Firm

A key distinction of the most successful “solo” advisory firms is that they’re actually not purely “solo” advisors. Instead, they typically add a small number of core staff members as they grow, to support the sole advisor/owner. FA Insight estimates that an advisory firm will usually need to hire one full-time-equivalent staff member for every $260,000 in revenue, and will need to add a “professional” (i.e., paraplanner or associate advisor) staff member every $620,000 of revenue.

Accordingly, the typical “highly profitable” solo advisor is actually a solo advisory firm owner plus an admin staff member as the firm grows towards $500k of revenue. In turn, this becomes a solo advisor plus a paraplanner/associate advisor by about $600k of revenue (plus the existing staff member) as the firm approaches 75-100 clients and it becomes overwhelming for just one lead advisor to handle all client financial planning needs solo. Then, as the client base grows further, the successful solo typically adds one more staff member as the firm approaches $1M of total revenue, for a total headcount of four (including the advisor/owner).

On the other hand, while leveraging staff resources is good, what the benchmarking studies actually reveal is that the success and profitability of the solo advisor is driven heavily by their ability to limit the size of staff by utilizing them efficiently. In other words, the difference between the most profitable solos and the rest is that the less profitable ones already have three staff members by $300k of revenue, and end out with five or more staff members as they approach $1M of revenue. It’s the staff efficiency – and ostensibly, the use of technology to leverage their staff effectively – that characterizes the most successful solo advisors, and their ability to handle more clients per staff member.

Thus, thanks to what appears to be a more efficiently operated business, the “best” solo firms are running around 30-40 clients per staff member (including the advisor), and have a paraplanner/support advisor allowing the lead advisor to handle 125-150 clients (an average of 62-75 clients “per professional” including the advisor/owner and support advisor). Which is especially efficient compared to larger advisory firms, as the Investment News research shows those typically only average 50-65 clients per professional and 25-35 clients per staff member (including all staff members across the organization).

Sole Proprietor Financial Advisors Serving The Mass Affluent

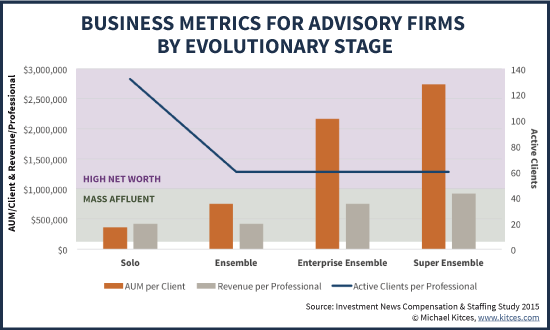

Notwithstanding the efficiencies found in the solo advisory firm, it’s the largest advisory firms that are often referred to as being the most “productive”, because industry research shows that advisors at big firms tend to manage the most client revenue per advisor. Accordingly, while the Investment News study shows the typical solo advisory firm has $423k of revenue per professional, at Super Ensemble firms (those with over $1B of AUM and $10M of revenue) each professional manages an average of $925,977 of revenue!

Yet the caveat to this data is that as it turns out, advisors at the largest ensemble firms are not actually more “productive” as measured by the number of clients they serve. Instead, as noted above, larger firms tend to have fewer clients assigned to each advisor, and the higher revenue per professional “productivity” at large firms is driven entirely by the fact that the largest firms have the largest (i.e., wealthiest) clients!

Thus, the typical client of a Solo advisor has “just” $363k of AUM, while the typical Ensemble firm client has $758k, and the typical Super Ensemble client has $2.7 million of AUM. These increasingly large client sizes at the largest advisory firms allow the advisors at those firms to appear the most “productive”, despite the fact that it’s actually solo advisors managing as many as 125+ clients (solo or with the help of a paraplanner), while the largest firms typically have no more than 60 clients per advisor professional!

In other words, notwithstanding all the discussion that “RIAs only serve the affluent”, the reality appears to be that the typical client of most RIAs fits squarely into the Mass Affluent demographic (from $100k to $1M of investable assets). Solo RIAs serve clients at the lower end of the mass affluent scale, ensemble firms serve clients at the upper end of the mass affluent scale, and it’s only when firms cross $500M of AUM and $5M of revenue and reach the “Enterprise Ensemble” category that multi-millionaire high-net-worth clients begin to show up as “typical” (due ostensibly to the ‘gravitas’ of the larger firm, and/or its ability to more effectively scale its marketing process to bring in high-net-worth clientele). Yet these large RIA firms serving the high-net-worth (HNW) client are actually the minority of firms; in the Investment News study, fewer than 20% of advisory firms were in the upper two size categories and serving HNW clients! And given that the benchmarking studies tend to oversample larger RIAs (who have the time and resources to participate in benchmarking studies), and Investment News didn't include advisors with less than $100,000 of revenue (which tend to be smaller solos still getting started), if anything the total number of RIAs who focus on high-net-worth clientele is likely an even smaller percentage!

Similarly, the FA Insight data also finds that solo advisors tend to serve “smaller” clients in the mass affluent segment; “standout” operator firms (under $500k of revenue) have an average client AUM of $398k, and the standout cultivator firms (the largest solo-owned firms with $500k to $1.5M of revenue) generate $811k of revenue with an average client AUM of $864k. And realistically, successful firms will likely have a “few” large clients that skew the average upwards, meaning the median client AUM at solo advisor firms is probably even lower (and even more squarely in the mass affluent segment).

Notably, the FA Insight research also suggests that it’s the smallest firms that may be doing the most innovating around how to serve “smaller” mass affluent clients as well, with alternative forms of hourly and especially (annual or monthly) retainer fees; the research found that amongst the standout operator firms, a whopping 1/3rd of revenue was coming from hourly or retainer fees, compared to less than 10% of revenue for the other operator firms (though notably, amongst the largest advisory firms, the most profitable standouts were significantly less likely to charge hourly or retainer fees and more likely to stick with AUM fees). This suggests that larger advisory firms are finding that AUM fees continue to be effective for high-net-worth clientele, but that smaller advisory firms are increasingly experimenting (successfully!) with using retainer fees to support an adequate level of revenue per client amongst the mass affluent.

More broadly, what all of this suggests is that, regardless of industry debate to the contrary, both the latest 2015 Investment News Compensation And Staffing Study and also the newest 2015 FA Insight “People And Pay” study reveal that RIAs actually can (and do) serve the mass affluent, and are capable of doing so very profitably! And the solo practitioner advisor is not only not dying off in the face of large-firm and robo competitors, but appears to actually be capable of surviving and thriving by leverage staff and technology to serve those clients effectively – and while they may not be building a business that can be sold for a princely sum, the take-home compensation of solo financial advisors is competitive to all but the owners of the very largest advisory firms!

So what do you think? Are financial advisors actually doing a better job serving the mass affluent than RIA critics have suggested? Have financial advisors been pressured to grow more than is actually necessary? Is the leverage of technology efficiency allowing the solo financial advisor to compete more efficiently than anyone ever anticipated?

Great article, Michael.

But this can’t be right.

All the big brokerage firms who are fighting fiduciary responsibility claim they can’t cost effectively serve the mass affluent 🙂

Russ,

Indeed, it’s sad that anti-fiduciary lobbyists have made the case that RIAs “only” serve high-net-worth investors based on a small subset of the largest RIAs, and completely ignored the mass of RIAs that serve the mass affluent! :/

– Michael

Great article showing that AUM is not the only measurement that matters. Though I am not yet a “standout” cultivator, my solo practice is close to those levels of profitability. Prior to your article today I thought I was the only one intentionally limiting the size of my practice as profit margins seem to decline dramatically as firms grow. Add in a measurement or two on quality of life (e.g. days off work) and I think solo firms are tough to beat.

Matthew,

You’re definitely not alone in this. It’s far more common than most seem to have believed, and as the numbers show is possible to be quite profitable in doing so! 🙂

– Michael

Quite right, Michael. We solo practitioners also get to create a lifestyle profession; serving clients that we like and who like us. I have asserted this as our custodians and other experts keep harping on growth.

Michael

Does the study talk about solos or is it really about silos?

i.e.

Solo refers to an office with just 1 professional advisor with client management services.

Silo refers to an office 1 professional advisor who runs an office with a few other producers (multi-advisors) but who is not an ensemble or enterprise.

Maria,

The benchmarking studies are based on the actual number of advisors in the RIA. So we’re talking actual solos. A 5-advisor silo firm is just a not-well-run ensemble in this data. 🙂

– Michael

Thanks Michael, for the clarification.

Michael – As someone who has served the Mass Affluent Baby Market for more than 25 years, I can attest that it’s not only a profitably business niche, but one that’s rewarding, demanding and humbling.

I agree with Matthew Jarvis. Everything I read in the trade press warns about the decline of the solo practitioner. My experience as a solo practitioner has been quite positive. Your article reinforced my perceptions and experience. By the way, I have a home office. Over 90% of the work done by my assistants is done virtually. I pass the savings on to my clients. While this lowers my revenues, the margins are great. Thanks!

You have to love it when somebody shines the light of reality onto some long-held piece of conventional wisdom. This rings a lot of bells that sound true to me and my experience. Thanks, Michael.