Despite being a highly regulated industry, the bizarre reality is that the title “Financial Advisor” itself is largely unregulated. Instead, the financial services industry regulates financial advisors not by the advice they give, but by whatever it is that they implement after their recommendations are delivered – where those who implement insurance are regulated by state insurance regulators, those who implement investment products are regulated by FINRA, and those who implement managed portfolios are regulated by the SEC or state securities regulators.

As a result, historically all it taken to call oneself a “Financial Advisor” was a license to sell an insurance or investment product, most commonly via a Series 6 or Series 7 license (to sell brokerage products), a state life-and-health insurance license (to sell insurance and annuities), or a Series 65 license (to earn an advisory fee for managing a portfolio).

Yet in practice, this means the legal bar to become a “Financial Advisor” is incredibly low, based only on understanding the sales and business conduct laws to which the “advisor” will be subject. In other words, becoming a “Financial Advisor” doesn’t include any requirement to actually test and prove one’s competency to give quality financial advice!

Of course, while you might not need to know much about finances or advice to hold out as a provider of financial advice, many financial advisors do in fact invest heavily into their own competency and skills in delivering financial advice. Not because it’s a legal requirement. But simply because it’s good business. And it’s the right thing to do for clients.

After all, the reality is that it only takes 40 minutes of bad advice to potentially destroy 40 years of good financial habits. One catastrophic financial decision can turn the course of a client’s entire life. In the 21st century, “money decisions” are survival decisions, and financial advice has a direct impact on our ability to survive and thrive.

So how does one distinguish between the good financial advisors who are serious about their craft, and the rest who may use the “financial advisor” label but are really in the business of distributing financial services products?

Because those who are really in the business of financial advice aren’t financial advisors. They’re Financial Advicers.

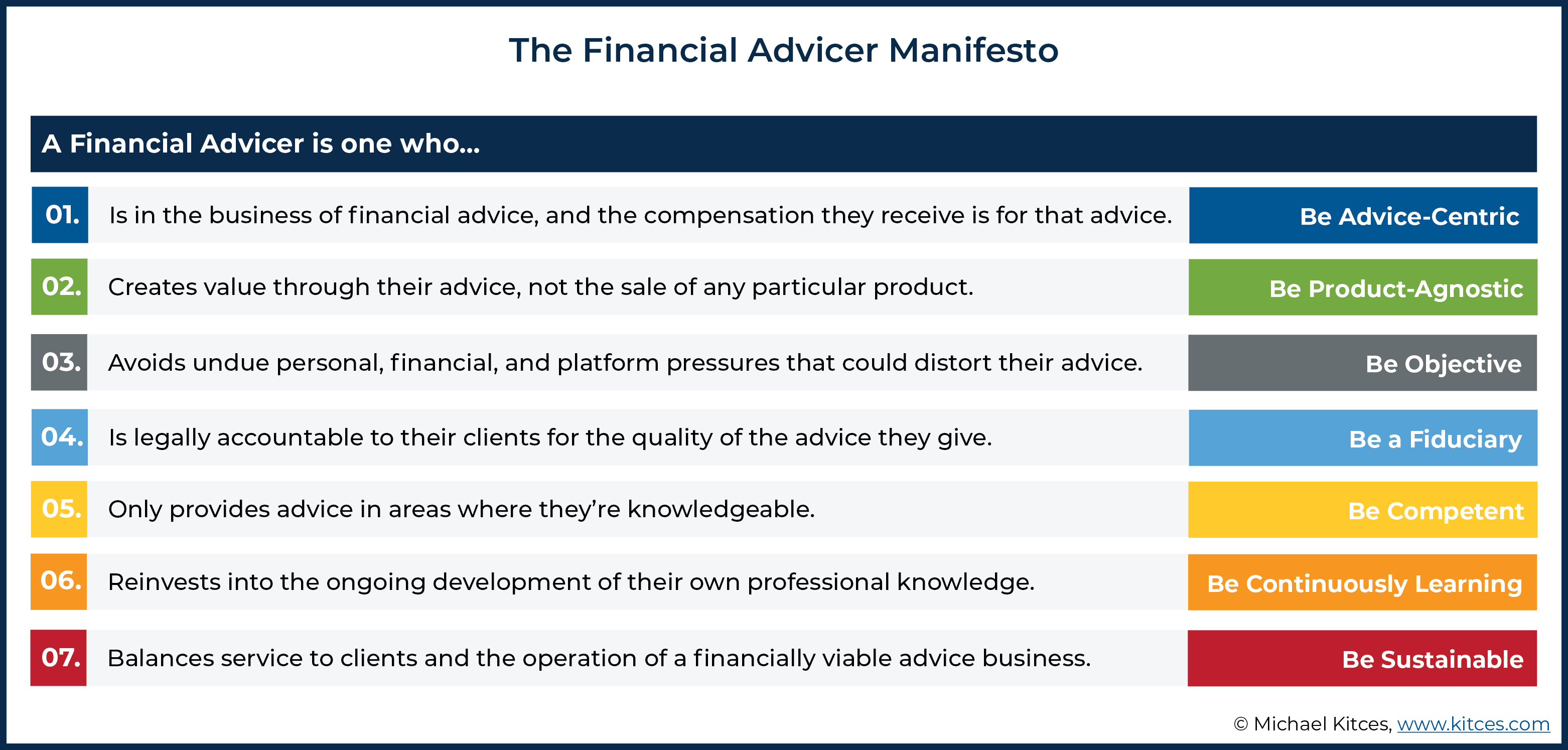

At its core, being a Financial Advicer means being someone who is first and foremost in the business of financial advice (not financial products), and the compensation they receive is remuneration for that advice (not a reward from product manufacturers or distributors for implementing the products they wanted to have sold).

Not to say that implementation of financial advice isn’t important. But just as there’s a difference between a doctor that prescribes medication, the pharmacist that fills the prescription (but doesn’t do the prescribing), and the drug company that manufactures the drug for sale, there’s a difference between a Financial Advicer hired by their clients to prescribe recommendations, and those employed by product companies to sell and implement the company’s products (or fill the orders that consumers come to purchase).

Because when you’re a Financial Advicer, the product isn’t the product. The advice itself, and the Financial Advicer delivering it, are the “product” that the client is purchasing.

Which is why Financial Advicers operate as fiduciaries (i.e., by having an affiliation to a Registered Investment Adviser, which is literally legally required to be in the business of financial advice). So that the Financial Advicer is legally accountable to their clients for the quality of the advice they provide.

In addition, this is why Financial Advicers have not only a substantive continuing education requirement – as all bona fide professions – to continuously improve their advice, but an outright business incentive to continue to invest in themselves and their education to better their business and their value proposition to clients!

The key distinction, though, is that being a Financial Advicer is not a legal or regulatory designation; it’s a way of being, an approach to the business of financial advice that recognizes the sacred duty that we have to the clients we serve.

Here at Kitces.com, it’s the journey of becoming a Financial Advicer, and the need for the professional development of Financial Advicers, that we aim to support.

Because in the end, Financial Advicers not only deliver expert advice. Financial Advicers serve as guides that can facilitate a (re-)alignment of the client’s money with their goals and purpose, in a manner that transforms lives.

Which is why we’re so committed to our mission at Kitces.com: Making Financial Advicers Better, and More Successful. And helping the entire financial services industry make the transition from our sales-based roots as Financial Advisors, to our advice-centric future as Financial Advicers.

Join our Financial Advicer community, and see what it’s about for yourself.