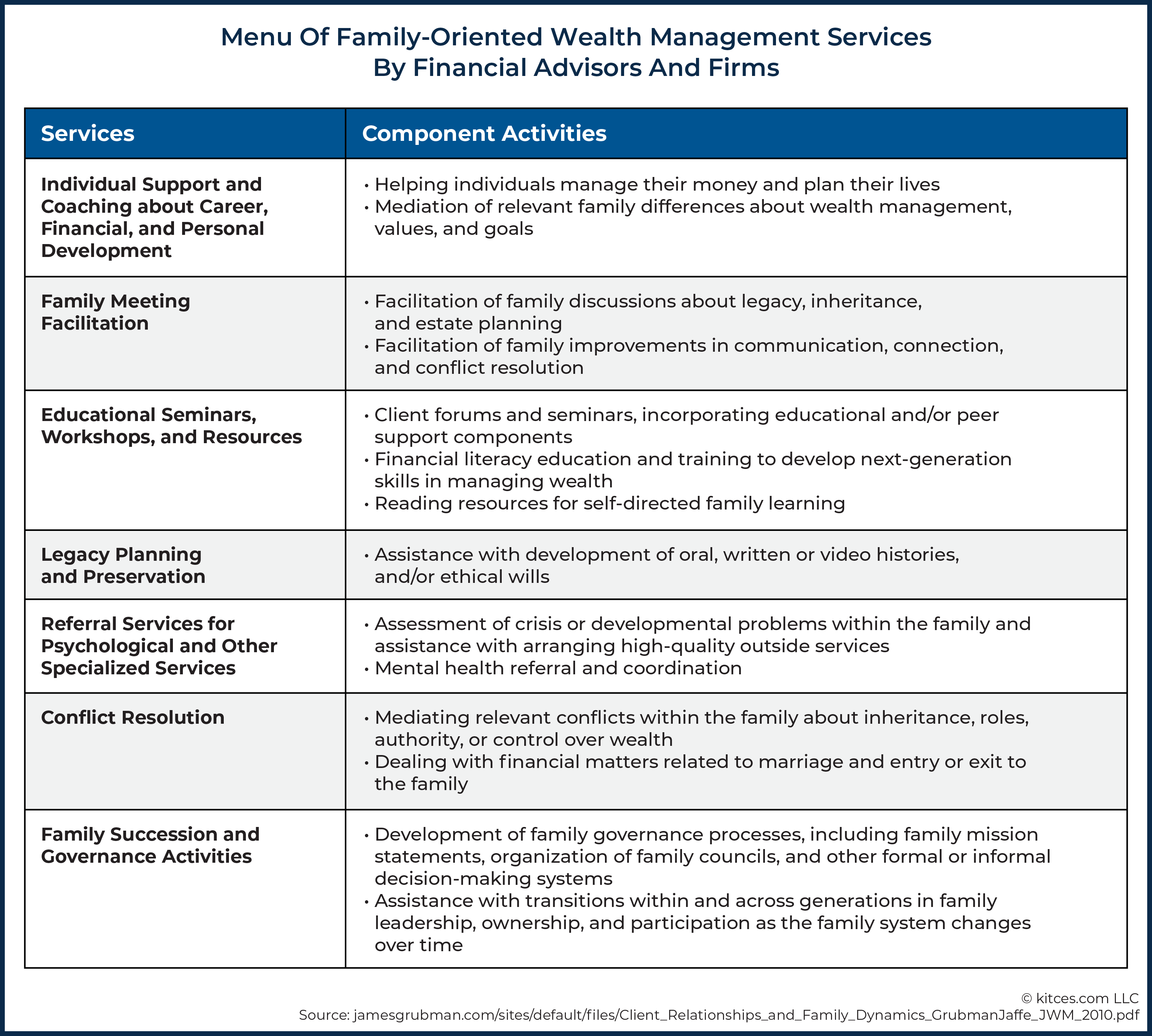

Executive Summary

As 2021 comes to a close, I am once again so thankful to all of you, the ever-growing number of readers who continue to regularly visit this Nerd’s Eye View blog (and share the content with your friends and colleagues, which we greatly appreciate!). This year has been one of mixed feelings for most financial advisors – a year where many people have struggled with the direct and indirect impacts of the ongoing pandemic, from health to employment challenges, but one where many financial advisory firms have managed to adapt and even excel with newfound growth as more consumers realized they need a financial advisor. Personally, it has been a big year of change as well, with a(nother) doubling of the Kitces.com team in 2021 (now more than 20 people who help to make it all happen!), as we expand further into Courses and online Summits to fulfill our own mission of “Making Financial Advicers Better and More Successful”.

We recognize (and appreciate!) that this blog – its articles and podcasts – is a regular habit for tens of thousands of advisors, but that not everyone has the time or opportunity to read every blog post or listen to every podcast that is released from Nerd’s Eye View throughout the year. As many of you noted in response to our Reader Surveys, most choose which content to read or listen to based on headlines and topics that are of interest (and skip the rest). Yet in practice, this means that an article once missed is often never seen again, ‘overwritten’ (or at least bumped out of your Inbox!) by the next day’s, week’s, and month’s worth of content that comes along.

Accordingly, just as I did last year, and in 2019, 2018, 2017, 2016, 2015, and 2014, I've compiled for you this Highlights List of our top 20 articles in 2021 that you might have missed, including some of our most popular episodes of ‘Kitces & Carl’ and the ‘Financial Advisor Success’ podcasts. So whether you're new to the blog and #FASuccess (and Kitces & Carl) podcasts and haven't searched through the Archives yet, or simply haven't had the time to keep up with everything, I hope that some of these will (still) be useful for you! And as always, I hope you'll take a moment to share podcast episodes and articles of interest with your friends and colleagues as well!

In the meantime, I hope you're having a safe and happy holiday season. Thanks again for the opportunity to serve you in 2021, and I’m excited to share more soon about some new initiatives we’re planning to do even more to support the Financial Advicer community in 2022 and beyond!

Authors:

Don’t miss our Annual Guides as well – including our list of the “11 Best Financial Advisor Conferences To Choose From In 2022”, the ever-popular annual “2021 Reading List of Best Books For Financial Advisors”, and our increasingly popular Financial Advisor “FinTech”Solutions Map!

2021 Best-Of Highlights Categories: Financial Planning | Scaling Advice | Business Management | Marketing | Career Development | Retirement | Tax | Investments | Podcasts

Financial Planning

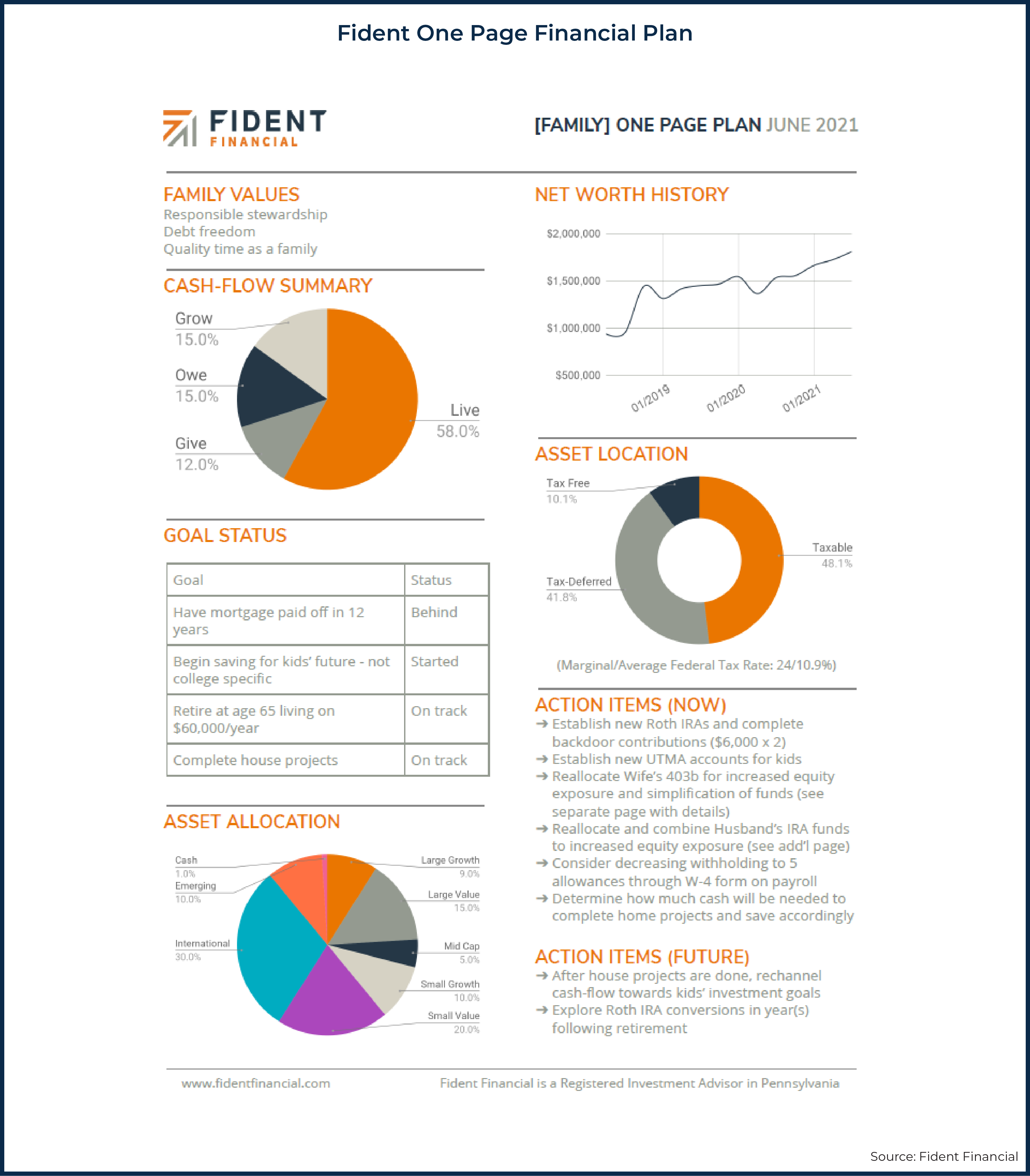

The One-Page Financial Plan: Focusing Advice On What Matters Most – Advisors have traditionally presented clients with a lengthy financial plan, which may include every detail a client might (or might not) be interested in, as a way to demonstrate the depth of the advisor’s knowledge and the amount of analytical work the advisor put into the planning process.

The One-Page Financial Plan: Focusing Advice On What Matters Most – Advisors have traditionally presented clients with a lengthy financial plan, which may include every detail a client might (or might not) be interested in, as a way to demonstrate the depth of the advisor’s knowledge and the amount of analytical work the advisor put into the planning process.

However, the length of a financial plan is not written in stone (and neither is the ‘requirement’ that it be presented in a binder!). With that in mind, financial advisor and client communication guru Carl Richards made the case in his book The One-Page Financial Plan that all of the ‘need to know’ information for a client can and should be distilled into a single page – the One-Page Financial Plan (OPFP).

The creation of an OPFP is about focusing the limited space to target what each client truly needs to see, and wants to talk about. In addition, the conciseness of the OPFP allows it to be a ‘living plan’ that can be more readily updated and maintained (as it does not require multiple pages of revisions each time a client’s circumstances change). In fact, as guest author Jeremy Walter shows with a sample of his own OPFP that he uses with clients, advisors can start a first draft of the OPFP as soon as they meet with a new client, and adjust it as they gather and analyze the client’s information.

Ultimately, while transitioning to using the OPFP might seem like a big leap for those accustomed to the more ‘traditional’ full-length financial plan, the time and information efficiencies created can improve the advisor’s financial planning process, and in the end, a shorter financial plan doesn’t necessarily make it a “lesser” plan as long as it still answers the client’s two biggest questions: “Am I doing OK?” and “What should I do next?”.

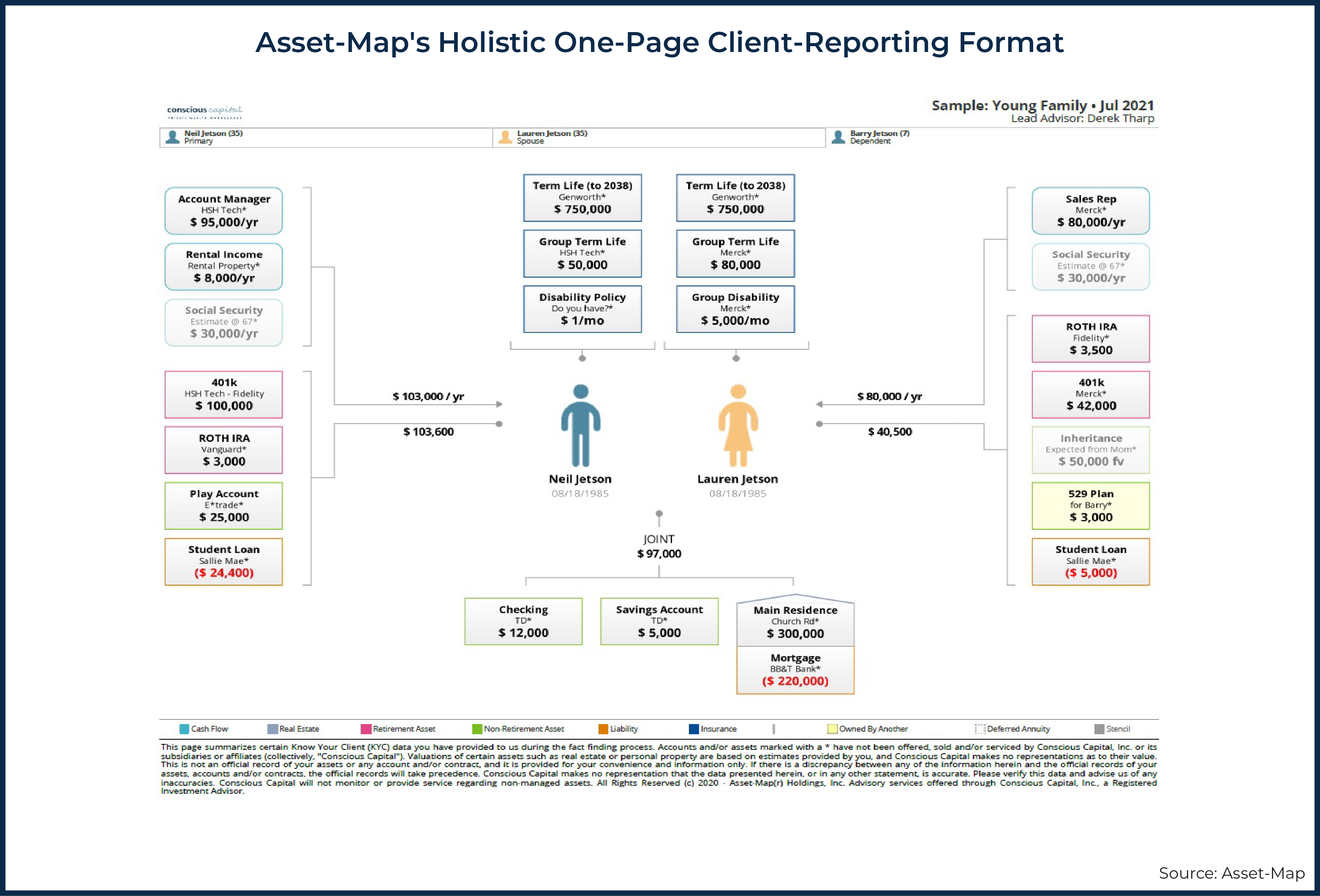

Using Asset-Map To Develop A (Gestalt) Visualization Of The Holistic Financial Plan – Financial advisors collect a wide range of data from clients, but bringing it all together in a way that the client (and advisor themselves) can understand is challenging, especially since the more data and complexity there is, the longer the financial plan tends to be, and the harder it is to synthesize.

Using Asset-Map To Develop A (Gestalt) Visualization Of The Holistic Financial Plan – Financial advisors collect a wide range of data from clients, but bringing it all together in a way that the client (and advisor themselves) can understand is challenging, especially since the more data and complexity there is, the longer the financial plan tends to be, and the harder it is to synthesize.

In order to help advisors and clients see the bigger picture, the company Asset-Map created a tool that works from a Gestalt perspective – showing a visualization of the whole that, while it may not contain every possible detail, is still more valuable as a whole than the sum of the parts – by providing a graphic summary of a client’s entire financial situation. These summaries are presented as a one-page, mind-map-style report, which helps advisors to quickly draw out patterns and formulate holistic perceptions that are relevant to the client’s broader environmental contexts, including where they are in their career and their family situation.

For clients, an Asset Map provides a useful visual summary of their household, showing them how all the individual pieces of their financial lives interact and create their broader financial situation. Having all the information in an easy-to-understand format, and in one place, can also provide clients with the reassurance that their advisor has captured and considered all of their financial details (and help them to easily see if they need to let their advisor know about any pieces of important data that may be missing!).

The key point is that when analyzing a client’s financial situation, viewing the whole picture as a complete unit rather than as individual parts, leveraging a software solution like Asset-Map, can result in not only better-informed and more confident clients, but also improved client data tracking and financial planning recommendations!

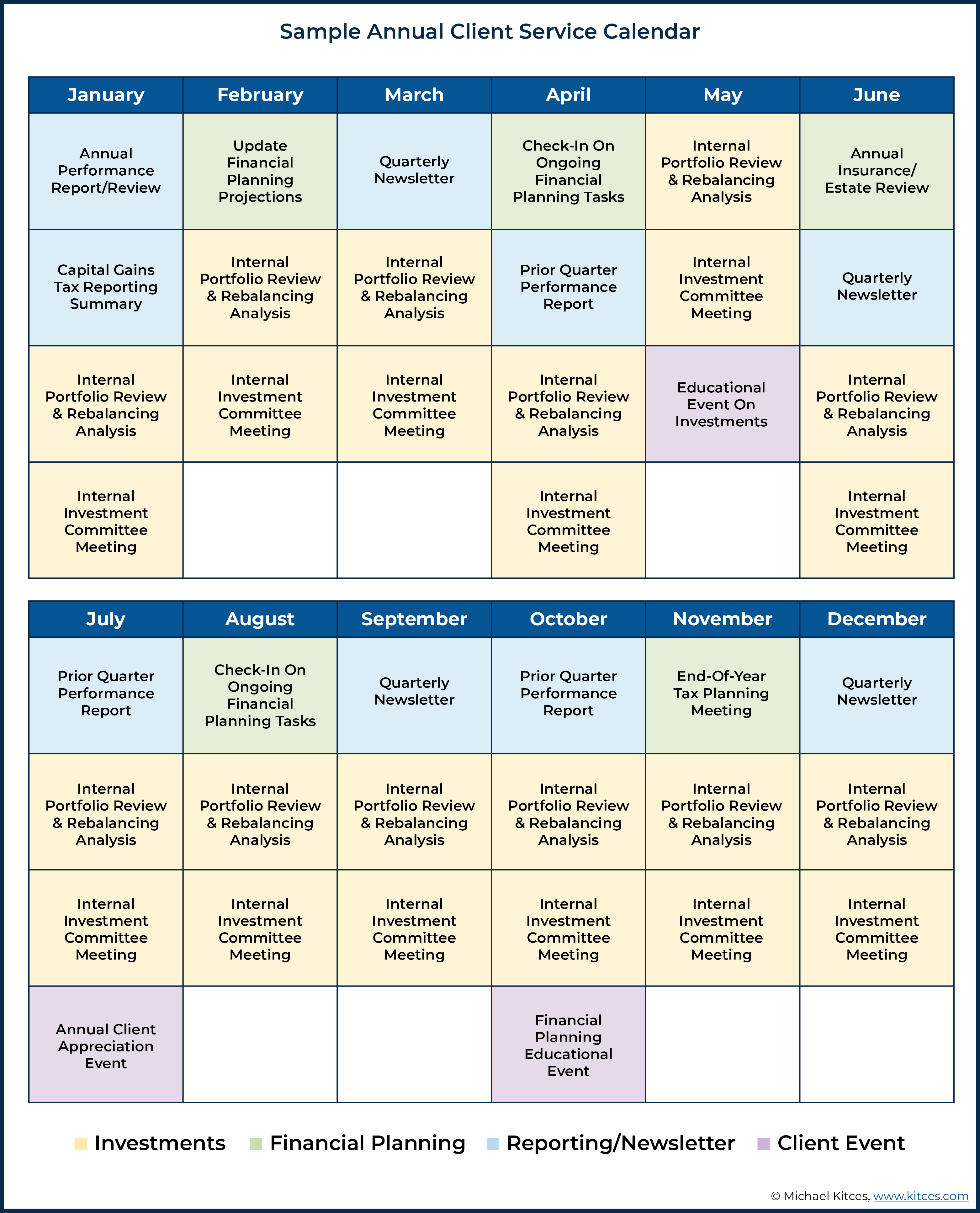

Making Financial Planning More Tangible Using (Turnkey) Deliverables For Clients – When meeting with prospective and current clients, advisors are used to communicating the intangible aspects of financial planning, such as their knowledge, reliability, empathy, and responsiveness. However, advisors can also consider enhancing the tangible aspects of their client relationships — from the physical experience of the service to the deliverables they provide — which can improve the client’s experience with the firm and the otherwise-intangible financial planning process.

Making Financial Planning More Tangible Using (Turnkey) Deliverables For Clients – When meeting with prospective and current clients, advisors are used to communicating the intangible aspects of financial planning, such as their knowledge, reliability, empathy, and responsiveness. However, advisors can also consider enhancing the tangible aspects of their client relationships — from the physical experience of the service to the deliverables they provide — which can improve the client’s experience with the firm and the otherwise-intangible financial planning process.

Some examples of tangibles that can influence a prospective (or existing) client’s perception about the service they will receive from their financial advisor include the condition and décor of the office space, the appearance and attire of employees, and the materials associated with the financial planning service itself. And while creating tangible deliverables can seem time-consuming, systematizing a firm’s financial planning processes (such as through meeting surges or a client service calendar) can also make it easier to systematize (and be more time-efficient with) the deliverables along with them.

In addition, advisors can take advantage of turnkey resources to further systematize their processes and deliverables. These include stand-alone planning modules (e.g., Right Capital’s menu of planning report options), customizable template tools (e.g., fpPathfinder’s financial planning checklists and flowcharts), and analyses of specific issues (e.g., Holistiplan’s tax analysis report). For the greatest effect, these deliverables can be introduced throughout the five key stages identified as a client’s most memorable milestones in their relationship with an advisor, from their first introduction to data gathering and analysis, and finally, plan implementation and the ongoing engagement between the advisor and the client.

In the end, the key point is that there are many tangible deliverables already packaged and available on a turnkey basis for advisors to incorporate into the menu of services they provide to make their client experience more tangible. And by considering the most memorable stages of the client journey, advisors can strategically implement impactful deliverables that remind clients how valuable advisors really are!

Scaling Advice

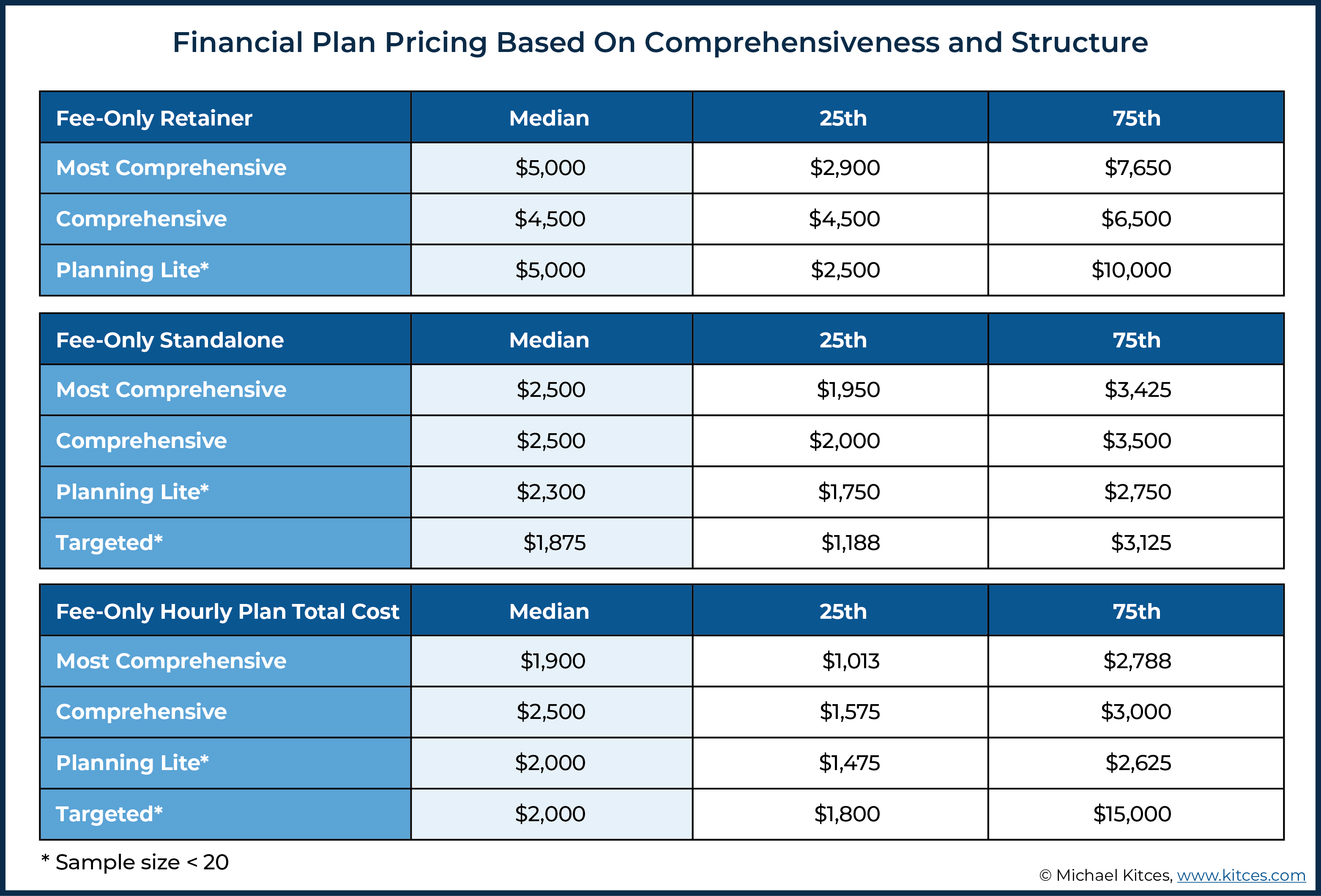

Financial Advisor Fee Trends And The Fee Compression Mirage – In an environment where fees on financial products have been under intense price competition, some industry observers have posited that financial advice will experience similar fee compression. However, the latest Kitces Research on the Financial Planning Process found little evidence that this was the case. On the contrary, the collected data suggests that median financial advice fees in 2020 significantly increased, relative to 2018 fees, for standalone fees (12.4% increase), retainer fees (25% increase), and for hourly fee rates (25% increase)!

Financial Advisor Fee Trends And The Fee Compression Mirage – In an environment where fees on financial products have been under intense price competition, some industry observers have posited that financial advice will experience similar fee compression. However, the latest Kitces Research on the Financial Planning Process found little evidence that this was the case. On the contrary, the collected data suggests that median financial advice fees in 2020 significantly increased, relative to 2018 fees, for standalone fees (12.4% increase), retainer fees (25% increase), and for hourly fee rates (25% increase)!

When considering industry channels, advisors in RIAs charged higher median fees than those in the broker-dealer channel. Similarly, financial advisors with a CFP designation generally charge higher fees than those who are not CFP professionals.

The study also computed implied hourly rates for advisors using non-hourly billing models, finding that primarily AUM advisors are generating revenue at rates that would imply hourly fees between $350 and $800. This is in stark contrast to the $100 to $300 implied hourly fees generated by advisors operating on a primarily hourly basis, and speaks to the challenge of building an hourly practice that is as financially successful as those operating on an AUM basis at common fee levels.

The key point, though, is that there does not appear to be any overall trend of decreasing financial planning fees, despite common claims that fee compression is coming for financial advisors since the rise of the robo-advisor ‘threat’ a decade ago. In fact, the trends seen in the study are increasing fees across the range of advisor fee models, as advisors increasingly focus on honing an advice-centric value proposition beyond (increasingly commoditized) financial products!

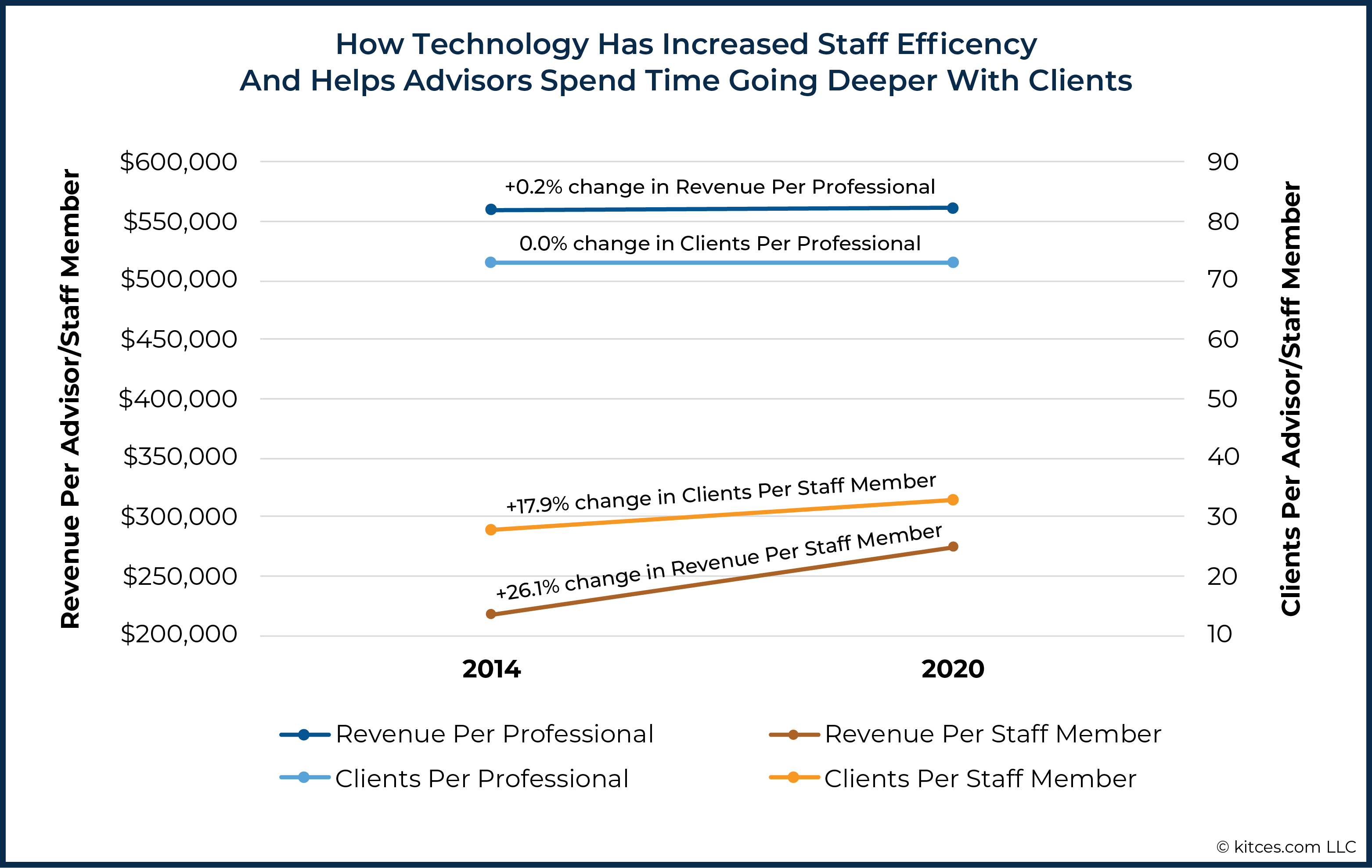

Scaling Financial Advice: What Actually Drives Efficiency And Advisor Productivity – While improvements in technology have led to increased productivity in a range of industries, financial advisor productivity has remained remarkably flat for nearly a decade, as thus far, recent improvements in technology are only showing productivity increases in the back-office efficiency of advisory firms. However, Kitces Research into “How Financial Advisors Actually Do Financial Planning” finds that enhancements in advisor productivity are beginning to emerge, not as a result of technology, but driven by three (non-technology) factors: client variability, advisor expertise, and (professional) staff support.

Scaling Financial Advice: What Actually Drives Efficiency And Advisor Productivity – While improvements in technology have led to increased productivity in a range of industries, financial advisor productivity has remained remarkably flat for nearly a decade, as thus far, recent improvements in technology are only showing productivity increases in the back-office efficiency of advisory firms. However, Kitces Research into “How Financial Advisors Actually Do Financial Planning” finds that enhancements in advisor productivity are beginning to emerge, not as a result of technology, but driven by three (non-technology) factors: client variability, advisor expertise, and (professional) staff support.

In terms of client variability, when advisors get more focused into a particular specialization or niche clientele, it enables them to develop more ‘repeatable expertise’ simply by targeting a more consistent group of clients who have more consistent needs to be serviced in the first place. This leads to the average niche-centric advisor spending 13% less time doing middle- and back-office support work, being able to service 14% more clients, and attracting more affluent clients (who pay higher fees), such that the top 10% niche/specialized advisors earn nearly 67% more than the top 10% non-niche advisors (earning $660,000 versus $395,000, respectively)!

Similarly, advisors who invest in their own expertise (e.g., by earning advanced degrees and designations) are able to complete the financial planning process with clients in significantly less time – a major increase in advisor productivity. Specifically, CFP professionals complete the financial planning process in nearly 22% less time on average than non-CFP advisors.

Kitces Research also shows that advisors who leverage professional support staff (i.e., paraplanners and associate advisors) to aid in the planning process have more time to spend in client meetings, leading to significantly more clients serviced and greater advisor take-home pay (even after the cost of the staff support)!

Ultimately, while technology may provide incremental improvements in advisor efficiency over time, Kitces Research shows that the greatest differences in advisor productivity are driven by the variability of their clientele (or lack thereof!), the depth of expertise of the advisor themselves, and how the firm leverages professional (not ‘just’ administrative) staff support to focus the advisor’s time where it has the most impact: in meetings providing value to clients!

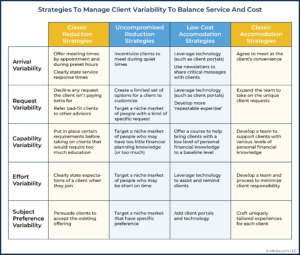

Managing Client Variability As A Pathway To Scalable Efficiency – As the typical financial advisory firm grows, so too does their ever-widening range of client needs. Rather than trying to figure out how to gain efficiency when serving an ever-widening range of clientele, though, an alternative approach is to actually try to tackle the issue of ‘client variability’ itself, recognizing that the advisory firm has a choice in the first place on whether to have clients with a wide range of needs (or not!), and, if so, whether or how much to actually accommodate those varying needs.

Managing Client Variability As A Pathway To Scalable Efficiency – As the typical financial advisory firm grows, so too does their ever-widening range of client needs. Rather than trying to figure out how to gain efficiency when serving an ever-widening range of clientele, though, an alternative approach is to actually try to tackle the issue of ‘client variability’ itself, recognizing that the advisory firm has a choice in the first place on whether to have clients with a wide range of needs (or not!), and, if so, whether or how much to actually accommodate those varying needs.

In her Harvard research on “Breaking the Trade-Off Between Efficiency and Service”, Dr. Frances Frei highlights two alternative strategies to manage client variability between just “doing more and charging more” or “doing less and charging less”: low-cost accommodation (where the firm offers flexibility to clients but ‘only' within a fixed range of choices), and uncompromised reduction where the firm doesn’t make compromises in the services it offers but instead reduces the breadth of who the firm serves in order to have a more focused clientele where their ‘customized’ services can still be delivered as repeatable expertise.

These techniques can be applied across each of the domains where client variability occurs: ‘arrival variability’ (by streamlining client meetings), ‘request variability’ (by using portals and digital tools to manage client requests), ‘effort variability’ (using tools to smooth data gathering and account openings), and ‘subjective preference variability’ (by standardizing solutions for common client preferences or systematizing higher-level service requests).

The key point is that advisors have an opportunity to either find more scalable low-cost accommodations for client variability that at least partially acquiesce to client requests while also enhancing efficiency, or to consciously choose a less-variable range of clientele in the first place in order to create room to provide a deeper service for those clients’ unique needs!

Business Management

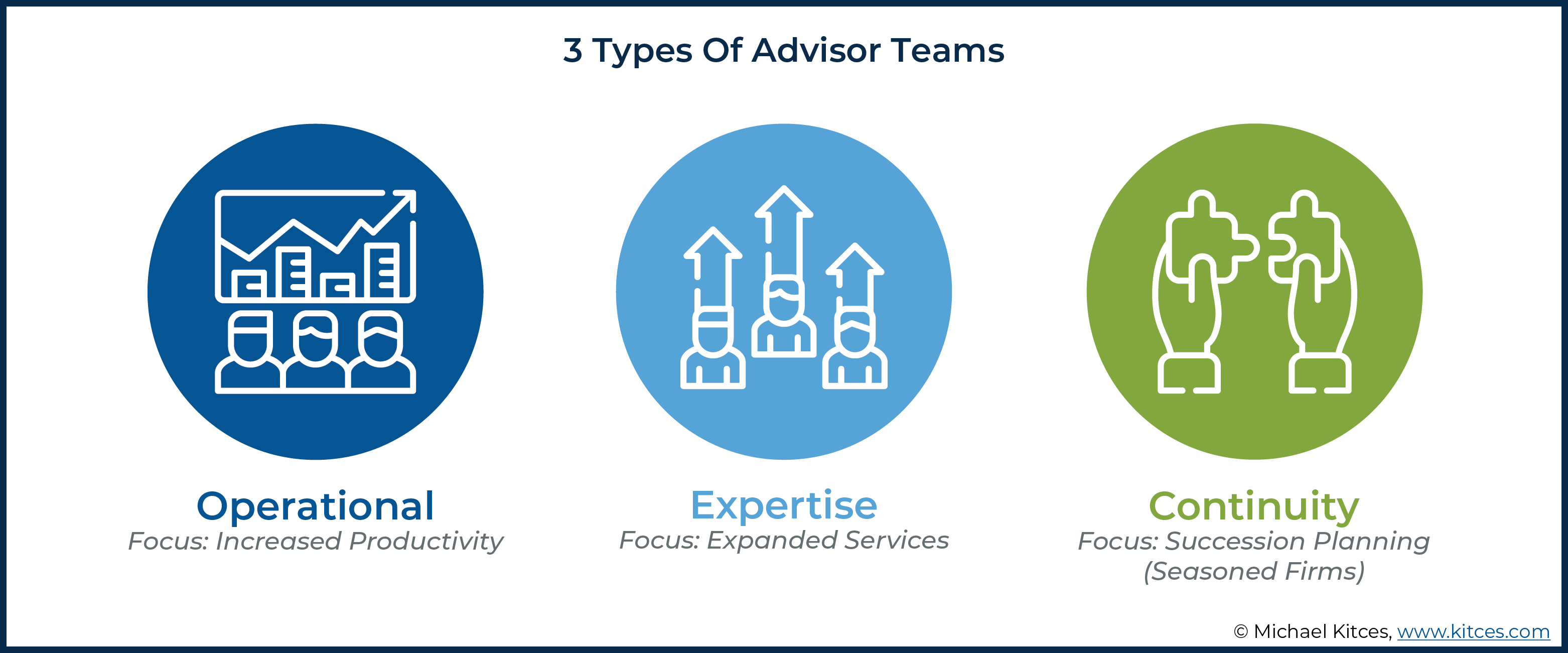

Three Types Of Advisor Teams And How To Leverage Each To Achieve Firm Goals – As an advisory firm grows, it can reach a critical mass of clientele that requires the firm to expand its capacity by shifting from the ‘solopreneur’ advisor model into forming an advisor team. Yet while the team model can improve operational productivity, expand service, and develop next-generation advisors, the ideal type of team to accomplish each of those goals is different, and as a result, it’s crucial to get clear about the purpose of the team to ensure those who are hired have the necessary skills!

Three Types Of Advisor Teams And How To Leverage Each To Achieve Firm Goals – As an advisory firm grows, it can reach a critical mass of clientele that requires the firm to expand its capacity by shifting from the ‘solopreneur’ advisor model into forming an advisor team. Yet while the team model can improve operational productivity, expand service, and develop next-generation advisors, the ideal type of team to accomplish each of those goals is different, and as a result, it’s crucial to get clear about the purpose of the team to ensure those who are hired have the necessary skills!

The three team models are the Operational advisor team, Expertise advisor team, and Development advisor team. The Operational team can increase revenue productivity and operational efficiency by establishing work roles that support advisors, allowing them to maximize their face time with clients, but requires trust to develop among all team members. The Expertise Team includes multiple advisors across different areas of expertise (e.g., CFPs and CPAs) to provide clients with more of a ‘one-stop-shop’ experience for their financial planning needs, and requires the firm owner to identify the specific services to be offered to that the right set of experts is selected for the team. The Development Team fosters new and rising talent in the firm, which requires establishing (time- and labor-intensive) training programs and a willingness of seasoned team members to delegate tasks to those with less experience to give them opportunities to learn (including the chance to make mistakes that they learn from!).

In the end, choosing the right type of team will depend on what is most important to the firm and the company’s overall goals, as advisors looking to expand services will hire very different types of teams than those looking to scale their existing services (Expertise vs Operational teams, respectively). But by taking the time to get a clear understanding of the goals the advisory firm is really trying to achieve, it’s easier to target the right type of team that brings the specific solutions necessary to meet organizational goals!

Alternative Custodian Options For Independent RIAs In The Wake Of Schwabitrade – For most independent RIAs who want to manage client portfolios, having an independent RIA custodian to work with is a necessity, given that custodians not only actually hold client assets (an important consumer protection) but also provide the core technology platform for a wide range of investment and billing services.

Because RIA custodians make very little to nothing from each trade in a client’s account, though, the businesses must operate with enormous volume to achieve the economies of scale to be able to compete with ‘alternative’ revenue streams. This has led to a wave of RIA custodial consolidation, with the largest being Charles Schwab’s acquisition of TD Ameritrade, leaving Schwab and Fidelity as the two big players in the RIA custodian space.

However, RIAs have more than just ‘Schwabitrade’ and Fidelity to choose from. While these giants can provide a wider range of services at the lowest cost, other RIA custodians offer service models that could better fit a given RIA. These include BNY Mellon’s Pershing Advisor Solutions and its ‘Menu of Models’ approach, Shareholder Services Group’s (SSG) high-touch service approach for advisors with no AUM minimums, TradePMR’s custom-built advisor technology platform, SEI’s all-in-one investment platform for RIAs, and newcomer Altruist’s efforts to build a ‘next generation’ RIA platform.

Ultimately, the reality is that, like the financial advice business itself, one size rarely fits all, and many clients (and their advisors) have unique needs that necessitate a more specialized solution. For advisory firms in this position, moving beyond the giant RIA custodians (and their ‘free’ offerings) in order to get the services and capabilities that are most meaningful for their firm and the clients they serve could be worth paying a little more for!

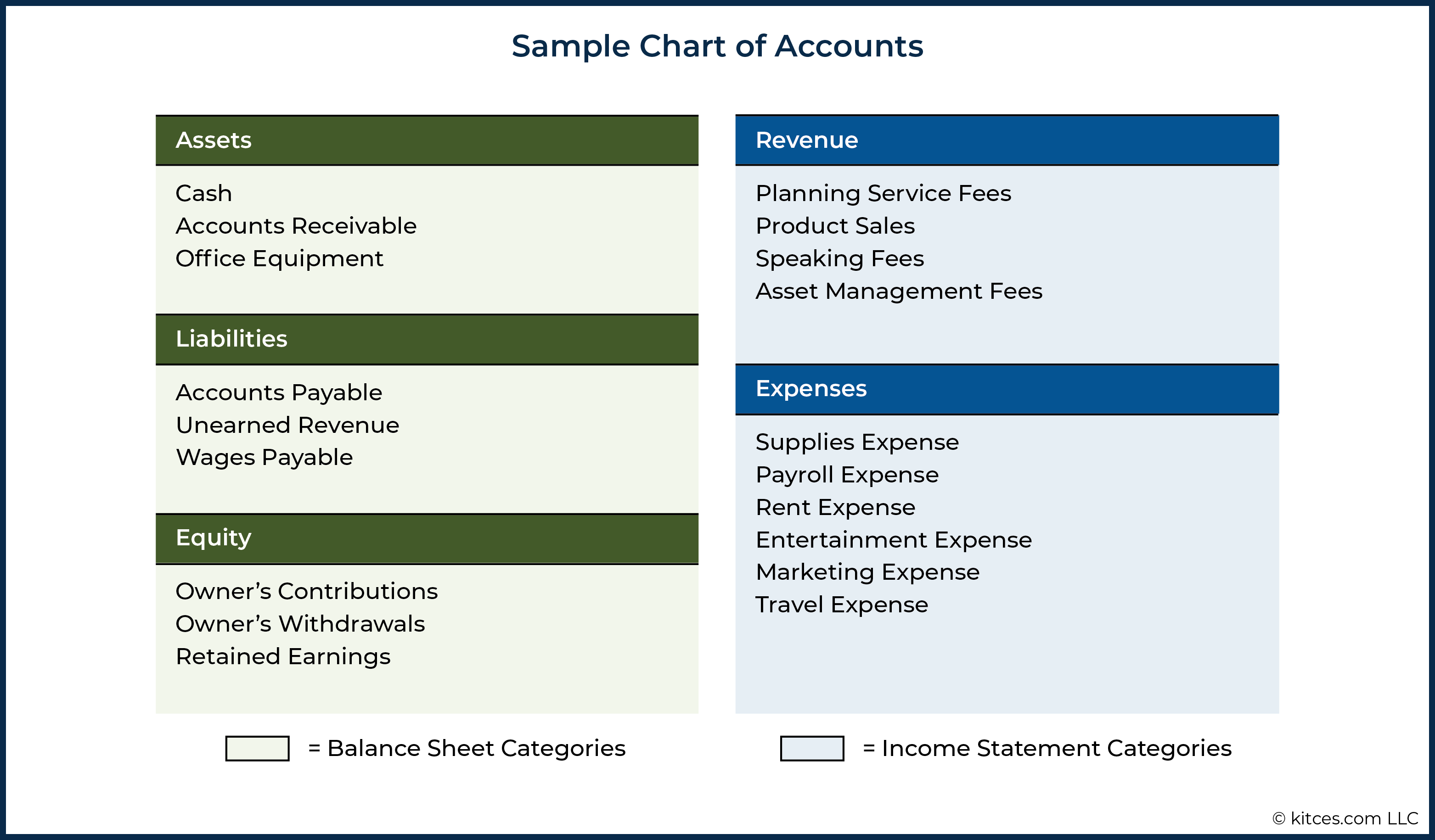

Creating A Chart Of Accounts: A Practical Guide For Financial Advisory Firms – Financial advisory firm owners are typically focused on gathering financial information from their clients to analyze their financial situation and make recommendations, but the reality is that advisory firms also require quality financial data about their own businesses to make informed decisions. And the key for consistent and accessible data that gives a clear picture of the firm’s financial health is having clear bookkeeping systems, guided by a standardized Chart of Accounts.

Creating A Chart Of Accounts: A Practical Guide For Financial Advisory Firms – Financial advisory firm owners are typically focused on gathering financial information from their clients to analyze their financial situation and make recommendations, but the reality is that advisory firms also require quality financial data about their own businesses to make informed decisions. And the key for consistent and accessible data that gives a clear picture of the firm’s financial health is having clear bookkeeping systems, guided by a standardized Chart of Accounts.

The first step towards building an effective Chart of Accounts is to sort business transactions in the firm’s bookkeeping systems (e.g., Quickbooks) into five categories: Assets, Liabilities, Equity, Income, or Expenses. These are then divided into subcategories – the “Accounts” in the Chart of Accounts – that are specific to the individual firm's operations. This means that firm owners have a great deal of flexibility when deciding how many (and which) Accounts should be used to track their firms' financial data.

A well-designed Chart of Accounts can be used to generate financial data that provides clear details about how different areas of the firm are performing, and where improvements can be made. Using consistent industry-recognized Chart of Accounts categories also makes it more readily feasible to participate in (and compare with) industry benchmarking studies to evaluate the firm's performance alongside its peers, which provides another useful approach for owners to gauge their firms' financial health.

Ultimately, the point of the Chart of Accounts is not just to have a system for organizing the firm's financial data, but to structure that financial data in a way that makes it easily accessible to use for business planning purposes. And by referencing an industry-standard Chart of Accounts template, firm owners can ensure that their firm's financial data will help them make the most well-informed decisions for their business!

Marketing

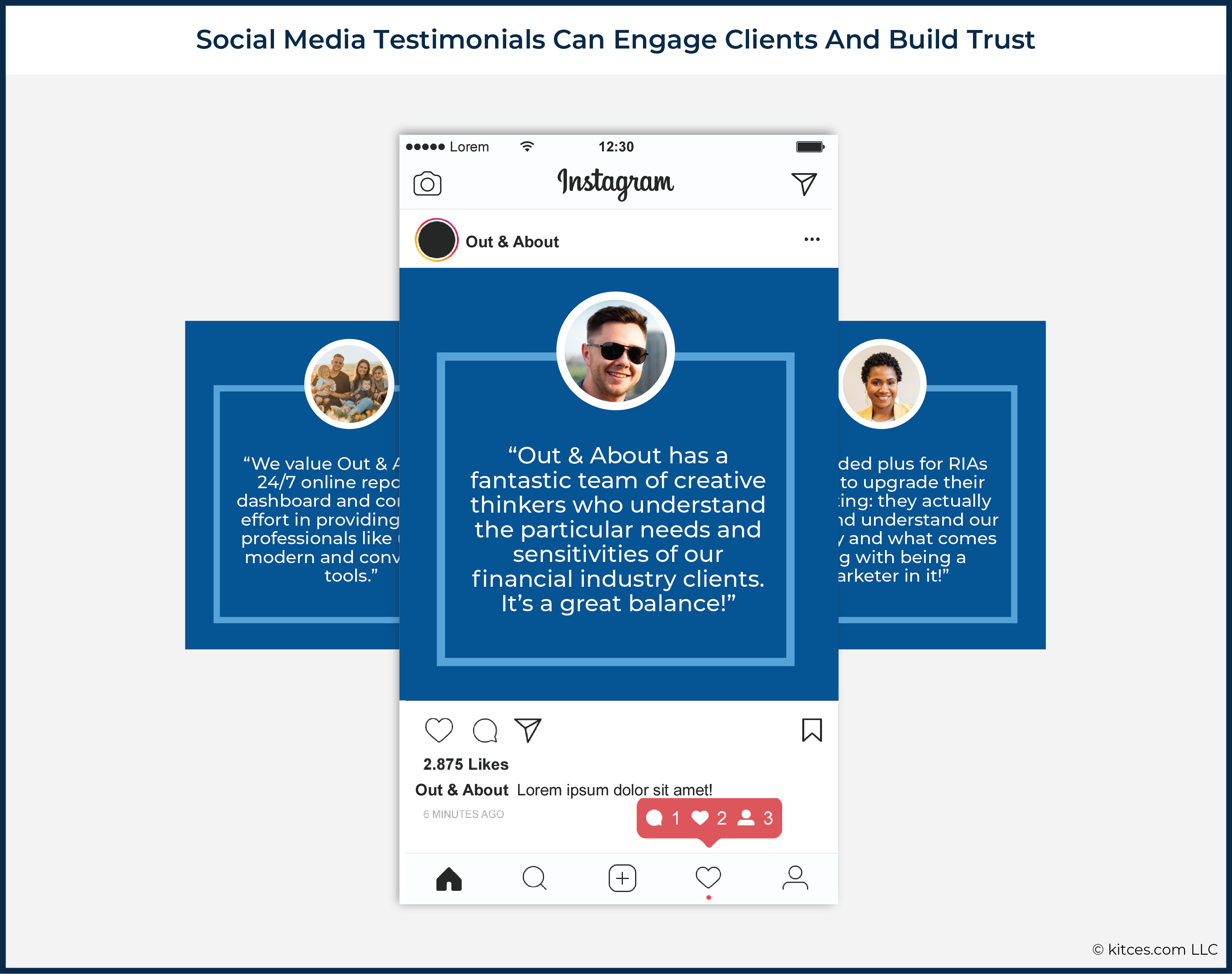

Client Testimonials: Leveraging The New SEC-Acceptable Marketing Practices To Connect With New And Existing Clients – From the 1970s until this year, the Securities and Exchange Commission (SEC) prohibited RIAs from using client testimonials in their advertising, in order to ‘protect’ consumers by preventing advisors from using select client testimonials in a manner that could potentially just showcase only their best investment results and not a ‘typical’ client outcome.

Client Testimonials: Leveraging The New SEC-Acceptable Marketing Practices To Connect With New And Existing Clients – From the 1970s until this year, the Securities and Exchange Commission (SEC) prohibited RIAs from using client testimonials in their advertising, in order to ‘protect’ consumers by preventing advisors from using select client testimonials in a manner that could potentially just showcase only their best investment results and not a ‘typical’ client outcome.

But as consumers have become increasingly reliant on testimonials and online reviews when choosing a wide range of products and services in the modern internet era, the SEC has also changed its view and in May finalized its updated Marketing Rule to allow the use of testimonials in RIA advertising materials. This change offers a new opportunity for advisory firms to provide social ‘proof’ of their ability to build relationships and create value through their services, and to develop trust and a positive reputation among potential clients.

Of course, firms will first have to generate a ‘supply’ of testimonials, which could come from existing material on third-party sites (e.g., Yelp), a Net Promoter Score (NPS) survey, or a direct email request to current clients to obtain new testimonials. Once they are collected, advisors can then select the best testimonials to use, which will go beyond general praise and will instead reflect the firm’s own values and specialization. And then adhere to the SEC’s new compliance rules for the required disclosures and documentation necessary to use these testimonials.

Of course, regardless of how the testimonials are ultimately used, they should complement the firm’s overall marketing strategy, and comply with SEC rules, including appropriate disclosures and client confidentiality. Luckily, the same principles that make for an effective testimonial – honesty, authenticity, and transparency – also lend themselves to compliance under the new rule, so that ultimately, firms that take advantage of the new rule allowing testimonials can do so while highlighting their services in a relatable, trust-building way!

Communicate Your Value As An Advisor By Explaining The “How” And Not Just The “What” – Advisors are used to communicating the services they offer, from retirement planning to investment management, to prospective and current clients. However, because it’s difficult to convey the value of an intangible service to prospects and clients, often it’s more effective to explain how the advisor will implement their strategies, which makes it possible to demonstrate the advisor’s value by showing the process itself!

Communicate Your Value As An Advisor By Explaining The “How” And Not Just The “What” – Advisors are used to communicating the services they offer, from retirement planning to investment management, to prospective and current clients. However, because it’s difficult to convey the value of an intangible service to prospects and clients, often it’s more effective to explain how the advisor will implement their strategies, which makes it possible to demonstrate the advisor’s value by showing the process itself!

After all, while clients expect that they will get a financial plan and/or have their assets managed by the advisor, the fact that the advisor will ultimately deliver a financial plan and implement portfolio trades doesn’t actually differentiate them; instead, it’s how they conduct their financial planning and investment processes that actually demonstrate their unique value. This means that considering the impact of communicating how prospects-turned-clients will be guided and supported through the financial planning process – the actual steps of the process and what the advisor will actually do in each step – is an opportunity to sell value.

One tactic advisors can use to better explain the ‘how’ of their service offerings is to create a chart that clearly identifies not just the services the advisor offers, but also the process they use to provide each of those services. This can be useful both internally (to improve focus on processes versus services), and with prospective clients (as a tool to facilitate discussions of not only their financial planning priorities, but also their expectations of the advisor). For instance, the advisor might not just state that they do “estate planning”, but their process of meeting with clients three times to explore their financial goals and history, review and diagram their existing estate documents, and then meet jointly with an attorney to propose changes and make document updates.

Ultimately, while financial advisors may find it difficult to articulate their value in ways that are most meaningful to prospects, identifying how to switch to focus on language that highlights the “how” of an advisor’s services instead of just what the services are, can be a good opportunity to showcase value that will resonate with the prospect most!

Career Development

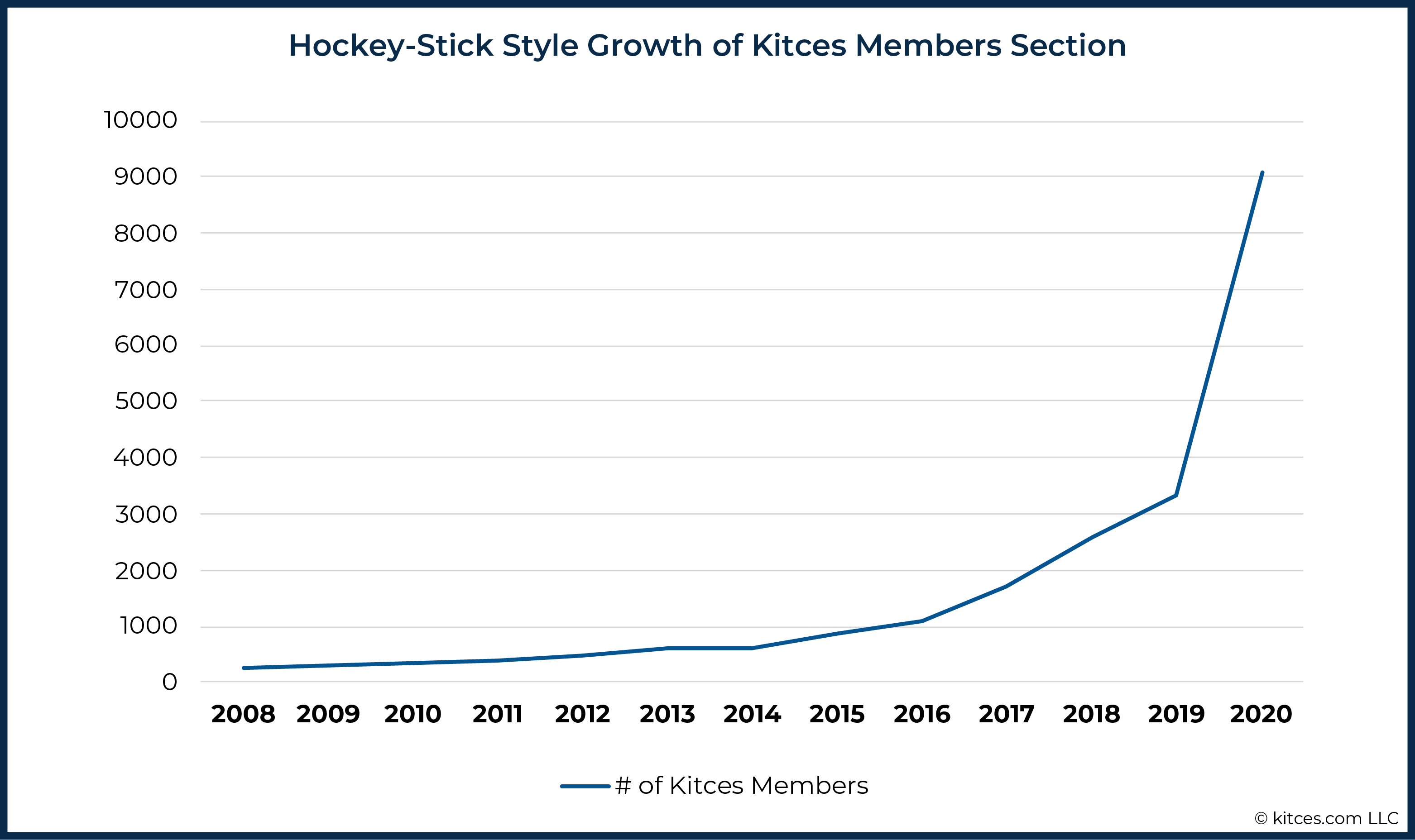

Creating Hockey-Stick Style Growth By Taking The Uncomfortable Leap – Everyone hopes that their lives will improve in the future, but we sometimes get stuck on the path to getting there. And while moving down a better path—whether it is creating a more profitable firm or having more personal time— can require a potentially scary moment of ‘taking the leap’, changing one’s mindset and thinking differently about what’s possible in the first place can make it easier for us to actually take the actions that will improve our lives!

Creating Hockey-Stick Style Growth By Taking The Uncomfortable Leap – Everyone hopes that their lives will improve in the future, but we sometimes get stuck on the path to getting there. And while moving down a better path—whether it is creating a more profitable firm or having more personal time— can require a potentially scary moment of ‘taking the leap’, changing one’s mindset and thinking differently about what’s possible in the first place can make it easier for us to actually take the actions that will improve our lives!

For an advisor, the first step to finding a better path is to write down their revenue, income, hours worked each week, and time off per year, and then write down what they hope it could be if there were no constraints. Bogan suggests the advisor then double those goals… and reflect on the negative thoughts that come to mind telling them ‘it can’t be done’ or is ‘too good to be true’. Facing these ‘limiting beliefs’ allows us to get clear on what we have been avoiding, why we have gotten stuck in that pattern… and what steps are needed to achieve a different and better outcome.

The key point is to understand that what limits our success is not actually figuring out how to get to the next level, but the stories we tell ourselves that lead us to deny ourselves what is actually possible. Of course, that doesn’t mean that the path of making a change won’t still entail challenges and a potentially significant amount of discomfort. But if an advisor has already become ‘comfortably uncomfortable’ with their current level of under-success, that discomfort can be redirected to their advantage!

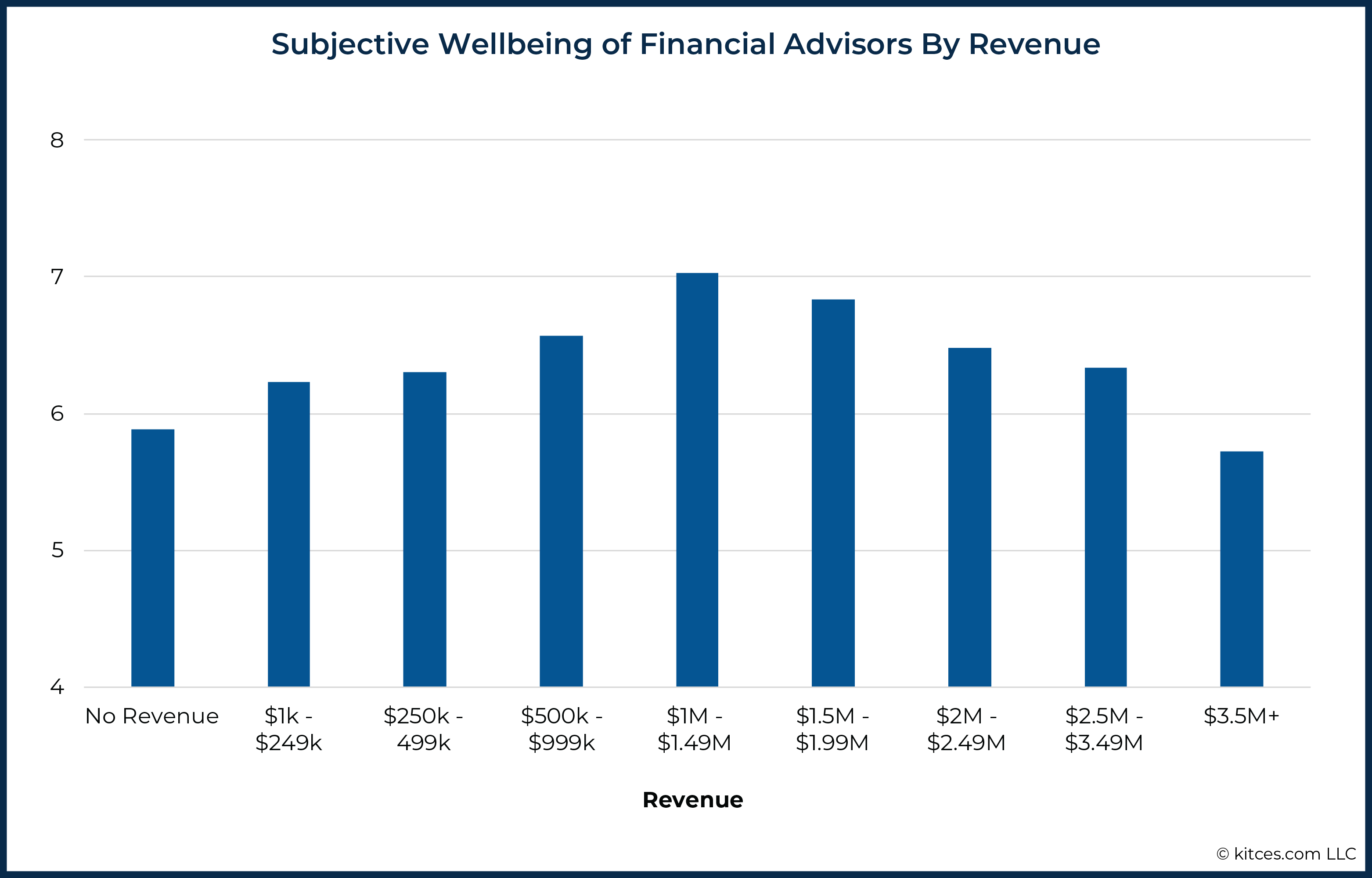

Lifting Advisor Wellbeing By Focusing On Time And Income Over Revenue Alone – Building a financial advisory business can be a rewarding endeavor. In fact, the latest Kitces Research on Advisor Wellbeing shows that financial advisors do in fact enjoy not only above-average income, but above-average wellbeing in all 18 sub-scales of the Comprehensive Inventory of Thriving (a comprehensive measure of wellbeing).

Lifting Advisor Wellbeing By Focusing On Time And Income Over Revenue Alone – Building a financial advisory business can be a rewarding endeavor. In fact, the latest Kitces Research on Advisor Wellbeing shows that financial advisors do in fact enjoy not only above-average income, but above-average wellbeing in all 18 sub-scales of the Comprehensive Inventory of Thriving (a comprehensive measure of wellbeing).

The caveat, though, is that while advisor wellbeing does steadily rise as advisor income grows, advisor wellbeing on average actually begins to decline once the aggregate revenue of the business exceeds $1.5 million. This shift appears to be driven by the reality that when revenue grows materially beyond this point, the firm’s infrastructure and staffing grow to the point where the founder’s role is transformed from an advisor to a manager, with an increased time burden, and potentially reduced autonomy over their own schedule.

In fact, dips in wellbeing are also observed at lower revenue levels (approximately $275,000, $550,000, and $825,000 of revenue), which are associated with capacity thresholds where advisory firms must typically hire to service their ever-growing number of clients.

Ultimately, maximizing the value of our time – i.e., earning the most revenue in the least amount of time – appears to be one of the greatest drivers of advisor wellbeing. Which means the key to ‘happy growth’ is not just adding more clients, but specifically increasing revenue per client (by attracting and serving more affluent clients who can pay higher fees), allowing advisors to do their most rewarding work. And in the long run, this could even mean growing one’s wellbeing by working with fewer clients… just the ones who most value the time and value that their financial advisor provides!

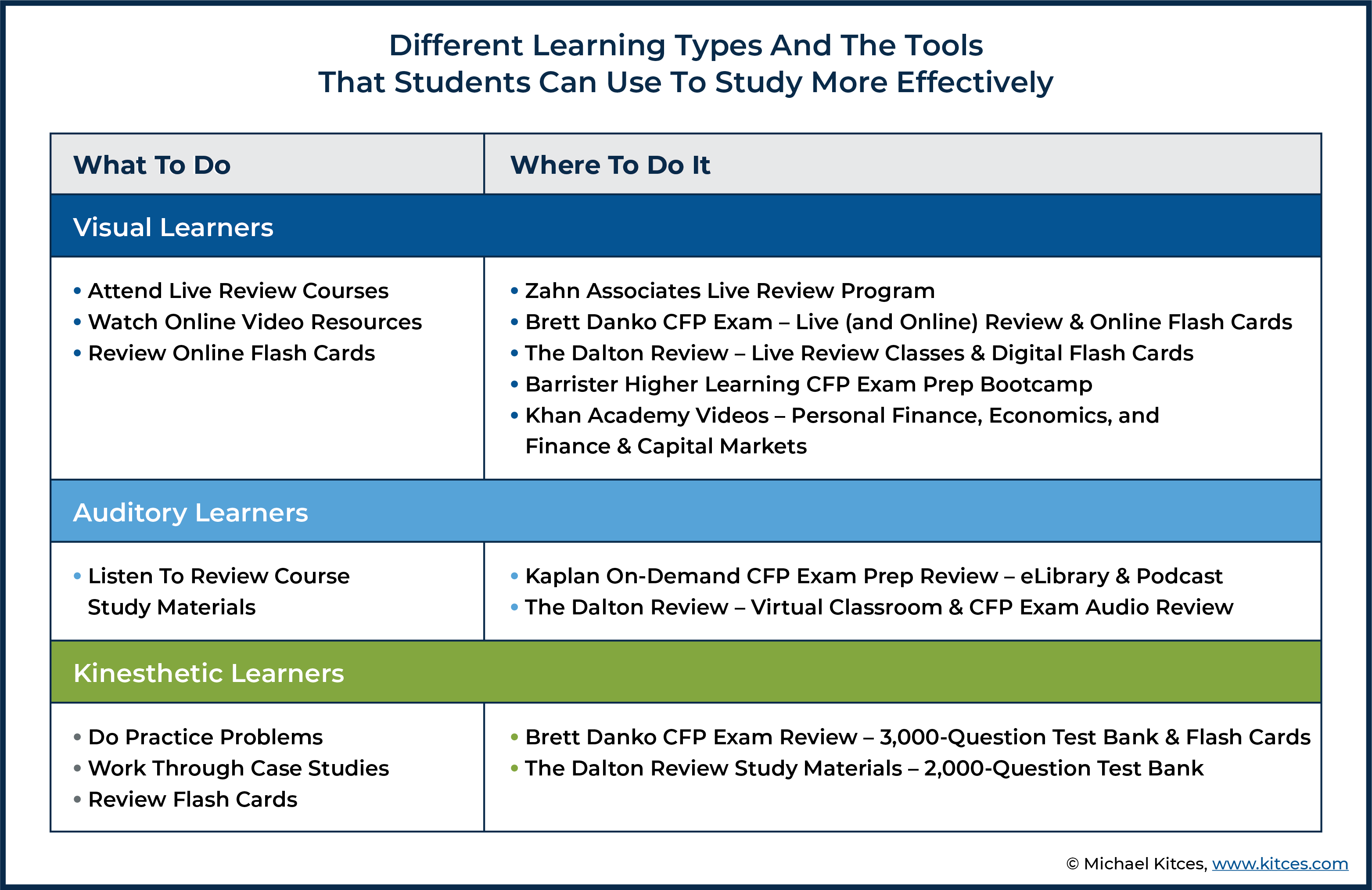

How To Study For (And Pass) The CFP Exam – Because the CFP Exam is a rigorous test with a broad scope of material covered, and a relatively low pass rate (generally ranging from 60-65%), candidates aspiring for CFP certification typically invest significant study time to ensure they pass the exam. And to make sure that they structure the time devoted to test preparation (typically 150-200+ hours) most effectively, candidates should consider several factors, including their study habits, the resources available to them, and how to structure a schedule to follow to stay on track to best prepare for the exam.

How To Study For (And Pass) The CFP Exam – Because the CFP Exam is a rigorous test with a broad scope of material covered, and a relatively low pass rate (generally ranging from 60-65%), candidates aspiring for CFP certification typically invest significant study time to ensure they pass the exam. And to make sure that they structure the time devoted to test preparation (typically 150-200+ hours) most effectively, candidates should consider several factors, including their study habits, the resources available to them, and how to structure a schedule to follow to stay on track to best prepare for the exam.

Perhaps most important, though, is to recognize that not everyone takes in information the same way, which means a study style that works well for one CFP candidate may still fail for another. Accordingly, it is helpful for candidates to reflect on whether they are more of a visual, auditory, or kinesthetic learner. This knowledge can not only help candidates understand the best way to study for the exam (e.g., kinesthetic learners might prepare best by doing practice questions, while auditory learners may prefer listening to podcasts that review the material), but also choose the best exam prep tools, including review programs that help candidates understand the style and pacing of questions, review the material on the exam, and provide practice questions and mock exams.

While the CFP exam requires significant preparation, in the end, the payoff of passing is well worth the sacrifice, given the higher average earnings of CFP certificants over other advisors. Which is a result of not only the knowledge learned – to more positively impact clients’ lives – but also because of the confidence that CFP professionals gain in being able to set themselves apart as competent and knowledgeable financial planners!

Retirement

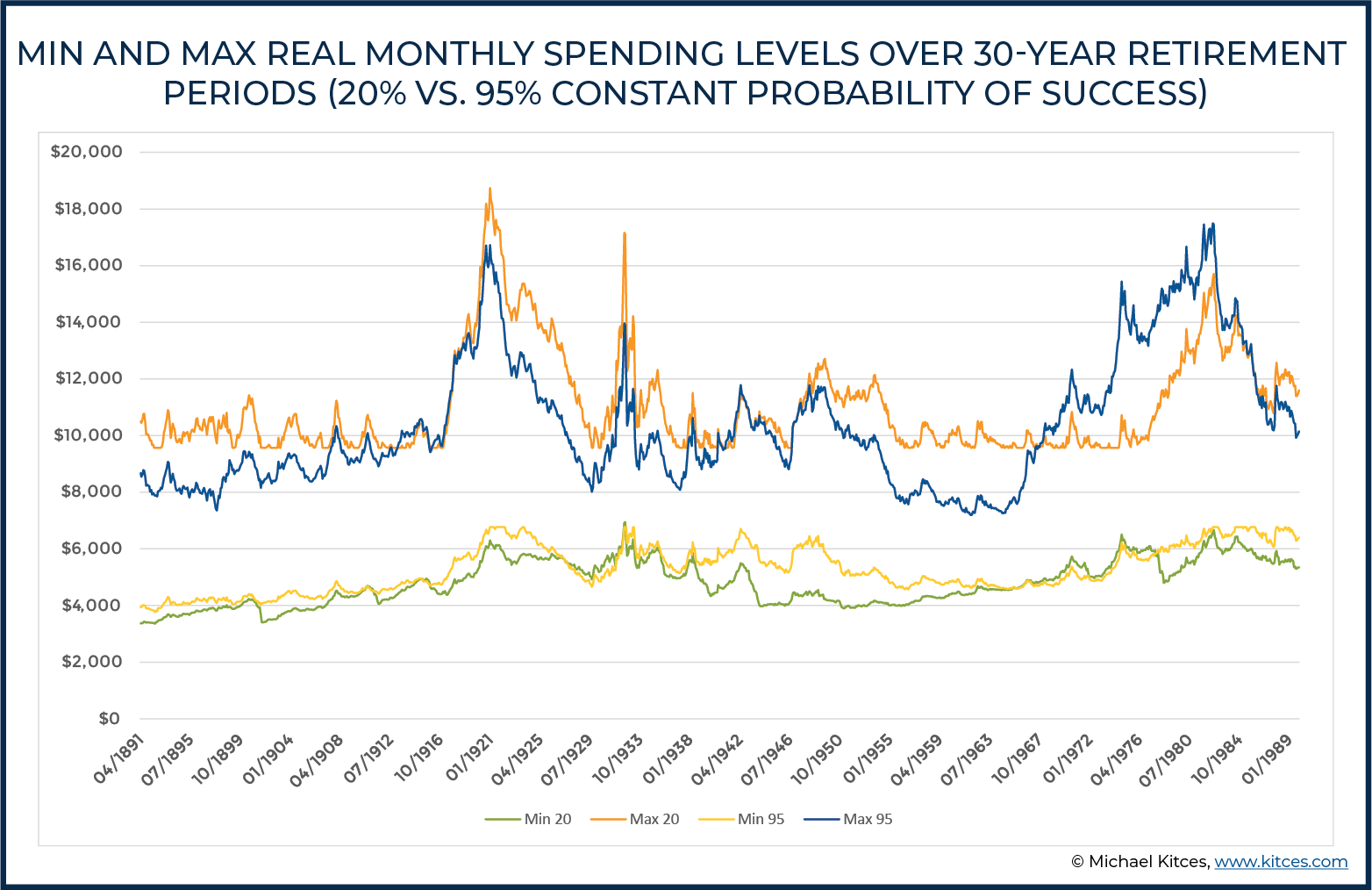

Why A 50% Probability Of Success Is Actually A Viable Monte Carlo Retirement Projection – Monte Carlo analysis has become the most commonly used method of conducting retirement projections for clients, with clients typically aiming for a very high ‘probability of success’ (because no one wants to “fail” at retirement!).

Why A 50% Probability Of Success Is Actually A Viable Monte Carlo Retirement Projection – Monte Carlo analysis has become the most commonly used method of conducting retirement projections for clients, with clients typically aiming for a very high ‘probability of success’ (because no one wants to “fail” at retirement!).

The caveat, though, is that while a probability of success result of less than 100% can be difficult to accept for clients who want a ‘guarantee’ that they will not run out of money in retirement, not all “failures” all the same. Instead, it is important to note how severe the failure is; for example, a client who relies solely on their investment portfolio for retirement has a much greater potential ‘magnitude of failure’ than a client whose income comes mostly from guaranteed sources that the portfolio merely supplements.

In addition, the reality is that retirees can – and typically do – make adjustments if their retirement spending and portfolio returns are veering off-track, long before they reach an actual moment of crisis. In fact, because the ‘safe’ spending level set at the beginning of retirement can be updated as time goes on, a Monte Carlo projection’s ‘probability of failure’ is really more of a ‘probability of adjustment’ instead.

And as it turns out, the adjustments to spending needed to stay on track in down markets are less than many retirees might think. When looking at historical data going back to 1871, the median, minimum, and maximum spending levels throughout 30-year retirement periods are actually quite consistent regardless of the probability of success used! In other words, for clients who are willing to make adjustments, initial spending levels are remarkably similar with a 50% or 90% initial ‘probability of success’; instead, the data show the probability of success level targeted is actually more about a trade-off between income and legacy than any genuine difference in the risk that a portfolio will be depleted.

The key point is that choosing a probability of success level to use is not as simple as being able to apply a one-size-fits-all rule or a natural tilt toward being 'conservative' for the sake of not running out of money. By reframing as a “probability of adjustment” instead, and presenting clients with a range of potential adjustment strategies, retirees may ultimately find it far more comfortable to choose substantively lower probabilities of adjustment, as they weigh for themselves their willingness to accept spending changes along the way, and the potential trade-offs between how much of their money they enjoy while they’re alive, and the amount they leave as a legacy instead!

Getting Comfortable Delaying Social Security With Six-Month ‘Reversible’ Delays – Financial advisors often assist clients in deciding when to file for Social Security benefits, helping them choose between filing prior to their Full Retirement Age (FRA) for a reduced benefit, filing at FRA for the ‘full’ benefit, or delaying benefits after FRA until (at the latest) age 70 to increase the monthly benefit by 8% per year. The challenge, though, is that while the objective ‘numbers’ can show how delaying often maximizes benefits over life expectancy, this decision can lead to subjective feelings of anxiety and doubt for clients who worry about making the ‘wrong’ decision.

Fortunately, the Social Security rules allow advisors to reframe the filing decision to make it easier for their clients to decide more confidently whether to file or delay. As in addition to an eligible individual being able to file at any time between age 62 and 70, once they have reached FRA, they can apply for up to six months of retroactive benefits, allowing them to receive a lump sum of accumulated payments while also activating their monthly benefits going forward.

Therefore, advisors can reframe the choice of when to file (after reaching FRA) as a series of reversible decisions for six months at a time – as if the client delays, they can always reverse their delay for the next 6 months… and if they accept that 6-month delay, they can delay for another 6 months (with the opportunity to reverse again, or not), and then continue to repeat the evaluation at each incremental delay. Not only does this framing provide the client with a more reasonable timeframe to foresee future health issues or other factors that could cause them to change their mind, but because the six-month intervals align with the period in which individuals can apply for retroactive benefits, each six-month decision remains entirely reversible.

Notably, there are some risks and tradeoffs to this strategy (e.g., the temporary spike in income when the retroactive benefits are paid, which could impact tax deductions, credits, and Medicare premiums), by nudging clients with the option to consider when to claim benefits through six-month ‘reversible’ decisions, advisors can potentially help them make better choices and to act (or not act, and instead delay) with confidence!

Tax

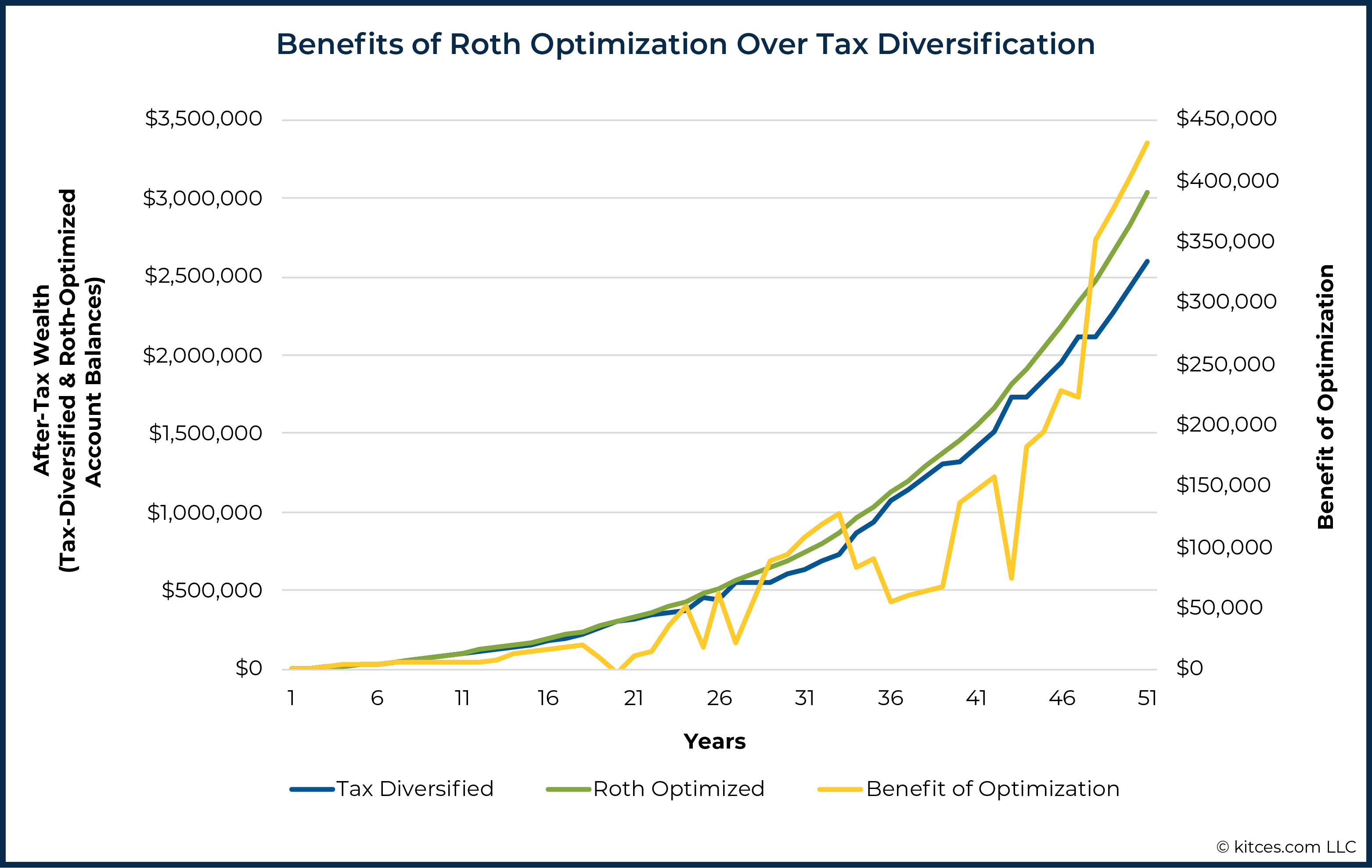

Limits Of Tax Diversification And The Tax Alpha Of Roth Optimization – The Roth IRA has been an incredibly popular retirement vehicle, thanks to its ‘unlimited’ potential for generating tax-free growth. Of course, the caveat is that contributions to Roth accounts are still taxed upfront, unlike traditional retirement accounts that are not taxed until withdrawal, which means in the end the benefit of a Roth-style account isn’t about preferential tax treatment, per se, but choosing to pay taxes now (at the time of contribution) instead of later (when withdrawn). For those who aren’t certain which will turn out better, it’s not uncommon to choose to ‘tax diversify’ by splitting contributions between Roth and traditional accounts. Yet in the end, this strategy does not actually diversify the risk of a change in tax rates, but rather simply neutralizes the opportunity altogether!

Limits Of Tax Diversification And The Tax Alpha Of Roth Optimization – The Roth IRA has been an incredibly popular retirement vehicle, thanks to its ‘unlimited’ potential for generating tax-free growth. Of course, the caveat is that contributions to Roth accounts are still taxed upfront, unlike traditional retirement accounts that are not taxed until withdrawal, which means in the end the benefit of a Roth-style account isn’t about preferential tax treatment, per se, but choosing to pay taxes now (at the time of contribution) instead of later (when withdrawn). For those who aren’t certain which will turn out better, it’s not uncommon to choose to ‘tax diversify’ by splitting contributions between Roth and traditional accounts. Yet in the end, this strategy does not actually diversify the risk of a change in tax rates, but rather simply neutralizes the opportunity altogether!

An alternative to the ‘tax diversification’ strategy is to ‘Roth optimize’ exactly when to add dollars to tax-free Roth accounts (or to contribute to traditional pre-tax retirement accounts instead). Because a household’s tax rates typically vary throughout life (e.g., lower during career transitions or when time out of the workforce to care for a family member, and higher during peak earnings years and when major bonuses are paid or business liquidity events occur), there will be years where a household can ‘time’ its tax situation by contributing to traditional IRAs in years when income and tax rates are high, and tactically switching to Roth contributions (or even engaging in Roth conversions) when tax rates are unusually low.

And while there is always a risk that the government will change tax rates in the future, in reality, tax deductions have often changed alongside the brackets, such that changes in effective tax rates have actually been remarkably narrow throughout history. In other words, the variability of tax rates due to Congress (which we can’t control) is actually dwarfed by changes in tax rates within the household over time (which can be planned for!).

The key point is that arbitrarily splitting dollars between traditional and Roth-style retirement accounts as a tax diversification strategy isn’t actually a positive wealth-creating strategy; instead, it is more akin to ‘going to cash’ and eliminating the opportunity altogether. For those who want to actually maximize wealth with the traditional-vs-Roth decision, the better approach is to try to Roth-optimize by timing when to shift between traditional and Roth accounts.

Can A Charitable Remainder UniTrust (CRUT) Truly Replace The Benefits Of The “Stretch” IRA? – The SECURE Act of 2019 dramatically limited the ability of non-spouse Designated Beneficiaries to ‘stretch’ distributions from the inherited retirement accounts, and instead imposed a 10-Year Rule to liquidate the accounts for most non-spouse beneficiaries. Because this compressed liquidation period for retirement account beneficiaries raises the chances that the beneficiary will be bumped into a higher tax bracket, some practitioners have considered using Charitable Remainder UniTrusts (CRUTs) to reduce the tax impact on beneficiaries.

However, while CRUTs can appear to approximate many of the qualities of the ‘Stretch’, they are rarely the optimal choice for those retirement account owners who are primarily interested in transferring as much wealth as possible to heirs. This is because such trusts are generally not even possible to establish with lifetime distributions for beneficiaries in their early 20s or younger, and older beneficiaries often do not live long enough to make the extended tax deferral outweigh the ‘loss’ of the CRUT’s remainder assets that must pass to charity. The CRUT tactic also limits the optionality of a beneficiary (who has to wait to receive the full amount of their inheritance), and increases organizational and operational expenses (as the CRUT must be drafted, maintained by a trustee, etc.).

But while CRUTs have probably been over-hyped for purely their wealth-transfer ability, for retirement account owners looking to satisfy both legacy (to heirs) and charitable goals, they can still be a powerful tool. In many situations, the result of such planning will be a modest reduction in the wealth passed to heirs, in exchange for a much larger increase in the amount that goes to charity (in lieu of going to Uncle Sam in the form of ongoing income taxes).

Ultimately, if just the right circumstances present themselves, or if a retirement account owner is sufficiently charitably inclined, naming a CRUT as the beneficiary of a retirement account is a planning strategy worth exploring. But for retirement account owners solely looking to maximize the transfer of wealth to heirs, the bottom line is that a CRUT is generally not a great (or is at least a “risky”) alternative to just accepting the limited 10-year rule for an inherited retirement account.

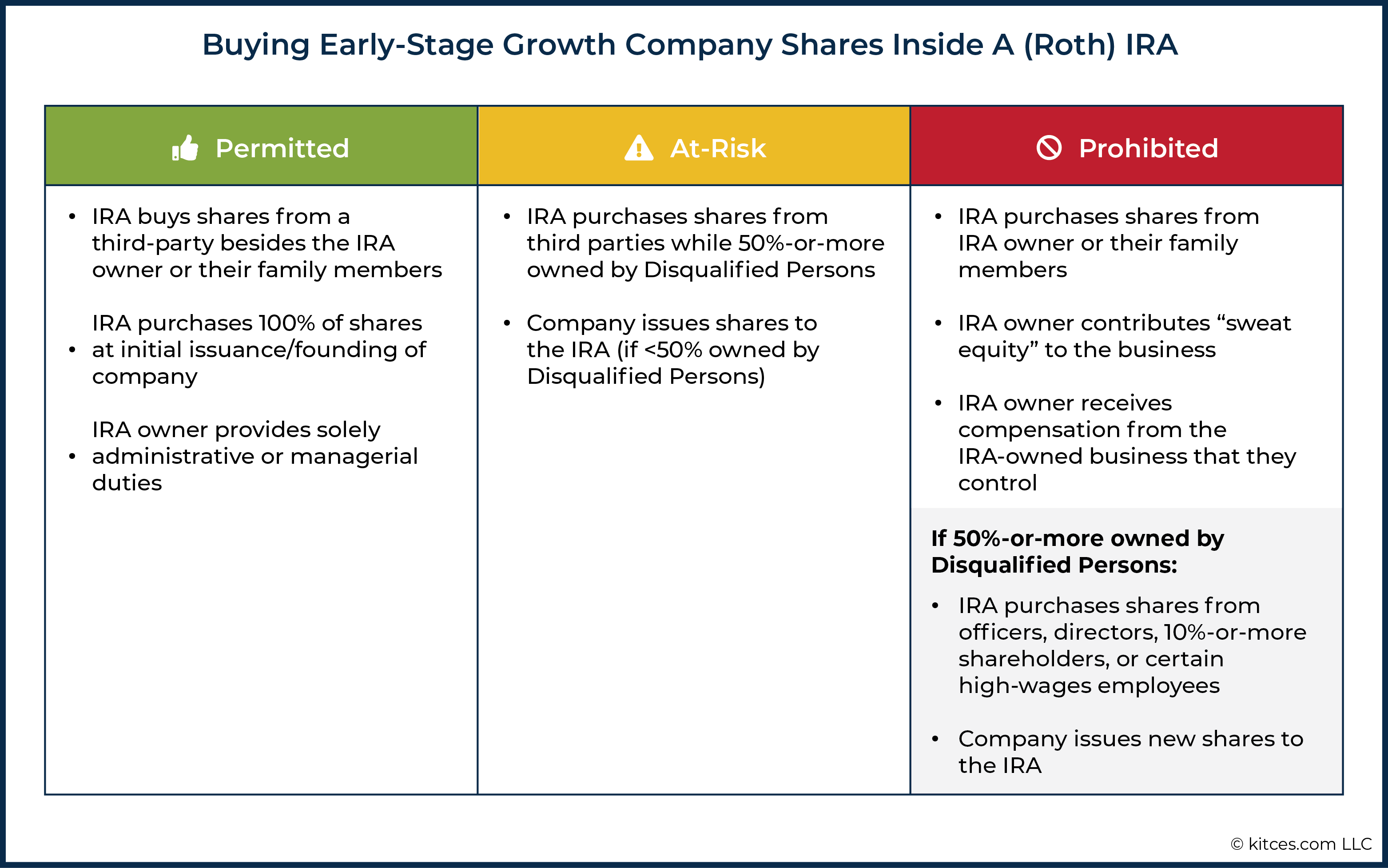

Investing A Roth IRA In Early Stage Growth Companies Without Violating Prohibited Transaction Rules – A June article from ProPublica on how Peter Thiel built up a $5 billion Roth IRA (in large part by putting into the Roth account early stage company shares that subsequently skyrocketed) made many business owners wonder how they could shift some of the value of their growing business into their retirement account as well. However, the reality is that while a Roth IRA can own shares of privately held companies, there are limitations on who an IRA can buy shares from, and who can be compensated by an IRA-owned company, under the so-called “Prohibited Transaction” rules.

Investing A Roth IRA In Early Stage Growth Companies Without Violating Prohibited Transaction Rules – A June article from ProPublica on how Peter Thiel built up a $5 billion Roth IRA (in large part by putting into the Roth account early stage company shares that subsequently skyrocketed) made many business owners wonder how they could shift some of the value of their growing business into their retirement account as well. However, the reality is that while a Roth IRA can own shares of privately held companies, there are limitations on who an IRA can buy shares from, and who can be compensated by an IRA-owned company, under the so-called “Prohibited Transaction” rules.

At the highest level, the Prohibited Transaction rules restrict an individual from using their (Roth) IRA to engage in various types of transactions with certain “Disqualified Persons”, which include the IRA owner themselves, certain family members, along with businesses (as well as their officers and other key individuals) in which a Disqualified Person owns at least a 50% stake. The Prohibited Transactions with Disqualified Persons for IRAs include buying/selling property, lending/borrowing, or furnishing/receiving goods, services, or facilities. Failure to abide by these rules results in a deemed distribution of the entire IRA as of January 1 of the year in which the Prohibited Transaction occurs (causing a forced liquidation of the entire retirement account and forfeiting its tax-preferenced status altogether!).

That said, an individual who wants to start a new business owned by an IRA can do so as long as the shares are issued to the IRA prior to the formation and capitalization of the company. Yet, these entrepreneurs must still be cautious with respect to their providing services or receiving compensation from the company, which could create a Prohibited Transaction. However, once the company has been created – and especially where it is majority-owned by the founder – the Prohibited Transaction rules make it difficult to get shares into the IRA at all.

Ultimately, while IRAs can be used to purchase private, non-public companies, the Prohibited Transaction rules significantly restrict both who can sell shares to the IRA, what compensation the entrepreneur can receive when working for an IRA-owned company, and even the ability to contribute sweat equity to an IRA-owned company. Which is important to navigate, given the harsh tax consequences associated with the Prohibited Transaction rules, and in practice greatly diminishes the opportunity for most small business owners to hold their businesses in a (Roth) IRA!

Investments

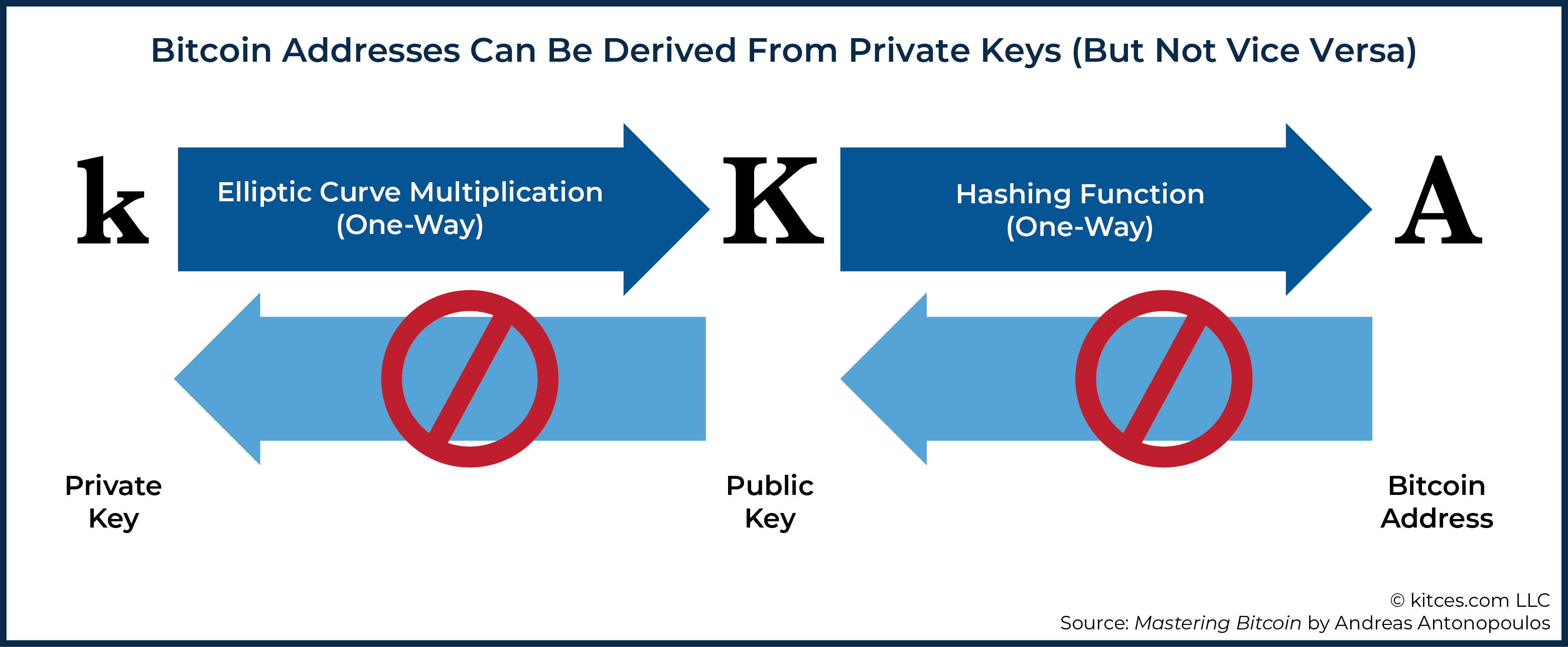

Storing Cryptocurrency Securely: The Safest Options For New And Experienced Investors – Bitcoin and other cryptocurrencies have gained significant attention this year thanks to their dramatic price swings and growing uptake among retail investors. One of the challenges for cryptocurrency investors (and their advisors), though, is keeping crypto holdings secure, given that the whole point of “decentralized finance” is that they cannot be held directly in a traditional brokerage account.

Storing Cryptocurrency Securely: The Safest Options For New And Experienced Investors – Bitcoin and other cryptocurrencies have gained significant attention this year thanks to their dramatic price swings and growing uptake among retail investors. One of the challenges for cryptocurrency investors (and their advisors), though, is keeping crypto holdings secure, given that the whole point of “decentralized finance” is that they cannot be held directly in a traditional brokerage account.

Instead, cryptocurrency is held in a virtual “wallet”, a digital account structure that is built around a ‘public key’ (the digital address to which cryptocurrency deposits are made or withdrawn from) and a ‘private key’ (the password that the owner uses to access the account). The caveat, though, is that because anyone who gains access to the private key can access – i.e., take all the cryptoassets from – a crypto wallet, it’s especially important to keep private keys secure. And hackers are especially focused on trying to gain access to crypto owners’ private keys.

In practice, advisors have several solutions available for storing clients' (or their own) crypto holdings. For the less tech-savvy advisor, using a reputable exchange or storage provider that provides wallets via their platform can be a lower-risk solution, particularly as more mature firms develop in this space. For the slightly more tech-savvy user, though, hardware wallets are likely the ideal balance between security and the technical sophistication needed to implement a strategy. These are single-purpose computing devices that are designed solely to store cryptocurrency keys. Quality hardware wallets use a combination of security features that help ensure that someone’s coins are safe and retrievable, even in the event that their hardware wallet is lost or stolen.

The key point is that those who own cryptocurrency need to take appropriate security measures to address the unique nature of how these assets are owned and held. This is especially true for those who are looking to invest not only for themselves, but also for others. The good news is that as cryptocurrency investing becomes more mainstream, more options are coming available for investors to use (or advisors to facilitate on their behalf)… although ironically, as cryptocurrencies become accessible through more ‘traditional’ platforms, they may become less differentiated as an investment holding and perform more like other ‘traditional’ investment assets!?

Podcasts

#FA Success Ep 247: Systematizing How To ‘Deliver Massive Value’ To Charge What You’re Really Worth, With Matthew Jarvis – Financial advisors want to deliver value to clients and be compensated appropriately for that work. In this episode, Matthew Jarvis explains how he systematized his business processes, and a regular (quarterly) series of client deliverables, in order to deliver even more value to his clients… and then raised his fees by 50% (to a baseline AUM fee of 1.5%!) so that he is fairly compensated for the greater value he now delivers!

Matthew has managed to double his firm’s AUM (to $240M) in the past four years by focusing on onboarding increasingly higher net worth clients, adding an advisor to increase capacity, and benefiting from the systematized processes. Of course, not all tasks along the way have been pleasant, and Matthew uses a concept he calls “extreme accountability” to get himself to move forward on difficult tasks by making the status quo even more unpleasant than the task itself. For example, he was only able to make the move to hire an additional advisor after getting over his limiting belief (or “head trash” as he calls it) around doing so.

Matthew has also improved the performance of his firm by “graduating” some of its least profitable clients onto other advisors. By framing the separation as a way for the client to move on to a different advisor (with recommendations from Matthew) who can service them better, and refunding an entire quarter’s worth of fees, Matthew was able to get past the limiting belief that he was doing wrong by the clients.

The key point is that an advisory firm owner has to make difficult choices in order to deliver ‘massive value’ to clients and be compensated accordingly. However, as Matthew shows, this can be done in a way that can make both the advisor and their (current and former) clients feel empowered!

#FASuccess Ep 210: Growing Your Client Base By Making Advice The “Product” And Quantifying Its Value, With Sten Morgan – The financial advisory industry traditionally emphasized sales of products (e.g., life insurance policies or mutual funds) rather than the sale of the advice itself. However, the ground is shifting on this issue with new fee models that charge for advice first. With the caveat that advice itself is even less tangible than financial services products, making it harder to explain the value of that advice (and why it’s worth the fee that the advisor charges).

In this episode, Sten Morgan explains how he has built his advisory firm by making himself and his planning ideas into his ‘product’, charging first and foremost for his advice. He begins demonstrating his expertise with prospects from the very beginning by highlighting new planning ideas for them right away, rather than waiting until they officially become clients. In addition, Sten quantifies the value he provides to clients (e.g., through reviews of their current insurance and estate documents), which demonstrates to prospects that his firm has already identified areas where they can save money.

While it might seem like Sten is giving away the ‘goods’ for free, this approach has turned out to be quite profitable, as Sten’s firm now has 220 clients and is able to charge planning fees of up to $8,000 per month. While his firm previously relied on investment advisory fees, financial planning is now the firm’s fastest-growing segment.

Ultimately, Sten has found success in being advice-centric rather than investment-centric by clearly demonstrating his value to clients. And as his track record converting prospects into clients demonstrates, giving insights away for free upfront can lead to significant ongoing profits for the firm!

Kitces & Carl Ep 54: Showing Financial Planning Value On An Ongoing Basis After The First 6 Months – In the past, advisors used financial plans as a jumping-off point to sell products to clients that would solve the problems identified in the plan. But in a world where advice is the product (that clients pay for on an annual basis) advisors need to find ways to demonstrate their ongoing value to clients.

In this episode, Michael and Carl discuss how consistency is the most important aspect of demonstrating ongoing value to clients. For instance, some advisors adhere to an outreach and meeting cadence throughout the year to ensure a certain number of in-depth meetings and touchpoints. Others systematize the process even further by sharing checklists of regularly performed tasks and client service calendars to communicate to clients that the advisor is routinely paying attention to their individual situations.

Some advisors use trackers that allow clients to view the financial progress they have made during their relationship with the advisor. These can track net worth, the amount of money the client has saved as a result of the advice they have received, or even a custom ‘score’ that assigns point values to the various pieces of the financial planning process.

The key point is that being consistent is not just about creating a financial plan, but about showing clients that all the different pieces of their financial puzzle are regularly taken care of. But doing so isn’t just a matter of saying that the advisor will be available whenever the client may need them, but instead actually formulating a process that is executed consistently to show clients that the advisor is showing up and ready to serve on an ongoing basis!

Kitces & Carl Ep 67: Setting A Personal Growth Goal When You Don’t Need More Revenue For Success – The financial advice industry has traditionally been geared towards attracting individuals who thrive in a career where their earnings have the potential to increase depending on how hard they work. And while recent Kitces Research on Advisor Wellbeing shows that an advisor’s wellbeing steadily improves as their take-home pay increases, there is an inverse relationship between wellbeing and firm revenue once the revenue passes a certain point (about $1.5 million), suggesting there is a limit to where firm growth can contribute to wellbeing.

In this episode, Michael and Carl first discuss how firm owners can identify the firm's growth point where their personal wellbeing will decline. From there, they explore strategies to mitigate that decline, including identifying the practice’s most profitable clients, ‘transitioning’ the other (less) profitable clients by referring them out to an advisor that can do a better job of serving them, and then trying to replicate those ideal clients that remain behind.

They then discuss how firm owners can then consider what their own ideal life looks like. This could include their own life planning process (e.g., George Kinder’s life planning approach), or setting audacious personal (not business) stretch goals, like training to run a marathon.

Ultimately, the key point is that there are specific steps advisors can take to improve their own wellbeing once they get to a point where they don’t have to work as hard to grow their business – besides just “grow even more!” – and can start reaping some of the rewards for all the hard work they put in, in order to get to that place. And while not all advisors have reached that point (yet), the takeaway remains that simply going through the exercise of thinking about what their goals will be, once they’re making enough in their business that they don’t need to keep growing revenue just for growth’s sake, can help ensure that they are building their business with intent and are focusing on the long-term goals that really mean the most!

Leave a Reply