Executive Summary

As so-called "robo-advisors" continue to grow, offering their services to more and more consumers at a modest 0.15% - 0.35% cost, the question arises whether such services will ultimately be a threat to traditional advisors. Can human advisors survive in a world where robo-advisors commoditize the cost of passive strategic portfolio construction down to almost nothing? What can today's advisors do to fend off the threat?

A closer look at the robo-advisors, though, reveals that many of the tools and strategies they implement are not actually unique, and can be implemented effectively by human advisors as well. For instance, advisors that utilize model portfolios and implement with "intelligent" rebalancing software can already offer most of the continuous-monitoring automated rebalancing and tax loss harvesting offer by robo-advisors today. And human advisors can also go beyond just offering investments, providing a wider array of personal financial planning services, and augmenting the relationship with technology tools from account aggregation and financial dashboards to online collaborative financial planning software and "meeting" with clients via tools like Skype and GoToMeeting that allow them to maintain relationships in a highly efficient manner.

As advisors evolve, the landscape of the future may look less like robo-advisors threatening human advisors directly, and more like robo-advisors commoditizing certain parts of what today's advisors deliver, forcing traditional advisors to adapt and either get far more efficient ("do as they do"), or move up the value chain with financial planning advice and deeper relationships, or all of the above, to continue to keep their costs aligned to the value they actually deliver. While this transition isn't impossible - in fact, it's similar to the one advisors have gone through as they moved away from being paid for stock implementation with the rise of online discount brokerage - advisors who continue to lag in the implementation of technology and/or add little beyond the raw implementation of a passive strategic rebalanced portfolio may find it increasingly difficult to grow and compete at a reasonable price, while those who adopt the tools, technology, and techniques of the robo-advisor themselves - and then build on top of it with financial planning services and technology-augmented relationships - will find themselves best positioned to continue to survive and thrive.

Do As They Do (Systematize And Automate Portfolio Implementation)

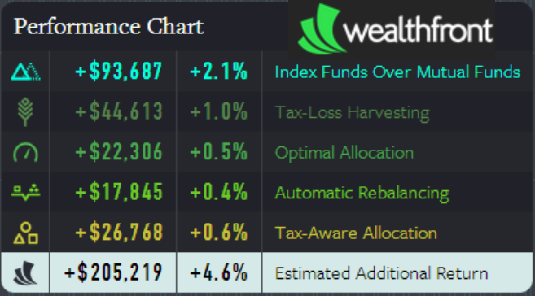

The "true" robo-advisors like Wealthfront, Betterment, and FutureAdvisor offer well-diversified passive strategic portfolios, generally monitored continuously for rebalancing and tax-loss harvesting opportunities, for a mere 15bps - 35bps, in a world where the 'typical' advisor charges nearly 1% on assets under management (AUM).

While this cost structure might imply a very simple, unsophisticated portfolio that has little cost and delivers little value, in practice the efforts to manage investment costs, match optimal asset allocations to goals and risk tolerance, automate rebalancing, and implement various forms of tax-sensitive strategies, quickly adds up to significant potential value. The chart below shows the primary "value-adds" (in percentages, and the additional dollar amount that would be accumulated from a $100,000 starting position over the span of 20 years) that Wealthfront communicates as a part of its marketing.

Yet the reality is that these benefits the robo-advisors offer are not necessarily unique to the robo-advisors; in reality, any advisor can create a systematized investment process that offers a series of model portfolios to clients, and then monitor those portfolios on a continuous basis for using software to take advantage of opportunities. In fact, the key areas in which robo-advisors leverage technology - automatic rebalancing, proactive tax-loss harvesting, and asset-locating investments on a tax-aware basis - have already been available to and implemented by advisors in the form of "intelligent" rebalancing software for a nearly decade now!

Of course, recent industry surveys suggest that the majority of advisors still do not use rebalancing software; nonetheless, the point remains that advisors actually already have the tools necessary to do virtually everything the robo-advisors offer, and can do for their clients just as the robo-advisors do now! Except, of course, that human advisors are not limited to their investment offering, and have the potential to offer far more, as well...

Go Beyond Just Passive Portfolio Construction

As discussed previously on this blog, one of the powerful effects that is occurring as a result of evolving technology and the growth of robo-advisors is the steady commoditization of a well-diversified passive strategic portfolio (and investment management more generally). Simply put, if the sole value propositions you as an advisor provide to clients for a 1% fee are portfolio construction, diversification, and continuous monitoring with appropriate tax-sensitive rebalancing, your business may well be in danger for being overpriced.

Yet in practice, many (though certainly not all) financial advisors have long since been evolving their value proposition beyond "just" the essentials of portfolio construction. The entire growth of comprehensive personal financial planning services represents the clearest example of this trend - with the number of CFP certificants having more-than-doubled in the past 15 years to nearly 70,000 - as advisors seek to differentiate themselves beyond just portfolio construction alone.

Notably, though, most of the "robo-advisors" are still remarkably investment-centric in their offering, and are not necessarily focused at all on the "other" aspects of a client's financial world. That's not necessarily a knock against the robo-advisors, but simply an acknowledgement that passive strategic portfolio construction is conducive to systematic implementation with algorithm-based technology, while good financial planning goes beyond a technology solution and generally requires a more human touch, due both to the complexity of the information and the the social accountability that helps to address the challenge of getting another human being to actually change their behavior.

In other words, simply put, financial planning is the anti-commoditizer, and therefore for the foreseeable future is the anti-robo-advisor value-add as well. And the differentiator is likely to remain in place for a long time to come, because changing financial behavior requires more than just an efficient technology tool to deliver information. After all, if information alone was sufficient, the country's obesity problem would be solved with a website that just explains you need to "eat less and exercise more" - yet just as that clearly is not resolving the issue, neither is it likely that a robo-financial-planner explaining you need to "spend less and invest more (in a diversified and continually monitored portfolio)" will succeed either. While technology tools may be able to better help us understand our position and track our progress, technology is more likely to augment human interaction around changing financial behaviors, rather than replace it, as our brains are just not hard wired to feel accountable to computers the way we do to another human being!

Augment The Relationship With Technology

Notwithstanding the uniquely human aspects of financial planning and behavior change, the reality is that technology can still be highly effective to augment the relationship and enhance communication and collaboration... and advisors have been very slow to adopt technology to augment client relationships.

For instance, just because financial planning may thrive on a human interaction, and even a face-to-face interaction, doesn't mean it needs to be an in person meeting to make the connection. Sometimes, the best and easiest and most efficient way to communicate is by other means, ranging from telephone and email to the rising trend of using video communication (e.g., Skype) and screen-sharing collaboration tools (e.g., GoToMeeting). In the past, advisors have tried to make themselves more efficient by delegating work to their clients ("rather than taking/wasting the time to drive to my clients, I'll make my clients come see me in my office instead!"), but using video technology for communication in particular allows that travel time to be permanently eliminated altogether, making everyone more efficient, while still preserving a real face-to-face visual connection and the essential non-verbal communication that goes along with it. Simply put, just because there's no way to shake hands at the end doesn't change the fact that a video meeting is still a face-to-face meeting!

Similarly, technology provides not only opportunities for better communication, but better collaboration as well. The growing range of online financial dashboards and personal financial managers (albeit with few PFM tools currently available to financial advisors, though this may change soon!), not to mention full-powered financial planning tools that both advisors and their clients can access, create an opportunity to engage clients at a deeper level. While many advisors have been resistant to sharing their technology with clients, the robo-advisors have openly embraced it; in fact, Personal Capital gives away its financial dashbaord for free as a primary means of marketing and finding new clients in the first place, following up with those who use its free software to see if they would like more assistance to achieve their financial goals - and with a greatly expedited advice process, as the client's information is already fully uploaded and integrated into the software (while the typical advisor still struggles to get clients to send in data gathering forms!)!

In other words, technology doesn't have to be an either-or "robots versus humans" scenario, and in practice it may be the technology-augmented humans - the "advisor cyborgs" - that will ultimately be the real winners in the future (with the tools of the robo-advisor powering much of their human advisory business!).

Bottom Line For Advisors To "Compete" With Robo-Advisors

So what's the bottom line to compete with robo-advisors, and/or to avoid having your business (or future growth) undermined by them? There are a few clear steps for evolution, similar to the way that advisors had to adjust as the rise of online discount brokerage eliminated the compensation of being paid to implement stock trades:

- Systematize your investment process. It's not just to actually implement investment strategies on a more consistent basis for clients, but because the reality is that if your investment process isn't systematized and you're not implementing model portfolios consistently, it will be nearly impossible to leverage technology (i.e., rebalancing software) for maximal efficiency.

- Get on board with rebalancing software. Unless you just plan to give up implementing investments for clients altogether (or intend to outsource the investment management altogether), using technology to monitor and manage client portfolios will be key in the future. In today's environment, many advisors justify their different-for-every-client portfolios as being "deeply customized" for each client, but given the impossibility of continuously monitoring such portfolios effectively (not just their allocations, but due diligence on the underlying investments themselves!), the "different investments for every client" approach may soon be nothing more than an indicator that the advisor neglects their portfolios (at least relative to the truly continuous daily monitoring and tax-sensitive management of a robo-advisor)!

- Provide financial planning services that go beyond portfolio-only solutions (especially if you're passive). Building a well-diversified passive strategic portfolio is on its way to being totally commoditized, and as the technology improves and transaction costs decline may even disintermediate most mutual funds and ETFs altogether, which in turn will drastically drive down AUM pricing for pure portfolio construction. As a result, advisors who wish to defend their pricing must either find other value-adds to bring to the table (e.g., including extensive financial planning as a part of their AUM pricing), or add value to the portfolio above-and-beyond mere diversified portfolio construction (e.g., have a more active investment management approach that actually delivers results, as alpha can always justify higher costs... if it can actually be delivered, of course!).

- Utilize technology to augment the client relationship. Don't view technology as a competitor or commoditizer, but as a tool that can drive down the cost to deliver already-commoditized services and help provide them more efficiently to clients, so advisors can focus on areas where they truly add value (and leverage technology in those contexts as a collaborative tool). The investing public is already finding a wide and growing range of technology websites, tools, and apps that help them track and monitor the progress towards their goals; these are tools that advisors can and should embrace to augment their relationship, and make it even more engaging and collaborative.

Ultimately, advisors that are slow to change, and cling too long to solutions that are being commoditized (passive strategic portfolio construction) or fail to adopt technology that makes them more efficient and helps augment their relationship with clients may still find that their current clients continue to retain and stick around. After all, those clients are already accustomed to the service the advisor provides, have a relationship, and it takes a lot for a client to be unhappy enough to actually leave. But those same advisors may find themselves increasingly facing a growth wall, where their costs and efficiency make it impossible to attract new clients, as new clients are slowly attracted to either robo-advisors, or more robot-like "cyborg" advisors instead.

I work as an advisor for a relatively large RIA, and I can tell you that we have been paying close attention to the growth in the “robo-advisor” space. As such, I’ve seen plenty of articles and blogs, and have even attended webinars on the subject of how traditional advisors need to adapt to survive and focus on unique value propositions in order to remain relevant. What I have yet to see, is anyone such as yourself, call out the custodians in our industry for their inability to deliver a similar technology solution that would allow any RIA to compete head-on with a robo-advisor.

Where are the custodian-maintained websites for us to on-board a client completely online without any paper? Sites that allow us to offer a similarly efficient process of managing clients’ investments and the compelling client experience just as the robo-advisors offer?

What the robo-advisors have really demonstrated, is that with significantly less than $100 million in venture capital funding, you can develop and implement efficient, scalable technology that brings the process of investment management to the 21st century.

While it is certainly true that in order for us and our practices to remain vibrant and relevant for years to come we have constantly be asking ourselves how can we provide more value to address our clients’ ever-changing needs, but so too should the custodians and other technology providers in our industry. Hopefully before it is too late.

ibpep…I totally agree with you. I work as an advisor at a small RIA and we use Schwab mainly as our custodian. Schwab has many good features, but their website is lacking in many ways to what these new robo-advisor’s can offer. In addition, I 100% agree with you about on-boarding a client. We still use a paper discovery form in my office, and the process is painfully slow and tedious for us as well as the client. I would love to see some changes in making it easier to get client’s information for financial planning purposes. For example, why not incorporate a mint.com like feature where client’s can link all of their accounts (investing and checking/savings) into a dashboard. This would allow the client expense questions to be dealt with much easier than they are now. Michael, great article, but could you please comment on your thoughts about what custodians can do to help the RIA’s they serve? Thanks!

Michael, Really enjoyed the article. Thanks for the well-constructed outline of how human advisors can evolve alongside us digital advisors.

ibep and Erik, I think Betterment Institutional might help with some of your present custodian pain points. Would be happy to connect with both of you. eli at betterment dot com.

-Eli

COO, Betterment

Since the new of “robo-advisors”, I’m seeing more FAs actually do SWOTs and more are admitting they have competition, something they tell me they don’t have (yes, even local competition). Which to me has been very strange.

Many are looking at their portfolio, operations, admin, customer service, etc. systems (or lack thereof). Some aren’t able to change over now, but they’ve got changes in their radar.

I know of a few who, over the last 12-months, have changed custodians, primarily to better systematize their firms, too.

Good thing, for sure. It allows advisors and planners to do more of the work they enjoy doing and give clients the type of (holistic) services they want.

Michael, Great article! I agree with all of your points. As CEO of Total Rebalance Expert, I have long been an advocate of automated, tax efficient portfolio management. For advisors to stay ahead of the curve, keep and grow their practices, they need to do all that the “robo-advisors” do and add in the personal, unique side.

Coincidentally, this article came out in the FT in the past week. http://www.ft.com/intl/cms/s/0/fc1001e0-f888-11e3-815f-00144feabdc0.html?siteedition=intl#axzz35YEGccP3

Great article Michael. A lot of what you mention here speaks to many of the quantitative aspects of the planning and investment process. I’d like to add as well that what many of the robo advisors offer is not only quantitative, but more importantly qualitative.

Here is an example. While many new and existing clients want an office to go visit, the robo avisors get around this by portraying an image on the web that is both comforting and relevant. The websites are smooth, Web 2.0 enabled, the blog is written in a friendly tone, they have useful features (not a scrolling ticker across the top) and leverage tech as much as they can but only when they have to. But at the end of the day they never loose that “friendly” image. Sure many RIA shops are doing this, but I’d think the majority are still struggling.

There is a big unknown here and it speaks of relevancy and how to relate to clients in non financial terms.

But coming back to the office space, ironically I think its where RIA shops have a significant ace up their sleeves and they don’t even realize it. Small things like a “hip” office, hard wood floors, new technology, casual seminars and a lot of smiles (not in white shirts or ties) could help traditional firms compete with robos. Loose the thick red carpets, dark wood, ships in a bottle and pictures of schooners on the wall and learn how to create an image where clients can more readily relate. One example here that comes to mind is oXYGen Financial out of Atlanta.

Because of the 1% fees and the fact that they already have offices, what I see as an evolving trend would be for clients to split their dollars in a hybrid core-satellite structure where Betterment gets 30% and the local advisor gets 70%. Keep one for the low fees ( Betterment, Learnvest, Wealthfront…etc..etc are far away from launching local offices) and then use the other for the service touch points you mention that 100% require a face to face interaction.

In the long run, the service touch points baked inside local RIA offices could put a serious dent in robo aspirations…..unless the robo firms figure out a way to install satellite centers around the country and bring that same level of comfort from the web to the streets.

Win win for both sides.

A good article and thank you for publishing. It is interesting as we evolve towards an ever greater ‘digital life’ to see a perspective on how ‘robo’ and ‘personal’ can exist. I believe that the personal interaction evolve more as being a facilitator to help the client manage their own investment decisions than providing a direct alternative.