Executive Summary

Borrowing money has a cost, in the form of loan interest, which is paid to the lender for the right and opportunity to use the borrowed funds. As a result, the whole point of saving and investing is to avoid the need to borrow, and instead actually have the money that’s needed to fund future goals.

A unique feature of a 401(k) loan, though, is that unlike other types of borrowing from a lender, the employee literally borrows their own money out of their own account, such that the borrower’s 401(k) loan repayments of principal and interest really do get paid right back to themselves (into their own 401(k) plan). In other words, even though the stated 401(k) loan interest rate might be 5%, the borrower pays the 5% to themselves, for a net cost of zero! Which means as long as someone can afford the cash flows to make the ongoing 401(k) loan payments without defaulting, a 401(k) loan is effectively a form of “interest-free” loan.

In fact, since the borrower really just pays interest to themselves, some investors have even considered taking out a 401(k) loan as a way to increase their investment returns, by “paying 401(k) loan interest to themselves” at 5% instead of just owning a bond fund that might only have a net yield of 2% or 3% in today’s environment.

The caveat, though, is that paying yourself 5% loan interest doesn’t actually generate a 5% return, because the borrower that receives the loan interest is also the one paying the loan interest. Which means paying 401(k) loan interest to yourself is really nothing more than a way to transfer money into your 401(k) plan. Except unlike a traditional 401(k) contribution, it’s not even tax deductible! And as long as the loan is in place, the borrower loses the ability to actually invest and grow the money… which means borrowing from a 401(k) plan to pay yourself interest really just results in losing out on any growth whatsoever!

The end result is that while borrowing from a 401(k) plan may be an appealing option for those who need to borrow – where the effective borrowing cost is not the 401(k) loan interest rate but the “opportunity cost” or growth rate of the money inside the account – it’s still not an effective means to actually increase your returns, even if the 401(k) loan interest rate is higher than the returns of the investment account. Instead, for those who have “loan interest” to pay to themselves, the best strategy is simply to contribute the extra money to the 401(k) plan directly, where it can both be invested, and receive the 401(k) tax deduction (and potential employer matching!) on the contribution itself!

401(k) Loan Rules And Repayment Requirements

Contributions to 401(k) and other employer retirement plans are intended to be used for retirement, and as a result, 401(k) plans often have restrictions against withdrawals until an employee retires (or at least, separates from service). As a result, any withdrawals are taxable (and potentially subject to early withdrawal penalties), and even “just” taking a loan against a retirement account is similarly treated as a taxable event under IRC Section 72(p)(1).

Yet unfortunately, the reality is that from time to time, employees may need to access the funds in their 401(k) plan before retirement, at least temporarily. To help address the need, Congress created IRC Section 72(p)(2), which does permit employees to take loans directly against their 401(k) or other qualified plan balance from the 401(k) plan administrator, subject to certain restrictions.

The first restriction on a 401(k) loan is that the total outstanding loan balance cannot be greater than 50% of the (vested) account balance, up to a maximum cap on the balance of $50,000 (for accounts with a value greater than $100,000). Notably, under IRC Section 72(p)(2)(ii)(II), smaller 401(k) or other qualified plans with an account balance less than $20,000 can borrow up to $10,000 (even if it exceeds the 50% limit), although Department of Labor Regulation 2550.408b-1(f)(2)(i) does not permit more than 50% of the account balance to be used as security for a loan, which means in practice plan participants will still be limited to borrowing no more than 50% of the account balance (unless the plan has other options to provide security collateral for the loan). If the plan allows it, the employee can take multiple 401(k) loans, though the above limits still apply to the total loan balance (i.e., the lesser-of-$50,000-or-50% cap applies to all loans from that 401(k) plan in the aggregate).

Second, the loan must be repaid in a timely manner, which under IRC Section 72(p)(2)(B) is defined as a 401(k) loan repayment period of 5 years. In addition, IRC Section 72(p)(2)(C) requires that any 401(k) loan repayment must be made in amortizing payments (e.g., monthly or quarterly payments of principal and interest) over that 5-year time period; interest-only payments with a “balloon” principal payment is not permitted. If the loan is used to purchase a primary residence, the repayment period may be extended beyond 5 years, at the discretion of the 401(k) plan (and is available as long as the 401(k) loan for down payment is used to acquire a primary residence, regardless of whether it is a first-time homebuyer loan or not). On the other hand, there is no limit (or penalty) against prepaying a 401(k) loan sooner (regardless of its purpose).

Notably, regardless of whether it is a 401(k) home loan or used for other purposes, a 401(k) plan may require that any loan be repaid “immediately” if the employee is terminated or otherwise separates from service (where “immediately” is interpreted by most 401(k) plans to mean the loan must be repaid within 60 days of termination). On the other hand, 401(k) plans do have the option to allow the loan to remain outstanding, and simply continue the original payment plan. However, the plan participant is bound to the terms of the plan, which means if the plan document does specify that the loan must be repaid at termination, then the 5-year repayment period for a 401(k) loan (or longer repayment period for a 401(k) loan for home purchase) only applies as long as the employee continues to work for the employer and remains a participant in the employer retirement plan.

To the extent a 401(k) loan is not repaid in a timely manner – either by failing to make ongoing principal and interest payments, not completing repayment within 5 years, or not repaying the loan after voluntary or involuntary separation from service – a 401(k) loan default is treated as a taxable distribution, for which the 401(k) plan administrator will issue a Form 1099-R. If the employee is not already age 59 ½, the 10% early withdrawal penalty under IRC Section 72(t) will also apply (unless the employee is eligible for some other exception).

Treasury Regulation 1.72(p)-1 requires that the qualified plan charge “commercially reasonable” interest on the 401(k) loan, which in practice most employers have interpreted as simply charging the Prime Rate plus a small spread of 1% to 2%. With the current Prime Rate at 4.25%, this would imply a 401(k) loan rate of 5.25% to 6.25%. And notably, these rates are typically available regardless of the individual’s credit rating (and the 401(k) loan is not reported on his/her credit history), nor is there any underwriting process for the 401(k) loan – since, ultimately, there is no lender at risk, as the employee is simply borrowing his/her own money (and with a maximum loan-to-value ratio of no more than 50% in most cases, given the 401(k) loan borrowing limits).

In fact, technically a 401(k) loan is really more akin to the employee receiving a (non-taxable) advance of their 401(k) account balance, as ultimately the plan administrator simply liquidates and distributes the employee’s own money to them, and the subsequent repayment of principal and interest simply go back to the employee’s account. In other words, the employee’s 401(k) loan repayments are really just making principal and interest payments to themselves (or rather, to their existing 401(k) account), not to a lender (as is the case with a traditional loan, or a “Bank On Yourself” life insurance policy loan). Though as a loan made by the employee to themselves, any “interest” repayments to the 401(k) plan are not deductible as loan interest, either.

On the other hand, since a 401(k) loan is really nothing more than the plan administrator liquidating a portion of the account and sending it to the employee, it means that any portion of a 401(k) plan that has been “loaned” out will not be invested and thus will not generate any return. In addition, to ensure that employees do repay their 401(k) loans in a timely manner, some 401(k) plans do not permit any additional contributions to the 401(k) plan until the loan is repaid – i.e., any available new dollars that are contributed are characterized as loan repayments instead, though notably this means that they would not be eligible for any employer matching contributions. (Other plans do allow contributions eligible for matching, on top of loan repayments, as long as the plan participant contributes enough dollars to cover both.)

In the meantime, it’s also notable that because there is no lender profiting from the loan (by charging and receiving interest), many 401(k) plan administrators do at least charge some processing fees to handle 401(k) plans, which may include an upfront fee for the loan (e.g., $50 - $100), and/or an ongoing annual service fee for the loan (typically $25 - $50/year, if assessed).

Nonetheless, the appeal of the 401(k) loan is that, as long as the loan is in fact repaid in a timely manner, it provides a means for the employee to access at least a portion of the retirement account for a period of time, without having a taxable event (as would occur in the case of a hardship distribution, or trying to take a loan against an IRA), and without any stringent requirements on qualifying for the loan in the first place, beyond completing the brief paperwork and perhaps paying a modest processing fee.

Why Paying 401(k) Loan Interest To Yourself Really Isn’t

Beyond the appeal of the relative ease of getting a 401(k) loan (without loan underwriting or credit score requirements), and what is typically a modest 401(k) loan interest rate of about 5% to 6% (at least in today’s low-yield environment), some conservative investors also periodically raise the question of whether it would be a good idea to take a 401(k) loan just to increase the rate of return in the 401(k) account. In other words, is it more appealing to “earn” a 5% yield by paying yourself 401(k) loan interest, than it is to leave it invested in a bond fund in the 401(k) plan that might only be yielding 2% or 3%?

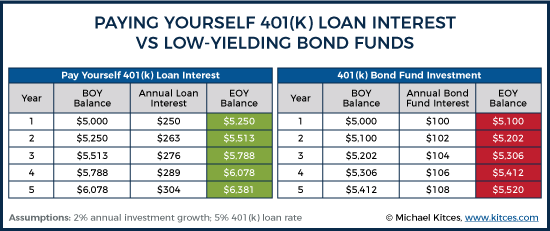

Example 1. John has $5,000 of his 401(k) plan invested into a bond fund that is generating a (net-of-expenses) return of only about 2%/year. As a result, he decides to take out a 401(k) loan for $5,000, so that he can “pay himself back” at a 5% interest rate, which over 5 years could grow his account to $6,381, far better than the $5,520 he’s on track to have in 5 years when earning just 2% from his bond fund.

Yet while it is true that borrowing from the 401(k) plan and paying yourself back with 5% interest will end out growing the value of the 401(k) account by 5%/year, there is a significant caveat: it still costs you the 5% interest you’re paying, since paying yourself back for a 401(k) loan means you’re receiving the loan interest into the 401(k) account from yourself, but also means you’re paying the cost of interest, too.

After all, in the earlier example, at a 2% yield John’s account would have grown by “only” $412 in 5 year, while at a 5% return it grows by $1,381. However, “earning” 2%/year in the bond fund costs John nothing, while “earning” $1,381 with the 401(k) loan costs John… $1,381, which is the amount of interest he has to pay into the account, from his own pocket, to generate that interest.

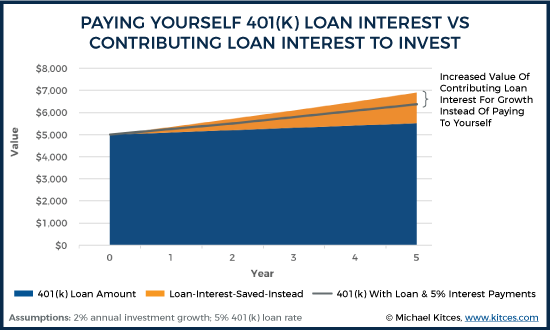

Yet if John had $1,381 available to pay into the 401(k) account as loan interest, he also could have simply saved and invested that money for himself! In other words, John already has the $1,381 – inside of his 401(k) account as loan interest, or outside the account ready and waiting to pay. Except if he didn’t use it for “loan interest” to himself, he could have invested it for a return, too!

Example 2. Continuing the prior example, John decides that instead of taking out the 401(k) loan to “pay himself” 5% interest, he keeps the $5,000 invested in the bond fund yielding 2%, and simply takes the $1,381 of interest payments he would have made, and invests them into a similar fund also yielding 2%. After 5 years of compounding (albeit low) returns, he would finish with $5,520 in the 401(k) plan, and another $1,435 in additional savings (the $1,381 of interest payments, grown at 2%/year over time), for a total of $6,955.

Notably, the end result is that just investing the money that would have been paid in loan interest, rather than actually paying it into a 401(k) account as loan interest, results in total account balances that are $574 higher… which is exactly the amount of additional growth at 2%/year that was being earned on the 401(k) account balance ($520) plus the growth on the available additional “savings” ($54).

In other words, the net result of “paying yourself interest” via a 401(k) loan is not that you get a 5% return, but simply that you end out saving your own money for yourself at a 0% return – because the 5% you “earn” in the 401(k) plan is offset by the 5% of loan interest you “pay” from outside the plan! Yet thanks to the fact that you have a 401(k) loan, you also forfeit any growth that might have been earned along the way! Which means paying 401(k) loan interest to yourself is really just contributing your own money to your own 401(k) account, without any growth at all!

Taxation Of “Contributing” With 401(k) Interest Payments Vs Normal 401(k) Contributions

One additional caveat of using a 401(k) loan to pay yourself interest is that even though it’s “interest” and is being “contributed” into the 401(k) plan, it isn’t deductible as interest, nor is it deductible as a contribution. Even though once inside the plan, it will be taxed again when it is ultimately distributed in the future.

Of course, the reality is that any money that gets invested will ultimately be taxed when it grows. But in the case of 401(k) loan interest paid to yourself, not only will the future growth of those loan payments be taxed, but the loan payments themselves will be taxed in the future as well… even though those dollar amounts would have been principal if simply held outside the 401(k) plan and invested.

Or viewed another way, if the saver actually has the available cash to “contribute” to the 401(k) plan, it would be better to not contribute it in the form of 401(k) loan interest, and instead contribute it as an actual (fully deductible) 401(k) plan contribution instead! Which would allow the individual to save even more, thanks to the tax savings generated by the 401(k) contribution itself.

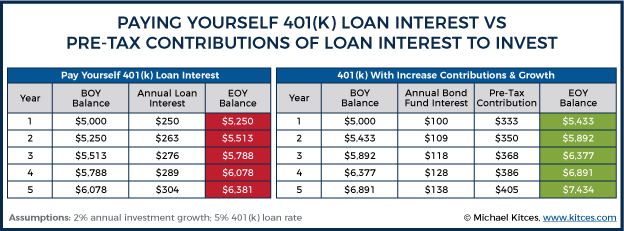

Example 3. Continuing the earlier example, John decides to take what would have been annual 401(k) loan interest, and instead increases his 401(k) contributions by an equivalent amount (grossed up to include his additional tax savings at a 25% tax rate). Thus, for instance, instead of paying in “just” $250 in loan interest to his 401(k) plan (a 5% rate on $5,000), he contributes $333 on a pre-tax basis (equivalent to his $250 of after-tax payments). Repeated over 5 years, John finishes with $7,434 in his 401(k) plan, even though the account was invested at “just” 2%, compared to only $6,381 when he paid himself 5% loan interest!

In other words, not only is it a bad deal to “pay 401(k) interest to yourself” because it’s really just contributing your own money to your own account at a 0% growth rate, but it’s not even the most tax-efficient way to get money into the 401(k) plan in the first place (if you have the dollars available)!

Why A 401(k) Loan Should Still Be For Need, Not Investing

Ultimately, the key point is simply to recognize that “paying yourself interest” through a 401(k) loan is not a way to supplement your 401(k) investment returns. In fact, it eliminates returns altogether by taking the 401(k) funds out of their investment allocation, which even at low yields is better than generating no return at all. And using a 401(k) loan to get the loan interest into the 401(k) plan is far less tax efficient than just contributing to the account in the first place.

Of course, if someone really does need to borrow money in the first place as a loan, there is something to be said for borrowing it from yourself, rather than paying loan interest to a bank. The bad news is that the funds won’t be invested during the interim, but foregone growth may still be cheaper than alternative borrowing costs (e.g., from a credit card).

In fact, given that the true cost of a 401(k) loan is the foregone growth on the account – and not the 401(k) loan interest rate, which is really just a transfer into the account of money the borrower already had, and not a cost of the loan – the best way to evaluate a potential 401(k) loan is to compare not the 401(k) loan interest rate to available alternatives, but the 401(k) account’s growth rate to available borrowing alternatives.

Example 4. Sheila needs to borrow $1,500 to replace a broken water heater, and is trying to decide whether to draw on her home equity line of credit at a 6% rate, or borrowing a portion of her 401(k) plan that has a 5% borrowing rate. Sheila’s 401(k) plan is invested in a conservative growth portfolio that is allocated 40% to equities and 60% to bonds. Given that the interest on her home equity line of credit is deductible, which means the after-tax borrowing cost is just 4.5% (assuming a 25% tax bracket), Sheila is planning to use it to borrow, as the loan interest rate is cheaper than the 5% she’d have to pay on her 401(k) loan.

However, as noted earlier, the reality is that Sheila’s borrowing cost from the 401(k) plan is not really the 5% loan interest rate – which she just pays to herself – but the fact that her funds won’t be invested while she has borrowed. Yet if Sheila borrows from the bond allocation of her 401(k) plan, which is currently yielding just 2%, then her effective borrowing rate is just the “opportunity cost” of not earning 2% in her bond fund, which is even cheaper than the home equity line of credit. Accordingly, Sheila decides to borrow from her 401(k) plan, not to pay herself interest, but simply because the foregone growth is the lowest cost of borrowing for her (at least for the lowest-yielding investment in the account).

Notably, when a loan occurs from a 401(k) plan that owns multiple investments, the loan is typically drawn pro-rata from the available funds, which means in the above example, Sheila might have to subsequently reallocate her portfolio to ensure she continues to hold the same amount in equities (such that all of her loan comes from the bond allocation). In addition, Sheila should be certain that she’s already maximized her match for the year – or that she’ll be able to repay the loan in time to subsequently contribute and get the rest of her match – as failing to obtain a 50% or 100% 401(k) match is the equivalent of “giving up” a 50% or 100% instantaneous return… which would make the 401(k) loan drastically more expensive than just a home equity line of credit (or even a high-interest-rate credit card!).

Nonetheless, the fundamental point remains: despite the classic view that 401(k) loan interest is a cost where you are simply “paying yourself”, the reality is that it’s not a direct cost at all, nor a prospective return. Instead, the true cost of a 401(k) loan is the opportunity cost of not having funds invested to grow (including the risk of losing out on 401(k) matching as well, if applicable), which can actually be an appealing cost relative to other borrowing alternatives for those who need a loan (especially those with credit scores in the 600s or below, who may not have any good borrowing alternatives!). Nonetheless, “paying 401(k) loan interest to yourself” will never be superior to just investing the money and generating any return at all!

So what do you think? Is a 401(k) loan really more akin to an employee receiving a (non-taxable) advance of their 401(k) balance? Do your clients seem interested in 401(k) loans? In what circumstances does it make sense to utilize a 401(k) loan? Please share your thoughts in the comments below!