Executive Summary

One of the greatest strengths of providing ongoing financial planning and investment management for an AUM fee is also the model’s greatest challenges: because the revenue is recurring, and industry retention is so high, as long as advisors can survive long enough, they can eventually accrue enough clients to build a sizable business. Thus, one of the greatest predictors of an advisor’s income, and the size of his/her business, is simply the number of years the advisor has been in practice.

However, the fact that advisory firms steadily accrue (and rarely lose) any clients means that eventually, the growth of the business will necessitate hiring. And then more hiring. And at some point, there are so many clients, and so many employees serving them, that the advisor ends up spending more and more time doing tasks in the business that aren’t enjoyable, and less and less time working with the clients he/she once enjoyed.

In a new book entitled “The Pursuit of Absolute Engagement”, industry consultant Julie Littlechild studies how financial advisors and their firms can unwittingly veer off course, and what it takes for the advisor to become re-engaged in the business again. Because the reality is that failing to do so can eventually lead to a point of burnout, where the advisor loses control of the business – and instead it feels like the business controls you!

Ultimately, the path to finding meaningful engagement with the business again is all about (re-)creating its future with a specific intent – to identify the kind of clients that you enjoy working with, the kind of work you enjoy doing for them, and the role in the business that is the most personally engaging and fulfilling for you. For most advisors, the idea of finding a focus – to the exclusion of clients and tasks that don’t fit the mold – is terrifying, both for the change it entails, and the risk to the business. But as Littlechild points out, the truth is that for many advisors, the best path forward for future growth is all about focusing in on the right clients, the right work, and the right role, that helps the advisor find “Absolute Engagement” – because when you’re truly engaged in the business, your newfound energy is likely to do more to propel the business forward than any other business strategy could have accomplished anyway!

How The AUM Model Leads To Business Burnout

One of the greatest virtues of the AUM model is that it’s a recurring revenue business model. While it’s still challenging to get clients, those who do become clients tend to remain clients, paying ongoing fees for ongoing services. And because advisors are well incentivized to service their clients, and it’s so much work for the client to change advisors, most clients stick around for a long time, with industry retention rates averaging close to 90% by some measures, and the largest RIAs enjoying annual retention rates as high as 97% according to the latest Investment News RIA benchmarking survey. The end result of these high retention rates is that most advisors can make a substantial income and grow a sizable business, if they can just “survive” long enough to accumulate a sufficient number of clients in the first place (and navigate the “income gap” during the early years until revenue grows enough to provide a reasonable take-home pay).

In fact, with industry retention rates so high, advisors who can gain enough clients in the early years to keep going and continue attracting clients will inevitably hit a wall, where they reach the sheer maximum number of clients that any advisor has the capacity to handle. At that point, it becomes necessary to hire a paraplanner and administrative staff to help. Yet soon, another wall is reached, where the advisor has to actually train up the paraplanner to become an associate advisor and begin to take over and manage some client relationships. As the associate advisor takes over some client relationships, the advisor can add more clients and continue to grow the business further, but that ultimately necessitates the hiring of even more staff to help support both advisors. “Suddenly”, the advisory firm has 3, 5, or even 7+ employees, and the advisor spends as much or more time managing employees than actually working with clients!

The end result is that as advisory firms “accumulate” clients over time, and the staff and infrastructure grow to accommodate, the founding advisor’s role can shift substantially – in ways that are not always healthy. Days are spent engaged in tasks that are necessary for the business, and may continue to grow its value, but are no longer personally fulfilling. Yet there’s no option to do otherwise because, at this point, all the work and growth is “necessary” to sustain the business, the standard of living for the advisor and his/her family, and the expectations of all those clients and employees. Which means, as the advisor, you’re no longer in control of your time nor really even running the business anymore. Instead, the business is running you. And unfortunately, if nothing is done, there’s a high risk that this path eventually leads to burnout.

So what’s to be done? In her new book, “The Pursuit of Absolute Engagement”, Julie Littlechild suggests that the key is taking an intentional pause to reflect on the business, and your role, and to begin proactively setting a new vision for your future. Because whether you got here as a result of incremental shifts of the business that over time have taken you further and further from where you wanted to be, or because you didn’t have a particular vision and were just rolling along with the growth (but now finding yourself where you don’t want to be), or simply because you’ve had a change of heart about your role in the business and feel the need for something new… nothing changes until you take the time to reflect and figure out, from here, what kind of business you really want to create in order to (once again) give you the feeling of being truly engaged in the business.

So what’s to be done? In her new book, “The Pursuit of Absolute Engagement”, Julie Littlechild suggests that the key is taking an intentional pause to reflect on the business, and your role, and to begin proactively setting a new vision for your future. Because whether you got here as a result of incremental shifts of the business that over time have taken you further and further from where you wanted to be, or because you didn’t have a particular vision and were just rolling along with the growth (but now finding yourself where you don’t want to be), or simply because you’ve had a change of heart about your role in the business and feel the need for something new… nothing changes until you take the time to reflect and figure out, from here, what kind of business you really want to create in order to (once again) give you the feeling of being truly engaged in the business.

Finding Absolute Engagement As A Financial Advisor

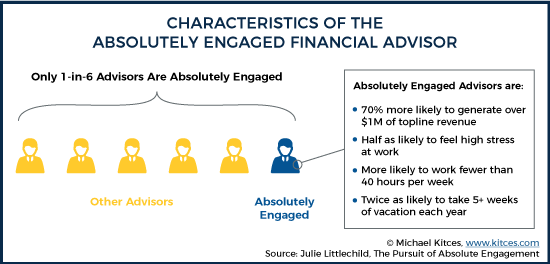

In a study of more than 600 financial advisors, Littlechild has found that about 1-in-6 are “Absolutely Engaged” in their advisory firms. The significance of being Absolutely Engaged is that those advisors were more likely to focus their time on the activities that propel the business forward, and, as a result, were 70% more likely to be generating over $1M of topline revenue. Notwithstanding this growth, though, they were also half as likely to feel high stress at work, twice as likely to report excellent health, and 50% more likely to wake up feeling energized in the morning. Furthermore, they were more likely to work fewer than 40 hours per week, and twice as likely to take off five-or-more weeks of vacation each year, notwithstanding their sizable revenue/income.

As Littlechild puts it, what makes Absolutely Engaged advisors unique is their effectiveness and success in aligning a vision for themselves and their personal lives alongside a vision for the business itself. In particular, Absolutely Engaged advisors have a clear focus on the clients they wish to serve, the work (i.e., services) they wish to provide for those particular clients, and the role they personally want to fulfill in the business. As distinguished from the typical advisor, where the clients are often “whoever is willing to do business” (and meet our minimums), the service is “whatever the clients want/need”, and the founder-advisor’s role is “whatever the business needs me to do.” Because, as noted earlier, that’s simply the reality of how much advisory businesses evolve in the early years.

So how can an advisor re-focus and get “back on track”? As the “Absolute Engagement” name implies, Littlechild suggests the starting point is to pause and reflect on what it is that personally engages you. Who are your ideal clients – the ones who aren’t just profitable to the firm, but who are also mentally stimulating and engaging for you, that you most enjoy working with? What kinds of services do you need to offer to those particular clients to attract more of them to the business, where the work is genuinely engaging for you? And what role can you play in the business where, when you’re fully engaged, adds the greatest value to the business?

From there, it’s feasible to try and figure out what needs to change today, in order to move towards that vision of the ideal (and fully engaged) future. Notably, the point is not necessarily to “ditch” the business and go an entirely new direction in life; in many cases, it’s just a matter of starting to shape the clients, the services, and your role with more deliberate intent, making incremental changes that over time will move you to a point of greater engagement. That might include plans to let go of “bad fit” clients as more ideal ones join. Or a next hire that allows you to begin letting go of certain tasks and shifting your role. Or simply focusing in further on what activities you both love to do and really need to do, and figuring out how to delegate everything else (that either isn’t engaging for you, or isn’t really necessary for you to be doing in the first place).

Absolutely Engagement Matters For Client, Too!

Notably, Littlechild’s research finds that striving for absolute engagement isn’t just relevant for the advisor to feel more fulfilled. It’s relevant for clients, too.

Because, as Littlechild’s research also shows, client engagement is a key metric for making the advisor more referrable, as well. In the past, the prevailing view amongst advisors was that as long as clients received good service, they would be loyal and retain, and eventually and inevitably begin to refer. Yet the reality is that the mere fact a client hasn’t left doesn’t necessarily mean they’re satisfied. And mere “satisfaction” alone isn’t enough to drive a referral anyways these days, as there’s a large gap between simply being content with the advisor, and acting as his/her advocate or raving fan. Which means the mere fact that a firm has good client retention and favorable client satisfaction surveys doesn’t mean it’s going to see many referrals anytime soon.

Instead, what really defines the client who is not only loyal, but an active referrer, is engagement. Yet going beyond just “good service” to meaningfully engaging clients requires crafting a client experience that is truly engaging for them. For instance, an advisor who works with professional football players might not just “do their financial plan”, but work with their agents, provide financial education to their family, and help them figure out what path to pursue after their sports career is over. More generally, the question is what you’ll do at every step of the client’s journey with the firm, from the first introduction and meeting to the onboarding and planning process to the future meetings and reviews, to craft a more meaningful experience to the client.

In addition, Littlechild points out that truly engaging clients requires actually making them part of the process – an approach that was dubbed “co-creating the value” by researcher C.K. Prahalad and Venkat Ramaswamy. In essence, the question is not “what can be delivered to clients”, but instead is “what can be created with clients”. For instance, is financial planning software something you use to analyze a client’s situation in your office and deliver a plan to them, or is it something you use with the client in the conference room to create the plan together? More generally, the point is simply to recognize that delivering “a plan” or “a portfolio recommendation” to a client doesn’t engage them; to be engaged, they literally need to be engaged as part of the process in a more collaborative manner.

Again, though, the starting point for all of this is for the advisor to decide exactly who their target clientele is that they want to serve, and what exactly it is the advisor can deliver to the client. Not only in order to make it more fulfilling and engaging for the advisor, but also because the reality is that if the advisor doesn’t select a focused type of clientele to serve, it will be virtually impossible to craft a consistently high quality and engaging client experience when every client is different.

Of course, the reality is that engaging in this kind of soul-searching about your advisory business and the clients you serve, is not easy. As Littlechild herself points out in the book, there will be many blocking points. You may get stuck focusing on what everyone else thinks you “should” do, given responsibilities to family or employees. It may be hard to commit to making a change, because change implies that your efforts in recent years may have been “mistaken” and going in the wrong direction. Change is hard, and staying in your comfort zone – even if it’s not a very fulfilling or engaging one – will likely feel easier.

Fortunately, for those who are hoping to get unstuck, the good news is that Littlechild’s book provides not only inspirational reading, but also some very hands-on tools and workbook materials to help navigate the path. Including not only the questions to ask yourself to really think through your ideal vision for clients, work, and your role in the business, but also how to start evolving your business focus and client experience, and even why it’s so important to form or join a Mastermind group (because having people to help hold you accountable to making the change is crucial for seeing it through!).

But the bottom line is simply to remember that in a helping profession like financial planning, you are more important than anyone else. Because if you’re not happy and engaged in your practice, and don’t take care of yourself, you won’t be of much help (for long) to your clients, either. Which is perhaps why Littlechild’s book is so unique – because it makes the point that finding a niche clientele to focus on isn’t about finding the most profitable (niche) clients; it’s about finding the ones that are most engaging for you (and that you can be engaging for), recognizing that the energy you’ll get from enjoying your business again will be more likely to grow profits in the long run than any other business strategy anyway.

And so for any advisors who are feeling “stuck” in the business, and that it’s no longer fun and engaging the way it used to be, I strongly urge you to get a copy of Julie Littlechild’s “The Pursuit of Absolute Engagement: Intentionally Design A Business That Supports The Life You (Really) Want To Live”, and see if it can help you get re-engaged with your business once again!

And so for any advisors who are feeling “stuck” in the business, and that it’s no longer fun and engaging the way it used to be, I strongly urge you to get a copy of Julie Littlechild’s “The Pursuit of Absolute Engagement: Intentionally Design A Business That Supports The Life You (Really) Want To Live”, and see if it can help you get re-engaged with your business once again!

So what do you think? Do you find “engagement” to be a meaningful way to think about your happiness with and involvement in the business? Do you feel like you’re trapped in an advisory business you built but no longer enjoy? Please share your thoughts in the comments below!

I don’t disagree with the numbers of business growth for the fee only advisor. But, it seems contrary to a lot of what the government is claiming in the DOL efforts. The idea that “commissions are evil” and how Americans are paying “$17 billion too much each year for financial advice”.

I’m sure some of that is closet index funds charging 1.3% instead of a fraction of that. But, much of the war against commissions seems to be around the idea that it’s too costly.

The graphs above show that a commission based model (or at least one done right) could be less costly for clients — perhaps the underlying fund costs aren’t considered there, and that’s a large part of where the oft-quoted “$17 billion” number is coming from.

The fallacy in the DOL thinking is assuming that there is one right way and that it applies to everybody. The truth is what is best for any individual depends on that individual’s needs … and these needs can be quite different from one person to the next. “One size fits all” is not a prudent way to deal with finances.

The DOL fiduciary ruling has two major problems with it:

1) Requiring a “financial institution” to sign off on fixed indexed annuity sales with fiduciary liability when the independent life and annuity channel doesn’t work that way (and assuming that insurance companies want to remain “product manufacturers”.

2) By elevating the standard of care (from suitability to fiduciary), the lawsuits against such sales would escalate because of the term ‘fiduciary’ being used. I’d rather see it called a ‘professional’ standard, where “not unsuitable” is no longer the minimum acceptable standard.

I’m not afraid of this ruling as I use a disciplined and documented process and I have never cared about any kind of incentive programs, trips, etc. The ruling made sense… in theory. It’s the practical application of it is where I disagree.

Fantastic article! You’ve essentially answered the questions I sent you regarding insurance-only agents (life insurance and annuities) considering adding a Series 65 and joining or forming an RIA should be looking into to ensure that they are complying with the letter and the spirit of the laws governing the Investment Advisers Act of 1940.

I have posted excerpts of your post with full links to the Insurance-Forums discussion forum so other insurance agents (who are often courted to becoming affiliated with an RIA) can also benefit and look into Series 65 licensing “with eyes wide open”.

As a fee only financial planner who went through this transition several years ago (although only 5% of my business was transaction related . . . so the migration for easier for me than others), a few thoughts:

* The culture of a fiduciary firm has less to do with the compensation and more to do with ethics and living/breathing doing what is best for clients. The fiduciary relationship a firm has with its clients isn’t in the same ballgame as a transaction based relationship. Not the same ballgame. Not in the same ballpark. Not even being played in the same city.

* The notion of reverse churning is and will be a dominant theme in the years to come. I see deep problems in the cultures of other firms where no ongoing work is being done to justify the fee being charged is a breach of your duty to your clients. (The lack of ongoing documentation and due diligence on third party money managers will be the low hanging fruit picked first by regulators and attorneys).

* The transition of clients from commission to fee relationships will also be fertile ground for regulators. Document justifications. Embrace doing what is best for your clients.

* I must admit that the clarity of purpose being the owner of an RIA has dramatically simplified my relationships with my clients, employees and community. My company is no longer muddled as the former BD/Insurance Sales company and has a clear mission in the minds of all of our constituents. (Another disclosure – I was a terrible product salesman, but a perfectly adequate client advocate).

So why “take on and off your fiduciary hat” when you don’t need to, your clients don’t want you to and you couldn’t be all things to all people anyway?

That chart up there which shows the dramatically higher revenue generated with the fee model is EXACTLY why I have not transitioned to it. I make a great living, and the floor of my annual compensation is the .25% trail fee. A $1 million account pays me $2500 in gross revenue x 90%, which equates to $250 per hour for nine hours per year. That is ample for getting the job done right for the client. I could not look someone in the eye and tell them that they were going to pay me $10,000 PER YEAR to look after them and help them reach their goals. Looking back at that same chart, how many billions have been moved from ‘A’ shares to a fee model that quadrupled (or more) the investment professional’s income and doubled or tripled the client’s annual expenses. Reverse churning is RAMPANT, and the fact that the process is presented as being in the client’s best interest makes my blood boil.

Paul,

To each their own on their advisory fee. There’s no requirement to charge 1%, it’s simply an example. Some charge less, some charge more. If you prefer to build an advisory model at 0.25% instead, that’s still your prerogative?

That aside, as I’ve noted previously on this blog, expect a LOT of regulatory scrutiny in the future as advisors make this shift, if they don’t really provide ongoing services and value to substantiate that their fees aren’t just reverse churning… see https://www.kitces.com/blog/reverse-churning-in-advisory-accounts-problems-for-fiduciary-advisors/

– Michael

Michael,

I’d love to see you write a blog on why this approach is also good for the investor. Your chart shows the increased cost of advice under the annual fee model, and commenters have naturally seized on that to suggest that fee-only advice is more expensive. But the cost of advice is only part of the equation, as you well know. When you include the cost of products sold to implement the advice, how do the two models stack up for the investor? How should investors measure whether the advice is a good value for them?

Thanks Barbara. I’d agree it’s perplexing. I understand more conflicts of interest may arise in a pure commission model if one product offers a richer payout (but it’s less effective or advantageous for the investor). At the same time, we have politicians making regular comments about citizens paying too much for investment advice. And many of the DOL rules to change things have focused on eliminating the commission based model. Many firms are giving it up or generating large amounts of paperwork to enable it for select clients that request it for specific circumstances.

I believe there’s probably a balance when it comes to the client getting good advice, no conflicts in investment recommendations and the advisor being able to maintain a business that allows him to provide those services. Hopefully politicians will agree to allow us to continue working and not demonize us more in our efforts to provide the services we do give.

For the record, the rule does not focus on eliminating the commission based model, although that can sometimes be difficult to discern as a result of the rhetoric. As you probably know, ERISA prohibits advisers from having a financial stake in their investment recommendations. The rule permits it, under conditions designed to ensure that conflicts don’t adversely affect the advice given. It is the extent and scope of the conflicts built into the commission model — not the commissions but the differential compensation — that make that so challenging. In my view, that’s a fault with the business model, not the rule. The good news is that products are being brought to market that would ease those challenges, if industry doesn’t succeed in killing the rule first. If those developments, like clean shares and new more investor-friendly annuities, are allowed to take their course, commission accounts really do become a far more attractive option for many, many investors who do not need ongoing portfolio management or comprehensive financial planning. Absent a best interest standard, though, and with no mitigation of conflicts, the commission based model remains a very risky proposition for investors who aren’t equipped to discern whether their financial advisor’s recommendations are beneficial or toxic.

Barbara,

The key distinction here is that it’s not just a different pricing model. It’s a different SERVICE model as well. Thus statements in the article like “Which means adding enough value to charge an advisory fee is increasingly about doing more than just creating a diversified asset-allocated portfolio and monitoring it, because that service is becoming commoditized. Instead, advisory firms are now faced with providing more and more personal financial planning advice, to help bolster their value proposition and justify their advisory fees.”

From the consumer perspective, the fundamental benefit here is a realignment of interests. The challenge of a 7% commission vs a 1% advisory for 7 years is that while the compensation may be the same, the commission advisor has no incentive to provide any ongoing services or value after the moment of sale (and the 7% commission is vested). The 1% advisor has to do work, EVERY YEAR, to justify their value, EVERY YEAR. If the 1% advisor stops delivering value in year 4, they get fired in year 4, and the client only ever pays 4%. With the commission scenario, if the advisor stops delivering value on DAY 2, the client is still locked into that already-paid cost for the next 6.99 years.

Clearly, a subset of consumers may not WANT to pay for those ongoing services. And they have the prerogative not to. That’s why self-directed options, call-center or branch-sales-rep-supported options, etc., are available as well. But the benefit of the alternative arrangement, and the adjustment of the fee structure, is that selling a 7% commission means just convincing the client once, ever, to sign a piece of paper to do the transaction. Selling 7 years of 1% AUM fees means seven years of providing value, one year at a time, because the firm that stops providing value gets fired and loses their income stream. Which means there’s FAR more natural marketplace pressure for advisors to always be delivering value, each and every year, indefinitely. (And lest we forget, it also reduces the incentive to re-up commissions with product churn, which is a whole other conversation.)

– Michael

This is very true, and certainly not limited to financial advisors. Plumbers, florists and landscapers who do good work and build a client base all run into this issue too. Often you find yourself engaged in the day-to-day logistics instead of doing the hands-on work you love to do.

Littlechild is correct in that the business owner needs to set the vision, steer the ship, and remain fully engaged. However, freeing up the time to think and work at this higher level requires a more mechanical shift as well – systems and tools need to be put in place.

This shift is addressed beautifully in two very well-known books that I’d highly recommend to any business owner, especially those who find themselves at a point where “the business is running you”.

The E-Myth (especially for Financial Advisors!)

https://www.amazon.com/Myth-Financial-Advisor-Expert/dp/0983500150

@emyth

and…

Work The System

https://www.amazon.com/Work-System-Mechanics-Working-Revised/dp/160832253X

@workthesystem