Executive Summary

Traditionally, most financial advisory firms’ business models have been centered around managing their clients’ investment portfolios. Even for firms that offer comprehensive financial planning, investment management is often an important – and, for firms that charge fees on an AUM basis, required – part of the firm’s services. However, there is a segment of potential clients who are not interested in delegating their investment management responsibilities to an advisor, but who are seeking professional guidance on actions that they can take and implement on their own – providing an opportunity for advisors to build a sustainable business offering “Advice-Only” financial planning, without the investment management.

In this guest post, Cody Garrett, CFP – founder of Measure Twice Financial, an Advice-Only financial planning firm – writes about what it means to provide Advice-Only financial planning, the types of clients who engage with his services, how Advice-Only advisors get paid, and how to make it a sustainable business model. Additionally, Cody provides a template for a comprehensive Advice-Only financial planning process that he developed in the course of building his own practice.

Advice-Only financial planning generally serves clients who are comfortable performing investment management tasks on their own, but who have questions about their own situations and strategies that require more personalized advice than YouTube videos or personal finance websites can provide. With most advisory firms still requiring clients to give up control over their investments just to get ‘in the door’, advisors who provide personalized financial planning – while allowing the client to manage their own assets – are highly sought out by these “Do-It-Yourself” (but not “Learn-It-Yourself”) investors.

For advisors who offer Advice-Only planning, the sustainability of the model ultimately depends on how many clients the advisor can (or wants to) serve, and how much revenue from each client they can realize. But because their fees are tied to their advice rather than asset management, Advice-Only advisors can charge a level of fees that reflect the value of the advice that they give – meaning that, for advisors who can provide high-value financial advice to clients with complex needs (and charge fees commensurate with that value) the Advice-Only model can be not just sustainable, but can also give the advisor the flexibility to control both their schedule (since it is not dictated by the schedule tethered to the working hours of the financial markets) and their own income (which does not need to depend on their clients’ asset levels).

Ultimately, for advisors who are passionate about giving comprehensive financial advice – but less so about managing assets – Advice-Only planning is a way to serve clients whose needs align with the advisor’s own expertise and ability to provide value. And because so (relatively) few firms currently offer Advice-Only planning, the firms that do provide it can take advantage of the growing demand for Advice-Only planning to differentiate themselves from traditional AUM-based firms and build a sustainable, flexible advice-based practice!

What Is An Advice-Only Financial Planner?

Advice-Only financial planning is a fee-only model that serves (typically Do-It-Yourself, or DIY) investors without the expectation, obligation, or even the option to manage their investments. Unlike traditional advisory models that serve clients seeking to delegate the management of their assets, advice-only financial planning prioritizes the advice itself over (delegated) implementation, along with education to help clients and their families gain the understanding necessary to implement their own (now-well-informed) decisions.

While the financial planning industry generally assumes that DIY investors are uninterested in working with advisors – because by definition, they ‘do it’ and implement themselves, not by delegating to an advisor – this is not necessarily the case. The reality is that not all DIY investors are actually ‘learn-it-yourself’ investors as well, because many of them do seek out professional guidance to learn about personal finance and receive advice on the decisions they’re considering (rather than look up and try to figure out the information on their own). In my own practice as an advice-only financial advisor, I serve families who often say, “I don't know what I don't know,” and they value one-on-one financial guidance without strings attached: no products, no commissions, and no managed accounts.

The gap for DIY investors seeking out professional advisors exists because, on their own, DIY investors often can only find sources of financial education from personal finance websites that push dogmatic, one-size-fits-all advice to a wide net of consumers: “Never Do That”, “Always Do This”, or offering “The Top 10 Things You Should Know”. The issue with many of these (often clickbait-loaded) sites is that the personal side of personal finance is often left out, with many of these sources failing to offer anything but very basic information and common denominator solutions.

In fact, many of these sites serve simply as a hearth for financial product advertisement and frequently cross the line between education and dictation, telling readers what to do and buy rather than providing objective insights and encouraging financial self-analysis. Which is not helpful for DIY investors seeking substantive resources that go beyond the noise and the basics often found on such personal finance websites and are instead seeking solutions that help them ask better questions of themselves.

Nerd Note:

While there are oceans of financial misinformation on the internet that can potentially mislead DIY investors, some helpful resources do exist for individuals and their families at every stage of financial wellness. For example, the ChooseFI podcast has educated and encouraged listeners (including myself) to be intentional about aligning money with personal values. But finding the ‘reputable’ DIY content, and differentiating it from advertising content, still takes time and energy that not all DIY investors have – because, again, the fact that they have the time and inclination to DO it themselves doesn’t mean they have the time and inclination to find the optimal educational content to LEARN it themselves.

Who Engages With The Advice-Only Model?

Often overwhelmed by conflicting financial media and understanding that Google is not the best source of information explaining how to create a personalized financial plan, some DIY investors are eager to consult an expert for a second opinion because they do want a comprehensive plan that focuses on their unique objectives.

The key distinction is that DIY investors are comfortable implementing – i.e., managing their own investments at the custodians of their choice – and they do not want to pay for ongoing implementation and monitoring. With the race to zero fees, low-cost mutual funds and ETFs, and automated portfolio rebalancing, DIY investors often view investment management as the least valuable piece of the puzzle. This makes it especially challenging when the overwhelming majority of financial advisors are building their businesses around the Assets Under Management (AUM) model, where delegating the portfolio is a requirement to work with the advisor, which DIY investors reject. But the fact that such investors are anti-AUM does not mean they are anti-advisor; instead, they simply seek out a non-AUM, advice-only advisor!

Earlier in 2021, I received a phone call from a frustrated prospective client. He had interviewed over ten fee-only financial planners, and none would provide financial planning services without an expectation (and ultimately, an obligation) to also manage his money. However, he wanted to work with a CFP professional who would give him personalized education so that he could make his own important financial decisions. He was not ready to give up control of his investments just to get the (non-investment) advice he was seeking.

There are dozens of similar stories from DIY families seeking financial planning advice without investment management services. Many of them have questions such as, "Does it make sense to start Roth conversions, and how much should I convert?”, “How do I distribute retirement income before age 59 ½?”, and “What are my blind spots?”

Given the apparent lack of advice-only financial planning services offered without an obligation to manage client assets, I launched my own practice to meet this need. Within five months of my firm’s registration, over 70 DIY investors had submitted inquiries to request an advice-only planning engagement.

The demand for advice-only outpaces the supply and will continue to grow, especially as DIY investors become aware of a model that aligns with their expectations for personalized education, retained investment control, and fee transparency. DIY investors are known for their ability to do research, and finding an advice-only advisor is no exception. Accordingly, the key to serving DIY investors is to be easily findable.

How Do Advice-Only Financial Advisors Get Paid?

Good financial advice is not one-size-fits-all; similarly, the way advice-only advisors charge their clients can and does take multiple variables into account. The common factor to the advice-only model, though, is that it is entirely a fee-for-service model that requires payment for the advice itself and not for its subsequent implementation (i.e., no commissions and no AUM fees, ‘just’ the fees for the advice).

The following questions, in this order, address the key factors that can influence how an advisor can select an appropriate advice-only billing system:

- Who do you serve?

- How will you provide value?

- What is the most appropriate way for the clients you serve to pay for the value you provide?

Advice-Only Compensation Models

While there can be any number of answers to the first two questions identifying an advisor’s clients and services (depending on the advisor’s particular niche or specialized focus), the three most common answers to the last question that address compensation include fee-only options suitable for advice-only services. These consist of hourly, ongoing retainer, and project-based fee models.

Hourly planning fees can align well with a client’s need for limited-scope financial guidance, pay-as-can-afford pricing, and periodic check-ins. The advisor charges for actual hours spent, including time in client meetings, document review and preparation, and plan development. The hourly rate and scope of the engagement are mutually defined to provide fee transparency, and the advisor tracks when the clock is ticking. Kitces Research shows that the median hourly rate for financial advisors is $250/hour and typically ranges from $150 to $350/hour.

Ongoing retainers are appropriate for clients who seek not just education but ongoing accountability from a trusted guide, who supports them as they implement tasks throughout the year. Ongoing planning makes numerous financial topic areas more manageable, often supported by a monthly or quarterly service calendar that provides modular planning along the way. This fee structure aligns with DIY investors who seek ongoing financial coaching alongside investment advice. In practice, Kitces Research shows that advisors using a retainer model charge a median fee of $4,000/year, with a typical range as low as $1,200/year and as high as $8,000/year.

Project-based billing is useful for engagements that involve the creation of a one-time plan that may span several weeks or months (which makes it less practical for straight by-the-hour billing), but are still limited in duration, such as a flat-fee review that equips clients with the knowledge to implement decisions without ongoing monitoring. This is a good fit for clients who are just looking for a second opinion, but who want to go through a full planning process and not just ask questions by the hour (hence why I named my own practice “Measure Twice”). Kitces Research shows that the median standalone financial plan fee is $2,500 but typically ranges from $1,000 to almost $5,000 per engagement (and may be even higher for extended planning engagements).

Since advice-only planning does not involve investment management, and the value of a financial planning relationship is not correlated to investment returns (which in turn generate performance that is largely out of the advisor’s control), the planning fee is usually unrelated to a client’s level of investable assets. Instead, in practice, planning fees are more commonly related to the client’s overall net worth or household income – as those are the sources from which the client will pay the fee, which must still feel ‘affordable’ to the client given what they have.

Though given that those with higher incomes and/or higher net worth often have greater complexity, there is still a potential for a ‘healthy’ level of fees for each engagement. (For instance, our typical engagement is a $6,400 project-based fee for a 3-month planning process.)

Sustainability Of Advice-Only Financial Planning Models

The profitability and sustainability of the advice-only model depend on the financial needs of the business, the firm owner, and employees. The driver for all of it, though, simply boils down to the number of clients or engagements the advisor (and/or their team) can serve, and the average revenue generated by each client or engagement.

Historically, the hourly-only model has struggled to scale, driven primarily by the fact that when engagements are ‘only’ paid by the hour for a 1–2 hour meeting – at what might end out to net an average of only $300 to $500 per engagement – it takes an extraordinarily large (by financial-advisor standards) number of engagements to sustain the business.

For instance, generating $200,000 of revenue would require upwards of 400 engagements at $300 to $500 each, and few individual advisors manage to ever get more than a dozen or few new clients in a year (especially when they have to service so many engagements as well) unless they have an especially strong and highly scalable marketing system in place.

However, not all advice-only engagements need to be quite that limited in scope. After all, when the advisor is charging $2,500 per standalone plan (per Kitces Research), the requisite number of financial plans drops to ‘just’ 80 per year. If the advisor is charging $4,000/year in retainer fees, the number of clients needs only be 50 to sustain $200,000/year of revenue (and because clients are recurring, the advisor can even build to that number steadily over the span of several years).

In turn, for advisors who are able to serve clients with greater financial wherewithal and greater complexity – for whom they can deliver greater value and charge higher fees commensurate with that value – the sustainability improves even further.

In my own practice, I offer comprehensive financial planning as a flat-fee, project-based engagement of $6,400 for a 3-month planning process. Every household pays the same fee for the same service and process, regardless of income, assets, marital status, or planning objectives; though in practice, it's not uncommon for my clients to have several million dollars of net worth (that they are comfortable managing themselves). I want to avoid complex fee structures that are difficult to explain. Half of the planning fee is paid upon signing our engagement letter, and the remainder is paid upon delivery of the plan document.

I deliberately limit my one-on-one planning capacity to two engagements per month, dedicating 10 hours per week to financial-planning work. Based on my current planning fee of $6,400, taking off one month per year, my gross annual revenue capacity is $140,800 per year. Notably, this means that even by ‘just’ doubling my target planning engagements to four per month, the business would be generating $281,600/year in planning fees while still requiring only 20 hours per week. Given the time it takes to complete my planning process (approximately 20 hours per engagement), this equates to a $320/hour fee structure (albeit paid by the holistic engagement and not on a standalone hourly basis).

However, while a $280,000/year revenue potential is feasible, as a solo business owner, financial planner, and husband, I have determined what 'enough' means for my own family to maintain our desired lifestyle. As the demand for advice-only financial planning exceeds my intended supply (as again, so few financial advisors operate on an advice-only basis, that providing such services creates its own influx of prospects), serving 22 new families per year, or doing 29 annual plan updates (since they require 25% less time), is sustainable for me.

With only a portion of my workweek dedicated to one-on-one planning, other time is spent creating one-to-many educational content. I pay myself 30% of my gross revenue to cover our personal expenses, and the remainder covers taxes, business expenses, and additional savings on my family’s path to financial independence.

In turn, since I run a 100% remote firm, incur low business expenses, and can control my schedule unrelated to the securities exchanges, I have valuable freedom over my time. Without prioritizing revenue growth as the metric of advisor success, I can spend more time and resources providing value to families who are not traditionally served by advisors. My current metric of professional (and personal) success is based on the question, “How much can I give away without expecting something in return?”

Ultimately, this has led to the development of a multi-structured business that allows me to provide value through both one-on-one and one-to-many financial education. Measure Twice Financial serves families with advice-only financial planning, Measure Twice Money publishes educational resources for DIY investors, and Measure Twice Planners teaches financial advisors how to create comprehensive financial plans. Limiting my capacity for one-on-one engagements through Measure Twice Financial allows me to do even more of what I love – learn and teach – and share that passion with others through my other business structures. I feel most successful when both the families and planners I help feel empowered to improve their own circumstances.

Ongoing retainer and hourly advice-only planners can adopt similar structures by calculating the average time allocation per client engagement and determining the revenue required to maintain desired personal and business expenses.

What Do You Do In An Advice-Only Engagement?

Many DIY investors want to engage with an advice-only financial planner for a one-time financial plan. Although this is the only service I offer, I emphasize to families that ‘plan’ is both a noun and a verb; while it is important to create an initial written plan, it is also important to adapt and proactively plan to prepare for life’s inevitable changes. Upon the plan presentation, many clients recognize the value of planning and want to know how to work together moving forward.

Accordingly, I offer flat-fee engagements to help families refine their plan annually or less often, with no obligation. If clients seek monthly accountability and monitoring of their implementation plan throughout the year, I gladly refer them to other advice-only planners who offer the retainer model with similar philosophies.

My comprehensive planning process is most suitable for clients who want to take a quick, deep dive into personalized financial education but who also want to graduate to implement the decisions themselves. Implementation may include investment rebalancing, account consolidation and rollovers, cash flow systemization, and refinancing.

An Advice-Only Financial Planning Process

My comprehensive planning process begins with a prospective client reaching out to me, usually through direct messaging on social media or through my website contact page. Because I have been an active member of many personal finance Facebook groups (even before I became an advisor), most of my prospective clients have observed the value of financial planning through my educational posts and comments on social media, where I have helped others go beyond the basics (albeit without giving personalized advice or selling my planning services, being in a community Facebook group).

The best way to learn is to teach, and I sharpen my knowledge each time I help members within the online communities in which I am active. I believe the best way to market is to be remarkable, giving to others without expecting anything in return. By sharing educational content without the intention of gaining clients, I am sought by DIY investors who value my authentic curiosity and willingness to help.

I direct all planning inquiries to my website, which is intentionally designed with transparency by clearly including the services, process, and fees. This way, future client conversations can focus on developing the relationship rather than discussing the mechanics of how I work and how they would engage me.

As advisors interested in the advice-only space seek to clarify their own messages to prospective clients and customize their websites for a new type of client, Donald Miller’s book, Building a Story Brand, can be a useful resource. Miller’s process helped me to clarify my own brand messaging and find the right words to describe my service by using elements of effective storytelling (e.g., by illustrating how a hero needs a guide). It will also be helpful for advisors to discover their publishing medium of choice – video, audio, prose, art – and to begin creating content speaking to ideal clients through that medium.

As advisors interested in the advice-only space seek to clarify their own messages to prospective clients and customize their websites for a new type of client, Donald Miller’s book, Building a Story Brand, can be a useful resource. Miller’s process helped me to clarify my own brand messaging and find the right words to describe my service by using elements of effective storytelling (e.g., by illustrating how a hero needs a guide). It will also be helpful for advisors to discover their publishing medium of choice – video, audio, prose, art – and to begin creating content speaking to ideal clients through that medium.

Since I also define success as the ability to create and meet expectations, I carefully communicate with collaborative language from the beginning of the planning relationship. Examples include saying "our" instead of "your" when sharing meeting links, and "the families I serve" instead of "my clients" to avoid false possession. Doing this reiterates the personal side of finance and changes the way I view business relationships, focused on gratitude and collaboration rather than financial transactions.

My comprehensive financial planning process features three meetings over three months, including our introductory call, data-gathering review meeting, and plan presentation call. These occur by video conferencing within the first two months, providing an additional month to encourage questions for clarity and confidence before our formal engagement ends. The whole process takes between 18 and 22 hours, based on how many financial planning areas are involved.

Meeting #1: Introductory Call For 1 Hour

This is an opportunity to learn about the family, discuss their objectives and values, and mutually define expectations for a planning relationship. Tangible examples of the planning process may also be shared, including topic area summaries that apply to the family's prioritized objectives.

After our introductory video call, the clients privately discuss whether to engage my services. If they choose to do so, they send me an email request to move forward. The financial planning engagement letter and the first half of the planning fee ($3,200 of the full $6,400 engagement fee) are submitted through AdvicePay before any financial information is shared.

Meeting #2: Reviewing Client Information For 1.5 Hours

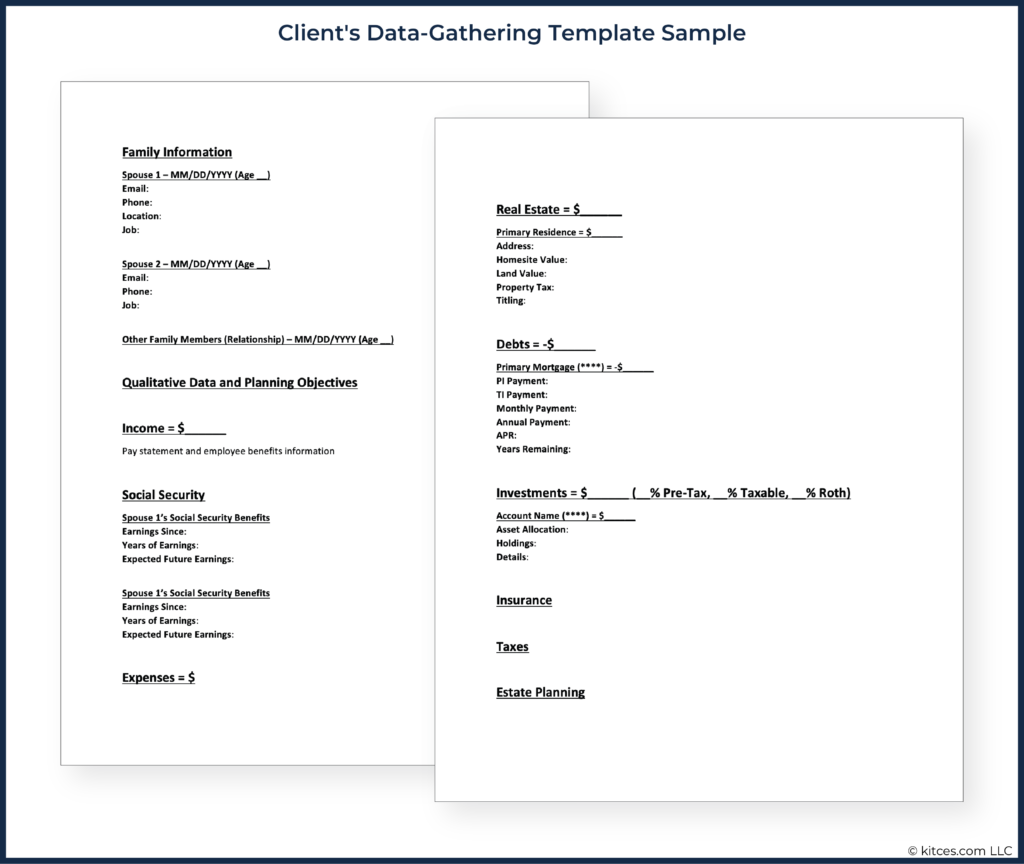

Once the formal engagement begins, and before the second meeting, the family receives a data-gathering checklist (asking for "everything in your life with a number on it”) and an eMoney login that they can use to share requested documents and connect financial accounts.

An average of 40 documents are shared using the eMoney document “Vault”, including information reporting on the following areas:

- Investments (taxable brokerage, retirement, education, health savings);

- Liabilities (mortgages, auto loans, student loans, private loans, credit cards);

- Income and expenses (pay statements, Social Security, living expenses);

- Risk management and insurance (life, disability, health, long-term care, property, and casualty);

- Employee benefits (employee handbooks, SPDs);

- Income tax (federal, state, and local returns); and

- Estate planning (wills, powers of attorney, advance directives, beneficiary designations, trusts).

Excited to learn and eager to move forward with the financial plan development – after all, they sought out my advice-only planning services – the DIY investors I serve usually share all of this requested information within a few days. I review and summarize the quantitative data between meetings #1 and #2 using a simple Word document template organized by planning topic. By the end of a planning engagement, this detailed document typically becomes 10 to 12 pages long.

Click to download as a Word document.

Financial documents not only tell a story about a family, but also offer opportunities to learn about the clients through unique questions that only arise through reviewing these documents along the way. The best questions to ask stem from a place of authentic curiosity to learn more about the families we serve. Examples of just a few questions that can arise from reviewing a client's documents alone include the following:

- A spouse’s work history upon review of a Social Security statement;

- The location of specific family members from designated estate executors and agents; and

- Future car purchases from auto insurance policies.

Aligning financial data with personal objectives and values can change the way families view and communicate about money, reiterating the power of financial planning beyond investments.

During the second meeting, where we review the information collected during the data-gathering process, we collaboratively confirm the accuracy of the prepared summary and reestablish the family's financial objectives.

Throughout this meeting, held over a video call, I share the Word document summary of the data-gathering materials on the screen to show families exactly what I see, again establishing expectations for a collaborative planning experience. We end this meeting by scheduling our plan presentation call.

Meeting #3: Plan Presentation For 2.5 Hours

Using Excel, Word, and Adobe Acrobat, I develop one-page topic summaries for each area of the plan. I have created Excel sheets and custom calculators to analyze debt repayment strategies, pay statements, investment accounts and holdings, retirement savings needs, Social Security projections, education savings needs, and income taxes. The topic summaries are formatted in Word and then exported as PDFs to assemble, protect, and share the 40- to 50-page plan deliverable.

While financial planning software can be a good way to gather client information and conceptualize income sources and RMDs, I find that the reports exported from planning software programs tend to be overly detailed, impersonal, and unhelpful for plan presentation. Since my plan deliverable is a vehicle to guide families through educational conversations, I prefer to customize each topic summary based on their unique learning curriculum.

The applicable topic summaries are followed by an executive summary and Measurable Action Plan (MAP). The order of the planning areas is intentionally crafted, by summarizing where the client is (current financial ecosystem), then moving through a story of where they could go (opportunities for change), and concluding with a roadmap illustrating how they can get there (recommendations for implementation).

Over the past two years, I have incrementally built over 50 templates based on specific educational opportunities. The ease of using my own customized templates, rather than struggling over the lack of control with planning software reports, continues to make the plan development more efficient with each iteration of the process.

When a unique topic area arises, I create a new template, available to be customized for future use. Although creating a plan document from scratch may be more time-consuming than exporting traditional planning software reports, the personalized output provides substantial value to DIY investors who desire to go beyond the basics.

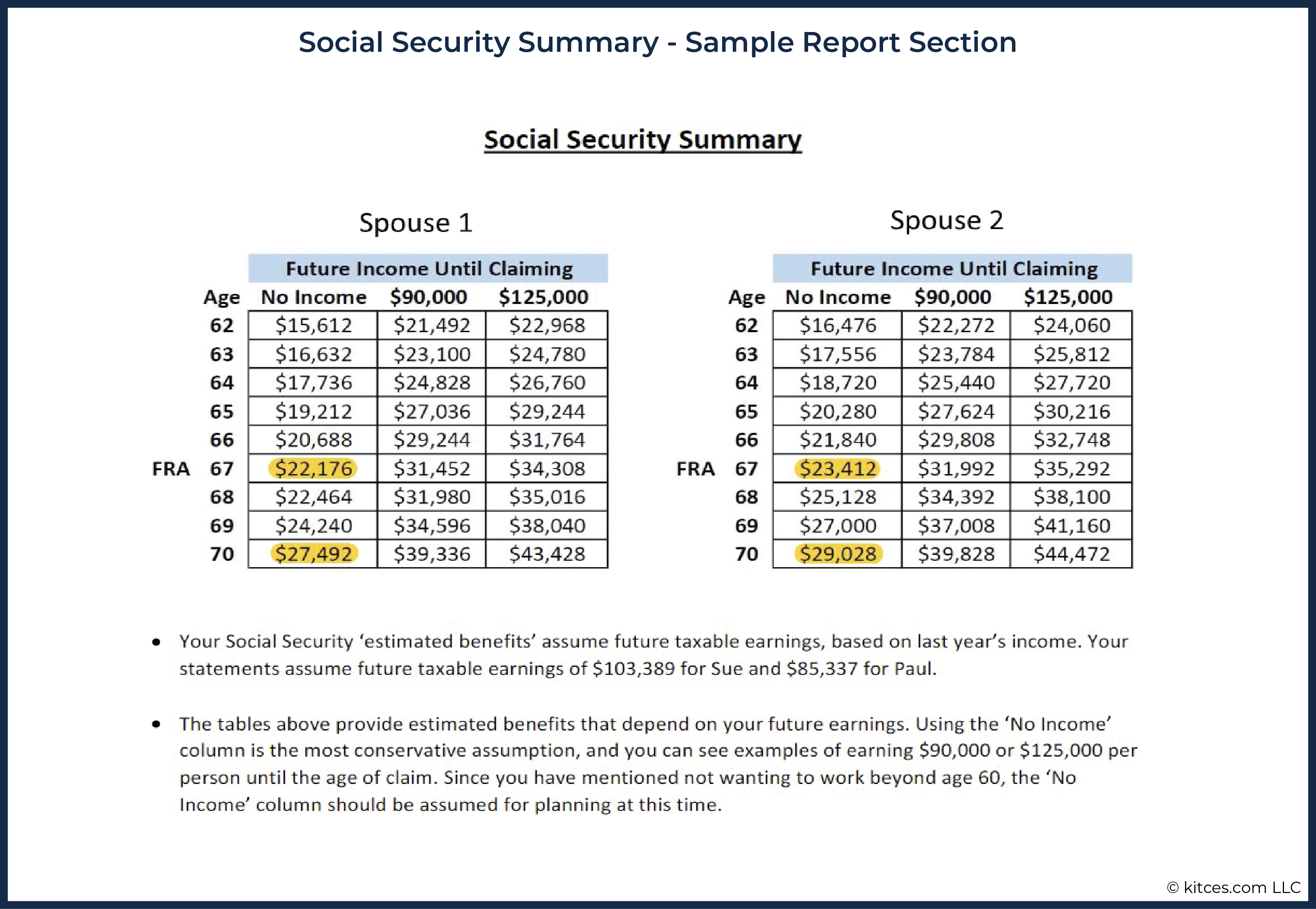

For example, when reviewing a client’s estimated Social Security retirement benefits, clients are provided with detailed results from the analysis, which are organized in an easy-to-read format in their summary document.

The educational nature of the plan presentation helps families understand both rational and reasonable approaches to each personal financial decision.

For instance, the rational, logical approach to debt repayment may compare historical investment returns to fixed interest rates over various time horizons, while the reasonable, personal approach may consider the client’s unique circumstances and feelings about debt in alignment with future retirement cash flow needs.

Rather than telling families what to do or simply doing it for them, I provide education to help them understand the 'what' and 'why' before any implementation occurs. Because when families make their own decisions with this level of understanding, the advice is more likely to stick and be implemented.

Upon delivery of the physical plan document with a hand-written note to show gratitude, the second half of the planning fee is paid.

Implementation

Although advice-only planning does not involve ongoing portfolio management, I still provide tailored investment advice during the plan presentation. This includes specific asset allocation examples, describing both basic and detailed options with low-cost funds.

Depending on the amount of time needed for the data-gathering process and on the client’s availability, the three-meeting process usually occurs within two months, allowing a third full month to address any questions (which the clients are encouraged to ask). During this time, I also offer to help families understand the investment platform of their choice. Using screen sharing during video calls, I teach families how to review cost basis information, open and transfer accounts, and reallocate their investments.

I typically suggest using M1 Finance for retirement accounts since it provides dynamic and one-click rebalancing. I prefer Fidelity for taxable brokerage accounts and HSAs, due to its user-friendly interface, control over tax harvesting, and customer service.

Notably, the key distinction between simply delegating tasks to clients and delivering good advice-only financial planning services involves teaching clients not just how to implement tasks but also why the tasks are important so that clients can proceed with clarity and confidence moving forward. If new planning considerations and questions arise beyond our three-month process, we can mutually define a new scope of engagement. There is no expectation or obligation for clients to continue working with me beyond the initial planning engagement.

Many DIY investors tend to assume that our industry does not want to serve them without taking control of their assets. And while there are numerous advisors who have the knowledge and capacity to help, they don’t always offer a service, process, and compensation model that aligns with this specialized advice-only demand.

As in the end, while many advisors do offer investment management and financial planning, and may even offer financial plans on a standalone basis, when the advisor is still primarily in the AUM business, there is often a subconscious bias or nudge for clients to move towards implementing their portfolio with the advisor, which clients can quickly sense. And this is what creates the opportunity to differentiate specifically as an advice-only financial planner… where DIY investors can be confident that their advisor will not solicit their investment assets, and instead remain fully focused on only their financial planning needs.

As DIY investors learn about the importance of comprehensive financial planning and become aware of advice-only offerings, I believe advice-only financial planning will continue to gain popularity across all age groups, not limited to millennials and younger. About half of the clients I serve are between ages 50–60, with many families wanting to graduate from using an advisor for investment management, now that they know advice-only planners exist.

And in my experience, the demand for this model already exceeds the supply, so I encourage financial planners to consider reestablishing who they want to serve and how they can provide value. Some advisors may find the advice-only model quite appealing, especially for those who are passionate about financial education but who want to free themselves from the tasks and time commitments of investment management.

Alternatively, some advisors may want to work outside of market-trading hours or stick to email and video calls for client communication instead of phone calls or in-person meetings. By asking themselves how they would prefer to work with their own financial planner, advisors can decide if they resemble the ideal version of themselves and whether they can be that advisor to the communities they serve. Creating a business that aligns with who and how an advisor wants to serve can help them remember the importance of keeping finance personal – for themselves and for the families they help!

What a great article on a non-traditional compensation model for delivering massive value to clients! My hat is off to Cody for building such an intentional practice and my thanks to him for so transparently sharing his process.

I must confess I also enjoyed that he was able to articulate the value of a non-AUM fee model without feeling the need to bash all the other comp models.

Excited to see what comes next.

I appreciate your kind comment, Matthew! I believe delegators, DIYers, and families in between can experience massive value through financial planning. Like with financial advice itself, there is no one-size-fits-all model that fits everyone. The compensation model itself is not where the value lies but how the intentional service and process align with the expectations of the unique families I serve.

Story Brand is a great book every planner could benefit from reading. Great that you included it in the article.

Along with The E-Myth: Revisited and Traction, Building a StoryBrand has been so helpful in the development of my firm.

Hi Cody – very cool work you’re doing! I would think that one of the benefits of advice-only planning would be the potential to not have to register as an RIA at all, avoiding the associated costs and headaches. This would preclude you from giving specific investment advice, but surely there is a way to keep things general and the DIY clients could figure out how to implement reasonable portfolios? Have you considered this? My understanding is that you can give all the financial planning advice you want and it doesn’t matter to the SEC or state regulatory authorities until you start giving “investment advice for compensation.”

Thank you, Jeremy. I do wonder about the future of regulation in this area. Since I want to provide specific investment advice, including personalized tax harvesting strategies and reallocation guidance, I will continue to give investment advice for compensation and remain registered as an RIA. Although the selection of investments is a very small piece of the planning puzzle, I still prefer to include it in practice moving forward.

Very good article. I was hoping there might be some information regarding how an “Advice Only” financial planner (no investment advice) would need to be licensed and/or registered. Also, it would be beneficial to have information regarding the line between allowable asset allocation discussion versus giving “investment advice”.

Thank you, John! Although there is no advisor discretion of investments, advice-only financial planners provide personalized investment advice, requiring RIA registration in my case. I help clients select the specific securities, but they implement the trades. You bring up a unique insight about the line between general asset allocation (mix between equity and fixed) and specific advice (providing tickers, etc.). I would love to understand a clear distinction between financial coaching (usually without specific investment advice) and financial planning.

The reason your article caught my attention is that I have been trying to get guidance on how I can provide comprehensive financial planning (no investment advice beyond asset allocation) for a fee, without being an RIA. The good folks at CFP punted on the question. Maybe I simply need to change the terminology to Financial Coaching.

I am interested to find out more. There are many career changers who have mentioned wanting to do this without the registration and CFP experience requirements.

You can see more about Financial Coaching models at https://www.kitces.com/blog/financial-coaching-what-it-is-and-how-to-become-one/ as well.

That being said, as Cody noted, such advice often veers into the realm of providing personalized investment advice – especially with those who pay more substantial fees (and thus tend to have more wealth including investment assets that are covered under the advice arrangement) – which triggers RIA registration. The registration requirement occurs when you provide advice on investments for compensation; it has no relationship to whether you also MANAGE those investments. See https://www.kitces.com/blog/registered-investment-adviser-requirements-series-65-exam-timing/ for further discussion.

– Michael

Kudos, Cody, for outlining the value provided by the advice-only model. And thanks to Nerd’s Eye View for highlighting this little-known segment in our field. As Cody found in his startup phase, there is so much more demand for than supply of advisors for this service. One ironic client group I would add are other financial professionals- CPAs, corporate CFOs, insurance agents, other planners – they don’t need/want someone to manage the money, but often want someone looking over their shoulder, or sometimes reassuring their spouse! They totally appreciate the value provided by the advice too. Cody, have you thought about getting project-based advice-only planners together in some sort of community? I too have a steady stream of inquiries and a limited number of weeks that I want to work doing planning, so I am constantly looking for advisors to refer out to. Thanks again for highlighting this work.

Thank you for your kind comment, Holly! Yes, I am part of an advice-only mastermind group and a private Facebook group for advice-only financial advisors (https://www.facebook.com/groups/2858732627742143). I also have trouble finding other advice-only planners for referrals, but I hope to collaboratively create a solution for this. I believe there will be dozens of financial planners moving into this model within the coming year.

Cody thank you for the detailed explanations and your own approach. It’s a really valuable article for us, as we are the first fee only financial firm in Ukraine.

Cody, fantastic article! Thank you for providing such valuable information about your advice-only firm. If you recommend a product such as permanent life insurance or an annuity, do you refer this to another advisor or do you help the client buy these products online?

Also, are your custom excel calculations going to be available for purchase on Measure Twice Planners?

I appreciate your kindness, Matthew! When I recommend any investment or insurance products, I refer to another professional who specializes in that space and doesn’t have a conflict to go beyond that scope. Most of my planning tools will be shared for free at Measure Twice Money.

I came across this article and was greatly impressed with the level of details and the value financial planners bring to the table. I am a certified CFP and want to open my own fee-only based practice. Cody, can you share how I should start and the registration and forms I need to fill before I can start offering advice. Thanks!