Executive Summary

The financial services industry has long presented itself as one with high earning potential. As the saying goes, “there’s a lot of money in the money business”. For financial advisors, in particular, the career is often held out as one where advisors have ‘unlimited’ income potential… or at least, an earnings opportunity that is limited only by the hours of hustle that the advisor is willing to put in to build their book of clients.

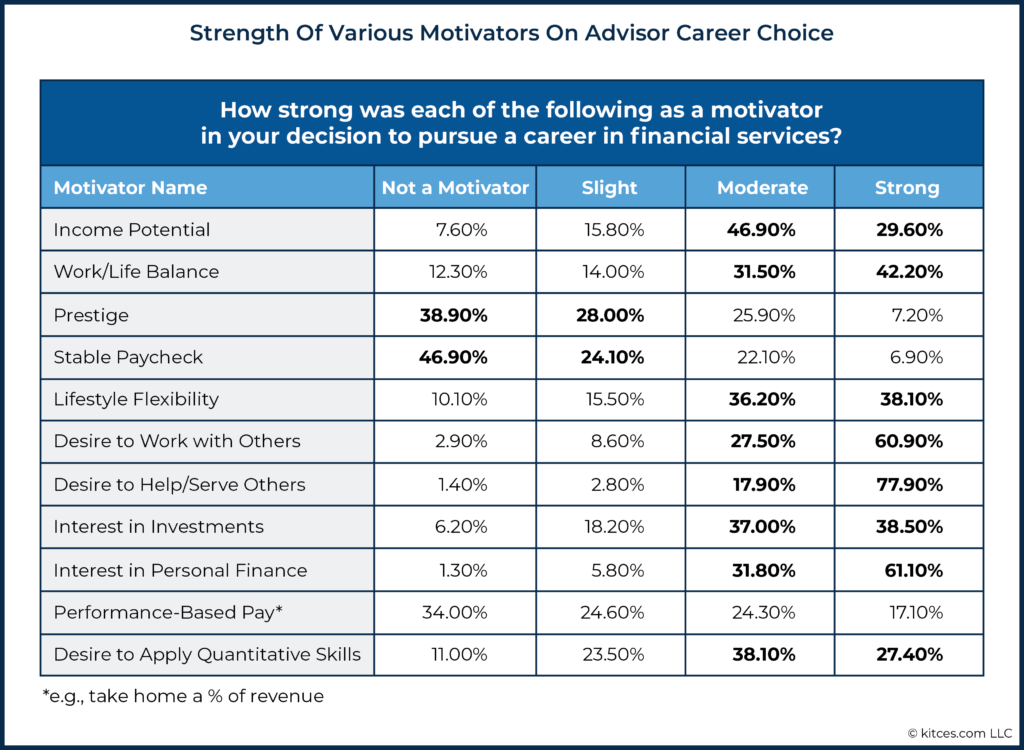

Yet, while the average established financial advisor does earn significantly more than the median US household ($192,000 versus $68,700, respectively, according to the latest Kitces Research study), what’s even more notable is that when it comes to overall wellbeing, the average financial advisor actually outscores the typical American on all 18 subscales of the Comprehensive Inventory of Thriving! In other words, the career of being a financial advisor isn’t only one of above-average income, but it is rewarding across all domains of wellbeing, from relationships to engagement to mastery and meaning… with a particular focus on self-efficacy and accomplishment. In other words, the career of being a financial advisor is particularly conducive to those who are good at setting goals and being able to take action to achieve them… who then work with clients to help them set and achieve their own goals, too!

Unfortunately, though, one of the hardest aspects of being a financial advisor is simply figuring out what path to pursue to be a financial advisor, in an industry with choices from employee to independent, broker-dealer to RIA, large national firm to local boutique (or even just hanging one’s own shingle as a solo advisor!). For which it seems that every successful financial advisor says “their” channel and business model is the best… and in practice, relatively few advisors change channels at all throughout their careers!

However, as our 2020 Kitces Research study on Advisor Wellbeing reveals, not all advisor channels and business models are truly equal when it comes to advisor wellbeing. Instead, the reality is that the ‘best’ channel and business model for an advisor depends on their own intrinsic motivators and preferences. For instance, advisors who greatly value their autonomy may eschew the wirehouse model and pursue independence, while those who value income the most will tend to start their own firm (even though doing so is far more time-consuming), while those who value their time over just maximizing income may prefer an employee career path rather than trying to ‘eat-what-you-kill’ as an advisor who has to get their own client base.

In order to explore this further, we’re excited to announce our latest 2021 Kitces Research study on Advisor Wellbeing, specifically to delve more deeply into the intersection of what leads to the greatest levels of happiness and wellbeing as an advisor, and the motivators that lead us to become financial advisors (and to choose certain channels and business models over others). Notably, this year’s Wellbeing survey is shorter than our ‘typical’ Kitces Research study, and it’s our hope that every advisor will take a few minutes to share their own experiences and perspectives for this important research!

Thanks in advance for your participation and willingness to contribute!

What We Learned In The 2020 Kitces Research Study On Advisor Wellbeing

According to the latest Kitces Research study, the median income of an established financial advisor is almost 3X the median household income ($192,000 versus $68,700, respectively). Yet as the saying goes, “money can’t buy happiness”, and most people have at some point or another witnessed the person who earns a great income, but may have sacrificed ‘too much’ in the process. Which raises the question of how financial advisors who experience above-average income fare when it comes to their personal wellbeing.

In our 2020 Kitces Research study on Advisor Wellbeing, though, we found that in practice, the financial advice business is not only financially rewarding… it is very personally rewarding as well. In fact, using the Comprehensive Inventory of Thriving (CIT) – which evaluates wellbeing across 7 broad domains of Relationships, Engagement, Mastery, Autonomy, Meaning, Optimism, and Subjective Wellbeing – the research shows that financial advisors outscore the general population in all 18 subscales of the CIT!

Of particular note is that financial advisors score the furthest above the general population on the dimensions of self-efficacy and accomplishment – the measures of whether we feel capable of achieving our goals, and our sense of progress towards those goals. Which means, in essence, that financial advisors thrive in setting goals for themselves and then pursuing and achieving those goals. No surprise, then, that their chosen career is to help others identify, pursue, and achieve their goals, too!

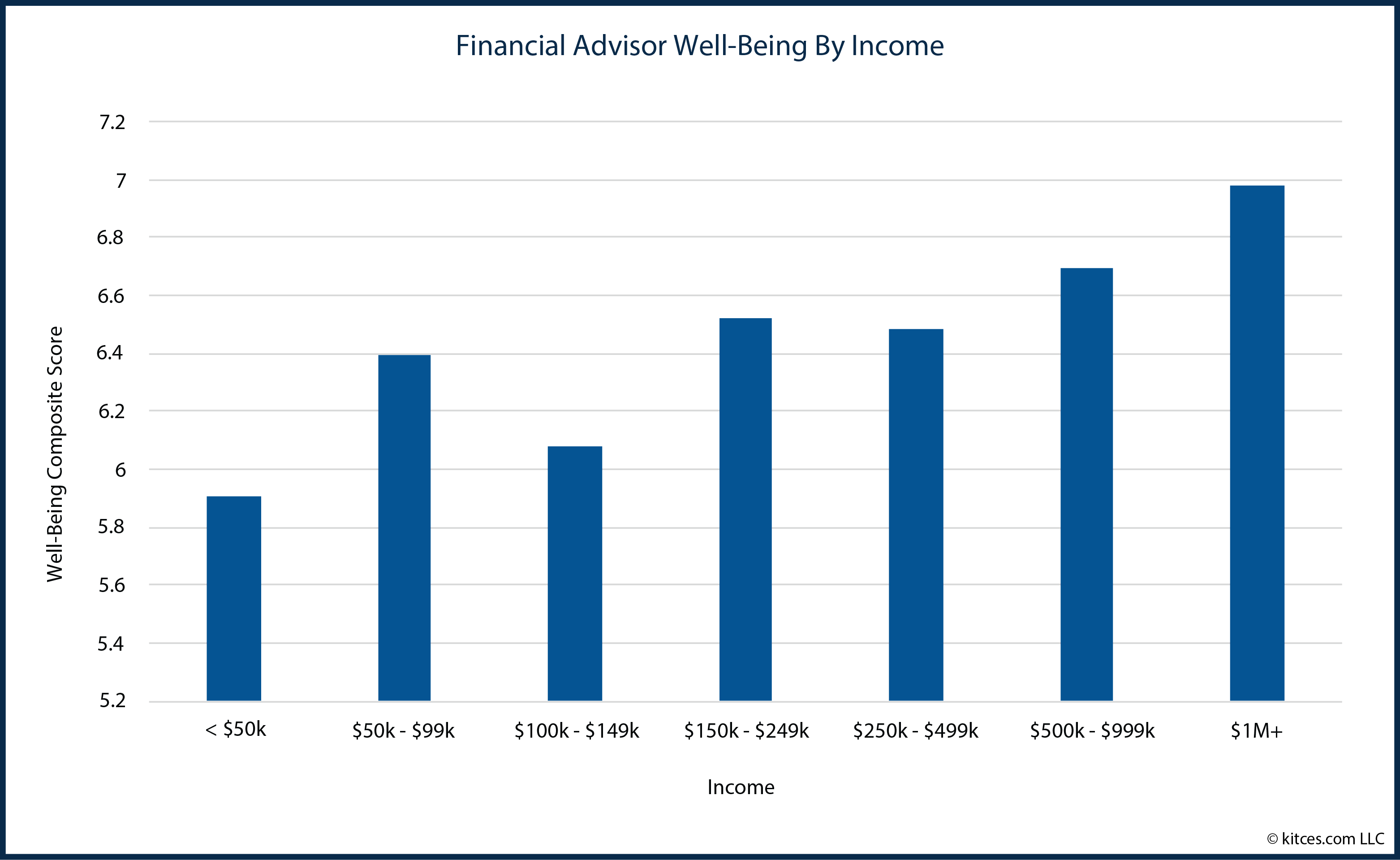

In fact, our results show that advisor wellbeing rises fairly steadily as advisor income rises with the accomplishment of successively higher personal goals… and unlike other research on the general public, where wellbeing tends to level off as income rises above a certain threshold, advisor wellbeing continues to rise as income rises!

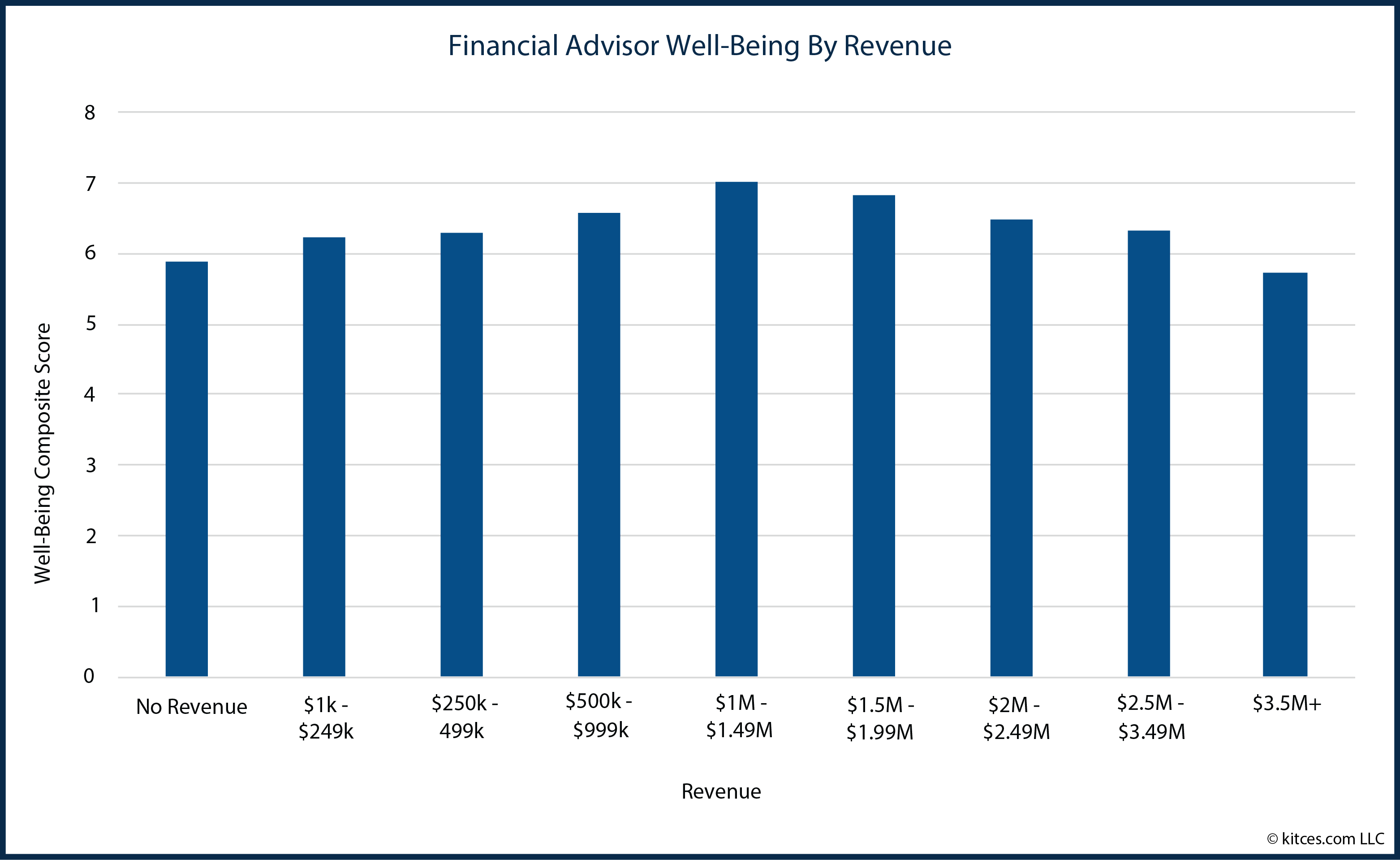

Notably, though, the trend does not hold when it comes to revenue, though! Instead, while advisor wellbeing does rise steadily until revenue crosses $1M, further increases in revenue actually witness a steady decline in advisor wellbeing, which accelerates as the advisory firm and its revenue grow further!

The trend shouldn’t be entirely surprising, though, as the reality of growing an advisory business is that by the time a firm materially exceeds $1M of revenue, it ‘inevitably’ reaches the point where it must add more advisors (beyond the original founder/owner)… which means both that the next 100 new clients are significantly less profitable than the first 100, and when advisory firms typically hire a new team member every $275,000 of revenue, that further growth increasingly shifts the role of the advisor themselves from being a client-facing advisor to being a manager of an advisory firm team. A significant conflict of focus when the primary motivators for financial advisors are to work with and serve clients… not necessarily to manage people!

Aligning Our Advisor Career Choices With Our Personal Wellbeing

One of the biggest challenges for newcomers considering whether to become a financial advisor is that there are almost a dizzying number of ways to pursue the career. Prospective advisors can join an established firm in an employee model, or be an independent who hangs their own shingle. They can join a large national wirehouse or a small local boutique. They can seek out a role that requires getting their own clients, or one where clients are provided to them.

The situation is complicated by the fact that, upon asking an advisor in any particular channel if theirs is a “good way to become a financial advisor”, the answer from the successful advisor in that channel is virtually always “yes”… followed by statements of why their channel is better than any other. Independent advisors criticize the wirehouse for its red tape and corporate bureaucracy and praise the freedom of independence. Wirehouse advisors criticize independents for the lack of systems and the distractions of building a firm’s infrastructure from scratch that limits the time to simply serve clients. Advisors who have built their own client base and firm as owners criticize the employee channel for having a more limited financial upside and laud the benefits of controlling your own income and destiny. Employee advisors criticize the eat-what-you-kill model for its high pressure and stress and extol the benefits of having a stable salary and a set schedule where the job doesn’t intrude on nights and weekends.

In fact, arguably one of the most astonishing aspects of how many different channels and choices are available to financial advisors is how little advisors actually shift between those models over time. After all, even “major” industry trends like the breakaway broker movement from wirehouses to independents are measured by how many “dozens” of advisors broke away… from a wirehouse channel with nearly 50,000(!) advisors across the big 4 (Merrill Lynch, Morgan Stanley, UBS, and Wells Fargo), which amounts to a breakaway attribution rate that may be no more than just 0.1% to 0.2%/year. More generally, Cerulli Associates finds that aggregate market share for financial advisors across the channels rarely changes more than about 1%/year.

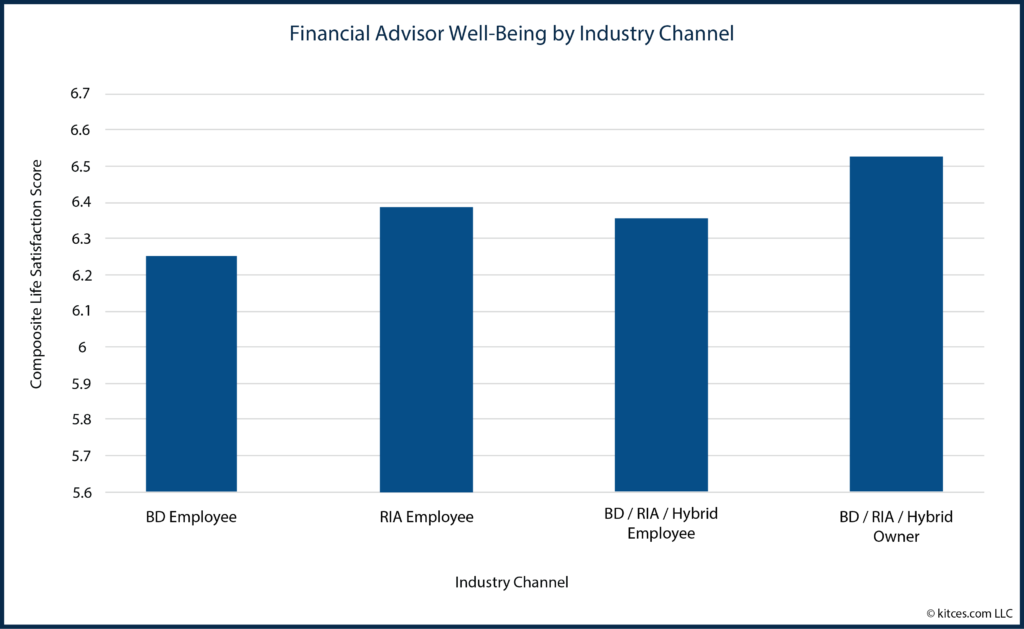

What this ultimately suggests is that one advisor channel may not be objectively “better” than another… and instead, that some channels are better than others for certain advisors based on their own preferences. For instance, Kitces Research on Advisor Wellbeing shows only a very small difference in advisor wellbeing between employee advisors at broker-dealers versus those at RIAs, and a very slight difference between employee advisors and independents who own their own practices!

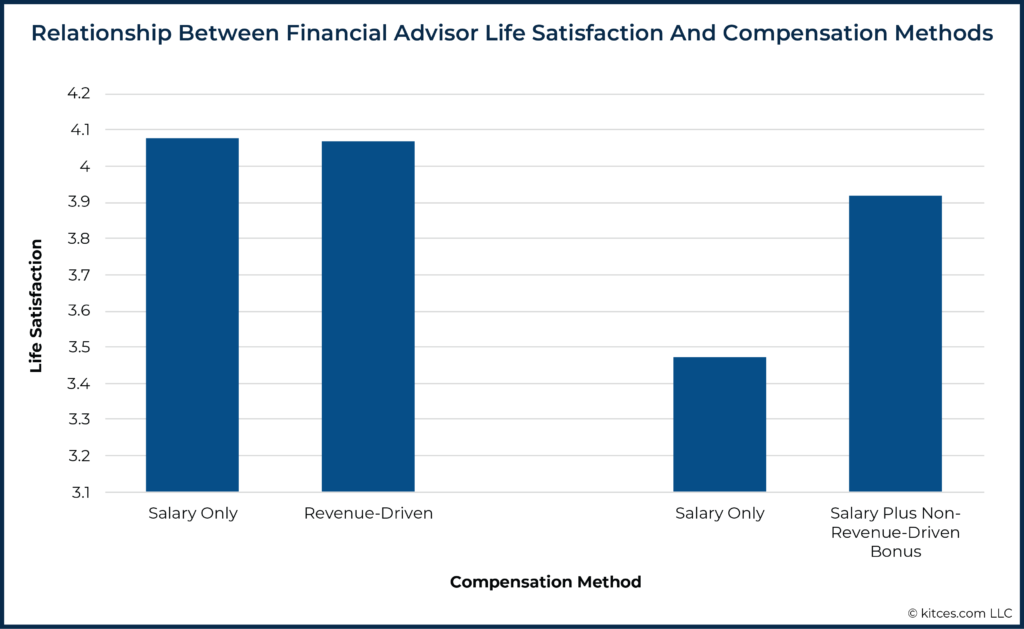

Notably, though, there are actually much bigger differences within the groups. For instance, our research does find that because advisors are very focused on goal-achievement for themselves, having the autonomy to really impact their outcomes – whatever the channel may be – is of significant importance. Thus, for instance, advisors overall have little difference in wellbeing between being salaried or having revenue-driven compensation. However, amongst associate advisors in particular – who typically aren’t in a position to bring in their own clients – there is a strong preference for a salary plus non-revenue-driven bonuses (e.g., individual bonuses that are still under their own personal control).

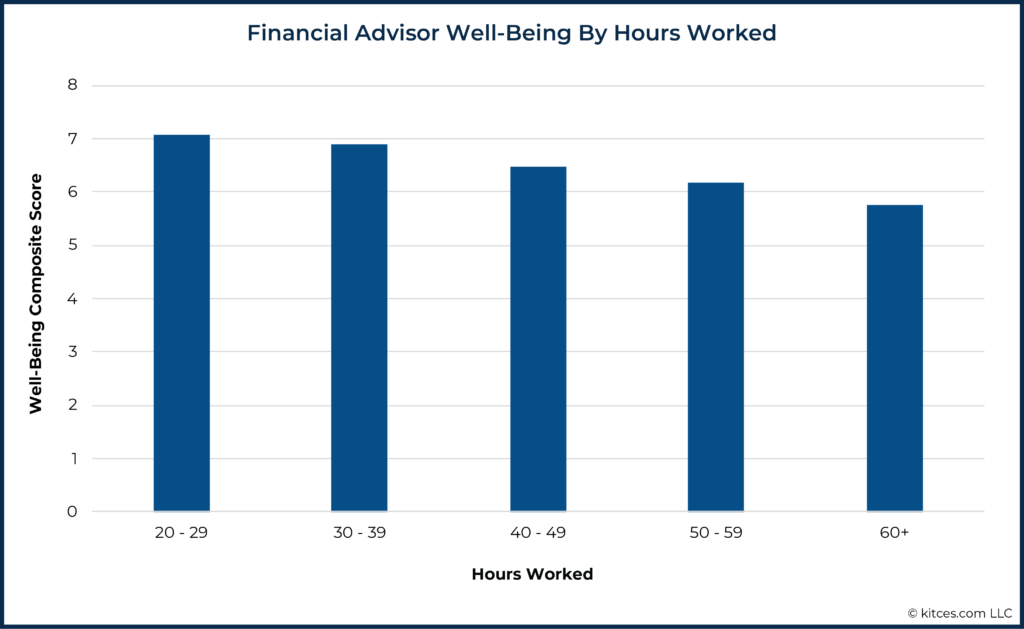

As it turns out, though, the greatest predictor of advisor wellbeing is not actually the industry channel or business model, but simply the amount of time that the advisor spends to earn the income that they earn! For which the happiest advisors are actually those who have a focused practice with a limited number of high-revenue clients, allowing them to work less than 30 hours every week and enjoy the highest levels of wellbeing. While any level of additional hours worked every week is associated with successive decreases in wellbeing as the time increases.

Of course, the caveat is that a coterie of high-revenue clients doesn’t just magically appear, and instead can take many many years of work to get there. Along the way, income is lower, and hours are higher. In addition, as noted earlier, advisor wellbeing continues to rise as income rises, with no apparent plateau. Which runs somewhat contrary to the reality that the highest levels of wellbeing are found amongst the advisors who work the fewest hours (not those who work the most hours to achieve the highest income).

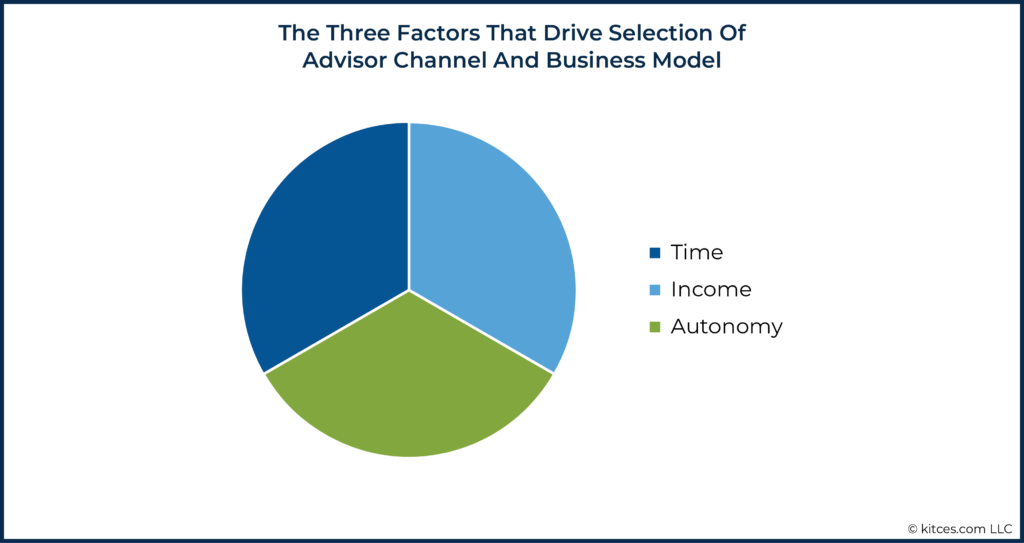

Which ultimately suggests that in the end, advisor wellbeing is more a function of trade-offs. Spending more time can build income, but building income takes time. While those who prioritize time more than income may choose a salaried employee job that has less income upside but achieves better working hours more quickly. Unless the advisor greatly values control and autonomy and wouldn’t be happy as an employee, in which case they ‘have to’ become an independent and work to build their practices. But they must then decide how big they want to build it and how much to trade off time for current or future income!

Thus, for instance, the advisor who prioritizes income but not autonomy may choose a wirehouse, while an advisor who prioritizes time over income may choose an employee model, and those who prioritize income and autonomy over time may choose to become an independent (and then over time, may choose to reinvest their income to ‘buy’ more autonomy to reduce their time, also known as a “lifestyle practice”).

Participate In The 2021 Kitces Research Study On Advisor Wellbeing

In our new 2021 Kitces Research Study On Advisor Wellbeing, we’re aiming to better understand how the motivators that lead us to become financial advisors, and how the ways we weigh factors like time, income, and autonomy, influence the decisions we make about which channels to affiliate with and the business models we choose. In the hope that by better understanding what influences the choice of channels and business models, we can help advisors get started in the right channel, and help those who may be unhappy in their current environment to figure out what change would help them to improve their own happiness and wellbeing.

We hope you are excited about this new advisor research as well and can support us by participating in our new Advisor Wellbeing survey (at least for those readers who are financial advisors!). This year’s survey is shorter than past surveys and should take about 20-25 minutes to complete. All participants will receive a free copy of the final Kitces Research white paper that we produce, providing you with our latest research on what drives wellbeing… and hopefully giving you some ideas about the changes you could make in the future to improve your own wellbeing!

Thank you in advance for taking a little time to participate in this important financial planning research study!

Awesome blog! Thanks for sharing this information.

Happy to be of service! Can’t wait to share out results! 🙂