Executive Summary

In response to the unfolding COVID-19 global pandemic (as the US this week surpassed China as the country with the most confirmed cases in the world), the US Senate has passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act, a $2 trillion emergency fiscal stimulus package, in order to help ease the effects of the resulting economic damage. While the House has yet to vote on the bill, it is anticipated to be approved and signed into law by President Trump shortly thereafter and includes a wide range of provisions for both loans and outright rebate payments or tax credits aimed at helping individuals, businesses, healthcare entities, and state and local governments meet short-term cashflow demands.

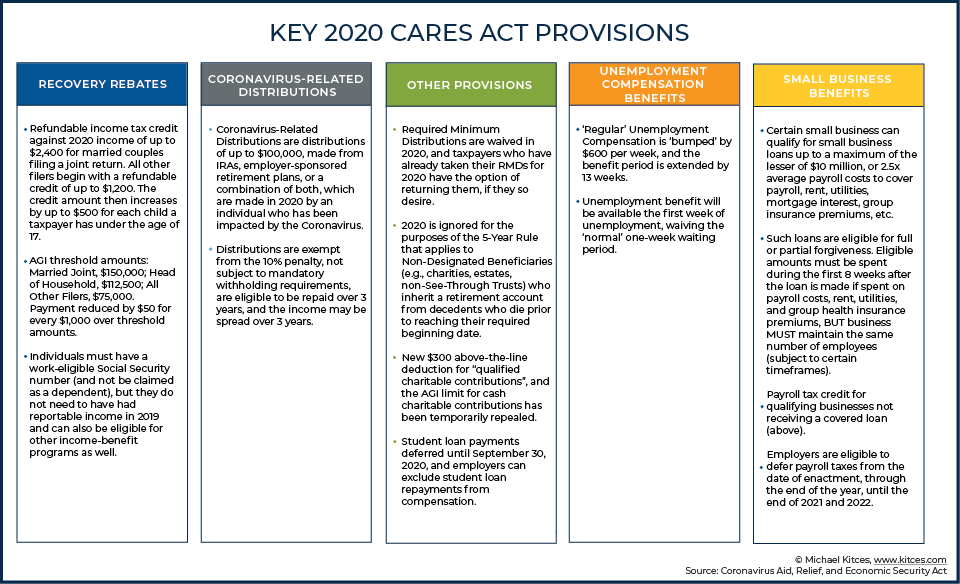

In the context of financial advisors and the clients they serve, the most notable provision in the bill is the direct payments to taxpayers. Specifically, individuals who had up to $75,000 in adjusted gross income in 2019 will receive a one-time payment of $1,200, while married couples with AGI up to $150,000 will get $2,400. Additionally, taxpayers will receive an additional $500 for each qualified child, while individuals and families with income above their respective thresholds will see their relief payments reduced by $50 for every $1,000 in AGI. Notably, while individuals must have a work-eligible Social Security number (and not be claimed as a dependent), they do not have to have had reportable income in 2019 and can also be eligible for other income-benefit programs as well.

From the retirement planning perspective, notable provisions of the CARES Act include the elimination of the 10% early withdrawal penalty on distributions from retirement accounts for so-called “Coronavirus-Related Distributions” (with the option to spread income taxation over three years, and the ability to recontribute back to those same accounts to make up in the future), the suspension of required minimum distributions (RMDs) in 2020 for a wide variety of retirement account (for both account owners as well as beneficiaries) as well as the ability to return current-year distributions, an increase of $600 per week for unemployment benefits for up to four months as well as an expansion of benefits for those who would otherwise not normally qualify (like self-employed individuals and independent contractors), and the deferral of Federal student loan payments through September 30, 2020.

With respect to small businesses that have been impacted by COVID-19, certain small businesses with up to 500 employees will be able to take out loans (up to $10M depending on payroll costs and other factors), which will be eligible for forgiveness if used to cover payroll and other expenses (like rent and utilities), along with other ‘employee retention’ tax credit opportunities. Other benefits for businesses include a delay in the employer’s portion of Social Security payroll tax until January 1, 2021 (with half of the deferred amounts due at the end of 2021, and the other half due at the end of 2022), and more flexible Net Operating Loss rules to obtain immediate refunds, among others.

Beyond benefits for individuals and businesses, the CARES Act provides for $454 billion in emergency lending, not only to states and municipalities, but to airlines and other businesses critical to US national security, and another $150 billion allocated proportionally to state and local governments to offset amounts used to respond to the pandemic.

Ultimately, the key point is that the CARES Act is a historic emergency relief program for Americans and provides much-needed assistance for those affected by the pandemic and the resulting economic damage. And with changes in tax laws come planning opportunities for clients. However, the CARES Act is not without its caveats. As while relief payments to individuals and families are based on 2019 AGI levels, there will be countless Americans currently experiencing sudden financial hardship and unemployment who are seeing significant declines in income, but sadly, will not qualify for relief checks. Similarly, small business relief provisions – for both clients of financial advisors, and potentially financial advisors in their own businesses – do have very specific requirements to qualify (in an effort to ensure the dollars go where needed most, but inevitably meaning that some that are close to ‘the line’ must engage in planning to actually qualify). At the very least, though, the CARES Act will be a dominant conversation for financial advisors and their clients in the months to come as Americans (and the world) continue to cope with the current COVID-19 crisis.

*** Author's Note: Since the publish date of this article, additional guidance has been released on certain provisions discussed below. Check out our Advisor’s Guide To The Paycheck Protection Program resource page for up-to-date information on all the important PPP provisions!

In recent weeks, the novel Coronavirus (COVID-19) has emerged as a bona fide global “pandemic” according to the World Health Organization, with exposures doubling in many countries (including the US) every 3-5 days, and threatening to quickly swamp the health care system’s ability to treat those who experience more serious and potentially life-threatening symptoms.

To minimize the risk of an increased fatality rate due to overwhelming the health care system, and learning from prior pandemics like the Spanish Flu in 1918, epidemiologists have urged countries to “flatten the curve” by engaging in measures that won’t necessarily stop but do slow the spread of the virus… ensuring that even if ultimately most people do get infected, the health care system can handle their health needs as sickness spreads.

Consequently, various counties, cities, and even entire states have engaged in “shutdowns” with various work-from-home or outright shelter-in-place mandates, and the President has encouraged the entire nation to engage in “social distancing” and avoid gatherings of more than 10 people at a time.

The caveat, of course, is that when people don’t go out because they’re remaining socially distant and sheltering in place, many businesses see drastic curtailments of their entire customer base, from hotels and airlines to restaurants across the nation. As a result, the outbreak of the coronavirus has resulted in what is by far the largest spike in single-week unemployment claims ever, up 3.3 million in just a week. And of course, beyond the outright hardship for those who lost their jobs, the longer people remain unemployed, the further their inability to earn and spend can ripple through to the rest of the economy.

To help fill the void, the Federal Reserve has taken dramatic steps in monetary policy to keep the financial system stable. And Congress has sought to complement their effort with major fiscal stimulus – in what now appears to be the largest economic stimulus package in our country’s history.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020 is an estimated $2 trillion package, including nearly half a trillion dollars in individual rebate checks (akin to how the US has handled prior crises in the past 20 years), another $500B for support of several severely-damaged industries, nearly $400B support including tax credits for wages and payroll tax relief, over $300B of support for state and local governments, and almost $150B for various initiatives to support hospitals and the health care system.

As of the publication of this article, the CARES Act has been passed by the Senate and is anticipated to ultimately be passed by the House and signed by President Trump in the coming days. Nearly 900 pages in length, the CARES Act will undoubtedly be pored over for weeks and months to come, but contained below are the most notable provisions relevant to financial advisors and their clients, in particular, to engage in proactive client conversations in the coming days and weeks.

Breaking Down The Recovery Rebates

Perhaps no single provision in the CARES Act has received more interest from the general public than Section 2201, Recovery Rebates For Individuals. In short, people want to know whether they should be expecting a check from Uncle Sam, and if so, how much the check will be for.

The good news is that according to estimates by the Tax Foundation, over 90% of taxpayers should receive some amount of Recovery Rebate. The bad news is that thanks to the way the law was drafted, there may be a substantial number of people who could really use the help right now who won’t qualify, and even for those that do, practical issues with how such payments may be distributed could substantially delay their receipt!

Calculating The Amount Of A Taxpayer’s Recovery Rebate Advance

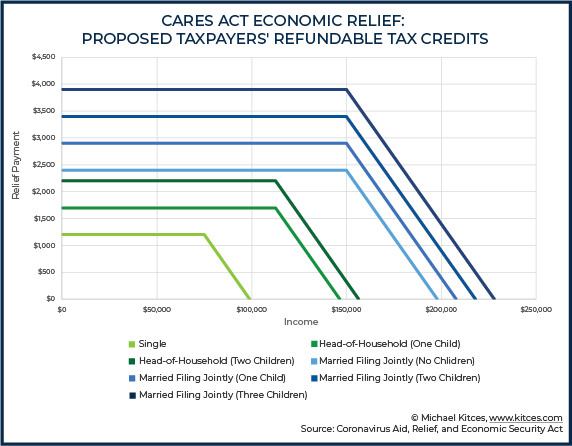

As a starting point, the CARES Act provides a refundable income tax credit against 2020 income of up to $2,400 (more on this in a bit) for married couples filing a joint return, while all other filers begin with a refundable credit of up to $1,200. The credit amount then increased by up to $500 for each child a taxpayer has under the age of 17.

Thus, a single taxpayer with one child would be eligible for up to a $1,200 + $500 = $1,700 refundable credit, while a single taxpayer with two young children would be eligible for up to a $1,200 +$500 + $500 = $2,200 credit. A married couple, on the other hand, with one child and who file a joint return, would be eligible for up to a $2,400 + $500 = $2,900 credit, while the same couple with four children would be eligible for up to a $2,400 + $500 + $500 + $500 + $500 = $4,400 credit.

If you’ve read the last two paragraphs closely, you probably noticed a lot of “up to”s in there. And there’s a reason for that. As a taxpayer’s income begins to exceed their applicable threshold, their potential Recovery Rebate Payment (their credit) begins to phase out. More specifically, for every $100 a taxpayer’s income exceeds their credit, their potential Recovery Rebate will be reduced by $5.

The applicable AGI threshold amounts are as follows:

- Married Joint: $150,000

- Head of Household: $112,500

- All Other Filers: $75,000

Example #1: Mickey and Jackie are married and file a joint return. They have four children, ages 10, 13, 15, and 17, and have $176,000 of Adjusted Gross Income (AGI).

As such, they are eligible to receive a maximum Recovery Rebate of $2,400 + $500 + $500 + $500 = $3,900! (Note: Recall that the potential Recovery Rebate is only increased by $500 for each child under 17, so only three of the couple’s children qualify.

But while $3,900 is the maximum potential Recovery Rebate the couple to which the couple could be entitled, they have income in excess of their $150,000 threshold amount. More specifically, they are $26,000 over their threshold amount, so their recovery rebate must be reduced by $26,000 x 5% = $1,300.

As such, the ultimate Recovery Rebate check that Mickey and Jackie will receive will be $3,900 - $1,300 = $2,600!

Notably, by virtue of the way the Recovery Rebate is phased out, two taxpayers who have the same filing status will have different phaseout ranges if they have a different number of qualifying children. Because while a taxpayer’s Recovery Credit will begin to phase out after income exceeds a threshold determined by filing status alone, the starting (potential) Recovery Credit ‘burn rate’ is a constant $5 per $100 of additional income. Thus, as can be seen in the graph below, the greater the number of qualifying children a taxpayer has, the wider their phaseout range.

Recovery Rebates Will Be Dispersed Based On 2018/2019 Income But Are Actually For 2020

One of the more confusing aspects of the Recovery Rebate is that it has a bit of a ‘split personality’, in that the initial amount paid will be based on either a taxpayer’s 2018 or 2019 income tax return (whichever is the latest return that the IRS has on file), while it will ultimately be ‘trued up’ if a taxpayer is owed money based on their actual 2020 income.

In other words, Congress is going to ‘front’ taxpayers an estimated amount based on their 2018/2019 incomes, but if the 2020 return shows they really ‘deserved’ it, they’ll get it after all, albeit much later. This little ‘wrinkle’ may cause any number of headaches.

Perhaps the individuals most negatively impacted by Congress’s choice to process the Recovery Rebates this way are those taxpayers who had high income in 2018/2019, but who have since been laid off, furloughed, or had their incomes substantially decrease for other reasons. In such situations, individuals may have a genuine need for income at this very moment. And while they won't ultimately benefit from the Recovery Rebate until April of 2021 (or whenever they file their 2020 return), that is of absolutely no use to them today!

Example #2: Georgia is a single taxpayer with no children who made $150,000 as a boutique travel agent in 2019, the most recent year for which a tax return is on file with the IRS. Unfortunately, in early February of 2020, after making just $8,000 for the year, she was let go and has been unable to find new employment.

Suppose that Georgia is not re-employed until July, and ultimately makes ‘just’ $45,000 in 2020. Given these set of facts, Georgia is actually eligible for a $1,200 Recovery Rebate, because her income is well below the $75,000 threshold amount for single filers.

However, because Georgia’s 2019 income was $150,000, she won’t get any cash flow assistance now via a Recovery Rebate check (or direct deposit) but, rather, will have to wait until her 2020 income tax return is filed to have it applied.

Now I ask you… How does that possibly help Georgia now, when she is at the greatest need? (Hint: It doesn’t.) And given the fact that just yesterday it was announced that nearly 3.3 million (!) people filed for unemployment between March 15th and March 21st, it’s likely that there are a lot of ‘Georgia’s' out there!

Of course, while many taxpayers are likely to see income decreases in 2020 as compared to previous years, some will surely see their incomes rise. And for some, that might mean that they get a check for a Recovery Rebate now that they don’t really ‘deserve’ based on their ultimate 2020 income.

Perhaps surprisingly, there will be no clawback on the ‘excess payment' when they file their 2020 return. Such (lucky) individuals get to keep their recovery rebate!

Example #3: Sunny is a toilet paper distributor who files a joint return and has four children under the age of 10. Therefore, he has a potential Recovery Rebate of $4,400.

In 2019, the most recent year for which a return is on file with the IRS, he and his wife had AGI of $130,000, well below their threshold amount of $150,000. As such, the IRS will send Sunny a check for $4,400, his maximum potential rebate amount.

Suppose, though, that due to a large increase in the demand for toilet paper in 2020, Sunny has his best year ever, and he and his wife have $240,000 of AGI. Despite the fact that they are well above the income phaseout range, they get to keep the $4,400 Recovery Rebate, further enhancing what is, at least from an income perspective, already an excellent year for the couple.

(Nerd Note: While the filing deadline for 2019 income tax returns has been extended to July 15, 2020, those taxpayers whose incomes were low enough in 2019, but not low enough in 2018, to receive a Recovery Rebate advance now, may wish to file their 2019 return as soon as possible to try and get it in before the IRS calculates the current payment amount. There is currently no information available on when the ‘drop-dead’ date for such a submission will be, so the sooner, the better!)

And, of course, income is far from the only thing that may change over time. For example, there were about 3.8 million children born in 2019 that won’t show up on a 2018 return, but for whom parents may be entitled to a $500 Recovery Rebate. Marriages and divorces have occurred, and people have died.

All of these may result in Recovery Rebate payments (or lack thereof) that are being received now ending up being dramatically different than the ‘real´ Recovery Rebate an individual is entitled to based on their 2020 facts and circumstances, and that won’t be sorted out until the 2020 return is filed.

Where And When Recovery Rebate Advances Will Be Paid

The urgency with which some taxpayers need income cannot be overstated. For them, the Recovery Rebate cannot come soon enough. Unfortunately, it’s likely to be at least a month, if not more, before such payments will actually be received. The CARES Act requires that these payments be made as soon as possible, but early indications from the Treasury Department are that “as soon as possible” may not be until sometime in May.

As for where the Recovery Rebate payments will be made, it depends. It appears that individuals receiving Social Security benefits will receive their Recovery Rebate in the same account they receive their Social Security benefits. The CARES Act also authorizes Recovery Rebate payments to be made to the account into which a taxpayer’s 2018/2019 refund was deposited. Other payments will be sent to the last known address on file.

No doubt, this raises potential issues of its own. For instance, what happens if a client had their 2018 refund direct deposited into an account which is no longer active? Or what happens if a taxpayer has moved since they filed their last return? In such instances, tracking down ‘lost’ Recovery Rebate payments may be a bear, as the CARES Act indicates that the IRS will provide a phone number for individuals to report such issues.

Coronavirus-Related Distributions

Mirroring similar relief that has been provided to individuals in Federally declared disaster areas in the past (for things like hurricanes, wildfires, and floods), the CARES Act creates Coronavirus-Related Distributions. Coronavirus-Related Distributions are distributions of up to $100,000, made from IRAs, employer-sponsored retirement plans, or a combination both, which are made in 2020 by an individual who has been impacted by the Coronavirus because they:

- Have been diagnosed with COVID-19;

- Have a spouse or dependent who has been diagnosed with COVID-19;

- Experience adverse financial consequences as a result of being quarantined, furloughed, being laid off, or having work hours reduced because of the disease;

- Are unable to work because they lack childcare as a result of the disease;

- Own a business that has closed or operate under reduced hours because of the disease; or

- Meet some other reason that the IRS decides to say is OK.

Given the laundry list of potential individuals who may qualify for relief under this provision, it seems rather clear that Congressional intent was to make this provision broadly available. The IRS will likely operate in kind, and take a liberal view of who has been impacted by the Coronavirus enough to qualify for a Coronavirus-Related Distribution.

There are a number of potential tax benefits associated with Coronavirus-Related Distributions. More specifically, these include:

- Exempt From the 10% Penalty - Individuals under the age of 59 ½ may access retirement funds without the normal penalty that would otherwise apply.

- Not Subject to Mandatory Withholding Requirements – Typically, eligible rollover distributions from employer-sponsored retirement plans are subject to mandatory Federal withholding of at least 20%. Coronavirus-Related Distributions, however, are exempt from this requirement. Plans can rely on a participant’s self-certification that they meet the requirements of a Coronavirus-Related Distribution when processing a distribution without mandatory withholding.

- Eligible to be Repaid Over 3 Years– Beginning on the day after an individual receives a Coronavirus-Related Distribution, they have up to three years to roll all or any portion of the distribution back into a retirement account. Furthermore, such repayment can be made via a single rollover, or multiple partial rollovers made during the three-year period. Finally, if distributions are rolled using this option, an amended return can (and should) be filed to claim a refund of any tax paid attributable to the rolled over amount.

- Income May Be Spread Over 3 Years – By default, the income from a Coronavirus-Related Distribution is split evenly over 2020, 2021, and 2022. A taxpayer can, however, elect to include all of the income from a Coronavirus-Related Distribution in their 2020 income.

(Nerd Note: Although, in general, spreading the income of a retirement account distribution over three years is likely to result in a better tax outcome than including all the income in just a single tax year, that may not be the case now. Notably, if an individual is experiencing significant financial difficulty and, to meet expenses, they take a Coronavirus-Related Distribution, it likely indicates lower-than-normal income, at least temporarily, for 2020. If higher income is expected in future years as life returns to ‘normal’, it may be best to include all the income on 2020’s return. Plus, as an added bonus, if some or all of the distribution is later rolled over within the 3-year repayment window, it’s only one tax return to amend!)

Enhancements To Loans From Employer-Sponsored Retirement Plans

Many employer-sponsored retirement plans, such as 401(k)s and 403(b)s, offer participants the option of taking a loan of a portion of their retirement assets. For individuals who have been impacted by the coronavirus (using the same definition as outlined above for Coronavirus-Related Distributions), the CARES Act enhances the ‘regular’ plan loan rules by allowing (but not requiring) plans to relax such rules in the following three ways:

- Maximum Loan Amount is Increased to $100,000 – In general, the maximum amount that may be borrowed from an employer plan is $50,000. The CARES Act doubles this amount for affected individuals.

- 100% of the Vested Balance May Be Used – In general, once an individual has a vested plan balance that exceeds $20,000, they are only eligible to take a loan of up to 50% of that amount (up to the normal maximum of $50,000). The CARES Act amends this rule for affected individuals, allowing them to take a loan equal to their vested plan balance, dollar-for-dollar, up to the $100,000 maximum amount.

- Delay of Payments – Any payments that would otherwise be owed on the plan loan from the date of enactment through the end of 2020 may be delayed for up to one year.

Required Minimum Distributions Are Waived In 2020

Section 2203 of the CARES Act amends IRC Section 401(a)(9) to suspend Required Minimum Distributions (RMDs) during 2020. The relief provided by this provision is broad and applies to Traditional IRAs, SEP IRAs, and SIMPLE IRAs, as well as 401(k), 403(b), and Governmental 457(b) plans. Furthermore, the relief applies to both retirement account owners, themselves, as well as to beneficiaries taking stretch distributions.

In one somewhat surprising twist, the CARES Act not only eliminates RMDs for 2020 but any RMD that otherwise needed to be taken in 2020. More specifically, individuals who turned 70 ½ in 2019, but did not take their first RMD in 2019 (and thus, would have normally been required to take such a distribution by April 1st, 2020, as well as a second RMD for 2020 by the end of 2020) do not have to take either their 2019 RMD or their 2020 RMD! Thus, these procrastinators get to escape two RMDs instead of just one!

However, it is worth noting that while Required Minimum Distributions are suspended for 2020, voluntary distributions are still allowed, including Qualified Charitable Distributions (QCDs) for IRA owners and IRA beneficiaries age 70 1/2 or older. And while such a distribution would not, for 2020, offset any amount of a taxpayer's RMD (because they don't have one), it still allows an individual to use entirely pre-tax dollars to satisfy their charitable intent.

Returning Unwanted 2020 RMDs That Have Already Been Distributed

Despite the fact that we’re not quite yet through the first quarter of the year, a number of individuals have already taken their RMDs – or at least, what they thought was their RMD at the time – for 2020. Now, in light of the CARES Act, these individuals may wish to ‘return’ unwanted and no longer necessary RMDs.

For IRA, 401(k), and other retirement account owners, this may be possible in two different ways. In a best-case scenario, the ‘RMD’ distribution will have taken place within the last 60 days, and the distribution won’t be prevented from being rolled over due to the once-per-year rollover rule (either because it came from a plan, is going to a plan, or because no IRA-to-IRA rollover has been made within the past 365 days). In such instances, an individual can simply write a check, or otherwise transfer an amount equal to the ‘RMD’ back into a retirement account before the end of the 60-day rollover window.

Additionally, in April 2020, the IRS released Notice 2020-23, which extends the 60-day rollover rule for distributions taken on or after February 1, 2020 to the later of 60 days after receipt of the distribution, or July 15, 2020. Thus, only 2020 distributions taken in January are outside of their applicable rollover window.

For retirement accounts owners who took their RMD very early in the year, and for whom the 60-day rollover window has already expired, there is another potential approach. If it can be shown that the individual has been impacted by the COVID-19 crisis enough to qualify under the liberal guidelines outlined earlier for a Coronavirus-Related Distribution, then the rollover can still be completed… anytime for the next three years (from the date the distribution was received)!

Notably, while most benefits in the CARES Act are only available for actions occurring either after the President declared a national emergency or, in other cases, the enactment of the law, the Coronavirus-Related Distribution provision can apply to distributions as early as January 1, 2020! (Tip o’ the hat to Jamie Hopkins for thinking this one up!)

But what about beneficiaries who took RMDs already? Is there any relief for them? Unfortunately, the answer is no. A beneficiary is not eligible to make a rollover. Period. As such, even if the distributed RMD was made within the last 60 days, there is no way to get it back into the inherited retirement account.

(Nerd Note: The lone exception for beneficiaries would be for a spouse who chose to remain a beneficiary of the deceased spouse’s retirement account. In such an instance, they may be eligible to put the RMD back into their own retirement account, as a spousal rollover, using one of the methods described above.)

2020 Is Ignored For Purposes Of The 5-Year Rule

A final item addressed by the CARES Act’s suspension of RMDs for 2020 is the way it impacts the 5-Year Rule that applies to Non-Designated Beneficiaries (e.g., charities, estates, non-See-Through Trusts) who inherit a retirement account from decedents who die prior to reaching their required beginning date.

In general, such beneficiaries must distribute the entirety of their inherited assets by the end of the fifth year after the retirement account owner’s death. The CARES Act, however, allows 2020 to be ignored, or simply not counted as one of those five years. Thus, for Non-Designated Beneficiaries subject to the 5-Year Rule who inherited from a decedent dying between 2015 – 2019, the 5-Year Rule is effectively a 6-Year Rule!

(Nerd Note: Many individuals have been inquiring whether a similar extension of time applies to the new 10-Year Rule imposed by the SECURE Act on Non-Eligible Designated Beneficiaries. The answer is, “No.” Recall that 2020 is the first year that an individual could have died with and had a beneficiary subject to the 10-Year Rule. And the 10-Year Rule does not actually begin until the year after the year of death. Therefore, 2020 doesn't count as 1 of the 10 years for purposes of the 10-Year Rule!)

Temporary New $300 Above-The-Line Deduction For “Qualified Charitable Contributions”

Having recently removed many of the above the-line-deductions via the Tax Cuts and Jobs Act (TCJA) in the interest of simplicity (at least that’s what they said), Congress promptly introduces a brand-spanking-new above-the-line deduction in the CARES Act for Qualified Charitable Contributions made to qualifying charities.

As with many things, when it comes to taxes, there is both good news and bad news. The bad news is that the deduction, which is effective for tax years beginning in 2020 only (as clarified by a report from the Joint Committee on Taxation), is limited to a whopping (note copious amounts of sarcasm) $300. Even for a taxpayer in the highest tax bracket of 37%, that still ‘only’ amounts to an actual tax-bill-savings of $111. Every little bit helps, but it’s hardly going to be a windfall for anyone, as for a taxpayer in the 12% bracket, the ‘full’ deduction would amount to $36 of tax savings.

The good news, though, is that while the impact on an individual basis may not amount to much, a substantial number of people will be able to take advantage of this not-so-substantial benefit. That’s because, in order to claim the deduction, a taxpayer cannot itemize deductions on their Federal return. But thanks to the TCJA’s near-doubling of the standard deduction, only about 10% of taxpayers today itemize deductions on their Federal return… which means about 90% of taxpayers can potentially benefit from this new tax break in at least some way!

Notably, Qualified Charitable Contributions must be made in cash. And they cannot be used to fund either donor-advised funds (DAFs) or 509(a)(3) “supporting organizations”.

(Nerd Note: Many individuals have been inquiring whether a similar extension of time applies to the new 10-Year Rule imposed by the SECURE Act on Non-Eligible Designated Beneficiaries. The answer is, “No.” Recall that 2020 is the first year that an individual could have died with and had a beneficiary subject to the 10-Year Rule. And the 10-Year Rule does not actually begin until the year after the year of death. Therefore, 2020 doesn’t count as 1 of the 10 years for purposes of the 10-Year Rule!)

AGI Limit For Cash Charitable Contributions Temporarily Repealed

Section 2205 of the CARES Act temporarily increases the AGI limit on cash contributions made to charities from a maximum of 60% of AGI (previously increased from 50% by the TCJA), to a maximum of 100% of AGI for “qualified contributions”. As such, an individual can completely wipe out their 2020 tax liability with charitable contributions. If total charitable contributions exceed the 2020 100%-of-AGI limit (so, effectively, once a taxpayer has brought their 2020 income tax liability to $0), the excess may be carried forward as a charitable contribution for up to 5 years.

Notably, though, like Qualified Charitable Contributions, this provision expressly prohibits such contributions from funding either donor-advised funds (DAFs) or 509(a)(3) “supporting organizations”.

Relief For Student Loan Borrowers

The CARES Act includes several provisions aimed at providing relief to student loan borrowers, including the following:

Student Loan Payments Deferred Until September 30, 2020 – Section 3513 suspends required payments on Federal student loans though September 30, 2020. During this time, no interest will accrue on this debt. Unfortunately, though, while required payments are suspended, voluntary payments are not prohibited. And by default, payments will continue unless individuals take proactive measures to contact their loan provider and pause payments.

Also notable is that this period of time will continue to count towards any loan forgiveness programs. As such, any student borrower who intends to qualify for a program that will ultimately forgive the entirety of their Federal student debt (such as via the Public Service Loan Forgiveness program) should immediately pause payments. Because whereas other borrowers who continue to pay Federal student loans during this time may simply be paying down what is effectively 0% debt (at least temporarily), those borrowers who will ultimately have their outstanding student debt forgiven (upon completion of whatever requirements are necessary for their particular loan forgiveness program) are paying down a debt that would otherwise be wiped clean anyway!

Finally, all involuntary debt collections are also suspended through September 30, 2020. This not only includes wage garnishment or the reduction of other Federal benefits but the reduction of any tax refund (for student loan purposes). As such, borrowers of student debt who are delinquent on payments and would normally be subject to a reduction of their tax refund have an incentive to file their tax returns early enough so that the refund is processed before this relief expires.

Employers Can Exclude Student Loan Repayments From Compensation – Section 2206 provides employers a (very) limited window of time in which they can take advantage of a special rule to aid employees paying down student debt. In general, amounts paid by an employer to an employee which are used to pay student debt (or payments made by an employer directly to the loan provider) are considered compensation to the employee and are subject to income tax.

Under Section 2206, however, employers have from the date of enactment of the law, through the end of the year, to provide employees with up to $5,250 for purposes of student debt payments and exclude those amounts from their income. This amount, however, is coordinated with the ‘regular’ $5,250 limit that employers can provide employees tax-free for current education. As such, the total maximum tax-free education assistance an employer can provide an employee in 2020 is $5,250.

Pell Grant and Subsidized Federal Student Loan Relief For Students Leaving School – Both Pell Grants and Subsidized Federal Student loans are subject to various limits. Section 3506 of the CARES Act excludes from a student’s period of enrollment any semester that a student does not complete due to a qualifying emergency. Section 3507 does the same with respect to the Federal Pell Grant duration limit.

Curiously, both provisions are contingent upon the Secretary of Education being “able to administer such policy in a manner that limits complexity and the burden on the student.” Upon first glance, these provisions would appear to create far more “burden” for the Secretary of Education than they do on the student!

Finally, if a student withdraws from school during the middle of a semester (or equivalent) because of qualifying emergency, Section 3508(b) eliminates the amount of a student’s Pell Grant that would normally have to be returned, while 3508(c) cancels any Direct loan that was taken to pay for the semester.

Definition Of Qualified Medical Expenses For Certain Tax-Favored Accounts Is Expanded To Include Over-The-Counter Expenses

Per Section 3702 of the CARES Act, beginning in 2020, the definition of qualified medical expenses, for purposes of Health Savings Accounts (HSAs), Archer Medical Savings Accounts (MSAs), and Healthcare Flexible Spending Accounts (FSAs) is expanded to include over-the-counter medications.

Qualified medical expenses for such accounts are further expanded to include amounts paid for “menstrual care products”, which are defined as “a tampon, pad, liner, cup, sponge, or similar product used by individuals with respect to menstruation or other genital tract secretions.’’

Other Select Provisions Related To Individual Healthcare

It should come as no surprise that the CARES Act is absolutely loaded with health-related provisions (it is, of course, being passed in response to what is likely the single greatest health-related event of most Americans’ lives). With that in mind, other notable personal healthcare provisions include the following:

- Medicare Beneficiaries will be eligible to receive the COVID-19 vaccine (when available) at no cost (Section 3713);

- During the COVID-19 emergency period, Medicare Part D recipients must be given the ability to have, upon request, up to a 90-day supply of medication prescribed and filled (Section 3714);

- Telehealth services may be temporarily covered (through plan years beginning in 2020) by an HSA-Eligible HDHP before a participant has met their deductible (Section 3701); and

- Rules for providing Telehealth services are relaxed during the COVID-19 emergency period for Medicare (Section 3703), Federally Qualified Health Centers (FQHCs) and Rural Health Clinics (RHCs) (Section 3704), Home Dialysis (Section 3705), and Hospice Care Recertification (Section 3706).

A Cornucopia Of Additional Unemployment Compensation Benefits

Almost immediately, it was clear that the social distancing policies, limitations on gatherings of large groups, and, in the areas hit the hardest by COVID-19 crisis, government-ordered lockdowns would have a dramatic impact on businesses and their ability to retain workers.

That expectation proved a reality yesterday, as the number of individuals applying for unemployment in the most recent (weekly) period jumped to nearly 3.3 million, a figure so high it is an order of magnitude higher than anything seen in generations!

For the many who have already lost their jobs, and for the countless more who will likely find themselves subject to the same fate in the coming weeks, there is, thankfully, some (relatively) good news. Unemployment compensation benefits have been significantly expanded by the CARES Act. These enhancements include:

Pandemic Unemployment Assistance – Self-employed individuals (who are generally ineligible for unemployment compensation benefits), and other individuals who are ineligible for ‘regular’ unemployment, extended unemployment or pandemic unemployment insurance, or run out of such insurance, will be eligible for up to 39 weeks of benefits via this provision.

Uncle Sam Will Cover Unemployment for the First Week of Unemployment – In general, individuals are ineligible to receive unemployment benefits the first week that they are unemployed. It essentially amounts to an elimination period that’s meant to encourage people to try and get another job quickly so as to avoid the week without income. Of course, at the present time, finding work quickly will be difficult, if not impossible. And in recognition of this fact, the CARES Act offers to pay states to provide unemployment compensation benefits immediately, without the ‘normal’ one-week waiting period.

‘Regular’ Unemployment Compensation is ‘Bumped’ by $600 per Week – Section 2104 of the CARES Act provides states with the ability to increase their unemployment benefits by up to $600 per week with Federally-funded dollars, for up to four months. This has the ability to dramatically increase the amount of money an individual is entitled to temporarily receive via unemployment compensation benefits, as the average weekly unemployment benefit nationwide is under $400! Thus, many individuals will see their unemployment checks increase by 150% or more, thanks to this part of the CARES Act.

(Nerd Note: It’s this part of the bill that briefly stalled the legislation in the Senate, as concern was raised by some legislators that, with enhanced payments, some individuals would actually make more collecting unemployment insurance than they would be by returning to work. Certainly, a fair concern, but one that was ultimately able to be seen past in an effort to move the bill forward and get aid to those who need it.)

Unemployment Compensation is Extended by 13 Weeks– In the event that people are nearing – and ultimately reach – the maximum amount of weeks of unemployment compensation provided under state law, Section 2107 of the CARES Act will allow them to receive such benefits for an additional quarter.

Incentives to Create Short-Time Compensation Programs – Section 2108 of the CARES Act provides an incentive for states who do not currently have “short-time compensation” programs to establish such programs by covering 50% of the establishment costs incurred through the end of the year. Short-time programs are meant to help those employees who have seen hours cut (or similar cuts) and have had income drop, but who are still employed, and therefore, ineligible for unemployment compensation benefits.

Paycheck Protection Program And Forgivable Loans

Another significant potential benefit included in the CARES Act for ‘small’ business owners is the Paycheck Protection Program, a (partially) forgivable loan program offered through the Small Business Administration (SBA). Such loans – which were so popular after the CARES Act was initially passed that the program ran out of funds, only to be ‘refilled’ by Congress via subsequent legislation in April 2020 – must be applied for by June 30, 2020, and can have a maturity of 2 years. They may be provided via existing approved SBA lenders, as well as lenders who are otherwise certified by the SBA to offer such loans. Furthermore, such loans will be 100% guaranteed by the SBA.

Qualifying For The Paycheck Protection Program

Businesses, including sole proprietorships, that have fewer than 500 employees (including affiliated businesses), or the employee size standard under NAICS Code, if larger, are eligible for this relief (food service businesses also apply if they employ fewer than 500 people per physical location). Eligible borrowers are also required to make a good-faith certification that the loan is necessary due to the uncertainty of current economic conditions caused by COVID-19 (though under a recent safe harbor announced by the U.S. Treasury via FAQs, the certification for any loan equal to or less than $2 million will be deemed valid).

Under the Paycheck Protection Program, lenders will generally be able to issue SBA 7(a) small business loans up to a maximum of the lesser of $10 million, or 2.5 times the average monthly payroll costs over the previous year (excluding annual compensation of amounts over $100,000 per person), plus the amount of certain refinanced Economic Injury Disaster Loans. And the proceeds of such loans may be used to pay a variety of costs, including:

- Payroll costs

- Group health insurance premiums and other healthcare costs

- Salaries and/or commissions

- Rent

- Mortgage interest (excluding amounts pre-paid)

- Utilities

- Other business interest incurred prior to February 15, 2020

Benefits Of Loans Issued Under The Paycheck Protection Program

The single largest potential benefit of a loan issued under the Paycheck Protection Program is the possibility of having all or a portion of the loan forgiven. The amount eligible to be forgiven is the amount spent, during the first 8 weeks after the loan is made, on:

- Payroll costs, excluding prorated amounts for individuals with compensation greater than $100,000;

- Rent pursuant to a lease in force before February 15, 2020;

- Electricity, gas, water, transportation, telephone, or internet access expenses for services which began before February 15, 2020; and

- Group health insurance premiums and other healthcare costs.

If this sounds too good to be true, it won’t surprise you to learn that there is a catch. In order for the above amounts to be forgiven, the business must maintain the same number of employees (equivalents) in the eight weeks following the date of origination of the loan as it did during other specified periods (generally from either February 15, 2019, through June 30, 2019, or from January 1, 2020 through February 29, 2020, but different dates may apply to certain seasonal businesses). To the extent this requirement is not met, the amount eligible for forgiveness will be reduced, ratably. Additional reductions in the amount to be forgiven will be incurred if employees with under $100,000 of compensation have their compensation cut by more than 25% as compared to the most recent quarter.

And as if this benefit wasn’t good enough, it actually gets even better! Any debt forgiven pursuant to this provision is not included in taxable income for the year.

Second, the maximum interest rate that can be charged for a loan made under this program is 4%. Small businesses tend to be risky borrowers, so the ability to borrow up to $10 million at no more than 4%, and over a term of up to 10 years, is a pretty significant ‘win’ for many small businesses in and of itself!

Finally, payments for loans made under the Paycheck Protection Program will be deferred for a period of no less than six months and no longer than one year. Additional guidance will be provided to lenders within 30 days of enactment to further elaborate on the 6-to-12-month deferment period.

New “Employee Retention Credit For Employers Subject To Closure Due to COVID-19”

The economic fallout as a result of the COVID-19 epidemic is unprecedented. As businesses have shuttered their doors or cut back on hours or services, individuals have been laid off in record numbers. As an incentive to encourage businesses who have been hit hard by the economic effects of the COVID-19 crisis from making further layoffs, Section 2301 of the CARES Act introduces a new payroll tax credit (provided they are not receiving a covered loan under section 7(a)(36) of the Small Business Act).

Qualifying For The Employee Retention Credit

The ‘trigger’ for a company to begin to be eligible for the credit is that operations of the company have been fully or partially suspended during a quarter either as a result of a governmental authority or in which revenue in 2020 has less than 50% of the revenue from the same quarter in 2019.

As such, a business which is not at least partially suspended because of government restriction, and which never sees its year-over-year quarterly revenues plummet below the 50% mark, will not be eligible for the credit.

For those businesses that do meet this (unfortunate) requirement, the business will continue to qualify for the credit until the earlier of:

- The end of 2020; or

- Depending upon the method of qualification for the credit, there is either a quarter without a government-required suspension of operations, or the quarter following the quarter in which gross revenue from the current quarter exceeds 80% gross revenue from the same calendar quarter in 2019, whichever is sooner.

Notably, for businesses qualifying for the credit based on revenue, by virtue of the fact that at least one quarter’s revenue in 2020 must be more than 50% less than the revenue for the same quarter in 2019, a company experiencing a sustained substantial (but not-substantial-enough) decrease in revenue throughout the year, may never qualify for the credit (as can be shown with company B in the example below).

Meanwhile, as evidenced in the example below, a company that experiences a more temporary, but dramatic decline in revenue, and which actually experiences a much better year overall, may, in fact, qualify for the credit in one or more quarters!

Finally, it’s worth highlighting that the key metric used here is revenue, not profit. Thus, a business with a small profit margin, such as a grocery store (which tend to have margins of less than 5%) that loses ‘just’ 10% or 15% of revenue may, in fact, already be running at a substantial loss without cutting other costs.

Calculating The Employee Retention Credit

For business planning purposes, it is important for employers not only to understand that they are eligible for a credit but also to know how much of a credit they are eligible for, as this will help inform business decisions. In the simplest terms, the credit is equal to 50% of wages paid to each employee, up to a maximum of $10,000 of wages per employee. There are, however, as usual, some important caveats to which business owners must be made aware.

Specifically, businesses with 100 or fewer employees count “wages” very differently from larger businesses. For small businesses (100 or fewer employees), all wages (up to the $10,000 maximum limit per employee) are eligible to count towards the credit. By contrast, for larger employers with more than 100 employees, only wages paid to individuals (up to the $10,000 maximum limit per employee) who are not providing services (not working) during a government shutdown, or because business revenues have declined as outlined above, are eligible to count towards the credit. In both cases, wages include qualified health care expenses allocable to those wages.

Deferral Of Payment Of Payroll Taxes

Section 2302 of the CARES Act provides employers with another payroll-related tax break. With the exception of employers who have debt forgiven by the CARES Act for certain loans provided by the Small Business Administration, employers are eligible to defer payroll taxes from the date of enactment, through the end of the year, until the end of 2021 and 2022.

More specifically, 50% of the payroll taxes that would otherwise be due during this period may be deferred until December 31, 2021. The remaining 50% is due on December 31, 2022.

The good news for self-employed persons is that this relief applies to them too, at least with respect to the ‘employer equivalent’ portion of their self-employment taxes. Accordingly, 50% of an individual’s self-employment taxes, from the date of enactment through the end of 2020, may be deferred, with 50% of that amount (so 25% of 2020 self-employment taxes) due December 31, 2021, and the remaining deferred amount due on December 31, 2022.

Notably, payroll taxes and self-employment taxes fund programs such as Medicare and Social Security, which are significantly underfunded already. To mitigate further impact to these programs, the CARES Act authorizes Congress to appropriate amounts from elsewhere in an amount equal to the deferred amounts that would have otherwise gone into the Trust Funds. And interestingly, there doesn’t appear to be an offset when those deferred payments ultimately do go into the Trust Funds.

So, perhaps Social Security and Medicare actually get a little boost thanks to the CARES Act (which, admittedly, would probably just offset some of the effects of reduced payrolls in 2020)?

Net Operating Loss Rules Are Loosened

Section 2303 of the CARES Act amends the rules for corporations (other than REITs) with Net Operating Losses (NOLs). For many years, NOLs were allowed to be carried back up to two years and forward up to 20 years. The TCJA changed those rules, however, beginning in 2018, to allow such losses only to be carried forward, indefinitely.

Now, the CARES Act adjusts those rules once more, allowing any NOL from 2018, 2019, or 2020 to be carried back up to five years. In theory, this should allow companies to reduce prior years' tax bills, allowing them to claim refunds of amounts previously paid to provide further liquidity to get them through the COVID-19 crisis.

The CARES Act further enhances the ability of companies to use their NOLs to offset prior years' tax liabilities by amending another rule put in place by the TCJA. Under the TCJA, NOLs were only able to offset up to 80% of taxable income. Section 2303 of the CARES Act amends the law to allow for up to 100% of taxable income to be offset for 2018, 2019, and 2020.

Section 2023 also provides relief to non-corporations as well by temporarily repealing TCJA-created IRC Section 461(l), which limits the cumulative losses that a taxpayer may claim attributable to businesses (above the income attributable to those businesses) to no more than an inflation-adjusted $250,000 for single filers, and $500,000 for joint filers. These limits are repealed for 2018, 2019, and 2020. Accordingly, taxpayers who had losses suspended because of this provision in 2018 or 2019 should consider the potential benefits of filing an amended return.

In terms of returning unwanted RMDs, how do the logistics work when a custodian has withheld federal and state taxes from the original distribution? In this example, you are still within the 60 day rollover window. If you do add money back to your IRA and mark it as a 60 day rollover, do you just put in the full amount (before taxes were withdrawn) for now and then true-up when filing your 2020 taxes? Is there a way to work with your custodian to reverse the tax withholdings?

Can anyone clarify this for me? I interpreted the paragraph below as if a client who was of RMD age and met the criteria of a Corona Virus Distribution (created for those who are under 59.5, but need to make a withdrawal) may be able to rollover funds that were taken in January. I have been told that it is likely not possible and those CV Distribution guidelines are only for 59.5 and under and therefore the client is stuck with the RMD distribution no matter what.

“For retirement accounts owners who took their RMD very early in the year, and for whom the 60-day rollover window has already expired, there is another potential approach. If it can be shown that the individual has been impacted by the COVID-19 crisis enough to qualify under the liberal guidelines outlined earlier for a Coronavirus-Related Distribution, then the rollover can still be completed… anytime for the next three years (from the date the distribution was received)!”

Loan Forgiveness Program: Does it mean that a qualifying cost for loan forgiveness purposes also includes the amounts paid to an individual who receives K1 compensation up $100,000 (and for whom payroll taxes are not paid) ?

Almost no one believes that K-1 is included. Unfortunately declared salaries only.

Regarding the $100,000 withdrawal from a retirement account. How about this strategy for somebody who has pre and post dollars in their IRAs…thoughts?

Current Balances:

Trad IRA Pre-tax – $100,000

Trad IRA Post-tax – $15,000

Can we now take out the $100,000 pre tax funds and invest in brokerage to not lose out on possible growth (other than the tax deferral) then convert the post tax funds to Roth avoiding the pro-rata calculation double tax. Then redeposit the pre-tax funds next January?

It would be deemed prorata unless you had a stop over to a 401k/403b/457 en route to taking the distribution, but if you had access to that then you never had an issue with converting post tax basis to begin with, you could have always used the 401k/403b/457 to accomplish that goal.

If you’re laid off, and have a 401k loan, is there anything in the CARES act that deferrs the typical 60-day window where you have to pay it back?

As usual, the self employed individual is the veritable “red headed stepchild” of all such government programs and assistance. I see there is a brief mention of UC benefits for us but no real explanation and no further directions or links of any kind.

Recovery Rebate of $500 for a “qualified child”. Any idea what the reference date is to determine the “qualified child” age? My guess is 12/31/2019, so any child under 17 as of 12/31/2019 would qualify to be counted for that rebate even if 2019 tax return is not yet filed. That at least seems like the easiest way to implement it unless the law specifies differently.

Thank you for this very comprehensive discussion and overview of the CARES Act. It is one of the best overviews I’ve read thusfar.

My question surrounds the calculation of payroll expenses. A plain reading of the act states that salary is capped at a maximum of $100,000/employee per year. However, in calculating payroll expenses the definition is: salary, sick/vacation time, retirement contributions, health care insurance premiums and payment of state and local taxes. The overall payroll expenses do not appear to be capped at $100k/employee.

For those firms or practices with significant retirement contributions, this could be an additional amount that could be borrowed under the Paycheck Protection Act.

I don’t believe there is any relief for a (very) small business owner, no employees, not incorporated. Definitely losing sales due to covid-19. Can anyone enlighten me on this? I’m in Maine. Thanks in advance.

There is relief, you’re self employed. EIBL $10K to everyone. PPP to self employed is based on 2019 net income.

Thanks for this thorough summary of CARES Act provisions! I’m looking for some added clarity on unemployment benefits for a self-employed client in CA. The CA EDD site says to be eligible for unemployment benefits she needs to have paid into the UI system in the previous 5-18 months, but she’s been self-employed for years. Does the DUA need to be triggered for her to get unemployment? Or is the CA EDD site inaccurate? It really seems like she should be eligible. Thanks!

Does this mean that if a client, who does not itemize, makes a QCD of $50,000, the most they can deduct is $300? If so, this really hurts my clients, who I advised earlier this year, to make a QCD, as previously, the amount they donated could be fully deducted from their income (above the line) up to $100,000.

Please clarify. Thanks!

My interpretation:

1) Those who do not itemize can use the $300 above-the-line deduction.

2) Those who itemize can do both. (I am not clear on this point – maybe itemizers will be restricted from using the $300 deduction but that seems rather petty. Technically you would use the $300 above-the-line first and then the remainder as itemized. It is small dollars, but some itemizers would not get an actual tax benefit from the first $300 of charity that is within their standard deduction bucket)

4) The QCD is completely separate. No connection. I do not see any impact from CARES on QCDs. Personally I think Congress should now open up QCDs for those under 70 1/2. There is money there that could go to charity and charities are tremendously disadvantaged financially in this crisis when we really need many of them the most.

5) The only common thread is that neither QCDs, nor the $300 above-the line deduction can be used to contribute to a donor-advised fund.

P. 14 – AGI Limit for Cash Charitable Contributions Temporarily Repealed.

What does that last paragraph mean: “Notably, though, like Qualified Charitable Contributions, this provision expressly prohibits such contributions from funding either donor-advised funds (DAFs) or 509(a)(3) “supporting organizations”.

Does that mean the amount of charity that exceeds the 60% AGI limit cannot go into a DAF?

Does it mean that no cash contributions can go into a DAF?

Appreciated securities can still go into a DAF, correct (assuming there is any appreciation left)?

Jeff, I’ve been a huge fan of your work! One question to anyone who can clarify.. the Nerd Note surrounding the 5 year rule for Inherited IRAs mentions that the 10 year rule under the SECURE Act doesn’t get extended by a year, and the wording had me a little confused. Is the guidance that the first year (2020) doesn’t count at all? If that’s the case, I don’t think it’s an issue of the 10 years not applying, but that no deaths in 2020 get extended, and because it is new, the 10 year rule only has 2020 deaths. Essentially, whether the time frame is 5 or 10 years, if the death occurs in 2020, the time frame is not extended? If I’m getting that right, an estate Inherited IRA (5 year period) set up now from a 2020 death must still be distributed by 12/31/2025? Thanks to Jeff or whomever can clarify!

I have questions on the Paycheck Protection Program. Are you required to keep the employees for the covered period of Feb 15th through June 30th or just the 8 week period after the loan is made? I’m reading other articles that imply you could lay off employees now then apply for the loan in June and re-hire everyone. Is that correct? Also, is the 25% reduction in salary based off previous quarter or previous year?

Thanks for this great analysis. I have a question – I have an adult child who is a dependent college student in 2019, thus no rebate for him. However in 2020 I expect he will NOT be claimed as a dependent. When he files his 2020 tax return, can he claim the $1200 rebate? Or does the fact that he was a dependent in 2019 disqualify him?

Fabulous analysis!

Will the Recovery Rebate get counted as income on your 2020 Federal and State income taxes?

No, it is an advance against a tax credit. Tax credits do not count as income.

Hi, Any info on what required evidence is for Pandemic Unemployment Assistance? I.e., self-employment definition–e.g., folks with 1099s from piece work like musicians?

I already did a rollover from IRA to Roth of some shares that I think are overpunished and oversold but now I see I may have jumped the gun. Now these Coronavirus-Related Distributions seem much better since I could actually use the money and I can roll it back if I changed my mind or if circumstances change again. So if I read this correctly I could take $100,000 in shares from my IRA put it in a taxable account, wait for it to recover, pocket the gains and return back the initial $100,000, can’t I?

Any insight on section 1101 for the EIDL Grant up to $10,000. I’ve seen some people on the internet advising business owners or self-employed to simply apply to get the $10,000 whether they will qualify for a loan or not. What standards does the SBA have to protect against this fraud?

The law appropriates a certain amount of money for each of these programs. For example the Paycheck Protection Program gets $350B. What happens if the total amount requested exceeds this amount? Does the funding expand, or is it first-come, first-serve?

I have a 19 year old son, a college student, and a dependent for 2019 tax purposes. In the article it states “$500 per child up to age 17”. So what is he entitled to? He did file a 2019 tax return.

If he checked the box on his 2019 return saying that someone else can claim him as a dependent, then he’s not going to get any advance payment of the 2020 tax credit. If he did not check the box, then he’ll get $1200 this year. If he did check the box in 2019, but he is not your dependent in 2020, then he’ll get $1200 next year when he files his 2020 return.

Thanks for your response. So…he did check the “dependent” box, so he won’t get anything this year, and I won’t get the $500 since he is over 17. So next year, when I do his taxes, I’ll have to see if not claiming him as a dependent nets us more money than if I do. Good thing it is easy to do “what-ifs” with turbotax.

It is not a choice. If you can claim him then the child’s return still must report “can be claimed on another return”. A dependent claim is not transferable.

Next year, I have a choice. I either claim him or I don’t on my return. I’ll do both his and my returns and see which one is more favorable. My hunch is with college credit and child credit, it will be worth more than the $1200 to claim him as a dependent. If not, I won’t claim him, and he’ll get the $1200 when he files and won’t be a dependent.

Does the Recovery Rebate get counted as income on 2020 Federal and State income taxes?

Are agricultural entities, such as a wholesale plant nursery, eligible for CARES ACT benefits? Or do we have to deal with ag specific programs administered by the Farm Service Agency?

Regarding the RMD holiday: If someone has already executed some QCDs for 2020, could they add that amount back into the IRA and then take the charitable gifts as an itemized deduction?

Likely a smarter move to just leave as QCDs. QCDs are worth more than itemized deductions even if they exceed your RMD for the year.

But to the question, I’d say “probably”.

are RMD’s also waived for inherited IRA’s?

This Kiplinger article says no. https://www.kiplinger.com/article/retirement/T045-C000-S004-coronavirus-stimulus-you-can-wait-to-take-your-rmd.html

Kiplinger article is incorrect. The waiver applies to inherited IRA’s.

This is from Forbes…they are saying no rollover for inherited IRA’s as well.

https://www.barrons.com/articles/the-u-s-should-have-enough-medical-supplies-to-fight-coronavirus-trump-says-51585580076

Yes, but if the beneficiary has already received the RMD for 2020, he/she can’t “undo” the RMD like an account owner could. I think I read that right anyways 🙂

Thanks for this. for clarification—Are those filing as qualifying widows really subject to a $75,000 AGI threshold to qualify for the recovery rebate? Or would it be $112500? Asking as a widow with 2 dependent children.

You say: The applicable AGI threshold amounts are as follows:

Married Joint: $150,000

Head of Household: $112,500

All Other Filers: $75,000

Hi Pam, if you have dependent children then you file as Head of Household.

Yes, $75K for qualifying widows. The bill reads like this:

(1) $150,000 in the case of a joint return,

(2) $112,500 in the case of a head of household, and

(3) $75,000 in the case of a taxpayer not described in

paragraph (1) or (2).

https://www.congress.gov/116/bills/hr748/BILLS-116hr748enr.pdf

(Section 2201)

Great write up! It’s hard to find this depth of reporting and analysis.

I’m wondering if someone qualifies for a coronavirus-related withdrawal from an IRA or 401k, does that have to be a direct withdrawal (ie. turn to cash or a brokerage investment)? Could it be a Roth IRA conversion (sort of like a Roth IRA conversion ladder without a 5-year waiting period)?

I think the only benefit of the corona-virus related withdrawal is for people under 59 1/2 to be able to avoid the 10% penalty on withdrawals. People under 59 1/2 can do Roth conversions anyway without a 10% penalty.

I think the benefit is you can take the 100k distribution and spread the income/taxes over 3 years. Recognize 33.3k/yr as income and then put the 100k back into a Roth. It’s a good time to do a Roth conversion of your shares because the market is down.

Interesting question, but it seems to me that it wouldn’t qualify. If the purpose of the tax “stretch” (if you will) is for relief, then it seems it would only qualify on an actual distribution. Otherwise, there is a glaring Roth conversion loophole there, and the IRS is pretty good about covering those kinds of bases.

I agree. It would probably end up in tax court and who wants to go through that. Maybe a PLR though…….. if someone willing to try :))

This was a question I had as well. Could someone do a large Roth conversion and pay the taxes over three years? Taking advantage of the market being down, and currently low tax brackets to do a large conversion?

Jdm/Skip – yes, that’s what I’m going for. In addition to the reasons you were mentioning, I like the idea of converting $100,000 in year 1 and spreading out the tax liability over 3 years because of the 5-year waiting period on withdrawals from Roths. If you did conversions of $33,333 over 3 years, you’d be waiting until year 8 before you could withdraw the last of that money. I’m not looking to do that, but if I would have done it anyway, I’d rather have access to more money sooner.

I would imagine it has to be a withdrawal, like your RMD. You can’t convert the RMD to Roth; you can only take the distribution or give it away as a QCD.

Another variation?

1. Take a CVD distribution and roll into a Roth, instantaneously for same trustee or within 60 days if by check for trustee-to-trustee.

2. Before 12/31/2020, pay back the CVD with after tax(AT) cash.

Result: effectively transfers AT money into a Roth, of an amount up to the CVD limit. Since the CVD “loan” is opened and closed within tax year 2020, you avoid fronting the larger tax bill as well as avoid clawing it back later(by amending one or more tax returns).

“Beginning on the day after an individual receives a Coronavirus-Related Distribution, they have up to three years to roll all or any portion of the distribution back into a retirement account.”

Wondering if the conversion is disallowed because the Roth is considered a retirement account

While the article says “a retirement account”, the actual text of the law limits you to rolling it into an account that would otherwise be allowed under the Internal Revenue Code to receive a rollover from the original account. A Roth IRA cannot receive a rollover from a non-Roth account.

I do think if you have a 401(k) with high expense ratios or limited investment choices that you can’t rollover while currently employed, then you might be able to use this provision to get $100K out and into a regular IRA.

There are counter examples to “A Roth IRA cannot receive a rollover from a non-Roth account.”:

– TIRA->Roth, aka “backdoor Roth”

– 401k(after tax subaccount)->Roth, aka “mega backdoor Roth”

Both are well known and utilized for years, including myself.

The question I pose is the validity of TIRA(CVD)->Roth and payback with after tax $->TIRA(CVD)

“The question I pose is the validity of TIRA(CVD)->Roth and payback with after tax $->TIRA(CVD)”

See section 2202 of the CARES Act. You have to take the CVD as a normal withdrawal, not as a Roth Conversion, so you have no way to do the first step of your plan “TIRA(CVD)->Roth”.

Unfortunately, this doesn’t work and neither do any of the other Roth conversion strategies. You either do a Roth conversion or, if there isn’t money going from your Traditional IRA to a Roth IRA, it’s a Roth contribution subject to eligibility requirements. You can’t do a Roth conversion for $100,000 and then later decide you want to switch to a $100,000 Roth contribution. That’s effectively what you would be doing here and you’re not allowed to make $100,000 Roth contributions. It’s the same reason why you can’t do a Roth conversion and pay the tax over 3 years – because that’s not a conversion – it’s a $100,000 Roth contribution.

The context is TIRA->RothIRA conversion, aka backdoor Roth, which anyone can do and is not subject to the MAGI cap.

The question is if the “distribution” in CVD excludes or includes “conversion” in RothIRA conversion.

Thanks for the info, Zettai. I like what you’re thinking. I will probably wait to see if the IRS issues guidance before doing anything.

P.S. – That last reply wasn’t from me. Is there another “Jason” in this group?

Maybe a misunderstanding of your question but the conversion, aka backdoor Roth, is not subject to a MAGI cap BUT it is subject to the $6,000 ($7,000) annual limit. That’s the issue here. You can’t make a $100,000 backdoor Roth contribution and that’s the same issue here.

Can a 2019 RMD taken in 2020 be rolled back into an IRA?

I might be getting a little too creative here but if you could prove a Corona-virus related pre-mature 100k withdraw from an IRA (no penalty imposed) and then have 3 years to spread out the taxes on that w/d as the article states , could you then put it back into to a Roth IRA? Essentially doing Roth conversion of 100k and spreading out the taxes over 3 years. Thoughts?

One might also payback the distribution in 3 years from the Roth if age 59 1/2. Then it would be a 3 year tax free loan (because you pay it back), earning 3 years of tax free gains. A planned 2020 Roth conversion should be done irrespective of the 3 year loan in order to harvest the 2020 standard deduction etc.

You are accelerating a distribution, so the only question that matters is “did you trigger tax in a lower income year than you expect to have done in the future?” If your income hasn’t been impacted this year, I don’t know how triggering a taxable distribution would be of benefit when you could take it out in the future at a lower rate.

I agree if you think future tax rates will be the same as they are today…..the lowest since the beginning of the tax code. I would assume future tax rates are going to be higher……. much higher than they are today. Plus the benefits of tax diversification and the estate planning benefits of Tax free Roth inheritance by a non-spouse beneficiary. Your heirs could leave it untouched for a decade of tax free growth.

All very fair points and planning considerations that I agree with. Predicting future rates are impossible, so you need to work with what you have in front of you. If you are saying in the future that we will have elevated income tax brackets to make up for a government shortfall in taxes, we may also have restrictions placed around ROTHs as well. Point is, I would be hesitant to trigger $100k in current income, perhaps pushing myself into a higher bracket, for the sole purpose of a ROTH conversion because I have the option to spread out the payment over 3 years. This is different to me than converting a nondeductible contribution IRA into a backdoor ROTH or a super backdoor ROTH 401k.

Thank you for this timely analysis. One question that I have not seen covered is whether these direct payments will be included in MAGI for ACA eligibility? I understand the payments are not taxable.

No, they are not income and will not affect MAGI for ACA eligibility.

Quoted from above: “Specifically, individuals who had up to $75,000 in adjusted gross income in 2019 will receive a one-time payment of $1,200, while married couples with AGI up to $150,000 will get $2,400.”

What of those whose 2019 returns are still being processed at the time the rebate checks are being mailed? How will the feds know which AGI figure to use in calculating the amount of the rebate checks?

Jasper

They will use your 2018 return. The article mentioned if 2019 is much more beneficial to you than 2018 you should file your 2019 return ASAP. However, I do not know if that will make a difference as it takes time for a submitted return to be processed by the IRS. So, it could well be that a newly submitted return would not be on file when the amount of payment determination is made.

What if joint filers have an AGI >$200K but also have eligible children? Are they phased out entirely? The answer might be in your write-up (which is great, by the way, thanks) but I missed this distinction.

Yes, there is no rebate for a joint return with AGI over $198K, no matter how many children are listed as dependents.

That’s actually not right (and I blame the majority of other articles about this that are poorly written). You first add the $2,400 + ($500 x # of kids), then it starts phasing out at 5% of income over the $150K limit. The chart above shows MFJ w/ 3 children not completely phasing out until $228K.

You’re right. Thanks for the correction.

Amazing! Question on the student loan side of things. “Unfortunately, though, while required payments are suspended, voluntary payments are not prohibited. And by default, payments will continue unless individuals take proactive measures to contact their loan provider and pause payments.”

Where is the text to support the default options for payments unless individuals take proactive measures?

CFPB says the payment suspension is automatic and that no action is needed on the borrower’s part: https://www.consumerfinance.gov/about-us/blog/what-you-need-to-know-about-student-loans-and-coronavirus-pandemic/

The language in the text of the bill also uses the language Shall: https://www.govtrack.us/congress/bills/116/s3548/text Also, it looks to be only for 3 months that are definite and 3 months is up to the secretary. According to this it is section 4513 that the student loan info is in.

In the final bill: https://www.congress.gov/bill/116th-congress/house-bill/748/text the student loan section is Section 3513 and it was changed to Sept 30, 2020.

Thanks for the clarification I see it is 6 months in the final version and I had an old version.

For 2020 RMDs that are delayed, do they then need to be distributed in the subsequent year (much like the delayed RMDs in the first year of eligibility)? In other words, will that mean people are doubling up the RMD in 2021 (or tripling up if they delay their 2019 RMD as well) if they don’t take it in 2020?

No, you don’t have to take the 2020 RMD at any time in the future.

Hi Jeffrey

Two questions:

1. Will those with no tax liability for 2019 still be entitled to the tax rebate for self, spouse and dependent children?

2. If the 2019 first RMD has not yet been taken, I understand this will qualify under the RMD holiday. But will this also apply to the 2020 RMD…so for such an individual will get 2 years of RMD holday?

Thanks for the helpful info!

Can a family who has a household employee paid with W-2 wages and a properly established FEIN benefit from these provisions?

How about caregiver payroll? Example – 24 hour in-home care for elderly or disabled individuals.

Is it safe to assume that what passed the House today is exactly the same?

The other dependent credit is limited to $500 on your normal tax return. If in 2020 I didn’t claim those other dependents would they individually be eligible for the $1200 recovery rebate. If so is it refundable? Does the term “not a dependent of another taxpayer” for recovery rebate eligibility or does it mean not claimed as a dependent? If there is no clawback will a claimed dependent in 2019 able to be unclaimed as a dependent in 2020?

If someone “can be claimed” as a dependent in 2020, whether or not they were claimed, then they won’t be entitled to the $1200 on their 2020 returns. Technically, you can get the $500 in advance based on your 2019 return, and they can also get the $1200 on their 2020 returns if they’re now independent, and you won’t have to pay back the extra $500. However, the $500 is only for children under age 17, so there won’t be too many legitimate cases of a kid who was 16 in 2019 becoming independent in 2020, and I think you might get an inquiry letter from the IRS if you and your kid(s) file that way.

Is there any qualification other than being a business with fewer than 500 employees for the Paycheck Protection loans? Because they can be forgiven, it seems like every small business would want to take one of these whether there was coronavirus hardship or not.

I wonder what my rebate check will be.

My husband passed away in 2018, so I filed a joint tax return for that year. Our AGI did not exceed $150K.

I have not filed my 2019 tax return as a single person yet, so the IRS will not use that.

Will I get $2,400 since I filed a joint return for 2018, or $1,200 since the return indicated that my husband was deceased during that year?