Executive Summary

In the financial planning world, most firms are small businesses that are struggling to get larger, trying to grow the practice by simultaneously competing for the same biggest clients and at the same time serving anyone who is able and willing to pay for financial planning services while slowly raising minimums to become more profitable. In response, many practice management consultants have suggested that financial planners establish a niche to build their businesses, focusing on a smaller market they can dominate rather than a larger market they struggle in. Notwithstanding this advice, few firms have adopted the niche approach, most commonly out of a fear that if they narrow the focus of the practice it will simply lead to fewer clients. Yet the reality is that in other industries, firms are growing like never before by focusing not on the biggest clients and opportunities, but by capitalizing on "the long tail" of smaller, niche segments that can add up to real dollars, and become accessible because of the how the internet facilitates business in the digital age. Is it time for financial planners to similarly adopt the long tail approach?

The Long Tail

The concept of the long tail comes from an article of the same name written in the fall of 2004 by Chris Anderson, which was ultimately expanded into a book as well. The basic idea is that many industries have an opportunity for tremendous profit and success by focusing not on what's most popular, but on selling a large number of niche items, each of which is sold relatively few times but which in the aggregate adds up to a significant volume.

The concept of the long tail comes from an article of the same name written in the fall of 2004 by Chris Anderson, which was ultimately expanded into a book as well. The basic idea is that many industries have an opportunity for tremendous profit and success by focusing not on what's most popular, but on selling a large number of niche items, each of which is sold relatively few times but which in the aggregate adds up to a significant volume.

For instance, as Anderson wrote in the article, then-popular subscription music service Rhapsody made available 735,000 music tracks, and found that every one of its top 100,000 tracks was streamed at least once a month; in fact, this was true for its top 200,000, its top 300,000, and even its top 400,000 tracks. By contrast, a bricks-and-mortar music store at the time might have only carried about 40,000 tracks' worth of music; in other words, Rhapsody continued to see ongoing activity with an incredible number of tracks that traditional music stores didn't even offer, which individually recorded too few sales to be practical, but in the aggregate added up to big business.

And in point of fact, this activity was mirrored in other businesses at the time as well; the average Barnes & Noble physical bookstore carried 130,000 titles, but more than 50% of Amazon's book sales came from outside its top 130,000 titles. The average Blockbuster video rental store carried 3,000 DVD titles, yet 20% of Netflix rentals at the time were outside of the top 3,000 titles (and as Netflix access has grown, demand has shifted further into the tail). More recently, the trend is showing itself in the development of "apps" for mobile devices; by the end of the year, it's estimated that only 1/3rd of the revenue will come from the top 100 apps, with the other 2/3rds coming from the long tail of app developers.

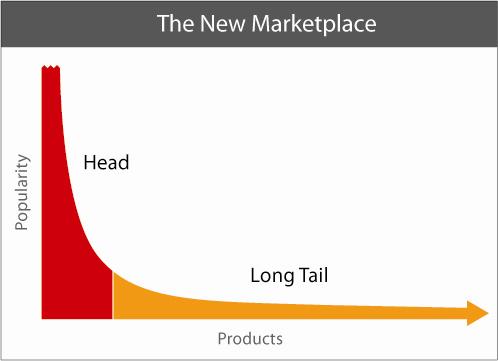

In essence, as shown in the graphic below, the amount of sales activity in the long tail (the orange area) can equal or exceed the activity of "the hits" or the most popular purchases.

Building A Tail Business

For many industries, the big trend of the past decade has been capturing the business opportunities in the long tail - a segment of the market that previously didn't exist. As noted above, more than half of Amazon's book sales come from outside its top 130,000 titles, which was all even a mega bricks-and-mortar bookstore would have carried 10 years ago. Which means that Amazon is generating a huge portion of its revenue not just by outselling and undercutting traditional book retailers in head-to-head competition, but also by creating a marketplace for books that weren't being sold anywhere before. In turn, this also means that authors whose books would have previously languished unread, now at least have some opportunity to find an audience.

What's significant about this phenomenon is that in most industries, there is an excessive focus on trying be at the head of the distribution, when the reality is that the tail has far less competition. Historically, it has been necessary to focus on the head, for the simple reason that if you were in the tail, it was as though you didn't exist at all; if you wrote the 140,000th, 175,000th, and 190,000th most popular books, you didn't see any of your books in a bookstore. But notably, that's no longer true, once Amazon came along and provided a way for them to be sold and reach a target audience. For Amazon, this was good business. For an author in the tail, though, it has created new business opportunities that never existed before. And this new trend is similarly true for those who produce movies that can be found on NetFlix, music than can be found on iTunes, or even those who want to buy other people's "junk" and sell it on eBay.

The Tail Business In Financial Planning

In the financial planning world, the reality is that most firms essentially run a "tail" business. Given the relatively few number of very large firms, and the incredible number of solo practitioners and 2-3 planner partnerships, the majority of financial planning ultimately gets delivered to the public from the tail.

However, many firms operating in the tail try to push themselves towards the head, notwithstanding the fact that the competition is tougher. This is common in other industries as well: movie studios that try to land mega blockbusters instead of "just" making a good, profitable movie; book publishers that hunt for the next bestseller instead of putting out quality titles that generate moderate sales produced at a reasonable cost; recording studios that hunt for the next great star.

Yet the irony is that while most firms tend to try to serve everyone, get the same biggest clients, drive up their minimums, and hunt for big fish in the same bloody ocean, the reality is that since most firms are in the tail, the optimal strategy is actually not to push towards the more competitive head, but instead to differentiate and focus on a clear segment of the tail that the firm can "own" and be dominant!

In turn, this is why it's increasingly viewed as a best practice for financial planning firms to progress towards operating in a niche, rather than trying to do everything for everyone. The niche practice is the tail business; the everything-for-everyone and bigger-and-bigger clients approaches are the most difficult markets to reach. Historically, an excessive focus on the niche would have been dangerous, for the same reason that trying to write books that wouldn't be bestsellers or produce movies that wouldn't be blockbusters was dangerous: if you couldn't make it to the head of the distribution, you might never be found at all.

What's different in today's world, though, is the emergence of the digital age, and the presence of the internet and services like Google that allow consumers to find exactly what they want, that best matches their interest, tastes, or financial planning needs. Just as the internet made niche authors read, niche music heard, and niche movies seen, so too does it create the opportunity for niche financial planners to actually be found, and to thrive in the tail like never before. If a financial planner creates a niche business that might only serve 100 people in the country, the reality is that now the financial planner actually can find those 100 people and work with them (or alternative, can be found by them), creating a successful business for which there is no competition!

So what do you think? Is your business in the head, or in the tail? Where do you want to compete? If your goal was to focus on the tail, how would you market and grow your firm differently?