Executive Summary

The Code of Laws of the United States defines Assisted Reproductive Technology (ART) as “all treatments or procedures which include the handling of human oocytes [eggs] or embryos”. For many individuals and couples with fertility struggles, ART has made biological parenthood possible. According to data from the Centers for Disease Control and Prevention, fertility treatments are on the rise with 284,385 ART cycles performed in the U.S. in 2017, and approximately 1.7% of all live births in the U.S. involve ART. The most common ART procedure is IVF; other procedures include Gamete Intrafallopian Transfer (GIFT), Zygote Intrafallopian Transfer (ZIFT), Intracytoplasmic Sperm Injection (ICSI), and Artificial Insemination.

As ART enables exciting new family opportunities, though, it also presents a number of financial and legal issues. For many, the extremely high costs and limited coverage by insurance companies create a high barrier to access ART procedures, forcing many to pay for treatments out of pocket, which have given rise to the proposal of several pieces of legislation in an effort to help make ART more accessible through insurance coverage. However, despite legislative efforts to expand insurance coverage for ART procedures, there is still no Federal requirement for insurers to provide ART coverage to policyholders. In turn, though, the lack of Federal laws requiring insurers to provide ART coverage has led thirteen states to pass their own “mandate-to-cover” laws (AK, CT, DE, HI, IL, MD, MA, MT, NJ, NY, OH, RI, and WV), and three have passed “mandate-to-offer” laws (CA, TX, LA) for residents and workers in those states. “Mandate-to-cover” laws require that some or all insurance plans have to cover certain fertility treatments, and “Mandate-to-offer” laws require that insurance providers offer certain testing and treatment services (although employers can decide which of those benefits, if any, to offer those covered by their plans). Some of these “mandate” states also carry certain exemptions for costs related to surrogacy, religious employers, and restrictions for same-sex couples.

Financial advisors can offer great value to their clients by reviewing their current health insurance policies and helping them understand whether their coverage includes fertility treatments, especially for individuals and couples living in non-mandate states. Some individuals may have access to coverage for ART procedures through employer-based group coverage, benefits available to government workers or military servicemembers, or public benefits like Medicare. Some employees who reside in non-mandate states, but who have employers with main offices in mandate states, may be able to benefit from the mandate-state policies as well.

A growing number of technology companies like Google, Facebook, and Spotify are also adding ART processes, such as egg freezing and IVF cycles, to their employee benefits packages. Advisors may want to encourage their clients to explore risk-sharing programs, scholarships and grants, and even traveling abroad where fertility treatments are offered at significantly lower cost (at least relative to the pricing of such services in the US).

The costs of ART procedures may also be mitigated by leveraging the tax code. The IRS considers “fertility enhancements” that help the taxpayer “overcome an inability to have children” as deductible medical expenses that can be claimed as itemized deductions (if the usual key thresholds for itemizing medical expense deductions are met). These deduction-eligible fertility enhancements include “procedures such as in vitro fertilization” and “surgery, including an operation to reverse prior surgery that prevented the person operated on from having children.”

Access to employer-provided tax-preferenced savings accounts, such as Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs), may provide additional tax-saving opportunities. A one-time IRA rollover to an HSA, called a Qualified HSA Funding Distribution (QHFD), can also be used to help fund expenses if income or liquidity is low.

Ultimately, the key point is that the cost of ART procedures can be unpredictable and potentially very expensive. While managing the costs of ART may take some creativity, advisors can help their clients successfully navigate the legal and financial complexities to minimize the emotional and financial burdens often experienced by those pursuing fertility treatments.

The Most Common Assisted Reproductive Technology (ART) Procedures and Their Costs

Since the birth of the first baby born via in vitro fertilization in the late 1970s, Assisted Reproductive Technology (ART), defined by the US Code of Laws as “all treatments or procedures which include the handling of human oocytes [eggs] or embryos”, has been widely used to help couples struggling with infertility disorders successfully achieve pregnancy. ART has also been a viable option for same-sex couples desiring to create families, individuals who decide to conceive solo, as well as those who choose to prioritize their careers and delay conceiving a child.

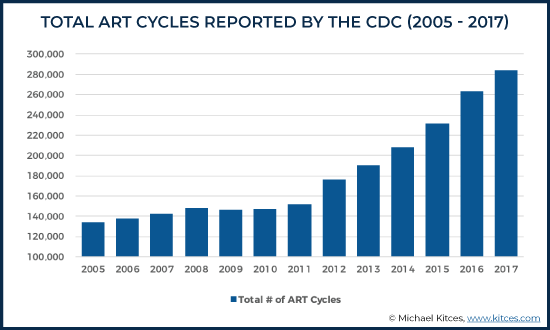

An estimated eight million births have been achieved worldwide through ART and its various modifications, and while ART remains a seldom-considered option despite its increased demand, its use has notably doubled over the past decade. In 2017 alone, the Centers for Disease Control and Prevention reported 284,385 ART cycles performed in the U.S., with approximately 1.7% of all live births in the U.S. resulted from ART in 2017.

In essence, the most commonly used forms of ART involve combining sperm with ova (female eggs) that have been surgically removed from a woman’s body and returning the fertilized eggs (embryos) to the uterus. It can also involve donating the embryo to another woman, man, non-binary person, or couple.

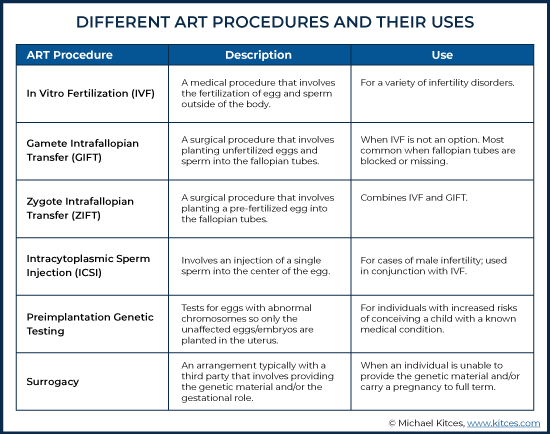

By far, the most dominant form of ART is In Vitro Fertilization (IVF), which involves extracting a woman’s eggs, fertilizing the eggs in a laboratory, and planting the resulting embryos in the uterus through the cervix.

Other ART procedures include:

Artificial Insemination, which involves any method of manually inserting sperm directly into a woman’s cervix, fallopian tubes, or uterus to achieve implantation and fertilization. While some forms of artificial insemination (e.g., intracervical or intrauterine insemination, where sperm is inserted into a woman’s cervix or uterus) are not true in vitro methods, any method that involves the introduction of sperm into a woman’s body, other than through sex, is artificial insemination.

Gamete Intrafallopian Transfer (GIFT) and Zygote Intrafallopian Transfer (ZIFT), which are variations of IVF-based artificial insemination methods that involve placement of the egg and sperm in the fallopian tubes instead of the uterus. With GIFT, unfertilized eggs and sperm are placed in the fallopian tube and fertilization happens inside of the body. Conversely, ZIFT involves the placement of a pre-fertilized egg in the fallopian tubes. Unlike IVF, which is a non-surgical procedure, both ZIFT and GIFT require surgery under general anesthesia and are considered options when IVF fails.

Intracytoplasmic Sperm Injection (ICSI), a technique used in conjunction with IVF methods and in cases of male infertility, when male sperm is unable to penetrate the outer layer of a female egg. It involves the injection of a single sperm into the center of an egg by an embryologist. Once the egg is fertilized, it is grown in a laboratory for 1-5 days before being placed in the uterus through IVF techniques.

Preimplantation Genetic Testing includes procedures used by individuals that have an increased risk for conceiving a child with a known genetic condition, or who want to screen for chromosomal abnormalities. This can be important if there’s a history of a genetic disease in the family or if the genetic history of the egg/sperm donor is unknown. In these tests, a single or a few cells are biopsied from the egg and/or embryos to test for chromosomal abnormalities, so that only the unaffected embryos are transferred to the uterus.

Surrogacy is an arrangement between an individual or couple and a third party called a gestational carrier (the “surrogate”) that can involve ART. The two most common forms of surrogacy are traditional and gestational. A traditional surrogate supplies both the egg, or genetic component, and the gestational role of carrying the pregnancy to term. ART may or may not be involved in this process. With gestational surrogacy, the gestational surrogate supplies no genetic material and simply gestates the provided embryo for the intended parent(s). IVF is always required for this scenario.

ART procedures tend to be an all-consuming process that can take an incredible toll – physically, emotionally, and financially. Access to these treatments can be an expensive proposition, and while competition among service providers may control pricing to some degree, many of the infertility clinics that exist in the U.S. still operate without regulation of cost.

And the cost of ART procedures is very wide-ranging. For example:

For GIFT and ZIFT procedures, the parent(s) can expect to pay $15,000 to $20,000 for each attempt. Other IVF procedures can range, on average, from $12,000 to $15,000 for one single IVF cycle, although a successful conception resulting in pregnancy often takes several IVF cycles.

The introduction of “Mini-IVFs”, which involve less embryo monitoring and lower required doses of fertility drugs, can decrease the price range to ‘just’ $5,000 to $7,000 per cycle.

ART procedures that use artificial insemination can cost an average of $15,000 per cycle depending on the type of procedure used and whether the partner’s sperm or an anonymous donor’s sperm is used.

An ICSI procedure by itself can range from $1,400 to $2,000, but this is on top of the general IVF cost, which on average, adds $12,000 to $15,000. The cost can be even higher depending on the IVF options used.

Gestational surrogacy is by far the costliest, with fees varying based on the needs of the intended parent(s). Overall costs can range between $80,000 to $100,000 if the individual or couple decide to donate their own eggs or embryos. These costs include the IVF procedure, agency fees, compensation and reimbursement to the gestational carrier, attorney and social worker fees, money to cover the carrier’s legal and medical costs, maternity wardrobe, and travel expenses. The total cost may go beyond $150,000 if the intended parent(s) are using donated embryos or genetic material if the IVF procedure involves several embryo transfers, and if unexpected costs arise (which can be incurred by the carrier due to lost wages for bed rest, or needed for housekeeping and child care).

Furthermore, prenatal exams, involving blood work, exams, ultrasounds, and initial and follow-up consultations, can generate additional costs. One woman’s account of her IVF journey included initial prenatal procedures costing approximately $1,000. Other expenses include donated genetic material ranging anywhere from $1,000 to $5,000, and hormonal medications ranging from $3,000 to $5,000. Cryopreservation (egg or sperm freezing) can involve initial costs of $10,000+ in addition to the annual storage costs.

Given all of the expenses involved, not to mention the unpredictable nature of how many attempts it may take to achieve a successful pregnancy, options involving ART procedures may seem out of reach for many aspiring parents.

Health Insurance Coverage Rules for ART

Health insurance companies frequently cite the variable and staggering cost of fertility treatments as a reason for their reluctance to provide coverage for these expenses. Insurers have also argued against considering infertility as an illness, although global health experts like the World Health Organization and the American Medical Association now deem infertility as a disease.

Insurers have also claimed that fertility treatments are not “medically necessary”, essentially asserting that ART is an elective procedure like cosmetic surgery and not necessary to preserve a patient’s health. Another frequent debate against insurance coverage for fertility treatments is that ART procedures are considered “experimental” given their relatively low success rates. According to the CDC 2017 Assisted Reproductive Technology Fertility Clinic Success Rates Report, the percentages of actual egg retrievals resulting in live births were 54% for patients under 35, 41% for ages 35 – 37, 27% for ages 38 – 40, 14% for ages 41 – 42, and 4% for ages 43 and older.

Although there have been efforts by policymakers to introduce legislation that addresses the lack of insurance coverage, no Federal requirement currently mandates insurance coverage for fertility treatments. Consequently, most people end up paying for ART procedures out of pocket, with little help from their insurance providers. According to a FertilityIQ survey of IVF patients in 2018, only 29% of IVF patients had fertility treatment coverage, and 71% had no coverage.

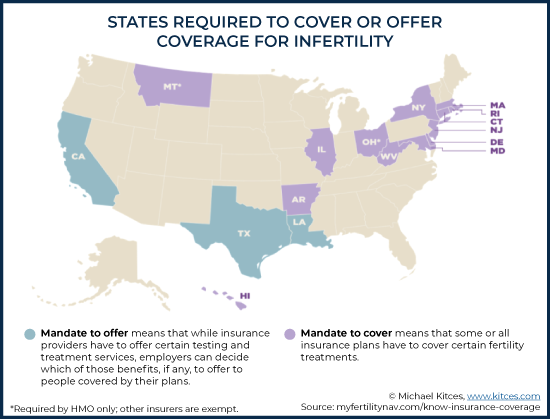

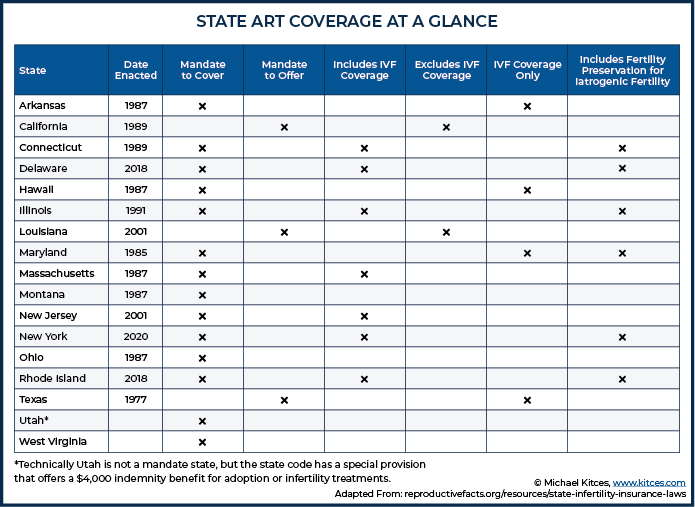

Due to the highly controversial nature of ART and the lack of national consensus, only 16 states — Arkansas, California, Connecticut, Delaware, Hawaii, Illinois, Louisiana, Maryland, Massachusetts, Montana, New Jersey, New York, Ohio, Rhode Island, Texas, and West Virginia – have enacted their own “mandate-to-cover” or “mandate-to-offer” laws.

Of the 16 mandate states, 13 have mandate-to-cover laws. A mandate-to-cover law requires an insurer to cover certain fertility treatments that are specified by individual state legislation. A mandate-to-offer law requires an insurer to let employers know that coverage of infertility treatment can be provided and allows the employer to decide whether to include any of the offered services in their insurance policies. However, it does not require insurers to cover specific fertility treatments or employers to purchase such policies. Three states – California, Texas, and Louisiana – have laws that require insurance companies to offer coverage for ART procedures.

Exactly what procedures an insurance company is willing to cover will depend on the individual state mandate. For example, California, which is a mandate-to-offer state, just passed a law in October 2019 requiring insurers to cover the cost of fertility procedures for cancer patients only. The bill requires coverage for fertility preservation such as sperm banking and egg freezing, but only before receiving any medical treatment that can cause infertility (e.g., chemotherapy). The mandate-to-offer excludes IVF treatments.

New York, a mandate-to-cover state, just passed an updated mandate that requires coverage for “medically necessary fertility preservation treatments (egg freezing and storage) for people facing iatrogenic infertility (infertility caused by medical intervention, such as radiation, medication, surgery, or other medical treatment.” The previous iteration of the law did not consider IVF, GIFT, and ZIFT as corrective treatments for infertility. The new law now requires private insurance carriers to cover up to three IVF cycles for employees covered under a fully-insured, employer-sponsored large group market policy starting January 1, 2020.

Arkansas, another mandate-to-cover state, requires only HMOs to cover the cost of IVF, and with certain restrictions. The state requires “the patient’s egg be fertilized with the spouse’s sperm”, a stipulation that has the propensity to be especially problematic for unmarried individuals and same-sex couples. Notably, many of the mandate states also exempt religious organizations from having to offer or provide coverage. A state-by-state summary of mandates and coverage can be found on the American Society for Reproductive Medicine website.

Because ART procedures can still be cost-prohibitive for many individuals and couples residing in a mandate or non-mandate state, several legislators have recently introduced policy proposals in an effort to make them more accessible through expanded insurance coverage.

As recently as May 2019, former 2020 presidential candidate and New York Senator Kirsten Gillibrand introduced a proposal as part of her presidential campaign called the Family Bill of Rights that would require insurance companies to cover expensive fertility treatments like IVF. The plan aimed to expand access to ART procedures “regardless of income, sexual orientation, religion or gender identity.”

Also in May, New Jersey Senators Cory Booker and Bob Menendez, and Connecticut Senator Rosa DeLauro re-introduced the Access to Infertility Treatment and Care Act, a bill that would require all health plans offered on the group and individual markets (including The Federal Employees Health Benefits Program, TRICARE, the VA, and Medicaid) to provide coverage for the treatment of infertility. The bill, which is in the initial stage of the legislative process, would also require coverage for ART procedures for individuals who undergo a medically necessary procedure that may cause infertility, such as chemotherapy.

Mitigating Healthcare Costs for ART in Non-Mandate States

Helping clients to find their way through the insurance minefield and to minimize out-of-pocket costs for fertility treatments can be a unique planning opportunity for advisors, especially if those clients reside in non-mandate states. While some clients may already have access to health insurance covering ART procedures through their employer (if they generously decide to offer the coverage, although the odds of this are low), advisors can help other clients find policies that do include ART coverage.

There are different ART insurance coverage options for individuals through their employers, depending on whether their existing insurance policies are “fully insured”, “self-insured”, or part of a government or military coverage plan.

A health plan that is “fully insured” means the employer has purchased the coverage from an insurance company, and the insurance company decides what will and will not be covered. While the employer ultimately decides which plan to purchase, they can’t influence what coverage the insurance company offers. Employees in states that don’t mandate coverage, or even mandate an offer to cover, may not have access to any ART coverage simply because no insurance plan in their state offers it.

However, employers with fully insured policies can inquire with their insurance brokers about “IVF Riders” or “Infertility Riders”, which are mini-benefit plans solely for IVF or infertility. If available, an employer can add these riders to their standard benefits plan. It can be worth it for an individual to contact their human resources or benefits administrator about the availability of an IVF rider.

Conversely, plans that are “self-insured” allow the employer full flexibility to dictate what is covered and what is not. If the employer decides to pay for infertility coverage, that coverage would apply to all of their employees across all 50 states, regardless of any state mandates (or lack thereof). This option creates a potential opportunity for those living or working in non-mandate states, as they could obtain access to coverage by working for an employer who voluntarily decides to provide coverage or who is forced to provide coverage by simply being headquartered in a mandate state.

If the client is a federal employee, an advisor can review their health insurance plan under the Federal Employees Health Benefits (FEHB) program to determine whether it offers coverage for ART procedures. As it currently stands, artificial insemination procedures are covered by FEHB Health Maintenance Organization (HMO) plans only, with possible limitations and exclusions. Other ART procedures like IVF may also be covered, depending on the type of coverage included in the FEHB plan (e.g, HMO vs. Fee-for-Service, High-Deductible Health Plan, Point of Service, etc.)

Notably, while it’s atypical for local government employers to offer fertility benefits to its employees, some big cities (e.g., New York, Chicago, and Baltimore) do offer generous benefits to city workers of up to $80,000 annually.

If an individual is under the age of 65 and receiving Medicare due to a disability, “reasonable and necessary” services associated with the treatment for infertility are covered under Medicare. Part B can pay for certain doctors’ services, outpatient care, medical supplies, and some medically necessary fertility treatments, though not IVF (e.g., cryopreservation). Medicare Advantage Part C plans also help cover fertility treatments if those treatments are also covered by Part B. However, Part D plans exclude fertility drugs from their coverage. Some Medigap plans, which are sold by private insurance companies, may offer coverage for IVF, though these plans may be more costly.

Advisors can also assist clients with reviewing their employee benefits package to see if they have access to any non-insurance employer-sponsored fertility benefits. The technology field is increasingly becoming known for its inclusive employment benefits packages, with a growing number of companies including Google, Facebook, and Apple, offering ART-related employee benefits, like oocyte preservation (egg freezing), in a recent push to recruit more women. Facebook, for example, offers fertility benefits of up to $100,000 per employee. Notably, companies like Spotify, eBay, and Tesla pay for an unlimited number of IVF cycles for their employees.

In a 2017-2018 industry study conducted by FertilityIQ, a website that publishes data on fertility treatments, many consulting and audit firms are known for offering excellent fertility benefits with a high percentage of companies paying for IVF, and doing so at lofty dollar amounts of $50,000 on average. Two major players, Bain & Company and Boston Consulting Group, offer an unlimited amount of ART coverage for their employees.

The FertilityIQ study also reported that banking and finance firms offer generous fertility benefits, with many of the large financial institutions like Bank of America and KKR providing unlimited coverage for IVF expenses. On the other hand, the legal field has very few law firms that offer IVF coverage, though the ones that do, such as Ropes & Gray and Skadden, do so generously with unlimited amounts of coverage.

In additional efforts to help subsidize ART-related costs, advisors can suggest that eligible clients explore risk-sharing programs (generally available for women under 40 who have no previous failed IVF attempts) as a potential option through a participating clinic. Given the low success rate of fertility treatments, these programs offer the possibility of a full or partial refund if an IVF treatment is unsuccessful after a certain number of cycles. Typically, one would pay an upfront flat fee for three to six cycles, and the total fee is usually less than what you would pay if you were paying for each of those cycles individually. However, if a person in a risk-sharing program conceives after just one or two cycles, they may end up paying more overall than they would have if they had paid for just one cycle at a time. Conversely, if going through the entire number of cycles results in a person being unable to conceive, the clinic would be required to refund the upfront fee paid. This is why the program is called “shared risk.”

A person choosing to go the route of a multi-cycle “risk-sharing” agreement should have a firm understanding of how the clinic defines “success” and “money-back guaranteed.” The individual should confirm that the clinic defines “success” as a live baby, and not just a positive pregnancy test (which could possibly exclude them from being able to use any remaining cycles for which they already paid, even if the pregnancy ends in a miscarriage).

For low- to middle-income households, there are a number of grants and scholarships available to help make ART procedures within reach. Fertility IQ is an excellent site that lists a plethora of both national and state resources. For example, Starfish Fertility Foundation offers IVF grants to any person in the U.S. without insurance coverage. The Bob Woodruff Foundation offers up to $5,000 to eligible veterans pursuing IVF treatments. Making Miracle Babies provides interest-free loans up to $18,000 to Jewish families in the Miami area.

Aspiring parents might also want to consider taking an “IVF vacation.” Clinics overseas in countries like Japan and Belgium are known for offering fertility treatments at significantly lower cost that can help save thousands of dollars on IVF costs compared to what one would pay in the U.S.

For example, the Fertility Treatment Abroad website reports the average price of IVF treatment in Brazil is $4,000, and in Ukraine – only $1,825. However, pursuing overseas treatments is not without its risks. According to the CDC, one may not have the same degree of legal protection abroad if something were to go wrong. If a person chooses overseas treatment options, they should do their due diligence by checking the accreditation of facilities by organizations such as the Joint Commission International or reviewing the Patients Beyond Borders directory, which includes a list of the top fertility centers worldwide.

Maximizing Potential Tax Benefits To Mitigate ART Expenses

Some of the costs of ART procedures may also be reduced using a variety of financial planning strategies. Fortunately, the IRS views the costs of fertility enhancements as deductible medical expenses, with Publication 502 specifically naming in vitro fertilization when used “to overcome an inability to have children”as an eligible deductible medical expense that can be listed on Schedule A.

Travel costs to the clinic (especially if traveling overseas for treatments), prescription fertility drug copays, and baby delivery costs are also tax-deductible as part of the medical expense deduction.

At least one Private Letter Ruling (PLR 200318017 released in May 2003) granted a taxpayer permission to consider the following surrogacy fees involving an egg donor as deductible medical expenses not covered by health insurance:

- Donor fees for time and expense in following proper egg-retrieval procedures;

- Agency fees for procuring the donor and coordinating the transaction between donor and taxpayer (recipient);

- Expenses for medical and psychological testing of the donor; and

- Legal fees for preparing a contract between the taxpayer and the donor.

Notably, Private Letter Rulings (PLRs) are technically only binding for the individual taxpayers who request them, which means the IRS doesn’t necessarily have to honor the same guidance in the future. Nonetheless, PLRs such as this are often used as an indication of the likelihood that the IRS may stand in favor of allowing similar surrogacy fees as tax-deductible medical expenses in the future, especially in similar-facts scenarios (e.g., that the expenses incurred are “due to an underlying medical condition”).

Additionally, the taxpayer would also have to exceed two key thresholds to deduct any ART-related expenses as medical expenses:

- Total medical expenses (including ART-related and any/all other medical expenses) must surpass 10% of AGI; and

- Total itemized deductions (including the portion of eligible medical expenses in excess of 10% of AGI) must surpass the applicable standard deduction amount ($12,200 for individuals and $24,400 for married couples in 2019; $12,400 and $24,800, respectively, in 2020).

For individuals who itemize deductions, scheduling all fertility cycle treatments and incurring as many of the related costs as possible in a single calendar year will be more likely to push their qualifying medical expenses above these required minimum threshold levels, as expenses can only be deducted in the year paid (and generally not for future medical care that will be received in a subsequent calendar year). If an individual does itemize, only their total qualified medical expenses that exceed the 10 percent of adjusted gross income are tax-deductible.

If someone works for an employer that offers a Flexible Spending Account (FSA), they can utilize the FSA to help pay for qualified ART-related expenses using pre-tax dollars as well. In fact, this option would likely provide a greater benefit than itemizing deductions because of the potential first-dollar-savings benefit (where insurance coverage requires co-pays or co-insurance amounts right away), and the FSA owner would not have to meet the two thresholds required for itemizing the expenses as deductions. An FSA would provide tax savings in two ways:

- Pre-tax payroll elections reduce the amount of taxable income reported on the W2 at the end of the year; and

- Pre-tax payroll elections reduce the amount of income subject to FICA deductions for the employee and the employer (up to 7.65% each).

The drawback of an FSA is that it has relatively low contribution limits, and annual contributions cannot be carried over for use in later years (i.e., if you don’t use it, you lose it). Individuals can contribute up to $2,700 as of 2019 ($2,750 for 2020). Married couples can contribute a total of $5,400 if each spouse has access to their own FSA through their employer. Given the high costs of ART procedures, FSA funds are unlikely to fully cover the costs of fertility treatments in a given year.

FSA balances also don’t roll over from one employer to another, in most circumstances. So if a person has money in an FSA, but switches employers, the money in that account is forfeited. Because of these rules, it is important for individuals to plan their FSA contributions and payments in accordance with their fertility treatments so that they don’t potentially lose money.

A Health Savings Account (HSA) can be an even more powerful tax-advantaged vehicle for paying for fertility treatments. These accounts are reserved for individuals with an HSA-eligible High-Deductible Health Plan (HDHP). HSA owners can create tax savings with tax-deductible contributions of up to $3,500 for 2019 ($3,550 for 2020) to an individual HDHP, and $7,000 for 2019 ($7,100 for 2020) to a family HDHP.

Unlike an FSA balance, though, an HSA balance can roll over year after year and from employer to employer, and contributions can continue to be made as long as account owners are covered by the HSA-eligible HDHP. Funds in an HSA can be invested and grown tax-deferred; while distributions made to pay for qualified health-related expenses are tax-free, distributions are taxable for any other expenses (and are subject to a 20% non-qualified withdrawal penalty if made before the account owner reaches age 65).

If an individual decides to contribute money to the HSA for anticipated ART procedures, they should confirm that their expenses are indeed “qualified” to avoid the 20% non-qualified withdrawal penalty. Qualified medical expenses for HSAs are generally the same expenses that would qualify for medical expense deductions (which includes in vitro fertilization and temporary egg/sperm storage), and must be incurred after the HSA is established. If they’re not careful, they may start using their HSA just to find out that a large portion of their fertility expenses will not be counted as qualified medical expenses.

For someone who does not have sufficient income or liquidity to maximize HSA contributions, a possible source of cash could be their existing IRA, using a one-time qualified HSA funding distribution (QHFD). With a QHFD, a tax-free transfer from an IRA to an HSA can be made during a given year. This transaction is only allowed once-in-a-lifetime and is limited to the HSA’s contribution limit for the given year. The transfer can be made without early distribution penalties from a traditional IRA, an inherited IRA, or an inactive SEP IRA or SIMPLE IRA (any employer contributions “made for the plan year ending with or within the tax year in which the distrubiton would be made” would disqualify a QHFD from a SEP or SIMPLE IRA). However, non-deductible contributions in an IRA cannot be transferred to the HSA; only pre-tax money can be rolled over. The account owner must remain eligible for their HSA for 12 months after making a QHFD; if they lose eligibility, then the QHFD becomes a taxable distribution.

Ultimately, the cost of ART procedures can be very unpredictable; for couples and individuals who decide to pursue fertility treatments, it is unclear how many cycles it will take to conceive a child and how much the process will cost. Even as policymakers and health insurance companies gradually work to improve coverage, those who reside in non-mandate states, are unable to self-finance, or lack access to fertility benefits from their employers may find the process of identifying how to subsidize costs daunting. It may take some creativity, but advisors can offer an excellent value proposition for clients by helping them navigate the financial complexities associated with fertility treatments.

the article has valuable information, very well explained about IVF treatment and its cost

For those that live a “Real Life” with real issues, not “Fake”book or perfect Instagram lives. Can’t wait to share this with those that struggle.

Really good article….Sharing

Thanks for sharing this helpful information for infertility couples. Most of the people are facing infertility problems & too difficult to finding the IVF Centers for IVF / Fertility Treatment near location.

As RN IV, RNC-MNN, CLNC, MBA, RIA, 1L who has attended the deliveries of many an infant in Berkeley, CA and resuscitated many an infant over the years, the delight for all couples to have a child is immense, joyful and gratifying. This post is being shared with my social media for all those infertility couples and not yet infertile couples who are forced to seek out the option of IVF. Should I active pursue my RIA and or join a B/D-Insurance Company after 40 years of nursing, I will act in my client best interest to promote this “rider” for clients in child bearing age(s). What a blessing…Jan

“Thank you for sharing such great information.

It has help me in finding out more detail about art ivf courses“

Absolutely fascinating subject matter. I’ll certainly keep this post bookmarked as a resource for IVF.

Such an informative blog. Thanks for sharing this information.