Executive Summary

It is a simple question: how much does it cost to get a comprehensive financial plan? Yet despite the rising popularity of financial advisors offering financial planning services, remarkably little has actually been published about what financial advisors charge for the service. Which is striking for both consumers – who want to know what a plan might cost – and for financial advisors themselves, who may want to benchmark whether the pricing for their financial plans is “reasonable” relative to their advisor peers and competitors (rather than solely setting the price based on its time-and-labor cost to the advisor).

In our latest Kitces Research survey on “What Financial Advisors Actually Do”, we found that the average cost for a standalone comprehensive financial plan is $2,400 (up from $2,200 in a 2012 study from the Financial Planning Association). Notably, though, our research finds that more and more advisory firms who offer financial plans actually are charging for them separately – rather than merely bundling the plan into their AUM fees – and in fact there is a growing rise of financial advisors who are charging for financial plans solely in a “fee-for-service” manner (hourly fees, monthly subscription fees, or annual retainer fees), rather than blending fees with AUM at all.

In addition, not surprisingly, financial plan fees did vary significantly from one firm to the next, although as it turns out, the biggest driver of financial planning fees is not the cost (i.e., how long it takes) to produce the plan, nor even how comprehensive the plan is, but the affluence of the client themselves paying for the plan in the first place. In other words, clients with more financial means to pay for a financial plan tend to pay more for a financial plan. Opening a debate of whether more affluent clients pay more for financial plans simply because they can afford to do so, because they tend to use more experienced advisors with deeper expertise (even if “the plan” itself is the same), or simply because their higher net worth and affluence means they perceive more value in the financial plan, to begin with.

On the other hand, it’s notable that, because financial advisors only spend about 50% of their time on client-facing activities in the first place, advisors are still greatly limited by how many financial plans they can do and how many clients they can support, which ultimately limits their ability to charge for their time and generate revenue. In the end, the average advisor generates a fee of about $150/hour for their client-facing activities… even as they only spend about 50% of their time on client activities that generate fees in the first place.

On the other hand, the research does indicate that advisors who have advanced professional designations, and more years of experience, do manage to command higher financial planning fees in the marketplace. Though, again, this appears to be less a function of advisors with greater credentials and experience charging higher fees, per se, and more the result of experienced and credentialed advisors being more effective at attracting the more affluent clients who are willing to pay higher fees and perceive greater value in the financial plan in the first place. Which means in the end, when it comes to setting the cost and determining value, the answer to “what should a financial plan cost” truly is in the eyes of the beholder.

How Much Does A Financial Plan Cost?

How much does a financial plan cost? It seems like a relatively straightforward question to answer. In fact, some of you might already be thinking, "Easy, a financial plan normally costs 1% of assets under management," (which is probably not quite the whole truth). But yes, to that point, it is well established that the industry has retained and continues to retain its ongoing love affair with AUM-based pricing. However, this "answer" or this "industry standard" does not honestly or exactingly answer this "simple" question.

Historical Data On How Much A Financial Plan Costs

The leading historical study answering the question “how much does a financial plan cost” was a “Financial Plan Development and Fees” study produced in 2012 by the Financial Planning Association (FPA) and its Research And Practice Institute, which surveyed 527 of its financial advisor members on the financial planning fees they charge their clients.

The FPA Planning Fees study found that, for advisors who charge a flat fee for a comprehensive plan, the median fee charged was $2,250. Advisors who charged an hourly fee had a median of $193/hour, and those who charged retainer fees had a median cost of $2,450/year.

Notably (though not surprisingly), the FPA study found that fees charged appeared to be directly related to the depth of the plan for clients, as comprehensive plans had a median cost of $2,250, while more modular financial plans had a median fee of only $850. Time spent working on a financial plan also mattered. The more time the plan took to develop, the more expensive the plan was, and the average advisor reported having spent 11.9 hours on a single financial plan.

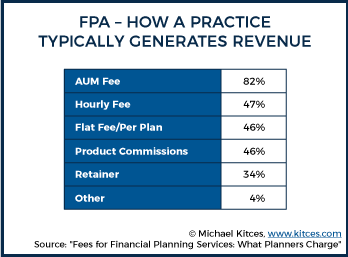

However, the FPA study also noted charging “just a fee” for a financial plan was rather rare, stating that “Assets under management (AUM) fees still reign supreme, with nearly twice as many advisors reporting that their practices use an AUM fee to generate revenue compared with any other revenue method.” Still, though, AUM-centric didn’t mean AUM was the only fee model at play when charging for financial advice. In fact, the FPA report found 82% of advisors reported using an AUM fee, but most of those also had some kind of hourly, flat, or retainer-based financial planning fee structure as well (either separately, or on top of their AUM fee).

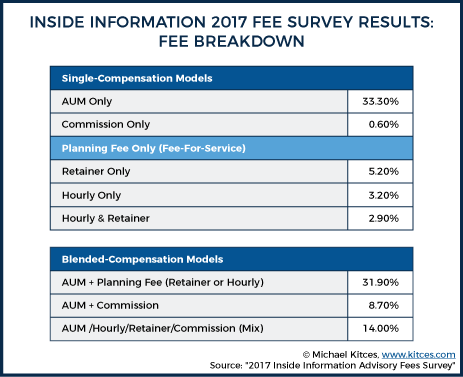

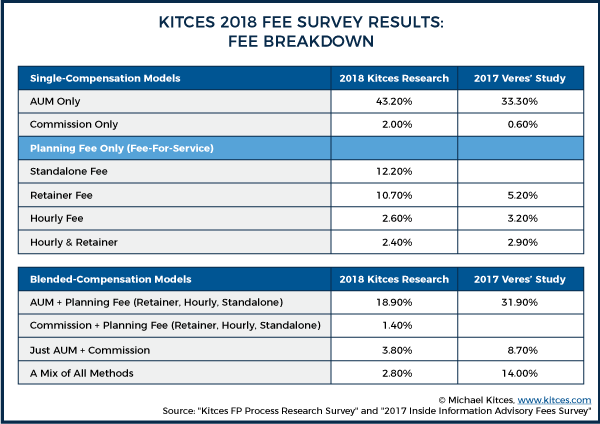

A more recent 2017 study on the fees that advisors charge, by Bob Veres, included 956 advisors at RIAs and broker-dealers and similarly found that while the AUM model remains dominant (even amongst those who deliver financial planning and not “just” investment management), the trend in overlapping fees has continued. Specifically, Veres found that more than half of financial advisors doing financial planning (nearly 55%) were charging an AUM fee as well as a separate financial planning fee, and that charging only AUM fees is actually only done by a minority of advisors.

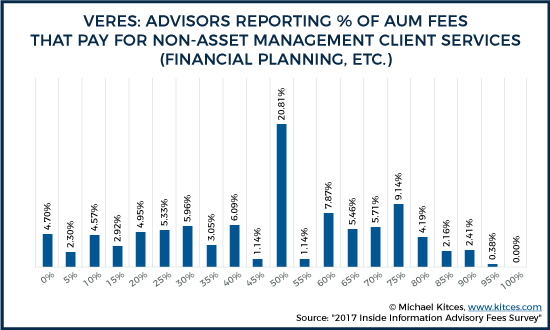

And in turn, the fact that nearly 1/3rd of firms stated that they did financial planning while charging only an AUM fee did not stop them from believing that a portion of the AUM fee was actually “the planning fee.” In fact, when Veres asked just that, “When you charge an AUM fee, what percent of it should properly be allocated to managing assets vs. non-asset management like financial planning?” the results were clear in that advisors, even those charging just AUM, saw the fee in parts (i.e., the one AUM fee was for both investment management and financial planning). Notably, though, while advisors almost unanimously showed that they believe the planning work deserved some kind of fee associated with it (or allocation of the AUM fee towards it), there was no clear consensus on what percent of the AUM fee covered financial planning.

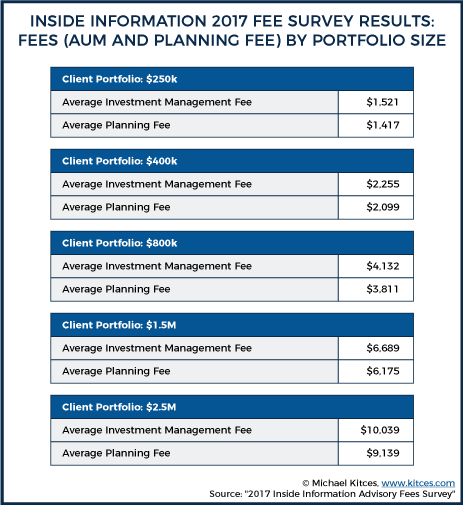

Nonetheless, Veres did attempt to calculate, using data from the AUM-only advisors, how advisors were divvying up the asset management fees versus the planning fee for a wide range of portfolios, having collected AUM fees based on portfolio size, and the percentage of the fee that each advisor typically counted toward asset management versus planning services seen below in the Inside Information 2017 Fee Survey Results chart.

Interestingly, though, one trend that sticks out from both the FPA and Veres studies was that there was remarkably little variation in advisory fees by the experience level of the advisor themselves. Neither study found any material difference in the (dominant-model) AUM fees charged by less experienced advisors versus more experienced advisors. This may simply be because advisors, new or old, have the same fee schedule, but more experienced advisors will manage to attract more affluent clients (who then pay higher fees simply because their accounts and therefore AUM fees are larger, even though the AUM fee schedule itself is the same). On the other hand, outside of AUM fee trends, the FPA study did find that standalone planning fees tend to be higher for more experienced advisors when looking at modular plans – advisors with less than five years of experience charged $550, while advisors with 20+ years charged $1,000.

The Latest Kitces Research On How Much A Financial Plan Really Costs

Given that the FPA study on Financial Planning Fees is now more than 6 years old, and the more recent Veres study did not specifically analyze financial planning fees in particular, Kitces Research decided in 2018 to conduct its own study on what financial planners really charge for their financial planning services.

The results, based on the lead and associate advisors from a sample of more than 1,000 financial planners, found that the ongoing rise of financial planning (versus just investment management) is slowly but steadily causing a split in the advisor community, where fewer advisors are charging blended fees, and more and more advisors are either all-in on the AUM model or all-in on some standalone fee-for-service model.

Specifically, the Kitces Research study found that the percentage of financial planners charging “just” AUM fees is up to 43.2%, but the percentage charging “just” on a fee-for-service basis (e.g., standalone fee, retainer fee, or hourly), is up to 27.8% (as compared to only 11.3% in Veres’ study). In turn, only 26.9% of advisors were charging some sort of blended fee model (AUM, Commissions, and fees), down from 54.6% in the Veres study.

What Do Advisors Charge for JUST A Financial Plan?

With the rise of more financial planners charging standalone planning fees in various fee-for-service models (as well as those who charge separate planning fees on top of AUM fees), our Kitces Research study was able to collect some of the most robust data ever collected on what financial planners actually charge for their financial planning services.

Notably, though, the average cost of a financial plan for (just) a fee, even amongst the advisors charging solely under a fee-for-service model, varied depending on which type of fee structure was being used in the first place.

However, when comparing and contrasting those advisors who charged for financial planning using a planning-fee-ONLY model, versus those that used a blended planning-fee-PLUS (plus AUM or commissions) model, some interesting trends emerged.

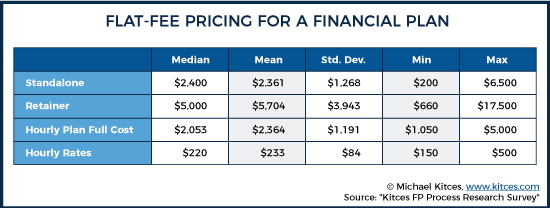

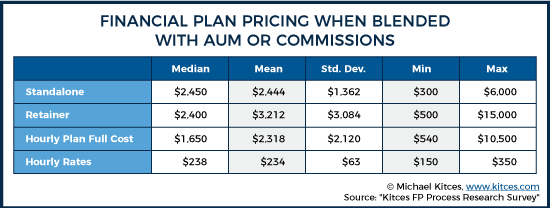

First, for those advisors who reported charging a standalone fee for a financial plan – it did not seem to matter if they charged “just the fee” or if they charged an AUM plus a separate planning fee, the fees were relatively similar (with a median right around $2,400). In other words, when advisors charge for a financial plan, they appear to be fairly consistent in charging for that plan; the AUM fees, if separately charged for implementation, appear to be positioned as a separate service (as opposed to discounting financial planning fees and then trying to “make them up” on subsequent AUM fees when assets are gathered).

The same trend can be said of hourly. Hourly planners do not appear to be increasing or decreasing fees in recognition of the potential for subsequent AUM fees. The typical hourly fee for advisors who charged only planning fees was $220 ($233 average), while those who charged hourly fees and for subsequent AUM fees had a typical hourly fee of $238 ($234 average). Moreover, when advisors work via “projects” (e.g., a bundled set of hourly fees to construct a full plan), the sometimes-additional AUM fee that they may also receive still does not impact or discount the price of the financial plan.

When it comes to ongoing planning fee models, though – i.e., advisors who charge ongoing retainer fees for an ongoing financial planning relationship rather than “just” a one-time standalone planning fee for a one-time planning engagement – a different pattern emerges. Because a retainer fee is an ongoing relationship-based model – as opposed to hourly or standalone planning fees, which are more transactional – when AUM fees are removed from the picture, retainer fees must carry the full weight of supporting the ongoing holistic advice relationship. Accordingly, advisors charging only retainer fees had a median fee of $5,000/year, compared to less than half that amount ($2,400/year) for those also charging AUM fees.

How Financial Advisors Are Setting Fees…

The standard way to set pricing for a service is to figure out its cost, add an allowance for a profit margin, and price accordingly. And given that financial planning is a time-intensive service, one would naturally expect that the cost of a financial plan would be tied to the time it takes to produce the plan (as was shown in the earlier 2012 FPA study).

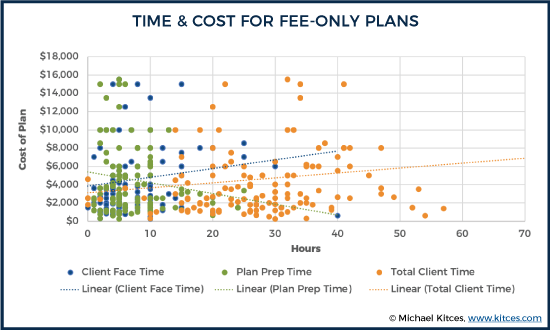

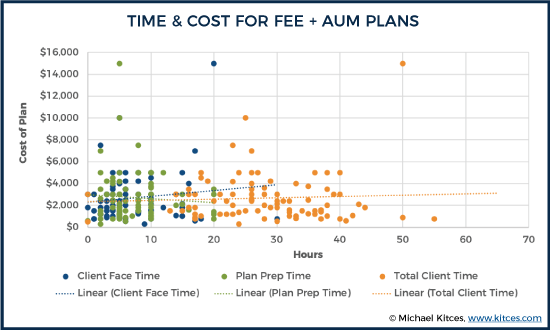

However, based on our Kitces Research data, the pattern is not so cut and dry. In fact, there were no statistically significant relationships between the total time to produce a financial plan and its cost when aggregated across all the advisor business models.

A deeper dive, though, reveals that the lack of any relationship between the time to produce a plan, and its cost, on average, may itself be a function of blending together the different fee structures. When examined separately, fee-only models showed a fairly strong positive relationship between total time and client face-time and the planning fee, but a negative relationship to actual plan constructive time and the fee. Whereas fee+AUM models showed similar trends (positive relationship between total and client-facing time and costs, but negative relationship between plan construction time and plan costs), but the relationship was not quite as pronounced. Which isn’t entirely surprising, either; those engaged in fee-only planning have more of a business incentive to really pay attention to the profitability of plans (fees charged relative to time spent), when it is their sole source of revenue as an advisory firm.

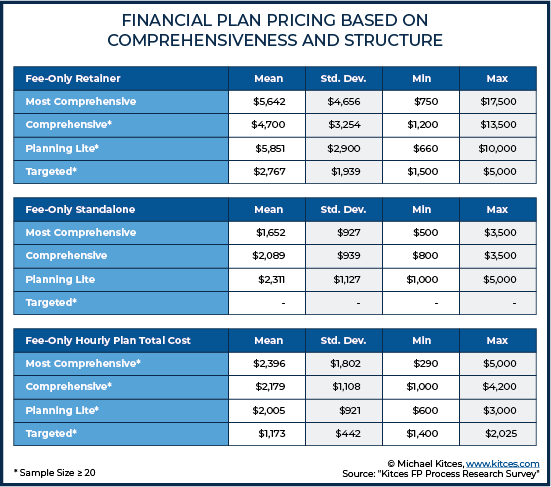

Similarly, there were no statistically significant differences between the comprehensiveness of the plan and its fee… except for when it came to fee-only retainer plans. As in the Kitces Research survey, advisors were asked to identify, from a list, what topics they included in their financial plans, and this list was then used to create four categories that described the plans based on the number of topics/items/services within the plan. The category of "Most Comprehensive"was given to plans with 13+ items, 10-12 item plans were referred to as "Comprehensive", 6-9 item plans were labeled as "Planning Lite", and "Targeted plans" covered 5 or fewer areas. And as shown below, targeted plans were not surprisingly the least expensive across the board.

However, outside of targeted plans, all plans, regardless of comprehensiveness, hover around the same pricing! Retainers are around $5,000, Standalones are around $2,000, and the total cost of an Hourly Plan also runs around $2,000. In other words, the most comprehensive plans were not priced significantly higher than relatively “lite” plans covering just a handful of planning modules.

Though notably, the lack of any difference may be a testament to the efficiency of planning software – that even as advisors add more breadth to a plan, it doesn’t take a lot more time.

The key point, though, is that there is remarkably little direct relationship between what financial planners charge, and the time (and implicit time-based cost) to produce it. Instead, the results suggest that advisors are still most heavily focused on charging for financial planning by literally charging for “the plan” itself (i.e., the physical plan deliverable). Which can even create mismatches in pricing, as it inevitably suggests there may be a number of financial planners who are not charging enough (i.e., charging above-average fees for an above-average time cost to create the plan in the first place).

Value-Based Pricing Of Financial Planning

On the other hand, it turns out that advisors do at least engage in some level of value-based pricing. Or at least, adapt the depth and scope of their plans (and pricing) to the level of clientele they serve (and what those clients can afford in the first place).

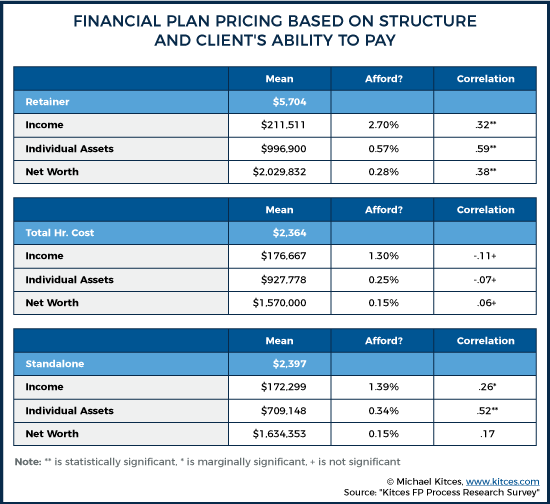

Specifically, our Kitces Research study found that, across the board, the more affluent the client (whether measured by income, investable assets, or net worth), the higher the fees planners tend to charge them for a financial plan (particularly when it comes to standalone or retainer fees).

In essence, the data suggests that the fees charged transactionally for a standalone financial plan (or more directly, the fees that clients are willing to pay for a financial plan) amount to roughly 1.3-1.4% of their income and/or 0.15% of their net worth (when looking at standalone and total-hourly scenarios). While a more holistic ongoing planning relationship – for an ongoing retainer fee – averages about 2.7% of income or 0.3% of net worth. Overall, though, even in fee-for-service models, the tie back to investable assets is remarkably inescapable – as investable assets were still the best predictor of fees, even for advisors not charging an AUM fee! Which suggests that even clients who engage fee-for-service financial advisors are still comparing those retainer or standalone planning fees to what an AUM-based advisor would charge… such that the most acceptable “non-AUM” fee is still the one that is comparable to what an AUM-fee advisor would have charged.

On the other hand, hourly fees (and the cumulative hourly fees incurred for an hourly advisor’s typical engagement) had no predictive relationship to income, assets, or net worth, suggesting that the hourly model truly is a more flexible model that serves a wider range of clients (while retainers and standalone comprehensive planning fees scale more directly with the client’s financial ability to purchase them).

The key point, though, is that financial planning fees, in general, appear to have more of a relationship to the income and net worth (i.e., their client’s affluence) and especially the investable assets of the client themselves, rather than the comprehensiveness of plan or the time it takes to produce. Or stated more directly, clients pay for financial planning based on what they can afford (and ostensibly, the value they perceive relative to their affluence), rather than the time or other costs of the service being provided. Which is important, as it suggests that advisors who can reach more affluent clients will have better pricing and margins for a similar service, helping to explain why it is that most financial advisors tend to institute minimums and move “upmarket” towards more affluent clients as they gain more experience and their practices mature.

More generally, these results also suggest that the better way for financial planners to price their services (or at least, what works better in practice) is to better show how the plan relates to the value the client receives relative to their own income and net worth, and not try to justify fees based on how much time/effort it costs the advisor to produce the advice in the first place. Though at the same time, these results also suggest that, particularly amongst more affluent clients, there may be more opportunity for fee and pricing disruption, given that the connection between an advisor’s financial planning fee and the cost to produce that plan is so "tenuous" in the first place!

Other Factors That Impact Financial Plan Pricing

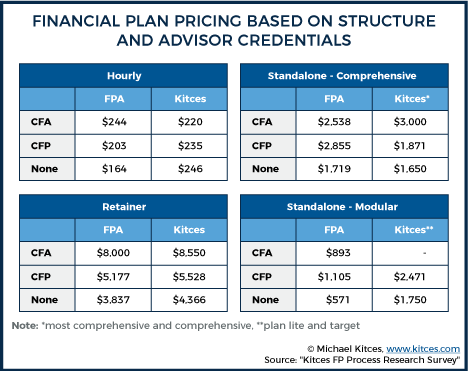

When it comes to other factors that may impact the pricing of a financial plan, another not-surprising key factor is the impact of professional education itself. As the FPA’s study in 2012, along with the current Kitces research study, found that certification, of many types, matters. Advisors with no certification charge less than those advisors with some sort of professional certification.

However, given the earlier results that financial planning fees themselves are more directly correlated to the affluence of the client than the comprehensiveness of the plan (or at least, the time to produce the more comprehensive plan), these results imply that the benefit of a certification may not be the ability to get paid more for a comprehensive plan, per se, but instead the ability to better get in front of more affluent clients who are willing to pay more for planning advice in the first place. In other words, professional certification doesn’t necessarily allow advisors to charge more for their plans, but it does appear to get them access to more affluent clients who can pay more (whether by having more confidence as a financial planner, or more credibility due to the certification itself?).

On the other hand, our Kitces Research results suggest that there is still some premium associated with the depth of a financial plan – or at least, that some types of planning software are better positioned to produce financial plans to those more affluent clientele who, in turn, are willing to pay more for the outcome.

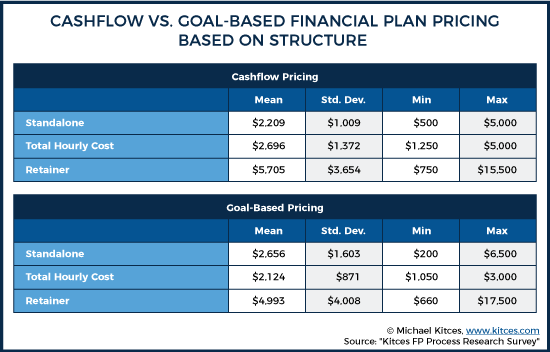

Specifically, in retainer situations, advisors who use more cash-flow-based financial planning software (e.g., eMoney Advisor, NaviPlan, and MoneyTree) command higher financial planning fees than those who use goals-based software (e.g., MoneyGuidePro, Advizr, and RightCapital). Though the exact opposite is true for standalone and hourly planning fees (where clients pay more on a standalone basis for a goals-based financial plan output than a cash-flow-based plan).

Thus, to the extent that plan preparation time was related to financial planning fees, it appears that the time it takes to use more comprehensive financial planning software to produce a more in-depth plan is rewarded in the marketplace by clients, at least when a long-term or ongoing relationship has been established. Thus, while the average time to prepare a plan in cash-flow-based planning software was 8.0 hours, compared to only 7.2 hours for goals-based planning software, retainer advisors were rewarded for this (slight) extra time.

What Is A Financial Advisor's Time Really Worth?

One of the fundamental challenges in a time-based service business like financial planning is that financial advisors can’t necessarily get paid for 100% of their time in the first place. From administrative to management tasks, not to mention personal professional development, the actual time that advisors spend in client-facing meetings (or more generally, on client-specific tasks) for which they can change is only about half of a typical advisor’s total time.

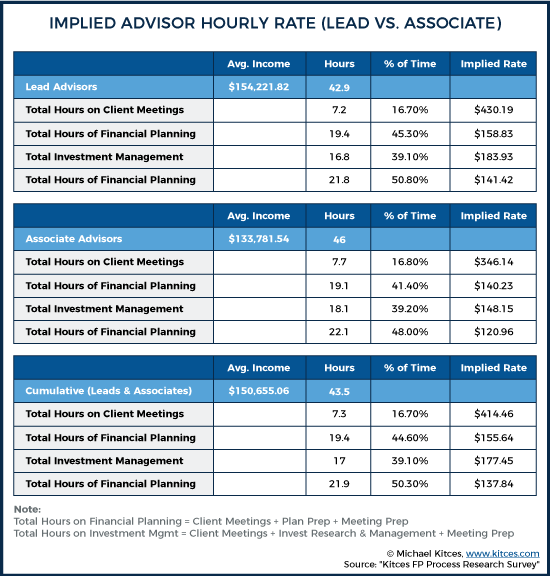

Overall, our Kitces Research study results found that advisors work an average of about 43 hours per week, which is 2,150 hours per year (assuming a 50-work-week year). In the 43-hour week, they reported spending a total of approximately 22 hours on or with clients (meetings, plan prep, investment research and management, and client service). Of specific interest, just over 7 of the total 22 hours was spent on just plan preparation, and another 7 hours were spent in client meetings (with the rest on other client meeting preparation and investment-related tasks).

Which means overall, advisors spend just over 50% of their time, or about 1,100 hours per year, on direct-related client activities. Thus, with an average advisor income of $150,655, the typical advisor is effectively compensated $137/hour for their 1,100 hours of direct-client-activity time.

Taking a deeper dive into these implied hourly rates, lead advisors not surprisingly do make more than associate advisors. Though notably, it appears that lead advisors typically just delegate a portion of each client task to their support advisors, while retaining the rest… such that the total time for both lead and associate advisors is not substantively different (just their implied hourly rate for those tasks).

On the other hand, the data does reflect the relative efficiencies that pure investment management has over financial planning activity alone (or at least, how clients are willing to compensate for those activities). Thus, even though investment-related activities are typically a lower percentage of an advisor’s time than financial planning activities, the implied hourly rate for investment management-related tasks is still nearly 15% higher for lead advisors managing those investment-versus-financial-planning relationships.

Key Takeaways On How Much A Financial Plan Costs (And What Advisors Charge)

Ultimately, the bottom line is that investment management alone is increasingly commoditized and pressure grows on financial advisors to deliver more value (i.e., actual comprehensive financial planning!). And from this perspective, it does appear that more and more advisors are beginning to deliver – and charge separately for – financial planning. In fact, advisory firms appear to be in the process of bifurcating themselves into those that are predominantly AUM-based, and those that are primarily fee-for-service, with a decreasing number that do a blend of each.

However, the market for financial plans still appears to be relatively inefficient. This is perhaps not surprising, given the intangible nature of financial planning itself, and the fact that most clients don’t really know what a financial plan is or what they’ll likely get out of it, at least until after the fact. Thus, financial planning fees bear little apparent relationship to the comprehensiveness of the financial plan itself, or the time it takes the advisor to move the client through the entire financial planning process.

Instead, value appears (as always) to be in the eye of the beholder, such that the fee clients are willing to pay is most directly related to the client’s own affluence (whether measured by income, net worth, or investable assets), and the value that the client perceives will be received from the plan (relative to their own existing financial situation). Which suggests that advisors are at least able to convey and deliver more perceived value for those more affluent clients (who ostensibly have more complex and high-stakes problems to be solved with financial advice in the first place). But at a minimum, it also suggests that there are still many advisors who are trying to deliver a more comprehensive and time-intensive service to clients who simply can’t afford to pay for that much of the advisor’s time and/or the comprehensiveness of the plan… such that time and comprehensiveness itself bears little relationship to the planning fee. And indirectly, these results also reflect the ongoing challenge of financial advisors in explaining the value of financial planning advice in the first place (and the greater value of more in-depth and more comprehensive financial plans).

Nonetheless, these results ultimately do suggest that financial advisors are able to be reasonably compensated for their time, at least on average, with the typical implied hourly rate of a financial advisor’s client-facing time generally falling in the $100 to $150/hour range (and adding up to a total income averaging nearly $150,000/year for a lead financial advisor). And with advisors only spending approximately 50% of their time on client-facing activities in the first place, arguably the best path to growth for most advisors may not be figuring out how to charge more for their financial plans, but simply how to better delegate tasks to spend more time on client-facing activities like financial planning in the first place.

The bottom line, though, is simply to recognize that the market has at this point seemed to home in on a relatively “standard” financial planning fee, of just over $2,000 for a comprehensive financial plan… a fee that has changed remarkably little over the past 6 years (from only about $2,200 for a plan under the FPA’s original study to $2,400 today). And to the extent that more financial advisors are offering financial planning, fees may, thus far, still be held down by the fact that most also charge AUM fees for investment management and/or receive commissions for implementation, limiting the need to charge more for a financial plan in the first place. Yet with a difference emerging between the cost of a financial plan alone, and financial plans that are “cross-subsidized” by implementation, along with the ability of advisors to charge higher fees when using more comprehensive financial planning software and building long-term relationships, there arguably is still room for financial planning fees to drift higher in the coming years as increasingly commoditized investment management services fade to the background (or at least, split into an increasingly separate service with an independent fee structure of its own).

Thank-you for this extensive research. The title should be “What is being charged for Financial Planning?” The actual cost of a comprehensive financial plan must by calculated by each firm. Building in what it takes to on-board a client, collect data, prepare the plan, present the plan and facilitate the collaboration between professionals to see the plan properly implemented with ongoing updating, servicing and answering client questions. Each firm needs to track their hours to do each of these functions come up with a total labor cost, overhead cost and add in a reasonable profit margin. That then determines the cost to prepare, present, implement a plan and provide ongoing updates and service. Then there is establishing a method to communicate the charge to the client based on each individual situation and the anticipated work load.

I’m not sure that wealthy individuals and families “shop around” for comprehensive financial planning advice based on cost for something that is extremely difficult to quantify. The planning time and process for these people is lengthy and intensive. It involves all of their other advisers (CPA, Attorney, Investment Provider, etc). Just the detail and questions surrounding the data and document gathering can take many hours due to the requirement to pull it together from so many sources. And then there’s the analysis of wills, trusts, investments, real estate, private business holdings, structure, ownership, tax returns, agreements between partners, blended family issues, etc. I have found that just this preliminary phase can take dozens of hours and multiple meetings. I have done plans that require months to develop and document, and a couple of years to implement as you get buy-in from all the constituents, change current advisers if necessary, qualify for insurance if needed (I don’t sell insurance), transfer securities to a new custodian, develop new wills, trusts, shareholder agreements, etc.

Of course, as all of this is going on…..life happens and more changes are made. Many of these plans are worth $25-$50 thousand or more, but the value to the client family may be immeasurable in terms of the satisfaction of having it done. Think of the cost as a % of net worth. For a client who has a net worth of $20 million of more and owns one or more businesses, it’s about one to two tenths of 1% of their net worth and probably less than the annual compensation for one of his average employee. In fact, that’s how I have presented my proposal in some cases. I merely ask the client to “put me on the payroll” at the cost of their average employee for one year. And, like any employee, they can fire me at will. After the initial plan is done and implementation is progressing, we negotiate an annual retainer. Because… life happens things constantly change at the margin.

While I recognize this isn’t the point of the article, I feel it has to be said that the “actual” cost of a financial plan (comprehensive or otherwise) can be 10s or perhaps 100s of thousands of dollars if it isn’t executed initially and adjusted/updated on a regular basis. That’s why I think there’s little-to-no value in a financial plan (noun), but there is tremendous value in ongoing financial planning (verb).

Exactly. The financial plan is not the product. It’s a tool. My barber could sell me his clippers, but they’ll be almost useless in my hands even though I’ve watched him cut my hair for years. This is why I’ll probably never consider moving to a planning-fee-only model. It doesn’t align with what clients actually need.

Good article, but interest in the following question: any idea on how many advisors/planners that are doing retainer pricing, reduce their fee after the first year because it goes from a creation/implementation in the first year to ongoing monitoring and adjustment afterwards?

Pretty dated info