Executive Summary

As the average age of advisors creeps older every year, the industry has continued to predict an impending wave of advisors retiring and looking to sell their practices, leading to a massive buyer’s market for advisory firms. Yet thus far, data from FP Transitions suggests the number of buyers still outnumbers the sellers by a whopping 50:1, and the succession planning “crisis” has been little more than a mirage.

Nonetheless, a recent survey conducted by Aite Group and published by NFP Advisor Services suggests that advisory firm acquisitions may be happening far more than anyone realized, but are occurring primarily within wirehouses and large insurance-affiliated broker-dealers, and just not as much in the independent broker-dealer and RIA channels. On the one hand, this may be driven by the fact that large firms have had even more incentive to ensure a smooth transition to allow the parent firm to retain the clients; on the other hand, large firm acquisitions may also simply be driven by the fact that they are a closer-knit community and the majority of acquisitions seem to occur primarily through the existing personal contact network of the acquirer!

In addition, the Aite/NFP study also provides a rather unique glimpse into “what’s working and what’s not” in the world of advisory firm acquisitions, by comparing and contrasting the characteristics of deals and their subsequent implementation between firms that were happy with their acquisition, and those who later regretted it. The results paint a fascinating picture, with some firms patiently cultivating a network of potential firms to acquire, patiently evaluating and slowly vetting, but ultimately paying top dollar for quality firms and acting quickly to integrate the clients once the deal is consummated. By contrast, the study also finds that while many firms are discovering opportunities that “fall into their lap” when a firm approaches them to be acquired, often for a price that’s on the cheap, that these reactive deals are actually leading to the most problematic implementation, the lowest retention, and the worst satisfaction levels after the fact, despite their appealing price!

The Current Landscape Of Financial Advisory Firm Mergers & Acquisitions

To survey the current landscape of advisory firm acquisitions, Aite Group (in conjunction with NFP Advisor Services as the publisher) conducted a survey study of 401 financial advisors, including 100 who had completed an acquisition of a practice at some point along the way. Notably, this means that if Aite’s survey really was a representative sample, a whopping 1-in-4 advisors have already been a part of an acquisition at some point during their career (which, if it’s truly industry-wide, would suggest that as many as 75,000 advisors have been acquirers at some point in their career!?)!

Acquisitions ranged from those who did primarily to grow their existing practice (58%), to those who did it as an initial purchase of a client base/firm to launch their career (28%), to those who did it specifically to take on a new geographic area (5%) and more. About 60% of the acquirers had simply done it once, while the remaining 40% were serial acquirers who had done 2-or-more acquisition deals.

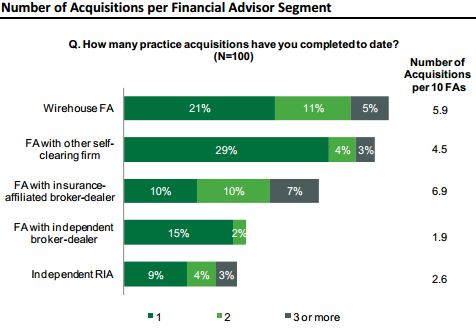

Notably, unlike some industry services that track primarily the merger and acquisition activity of independent RIAs, the Aite survey spanned a wide range of advisor channels, and somewhat surprisingly found that the independent RIA channel may actually be the least active for merger-and-acquisition activity amongst advisors! In fact, the rate of practice acquisitions amongst wirehouse and insurance-related broker-dealers was more than double the pace of independent RIAs, while independent broker-dealers averaged even fewer deals (with a slightly larger number of acquirers in the channel, but fewer than do multiple serial acquisitions). This also supports the total-advisor-data-based guesstimate by Dan Seivert at the recent Echelon Deals and Dealmakers Summit that there really may be far more advisor M&A activity going on than most (prior) industry studies have suggested!

Source: "Alpha Acquisition: Maximizing the Return on Your Practice Investment" by Aite Group & NFP Advisor Services

The Aite survey data doesn’t provide much indication or detail about why acquisition activity is so much higher at “employee” advisor firms, though it’s not hard to imagine that the entrepreneurial “wiring” that drives some advisors to the independent broker-dealer and RIA channels also makes them far less interested in being acquired or exiting their business at all (as David Grau of FP Transitions suggested in his recent book). It’s also possible that larger firms are doing more to encourage and facilitate merger and acquisition activity within their platforms, perhaps as an overall retention strategy for the parent firm, and/or to facilitate the recent large-firm trend towards team-based wealth management.

Lessons Learned From No-Regrets “Alpha Acquisitions” Of Advisory Firms

The goal of the Aite/NFP study was not merely to understand the current landscape of advisory firm acquisitions, but also to gain some perspective on best practices; in other words, are there particular characteristics of the most successful acquisitions as differentiated from the least successful, to better understand what “works” and what doesn’t when it comes to those seeking to buy an advisory firm?

While there are lots of different ways a successful acquisition might be evaluated – from client retention rates, to post-acquisition growth – the reality is that “success” can mean somewhat different things to different acquirers. Accordingly, the Aite/NFP study simply defined the most successful acquisitions as those where, after the fact, the advisor reported that he/she was “very satisfied” with the acquisition, and would do it again. These highly successful purchase transactions by advisors were dubbed “alpha acquisitions”.

In turn, advisors who rated that they were “satisfied” (but not “very satisfied”) and that they would still do it again were dubbed “near-alpha acquisitions”, and everyone else (either those who weren’t satisfied, and/or who wouldn’t do an acquisition again), were characterized as the “non-alpha” acquisitions.

Based on the Aite/NFP study sample, 25% of advisors fell into the alpha acquisition category, and 30% were non-alpha, with the other 45% in between. As noted above, then, the goal of the study was to evaluate whether there were (statistically) significant differences in the characteristics, tactics, and results of alpha versus non-alpha acquirers.

Challenges In Finding And Valuing An Advisory Firm To Purchase

Before an acquisition can occur, it’s necessary to find a firm to purchase, and to agree upon a reasonable valuation for the transaction. And in this regard, the Aite/NFP study finds there are significant differences between how alpha acquisitions occur, versus the non-alpha purchases.

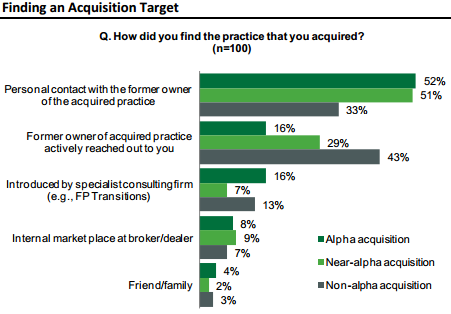

For instance, a key distinction between alpha and non-alpha acquirers is how picky they are about selecting a firm to purchase in the first place. Alpha acquirers take significantly longer on average to find a firm to purchase, with only 1/3rd of alpha acquirers finding their target within 2 years or less (by contrast, 70% of non-alpha purchases found their acquisition target in 2 years or less). In addition, a whopping 1/3rd of alpha acquisitions came when the firm wasn’t even looking for the opportunity, and it simply presented itself!

Alpha acquirers also tend to rely more heavily on their network and personal relationships to find acquisition targets in the first place, and then reach out to them proactively once a potential fit is presented; 52% of alpha acquisitions were from an existing personal contact that the firm reach out to, compared to only 16% where the acquired firm actively reached out about being acquired. By contrast, with non-alpha firms, only 1/3rd were initiated from an existing personal contact, while a whopping 43% were a result of the acquired firm reaching out, as shown below.

Source: "Alpha Acquisition: Maximizing the Return on Your Practice Investment" by Aite Group & NFP Advisor Services

These results suggest that in practice, when a firm reaches out to be acquired, the acquiring firms may be too hasty to pull the trigger on the transaction and not discriminating enough about the fit, to their subsequent regret. By contrast, firms that use their network to leverage existing contacts, and then initiate potential evaluations of an acquisition (rather than let the firms-to-be-acquired come to them), seem to fare better.

And notably, it appears that truly networking is the primary driver in finding acquisitions – the Aite/NFP results also found that only 1-in-10 acquisitions were brokered by an external consulting firm, with another 1-in-10 facilitated through an internal marketplace, while the rest are being driven by personal networks. This also implies that acquisitions may be more frequent at wirehouses and insurance-based B/Ds because those organizations tend to have a closer-knit network of advisors; with independent firms, there are often less connection points to other independent firms, which may be slowing down the pace of connections that can lead to acquisitions.

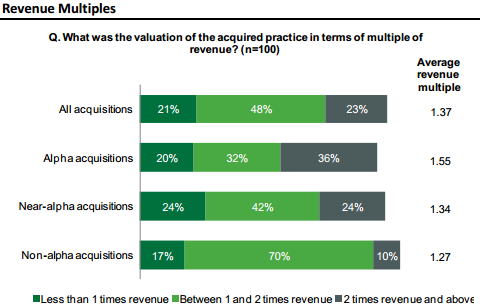

The Aite/NFP study also found that difficulty in setting an appropriate valuation can also be a warning sign of a problematic deal. While establishing a valuation is challenging across the board (even 44% of alpha acquisitions reported that it was difficult to determine the valuation), it is most problematic for non-alpha acquisitions, where it was a sticking point in a whopping 80% of the transactions. Notably, non-alpha acquisitions also tended to take a less holistic view of valuations, while alpha acquisitions tended to draw widely on a range of factors, including AUM, client service model, revenue mix, the longevity of the business, and cash flows from operations (however, “age of clients” was actually the least relevant factor for alpha acquisitions, suggesting age-related fears for acquisitions may be overblown!).

On the other hand, while valuation issues were more problematic for non-alpha purchase transactions, this doesn’t necessarily mean they were more expensive. In fact, the Aite/NFP study found that the alpha acquisitions tended to have the highest price point and revenue multiples (with a solid 36% of purchases at a 2X-revenue-or-higher price point), while the non-alpha acquisitions tended to be the cheapest (with 70% of transactions done between 1X and 2X revenue).

Source: "Alpha Acquisition: Maximizing the Return on Your Practice Investment" by Aite Group & NFP Advisor Services

In other words, it appears that while non-alpha acquirers were at least receiving a discounted price for the more problematic practice they were hurrying to buy, they still ended out less satisfied than alpha acquirers that paid a higher price for a practice that was ultimately a better fit! However, these results may also be driven by the fact that a whopping 77% of non-alpha acquisitions reported having difficulties obtaining a loan to fund the purchase, while only 25% of alpha acquisitions reported financing challenges, so their less-expensive purchases may have been driven by the lack of financing to facilitate them. Though ironically, while alpha acquisitions reported little difficulty with financing, they were actually far less likely to use any financing, with 52% of transactions not financed at all (compared to only 27% for non-alpha acquisitions)!

Client Retention, Staff Retention, And Post-Acquisition Implementation

What is perhaps most notable about the Aite/NFP study, though, is the fact that they also delved into the post-acquisition implementation of the deal, an area where few other studies have tread. And here, too, the Aite/NFP study provides some interesting perspective.

For instance, while alpha acquirers are much slower (pickier?) to reach an acquisition transaction, once it’s done they’re far faster on the follow-through to implement it, with 52% done with the transition in less than a year; by contrast, amongst non-alpha acquirers 70% were still trying to finish the implementation after 3 years.

To further the implementation, the study suggests it’s crucial for the advisor with the acquiring firm to actually meet with clients to help facilitate the hand-off to the acquiring firm; in alpha purchases, almost 50% of the advisors being acquired met with clients to brief them one or several times, while in a whopping 75% of non-alpha transactions clients were simply informed by a letter that was mailed or emailed to them.

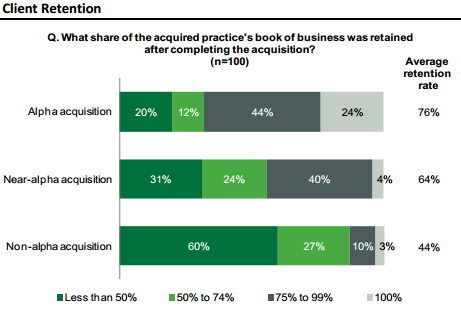

In addition, alpha transactions were far more likely to retain staff, with a whopping 57% of the deals retaining all staff, compared to only 19% of non-alpha transactions. This continuity of staff may go far to explain why a full 2/3rds of alpha acquirers retained 75%-or-more clients, while non-alpha firms only retained 75%-of-more clients in a mere 13% of scenarios (with a painful 60% of non-alpha acquisitions retaining fewer than 50% of clients!). Alpha acquisitions also saw significantly more post-implementation growth than non-alpha firms.

Source: "Alpha Acquisition: Maximizing the Return on Your Practice Investment" by Aite Group & NFP Advisor Services

Best Practices For Advisory Firm Acquisitions

Overall, the Aite/NFP study paints one of the deepest pictures we’ve seen yet of the landscape for advisory firm acquisitions, and best practices in executing them.

The top acquisition deals – the “alpha acquirers” – are slow and patient in finding firms, picky about who they do deals with, evaluate the deal thoroughly for valuation purposes, and when ready pull the trigger and move quickly to implementation, leveraging the outgoing advisor to make introductions and retaining staff to further expedite the transaction. And they find their deals by building and cultivating a network of personal contacts to find potential firms to acquire, and then proactively reaching out to those firms that may be a fit.

By contrast, those who often turn out to regret their deals – the “non-alpha acquirers” – are more likely to just take a deal that falls into their lap, struggle to get the financing to facilitate it, and negotiate down the price to an affordable point (with a great deal of difficulty), but even once the deal is consummated have further challenges actually integrating the old advisor’s clients into the new firm, especially if they have to terminate the ‘old’ staff and try to integrate all clients into the acquiring firm’s advisors and staff but without a sufficient handoff process.

Perhaps most notable, though, is the fact that while non-alpha acquirers did pay less for their “less effective” acquisitions – suggesting they may have still been getting a “fair price” for the challenges they faced – the non-alpha acquirers still reported that they were unsatisfied with the transaction and that they wouldn’t do it again.

In other words, the key takeaway for acquisition planning is that low quality deals “on the cheap” that fall into the advisor’s lap just aren’t worth it in the end. By contrast, the happiest acquirers actually tended to pay the most for the firms they acquired, but are able to transition and integrate the clients more rapidly, resulting in a far higher satisfaction rate as the acquirer, despite the higher price point!

For those interested, you can obtain your own copy of the Aite/NFP study “Alpha Acquisition: Maximizing the Return on Your Practice Investment” directly from their website. It’s definitely recommended reading if you’re considering an acquisition for your advisory firm, now or in the future!