Executive Summary

As a wave of next-generation clients starts to seek out help managing their finances, one of the most common challenges that they face is a high level of student loan debt. Unfortunately, advisors are generally ill-equipped to provide student loan analysis and planning, because, unlike traditional debt, student loans - and federal loans in particular - are subject to a dizzying array of repayment options (each of which can result in significantly different outcomes for borrowers) and forgiveness programs, which in and of themselves, are stunningly difficult to navigate. And, in a world where interest rates are rising quickly, the “easy” solution of refinancing older loans at a lower rate isn’t providing the same bang for the buck it once did, not to mention the fact that refinancing won’t make any sense for borrowers that recently took out loans while rates were at historic lows. Which means that a strong working knowledge of the various options for repaying federal student loans will increasingly be an important tool for advisors in coming years.

Fortunately, there is a growing number of tools to help advisors analyze their clients’ student loans, and in this guest post from Ryan Frailich, founder of Deliberate Finances, (a fee-only financial planning practice that specializes in working with couples in their 30's, as well as educators and nonprofit workers) provides comprehensive reviews and ratings for 8 student loan planning tools, including offerings from CSLA, RightCapital, the VIN Foundation, Loan Buddy, and Pay For ED (among others), and shares his thoughts on everything from features and flexibility, to their ease of use and usefulness of output.

Because the fact is that, often, those clients who come in with the highest level of debt, including doctors and lawyers who are just starting out, also happen to be ideal long-term clients, and having the knowledge and ability to potentially help them save a significant amount of money over the life of their loans is a great way to build long-term loyalty. And even for advisors who work primarily with Baby Boomers, the ability to help their children navigate the student loan landscape can assist in introducing you to your next generation of clients.

While not all the solutions that Ryan examines are targeted specifically at advisors and there’s still plenty of room for improvement with all of them, the good news is that FinTech developers are recognizing the importance of putting tools in advisors’ hands that will help clients with student debt navigate what is often the first (and most challenging!) aspect of their young financial lives. So, whether you have clients with questions about how best to manage and repay their student loans, are looking for ways to gain and develop expertise in this important area, or are simply interested in staying up-to-date on this rapidly evolving area of financial planning and FinTech, then we hope you find this amazingly comprehensive guest post from Ryan to be helpful!

When I work with my typical clients, who are usually in their 30’s, the most pressing topic is often something to the effect of, “How do I manage my student loans, and how should I weigh them against all the other things I want to be saving for?”

This isn’t surprising, given that more than 44 million Americans have student loans, with the total debt having recently passed $1.5 trillion dollars. Amongst 30-39 year olds, they hold $461 billion of student debt, or nearly 1/3 of all the student debt outstanding. For advisors who work with younger clients, it’s imperative to be properly equipped to incorporate student loan analysis into younger clients’ financial plans. And for planners who tend to work with Baby Boomers, helping your current clients’ children formulate a student loan plan could be a great way to build a bridge to your next generation of clients.

In fact, some of the highest levels of debt belong to those who might be ideal long-term clients for many advisors. Law school graduates now come out with an average of over $140,000 of debt, while medical school graduates are averaging more than $190,000. Knowing how to help them solve their number one concern as recent graduates becoming high-income professionals is a way to build trust and loyalty that will help lay the foundation for a business with continual growth for decades to come. But first, you have to actually know how to give advice in this area, and it’s much more complicated than other forms of debt.

Planners are used to looking at just a few variables when it comes to advising on debt management, mainly interest rates, monthly payments, overall cost of the debt over time, and looking to see if there’s an option to refinance to lower a monthly payment.

Student debt is an entirely different animal. In particular, while private student loans are also essentially a function of interest rate, repayment period, and total debt, federal loans often are not. There are a host of different federally-sponsored income-driven repayment plans, all of which have different criteria for use, and different outcomes for the borrower. In some you can use the MFS (Married Filing Separately) tax-status, but in others, that filing status would be disregarded for income-driven repayment amount calculations. There are forgiveness programs for public service, and forgiveness programs linked directly to income-driven plans, regardless of employer. There are job specific forgiveness programs, such as Teacher Loan Forgiveness or National Health Service Corps and Veterinary Loan Repayment. And while refinancing federal student loans may reduce loan interest or monthly payments, it can forfeit access to many of these programs (which itself may or may not matter, depending on the client’s situation).

This complexity regarding student loans, and specifically the intersection of various federal student loan programs, means it’s an area most advisors aren’t equipped to give great advice on, especially considering the CFP curriculum only scratches the surface. And it’s an area that has enough complexity to warrant more sophisticated tools, if only to be able to effectively analyze the complex trade-offs in the first place.

Knowledge of federal student loans is only going to become more valuable if interest rates continue rising. Recently, the reality is that refinancing has often simplified the process; given the downward trend of interest rates to historical lows, borrowers often took out loans at 6-7%, and could then refinance at 3-4% after graduating (giving rise to an entire industry of refinancing companies targeting students who had borrowed 4-6 years earlier at higher rates). As rates rise and borrowers come out of school into a rising interest rate environment where refinancing often won’t make sense for borrowers anymore, they’ll actually need to navigate the myriad of options in the federal system. For advisors, this means it’s likely that federal student loan repayment knowledge will be even more valuable in the coming decade than it is today.

Features to Consider when Selecting a Student Loan Analysis Tool

A promising sign is that in recognition of the growing need, there is an emerging industry of tools to help financial planners analyze student loans. Not all of them are intended specifically for financial advisors, and many of the tools are still in their early stages, which means that their capabilities range widely, and are changing regularly with development happening quickly.

Nonetheless, there is a core set of features that all advisors should look for when considering different software to conduct student loan analysis.

Ability to Import Data from NSLDS

Having accurate data is a must in order to properly analyze student loans. To cut down on errors, student loan analysis software should ideally be able to import student loan data directly from the National Student Loan Database (NSLDS), which is the central database for all federal student aid programs.

The NSLDS allows borrowers to download a text file with the status of their loans (i.e., Is the loan in forbearance? Deferment? Has the loan been defaulted on?), date of disbursement, initial balance, current balance, accrued interest, etc. The file itself is near impossible to make sense of directly, but a variety of tools can be used to organize and clean up the data to a useable format.

The NSLDS database is particularly important because the four major student loan servicers are not known for accuracy, nor for considering the best interests of the consumer.

Ability to Analyze Student Loans at the Household Level

With the variety of different payment plans available, it’s key that any student loan analysis tool be able to look at the entire household unit, not just each individual borrower.

The reason is not just due to the importance of considering the household’s entire ability to make student loan payments from a financial planning perspective (e.g., when both spouses have student loans), but because some payment plans, such as IBR & PAYE, allow for spouses who file MFS (Married Filing Separately) to use that status for income-driven repayment amount calculations. Others (REPAYE) ignore that distinction and look at total household income regardless of tax filing status.

Which means there may be a payment plan one spouse would choose if single, but not want to choose if married and filing jointly, or alternatively might make themselves eligible for by choosing to be married filing separately because the tax benefits lost by using MFS are less than the benefit of being able to look at income separately for student loans.

Adaptable Assumptions To Model Long-Term Student Loan Planning

Like any financial planning advice, we must take the best known information to date, and extrapolate it out into the future, using our best guess as to a host of variables, from inflation to investment returns to future tax rates.

In the context of student loan planning, this is particularly important for clients who may be working towards loan forgiveness, which is sometimes treated as a taxable event. Thus, the platform must be able to project what the tax impact of forgiveness would be, and an estimated amount the client would need to save (including growth) in order to be prepared for that so-called “tax bomb” that comes after 20 or 25 years of payments when the loan is typically forgiven.

Loan forgiveness, along with the trajectory of income-based repayment plans and their varying monthly payment obligations over time, also hinges heavily on future changes to income as well, so effective student loan planning tools must be able to easily model adjustable future income projections. Other key variables to be able to model include tax status, family size, and inflation assumptions.

Side-by-Side Comparison of Repayment Plans

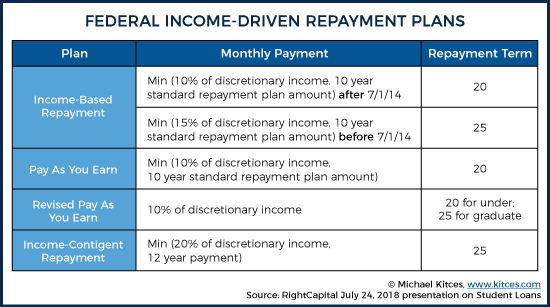

Under the umbrella of Federal Income-Driven Repayment Plans, there are actually four different payment plans that have become available and evolved over the past two decades (along with a 5th, Income-Contingent Repayment or ICR, which still exists but is no longer typically used because the others are all more favorable):

In addition to those plans, there is the 10-year Standard Repayment, in which loans are repaid across 120 consistent payments regardless of income, as well as the option to privately refinance (or alternatively to do a direct consolidation federally but without refinancing). There are also extended repayment and graduated repayment options (though they are rarely the best option these days).

The significance of these varying programs is, again, that the monthly payment, total amount repaid, amount forgiven (if any), and tax impact of these plans can vary widely. The software must be able to clearly show, based on the information entered, all of the factors listed above for at least the 6 most common repayment program options.

To demonstrate just how much the plans vary, let’s look at an example of a couple with the following situation:

- She is a surgeon and just completed residency and will be making $225,000 as a starting income.

- He is a teacher with a few years of work experience and currently makes $52,000.

- They have a combined student loan debt of $370,000, $300,000 of which is hers, and $70,000 is his.

The outcomes would change somewhat depending on assumptions regarding taxes, future earnings, family size, etc. If we assume:

- 3% annual wage growth

- 3% annual inflation

- Two children born in the coming decade

- Average student loan interest rate of 6.4%

- 35% income tax (combined federal & state)

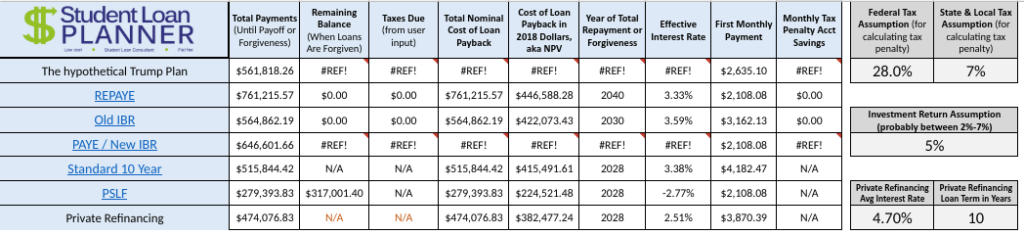

...then in this scenario, the Net Present Value of repayment ranges from $224,521 (if both use the Public Service Loan Forgiveness route) to as much as $446,588 (if both use the Revised Pay As You Earn plan). The first month’s payment, (assuming you could get both started on repaying the exact same month, which is rare), ranges from $2,108 to $4,182. That’s an enormous range!

The impact of choosing the right student loan repayment plan (and going even deeper, choosing the right initial plan and then knowing if and when to switch plans) can often be a six-figure decision over the borrower’s lifetime. So all software should be able to compare the impact of any route being considered.

Ability to Input Private Student Loans

Federal student loan debt is the overwhelming majority of the outstanding student loan debts, but there is also $113 billion of private student loans.

It’s important to be able to see any/all existing private student loans in any analysis to determine if a given monthly payment (across all public and private loans) is feasible, and whether it could make sense to consolidate existing federal loans and existing private loans into one loan (especially if a lower interest rate is possible).

Ability to Filter Out Unavailable Repayment Plans

The rules governing (and limiting the availability of) different federal repayment plans present an additional complicating factor for student loan analyses.

For example, the Income-Based Repayment plan caps payments at 10% of discretionary income if your first loans were taken out after July 1, 2014. It’s 15% for everyone who borrowed before that date. Another example is that Federal Perkins loans are not eligible for Public Service Loan Forgiveness. They would have to be consolidated first.

A student loan software solution that can hide options that aren’t actually available to a borrower would help many advisors make sure they aren’t recommending a path that the client isn’t actually able to follow anyway. Of course, advisors should know this information, but built-in fail-safes would help limit errors and reduce client confusion.

Review of 8 Tools for Student Loan Analysis

Before getting into the comparisons, it’s important to state upfront that none of the current vendors provide everything on the above list of desired features for financial advisors. The above is what would be ideal for a tool to have, but the current tools available aren’t there yet, so it’s a matter of figuring out which one best suits the advisor’s individual needs and planning approach.

Fortunately, most of them are also rapidly developing, so what exists now and what exists in 6 months will almost assuredly not be the same. In fact, two of the vendors here either have only launched a beta, or haven’t launched at all yet. (Michael’s Note: In fact, between this article being drafted in September and published today, multiple changes and new features have already been announced by several vendors, which demonstrates just how rapidly the tools are evolving!)

Based on the various factors listed above, below you will find my reviews of 8 tools for student loan analysis. Each tool will have an overall summary of how they line up on the key features discussed earlier, followed by a rating for Features (in the aggregate), Ease of Use, Quality of Output, and Flexibility, scored as follows:

1= Inadequate

2= Somewhat adequate

3= Adequate

4= More than adequate (Surpasses Expectations)

Listed in no particular order, the 8 Student Loan Analysis tools for financial advisors to consider are:

- CSLA

- Right Capital Student Loan Module

- Student Loan Planner’s Excel

- Studentloans.gov

- VIN Foundations tool

- Loan Buddy

- Pay For ED

- PayItOff

Certified Student Loan Advisor Technology (CSLA)

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

Yes |

Yes |

Yes |

Yes |

No |

No |

CSLA launched a beta version in 2017 of their platform and has most of the key features advisors would want.

CSLA is backed by the Certified Student Loan Advisor Board of Standards, a non-profit organization that also recently launched their own designation, the Certified Student Loan Professional. Recognized student loan expert Heather Jarvis is a board member, which demonstrates their commitment to having some of the most knowledgeable people in the country on their team.

Advantages

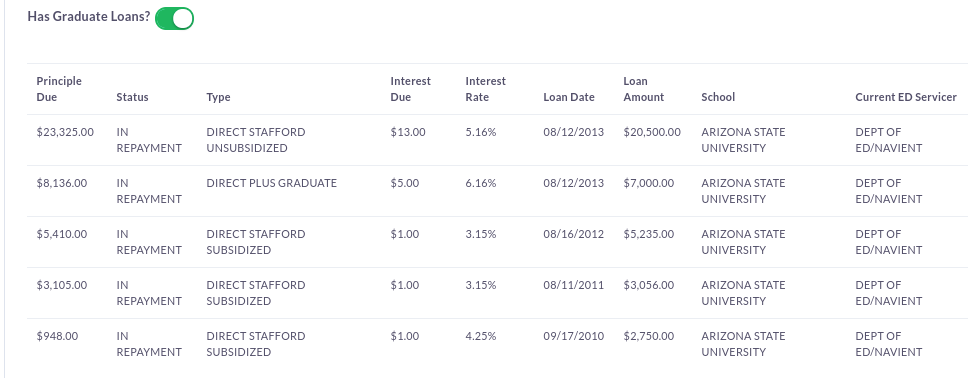

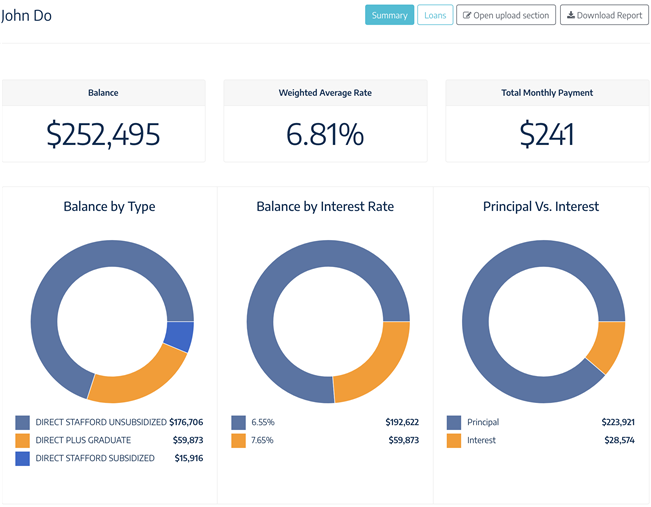

CSLA has the most robust detail and adaptability of any of the tools listed. Advisors can trigger an email to clients to have them upload their NSLDS data file, and it automatically populates with all of their loan info, as shown an in the example below.

(At one point the tool actually had a live link to the National Student Loan Database, allowing for real-time data flows, but that is no longer active due to FERPA [Family Educational Rights and Privacy Act] concerns.)

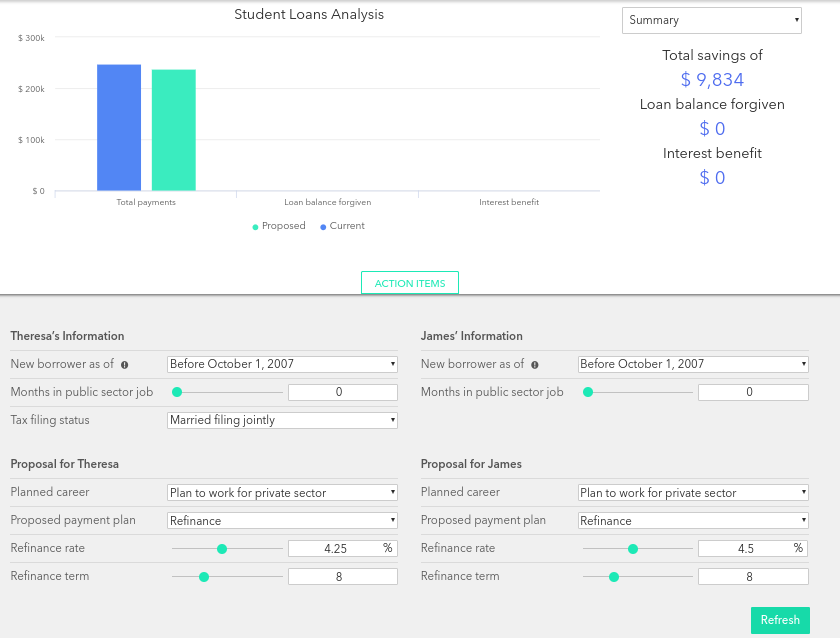

The “forecast” screen allows advisors to project AGI (Adjusted Gross Income) with annual growth, or override to account for an expected jump in earnings, such as when a medical resident becomes an attending physician. You can also project year of marriage, spouse’s income, and plans for future children, as those factors all impact the Income-Driven Repayment (IDR) plans.

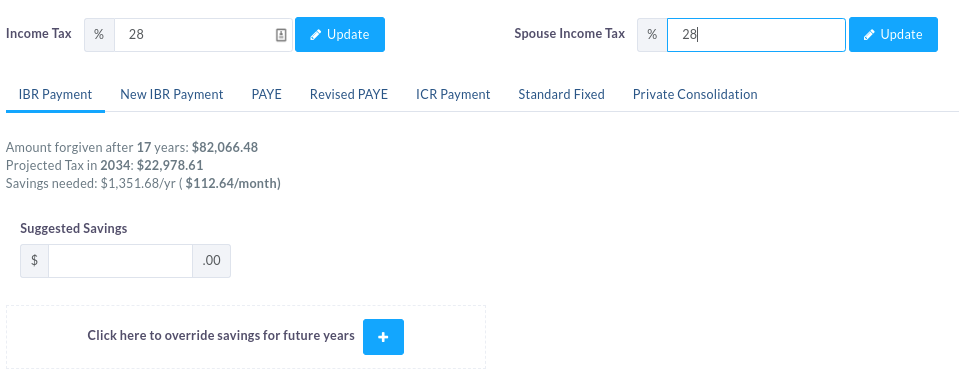

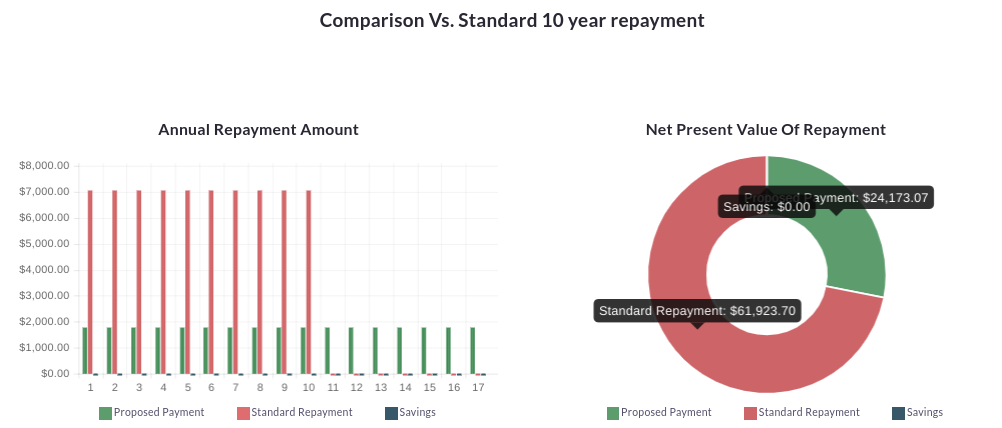

The Payment Plans screen allows easy comparisons across all the different plans, including showing the amount of the “tax bomb” that would hit those who use an IDR plan and have taxable forgiveness at the 20- or 25-year mark. By clicking on any of the tabs, you see the total cost of repayment, and how that compares to the 10-year standard plan. You can also see how monthly payments rise over time based on the inputs on the forecast screen.

Note: The “savings” calculation didn’t seem to work on this screen, despite there being a difference between the IBR plan vs the standard plan.

You can also go through year by year to see how the payments change with income growth, family size changes, etc.

Disadvantages

The CSLA platform is new, and there are definite areas to be improved. It relies on a client to upload their data, and there is not an easy advisor option to do so. There is no integration with any other financial advisor software programs (e.g., other financial planning software or CRM systems), so all the data on each client must be entered in manually, including data like salary, age, children, marital status, all of which most advisors already have elsewhere in their CRM and/or financial planning software. Existing private loans don’t have a spot to be entered, so the advisor has to manually put together any analysis of overall debt repayment based on their recommendations.

The other drawback on CSLA is that the initial launch was somewhat confusing. There was an initial beta last year with a price of $3/month per client uploaded and some initial training videos were posted on their website. But after several months, the client service and feedback essentially went dark. Multiple advisors have told me of calling repeatedly and not hearing anything back from the company. The platform remained live, but with little means of getting support (though their fee was also not charged during this time).

Their team has relaunched the tool and is now taking on advisors and billing their monthly per-client fee. With this relaunch, I hope to see a lot more support so that advisors aren’t left alone to navigate the software that by its nature is somewhat complex simply due to the complexity of the loans it is modeling and analyzing.

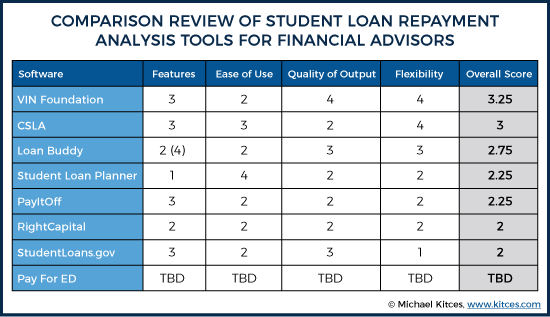

CSLA Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

3 |

3 |

2 |

4 |

3 |

Right Capital Student Loan Module

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

Somewhat |

Yes |

Yes |

Somewhat |

Yes |

Yes |

RightCapital recently released their student loan module and is the only financial planning platform to have built this functionality into their existing software. Given how different student loan analysis is versus a typical debt analysis, it’s a huge benefit to those advisors serving many clients with student loans.

Advantages

Embedding a student loan analysis tool into existing financial planning software is a tremendous advantage and is ideal for building a cohesive overall financial plan. All the existing assumptions around family size, income growth, tax rates, etc., are already built in and inputted for the rest of the plan. It also means one fewer system for the advisor and the client to navigate.

However, with RightCapital, data does not import from the NSLDS file, although you are able to link directly to the student loan servicer’s account data via the data aggregation that RightCapital provides. It’s not as good as having the NSLDS data, though, because the federal student loan servicers don’t always provide the most accurate or complete data. But it’s a start.

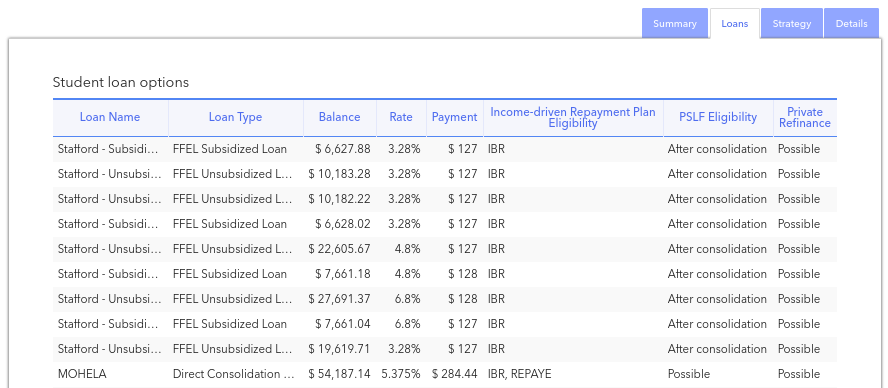

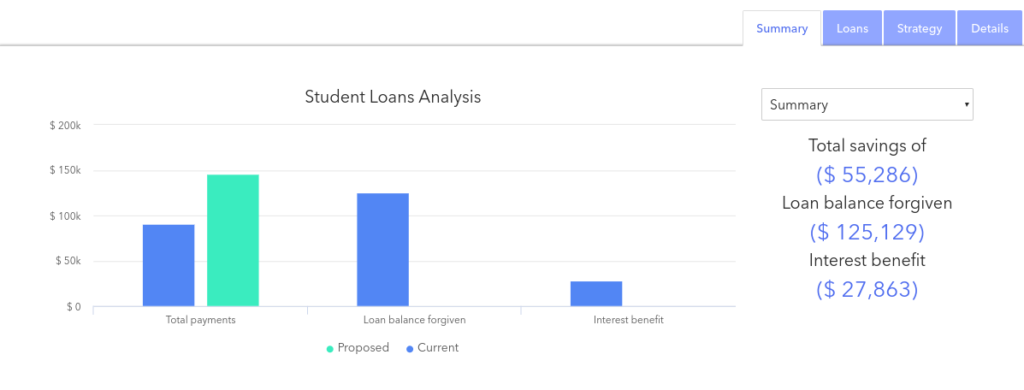

The summary tab allows advisors to easily toggle between different repayment plans and see the outcomes. There is no side-by-side comparison, but with a few clicks, advisors can see how much the total repayment and monthly repayment costs will be under different scenarios. Advisors can also differentiate between what route each spouse takes, so one may go for PSLF while the other privately refinances. Below is a screenshot for a couple who have decided to privately refinance, now that their income has risen to the point where continuing on (or maintaining eligibility for) an Income-Driven Plan does not make sense.

You can easily view the total student loans summary, including all the pertinent information about each loan and what programs the loans may be eligible for. For example, with the couple below, many of their loans are not eligible for PAYE or REPAYE because they are FFEL loans. The screen clearly shows which programs they and are not eligible for.

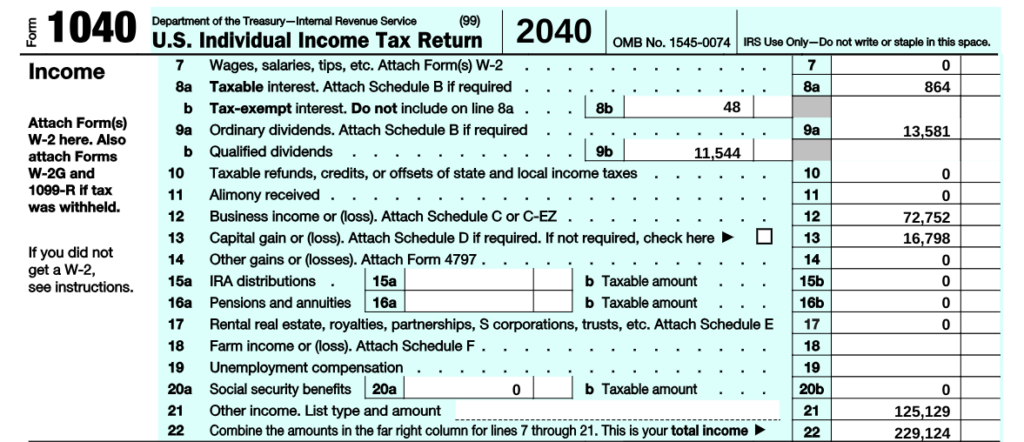

For some clients who have much larger debts than their income, and don’t have the long-term earning potential to pay off the debt, the RightCapital tool helps show what amount would be forgiven, as well as the year, and actually puts that forgiveness amount on Line 21 of the projected Form 1040 tax return in the rest of the financial planning software projections for that year. This lets you build your entire plan around that taxable forgiveness event in the future, though the software doesn’t automatically calculate how much to save in order to meet that tax bill in the year it will be due.

Disadvantages

Since the RightCapital student loan tool relies not on NSLDS but on student loan servicers, the imported client data still requires some cleanup, as the information transferred is not always accurate. I’ve found loans labeled “private student loan” when in fact the loan was federal. I also had a case where the NSLDS file said the interest rate was 3.8%, but the servicer was using 5.25%, so we had to do the legwork to confirm which one was accurate. In addition, RightCapital still requires manual entry of the Standard 10-Year Repayment option, since that doesn’t come in automatically, and is necessary for comparing different options.

Another downside is not being able to do a side-by-side view of the different repayment programs, like what CSLA (and the later-discussed VIN Foundation software) can do. Thus, a little more work is required to see what the major variables, such as total repayment, monthly payment, etc., wind up being, which actually drives the best decision outcome.

One other item is that the RightCapital student loan module has an all-or-nothing approach to strategy, and you can’t select different strategies by the individual loan. Let’s look again at the loans from the couple we used up above:

In this case, all of the Stafford loans belong to one spouse, whereas the MOHELA loan is the only loan for the second member of the couple. I ended up recommending privately refinancing all of the loans that had an interest rate above 4% but leaving the ones which are at 3.28% (and switching payment plans) since the refi came in at 4.25%. There is no way to mark which loans to include or exclude from the proposed strategy, so it still required using Excel to break down the total savings versus continuing on their current plan.

Another thing I’d like to see is better integration of the standard debt module RC has with the student loan module. Right now, on their regular debt analysis tool, you can’t model a refinancing. And on the student loan tool, you can model a refinancing, but you can’t increase the monthly amount contributed. These two tools should interact to fully model the possibilities for a client.

Overall, this student loan planning module is a great leap forward in terms of integration of student loan analysis into the overall plan, but still has work to be done to make it usable in all cases and without some outside calculations needing to be done for certain circumstances. The data feeds from the loan servicers also lack the completeness that tools which use the NSLDS file have.

RightCapital Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

2 |

2 |

2 |

2 |

2 |

Student Loan Planner Excel-Based Calculator

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

No |

Somewhat |

Somewhat |

Yes |

No |

No |

Student Loan Planner is a business entirely dedicated to conducting student loan analysis. Their team has now done 1,000+ student loan projects, and with that has built a tool for analyzing the student loan debts. They make an Excel-based tool available on the website for download by consumers, along with a wealth of other information about student loans.

Student Loan Planner is very much focused on direct-to-consumer work and does not hold itself out as a tool for advisors, but I know a few advisors who use the tool to help them conduct their student loan analysis.

Given the depth of knowledge required to give student loan advice, and the consequences of a mistake, many advisors may want to outsource this aspect of the financial plan to an expert. Student Loan Planner itself is one option to do so, and then the planner can take the recommendations generated from Student Loan Planner and its spreadsheet tool, and then integrate the recommendations into the overall financial plan.

Advantages

The Student Loan Planner calculator is very easy to use, and intuitive for anyone with a passing knowledge of using Excel. Although there is no NSLDS import function, it does allow a planner to type in all the relevant data points, and easily adjust the assumptions for future tax rates, family size, income, etc. It also provides a great table with side-by-side comparisons to see total payments, both in nominal dollars and NPV (Net Present Value) terms, any possible taxes due, year of forgiveness (if applicable), and monthly payment amounts.

Disadvantages

Not only does the Student Loan Planner tool not have the ability to import loan data from NSLDS, it, in fact, asks for the loans to be combined together into one input of the total loan balance and average interest rate. This makes analyzing a household where each spouse has student loans (potentially eligible for different federal programs) more difficult.

In addition, the tool does not have any way to notify a planner which federal repayment program is or isn’t available based on the data. For example, there’s no way to note whether a loan is an FFEL or Perkins loan, each of which have different rules governing what programs they are eligible for. This makes sense, as it’s not designed to be a tool for advisors, but does mean it’s of limited use to an advisor as a standalone tool. As ultimately, using Student Loan Planner requires the advisor using it to have even stronger student loan knowledge themselves, and not rely on the tool for anything beyond the actual calculation of the total repayment and monthly payments.

I’d encourage planners just beginning to learn about student loans to download Student Loan Planner’s spreadsheet to use for their own education, but it is not robust enough for most planners to use without assistance (which, admittedly, Student Loan Planner would likely be happy to be engaged for).

Student Loan Planner Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

1 |

4 |

2 |

2 |

2.25 |

StudentLoans.Gov Repayment Estimator

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

Yes |

Somewhat |

Somewhat |

Yes |

Somewhat |

Yes |

The Repayment Estimator from StudentLoans.gov is a tool directly from the U.S. Department of Education. It’s useful for relatively simple situations, such as a single person with fairly predictable income, but does not have the flexibility of some other tools, and thus isn’t as useful for advisors, especially when looking at more complex client scenarios.

Advantages

The StudentLoans.gov tool allows clients to log in under their account and do analysis with their own data pulling from the DOE’s database. This is great in that the advisor can be confident he/she is working with accurate information, but since there is no way for an advisor to get the data without logging in under the client's credentials, it presents a challenge for advisors to actually use at scale and without compliance concerns.

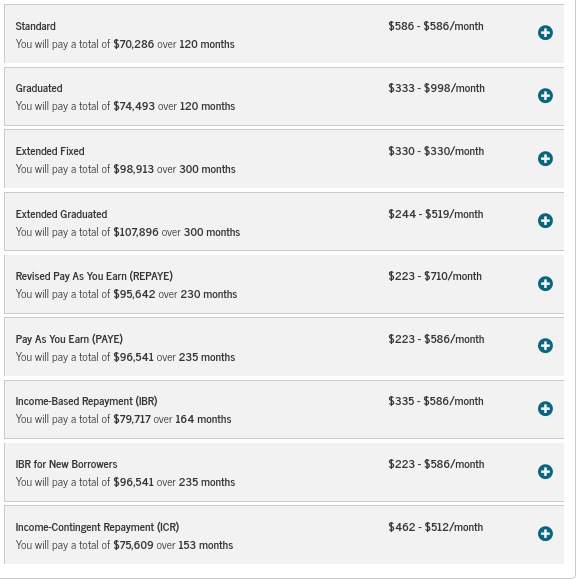

The StudentLoans.gov tool gives information only on the programs the client is eligible for as well, thus eliminating the confusion of attempting to enroll in a repayment program that the loan may not be eligible for. It also generates an easy to understand table comparing all your options, including nominal repayment cost, monthly payments, and timeline until the debt is gone, as shown with an example below:

Disadvantages

The StudentLoans.gov tool is not very flexible. For example, it uses an assumption of 5% annual income increases, and there doesn’t appear to be a way to override that with a more client-specific income trajectory. Similarly, you can enter current marriage and family info, but there’s no way to project the impact of those planned events at a future date. Even though a monthly payment amount will be drastically different for a single person than a married parent of two. Which means the ability to set when one estimates those life events to occur is very important.

You also cannot add information about the debt of a spouse and have that factor into a household-level plan. You could, similar to the Student Loan Planner tool, combine the two spouse's debt into one and manually enter the information, but that doesn’t allow the true depth of analysis to be done (especially relevant when spouses have a significant gap in incomes or debts).

For example, let’s look at two situations identical in aggregate, but different in the details:

|

|

Situation A |

Situation B |

|

Sam Income |

$100,000 |

$45,000 |

|

Sally Income |

$100,000 |

$155,000 |

|

Sam Debt |

$100,000 |

$260,000 |

|

Sally Debt |

$200,000 |

$40,000 |

In both cases the total income is $200,000 and total student loan debt is $300,000, but the correct repayment plan will vary significantly depending on future earnings expectations, types of loans, etc. Not being able to break out each spouse by themselves is a significant limitation with the StudentLoans.gov tool.

Studentloans.gov Repayment Estimator Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

2 |

2 |

3 |

1 |

2 |

VIN Foundation Student Loan Calculator

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

No |

Yes |

Yes |

Yes |

No |

No |

Veterinarians tend to graduate with a significant student loan debt relative to their income, and their student loan burden is a huge barrier to financial security for many veterinarians.

As a result, VIN Foundation tool comes courtesy of the Veterinary Information Network (VIN) website, and while it is nominally intended for their members (veterinarians), the tool is free online and accessible for anyone to use.

Advantages:

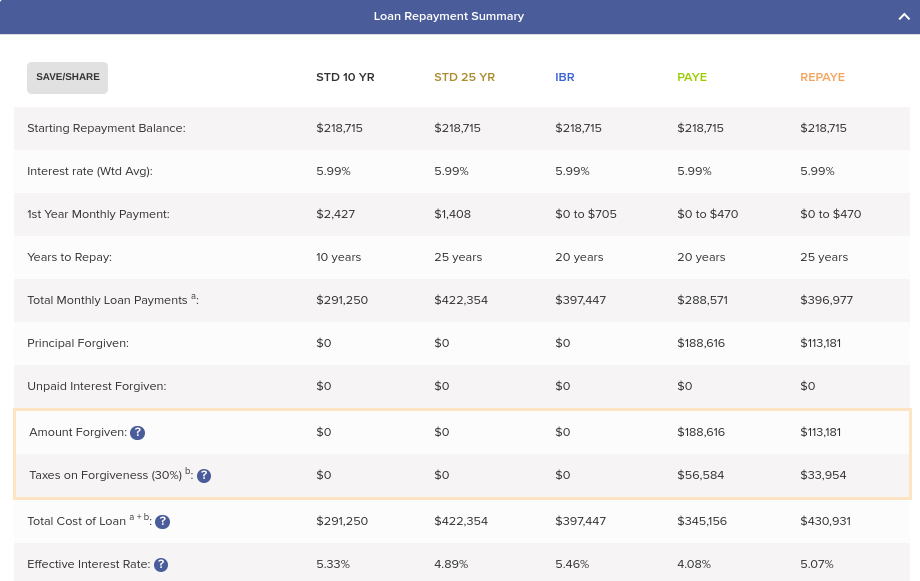

The VIN Foundation student loan tool is actually one of the most flexible tools for student loan analysis. Advisors are able to enter almost any variable they’d ever need to, including manually overriding income assumptions in future years as necessary. You can set future dates for marriage and kids and see how those impact the plan, including toggling between using the MFS and MFJ tax filing status. The software is able to include household level income and debts and provides a variety of tables and charts to show the impact of different repayment plans. An example of the outputs include:

Table showing side-by-side comparison of total repayment info

The simplicity of this table is a helpful starting point to have conversations with clients about what each route means for them both now and over the life of the loan.

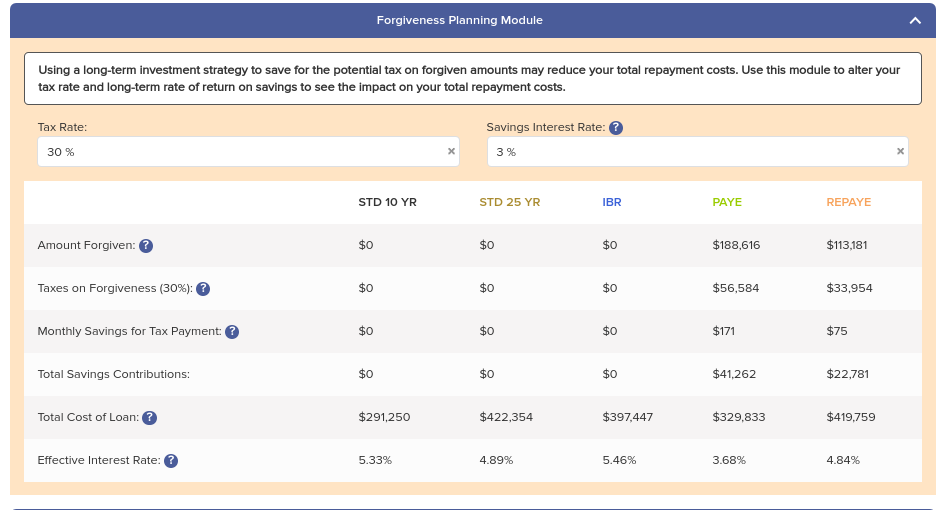

Forgiveness Planning Module to Prepare for the “Tax-Bomb” after forgiveness

If you’re having a client work towards one of the long-term student loan forgiveness programs, planning and saving for the taxation on forgiveness is vital. This can also help when a client is wavering on putting slightly more towards paying down the loan, versus paying the minimum and working towards forgiveness, because oftentimes, the cost of the income-driven plan + savings for the tax bomb is so similar to the amount needed to just pay off the loan that it makes more sense to work towards payoff and just get out from under the enormous debt burden.

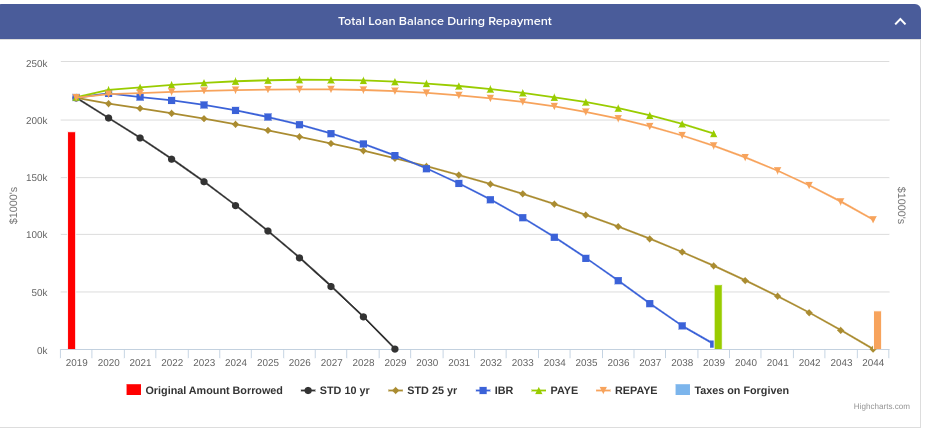

Graph of Total Loan Balance During Repayment:

This graph is very helpful to demonstrate to clients which plans will result in actually paying down the debt, and which don’t. In some cases, the negative amortization of a growing loan balance showing on this graph can help a client weigh the psychological impact of carrying a growing (or stagnant) debt for 20 or 25 years just to pursue forgiveness at the end.

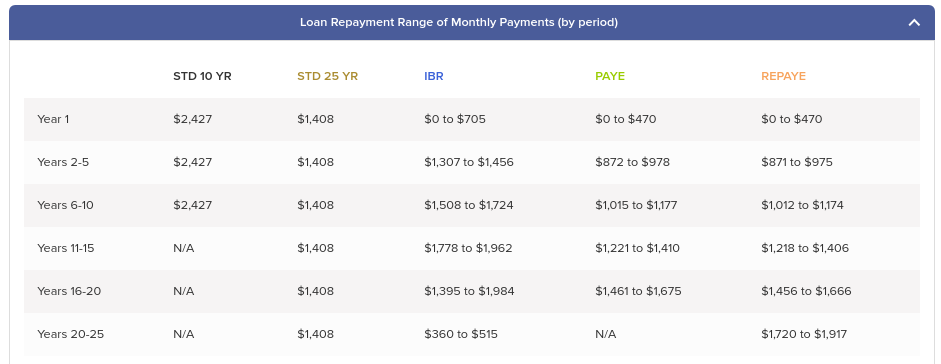

Range of Monthly Payments Across Payment Plans

It’s important for planners to evaluate not just the monthly payment at the start, but how it will grow as income grows and family size changes.

It’s also easy to save the analysis, which is vital given how many times a planner may need to come back to the data.

Disadvantages:

The VIN Foundation tool still requires a tremendous amount of planner knowledge to enter all the inputs properly. And there is no automated way to get data into the program (e.g., an NSLDS import option), so using the software takes a lot of manual entry. In addition, there is nowhere to enter the type of each student loan the client has, and thus there’s nowhere to see which student loan programs the loans are (or are not) eligible for, again forcing the advisor to rely on their own knowledge to know what to model (or not). Private loans are not able to be included in the analysis, either.

VIN Foundation Calculator Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

3 |

2 |

4 |

4 |

3.25 |

Loan Buddy

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

Yes |

Somewhat |

Yes |

Yes |

Yes |

Somewhat |

Loan Buddy was founded by a fee-only financial planner who specializes in working with physicians and thus has a lot of experience looking at significant student loan debt as part of a client plan.

With that advisor perspective, the Loan Buddy team is also looking to find ways to educate the advisor community about student loans and building a mechanism for advisors to easily tap other advisors to assist if they have a complex student loan case. They are also building out an advisor database for consumers to search and find an advisor who specializes in student loans associated with the consumer’s particular profession. Advisors will be able to get leads directly from the database, including the prospects student loan data, so Loan Buddy is both a software tool and potentially a high-quality lead generator.

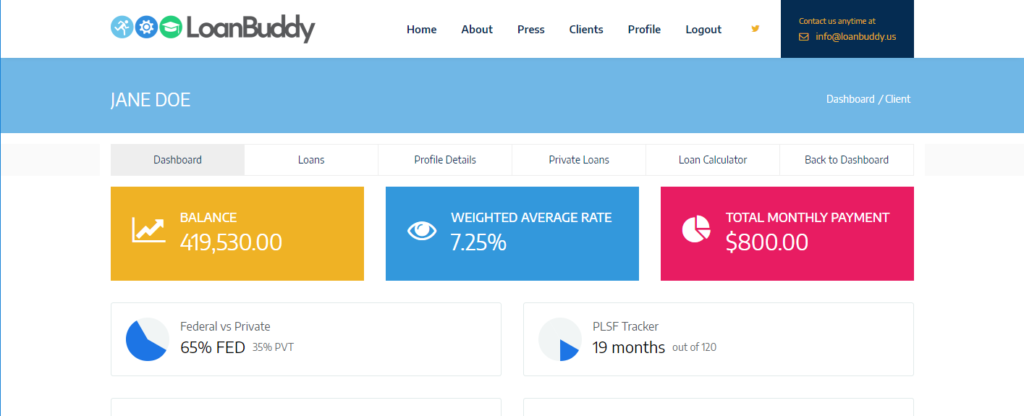

Loan Buddy will also be helpful for advisors looking to market their student loan knowledge. It tracks the overall amount of student loans advised on, as well as average student loan balance. Imagine a prospect calls and says “I have $185,000 of student loans.” It’s incredibly powerful for an advisor to be able to say, “My average client has $215,000 of loans, so I know how daunting that can seem. I’ve advised on over $4,000,000 of loans in the past 3 years and am confident we can find a plan that works for you.”

Notably, at the time of this review, Loan Buddy is primarily just a tool to aggregate information on and review clients’ student loans, but in the very near future, Loan Buddy plans to roll out their full suite of student loan repayment analyses and additional features, and from the demo I conducted, it will be a powerful tool.

Advantages

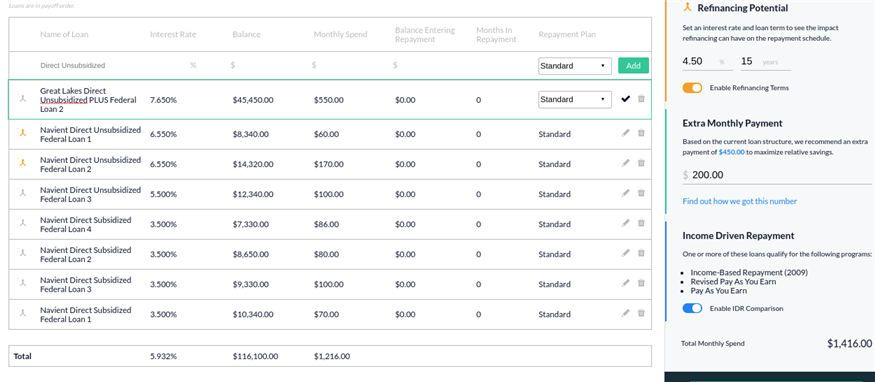

Loan Buddy translates the NSLDS data file into easy-to-digest data in no time. It’s clear exactly what is owed, since when, in what status, the applicable interest rate, and all other important data.

Loan Buddy is also easy to navigate and shows a lot of promise for the future. Of all the companies I spoke to, Loan Buddy seems to have the strongest knowledge around what planners want (not surprising since they were founded by one!), and how advisors would use the tool.

At this point, Loan Buddy builds the most robust history of student loans, which is a big advantage vs. tools that rely only on data aggregation. It can see the entire history of a loan, which is particularly important if there are consolidation loans made up of loans that may make a client ineligible for a particular program based on the disbursement date. This info isn’t available if a program is relying solely on data aggregation feeds.

Another perk of using all the information in the NSLDS file is that it keeps track of the number of months of eligible payments for Public Service Loan Forgiveness, and Loan Buddy pulls that number directly into the overall plan. The PSLF program can be difficult to navigate, so helping clients monitor their progress over time is of huge value to those striving for forgiveness through that program.

In the soon to be released version, all assumptions are adaptable and you can easily adjust for future changes in marital status or family size. Loan Buddy is also building in some guideposts for advisors, so if an advisor attempts to do something that isn’t possible for one reason or another, a message will appear to tell the advisor their current recommendation won’t work. For example, if a client has an FFEL loan and wants to go for PSLF, the system will notify the advisor that the loans must first be consolidated into a direct loan before going for PSLF.

Loan Buddy will also have an integration with First Republic to offer current student loan refinancing rates to borrowers in Zip Codes where First Republic makes loans. The hope is that this integration is the first of several that will make it so an advisor doesn’t have to go outside the system for refinancing rates. In the longer term future, this could potentially even be a spot to apply for and get a refinancing loan for the client based on individual credit history, but that is quite a ways off.

A feature no other system has that Loan Buddy is developing will be a database of available forgiveness programs and grants available to borrowers. Currently, Loan Buddy has populated the database with about 70 state or federal student loan programs, and they will be embedded in the software so that advisors are able to see if a unique program is available based on that client's state of residence and occupation. This database is not live yet, but their team is planning to make it into a robust database of currently available programs that may impact overall student loan repayment plans.

Disadvantages

Loan Buddy doesn’t yet actually do student loan repayment analysis within the software. To date, it relies on the planner to have a robust knowledge of student loans and do their own analysis of which route for repayment is best. It exists primarily just to capture and show (i.e., summarize) the relevant student loan information, so advisors can use it as a framework for discussion. Their full student loan calculator is being released in the coming month, but it will likely be several months until all of the features mentioned here are available.

From the demo I worked through, there are a few drawbacks. Unlike the RightCapital tool, all information about income and family size must be manually entered (since it doesn’t come over from the existing financial planning software data gathering input process), and there are no integrations to any financial planning software.

In addition, the software does not yet analyze a full household, where both spouses have student loan debt, and create a holistic plan; rather, it looks at each spouse individually to develop what plan makes sense for them. While this often is fine, there are situations where looking holistically at the household income and debts results in different recommendations than doing so individually, which Loan Buddy can’t show at this time.

The other concern about Loan Buddy is that they are trying to do many things at once (build the student loan tool, an advisor lead generator, advisor marketing statistics, etc.), and that could mean the core features aren’t developed as quickly as tools that have a narrower focus.

Loan Buddy Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

2 Current (4 Future) |

2 |

3 |

3 |

2.75 |

Pay For ED

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

Yes |

Yes |

Yes |

Yes |

Yes |

Somewhat |

The Pay For ED tool sounds like a promising new solution for advisors, but the platform is not yet live either. I’ve spoken at length with their team but not actually seen a demonstration of the stated capabilities. As with any software, the promised and the delivered can sometimes leave a gap. That said, the Pay For ED team has already successfully built a tool to help with Financial Aid planning (EFC Plus) before students go to college and has clearly done the work to deeply understand the features on a post-graduation student loan repayment tool that would help advisors as well. So this tool seems like it will be very useful if it can really deliver on the promised features.

Advantages

One of the unique features that Pay For ED is touting is a “max earnings” feature, which would show the maximum AGI a couple could have before income-based repayment no longer makes sense. This is very helpful to project ahead of time which plan makes sense for the long-term, given a client’s anticipated income trajectory, especially once you consider the interest subsidy that exists for some repayment plans but not for others. This reverse engineering can help take away some of the “guess-and-check” type work that an advisor may otherwise do to determine which repayment plan is best.

Disadvantages

Pay For ED is a promising tool, but we just don’t know yet whether it will meet the lofty expectations. One concern is that the company appears to be aiming to help across all aspects of planning for, paying for, and paying down debt from college education. The knowledge necessary to adequately plan how best to structure assets and pay for college is entirely different than the knowledge needed to repay existing student loan debt. A company with a somewhat wider focus may not have the precision on student loan repayment (or the readiness to build out advisor-relevant features) that a tool fully dedicated to that problem alone would have.

Pay For ED Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

TBD |

TBD |

TBD |

TBD |

TBD |

PayItOff

|

Importable Data |

Household Level Analysis |

Adaptable Assumptions |

Side-by-side comparisons |

Include Private Loans |

Filters by Available Plan Type |

|

Yes |

Yes |

Somewhat |

Somewhat |

Yes |

Somewhat |

PayItOff is the most recent entrant into this space, and their platform has about 60 advisors using a beta version. The full rollout of their tool will be unveiled during XYPN LIVE’s FinTech Competition in late September of 2018 as one of 6 finalists in the competition. The company was founded by a software engineer whose personal experience managing his student loans led him to realize just how much of a need there is for robust tools to analyze the various repayment options.

Advantages

PayItOff is the only tool to offer three different ways of bringing in the data: NSLDS data file upload, data aggregation links to loan servicers, and manual entry. This flexibility is the best of both worlds in that the live feeds from servicers have the most up to date data, but the NSLDS file contains the best historical information. They are still working on reconciling if any discrepancies arise from the two sources, but having both sources is a unique feature. The other unique data-gathering aspect of PayItOff is that it allows clients to link or enter other liabilities they may have as well, so their total debt can be taken into account when an advisor is looking to figure out how much in monthly debt payments a client can afford.

Once loans are in the system, you can enter available information on private refinancing options, and adjust any relevant information on the loans under review, such as current payment plan, months in repayment, etc. An advisor can also differentiate the best option for different loans. So, in the scenario mentioned above with a split of using the standard repayment plan and private refinancing, the advisor can use the checkmarks on the left of the screen to include or exclude certain loans from the refinancing calculation.

PayItOff has an algorithm to determine the recommended extra monthly payment to maximize relative savings. Advisors can then adjust the extra amount paid monthly based on the client’s actual ability to pay more each month.

Spouses can be linked in the system so you can aggregate household information together and come up with the best recommendations for the entire household unit.

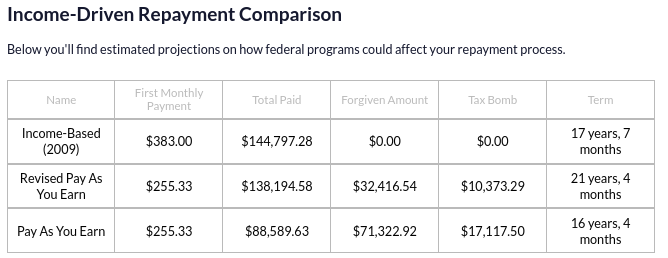

For clients pursuing Income-Driven Repayment, you can quickly see which plans you are eligible for and how they compare to one another, as shown with the table below.

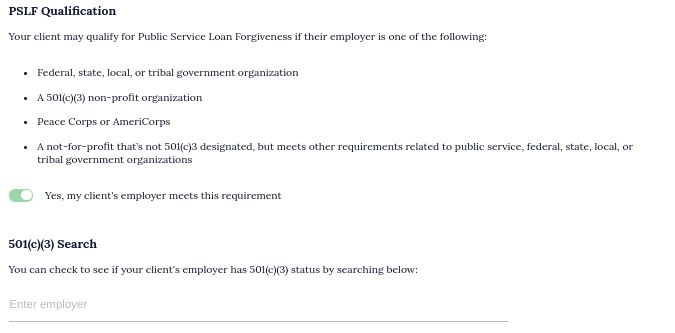

Something else I liked on the PayItOff app is their 501(c)(3) search for PSLF eligibility. It can sometimes be unclear if an employer is eligible for the program, so embedding a search tool is a useful feature. It isn’t perfect, as the tool only searches for entities that have the 501(c)(3) status, and there are some other non-501(c)(3) entities that are also eligible for PSLF, but it’s a good starting point.

Disadvantages

Overall, I found PayItOff to be difficult to navigate. It was often unclear to me where a piece of information comes from, or how to edit that information. Editing the imported loan data proved more difficult than I anticipated, and there were a few scenarios I struggled to model and was told afterward that analysis was not yet available.

Also, unlike a couple of the other tools, you aren’t able to see the loan history even if you upload the NSLDS file. This proved to be limiting, as I wasn’t able to easily see loan disbursement dates, which was confusing on a case I tried to run. The loan info showed all of the loans as being on the “standard” plan, which should be 10 years of level payments. But, since the loans had different repayment start dates, the system was telling me it would take 21 years until all loans are fully paid off. While I can see some scenarios in which this would play out if a client had some undergraduate debt they began repaying before taking on graduate debt, it wasn’t easy to understand how the system was arriving at the payoff term.

Currently, the assumptions for income, family size, and marital status can’t be altered, so it’s hard to truly project the terms of repayment as those items change.

There is a lot of potential here given the scope of features they have or are planning, but to right now the difficulty navigating the system makes it hard for me to recommend it as a comprehensive tool.

PayItOff Overall Score (1-4 scale):

|

Features |

Ease of Use |

Quality of Output |

Flexibility |

Overall Score |

|

3 |

2 |

2 |

2 |

2.25 |

What Advisors Want In Student Loan Planning Tools Going Forward

There are some promising student loan planning tools coming out for financial advisors, but nothing yet on the market that is truly a complete solution for student loan analyses. None of the tools I reviewed have all of the criteria used as a starting point for what advisors would want, though some are much closer than others.

In addition to the list discussed earlier, fellow advisors provided the following as things they’d love to see a student loan repayment tool do:

- Integrate with advisor CRM and comprehensive financial planning software tools (if not already part of the planning software).

- Automate reminders for income recertification for clients on income-driven plans, or integrations to push those reminders into the advisor’s CRM. (Each year a borrowing client’s income has to be recertified to recalculate payment amounts on IDR plans).

- Import current refinance rates from a set list of private refinance companies (e.g., SoFi, Earnest, Common Bond, etc.) to make it easier to see what is actually available currently in the private refi market.

- Database of available forgiveness programs linked to the occupation inputted by the advisor or client (i.e., if someone inputs “teacher,” all federal AND state teacher forgiveness programs would be brought up on a separate tab as considerations for the advisor to look at).

- Viewing of past loan consolidations.

- Cost impact of using MFS tax status (or not) when considering whether to use the REPAYE plan as a married couple.

Overall Takeaways on Student Loan Analysis Tools

Right now, there is no tool that truly can be called the go-to solution for student loan repayment analysis. Many advisors end up using some tools for certain clients that are simpler and having to do much of the analysis using Excel or other manual calculations for the more complex client situations.

However, it looks like we are on the cusp of getting advisors the tools to really support clients in making what is one of their most important financial decisions in many of their young lives. Given the competition in the area and the tremendous need, I anticipate that 12 or 24 months from now the tools above (and perhaps others!) will look dramatically different than they do today.

SUMMARY CHART:

Disclosure: Michael Kitces is a co-founder of XY Planning Network, which was mentioned in this article.