Executive Summary

When President Donald Trump oversaw the passing of the Tax Cuts and Jobs Act (TCJA) in 2017, substantive tax reforms were made with the intention of promoting economic growth that affected corporations, small businesses, and individuals. With the upcoming election in November, though, former Vice President and Democratic presidential nominee Joe Biden has proposed a tax plan that challenges several aspects of the current system in an effort to increase Federal tax revenues and address income/wealth inequality.

One of the key features of Joe Biden’s proposed plan is for ordinary income brackets to be adjusted for individuals with annual incomes over $400,000 (although whether this threshold applies to individuals or joint filers remains unclear), increasing the top tax bracket to the pre-TCJA rate of 39.6%. The income brackets for those with annual income levels under $400,000 will remain unaffected.

Biden’s plan also includes the elimination of the Qualified Business Income (QBI) tax deduction for pass-through business owners (e.g., partnerships, LLCs, S corporations, and sole proprietors) whose individual annual income is $400,000 or more, in effect, potentially increasing the tax bracket for high earners by 10% (from 29.6% for those eligible for the QBI deduction to the proposed highest rate of 39.6%). The plan would also cap the value of the rate at which itemized deductions can be taken to 28%, which affects those in the tax brackets above 28%, as their rate to determine itemized deductions would be reduced from their income tax bracket.

Another feature of Biden’s tax plan is a flat retirement contribution credit, as determined by a specific percentage (currently anticipated to be 26%) of the contribution amount to replace deductions of those retirement account contributions. This would, in effect, lower the tax burden for taxpayers in tax brackets under the proposed set rate (incentivizing taxpayers in lower tax brackets to contribute to tax-deferred retirement accounts), while increasing it for taxpayers in brackets over the proposed rate. Financial advisors who want to prepare for an expected Biden victory might consider accelerating income and deductions into 2020 for high-income earners because, for this group, income tax rates may be higher and deductions not as favorable if the passage of Biden’s tax plan does come to fruition. Accordingly, year-end Roth conversions may be a good strategy for some high-income earners to forgo the 26% credit in the present for the benefit of tax-free distributions in the future.

Enhancements to personal income tax credits made by the proposal include a higher Child Tax Credit (increased from $2,000 for children under 17 to $3,600 for children under 6 and $3,000 for all other children under 17), Child and Dependent Care Credit (from $3,000 to $8,000 for one child, and from $6,000 to $16,000 for two or more). The First-time Homebuyer Credit would be reintroduced as a refundable and advanceable credit of up to $15,000, and a brand-new proposed Caregiver Credit would provide $5,000 for informal long-term caregivers.

Long-term capital gains and qualified dividend tax rates would increase to ordinary income tax rates for income over $1 million under the proposed Biden plan (with the 3.8% surtax on net investment income to remain in place), and 1031 Exchanges would be eliminated for taxpayers with annual income over $400,000. Some strategies to mitigate the impact of these proposed changes would be to target lower annual capital gains realized, use municipal bonds for their (largely) tax-free character, reduce investments in the portfolio that produce dividends, take advantage of the tax deferral of investment-only variable annuities (for accredited investors, Private Placement annuities can also be a useful option), and use installment sales to regulate annual income levels, keeping them under $1 million as much as possible.

Additionally, Biden’s tax plan proposes to eliminate the step-up in basis rules that currently apply to inherited assets (that are not considered Income In Respect of a Decedent), which would impact both higher- and lower-earners potentially facing a significant and problematic tax bill on inherited assets. Thus, life insurance could see renewed potential as a tool to provide liquidity and/or mitigate the burden of a high tax liability resulting from the inheritance. Alternately, a more structured sale or gifting strategy throughout the owner’s lifetime can be a good way to mitigate taxes for the beneficiary should Biden’s plan pass.

A final key feature of the proposed tax plan would be a 50% reduction of the exclusion amount for estate and gift taxes, from $11.58 million to the pre-TCJA amount of $5.79 million. To be cautious, advisors may want to encourage their clients to use as much of their exemption in 2020 in case Biden is elected to office and his tax plan is approved. Other strategies that can be considered to deal with a smaller exemption in the long-term can potentially include the use of Grantor Retained Annuity Trusts (GRATs), Charitable Lead Annuity Trusts (CLATs), and sales to Intentionally Defective Grantor Trusts (IDGTs).

Ultimately, the key point is that even though there is much that can be planned for at this stage prior to the election – regardless of who wins the race – the most important thing for advisors to do in the present moment is to educate themselves (and their clients) about the impact that each candidate’s position will have on them, and to help them plan accordingly as election results come in!

Psst! I’ve got a secret to tell you. In just a little over a month, there’s going to be a really, really big election!

Thanks to the enormous power U.S. Presidents yield (which seems to be growing with each Presidency to overcome an increasingly gridlocked Congress), all presidential elections are big deals. But this one might be bigger than most. Not only are we electing a President to help us continue to navigate the worst global pandemic in more than a century, but perhaps at no time in our country’s history, since the Civil War, have the ‘two sides’ in our country been more divided… over everything from where, when, and how our children should be going to school, to how we should continue to reshape our tax policy to promote economic growth and equality under the law.

President Trump, the incumbent, oversaw one of the biggest revisions to the Internal Revenue Code in U.S. history with the passage of the Tax Cuts and Jobs Act (TCJA) in 2017 under a Republican-controlled House and Senate. While there’s always the chance for further changes, by this point, most taxpayers know what to expect from any additional 'Trump tax bills', which have tended throughout towards lower tax rates, business-friendly tax incentives, and retaining the popular individual tax deductions that remain.

By contrast, many taxpayers and clients are still learning about the agenda from Democrats should they regain power, and in particular, former Vice President Biden’s tax plan. In what is likely to be of little surprise to most Americans given the Democrats’ party platform, the cumulative tax proposals supported by presidential candidate Biden would create a more progressive tax system (which in tax policy terms means lower tax rates on lower-income individuals and higher tax rates on higher-income individuals) than we have today.

What might surprise many clients (and even some advisors) however, is just how progressive the sum of his proposed changes might be for certain high earners… which is important both for understanding the future implications on affected clients’ financial plans, but also because the potential for 2021 to be a major year of tax legislation that could influence tax planning today, through the end of the year (after the election outcome is determined), and into early 2021 as new legislation is finalized and potentially passed.

Key Elements Of Biden’s Proposed Tax Plan Changes To Ordinary Income Tax Brackets

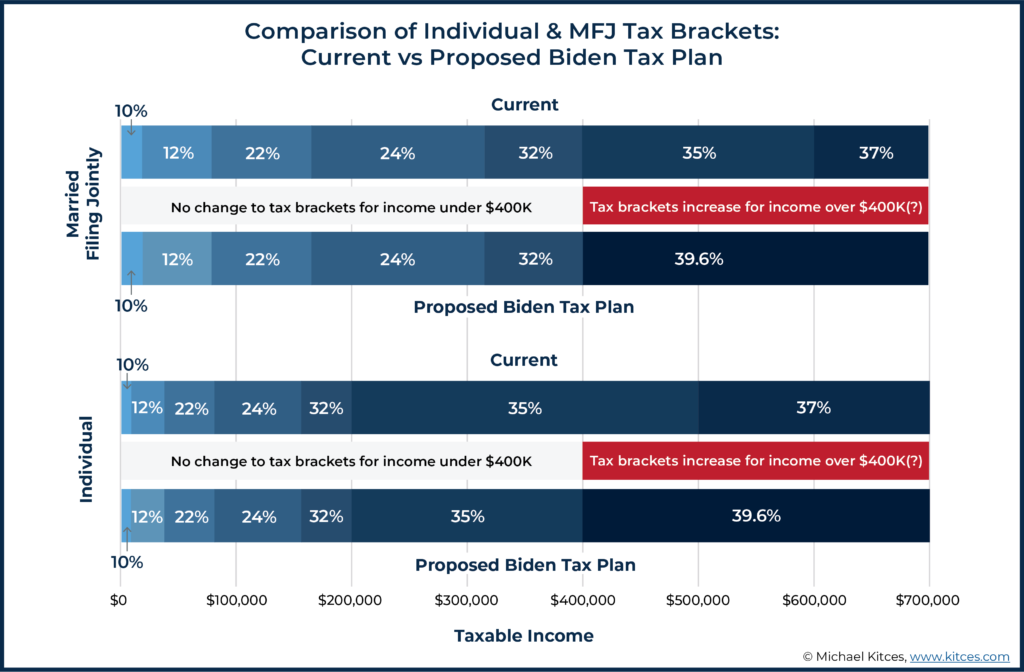

The centerpiece of candidate Biden’s proposed changes to ordinary income tax brackets is a pledge not to increase tax rates on those making less than $400,000, and that various changes – from new income tax brackets and restrictions on deductions – would only impact earnings above the $400,000 threshold.

On the other hand, while the scope of Biden’s prospective tax increases is limited only to those above those thresholds, projections by the Penn Wharton Budget Model suggest that those earning that amount or more would see their after-tax income drop by nearly 18%! Similarly, a separate estimate by the non-partisan Tax Policy Center found that Biden’s “plan would raise taxes on households in the top 1 percent of the income distribution (those with income more than $837,000) by an average of about $299,000, or 17.0 percent of after-tax income.”

In practice, though, such tax rate increases on top earners are only partially attributable to an increase in tax brackets, and instead are largely attributable to other tax policy changes that would restrict other tax preferences or deductions for those whose income exceeds the $400,000 threshold.

Biden Tax Plan Would Increase The Top Ordinary Income Tax Rate (Back) To 39.6%

One issue that always tends to garner a lot of interest is the top marginal income tax rate proposed by a candidate. To that end, Vice President Biden has proposed a (relatively?) modest, but immediate, increase of the top ordinary income tax bracket from the current top rate of 37%, to the top pre-Tax Cuts and Jobs Act rate of 39.6%. Absent legislation, this change is actually already scheduled to occur, as a part of the so-called 'sunset' of the Tax Cuts and Jobs Act in 2026; by contrast, Biden’s proposal would advance the 2026 date forward to 2021 (or the soonest that his tax legislation could be implemented).

Notably, though, while the Biden proposal would ‘only’ increase the top ordinary income tax rate to its pre-TCJA level of 39.6%, it would lower the income threshold at which that top rate would apply.

More specifically, in 2017 the 39.6% ordinary income tax bracket did not apply to single filers until they had taxable income of more than $418,000. And it didn’t apply to joint filers until they had taxable income that exceeded $470,000!

Now, some four years later, Biden would have the same rate begin to apply to income at ‘just’ $400,000. By contrast, in 2020, single filers with $400,000 find themselves ‘comfortably’ in the 35% bracket (they can have more than $100,000 of additional income before being ‘bumped’ to the top 37% rate). While joint filers with the same income would in ‘just’ the 32% bracket (albeit at the upper-end), such that a 39.6% bracket at $400,000 would effectively obliterate the current 35% tax bracket for married couples (who would instead jump from 32% to 39.6% at the new $400,000 threshold).

Nerd Note:

It is not entirely clear whether the $400,000 income threshold would apply to single filers, joint filers, or both. Currently, Vice President Biden’s website states only that “Joe Biden will not raise taxes on anyone making less than $400,000. Period.”

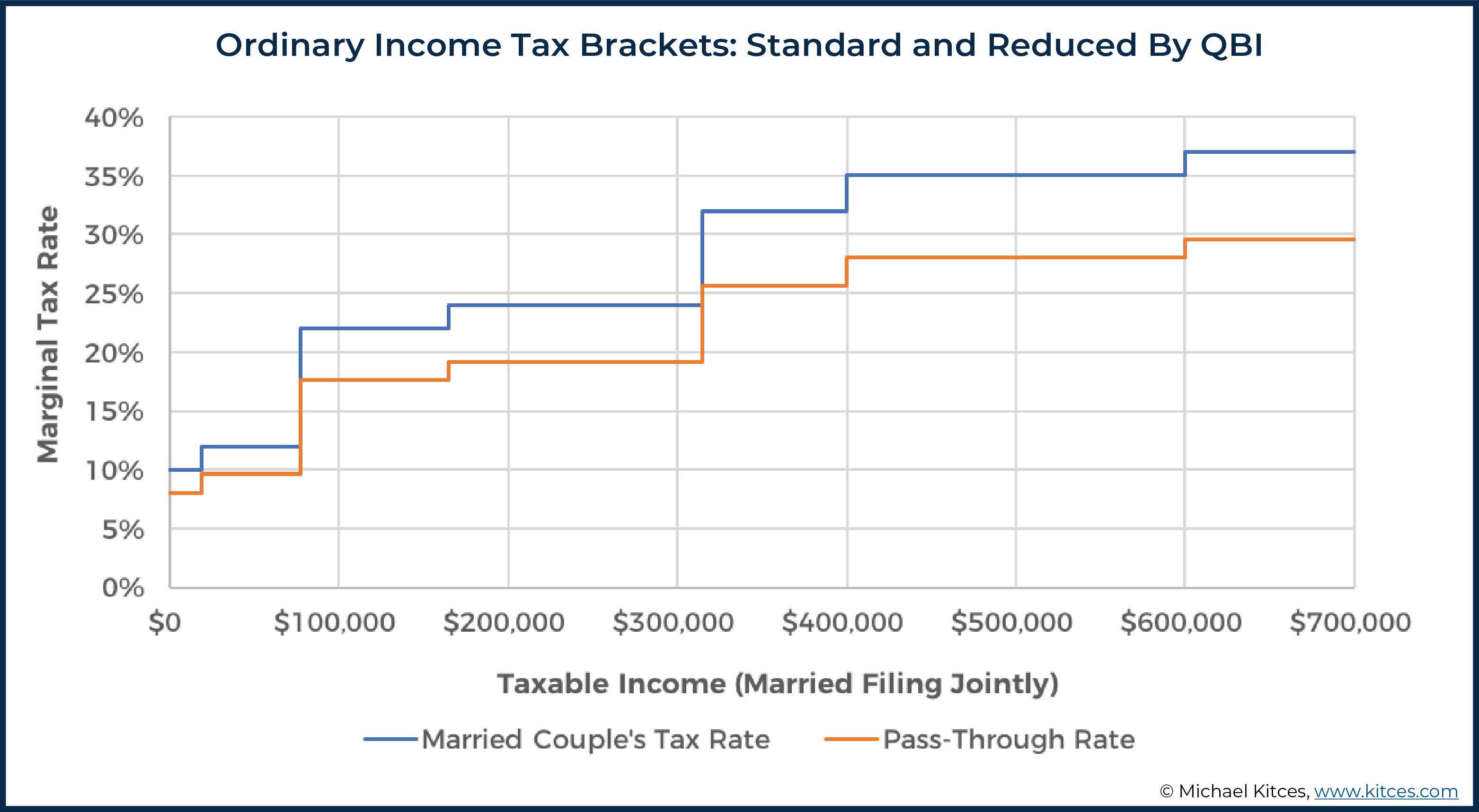

Biden Tax Plan Would Eliminate The Qualified Business Income (QBI) Tax Deduction For High Earners

$400,000 seems to be the ‘magic’ number that Vice President Biden has settled on when it comes to figuring out whose income tax liability should be left alone, and who should be responsible for picking up more of the overall tax burden. To that end, in addition to imposing a ‘new’ top tax rate of 39.6% on those taxpayers with $400,000 or more of income, the Biden tax plan also proposes to completely eliminate the Qualified Business Income (QBI) deduction for such individuals as well.

Under current law, the Qualified Business Income (QBI) deduction allows various “pass-through” business owners (including owners of partnerships and LLCs, S corporations, and even sole proprietors) to deduct 20% of their business income from their business income, such that they are only taxed on the remaining 80% of their income. This effectively reduces the tax bracket for pass-through business income by 20% of the otherwise-normal tax rate, such that the 10% ordinary tax bracket is only 8% for business income, the 24% bracket is only 19.2%, and the top 37% bracket is only 29.6%.

Notably, high-earning business owners of Specified Service Trade or Businesses (which includes doctors, lawyers, consultants, and unfortunately financial advisors) see their QBI deductions completely phased out once taxable income (for 2020) exceeds $426,600 for joint filers (half that amount for single filers), under the auspices that those who have high income from their own labor are not intended to receive the benefit (only those who are creating jobs for others and generate revenue and profits from those jobs beyond the owner/founder). Still, though, owners of pass-through businesses that are not classified as Specified Service Trade or Business can continue to enjoy the benefits of a QBI deduction with income of any amount (provided that the business pays enough wages and/or owns enough depreciable property to support the deduction).

By contrast, under the new Biden proposal, the QBI deduction would no longer be available to anyone earning more than $400,000/year, regardless of whether their pass-through business was a Specified Service Trade or Business, or not. And because the QBI phaseouts have in the past been determined based on an individual’s own tax return, ostensibly even if one or multiple businesses all stayed under the $400,000 threshold, as long as the business owner’s income reaches or exceeds the threshold, the QBI deduction would be lost… even if the income threshold was breached due to non-business (i.e., other wage or portfolio) income!

As a result, while the Biden tax plan would ‘only’ raise the top tax bracket by 2.6% (from 37% to 39.6%), the removal of the QBI deduction would, for pass-through business owners, result in an additional tax bracket increase of 10 percentage points (from the QBI-adjusted 29.6% under current law, to the new not-QBI-eligible 39.6% bracket under the Biden tax plan).

Nerd Note:

REIT dividends and net profits from publicly traded partnerships are also currently eligible for the 20% QBI deduction, regardless of a taxpayer’s income. It appears that, under the Biden tax plan, taxpayers with income in excess of $400,000 would no longer be able to claim a QBI deduction for these amounts too.

Biden Tax Plan Would Cap The Value Of Itemized Deductions At No More Than 28%

For high-earning individuals, the news doesn’t get much better on the deduction side of things. Specifically, the Biden tax plan calls for resurrecting an Obama-era proposal to cap the value of itemized deduction at 28%.

For taxpayers in the 10%, 12%, 22%, and 24% marginal brackets, this proposal would have little to no impact. Taxpayers in the 32%, 35%, 37%, or the proposed ‘new’ 39.6% bracket, on the other hand, could see a substantial increase in their effective tax rate. For instance, a client in the proposed ‘new’ 39.6% bracket who earns $5,000 and then immediately donates those dollars to charity would receive a $5,000 x 28% = $1,400 deduction. But their original tax bill on that $5,000 of income would have been $5,000 x 39.6% = $1,980, which in turn would still leave them with a $1,980 - $1,400 = $580 tax bill (the 11.6% tax rate differential) attributable to the $5,000 of income that they had earned and immediately donated and didn’t even have anymore!

Accordingly, the more a client’s marginal income tax bracket exceeds the 28% proposed cap for the benefit of an itemized deduction, and the greater the extent that the individual relies upon (or benefits from) itemized deductions reducing their tax bill, the greater the risk this proposal has to reduce their net-after-tax income. At a top tax bracket of 39.6%, this proposal would effectively result in a tax bracket as high as 11.6% on funds that were already received and donated.

Nerd Note:

While the newly proposed Biden tax plan cap on itemized deductions would most obviously impact charitable donations of income that are earned and subsequently donated (but leaves a tax bill behind), the cap would apply on any and all itemized deductions. Thus, for instance, the tax benefits of the mortgage interest deduction would also be more limited, as would the payment of state and local taxes (at least up to the $10,000 limit still available), and the other few remaining itemized deductions for typically-higher-income earners. On the other hand, for the nearly 90% of (generally lower and middle-income) households that no longer itemize deductions and instead claim the standard deduction, the new itemized deduction 28% rate cap would have no effect.

Eschewing Push-Pull Tax Strategies To Instead Stuff Income And Deductions Into 2020 Year-End Under A Biden Victory

The time has not yet arrived to implement planning strategies designed to mitigate the impact of Vice President Biden’s income tax proposals on high earners. The outcome of the presidential race is still far from certain, and even if Vice President Biden wins, if the Senate stays red (or much less likely, at least at this time, the House flips red), a future-President Biden would have a tough (if not impossible) time implementing many (if not all) of these proposals. But it’s never too early to start thinking about what high earners might want to consider if Democrats seize control of the White House and the Senate (and retain control of the House) after the November election.

One bit of good news for high earners is that, if such a “blue wave” were to occur, most of the income tax planning strategies to deal with the changes would be fairly straightforward. Of which the most popular will likely be a race to accelerate as much income, and as many deductions, as possible into 2020 before the year ends.

Notably, the joint acceleration of both income and deductions as a strategy is fairly odd, and likely a combination that many financial advisors and tax planners have not utilized before. Because while tax rates have changed quite a bit in recent history (especially at the top end of the income spectrum), whenever those changes have occurred, the planning has typically involved a “push-pull” approach.

If tax rates were expected to decrease, the strategy was to push off income into the future when it would be taxed at a lower rate, and then pull deductions forward into the current year, to have them offset income taxed at the higher rate. Conversely, if tax rates were expected to increase, the strategy was to push deductions to the future, when they would be able to offset income that would otherwise be taxed at the higher rate, and to pull income forward into the current year, to pay tax on it at the lower rate.

Put differently, the value of deductions has generally correlated with the income tax rate. A higher tax rate made a deduction more valuable, while a lower tax rate made a deduction less valuable, and the deductions were shifted either forward or back to whichever year was anticipated to yield the highest tax rate savings.

Yet Vice President Biden’s proposal to increase the tax rate that high earners (over $400,000) would pay, while simultaneously reducing the value of those deductions (via the introduction of a cap on the maximum benefit for itemized deductions) turns that ‘equation’ on its head. Should such proposals become law in the future, high earners may pay a lower income tax rate today, but if they’re in the 32% marginal income tax bracket or higher (the first bracket that is above the 28% proposed cap on itemized deductions), their deductions might also be worth more today than they might in the future).

Accordingly, if Democrats take control of the White House and both chambers of Congress, year-end tax planning for high earners in 2020 might be all about stuffing their returns with as much income and with as many deductions as possible! To that end, year-end Roth IRA conversions would become a particularly attractive option for some high earners, as Roth conversions represent an easy (possibly the easiest) way for a taxpayer to pull forward what would otherwise be future income into the current year.

Biden Tax Plan Would Implement A Flat 26%(?) Credit To Replace Deductions For Contributions To IRAs, 401(k)s, And Similar Retirement Accounts

Perhaps the Biden-proposal that would create the biggest planning challenges and opportunities for the greatest number of advisor’s clients is the proposal to eliminate the tax deduction for contributions to IRAs, 401(k)s, 403(b)s, and other pre-tax accounts, and to replace it with a new credit that would be (regardless of a taxpayer’s income) equal to a specified percentage of the amount contributed to the pre-tax account. Details regarding the exact percentage haven’t been made available, but the Tax Policy Center estimates that 26% would be revenue-neutral, and thus, represents a likely outcome (and one, for simplicity’s sake, we shall assume for the remainder of this article).

Here’s what the Biden website has to say about the proposal:

Equalizing the tax benefits of retirement plans. Current tax benefits for retirement savings provide upper-income families with a significant tax break, while providing a limited benefit for low- and middle-income workers. Biden will equalize benefits across the income scale, so working families also receive substantial tax benefits when they put money away for retirement.

In other words, the intention of the proposal is to adjust the current system away from a world where the dollar benefit of retirement contribution is higher for high-income individuals (who receive the tax deduction at their higher rates) and lower for lower-income individuals (who arguably need the benefit more given their more limited means to save for retirement in the first place), and instead to make the dollar benefit of tax savings for making contributions to a ‘pre-tax’ retirement account equal for all taxpayers. Thus, instead of a high-income earner saving $3,700 for a $10,000 contribution (at the top 37% bracket) and a low-income earner getting a tax benefit of only $1,000 or $1,200 (at the bottom 10% or 12% brackets), contributing $10,000 to a 401(k) would result in a flat credit of $2,600 (regardless of whether they were in the 37% bracket or the 10% or 12% brackets). The rules for contributions to Roth-style accounts, such as Roth IRAs and Roth 401(k)s, would be unaffected (since they are not pre-tax in the first place, and high-income earners are already absorbing the full impact of taxation upfront, at their current top tax brackets).

Relative to current law, creating a flat, revenue-neutral credit, would have the effect of lowering the tax burden for anyone with an income tax rate under 26% (and would even more-than-double the current tax savings of contributing to retirement accounts for those in the bottom tax brackets), while simultaneously increasing the tax rate for anyone with an income tax rate above 26% (who, similar to the cap on itemized deductions, would end out paying taxes on their income and receiving a tax benefit that would only partially offset the associated tax liability).

Planning For The Biden Tax Plan’s Flat Credit For Contributions To Traditional-Style Retirement Accounts

A change to the tax benefits for contributions to traditional-style retirement accounts from a (marginal-tax-rate) deduction into a (flat) credit would have substantial impacts to retirement planning for individuals across the income spectrum, and could also lead to a number of very unintended consequences.

Taxpayers with a marginal income tax rate above 26%, for instance, would be heavily incentivized to avoid traditional retirement accounts altogether, and instead, opt for Roth-style accounts. This would be particularly true for clients in high-income tax brackets today who also expect to be in relatively high-income tax brackets in the future.

To understand why, consider a client in the ‘new’ 39.6% bracket proposed by Vice President Biden who earns and then makes a $20,000 contribution to a traditional 401(k) and receives a $20,000 x 26% = $5,200 income tax credit. A $5,200 tax credit sounds nice, but since the $20,000 of earnings would no longer receive a deduction and would still be included in the client’s income, the client would have a gross income tax liability attributable to the $20,000 (put in the 401(k)) of $20,000 x 39.6% = $7,920.

Thus, such a client would have a $7,920 income tax - $5,200 retirement tax credit = $2,720 net tax liability attributable to the earnings, even after they’re fully contributed to the 401(k). Not coincidentally, that $2,720 amount represents a net 39.6% - 26% = 13.6% tax rate on that income in the year of contribution.

But at some point, those dollars will have to be distributed from the still-pre-tax account, right? Which means they’ll be subject to income tax again when they’re distributed!

And what if the client happens to still be in the 39.6% bracket at that time? Well, that means the cumulative tax rate on the contributed funds would equal a whopping 39.6% + 13.6% = 53.2%!

Oh… and it gets worse. Since the contribution would no longer be deducted from income on the Federal return when contributed to the 401(k) (because it generates a separate tax credit on another line of the tax return instead), the contribution would still be included in the Adjusted Gross Income calculation that typically carries down to the state level too. Which means, absent state legislation to the contrary, the formerly-pre-tax retirement contribution may end out being fully taxable at the state level when contributed. Furthermore, because the retirement account itself is still pre-tax, the balance might be fully taxed twice at the state level, when it shows up again in Federal Adjusted Gross Income as a withdrawal in the future (which may be ameliorated by state legislation to create ‘basis’ in the retirement account for state income tax purposes, but given that basis wouldn’t be there for Federal income tax purposes, it would be, to put it mildly, ’not fun to keep track of’)!

The Benefits Of Roth-Style Accounts For High-Earners Under The Biden Tax Plan

The ‘simple’ solution to this potential disaster of a tax situation for high-earners contributing to pre-tax retirement accounts? Don’t. Use Roth accounts instead.

As while in the past, top earners often found greater benefit in contributing to pre-tax accounts – claiming the tax deduction at today’s top rates – and deferring withdrawals to the future at hopefully lower tax brackets in retirement, with a flat credit for retirement contributions, the equation is flipped upside down.

Instead, it will suddenly be better for high earners to forgo the 26% credit today (and pay tax at whatever your income tax rate is), but be able to enjoy the tax-free distributions in the future (without the potential for partial or total Federal or state double-taxation on the dollars at contribution and withdrawal). It may be far from ideal for some high earners who count on the tax break provided by today’s 401(k), deductible IRA, etc., but at least it would limit the tax rate to no more than the ‘new’ 39.6% rate!

Compared to a potential 53.6% Federal rate (plus state!) for top earners, Roth accounts for high earners in the future will be a steal!

It’s also worth noting that this significant planning issue would not be limited to only those in the highest tax rate now and in the future (though it would be most pronounced for them). Others in lower-but-still-higher-than-26% brackets could also feel the sting. An individual in the 32% tax bracket would still face the potential of having ‘only’ a 26% credit at the time of contribution, but a full 32% tax rate at withdrawal, for a total tax rate of 38% (compared to ‘just’ 32% for contributing to a Roth-style account upfront under the new rules if implemented).

How Tax-Free Roth Accounts Become Less Valuable (And Traditional IRA Accounts Become More Valuable) For Younger Low-Income Earners Under Biden’s Tax Plan

While replacing a deduction with a flat 26% credit under the Biden tax plan would lead to more high-income earners contributing to Roth-style accounts, it would have the opposite effect for lower-income taxpayers.

For instance, whereas clients in the 12% ordinary income tax bracket today have limited incentive to contribute to a traditional-style retirement account (because the deduction doesn’t mean as much in terms of dollars, where a $1,000 contribution at a 12% tax rate produces ‘just’ $120 of tax savings), a contribution to the same account under the Biden proposal would more than double the associated tax benefit ($120 of tax savings today vs. $260 at a 26% credit under the Biden proposal)!

Indeed, somewhat incredibly, the net result of the implementation of a 26% flat credit for contributions to a traditional-style retirement account could be a complete ‘180’ of the current retirement plan contributions paradigm. Whereas today, high earners are often driven to contribute to pre-tax accounts (because of the relatively large reduction in their current tax bill), and low earners tend to favor Roth accounts because of the minimal benefit they receive from making contributions to pre-tax retirement plans, if the Biden proposal were to become law, it’s hard to imagine that more lower earners wouldn’t opt for the 26% credit (as Biden's plan incentivizes the use of traditional retirement accounts for low-income earners more than the current system), while high earners would almost certainly opt to use Roth-style accounts!

New And Expanded Personal Income Tax Credits Under Biden Tax Plan

Vice President Biden’s progressive tax proposals are further bolstered by an array of new and expanded credits, primarily targeted at lower- and middle-income households where they are most commonly utilized.

Such personal tax credits include:

- Child Tax Credit – The current credit of $2,000 per child under age 17 would be increased to $3,600 for children under age 6, and $3,000 for all other children under age 17.

- Child and Dependent Care Credit – The current credit of a maximum of $3,000 for one child, and $6,000 for two or more children would be expanded to a refundable credit of $8,000 for one child, and a whopping $16,000 credit for two or more children.

- First-time Homebuyer Credit – A new refundable and advanceable credit of up to $15,000. While specifics surrounding the credit have not yet been made public, the credit would most likely mirror the First-Time Homebuyer Credit first introduced during the (George W.) Bush administration in 2008, and later expanded by the Obama administration in 2009. In both situations, the maximum credit was capped at 10% of the purchase price of the home.

- Caregiver Credit – A new credit of up to $5,000 would be created to assist individuals who provide informal care to those in need of long-term care. Additionally, Vice President Biden’s plan calls for enhancing the current tax breaks associated with the purchase of long-term care insurance, though how exactly that would be done is not entirely clear.

Biden Tax Plan Proposal To Increase Long-Term Capital Gains Rates Back To Ordinary Income Above $1M And Limit 1031 Exchanges

While Vice President Biden has chosen $400,000 of income to be the ‘magic’ income number when it comes to increasing a client’s ordinary income tax rate, over in ‘long-term capital gains land,’ the new ‘magic’ income threshold is $1 million. More specifically, to the extent that a taxpayer’s income exceeds $1 million, the Biden tax proposal calls for taxing both long-term capital gains and qualified dividends at ordinary income tax rates (which at that point would be 39.6%)… plus the 3.8% surtax on net investment income that would still apply as well.

To be clear, the ordinary income tax rate would only apply to the extent that, when added to a taxpayer’s other income, their long-term capital gains and/or qualified dividends exceeded $1 million. So, for instance, if an individual had $900,000 of ordinary income and $250,000 of long-term capital gains, only the $1,150,000 - $1,000,000 = $150,000 of gains that represent income in excess of the $1 million mark would be subject to ordinary income tax rates.

Nevertheless, that still means that the top rate paid on such long-term capital gains income today, at 20% long-term capital gains tax + 3.8% surtax = 23.8%, would nearly double to 39.6% +3.8% = 43.4% for those with over $1M of income!

In a related capital gains proposal, the Biden tax plan also proposes the elimination of the 1031 Exchange for taxpayers with income in excess of $400,000. Under current law, 1031 exchanges can allow taxpayers to 'swap' tangible property held for investment with similar property, and avoid triggering a tax bill. Under the new proposal, a sale of real estate and re-purchase of replacement real estate would still be a taxable event for high-income earners (who, notably, would then also potentially face ordinary income tax rates on their real estate sale to the extent the capital gains fall above the $1M threshold). However, it’s not entirely clear at this point whether the $400,000 threshold to invalidate a 1031 exchange would include the gain trying to be deferred via the 1031 Exchange or not; expect more details in the future if and when the Democrats win in November and provide a more detailed legislative proposal of exactly how the new 1031 exchange limitation would be implemented.

Planning Strategies To Mitigate The Impact Of Vice President Biden’s Capital Gains Proposals

While they represent less than 1% of all taxpayers, households with more than $1 million in annual income stand to face the biggest impact of Biden’s proposed changes to the capital gains rules because, in many situations, those households can have substantial long-term capital gains and qualified dividends.

Accordingly, if Vice President Biden is elected, and it appears that his capital gains proposals are likely to become law, such taxpayers would want to consider employing a variety of capital gains mitigating strategies, such as:

- Reducing the size of their annual capital gains budget – While it’s important not to let the ‘tax tail wag the investment dog’, it’s also often a popular idea to establish an annual capital gains budget target, whereby the goal is to keep net capital gains at or below a specified dollar amount. An increase in the capital gains tax likely means reducing said budget, and for those with income below $1M to target the budget at just ‘enough’ to top up to the $1M threshold (without pushing capital gains over that line where they would jump from a 23.8% to 43.4% top tax rate).

- Up the use of municipal bonds – Municipal bonds remain largely tax-free (save for private activity bonds subject to the alternative minimum tax) under the Biden regime. Such bonds would become dramatically more valuable as the tax-equivalent yield compared to other investments' increases for ultra-high-income earners.

- Swapping dividend producing investments for non-dividend producing investments – Many investors love dividend-producing investments… and love may be an understatement. But when you’re seeing nearly 45% of those dividends evaporating instantaneously in the form of Federal taxes alone (not to mention the state income tax impact), they can quickly lose their appeal. Accordingly, should Biden’s proposed “harmonization” of the income tax rates for income in excess of $1 million come to pass, high earners would likely benefit from considering replacing certain dividend-producing investments with others that would not create as great of an annual tax drag.

- Increase the use of ‘bare bones’ Investment-Only Variable Annuities (IOVAs) – While most annuities today are sold for the guarantees associated with the products (e.g., a guaranteed minimum income stream, a guaranteed fixed rate of return, a guarantee of principal returned, etc.), the tax-deferral offered by the annuity ‘wrapper’ should not be forgotten. In recent decades, as the top income tax rate(s) has (have) declined, the tax-deferral offered by annuities has grown less important. If, however, the top income tax rate is increased, and the special tax rate enjoyed by long-term capital gains and dividends is curtailed, it could make low-cost, bare-bones, deferral-only (also known as “Investment-Only”) Variable Annuities more popular again, especially now that more and more annuity carriers are offering no-commission fee-based versions from which advisors can bill their AUM fees for ongoing management. And while there may not be a plethora of options available yet, $1 million-plus earners have an ‘ace’ up their sleeves. Since they will generally be accredited investors, in addition to the ‘regular’ deferral-only annuities available to the general public, they can also access Private Placement Annuities as well.

- Increase the use of Installment Sales – In general, most people want to receive the proceeds from a sale of… well… anything(!) as quickly as possible. However, if a client knows that by keeping their income below $1 million that they can cut their tax rate nearly in half, they might be more inclined to spread that income (gain) out over a number of years to keep most – or at least more – of the income below the $1 million mark and avoid it being taxed at the same rate as their ordinary income. This, of course, is precisely what an installment sale does!

- Harvest long-term capital gains in late 2020 – One easy way for ultra-high-earners (or those with more modest income, but who are looking to sell highly appreciated assets) to avoid long-term capital gains from becoming subject to the proposed new top rate of 39.6% is simply to harvest those gains in 2020 (before the potential change in rates becomes effective). While such a sale might accelerate the taxation of such gains, it might do so at a substantially lower rate than might otherwise apply. The decision to accelerate a sale in such a manner, particularly by older clients, would likely make even more sense if Biden’s plans for eliminating the step-up in basis (as discussed directly below) also came to fruition.

Biden Tax Plan Proposes Elimination Of Step-Up In Basis And New Potential Deemed-Sale-At-Death Rule

While the potential increase in long-term capital gains (and qualified dividend) rates would have a substantial impact for top earners, it is not the only seismic shift under the Biden tax plan when it comes to capital gains. As, in addition to eliminating the special tax rates for long-term capital gains and qualified dividends for income over $1 million, the Biden tax plan calls for eliminating one of the most far-reaching capital gains tax breaks in the entire Internal Revenue Code… the “step-up” in basis on inherited assets at death.

Under the existing rules, when the owner of an asset dies, the beneficiary of that asset generally receives the asset with a cost basis equal to the fair market value of the asset on the date of the decedent’s death. Known as the step-up in basis rules, the primary purpose of the rules is not actually to provide a tax break, per se, but simply in recognition that once the original owner passes away and the beneficiary inherits, the beneficiary often wouldn’t know what the original cost basis (and thus the capital gains exposure) is, especially since the original owner would no longer be around to explain it. Accordingly, the step-up in basis rules apply to virtually all inherited assets, except for certain pre-tax assets which fall into a category known as Income In Respect of a Decedent (e.g., IRAs and other retirement accounts, NUA, accounts receivable, deferred interest of EE bonds) that are excluded and remain pre-tax assets when received by the beneficiary (and since the IRD assets are entirely pre-tax, there wouldn’t be a need to know what the original owner’s cost basis was anyway).

Vice President Biden’s plan calls for the elimination of the step-up in basis on all (non-IRD) assets that would otherwise be eligible, and would prevent the death of an owner from ‘wiping clean’ the potential capital gains tax bill associated with the inheritance (and subsequent sale) of an appreciated asset.

What is less clear, however, is exactly how Biden would implement this policy. There is some speculation that Biden would simply call for the basis of the decedent to be carried over to the beneficiary. But as noted earlier, this is problematic in practice, because beneficiaries often don’t know – and original owners don’t always keep clear records – of what that carryover cost basis should be.

In fact, Biden has stated in the past that he’d consider any built-in gain of an asset to be taxable upon the owner’s death. The effect of such a policy would be to treat all of a decedent’s assets as if they were sold upon their death, which would result in the assessment of capital gains tax on any growth, and is similar to how appreciated assets at death are treated in other countries. It would still require a determination of the cost basis of the decedent’s assets, but for better or worse would at least be resolved ‘immediately’ upon the death of the owner, and not years or potentially decades later when the beneficiary liquidates inheritance assets in the future. With the ‘unfortunate’ consequence that it also results in an additional immediate tax liability and liquidity pressure on an estate that must settle up its capital gains obligations at death.

Feasibility Of Biden Tax Plan Proposal To Eliminate Step-Up In Basis

While it’s certainly possible that such a rule could eventually be adopted, there are at least a few reasons for clients fearing such a provision might consider sleeping a little easier. For starters, there have been two big efforts to eliminate the unlimited step-up in basis rule over the past 50 years, and both were unsuccessful.

In 1976 Congress eliminated the step-up and implemented carryover basis. The decision proved so unpopular with the American public – and perhaps more significantly, financial institutions – that implementation was repeatedly delayed until Congress finally just undid the change altogether in 1980. And in 2010, the estate tax was supposed to be eliminated altogether, with carryover basis reinstituted. But before the end of even that first year (2010), Congress had already given taxpayers the opportunity to opt back into the estate tax with an unlimited step-up in basis and had made the system ‘permanent’, and the only choice again beginning in 2011. Again, this was in part due to the reality that financial institutions, and the IRS itself, still weren’t sure how to track and determine compliance with the proper reporting of cost basis by a beneficiary that might not be due until years or decades after the original decedent passed away.

Beyond the political challenges of eliminating the step-up in basis, there are practical challenges as well. For instance, what if a decedent owns illiquid investments, such as a family business, or even a long-held family residence? Treating such assets as sold at the owner’s death could force heirs into selling these illiquid (often highly sentimental) assets. It’s hard to imagine that any political candidate would want to be the person known for instituting that.

Accordingly, if any changes to the step-up in basis rules are made under a Biden administration, it’s more likely the outcome would look something more akin to 2010, when (if a taxpayer’s estate chose the “no estate tax” option) the step-up in basis was limited to $1.3 million combined to non-spouse beneficiaries, while spouses were eligible for an additional $3 million of stepped-up assets. Which means the bulk of assets for the bulk of taxpayers would still be ‘sheltered’ with a partial step-up in basis, and only those with ultra-high-net-worth estates (that have not just millions of assets but specifically millions in gains) would still be exposed. Of course, there’s no guarantee that will be the case.

Planning Implications Of Biden Tax Plan Proposal To Eliminate Step-Up In Basis

While the Federal estate tax today only impacts a small number of ultra-high-net-worth estates, the reality is that millionaires and the ultra-wealthy may not be the only ones impacted by Vice President Biden’s step-up-in-basis proposals though.

If Biden were to turn death into a realization event for property (treat everything as though it was sold at the owner’s death), it would require a lot of families with more modest means to figure out how to pay that tax upon the owner’s death (particularly if there’s not a ‘gains exclusion amount’ rule as there was in 2010). For individuals with liquid investments, the ‘plan’ might be as simple as “Hey, just sell some of my stuff when I’m gone to pay the tax,” but for individuals with more illiquid investments, or with investments that they’d prefer to see heirs ‘hang on’ to, life insurance for tax purposes at death (though for income tax, and not estate tax) could see a resurgence as a viable approach.

For other clients, a ‘forced sale’ at death – at least what would be treated as a forced sale for income tax purposes – may result in a more structured selling of investments during life. Currently, advisors often encourage older clients with highly appreciated assets to hold them until death, so that their heirs can reap the benefit of a step-up in basis, eliminating the tax bill that would otherwise apply to the gain when sold.

If that gain won’t go away at death anymore, though, it may behoove more clients to strategically sell their investments throughout their lifetime in order to avoid a massive spike in gains on their final income tax return (or possibly an estate income tax return?), especially given the separate Biden proposal for a new top capital gains tax bracket, which could push year-of-death capital gains income over the $1 million threshold and turn tax-favored capital gains and qualified income into income taxed at the far less favorable 39.6% ordinary rate (plus an additional 3.8% surtax). Indeed, even with just a ‘regular’ carry-over basis (and no forced sale at death), strategic selling during clients’ lifetimes would likely increase, if only to ‘smooth out’ capital gains and avoid a year-of-death spike into the new top 39.6% + 3.8% = 43.4% capital gains tax rate.

Alternatively, if a forced sale of assets were to occur at death though, one strategy would be to avoid dying… while owning assets. In other words, prior to death, it would behoove an individual to gift assets to an heir (which allows them to avoid capital gains taxes until they choose to sell), rather than to die, incur the forced sale, and bequeath it to them afterward. Admittedly, one would think that if a forced-sale rule was put into place, there would be some sort of anti-gift-abuse rule to go along with it. But what that might look like, and how easy it might be to plan around such a rule, remains an unknown at this time.

Biden Tax Plan Calls For A Return To The Pre-TCJA Federal Estate And Gift Tax Exclusion

Vice President Biden’s proposal for estate and gift taxes is rather straightforward… Take us back to the ‘good old days’ before the Tax Cuts and Jobs Act. Notably, while not as progressive of a change as others in his own party have called for, Biden’s plan calls for an immediate halving of the current $11.58 million lifetime exclusion amount that applies to both estate and gift tax (individuals also have a separate $11.58 million exclusion for the Generation Skipping Transfer Tax (GSTT) as well), reverting back to what the inflation-indexed exemption would have been under President Obama (and Vice President Biden’s) rules while they were in office (as implemented under President Obama’s American Taxpayer Relief Act of 2012). Notably, this lapse of the current estate tax exemption amount back to its pre-TCJA limits is already scheduled to occur in 2026 – after the Tax Cuts and Jobs Act sunsets – but the Biden tax plan would accelerate that reversion back to the old limits in 2021 instead.

Of course, even at roughly $6 million per person of lifetime exemption amount, the overwhelming majority of Americans would continue to be able to sleep well knowing that their new worth was not large enough to ‘burden’ heirs with an estate tax liability (especially given the portability of the unused exemption to a surviving spouse, allowing nearly $12M of estate tax exemptions for a married couple). But… there are a lot more individuals with $6 million of net worth (and couples with a net worth of $12 million) than there are individuals with $12 million (and couples with $24 million).

Accordingly, even though most estates still would not owe the tax, there would be an exponential increase in the number of clients who would need to plan for (or to avoid) such potential!

Planning Strategies To Mitigate The Impact Of Vice President Biden’s Estate And Gift Tax Proposals

For many individuals with significant wealth, if Vice President Biden wins the presidential election and enjoys support in both the Senate and the House, the number one planning strategy to mitigate the impact of a potential reduction in the estate and gift tax exemption will be to use as much of it as possible before the end of this year. While there is much that we do not yet know about the outcome of the November elections, one thing is certain; the winners of the races won’t be taking office until 2021. Thus, the current $11.58 million exemption amount is with us through at least the end of 2020.

High-net-worth clients and others worried about the potential for a future lower unified exemption amount could simply use (up to) their full $11.58 million exemption later this year without triggering any transfer taxes. That’s true even if the exemption amount is reduced next year, or at some other point in the future, as the IRS is already on record stating that it won’t ‘claw back’ previous transfers (by gift or by bequest) of assets if the exemption amount goes back to its pre-TCJA levels.

Nerd Note:

While in general, it is not advisable to take any action now based on what might happen in the November election, one exception to that rule applies to clients who have estates large enough that a reduced exemption would become a planning concern, and who own hard-to-value assets, such as a private business. In such cases, the client may wish to engage in gifting prior to the end of the year if there is a ‘blue wave.’

As while cash, marketable securities, and similar investments are easy to value for gift purposes, assets such as the aforementioned privately held stock often present a greater challenge and may require a formal valuation in order to plan effectively. Such valuations can take several weeks or more in ‘normal times,’ but given the current pandemic, the state of our economy, and the potential mad-dash for valuations that could ensue if the balance of power shifts in D.C. in November, if such an appraisal or valuation may be necessary to plan for your client, they may wish to seek such services now, or face the risk that they cannot complete a year-end gifting process that begins after the election because they cannot complete the valuation in time to do so.

In future years, if the exemption amount continues to remain ‘low’, more clients will inevitably need to begin exploring more complex wealth transfer vehicles than have typically been necessary in recent years. Strategies such as the use of Grantor Retained Annuity Trusts (GRATs), Charitable Lead Annuity Trusts (CLATs), and sales to Intentionally Defective Grantor Trusts (IDGTs) would all become more valuable and more popular. Though notably, such estate planning strategies were also under consideration for curtailment or elimination in the past, and in turn may face legislative risks in the coming years of a Biden administration as well.

With the first Presidential Debate airing last night, the fact that we are just over a month away from a historic election is likely to really start to hit home for people. As such, and as election day draws closer, advisors should be prepared to field additional calls from clients asking “What if…?”

Many of those clients are likely to ask, or even encourage, action now, prior to the election, but in the overwhelming majority of circumstances, now is not the time for action. Not yet.

Rather, now is the time to help educate and inform clients about the candidates’ positions that are most likely to impact them. And perhaps even more important than that, it’s the time to make sure clients know what you are ‘on it’, you’re following events closely, and that no matter which way the election goes on November 3rd, you’ve got a plan of action already charted out. At the end of the day, that’s so often all a client really wants to – and needs to – hear.

Elections have consequences!

Michael knows what he is talking about. This was a great summary of possible changes and Great planning ideas if those changes are enacted.

I want to serve the clients that have these problems.

Keep the content coming!

Thanks for the kind words, Jack! Though this article was all Jeff Levine from our team! 🙂

Hope it helps!

– Michael

In the event of a “blue wave,” another useful planning tool for those expecting taxable income of $1 Million or more and significant capital gains would be opportunity zone investments.

Postponing the realization of those gains until a later date could prove to be highly beneficial.

Potentially, but investments made in 2021 will already be too late to reap several of the step ups, unless those provisions are extended.

Most individuals will have no idea which option (pre-tax or Roth) will be the best for them because they don’t know what their future income or marginal tax rate will be. Given that the higher income individuals will shift to Roth contributions under the proposal, it would be simpler to eliminate the pre tax option option for everyone. That way everyone “captures” their current bracket. If encouragement for lower paid to contribute is needed, then give credit of say 26% on the first $10,000 to everyone.

What happens to SALT limitations?

The SALT cap would remain in place (for the subset of investors who can still itemize). It’s just that if the SALT deduction is part of the itemized deductions for high-income taxpayers, it would ALSO be limited to a 28% deduction rate (in addition to the fact that only $10,000 can count towards the SALT deduction in the first place).

– Michael

For 401(k) contributions – if you have a less than 26% tax rate wouldn’t it make sense to do a pre-tax contribution, followed by an immediate conversion? E.g contribute $10K, get 2,600 in credits, convert @12% and pay 1,200 in tax. Net benefit 1,400 and tax free growth.

Potentially. Have to think there’d be some sort of recapture rule. But even without it, it would depend on what the current vs. future tax rates were. If future tax rates were lower, wait to convert and use the credit to offset other taxes today.

Jeff, what are your thoughts on the likelihood that Biden tax law changes if passed in 2021 are retroactively effective 1/1/21 as opposed to prospectively to 1/1/22 (or enactment date)? While it’s happened a few times, it seems to be rare to have it retro to affect people who have already made transactions based on current law. With the exception of Clinton’s 1993 tax bill, I think most of the retro increases have been to shut what were considered abusive loopholes. So it seems to be the exception. Curious on your thoughts particularly when it comes to advise for the last two months of 2020 that may be costlier if 2021 law remains unchanged. Thanks for the great article and planning ideas!

I would be interested to hear the answer to this as well! Jeff or Michael – any thoughts? How often are these done retroactively to the Jan 1st, when a new administration is not even in place until later?

Historically unlikely. That said… IF Dem flip the Senate and keep the House, I think it’s a pretty decent likelihood that we see action to reverse the TCJA changes. It won’t be pitched as a tax increase, but rather, an elimination of a tax decrease. No guarantees, but that’s my best guess at the moment!

Let’s not forget….the President does not set tax policy, only Congress can do that. So assuming Biden wins the election, most of these proposals will remain proposals unless Democrats also keep the majority in House and flip the Senate, a combination that did occur in 2008. The massive deficits created today will require legislative action to raise revenue and on the surface, many of these proposals targeted to the most wealthy certainly do seem worthy of consideration, with some of them likely seeing themselves into law even if the President and Congress remain red.

Another perspective to consider for the most wealthy clients. Per the Sept released Statistics of Income from the IRS, for 2018 under TCJA, those with AGI >$500K represent 1.45% of taxpayers but paid 39.7% of the income tax while those with AGI < $100K represent 73.5% of total tax filings and paid 18% of the total of income tax, before credits. The effective tax rate, before credits, calculated to be 6.78% for those in the $40-$50K AGI range, 9.03% of $75K - $100K and a weighted 26.3% for AGI > $500K. The proposed changes will almost certainly spread this gap wider. Add to this employment tax and state + local tax, for clients of states like OR, CA and NY could see effective rates climb from around 40% to 50% or higher.

Lot’s of tax planning opportunities for the higher AGI brackets may be forthcoming!

Superb summary – thank you for putting it all out there. Lots to consider!

Thanks Kim!

Good and very informative article, as always. However, it should be noted that candidates proposals are just that and things change if, and once, they are elected. Plus, a politician’s number one job is to get re-elected, so it’s unlikely they would aim too high for fear of losing future votes. It’s always good to look at politics and the impact in an agnostic fashion to not let personal biases get in the way of the difference between possibilities and probabilities.

Agreed. These are just proposals. Even if Biden wins the White House, implementation of some, or all of this will depend on how the House and Senate go as well. That said, proposals are a good indication of where things may go, either soon, or at some point in the future. For instance, the elimination of the stretch as part of the SECURE Act was foreshadowed by proposals for years.

Hi, Jeff Levine:

Any hope that the “stretch as part of the SECURE Act would be reinstated for a “certain reasonable level” of traditional 401(k)/IRA retirement savings that could be passed on to children or grandchildren?

Regards.

I was reading about Biden’s plan to impose a 12.4% Social Security payroll tax for wages above $400k. I noticed that didn’t make it to this article. Has there been a change in his proposed plan to do so? Thanks

Hey Darren,

Nope. That’s still part of the plan. Unfortunately, there’s not a ton of planning that can be done to avoid that tax for high earners, though… other than telling them to earn less 🙂

Awesome article and very informative… one quick question. Is the elimination of the step up in basis at death applicable to $1 million income earners only? In reviewing Biden’s proposals, they seemed to link the elimination of step up basis to those earning over $1 million only. However, in other articles it appears that the step up is all-together eliminated.

Thanks for the article, it is very informative and I’m sure to refer back to it often. One quick question… as I’ve reviewed Biden’s tax proposal, they seemed to link the elimination of step up in basis to income earners over $1 million only. However, in many other articles, it appears that the elimination of step up in basis at death applies universally. Any clarification on this would be helpful! Thanks!

How would the tax credit for qualified plan contributions work for Employee Stock Ownership Plans? With ESOPs, the company’s contribution to the plan is treated as a compensation charge for corporate tax purposes, such that it is fully deductible at the corporate level. It isn’t deductible at the individual (plan participant) level, but the effect is the same as giving a deduction at each participant’s marginal rate (they get a pre-tax contribution) and the company gets the full deduction at the corporate marginal rate (because it is treated as compensation expense).

Wouldn’t contributions to retirement accounts under this proposal become after-tax contributions given the contributions are no longer deductible? And in that case, wouldn’t the contributions be considered as basis in the account and therefore not subject to double-taxation upon withdrawal?

Retirement contribution deduction elimination ‘s impact would significantly depend upon whether the credit % is capped and what type of contributions count towards it – correct?

1. Elimination of retirement contribution deductions to income is a huge change for those who are reducing their earned income for taxes and earned income tax credit optimization.

If, for example – I earned $49,000 this year and contributed $24,000 to pre-tax 401k/403B/457 retirement. I would receive max EITC of $5,920 with two qualifying children + $1,200 x 2 (child tax credit refundable amount) = a tax refund of $8,320 in 2020. (Assumes 0 federal tax liability as std. deduction is $24,800) Assumes 0 state tax liability (true in my case).

However – under this new hint of law of no retirement deductions.- my income would not be reduced for federal taxation purposes and instead I would receive a flat $24,000 retirement contributions x 26% = $6,240 + child tax credits of (let’s be generic and just say $3,000 and $3,000) But we do not know how much of that child tax credit is refundable (currently only $1,400 out of the $2,000 is). So let’s say that $2,000 is refundable. That equals a tax refund of $10,240 – Federal tax liability.of $2,564 = $7,676. Because I can no longer reduce the earned income for EITC maximization – that credit falls down to $730 making the Biden hint of a plan total tax refund: $8,406

2. Which leads me to the question – for those of us that have multiple options to contribute to retirement: 401K + 403B + 457 defer comp + personal IRA’s – Exactly what DOES count and is there a limit other than the IRS max retirement contrib limit for said year in terms of what # is multiplied by the ( never detailed in Biden’s ‘plan’ ) 26% tax credit refund? Because I for example – contributed $40,000 to retirement this year between personal IRA and 403B/457 plans. Would I really get $10,400 in retirement tax credits? Or will they find a way to CAP the benefit to punish savers (they punish savers in every other way in our current economy so this is a valid question).

3. This is a shadow of a plan – lacking detail and clarity (which means that whatever comes out of it is unclear and likely not to benefit taxpayers.

Very interesting – but the details are necessary in full to come to a full decision.

I welcome comments on the above – I cannot be the only relatively lower income household that utilizes retirement contributions to maximize EITC and CTC tax credits (see gocurrycracker & frugalprofessor ‘s articles on the subject) ?

Thank You, great stuff here.

On the Biden tax plan website that is linked at top, it looks like they misstate some info about the current ind. Tax code.

“If Trump succeeds, 99% of this giveaway will flow to the top one percent. Billionaires will pay a lower tax rate than tens of millions of essential workers and middle-class Americans. In Trump’s America, a working family making $65,000 will pay 22% on every extra dollar they earn, not including payroll taxes, while billionaires will pay just 15% on their profits from investments.”

22% would start at $80k taxable income or over $100k gross and a Billionaire would prob pay 18.3%.

Will contributions to traditional 401k/403b and 457 plans still reduce taxable income?

Nope. Would be the same credit.

If a single individual gifts ~$6mm to an irrevocable trust this year (2020), and the estate tax exemption amount is reduced to ~$6mm next year, would the individual then have used 100% of their lifetime gift/estate exemption? Or would it be viewed that they have used 50% of their estate tax exemption amount because the lifetime gift/estate exemption amount in the year of the gift was ~$12mm?

Does anyone have a link to Biden’s ACTUAL proposed tax plan? All I can find is other peoples analysis of it but not the actual plan itself…

I havent been able to find the proposed plan, can I expect to get my deductions back that I once had pre Trump? I’m not a business owner, but I took a notable hit by not being able to write off the countless things I buy every year to do my job. Company doesn’t reimburse me, nor do they purchase them for me but they’re essential things I provide that do cost out of pocket.

Jeff any update here? When will they take this up? Since the dems dominate what is your expectation for this proposal and the effective date (retroactive or not) Will Biden get everything?

Hasn’t he also discussed applying the payroll tax to amounts of income over 400k?