Executive Summary

Yesterday, Blackrock announced that it was acquiring FutureAdvisor, one of the three original and “pure” robo-advisors who have been gathering assets and managing ETF portfolios directly for consumers. And despite FutureAdvisor having “just” $600M of AUM, and an estimated $3M of revenues, Blackrock’s purchase was rumored to be in excess of $150M.

However, it appears that Blackrock’s strategy was not simply to buy FutureAdvisor to expand its direct-to-consumer solution, but instead to pivot FutureAdvisor to become a robo-advisor-for-advisors solution, and license/offer the technology platform to a wide range of broker-dealers, insurance companies, banks, and custodians to turn their human advisors into tech-augmented "cyborg" advisors. In this context, as the world’s largest asset manager and a leading player in the ETF space already, the Blackrock deal appears to be visioned primarily as a means to further grow the size of the ETF pie and the Blackrock (iShares) market share by driving distribution to its ETFs through this new technology platform. The robo-advisor is now a distribution channel.

For financial advisors, the “good” news of the Blackrock deal is that “robo” tools may soon become increasingly available to a wider and wider range of advisor platforms. And ironically, because iShares – like Schwab’s Intelligent Institutional Portfolios – can profit from the underlying ETFs held in the portfolio, the future Blackrock FutureAdvisor solution may even undercut existing robo-advisor platforms, as the established financial services industry players continue to apply more and more pressure to the direct-to-consumer robo-advisor solutions. In other words, advisors and established firms are now driving the cost of robo-technology down to zero, relying on their ability to profit from the ‘traditional’ channels of manufacturing investment products (e.g., ETFs) and delivering personal financial advice, and out-commoditizing the robo-advisor commoditization.

Blackrock Acquires FutureAdvisor For $150M

This week, Blackrock announced that it was acquiring the “robo-advisor” platform FutureAdvisor, for an amount reported/rumored to be between $150M and $200M. According to a FutureAdvisor spokesman, the company had $600M of AUM at the time of acquisition, up from just over $230M last September (according to its last Form ADV Part II). The deal appears to be a “successful” exit for FutureAdvisor investors, as the company had “only” raised $21.5M of venture capital since it was founded in 2010, including a $15.5M Series B round last May that was reported to have pegged their valuation at $75M.

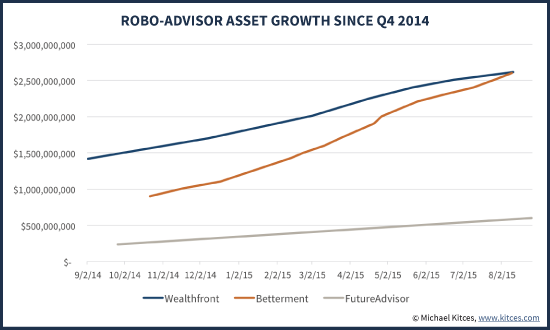

Relative to other robo-advisor platforms like Betterment and Wealthfront, which each manage approximately $2.6B of AUM based on their latest Form ADV Part II, FutureAdvisor was significantly smaller than competitors at “only” $600M. And while the company had experienced significant growth, it was also still significantly lagging the growth of its competitors, and falling further behind, though it’s not entirely clear whether FutureAdvisor’s challenges were due to its pricing (at 0.50% of AUM, FutureAdvisor charged more for AUM that its robo competitors), a smaller capital base to do aggressive marketing when competitors had raised 4-5 times as much funding (as previously discussed, client acquisition costs are the primary blocking point for robo advisors, or any advisors, to serve the middle market and mass affluent), or simply that it started a year or two later than the others and never caught up to their head start.

So from this perspective, it’s perhaps not entirely surprising that FutureAdvisor chose to exit and sell while it could. The movement for using technology and “robo” platforms to augment human advisors (the “cyborg” advisor category) has been increasingly popular over the past year (as predicted on this blog years ago when the robo movement was just beginning!), and existing financial services firms have been buying robo tools and client portal technology with a fury (from Fidelity buying eMoney, to Envestnet buying FinanceLogix and Yodlee, to Northwestern Mutual buying LearnVest and John Hancock buying Guide Financial). So in a world where FutureAdvisor was 3rd of the big 3 core robo-advisor players and falling further behind, just as established major financial services firms are getting hungry for comparable technology of their own, a deal was born.

Metrics Of The FutureAdvisor Deal And Blackrock’s Robo-Advisor Strategy – A Cyborg Solution For Broker-Dealers?

As a $4.7 trillion asset manager, Blackrock clearly has the capital to create its own “robo-advisor” technology solution, which raises the fundamental question: why purchase FutureAdvisor, and why pay $150M+ for a company that only had $3M of revenue (at 0.50% on $600M of AUM). At a 50X revenue multiple (and with a reported 40 employees, including a heavy component of San Francisco engineers, was almost certainly still quite cash flow negative), FutureAdvisor certainly wasn’t a “deal” by any traditional finance metrics for its own core business.

Instead, the key to the deal comes from Blackrock’s indication that it does not intend to continue targeting individual investors with the robo-advisor platform. Instead, Blackrock plans to use FutureAdvisor as a technology platform offering to banks, brokerage firms, insurers, and even 401(k) plans, and accordingly will be housed under its Blackrock Solutions technology platform. In other words, Blackrock didn’t purchase FutureAdvisor for its current AUM and its consumer-oriented strategy. Blackrock bought FutureAdvisor as a means to bolster its technology offering to other industry players, who will then ostensibly offer the platform to their own human advisors as a means to continue to gather more assets.

In essence, then, for Blackrock the robo-advisor has just become a new form of distribution channel for its iShares ETFs. Although the announcement of the acquisition on the FutureAdvisor website states that FutureAdvisor will continue to use a variety of ETF products for its managed ETF portfolios, the same statement was/has been made by Schwab when it announced the ‘objective quantitative selection criteria’ for its Schwab Intelligent Portfolios; nonetheless, Schwab ETFs “coincidentally” have turned out to be nearly 70% of its allocations, not to mention the additional profit that Schwab can generate by using the cash allocation in its portfolios as a way to distribute (and earn interest spread) on Schwab Bank solutions. Of course, Schwab Intelligent Portfolios are “free” to consumers (and their Institutional Intelligent Portfolios are free for $100M+ advisory firms), which raises the question of whether Blackrock will ultimately restructure the pricing of FutureAdvisor (reduce the AUM fee since Blackrock can make money via the iShares held in FutureAdvisor portfolios anyway?).

In fact, it wouldn’t be surprising at all if Blackrock was specifically eyeing the early success of Schwab Intelligent Portfolios (which picked up over $2B in just its first 2-3 months, mostly into its own proprietary products), as a reason to adopt a similar strategy of robo-advisor-as-ETF-distribution channel. The rapid growth of Vanguard Personal Advisor Services (VPAS) was also likely a consideration, although notably in the end VPAS is not actually a robo-advisor solution but a human-technology hybrid – a “cyborg” solution – and is probably more notable for its potential disruption of how financial planning services are delivered, not as a self-service robo solution.

Either way, Blackrock clearly views the FutureAdvisor acquisition as a significant opportunity to expand its ETF assets, either by growing adoption of ETFs overall, and/or expanding its ETF market share with a proprietary robo-advisor distribution solution. Relative to FutureAdvisor’s $600M of AUM, it’s hard to explain a $150M+ purchase price. Relative to Blackrock’s $4.7 trillion and the rapid growth of iShares, combined with the demand from broker-dealers, insurance companies, banks, and Blackrock’s other advisor partners to have access to the technology, the acquisition costs are easier to add up. Though it’s still unclear why Blackrock chose FutureAdvisor, and not some of the smaller and newer (and presumably less expensive) robo-advisor-for-advisors solutions like Trizic or Vanare Nestegg. When Envestnet decided to buy robo-advisor technology to integrate into its platform, it went with upstart Upside Advisor (at a deal rumored to be only a tiny fraction of the FutureAdvisor purchase).

Broader Industry Implications For Broker-Dealers And Custodians, And What’s In Store For Betterment And FutureAdvisor?

From the broader industry perspective, this high-profile Blackrock deal certainly goes a long way to cementing 2015 as the year of robo-advisor-for-advisors solutions. And to the extent they distribute the platform to various broker-dealers and insurance companies and banks and custodians, can help those companies stave off their own robo-advisor threat (as while robo-advisors were not really a threat to human advisors, the robo-advisor platforms were/are a significant threat to traditional technology-lagging advisor broker-dealer and custodian platforms!). In fact, given the shrinking number of available robo-advisor players at all, it looks increasingly likely that almost all established financial services firms that want to plug their “robo-advisor-for-advisors” gap at this point will need to partner with Blackrock’s new robo-advisor, Envestnet (which is building its own holistic technology platform for advisors), do a deal with Betterment Institutional similar to Fidelity, or use Schwab’s Institutional Intelligent Portfolios if they’re an advisor on the Schwab platform.

For the small subset of established financial services companies that still want to go at it on their own, they might try to build their own – although notably, Schwab has been the only major player choosing to do so at this point – or partner with one of the smaller robo-advisor-for-advisor platforms that are trying to make inroads. Although realistically, it may only take a few major players like Blackrock and Envestnet offering a robo solution across a wide range of insurance, broker-dealer, and even custodian platforms, before most of the robo-advisor-for-advisors upstarts find that established firms just prefer the stability of partering with other established firms. Alternatively, for the established companies that do decide to build, they might still decide to do it by acqui-hiring companies like Trizic or Vanare or the others that exhibited at this year’s T3 Advisor Technology conference.

In terms of the robo-advisor landscape itself, the Blackrock acquisition also continues to raise questions about what’s next for the remaining two major players, Wealthfront and Betterment. Realistically, it seems unlikely that either will pursue a similar sale strategy to FutureAdvisor anytime soon; both companies raised significantly more capital (including $105M for Betterment, and $129.5M for Wealthfront at a rumored $750M valuation!), necessitating dramatically higher valuations even than FutureAdvisor despite having only “marginally” more AUM and revenue (the companies do have quadruple the AUM of FutureAdvisor, but at what was already far-more-than-quadruple the valuations). In other words, the valuations of Betterment and FutureAdvisor are already so high that there may be no FutureAdvisor-Blackrock-style synergy deal to justify their valuation to an acquirer (Blackrock already is the world’s largest asset management, and even they “only” bought FutureAdvisor and “only” put $150M to the strategy). In other words, if even a $4.7 trillion asset manager like Blackrock "only" sees the robo-advisor distribution channel as being worth $150M, it doesn't bode well for the other robo-advisors. Which means for better or worse, Wealthfront and Betterment may have to just keep pushing their organic growth strategies and try to keep gathering clients and assets and scaling from here; any sale transaction would probably be an unfavorable exit (at least relative to their valuations at the last round of fundraising), even as both companies have enough cash and runway that there wouldn’t be any need to do such an (unfavorable) exit in the first place.

Still, the Blackrock deal significantly raises the stakes in the robo-advisor space. If the direct-to-consumer robo-advisors though it was a “little” competition when Schwab launched their direct-to-consumer offering, and Vanguard moved into the space with VPAS, wait until they see what happens when Blackrock uses its massive network of relationships with broker-dealers, insurance companies, and custodians to put a robo-advisor technology tool into the hands of tens or even a hundred thousand financial advisors in the coming year or two. Especially since Blackrock can profit from the robo-advisor as a distribution channel for its own ETFs, and may not even choose to charge anything for its service at all. Robo-advisor technology and companies are quickly changing from a B2C solution, to a B2B(2C) solution instead, the technology link between asset managers seeking assets and financial advisors that help to gather them. And notably, if that robo-advisor-for-advisors growth impairs the pace of growth for the direct-to-consumer robo-advisors like Betterment and Wealthfront, it may become increasingly difficult for those companies to attract and retain their top talent, in a FinTech world where the spoils of war go almost entirely to the #1 player, and not those who fall to the #2 and #3 (and lower) spots.

Ultimately, then, just as predicted at the beginning of the year, the commoditizing force of robo-advisor solutions against advisors may have just themselves been commoditized down to zero, as Blackrock potentially turns FutureAdvisor into the robo-advisor technology platform that every advisor gives “for free” to their clients, and on top of which the advisor gets paid for adding their own unique personal financial planning advice that robo-advisors can’t match.

So what do you think? Does the Blackrock acquisition of FutureAdvisor validate the direct-to-consumer robo-advisor model? Or present a new threat to it? Will human financial advisors effectively be able to adopt robo-advisor technology with their clients?