Executive Summary

The classic view of cash in the world of investing is that it’s something to avoid, or at least minimize. To the extent cash is truly needed for immediate or near-term liquidity, holding some may be a necessity. But the investment goal is always to hold as little cash as possible, and put the rest to work on your long-term behalf.

Except a recent research study by Ruberton, Gladstone, and Lyubomirsky finds that maintaining a healthy level of cash-on-hand (or at least in a checking or savings account) appears to improve our feelings of financial well-being and life satisfaction. And the relationship holds up even after controlling for income, spending, and other investments, as well as age and employment status. In other words, no matter how much total wealth and income we have, we’re just not as happy unless it’s also accompanied by a healthy pile of cash (or at least, a sizable and readily available bank account).

From the investment perspective, it’s purely irrational for anyone to need to hold a substantial cash balance above and beyond what’s needed to cover actual near-term spending needs. But the research results are more understandable given the research on mental accounting, that we tend to bucket our holdings into groups of current income, current assets, and future income (or at least, assets to fund future income). Which means even if we have ample income, and ample assets for future income, we’re just not content until we also have a healthy allocation to current assets. Which in practice, means cash (or at least cash equivalents).

As a result, rather than always encouraging clients to fully deploy their available cash, perhaps instead it would be better for advisors to start by asking clients “how much cash do you need to hold to feel comfortable and sleep well at night”, and then invest what’s left around that constraint. Because in the end, what’s the point of trying to invest a little more cash for a little more return, if in the long run greater wealth buys little additional happiness anyway, but having more-than-enough cash today may have a more positive impact on financial well-being? Or viewed another way, perhaps holding some comfort cash is not “under-investing”, but simply giving up on extra yield as a way to “buy” a little more financial contentment?

Does Your Bank Balance Buy Happiness?

As the old saying goes, “Money Can’t Buy Happiness”, but a growing base of research shows that it actually can. At least to some extent. Because it turns out that our happiness really is materially impacted depending on how we spend it. And studies have shown that our life satisfaction and emotional well-being really do seem to be correlated with having greater financial wealth and a higher income (at least up to an annual income of about $75,000).

However, “just” looking at absolute levels of income and wealth may be obscuring nuances in the relative impact of how those dollars are earned and/or are held. For instance, Shefrin and Thaler have found that people mentally earmark their dollars into three types of buckets – current assets, current income, and future income – and posited that not all of those buckets may contribute equally to our happiness and emotional well-being. For instance, we might not be as distressed about our lack of future income (e.g., lack of retirement savings) as long we have sufficient current assets and stable income today (satisfying at least two out of the three buckets). Or conversely, we could be more distressed despite having substantial assets – more than enough to cover our lifetime future income needs – if we don’t also have enough cash on hand to fill the “current assets” bucket as well (even if we don’t actually “need” it).

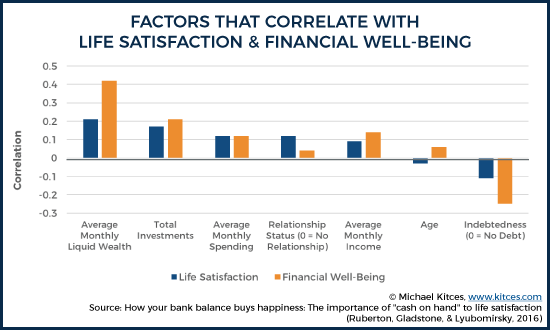

To test this, a recent study by Ruberton, Gladstone, and Lyubomirsky in Emotion analyzed 585 UK bank customers and their bank accounts and income and spending (as measured directly by inflows/outflows from those accounts), and then surveyed those customers to measure their Satisfaction With Life and feeling about Financial Well-Being (in addition to gathering further information about their other external investment accounts and debts, and their age, employment status, and relationship status).

The results revealed that the amount of someone’s “liquid wealth” – the value of checking and savings accounts – was in fact correlated with both financial well-being, and life satisfaction. In fact, liquid wealth had a stronger relationship to those factors than income, spending, investments, or indebtedness!

Even more important, though, the researchers found that the correlation between liquid wealth and measures of satisfaction and well-being remained even after controlling for all the other financial variables (as well as controlling for age, employment status, and relationship status). In other words, the study found that having cash on hand was positively associated with life satisfaction and well-being, regardless of how much the individual already had in income or investments and how much he/she was spending! Though notably, the researchers ultimately determined that having cash on hand was not directly contributing to life satisfaction, per se; instead, liquid wealth directly impacted perceived financial well-being, and it was the improvement in financial well-being that led to an improvement in life satisfaction as well (and again, with a far greater impact than just looking at total investment wealth alone).

Nonetheless, the striking bottom line of the study: a financial buffer of liquid cash available in checking/savings accounts, regardless of wealth or income, appears to confer a sense of financial security, which in turn is associated with positive feelings of financial well-being, and more life satisfaction. Or stated more simply, wealthy people with very little in cash may still feel more financially distressed than poor people with (relatively) more cash!

Caveats To The Cash-On-Hand Research

While one might interpret the results of Ruberton et. al. research as validating investors who say they feel better when holding substantial account balances in cash, it’s important to note that the study did find a substantial “diminishing effect” in the relationship between the two. Because the positive correlation was actually between life satisfaction/financial well-being, and the log-transformed balance of liquid wealth.

On a lognormal scale, each increasing step in liquid wealth represents a 10X increase in the actual account balance. Thus, while the research did find that for every 1 point increase in (log-transformed) liquid wealth, there was a 0.69 point increase in life satisfaction (on a 20-point scale), that means on average satisfaction increased by 0.69 in going from $1 to $10 of cash, another 0.69 for going from $10 to $100, another 0.69 for going from $100 to $1,000, another 0.69 for going from $1,000 to $10,000, etc. Which means cumulatively, going to $1 to $100 was as beneficial as going from $100 to $10,000, which in turn was as beneficial as going from $10,000 to $1,000,000 of cash. Or stated another way, the relative benefit of increasing cash severely diminishes at higher levels; going from $1 to $10,000 was exponentially more beneficial than going from $10,000 to $20,000.

Of course, that doesn’t mean everyone’s improvements in financial well-being, and the transition to diminishing marginal benefits, had the exact same thresholds. It may be that more affluent households have a higher demand threshold for cash. Or alternatively, because they have other investment assets, perhaps a lower demand for cash. There may also be variances in individuals, where perhaps some people simply have a higher proclivity towards holding cash, and others lower. Which means, to say the least, an inflection point where there are “dramatically diminishing returns beyond $10,000 of cash” shouldn’t be viewed as a sacred threshold. And of course, some people have trouble resisting the temptation to just spend liquid cash whenever it’s available.

In addition, it’s important to note that a correlation is just that – a co-relation between two factors. It technically doesn’t prove that greater cash balances cause higher life satisfaction and greater financial well-being. It’s possible, perhaps, that those who are already more satisfied with life, and therefore more optimistic about its opportunities, are more likely to hold cash (to have it available to spend on those opportunities). Or alternatively, perhaps people who are more financially competent and confident in the first place have greater financial well-being, and are also more likely to apply that knowledge and skillset by holding a “healthier” level of cash in emergency reserves. Which would mean it’s actually their financial competency that’s leading to both higher cash balances, and greater financial well-being.

Comfort Cash And Other Implications For Financial Advisors

Notwithstanding the research caveats, there is clearly strong face validity for the idea that holding greater cash reserves could be a causal factor that leads to better feelings about one’s own financial well-being. And for many financial advisors, it should resonate with the real-world demand of many clients to hold sometimes-substantial cash balances in their checking and savings accounts.

To some extent, this may simply be reflective of financial reality. Those who have little or no cash don’t just express greater distress about their financial well-being; they’re arguably more likely to actually be in financial distress, as extremely low cash balances suggest that the household lacks even a healthy emergency reserve and may already be struggling with financial contingencies it can’t afford. And we already know that consumers react more negatively to decreases in wealth or spending than they do positively to increases in the other direction; thus, it makes sense that those struggling to maintain their standard of living without a reasonable cash buffer, and are intermittently experiencing decreases in spending capabilities, would have materially lower financial well-being, compared to those who are wealthier with more-than-enough reserves to ensure household stability.

However, the key point of this research is that greater levels of liquid wealth were associated with improvements in financial well-being regardless of income or wealth levels. In other words, it doesn’t matter if the household actually needs (more) emergency reserves or not; there is still an improvement in financial well-being when the household increases its liquid wealth! To some extent, this shouldn’t be entirely surprising, as our entire banking system is predicated on the fact that consumers will demand more liquidity than they actually need; thus why banks can conduct long-term lending using short-term deposits. And as noted previously on this blog, the research on mental accounting had already suggested that this would be a likely part of the “hierarchy of retirement income needs” for a retiree. But the Ruberton research affirms that its scope is broader, as in this study the same effect occurred, despite the average participant being “just” 37 years old (and thus still far from retirement).

Nonetheless, from the classic investment perspective, the desire for holding substantial amounts of cash is both unnecessary (as long as other investment holdings are reasonably liquid), and/or is outright counter-productive (given the traditionally low, and currently near-zero yield on cash and cash equivalents). An inclination towards holding cash is typically viewed as an investment “mistake”, and something the financial advisor can help to rectify by “putting the cash to work”.

Yet while that may still be technically true for a pure investment perspective, this new research on liquid wealth and financial well-being suggests that fully deploying an investor’s cash reserves may actually have an emotional toll, and one that isn’t necessarily offset by the greater returns that may ensue (given, again, that low cash extracts a negative toll while greater wealth exhibits diminishing value). Or viewed another way, choosing to keep a substantial cash balance isn’t an “inefficient investment decision”, but instead a decision to “buy more happiness” with a healthy allocation of comfort cash!

Still, this does still raise the question of just how “cash-like” an individual’s liquid wealth must actually be, in order to satisfy the mental demand to have “enough” current assets. The researchers found a relationship between financial well-being and the balances of savings and checking accounts, so clearly physical cash in hand – actual dollar bills – isn’t a requirement. But would other slightly-less-liquid investments like bonds still count? Could stocks and ETFs that can be liquidated “at any time” still satisfy the need? Might the financial advisor be able to frame certain investment assets as “current assets” to make the client more comfortable with holding them in lieu of cash?

Similarly, what about other liquidity alternatives, like the availability of debt (e.g., a revolving credit line, or a home equity line of credit, or a standby reverse mortgage for a retiree)? Might it satisfy the investor’s need for current assets by deploying cash into investments, but having contingencies in place to borrow? Anecdotally, the answer appears to be “no”, given that it’s not uncommon for consumers to both accumulate emergency savings (earning zero) while also still holding unfavorable debt (e.g., high-interest-rate credit cards). Which suggests that the desire for cash is so strong that it’s not enough to use it to pay down debt and then just “re-borrow” later if necessary. We want to actually have the liquid wealth. (Technically, a similar phenomenon is occuring for any investor who keeps a mortgage while also holding a diversified portfolio including bonds, rather than using the bonds to repay the mortgage.)

Nonetheless, what all this suggests is that advisors pushing clients to put “as much of their cash to work” as possible could actually be causing greater financial stress, even if the mathematical reality is that on average deploying the cash will lead to greater financial wealth. In the extreme, it’s even conceivable that “over-investing” clients out of cash (that they don’t need for financial purposes, but might have needed for psychological purposes) could make them more likely to panic in volatile markets, and conversely that encouraging clients to hold enough “comfort cash” (whatever they feel is sufficient) might make them more willing to ride out times of uncertainty. Not because they need the cash, but because it satisfies their need to fill the “current assets” mental bucket, regardless of actual need.

On the other hand, it’s important to note that where the cash is held is likely to matter as well. To the extent that the desire for cash is a desire to “fill” the current assets bucket of the mental accounting framework, holding the cash in an investment account may still be sub-optimal. Because investment accounts, and especially retirement accounts, are more likely to be ear-marked as “future income” rather than “current assets” anyway. In other words, it may not just be about satisfying the client’s cash need, but specifically about holding the cash in a checking or savings account at the bank, and not in the portfolio. And in turn, this further opens the door to advisor technology solutions that help to manage and maximize cash yields (if holding more cash is really “necessary” after all).

But the bottom line is simply to recognize that, in a world where human beings are not always perfectly rational, the optimal pure investment strategy – to minimize low-yield cash to the extent it’s not necessary – may not actually make clients more satisfied with their own financial well-being. Which means perhaps it’s time to stop treating cash like a “problem” to be minimized, and more like a client psychological need to be satisfied, where the starting point is to ask them “how much cash do you need to hold to feel comfortable”, and then build the rest of the portfolio solution around that constraint. Which might actually help the client better stay invested for the long run anyway.

So what do you think? Does having more cash-on-hand (or in a liquid bank account) really help consumers to sleep better at night? Is it reasonable to “accommodate” a psychological desire for having more cash, if it helps clients to be happier? Please share your thoughts in the comments below!