Executive Summary

Social Security operates as an income replacement formula, with higher benefits for those who work for more years. As a result, benefits are very limited for those who don’t work for very many years, and are much higher for those with a full working career.

To avoid confusing those who haven’t worked very many years yet – but plan to – the standard Social Security benefits statement projects out anticipated future Social Security benefits based on the assumption that the individual will continue working until retirement. Which allows the individual to understand what Social Security benefit they are “on track for” as they continue to work until full retirement age. Except, of course, that not everyone actually plans to work until full retirement age!

For those who intend to retire early, the end result is that the Social Security Administration’s projected benefits calculation may turn out to be substantially higher than what someone will actually receive if they retire early, and never actually work as many years as anticipated. The lower someone’s lifetime earnings overall, and the earlier he/she retires, the more dramatic the impact can be, commonly reducing benefits by 5% to 10% when retiring early, and potentially far more for “extreme” early retirement. Although the impact is also substantially affected by whether recent earnings were higher or lower than their long-term average… and whether they’ve already paid into the Social Security system for at least 35 working years (or not).

Ultimately, the reality is that Social Security benefits aren’t actually reduced for those who retire early – they simply stop accruing additional benefits when they stop working. But given that Social Security projects the assumption of work until full retirement age, it’s crucial to recognize that actual benefits may be lower for those who retire early – even if they wait until full retirement age to actually receive those benefits. In the end, that may not stop a prospective early retiree from making the decision to stop working – and notably, continuing to “work” even after retirement can continue to increase benefits as well – but at a minimum, it’s crucial to take a moment and look at the individual’s inflation-adjusted historical earnings, to understand whether or how much of an impact not working to full retirement age may actually have on projected benefits!

Calculating The Income Replacement Rate For Social Security Benefits

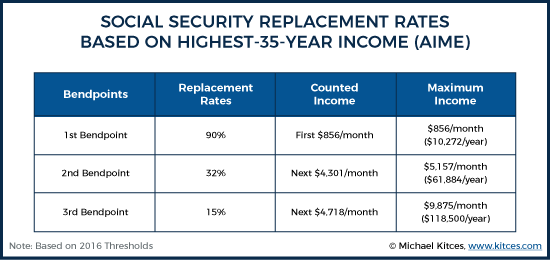

Although not commonly understood, the calculation of Social Security benefits is really nothing more than an income replacement formula, similar to a pension. Just as a pension might offer an up-to-70% replacement rate (based on years of service) based on the average of your last 5 years of wages, Social Security also provides benefits that are a replacement of your earnings based on your years of service. The primary difference is simply that Social Security uses a 35-year average of earnings that accrue based on your years of service (rather than just your last-3 or last-5 years of wages), and the replacement rate itself is based on your income (with those at the lower end of the income spectrum getting a higher replacement rate).

The individual’s 35-year average of earnings is known as “AIME” – Average Indexed Monthly Earnings – and is calculated as a monthly average income over 35 years (i.e., 420 months), and is inflation-adjusted (to account for the fact that 35 years ago, wages were lower simply because of inflation that hadn’t occurred yet). Notably, the lifetime earnings used to calculate the 35-year average of inflation-adjusted income is based on the highest 35 years of historical earnings, regardless of whether they were consecutive years or not.

Replacement rates are then calculated based on the highest-35-year AIME amount – with the first $885/month replaced at 90%, the next $4,651/month replaced at 32%, and anything else (up to the maximum $127,200/year, or $10,600/month wage base) replaced at 15%.

The final benefit is known as the Primary Insurance Amount (PIA), and becomes available to the retiree at Full Retirement Age (currently age 66, but rising to age 67 in the coming years).

Example 1. Over his lifetime, Charlie’s 35-year average income was $73,000 (once adjusted for inflation), or $6,083/month. As a result, Charlie’s Social Security benefit would be 90% of the first $885/month (which is $796.50/month in benefits), plus another 32% of the next $4,651/month of income (which is $1,488.32/month in benefits), plus 15% of the last $547.33/month in income (another $82.10/month in benefits), which means his total benefit is $796.50 + $1,488.32 + $82.10 = $2,366.92/month in Social Security benefits at Full Retirement Age. Relative to his $6,083/month of AIME, this is an effective replacement rate of 38.9% of his income in retirement.

To the extent the individual starts benefits early (i.e., before full retirement age of 66), the PIA is reduced by 6.66%/year for each year early, plus 5%/year for each additional year, up to a maximum early retirement age of 62 (which would be 6.66%/year x 3 years + 5%/year x 1 year = 25% reduction). Conversely, if the individual delays past full retirement age, benefits are increased by 8%/year for each delayed year, up to a maximum of age 70 (which would be 8%/year x 4 years = 32% increase). These formulas are ultimately adjusted down to the exact starting month of early or delayed benefits, for those who don’t have a full retirement age of exactly 66, or who start benefits a partial year early or late.

Example 1b. Continuing the prior example, if Charlie was born in 1955 (such that he’s turning 62 in 2017), his full retirement age would actually be 66 years and 2 months, which means starting his benefits as early as possible would be a reduction of 6.66%/year x 3 years + 5%/year x 1 year and 2 months early = 25.83% reduced. Thus, his $2,366.92/month benefit (at full retirement age) would be only $1,755.47 by starting as early as age 62.

How Social Security Benefits Are Projected At Retirement

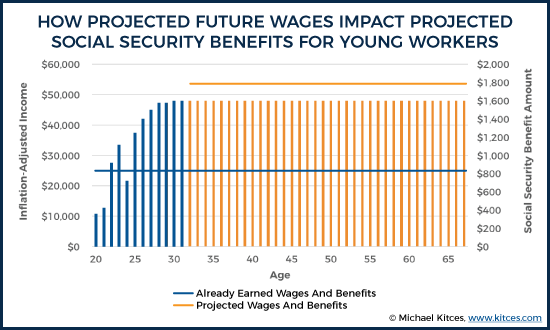

As noted earlier, Social Security benefits are calculated as an income replacement rate based on 35 years of your (highest) historical earnings (adjusted for inflation). Which means when you’re just getting started in your career as a teenager or 20-something, most of your 35-year average of earnings would be $0s, and any projection of Social Security benefits based on actual earnings would be near $0 in the early years. You wouldn’t really know how well your Social Security benefits were on track to replace your income in retirement until you actually had 35 working years to see the cumulative benefit (even if you knew and were planning to be working that long up front).

Accordingly, the Social Security Administration provides a regular statement to project future Social Security benefits, assuming that you will continue to earn at your current income level (based on your earnings for the past two years). This is shown as your “estimated taxable earnings per year after 2017” on the front page of the Social Security benefits statement. And projected benefits on the Social Security statement assume that amount will continue to be earned in every year until full retirement age – which can substantially change the individual’s “historical” earnings for calculating benefits (even though the earnings haven’t happened yet!).

Example 2. Andrew is a 32-year-old whose income has averaged about $35,000/year over the past 12 years (including both work he did in college, and after college). For the past 2 years, his annual salary is up to $48,000/year.

Accordingly, when his $35,000/year of average earnings for 12 years is stretched across the 35-year formula, Andrew’s “lifetime” average inflation-adjusted earnings is only $12,000 (including 23 years of $0s), or just $1,000/month. Which means his benefits would only be 90% x $885/month (the first replacement tier) + 32% x $115/month (his earnings in the second tier) = $796.50 + $36.80 = $833.30/month.

However, if Andrew really does plan to work for the rest of his available working years until full retirement age (which will be age 67 for a 32-year-old today), he can add another 35 years of income (from here) at his current $48,000/year salary, which would overwrite all of his prior years of earnings with higher income years, and provide him with a future Social Security benefit based on $48,000/year (or $4,000/month) of earnings. Which would result in a Social Security benefit of 90% x $885/month + 32% x $3,115/month = $796.50 + $996.80 = $1,793.30/month.

As a result, Andrew’s Social Security statement will show a projected benefit of $1,793.30/month, and not $833.30/month, even though the $833.30/month is the only benefit he’s actually earned up to this point. Because $1,793.30/month is what he’s on track to earn based on his employment and earnings trajectory, assuming he continues to work at his current pace.

Notably, the future benefit a prospective retiree would actually receive at full retirement age will actually be even higher than the projected benefit amount reported on the Social Security statement, due to the additional impact of inflation between now and full retirement age. Future benefits are projected assuming future earnings but are reported in today’s dollars, and as a result do accurately project the purchasing power of future benefits (even though the actual future dollar amount will be higher as inflation continues to compound). And the current-dollar value of Social Security benefits may even be understated, as Social Security actually adjusts the benefits into today’s dollars using wage inflation rates rather than price inflation rates (which may end out understating the value of future benefits by about 1%/year).

The Impact Of Early Retirement On Calculated Social Security Benefits

It’s crucial to recognize that the standard Social Security statement projects benefits assuming continued work, as it means that not working as late as full retirement age can reduce prospective benefits. Not because future benefits are actually reduced by stopping work early (though they are reduced by starting benefits early). But simply because projected statements assume continued work by default, such that its absence will still result in a lower actual benefit in the future than what was previously projected.

However, the actual impact on Social Security benefits of stopping work before full retirement age varies heavily, depending on what the prospective retiree had already earned in benefits – or more specifically, what additional years of work (and income) would have done to that individual’s highest-35-years earnings history.

Retiring Early From Declining Income Below The Highest 35 Years

After all, the reality is that if the worker already has 35 years of work history, all of which are at least as high as current earnings (after adjusting for inflation), then the prospective retiree isn’t actually earning any further increase in benefits by continuing to work! Because the AIME formula only counts the highest 35 years and drops the rest. So if the prospective retiree isn’t adding new years that are higher than the existing ones, the additional years of work have no impact. Which means stopping work early has no adverse impact, either.

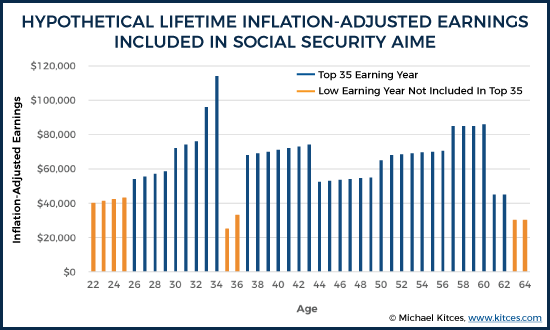

For instance, the chart below shows an individual’s historical (inflation-adjusted) earnings over a career, including a substantial ramp-up in the early years, followed by a career transition (with low income), then a steady series of raises, with a few wind-down years of consulting work at the end. The top 35 years are shown in blue, and the “low” years (not included in the top 35) are shown in orange.

As the chart above shows, additional years of work at the current consulting levels will have no impact on benefits – because there are already 35 years of historical earnings at even higher levels. As a result, quitting work after age 64 won’t have any impact on the benefits that were originally projected to begin at full retirement age of 66. (Though notably, starting benefits as early as age 64 would still reduce them by 13.3% for claiming early.)

Retiring Early From Rising Income Above The Highest 35 Years Of Earnings

On the other hand, if the prospective retiree has more than 35 years of historical earnings, but not all of those prior years were as high as today, there may still be some prospective impact to retiring early. In this case, it’s because the additional years of work are replacing prior years in the calculation of the highest 35 years of benefits. Which means eliminating them from the projection – by retiring early – loses out on some opportunity for increasing benefits.

For instance, the chart below shows the historical (inflation-adjusted) earnings of an individual who has been in his peak earnings years since a big promotion in his mid 50s, and is trying to decide whether to retire early at age 60. His current Social Security statement projects his retirement benefits to be $2,374.24, which implicitly assumes he will keep earning his $110,000/year salary until full retirement age, which means 6 more years of ‘knocking out” his $40,000/year earnings from back in his 20s.

Of course, the reality is that the prior $40,000/year of earnings will still be included in his Social Security benefits, if he stops working early and doesn’t replace them with later earnings. However, that means at the margin, each year he continues to work replaces an “old” $40,000/year salary with a “new” $110,000/year salary, a $70,000 difference that increases the 35-year AIME average by $70,000 / 35 = $2,000/year (or $166.67/month).

Given that he’s at the 15% replacement rate level (given how high his AIME already is), it means that each additional year he works increases his benefit by $166.67 x 15% = $25/month in benefits, or $150/month for 6 more years of working. Given that his projected retirement benefits were already $2,374.24, this means his benefits will be reduced by 6% by retiring at age 60 (even if he waits until full retirement age to receive the “full” benefit!).

Retiring Early Before 35 Years Of Work History

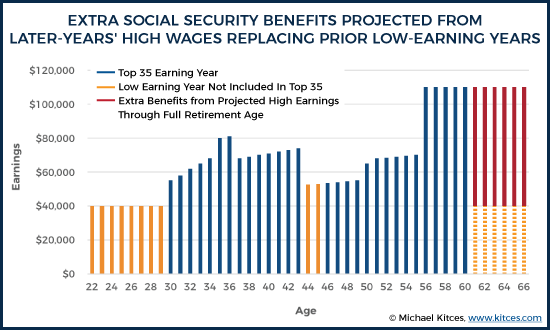

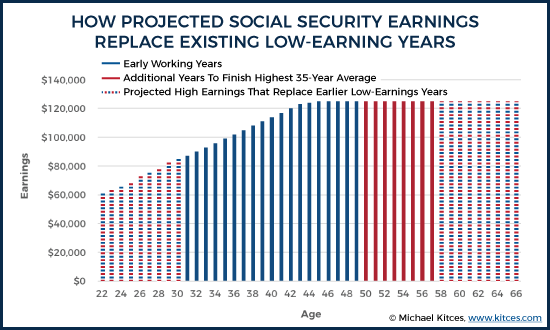

For those who don’t even have 35 years of historical income, though, the effect of retiring early can be even more substantial. For instance, if the individual above had been aiming to retire even earlier, then the reality is that social security early retirement age 55 likely doesn’t even have 35 years of earnings history. As a result, the additional projected years of working through full retirement age would both fill out the remainder of the highest 35 years, and replace lower earning years with new higher years. The exclusion of both – if retirement occurs early – can be substantial.

As the chart above shows, projected Social Security benefits would include 8 more years of $125,000/year earnings to complete the 35-year earnings history, and the subsequent 8 years would further increase AIME by overriding 8 early years that were at lower income levels. As a result, projected Social Security benefits would be $2,854.42/month based on an AIME of $9,885.71/month ($118,628.57/year). However, if the individual actually retires at age 50, and simply locks in the benefits he’s actually earned, the 35-year AIME (with only 28 years of actual earnings history) would be only $8,220.24, and Social Security retirement benefits would actually be just $2,606.21/month, not $2,854.42 as projected with continued work!

Planning For The Impact Of Early Retirement On Social Security

It’s important to remember that beyond “Just” the impact of retiring early on the calculation of projected benefits, that taking Social Security early can reduce benefits by more than 25%, due to the reduction on Social Security benefits claimed before full retirement age.

However, many prospective retirees can ameliorate this impact by simply retiring early, and waiting to actually begin Social Security benefits, simply spending down other assets in early retirement instead (which is often a good deal, given both the potential impact of the Social Security earnings test, and the often-appealing internal rate of return for delayed Social Security benefits).

Yet as shown here, early retirement has a second effect – it reduces the calculated Social Security benefit too, or at least fails to accrue more benefits by continuing to work (relative to the projected benefits on the Social Security statement), even if the retiree waits until full retirement age to actually begin the benefits.

However, the actual magnitude of the reduction will depend heavily on what the early retiree’s recent (and therefore projected) income is, relative to that individual’s earnings history (to understand whether more years of work replace prior years in the high-35 formula, or not). Which means the starting point is just to log into (or create) your account at the SSA’s My Social Security website, and look up what your earnings history actually is!

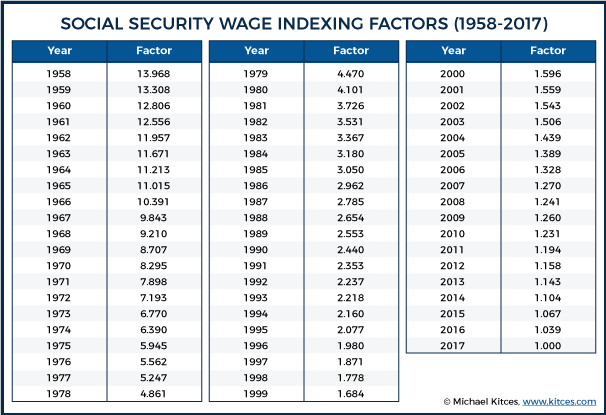

Unfortunately, though, since Social Security benefits are calculated based on the highest 35 years of inflation-adjusted earnings, it’s also necessary to adjust prior income into the current year’s dollar amounts. Based on the current wage indexing factors available from Social Security, income for each year can be multiplied by the indexing factor to determine what the inflation-adjusted equivalent income would have been in today’s dollars.

From there, you can then assess whether or how much additional income years between now and retirement may be impacting projected Social Security benefits, and to what extent the additional income years may either be increasing AIME by adding more years to the 35-year average, increasing AIME by replacing prior lower income years with new higher income years, or not impacting AIME at all because the highest 35 years are already set from prior earnings.

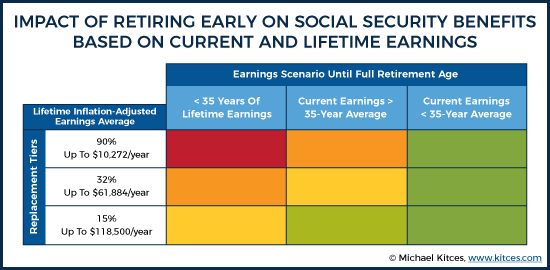

It’s also important to determine whether the average historical earnings would put the individual into the 90%, 32%, or 15% replacement rate tier, as the lower the AIME, the higher the replacement rate, and the greater the impact that additional earnings years will have (or conversely, the greater the adverse impact of not generating those earnings due to early retirement).

As noted in the chart above, those who don’t even have 35 years of historical earnings will be most adversely impacted by retiring early, especially if their AIME is in the 90% or 32% replacement tiers (while the impact is more muted for those already in the more-limited 15% replacement tier, with historical annual inflation-adjusted earnings averaging in excess of $61,884/year).

Those who have at least 35 years of earnings, but new earnings are replacing prior year earnings, will have at least some benefit for continuing to work (and conversely, face some reduction for retiring early). The higher the income replacement rate, the more adverse it will be to retire early and not benefit from that rate. Although in practice, the magnitude of the impact will depend on how much higher future earnings are anticipated to be over prior historical years. If the “new” years will only be $10,000/year higher in earnings than the (inflation-adjusted) past, the impact is still limited. If new years of income have a bigger gap, the consequences of retiring early are more severe.

On the other hand, for those where new earnings would be less than any of the prior highest 35 years of earnings history, the reality is that retiring early will have no actual adverse impact on Social Security benefits. This is why it is so crucial to determine historical (inflation-adjusted) earnings to make the assessment; because it’s the only way to find out if new earnings are actually higher than any of the highest in the prior 35 years, or not.

Of course, it’s also important to remember that the earlier the retirement, the more dramatic the cumulative impact can be. While retiring one year early rarely impacts Social Security benefits by more than 0.5% to 1% of benefits (especially for those already in the 15% or 32% replacement rate tiers), retiring 5+ years early can have a more substantial impact, and “extreme” early retirement (e.g., for those who retire in their 40s or earlier) can have a very dramatic impact, with actual Social Security retirement benefits far below what is projected from Social Security.

On the other hand, it’s also important to bear in mind that with the availability of spousal and survivor benefits, as long as one spouse (typically the higher earner) delays until age 70 and works to maximize their benefits, there is often no adverse impact for the other spouse to retire early and claim Social Security benefits early (as his/her own benefit, and additional years of work, will be overwritten by the spousal benefit anyway).

For those who want a more detailed estimate of the consequences of early retirement, the Social Security Administration itself does provide access to your Earnings History via the My Social Security website, a Retirement Estimator that can calculate what benefits would be reduced to if you retire early (which simply allows you to input your early retirement age, using Social Security’s data of your earnings history, to show you what your reduced benefit would be, assuming you also start early at age 62), or a highly detailed calculator tool you can download and install locally on your computer, called AnyPIA, to analyze further.

At a minimum, though, it’s important to recognize that while retiring early technically doesn’t reduce benefits – as Social Security benefits simply accrue to the positive by continuing to work, as long as it increases your highest-35-year average – the fact that the Social Security benefit statement by default assumes that you will continue to work until full retirement age means that a decision to retire early can and often will result in lower-than-originally-projected benefits. And the fewer years of earnings history you have, and the lower your overall income (such that you’re in the 90% or 32% replacement tiers), the more dramatic the impact. For those with a substantial history of earnings – e.g., 25+ years – fortunately the impact usually isn’t too severe, but can still be 0.5% to 1% of a reduction for each year of early retirement (in addition to the further reduction for actually claiming benefits early), which adds up quickly for those who retire very early. Though on the other hand, the fact that it’s possible to continue to increase benefits after retirement – even and including if you’re already receiving benefits – also means that those who “retire” but still work, even part time, may be able to further ameliorate the adverse impact of retiring early on Social Security (especially for those who still didn’t have 35 years of earnings history yet!).

So what do you think? Do retirees understand the implications of retiring early on Social Security benefits? How do you help clients evaluate the decision to retire early? Please share your thoughts in the comments below!