Executive Summary

From February 7th through February 9th, the CFP Board’s new Center for Financial Planning hosted their inaugural Academic Research Colloquium (ARC) in Washington D.C. The event brought together 215 academics from 130 colleges and universities to share and discuss research relevant to the financial planning profession, as a part of the CFP Board Center's longer-term goal of establishing itself as the “academic home” for the financial planning profession (and the research that supports it).

In this guest post, Derek Tharp – our new Research Associate at Kitces.com, and a Ph.D. candidate in the financial planning program at Kansas State University – provides a recap of the 2017 CFP Academic Research Colloquium, and highlights a few of the latest research studies with particularly relevant takeaways for financial planning practitioners.

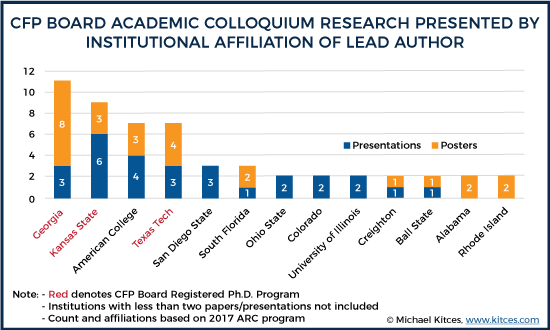

The 2017 CFP Academic Research Colloquium had a strong showing from some core financial planning academic programs, with scholars from Texas Tech, Kansas State, Georgia, and The American College serving as lead authors for nearly 50% of all research presentations and poster sessions. Additionally, the colloquium was successful in drawing in scholars from outside of the core financial planning programs, featuring lead authors from 27 other academic institutions, including Wharton School of Business, Harvard Medical School, and Yale.

The colloquium featured a wide range of topics. Some particularly relevant themes for financial planning practitioners ranged from diversity issues within financial planning (including an analysis of the experiences that increase female likelihood of pursuing a career in financial planning, as well as an examination of the predisposition of women to use the services of a financial planner), to client trust and communication (including the use of solution-focused financial therapy techniques to help clients set financial goals, and an investigation of how different types and frequencies of communication are associated with client satisfaction, trust, and commitment), and the always important topic of retirement planning (including a detailed examination of the use of QLACs in retirement income planning).

Overall, the inaugural CFP Academic Research Colloquium was an objective success. Attendance was strong from a wide range of educational institutions (including many not traditionally known for financial planning), research submissions were higher than expected, and the Center for Financial Planning was successful in recruiting a diverse group of academics and practitioners, above and beyond even what the FPA has been able to achieve in recent years with its partnership with the Academy of Financial Services. In the coming years, we will see whether the Center for Financial Planning is successful in their pursuit to become the academic home of financial planning research, but so far it's off to a very strong start.

2017 CFP Academic Research Colloquium

From February 7th through February 9th, the CFP Board’s Center for Financial Planning hosted their inaugural Academic Research Colloquium (ARC) in Washington D.C. The event brought together 215 academics from 130 colleges and universities to share and discuss research relevant to the financial planning profession. The CFP Academic Research Colloquium is part of a longer-term goal to establish the CFP Board Center for Financial Planning as the “academic home” for the profession.

Like most academic conferences, the CFP ARC included both paper presentations (breakout sessions where researchers present their research) and poster sessions (sessions where researchers stand by posters summarizing their research and converse with session attendees). There was a strong showing from some of the core financial planning programs, with scholars affiliated with Texas Tech, Kansas State, Georgia, and The American College serving as lead authors for nearly 50% of all presentations and poster sessions. But the CFP Academic Research Colloquium was successful in drawing in scholars from outside the core financial planning programs as well, featuring lead authors from 27 other academic institutions, including Wharton School of Business, Harvard Medical School, and Yale.

The 2017 Academic Research Colloquium also received strong industry sponsorship, with Merrill Lynch serving as the full event sponsor, and generous best paper awards of $2,500 being sponsored by TD Ameritrade, Northwestern Mutual, Merrill Lynch, and BMO Wealth Management. Other exhibitors included CFP educational publishers such as Kaplan, Keir, and National Underwriter, along with Columbia University’s CFP Board Teaching Program (an education program for those who would like to teach CFP education), industry supporting organizations like Garrett Planning Network and the National Endowment for Financial Education (NEFE), and financial planning software providers MoneyGuidePro and PlanPlus.

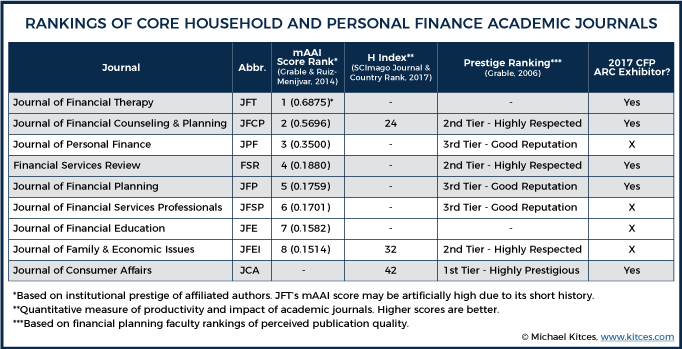

Many of the major journals which typically publish financial planning research were in attendance as well. Based on a journal ranking methodology developed by John Grable and Jorge Ruiz-Menjivar in 2014, four of the top five core household and personal finance journals were in attendance, including: Financial Services Review (Academy of Financial Services), Journal of Financial Counseling and Planning (Association for Financial Counseling and Planning Education), Journal of Financial Planning (Financial Planning Association), and the Journal of Financial Therapy (Financial Therapy Association).

Additionally, though it is not a “core” household and personal finance journal (and therefore not included among the eight core journals identified by Grable & Ruiz-Menjivar), the Journal of Consumer Affairs (American Council on Consumer Interests) was also in attendance, which is notable given that it is one of the most prestigious journals that publishes a decent amount of content relevant to personal and household finance. In fact, the Journal of Consumer Affairs has a higher H-Index (a quantitative measure of productivity and impact of academic journals) and a higher prestige ranking (based on a 2005 study of financial planning faculty) than all of the eight core journals identified by Grable & Ruiz-Menjivar.

Like any academic conference, some presentations were more esoteric and geared towards a narrow academic audience, but much of the research had practical insights for financial planners. The aim of this overview is to identify some particularly practical research from the 2017 CFP Academic Research Colloquium that may be of use to financial planners.

Women In Financial Planning – As Practitioners And Clients

The CFP Board’s diversity initiatives were a consistent theme throughout the colloquium. In April, the CFP Board will launch their “I’m a CFP Pro” initiative aimed at promoting gender and racial diversity among financial planners. Along those same lines, several studies at the 2017 Academic Research colloquium also explored gender issues regarding both consumers and financial planning practitioners.

The Predisposition of Women to Use the Services of a Financial Planner for Saving and Investing

One such study was The Predisposition of Women to Use the Services of a Financial Planner for Saving and Investing by David Evans of Purdue University and Jonathan Fox of Iowa State University.

In this study, which was based on David Evans’ 2009 dissertation at Ohio State, Evans and Fox examined the likelihood of women to seek help with financial questions relative to men. To examine varying tendencies between genders to seek financial advice, the authors’ analysis specifically looked at who the “financially most knowledgeable” spouse of a household was, and assumed that person would be driving the decision to use a planner. They analyzed data from the Survey of Consumer Finances and found evidence that households where the financially most knowledgeable spouse was female, were more likely to use a financial planner in assistance with saving and investment decisions compared to their male counterparts.

However, interestingly, this association was not the same across all education levels. For instance, in contrast to those with a college degree, men with a high school diploma were more likely to seek financial planner assistance than women with a high school diploma. Additional factors that were associated with higher usage of a financial planner included having a higher level of income and being less likely to take financial risk (which may be ironic, given that so many financial advisors focus on helping clients invest in ‘risky’ assets like equities).

Evans and Fox use their findings to draw implications for financial planners, governing institutions, and those who provide resources for consumers. In particular, they note that because men and women may process financial information differently, those aiming to educate consumers making financial decisions should also begin to formulate targeted information that appeals to men and women separately. In addition, they note the importance of planners being conscious of which spouse considers themselves to be most financially knowledgeable, as this can have important implications when working with couples.

The researchers’ findings regarding the different behaviors of advice-seeking couples may also help to explain the rising popularity of focusing on “women” as a type of niche clientele. While the scope of the research was limited to the propensity to seek financial planning advice, the fact that there were varying tendencies across household gender types suggests that there may be other differences in how financially-knowledgeable women seek out advice services as well, which may be conducive to formulating a niche.

In fact, Evans and Fox suggest that going forward we may need to go further than just a purely gender neutral approach and start actively targeting men and women differently. Of course, this must go beyond the cliché (and potentially offensive) approaches – such as simply adding a bunch of pink to marketing materials – and, instead, seek ways to genuinely connect with both men and women.

It is also worth acknowledging that households which used a financial planner were still more likely to identify the male spouse as the financially most knowledgeable (1,721 of the 2,691 households identified the male spouse as most knowledgeable). This could suggest there is at least some degree of consumer preference influencing gender biases within industry marketing, but even if that is the case, it raises interesting questions about social factors which may be influencing the division of labor among households and the role that industry may play in shaping that division in the first place.

A Qualitative Exploration of Female Perception of Pre-Service Experiences that Promote Pursuit of a Career in Financial Planning

Sticking with the gender theme, Kristy Archuleta of Kansas State University, Cliff Robb of the University of Wisconsin-Madison, and Charles Chaffin of the CFP Board conducted a qualitative exploratory study of female perceptions of the financial planning profession and experiences that encourage female likelihood of pursuing a career in financial planning.

Key themes that emerged from their research included that women who pursue a career in financial planning:

- Possess a dual desire to help people and work with money

- Had faculty or coursework experience that exposed them to females in those roles (highlighting the importance of faculty diversity)

- Gained practical experience (internships, job shadowing, firms tours, and exposure to practitioner guest speakers)

- Had family support

- Had opportunities to build and gain confidence

The researchers conclude that addressing underrepresentation in the financial planning community requires programs to increase awareness of the profession. In addition, offering multiple practical experiences (e.g., internships and firm tours) that can help boost self-confidence are also crucial—whether through formal experiences such as internships and job shadowing, or less formal experiences such as firm tours and exposure to practitioners as guest speakers. The authors particularly note the importance of multiple practical experiences given that some women were turned off by a single bad experience. For instance, one woman decided to pursue another career after a job shadow experience in which she met with a financial planner who claimed to never meet with clients. Of course, financial planners do meet with clients, but without additional practical experiences to correct her misconception, this participant chose to pursue a different career.

A further implication of the research may be the need to look for new avenues to recruit students to CFP programs in the first place. Currently, introductory financial literacy courses may play a role in attracting students with a potential disposition towards financial planning topics. Yet, if it’s true that both the desire to help people and an interest in personal finance are important to pursuing a career in financial planning, then it’s possible that the intellectual curiosity alone may not be sufficient for attracting students who will ultimately pursue a career in the field. Finding ways to reach students who possess a desire to engage in helping work yet may lack awareness of the potential to do that within a financial planning context may be equally, if not more, effective strategy for finding students who will pursue financial planning as a career rather than merely as a field of study.

Further, as the researchers note, there is a big opportunity for women currently in the profession to help out in this initiative. Getting involved in local university programs, teaching courses, serving as a mentor and a role model to students, or opening the doors of your firm to educational and experiential opportunities (even if unpaid), may all be important and effective ways to further promote gender diversity. To their credit, the CFP Board’s WIN Initiative and WIN-to-WIN Mentoring Program are two specific programs which have been addressing this challenge head on.

Communication And Building Client Trust

Another important topic that received a fair amount of attention at the 2017 Academic Research Colloquium was communication and building client trust.

Financial Goal Setting, Financial Anxiety, and Solution-Focused Financial Therapy

In their study, Financial Goal Setting, Financial Anxiety, and Solution-Focused Financial Therapy, Kristy Archuleta, Katherine Mielitz, David Jayne, and Vincent Le, all of Kansas State University, present experimental evidence that a solution-focused financial therapy approach to goal setting can reduce short-term financial anxiety.

In short, solution-focused financial therapy (SFFT) is a collaborative form of therapy that is focused on the future and setting goals to make a client’s situation better, rather than focusing on the past and where the client is struggling. SFFT is a specific application of solution-focused therapy within the context of financial issues. Of course, financial planners are not psychotherapists (and therefore should not be engaging in psychotherapy) and financial therapists do have a role that is distinct from financial planners—namely, the use of therapeutic techniques to treat mental disorders. Nonetheless, there are arguably still appropriate ways in which the techniques utilized by a financial therapist and a financial planner overlap. One particular area of overlap is the process of asking clients questions to help them set goals.

A core concept of SFFT is that clients already hold solutions to their problems, but may need help tapping into those ideas. For instance, clients may already have specific ideas of how they can save more, spend less, or engage in other positive financial behaviors, yet need some guidance in order to bring those ideas out. The role of an advisor (or therapist) utilizing SFFT techniques, would be to ask a focused set of questions specifically aimed at helping the client set their own goals.

Of course, there may also be times when a client lacks sufficient knowledge to set appropriate goals. In these instances, the role of the advisor would be to step in and provide the knowledge that is causing a gap, but rather than being the “expert” presenting the solution, the advisor would address the knowledge deficit and then step back, allowing the client to continue setting goals. Other key concepts within SFFT include scaling questions, the “miracle question”, and coping questions.

Based on a six-year exploratory clinical study, the researchers utilized results from pre- and post-tests of financial anxiety to examine whether attending a solution-focused financial therapy session reduced levels of self-reported financial anxiety. Participants agreed to take part in a single 20-minute clinical therapy session, in which student-researchers applied solution-focused financial therapy techniques to help participants set financial goals under the supervision of a licensed marriage and family therapist.

The research findings suggest that utilizing techniques of SFFT may allow financial planners to help clients develop financial planning goals in a manner that reduces financial stress. This may be particularly useful given that past studies have found that consumers experiencing low levels of financial anxiety are more likely to engage the services of a financial advisor and experience higher financial satisfaction. As a result, techniques like SFFT may be useful in establishing rapport and building trust when meeting with a prospective client.

Advisors who would like to learn more about solution-focused financial therapy can reference the Methods section of this 2015 paper from the Journal of Financial Therapy. Additionally, Chapter 8 of Financial Therapy: Theory, Research, and Practice provides an in-depth overview of SFFT.

The Value of Communication in the Client/Advisor Relationship

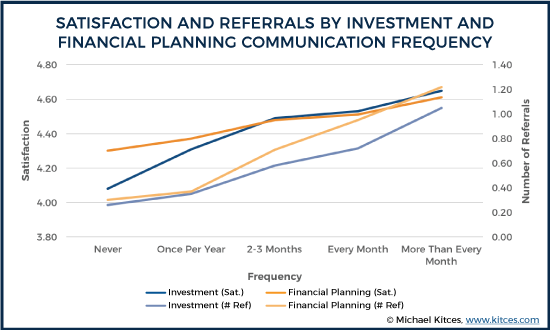

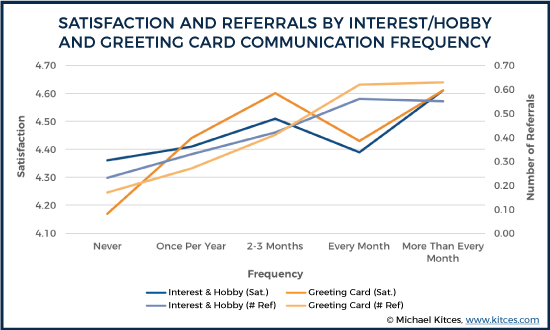

Yuanshan Cheng of Winthrop University, Chris Browning of Texas Tech University, and Philip Gibson of Winthrop University examine how different types and frequencies of communication are associated with client satisfaction, trust, and commitment. In particular, they examine the use of educational communication (both investment and non-investment education) and non-educational communication (such as greeting cards and notes and client interests or hobbies).

Using data from the Advisor Impact Survey consisting of 1,229 clients (1,088 after removing those who didn’t meet a $50,000 asset minimum or answer related questions) of US financial planning firms in 2014, the researchers find evidence that client satisfaction increases with higher usage of:

- Investment related educational communication

- Greetings cards

- Personal notes

- Scheduled meetings

Interestingly, the researchers warn that the overuse of interests and hobby communications can actually result in LOWER levels of satisfaction, trust, and commitment.

In particular, the researchers found evidence that the positive associations for using hobby and interests communication peaked around a frequency of once every 2-3 months and then declined beyond that. Additionally, the researchers provide the following findings:

- Higher frequencies of investment related educational communications were positively associated with the likelihood of continuing to use an advisor in the future and the percentage of assets they would entrust that advisor with.

- Higher frequencies of non-investment related educational communications were positively associated with referrals

- Greeting cards and personal notes were found to be more effective in building client trust and satisfaction relative to non-investment educational materials (e.g., Medicare, tax planning)

- The value of scheduled meetings seemed to peak around 4 meetings per year

The researchers also provide a warning that if client communication can effectively create client satisfaction, trust, and commitment, then it is possible that low-quality service providers could take advantage of clients who lack the sophistication to validate the quality of the services they are receiving.

Retirement Planning Research At The 2017 CFP ARC

Another topic that received plenty of attention at the 2017 CFP Academic Research Colloquium was the ever-important topic of retirement planning.

Incorporating a Qualified Longevity Annuity Contract (QLAC) into a Retirement Income Strategy

In their study, Incorporating a Qualified Longevity Annuity Contract (QLAC) into a Retirement Income Strategy, Michael Finke of The American College, Jacob Williams of Texas Tech University, and Tao Guo of William Patterson University delve into considerations for the use of a QLAC in retirement.

Introduced through legislative changes in 2014, a QLAC provides an opportunity for retirees to use qualified assets to purchase a longevity annuity equal to the lesser of $125,000 or 25% of the value of their eligible qualified assets. Finke et al. note that a QLAC can effectively serve as a means to shift qualified bond assets intended for later-life spending into an annuity wrapper. Through this approach, the remaining portfolio after purchasing a QLAC will have a higher equity allocation, but this is acceptable given that a QLAC effectively serves as an alternative to a bond allocation (with the added potential for earning mortality credits).

The researchers find that purchasing a $125,000 QLAC results in a reduction of the cost of funding nominal spending from ages 85 through 100 by about two-thirds relative to constructing a comparable bond ladder with a 4% return. Utilizing Monte Carlo analysis, the researchers find that a female retiree with a $1 million IRA and a 50/50 stock/bond allocation following a 4% withdrawal rule, can reduce her risk of running out of money by 31% by purchasing a QLAC with funds from her bond allocation (39% for a male retiree). Additionally, purchasing a QLAC has no impact on average bequest across potential longevity outcomes, because while those who die young may see a reduced bequest, those who live beyond average longevity will actually experience greater terminal wealth.

QLACs appear to be very attractive for retirement planning purposes, but they have seen limited adoption. Unfortunately, QLACs face many barriers to adoption, including client hyperbolic discounting, fear of illiquidity, client bias against “as good as it gets” solutions, and even the conflict of interest that AUM-based advisors face for recommending such strategies. These biases are not insignificant hurdles to overcome, but the potential benefits to retirees make a strong case for the use QLACs as part of a retirement income strategy.

Overall, the inaugural CFP Academic Research Colloquium appears to have been a great success. Attendance was strong, research submissions were higher than expected, and the Center for Financial Planning was successful in recruiting a diverse group of academics and practitioners. A full list of accepted papers and accepted posters can be accessed on the CFP Board’s Center for Financial Planning’s website. The 2018 CFP Board Academic Research Colloquium will be returning to DC from February 20-22, 2018.

So what do you think? Did you attend the 2017 CFP Academic Research Colloquium? Do you have plans to attend in the future? Do you think the Center for Financial Planning will become the academic home of the profession? Please share your thoughts in the comments below!

A divorcee born in 1949 has reached full retirement of 66 and filed for her benefit. Her younger ex-husband then reaches age 66 and also files. She may now receive the spousal benefit which is about twice as large as her own benefit. Should she, and can she change her own current filing to a “restricted application” in order to receive only full spousal benefits thus allowing her own PIA to grow. If she returns to work at age 66 and contributes to Social Security her own benefit would grow by 8% until age 70. Does this strategy make sense?

LL,

A few notes here…

– There’s no requirement for the ex-husband to be age 66 and/or file, to get an ex-spouse’s spousal benefit. All that’s necessary is for the ex-husband to BE age 62 to be entitled. (The “husband must have filed” part only applies if you’re STILL married.) So if the ex-husband was already 62 when the divorcee was 66 and filed for her benefit, she should have gotten her 50%-of-his spousal benefit at the time. Though with ex-spouses, SSA may miss this if you don’t request it, as they don’t necessarily know about your ex-spouse and spousal benefit eligibility until requested.

– Once she’s already filed for her benefits, she can’t file a restricted application for spousal benefits now. She’s already filed. She could suspend benefits, but that would suspend ALL benefits she’s eligible for (so she wouldn’t get the ex-spouse’s spousal). But it also appears irrelevant here – if her ex-spouse’s spousal benefit is larger, it doesn’t matter if she files a restricted application (to get spousal and delay her own), or just files to GET her spousal, because either way if the spousal is larger, that’s all she’s going to get in the long run. In other words, “restricted application” is what you do to get a SMALLER spousal benefit while you wait to switch to your own BIGGER benefit; if your own benefit isn’t bigger, there’s nothing to switch to, as you’ll simply get the larger spousal benefit anyway. (Though it might have been an option if her personal benefit was slightly smaller and would have been bigger with the 32% delayed retirement credits; but alas having filed, it’s too late now.)

– EVEN IF she’s filed, continuing to work will still increase her individual benefits (but not ex-spouse’s spousal benefits, as those are based on HIS earnings record, not hers). See https://www.kitces.com/blog/social-security-and-working-how-adding-to-social-security-work-history-can-increase-retirement-benefit/ for further details on increasing benefits by still working (even while already getting benefits).

– Michael

I had this situation with my mother.. it was complicated by the fact that she received a portion of her husbands military pension, which restricted her access to the ex-spouse SS benefit. When he died at 85, she lost her pension but was able to upgrade her SS benefit. All of this took place decades after one would normally look at this.. the lesson is to gather ALL family data and pay especial attention to any previous spouse or divorce situations. The SS benefit in this example ran dormant for 25 years!

As always, great article and content. Thank you.

Happy to be of service! 🙂

– Michael

Knowledge in this area can be a real “value-add” to clients. On more than one occasion, a potential client has been completely unaware that they were entitled to benefits from their ex-husband’s record. In one case, it meant an additional $15,000/year in income for her.

It felt great to be the bearer of such good news. And they are both still clients. 🙂

-Elliott Weir

Note: It maybe possible for a divorce person to remarry and still collect a divorcee spousal benefit. See POMS RS 00202.045. Re- marriage of a divorced person may still allow him/her to continue to collect their ex-spousal benefit. Here is Rule RS 00202.045 Remarriage of a DIvorced Spouse -Policy:

“The ,marriage of a divorced spouse will terminate entitlement to such benefits unless the marriage is to an individual entitled to widower(er)’s, mother’s, father’s, CDB divorced spouse’s or parents benefits”.

Social Security has many rules to keep track of.

Alan

Is the CFP Board going to release these papers to CFP practitioners ? I could not find any links to the papers, either on the Colloquium’s website or on the member site at CFP.net. I would like to think we would get access to this as our membership dollars went to support it. It is also a good opportunity to offer CE credits for in-depth material (similar to what we get through your site Michael!)

Adam,

The papers belong to the researchers who authored them, not the CFP Board. Most of these research studies are still in pre-publication phase; we linked to them directly, where publicly available. Stay tuned for more of them to be published in final version by their authors over time.

It’s also worth noting that the CFP Board is not a membership association, so our “membership dollars” didn’t go towards this. And in reality, the Center for Financial Planning is separately funded from the CFP Board itself. So our CFP certification fees didn’t go towards this either. The Center for Financial Planning is separately funded through a combination of charitable donations and sponsorship dollars. See https://www.kitces.com/blog/is-cfp-board-seeding-a-future-competing-membership-association-with-its-new-center-for-financial-planning/ for further discussion about the Center.

– Michael

Thanks for the insight Michael! I look forward to reading the papers, I’m glad there will be a central place to get more academic rigor to the profession.