Executive Summary

A core requirement of any bona fide profession is to have a professional Code of Ethics and Standards of Conduct that must be adhered to and a disciplinary enforcement process to remove professionals who don’t honor the standards. And while technically the CFP Board is not a sanctioned regulatory body but a 501(c)(3) public charity that owns a trademark for the CFP marks – and grants CFP certificants the right to use its private trademark in exchange for following its stipulated rules – the organization has been attempting to make financial planning a (more) recognized profession by similarly establishing a Code of Ethics, requiring CFP certificants to adhere to it, and enforcing against those who don’t follow its rules.

Accordingly, to the extent that last year, the CFP Board decided to lift its Code of Ethics and Standards of Conduct to formally adopt a fiduciary standard for all financial advice (or really, financial recommendations of any type) provided by CFP certificants, the CFP Board is now taking steps to refine its processes for enforcing those standards, with a series of proposed updates to its Disciplinary Rules and Procedures.

Yet alongside a number of more process-oriented refinements, the CFP Board has also put forth a rather controversial proposal: to allow CFP certificants to expunge their one-time public disciplinary sanctions (e.g., a public letter of admonition or a temporary suspension of the CFP marks) after 5 years. Despite the fact that recent studies of broker recidivism have found that those who have even “just” one misconduct disclosure on BrokerCheck are a whopping 5X more likely to engage in repeat misconduct, and a more recent study found that those who request expungement of their disciplinary records are even more likely to end out being repeat offenders anyway! While in the internet age when “nothing dies” once it's online, it’s not even clear if expungement of a public sanction from the CFP Board’s website really effectively vacates a CFP certificant’s record anyway… or just makes it harder for the public to find the information they need.

And so at a minimum, if the CFP Board is going to proceed with an expungement process, it should seriously consider more “aggravating factors” like additional private censures or the extent of client harm before automatically granting a time-based expungement, separate the process of expunging public sanctions from “just” bankruptcy-only disclosures, and apply a probationary period to expungement where any expunged sanctions are returned in the event of a future public sanction or private censure.

Ideally, though, the CFP Board should move away from its proposal for expungement, and instead simply provide the means for CFP certificants to add an explanation to their public disciplinary records (akin to what FINRA already provides), and perhaps better aid consumers by clarifying the nature of the infraction and whether or to what extent client harm actually occurred or not. And to the extent there is concern about an uptick in violation of the new fiduciary Standards of Conduct when they launch later this year, consider adopting a more lenient transition enforcement policy for the first year… rather than forgiving all 2020 infractions by 2025 regardless of their actual severity and client harm!

Fortunately, at this point, the proposed Disciplinary Rules and Procedures are just that – proposed – which means CFP certificants still have an opportunity to submit their own Public Comment letter expressing support or concern for the proposals to the CFP Board by January 29th.

CFP Board’s Enforcement Of The CFP Standards Of Conduct

Unlike state-granted licenses to practice medicine or accounting, the CFP certification is technically “just” a private trademark, owned by the CFP Board and licensed to CFP certificants to use. And in order to have the rights to use the marks, CFP certificants must pay the CFP Board’s certification licensing fee, and meet the “Four E’s” of the CFP Board’s Education, Exam, Experience, and Ethics requirements. And for those who fail to meet the upfront (Education, Exam, and Experience) or the ongoing (Ethics) requirement, the CFP Board can deny the use of the CFP marks… or in the case of an Ethics violation, suspend or revoke their future use.

From the trademark perspective, having a disciplinary enforcement mechanism for violating the CFP Ethics requirement – either through a temporary suspension or permanent revocation – is how the CFP Board ensures that professionals who use “their” trademark with the public represent it in a responsible manner.

But from a broader professional perspective… when financial planning itself is not regulated (only its component parts of insurance product sales, investment product sales, and investment advice), the CFP Board’s approach of offering a voluntary designation that has “voluntarily higher” Ethics standards is how the CFP Board can help to lift the standards for the overall financial planning profession. As to the extent that financial planners seek out the CFP Board’s education and recognition of using the CFP marks, financial planners effectively bind themselves not just to their legal and regulatory standards, but the CFP Board’s own (higher) standards.

Accordingly, it’s notable that the CFP Board doesn’t “just” decide whether to allow CFP certificants to keep using the CFP marks, or not, if an Ethics violation occurs. Instead, not only can the CFP Board revoke the marks or suspend them, it also reserves the right to issue a private censure on the CFP certificant’s record with the CFP Board, or even a public letter of admonition (which would be a moot point if the sole goal was to maintain/protect the trademark itself).

However, the fact that CFP Board’s discipline can have very public consequences – from public letters of admonition to a publicly-announced suspension or revocation of the marks – it’s crucial that the CFP Board have not only clear Ethics Standards that will be enforced but also clear and reasonable disciplinary processes for enforcing those standards. Especially since the CFP Board’s new, more stringent Standards of Conduct are set to take effect this October of 2019.

In fact, the looming effective date of the new Standards of Conduct, which expands the scope of both certain disclosure requirements (and more) broadly the fiduciary duty for CFP professionals themselves, means that it’s especially important to have strong disciplinary processes for what could be an uptick of infractions, including a potential wave of "new" infractions for CFP certificants who fail to get up to speed on the new Standards in time.

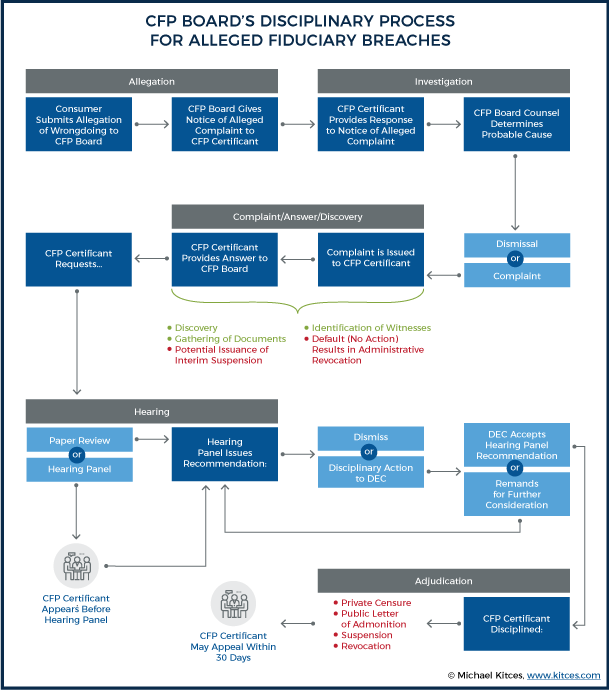

The CFP Board’s Disciplinary Rules And Procedures (And Appeals Process)

Enforcement of the CFP Board’s Code of Ethics and Standards of Conduct is the responsibility of its Disciplinary and Ethics Commission (DEC), which is comprised almost entirely of CFP certificants themselves (appointed by CFP Board CEO Kevin Keller) as a means of providing a “peer review” form of disciplinary enforcement. In other words, “fellow” practitioners determine what is within and outside the normal practices of CFP professionals (as opposed to attorneys or non-practicing CFP Board staff members) and when an Ethics breach has occurred.

The core of CFP Board’s disciplinary process is the formation of a 3-person “Hearing Panel,” which includes 2 members of the DEC and one outside volunteer (to ensure “the public” is represented alongside peer CFP practitioners in the adjudication process), and makes a recommendation to the full DEC for a disciplinary action.

Although notably, the starting point for the CFP Board’s disciplinary is with CFP staff – specifically, a CFP Board “Counsel” (staff attorney) – whose role is to receive alleged complaints when they come in, notify CFP certificants about the allegation and allow them to respond, and then decide if there is probable cause for a hearing to occur (and if so, issue a formal Complaint).

From there, the prospective Defendant has 20 days to respond with an Answer to the Complaint that provides any defense or explains any relevant mitigating circumstances, at which point the CFP Board Counsel can decide whether to proceed to the Formal hearing, dismiss the Complaint, or potentially accept a Settlement (for a Defendant who wishes to accept guilt, expedite the process, and save on the cost of a Hearing).

If the Complaint is recommended for a Hearing, a process of Discovery, gathering Documents, and identifying Witnesses occurs (as well as selection of an attorney or other Counsel to aid the CFP certificant’s defense), a Hearing date is set (and in extreme situations, an Interim Suspension may be issued), and then the Defendant (and accuser) make their case in front of the Hearing Panel. Who can then decide whether the Compliant is not sufficiently proven (or that discipline is not warranted), or make a recommendation for a disciplinary action to the full DEC for approval (which the DEC can then accept, or remand back to the Hearing Panel for further consideration). Although notably, any conviction or finding of guilt that has already occurred in a criminal court or with another regulatory entity (e.g., the SEC or FINRA) will automatically establish conclusive evidence of the CFP professional’s wrongdoing for CFP Board disciplinary purposes as well.

If CFP certificants do not comply with the disciplinary process in a timely manner (e.g., responding to Notices, Complaints, and Requests for Documentation, they can be found in Default and automatically subjected to an Administrative Order of Revocation of the CFP marks).

CFP certificants who believe there were relevant factors or issues not fully considered in the Hearing process then have the option to request an Appeal within 30 days of the Decision, which goes to a separate Appeals Panel to decide whether any of the findings of fact, determined rule violations, and/or disposition of the disciplinary proceeds were “clearly erroneous.”

Bankruptcy And CFP Fitness Standards

Notably, under the CFP Board’s “Fitness Standards” to become a CFP certificant, the CFP Board has also historically required CFP candidates to not have filed for bankruptcy at any time in the past 5 years, under the auspices that those who are struggling to handle their own financial situation shouldn’t be advising others, and also because those facing or recently emerging from bankruptcy may still be under a level of financial duress that could compromise the objectivity of their financial advice. However, CFP certificants did have the option of petitioning the DEC to review their situation and be granted relief.

In 2012, the CFP Board adjusted the bankruptcy process, and rather than barring CFP professionals with “just” one recent bankruptcy, instead requires that single bankruptcies simply be disclosed on the CFP Board’s website (as long as the CFP candidate has no other pending Investigations as well), with only two-or-more bankruptcies either barring the CFP candidate or coming before the DEC as a Petition for Consideration (i.e., requesting a review to consider granting an exception).

CFP Board Proposes Updated Disciplinary Rules And Procedures

In November, the CFP Board issued proposed changes to its Disciplinary Procedural Rules – which is not entirely surprising, as the CFP Board’s expanded fiduciary Standards of Conduct will take effect in October, and may potentially place a greater burden and volume of allegations on the CFP Board to investigate and potentially enforce in the first place.

Accordingly, the proposed Disciplinary changes, in part, just simplify and consolidate the process and its various supporting rules (e.g., technically, the Disciplinary Rules and Procedures and the Appeals Rules and Procedures were separate documents, and now will be consolidated into one), though they also seek to “clarify” and either expedite (in some situations) or deepen (in other scenarios) the CFP Board’s investigative capabilities.

For instance, the CFP Board’s proposal would formally make questions that the CFP Board asks of CFP certificants “under oath,” even and including during the preliminary Investigation process, and such oral examinations can and would be recorded and transcribed for future use (e.g., if the Investigation results in a formal Complaint and a DEC Hearing Panel).

In addition, the CFP Board expanded its ability to adopt rulings from other courts and regulators in its own Disciplinary process. Thus, while in the past, the CFP Board already granted itself latitude to adopt findings of guilt from another regulator (e.g., FINRA or the SEC) or a criminal court proceeding, any Civil Court finding that a CFP professional violated a law, rule, or regulation governing Professional Services, or engaged in fraud, theft, misrepresentation, or other dishonest conduct, will be deemed “conclusive proof” against the CFP certificant for CFP Board purposes as well (and cannot be Challenged). Though the CFP Board will now generally be limited to 7 years from when an alleged violation occurred (or 2 years after a Criminal Conviction, Civil Finding, or Professional Discipline, if later) to issue a Notice of Investigation in the first place (in essence, a form of “statute of limitations” for CFP professional conduct breaches).

The new rules also clarify that the CFP Board’s Investigation process will now more formally culminate in one of three outcomes: a Letter of Dismissal, a Settlement Offer, or a formal Complaint that will then lead to a Hearing Panel (or Paper Review).

In turn, the potential Settlement process is refined under the CFP Board’s proposed Disciplinary Rules, formally establishing a new “Settlement Review Panel” (separate from a Hearing Panel, but also comprised of at least 3 people, a majority of whom must be CFP professionals and DEC members) which, as the name implies, evaluates Settlement Offers and then submits a final recommendation on the Settlement Offer to the DEC for final approval (or Counteroffer). Notably, though, the new rules would require CFP Board staff Counsel to agree to the Settlement Offer before being presented to the Settlement Review Panel or the DEC (while previously, if a CFP professional facing a Complaint and CFP Board Counsel were at an impasse, the Respondent had the option to take a Settlement Offer directly to the DEC).

To further limit any “slippage” in its Disciplinary process, the proposed rules also stipulate that CFP certificants who attempt to drop their CFP marks in response to an Investigation to avoid public Disciplinary action (or in the extreme, terminate their financial licenses or registrations in response to an Investigation) can still be subject to an Interim Suspension of their CFP marks, and ultimately be found in Default (triggering a full revocation of their CFP marks).

In addition, the CFP Board expands its ability to discipline not just CFP certificants, but also CFP candidates who have not yet earned by marks, by giving the DEC the latitude to apply a Temporary or even Permanent Bar against a non-CFP to prevent them from using the marks (temporary or permanently) in the future.

Also notable in the CFP Board’s proposed Disciplinary Rules is that CFP professionals will have an elevated “Duty Of Cooperation” to comply with Requests (e.g., for Information) from the CFP Board regarding an Investigation, even if it’s not the CFP professional themselves being Investigated. (E.g., if the CFP certificant was merely a witness or an otherwise involved party.)

CFP Board Proposes Expungement Option With New Disciplinary Rules Proposal

In addition to its various refinements of its Investigative and other Disciplinary rules, perhaps the most notable addition in CFP Board’s proposed revisions to its Disciplinary Process is the new Sections 11.5 and 16.7, which would allow CFP certificants to file a new “Petition To Remove Publication” to have a prior disciplinary infraction expunged from their public record on the CFP Board’s website.

The Petition to Remove Publication would have to be filed at least 5 and no more than 10 years after the initial date the infraction is first published on the CFP Board’s website, and would be available in any situations where the disciplinary action was a Public Letter of Admonition, a suspension of 1 year or less, or a temporary bar of 1 year or less (in the case of a CFP candidate who was found guilty of wrongdoing before earning his/her CFP certification).

Notably, the Petition To Remove Publication would only be available if it was the CFP certificant’s only publicly-sanctioned infraction. Which means if another public sanction occurred, or the CFP certificant was under a new/second Complaint or investigation, the original public sanction couldn’t be removed.

The Petition to Remove Publication would apply both to “normal” public sanctions for misdeeds (including a public letter of admonition or a temporary suspension or bar), and also to Bankruptcy Disclosures (that are also reported on the CFP Board’s website).

Recidivism and Expungement Of CFP Board Disciplinary Actions

With the rise of the internet, and the ability to search online for information about prospective professionals that consumers might hire, public disciplinary actions have arguably become much more consequential than in the past. As simply put, it’s more likely than ever that a public disciplinary action will actually be discovered by a consumer, from CFP Board’s public records to regulatory systems like the SEC’s IAPD (Investment Adviser Public Disclosure) website, FINRA’s BrokerCheck, or third-party systems like BrightScope.

Accordingly, it is perhaps not surprising that interest in expunging disciplinary records has gained greater focus as well… and not always in a good way. In 2014, FINRA had to tighten its expungement processes under Rule 12805 after a study by the Public Investors Arbitration Bar Association (PIABA) showed that nearly 90% of expungement requests were being granted even in situations where there were financial settlements or monetary awards to consumers (i.e., in material grievance situations where consumers were financially damaged and remedied). And FINRA recently announced changes to further tighten its expungement processes after a follow-up study showed that 93% of expungement requests were still being granted in recent years.

After all, the whole point of having public disciplinary records is to make consumers aware if a broker or advisor has a history of problematic behavior, especially in situations where there was demonstrated client harm that occurred. As while it is true that some people who engage in bad behavior may reform themselves, given that not all complaints result in a public disciplinary action in the first place, even “just” one public disciplinary event can potentially be a hint of more problems that lurk beneath the surface. In fact, one recent study found that brokers who have a single material misconduct event on their FINRA BrokerCheck record were a whopping 5X more likely to engage in misconduct again in the future!

Furthermore, another recent study found that with the current FINRA expungement process, those who sought expungement were actually more likely to re-offend (both those who were successful and especially those who tried for expungement and failed), while ironically successful expungements don’t actually appear to improve the individual’s subsequent career prospects anyway (as firms sometimes ask about prior expunged infractions anyway, and in practice, public disciplinary actions often remain searchable and findable online anyway, given how often regulatory news information and even court documents are accessible or cached on multiple websites).

In this context, it is especially concerning that the CFP Board is not only granting the opportunity for expungement, but that such expungements are effectively “automatic” in all situations that didn’t result in long-term greater-than-one-year suspensions (which, in practice, are not common from the CFP Board) or permanent revocations (where the individual is no longer a CFP certificant, which makes their expungement on the CFP Board’s website a moot point anyway).

Even FINRA has an expungement process that, per the latest updates in Regulatory Notice 17-42, considers each situation on a case-by-case basis to determine the appropriateness of expungement, and under FINRA Rule 2080(b)(1), only grants expungement in situations where the allegation was factually impossible or clearly erroneous, the person was not actually involved in the alleged incident, or the allegation itself was false. While the CFP Board’s proposal would openly grant expungement in all situations regardless of whether or to what extent actual client harm occurred (as long as it wasn’t significant enough to result in a long-term suspension or revocation of the CFP marks in the first place).

Altering The CFP Board’s Proposed Disciplinary Expungement Process

So where should the CFP Board go from here?

The existing data and research suggest that allowing CFP certificants to expunge their records – notwithstanding the concern that some might genuinely be “reformed” from their prior misdeeds – is likely to cause more consumer harm than good. As again, prior Broker Misconduct research has found that those with even “just” a single disciplinary event were 5X more likely to engage in misconduct again in the future, and those who seek FINRA expungement are similarly more likely to re-offend than the average individual with misconduct. And in the case of FINRA, that’s a higher rate of misconduct for those requesting expungement even though FINRA expungements are only supposed to occur in situations where the allegations were false, factually impossible, or the accused was not actually involved in the incident). Whereas the CFP Board’s expungement process would apply for those who unequivocally did engage in wrongdoing, for which the DEC had already determined guilt and issued a disciplinary ruling in response.

In addition, the CFP Board’s current framework to Petition To Remove Publication and expunge a prior disciplinary action considers only other public sanctions and not private censures. Which means a CFP certificant with an established history of wrongdoing, who simply has “only” had one incident elevated to the point of a public sanction, can effectively have all such sanctions removed from public view. Similarly, a future private censure after a public sanction is expunged – which implicitly corroborates the consumer risk of the first incident – will remain hidden from the public, as such a private censure would both remain private, and would not “undo” a previously expunged public sanction.

On the other hand, it’s fair to recognize that bankruptcies – particularly in the case of a single bankruptcy event – are not necessarily a sign of wrongdoing, and once an individual is past the point of personal financial distress, should not necessarily compromise their fitness to be a CFP professional and work with the public. In point of fact, this is why the Fitness Standards only require a public disclosure of a bankruptcy that occurred within the past 5 years, to begin with.

Accordingly, to the extent that the CFP Board decides to proceed with an expungement process – encapsulating both a Petition to Remove Publication of bankruptcy incidents and public disciplinary sanction – the CFP Board should consider:

- Separate Removal of Bankruptcies from Expunging Public Sanctions. While functionally a bankruptcy can be handled with the same Petition to Remove Publication as expunging a public disciplinary action, the standards by which expungement occurs (or whether it occurs at all) should be separated for bankruptcy-only cases, versus those where actual wrongdoing occurred.

- Consider Private Censures as an Aggravating Factor. To the extent that expungement is considered with a Petition to Remove Publication, private censures should be considered an aggravating factor that limits the ability for an expungement to occur (not just other public sanctions).

- Consider Altering The Expungement Time Period Based On The Gravity Of Client Harm. Not all Complaints are the same, even if they have the same public disciplinary action (given the limited number of disciplinary tools available to the DEC). Accordingly, consider separating out public sanctions that were associated with actual client harm (e.g., financial damages to a client, or situations were a material financial arbitration award or settlement occurred), from those infractions that were more “administrative” in nature (e.g., improper use of the fee-only label but where no actual client harm is demonstrated).

- Attach A 10-Year Probationary Period to Expungement. In situations where a Petition to Remove Publication is approved, affirm that any subsequent Complaint that results in a Disciplinary sanction, whether a(nother) public sanction or even “just” a private censure, will cause the previously removed public sanction to re-appear on the CFP certificant’s record as a probationary failure.

Though arguably, given the available data on recidivism rates of those who have even “just” one public disciplinary event, and especially on the higher recidivism rate of those who seek expungement in the first place, the CFP Board should consider not allowing for the removal of public disciplinary actions – especially since they’ll live in the Wayback Machine forever anyway – and instead:

- Create A System Where CFP Certificants Can Attach Notes To Explain A Prior Sanction. Similar to FINRA, CFP certificants can be granted the opportunity to attach a “note” to their record that provides their own perspective and explanation of a public disciplinary action, allowing consumers to both see the historical event itself, and hear (or at least, read) the CFP certificant’s perspective.

- Label And Categorize The CFP Certificant’s Infraction Associated With The Sanction. To the extent that CFP certificants are concerned that a public sanction disclosed on the CFP Board’s website may unfairly bias a client against them (beyond the level merited by the infraction itself), the CFP Board can disclose not only the public sanction itself but also the nature of the infraction, and even provide a basic “categorization” of the type of infraction (e.g., “administrative” vs “client harmed” infractions) to help clarify the substantiveness of the infraction itself.

With such a system, CFP certificants can better explain their public disciplinary records and provide important context about the depth and materiality of the prior infraction, without granting a pathway that “automatically” expunges disciplinary actions given solely the passage of time (even and including in situations where a client was substantively harmed).

And to the extent that the CFP Board is concerned about a potential uptick in violations of the new Standards of Conduct as they take effect later in 2019, consider a pathway similar to the Department of Labor’s own Fiduciary Rule rollout, where it was announced that the regulator would take a more lenient and conciliatory approach towards enforcement for the first year, in addition to granting a transitionary period as the full scope of the rules took effect, to help CFP certificants get up to speed on the new rules as opposed to making examples of the first-reported wrong-doers.

Ultimately, the CFP Board’s proposed changes to its Disciplinary Rules and Procedures are just that – proposed. As noted earlier, a full copy of the proposed (i.e., “updated”) rules themselves can be found here, along with a briefer summary of key changes from the CFP Board here.

For those who still have concerns and want to share their own feedback – whether about allowing the expungement of prior public disciplinary sanctions, or any of the other proposed changes – you can submit a Public Comment to the CFP Board through their Comment Submission System here, or simply by emailing [email protected]. Comments are due by January 29th.

So what do you think? Should the CFP Board allow prior public disciplinary sanctions to be expunged after 5 years? Is the CFP Board taking “too much” control of the Settlement Offer process? Is a 7-year “CFP statute of limitations” appropriate? Should the CFP Board be permitted to conduct “on the record” oral examinations of CFP certificants during the preliminary Investigation phase? Please share your thoughts in the comments below!

Leave a Reply