Executive Summary

While the CFP Board has done a lot to justify its certification fees over recent years – from increasing the number of CFP certificants over the past 10 years by nearly 50% (despite the fact that the number of financial advisors is down over the past 10 years), to raising the status of the marks with its ongoing successful public awareness campaign – an important but little-noticed announcement was buried half way through the CFP Board's recent monthly email update: the CFP Board will be increasing its annual certification fee from $325 per year to $355. And while this increase may seem modest, because $145 of the total certification fee is earmarked for the public awareness campaign, the reality is that this is a 17% increase on top of the $180 portion that actually goes towards operations of the CFP Board. Which raises the question: why such a large increase, and why now?

In this week’s #OfficeHours with @MichaelKitces, my Tuesday 1PM EST broadcast via Periscope, we discuss the recently announced 17% increase in CFP Board certification fees, as well as why accountability of the CFP Board to its certificants is important, and why it is concerning that the CFP Board has given no substantive explanation for why it is pushing through such a large increase – and particularly for an organization coming off of a $1.3M surplus in 2015 and with over $20M in reserves.

Of course, fee increases aren't unusual in the long run for any organization, as it's essential to keep pace with rising staffing costs due to inflation. And this is still only the first increase the CFP Board has put in place since 2011... which, even then, was just tacking on the $145 surcharge to cover the public awareness campaign. It has actually been nearly 10 years since the CFP Board raised its core certification fees, relying instead on the rising number of new CFP certificants paying those fees to fund growth instead. Additionally, both the public awareness campaign and CFP Board satisfaction ratings appear to suggest the CFP Board is making some good progress.

Nonetheless, accountability is crucial, and especially since the CFP Board has been prone in recent years to taking actions without soliciting much input or holding public comment periods. In fact, while the CFP Board did put forth a recent public comment period on proposed changes to their Code of Ethics and Standards of Conduct, the reality is that their Disciplinary Rules and Procedures require the CFP Board to do this, and it has been over 5 years now since the CFP Board put forth a public comment period on any other changes to the 3 E's (Education, Exam, and Experience) – effectively eschewing the practice ever since the CFP Board got "voted down" in negative public comments regarding increasing the number of required CFP CE credits.

Which raises the question once again of why a 17% fee increase, and why now? Especially on top of the fact that the organization is already running a substantial operating surplus of $1.3 million dollars in 2015 and has more than $20 million in net reserves available. Was there a major downturn on the CFP Board's 2016 Form 990 that we just can't see yet? Is the CFP Board trying to raise more revenue internally for its Center for Financial Planning initiative, even though the organization originally said it would be funded separately (especially in light of the fact that the CFP Board tried to put through a $25 fee increase last year in the form of a "voluntary donation" that certificants were going to be defaulted into)?

Unfortunately, the reality is that we just don't know, because the CFP Board gave no substantive explanation for why it is pushing through such a large increase beyond saying that it "supports the operations of CFP Board in fulfilling its mission and strategic priorities". And so, while it's not necessarily a negative for an organization to raise its fees over time, the question remains: why does the CFP Board now, all of the sudden, need another $2.3 million in its operating budget for 2018? And what does it take to get some transparency and basic explanations from the CFP Board on why it is pushing through a 17% fee increase?

(Michael’s Note: The video below was recorded using Periscope, and announced via Twitter. If you want to participate in the next #OfficeHours live, please download the Periscope app on your mobile device, and follow @MichaelKitces on Twitter, so you get the announcement when the broadcast is starting, at/around 1PM EST every Tuesday! You can also submit your question in advance through our Contact page!)

#OfficeHours with @MichaelKitces Video Transcript

Welcome, everyone! Welcome to Office Hours with Michael Kitces.

This week, rather than taking one of your direct questions, I want to spend a few minutes talking about an important – but I think little-noticed – update that was buried halfway through the CFP Board's last monthly email update. Which is that the CFP Board is increasing its annual certification fee from $325 a year up to $355 a year.

The fee increase will be effective for everyone who renews their CFP certification starting November 1st or later, and it also includes everyone who goes through their initial CFP certification process after November. So everybody who's planning on taking the November exam coming up and passes the CFP exam is going to find out that once they do that and they get their CFP marks, certification fee's will be a little more expensive than previously expected.

Now, I can't fault any organization for periodically raising its fees. You know, it sucks from the consumer end to have to pay, but it's an inevitable reality, especially for any sizeable organization. If you have a lot of employees who tend to want raises every year, at some point, you have to increase your prices to keep up with inflation. And in point of fact, this is actually the first change in the CFP Board Certification fees since July of 2011 when its public awareness campaign first launched. But once you consider the fact that a part of our annual certification fee is the public awareness campaign, it turns out that this fee increase is actually a much bigger deal than you might realize.

CFP Certification Fees And The Public Awareness Campaign [Time - 1:45]

For those who don't remember or who got their CFP marks since 2011, prior to the CFP Board's public awareness campaign, the certification fee for CFP certificates was $360, payable every two years. The biannual fee structure was done that way to line up with the biannual CE certification cycle. So you need 30 hours of CFP CE credits every two years to renew and you paid a $360 certification fee every two-year renewal period. Which simply meant you affirmed your two-year CE cycle was done and then you paid your two-year recertification fee.

Now, when the CFP Board introduced their public awareness campaign, it announced two changes to the CFP certification fee at the time. The first, and kind of the big one, was that it was adding a $145 per year surcharge to the certification fee, specifically earmarked for the public awareness campaign. Now, multiplied across what at the time was about 64,000 CFP certificates, that produced about $9 million a year for the CFP Board to allocate to public awareness on top of a multi-million dollar commitment the organization made from its own reserves. The public awareness campaign was a big deal when it launched.

Now, the second change that was made at the time was to convert that biannual $360 certification fee into an annual $180 fee in steps. So they just took the $360 every two and made it $180 every one which adds up to $360 every two.

Now, paired together, that's how we got our current $325 a year certification fee that started in July of 2011. It was $180 which was the annual certification fee, basically to cover operations of CFP Board, and then another $145 a year specifically for the public awareness campaign. So, in this context, a $30 certification fee increase is a bit more sizeable than you realize because it's not really a $30 increase on $325.

Functionally, it's a $30 increase on the certification fee portion, which means CFP Board is moving their fee from $180 to $210, or across their whole operating budget, that's a 17% increase on the certification fees over what it's been charging for the past couple of years. And multiplied across what's now more than 78,000 CFP certificants, we're talking about a roughly $2.3 million revenue bump for the CFP Board next year. That's a $2.3 million increase in fees for an organization that runs its core on only about 14 million in certification fees in the first place, plus about $4 million for exam fees and CE sponsor fees.

Which raises this question, why so much of an increase now and all at once? Now, again, the increases aren't unusual in the long run and this is the first fee increase the CFP Board has done since 2011. And again, the increase in 2011 was just adding the $145 public awareness campaign surcharge on top of the what then was $360 biannual fee or $180 a year at the time. I think it's actually been almost 10 years since the CFP Board raised that core certification fee from $180 a year or $360 every two years.

In the meantime, it's just been relying on the growth and the top line number of CFP certificants who pay those fees to grow the organization. So catching up for a decade's worth of inflation adjustments is not unreasonable, but still, it's pretty noticeable when it happens all at once like this. Especially when the CFP Board ran a $1.3 million surplus in 2015 which is the last year. Their Form 990 is publicly available. So it's not like they're hurting for revenue on the operating budget right now.

Public Awareness Campaign And CFP Board Satisfaction Ratings [Time - 5:29]

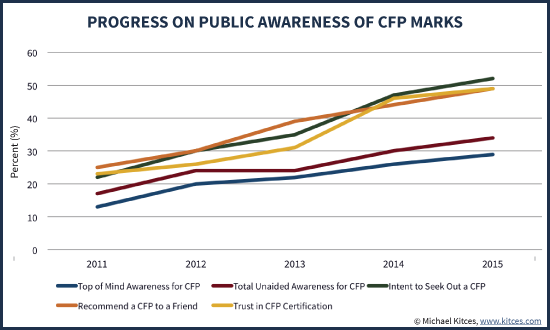

All this being said, I do think it's worth recognizing the substantial progress that the CFP Board is making these days in executing on its initiatives with the certification fees that we pay. As substantial as the fee increase was for the public awareness campaign, the latest tracking study showed that even by 2015, just four years in, CFP certification had passed the CPA licenses as the designation or license that consumers most believe a financial planner should hold.

And every measure of public awareness for the CFP marks, top of mind awareness, unaided awareness, trust in CFP certification, intent to seek out a CFP certficant were all up very materially in the past several years.

Not surprisingly, then, the CFP Board did a recent satisfaction survey amongst us – the CFP certificants – and found a mere 8% said they're dissatisfied with the effectiveness of the public awareness campaign and only 22% believe it wasn't worth the fee increase.

That's a pretty big deal, it was an 80% fee increase and almost 80% of advisors are still fully on board with it. So now we're saying what the CFP Board charges for what it does, it's getting results and most of us actually seem to be pretty satisfied with the results as I think we should be. And at the same time, it's crucial to recognize the success the CFP Board has had in actually growing the CFP marks themselves.

Bear in mind, if you look at data from Cerulli, the number of financial advisors in total is basically flat since 2011 and down almost 10% in the past 10 years, yet the number of CFP certificants is up 25% since 2011 and almost 50% in the past 10 years. That's phenomenal growth to achieve for the CFP Board – to be growing the ranks of the CFPs by 50% in a time when the head count of total advisors declined by 10%.

To the extent we pay CFP certification fees to CFP Board to maintain the marks and build awareness for them, the CFP Board does appear to be doing a heck of a job at executing and getting results for the fees we pay, which is why I so strongly advocate that anyone who wants to establish their career as a financial planner today and is looking forward to their career future needs to get CFP certification. It is becoming the baseline competency standard for actually being a real financial planner beyond just being licensed as an insurance agent or a registered rep salesperson.

And likewise, that's why even if someone has often disagreed with CFP Board about its policies over the years, I advocate submitting public comment letters. Speak out, and get involved to help shape the CFP Board's policies. The CFP marks and the CFP Board aren't going away, so if you don't like what the organization is doing, don't talk about dropping the marks, get involved and be a part of the change that you want to see.

CFP Board Accountability – Why A 17% Fee Increase Now? [Time - 8:17]

Now, at the same time, I'm a supporter of the CFP marks and the CFP Board, but I do think accountability is crucial, especially since the CFP Board has been prone in recent years to taking a lot of actions without soliciting much input or even holding public comment periods. Now, it did put forth a public comment period on the recent proposed change to the Code of Ethics and Standards of Conduct, but that's because its Disciplinary Rules and Procedures require the organization to do so.

Aside from that change, it's been over five years since the CFP Board put forth a public comment period on any other change to the other three E's – the education changes, exam changes, and experience requirement changes – all of which have experienced material changes in five years.

Ever since the CFP Board proposed to increase the number of required CFP CE credits in 2012 and got basically "voted down" in negative public comments, the organization has stopped soliciting public comments and there isn't even a way to access the prior public comments that were submitted. They're all supposed to be public comments, but CFP Board has failed to actually make them public.

And so, in that context, where I do think there are real concerns about CFP Board's accountability, it's a fair question to ask, why exactly it feels the need to take a 17% increase on certification fees for 2018? Why so much of an increase? Why now, especially if the organization is already running a substantial operating surplus of $1.3 million on an $18 million operating budget in 2015, and has more than $20 million in net reserves available?

Was there some major downturn for CFP Board in 2016 that we just can't see on the Form 990 yet because it's not publicly available? Or is CFP Board raising revenue in advance for some new initiative that we haven't even been told about yet and we're being forced to pay for it before we even know what it is? Or is CFP Board trying to raise more revenue internally for its Center for Financial Planning initiative even though they said originally that the center would be funded separately from contributed income?

Especially since CFP Board tried to put through a $25 fee increase last year by defaulting every CFP certificant into a $25 voluntary donation to the Center for Financial Planning, which they quickly eliminated 48 hours after we published an article about it here on Nerd's Eye View. So it may just be a coincidence, but it's hard to believe that the CFP Board tried and failed to put through a $25 a year donation to the Center last year, and now suddenly is pushing through a $30 increase in the certification fee this year. Is the fee increase to generate revenue from the Center that they couldn't get last year? Unfortunately, we don't know because the CFP Board gave no substantive explanation for why it is pushing through a 17% increase in the certification fee beyond saying it supports the operations of CFP Board in fulfilling its mission and strategic priorities.

And so again, while I'm not necessarily negative on any organization that raises its fees over time especially when it's the first increase in such a long time, the question remains: Why does the CFP Board now, all of a sudden, need another $2.3 million in its operating budget for 2018? You don't need $2.3 million on an already profitable $18 million operating budget just to give the whole team well-deserved salary raises.

So what initiatives is this actually earmarked towards? Is this the Center of Financial Planning already experiencing some kind of mission creep by taking a portion of CFP Board operating budget even though it was never supposed to come from operating budget dollars? What does it take to get some basic transparency and explanations with CFP Board on why it's pushing through a 17% fee increase? This isn't just 3% or 5% adjustment we can write off as an annual cost of living tweak. For a 17% increase and a $2 million revenue grab, we should be getting a little more substantive explanation.

In any event, I hope this is some helpful food for thought, maybe an announcement that you haven't seen. This is Office Hours with Michael Kitces, normally 1 p.m. East Coast time on Tuesdays, but I had a conflict yesterday so here we are today. Thanks for joining us everyone and have a great day.

So what do you think? Were you aware of the CFP Board's 17% fee increase? Should the CFP Board be more transparent about what this fee increase is going funding? Is it possible the Center for Financial Planning is already experiencing some mission creep? Please share your thoughts in the comments below!

Michael,

As you probably know already, I fully support all of your efforts for the most transparency and accountability available.

Financial planners certainly are forced to deal with organizational fragmentation (CFP Board, FPA, NAPFA, AICPA PFP/PFS, etc.) that results in a significant amount of overlap of effort and dues. Relative to the amount of annual dues for these memberships (my own financial advisor annual renewal dues are > $3,000 alone), we could see a LOT more value for what we’re putting in than we do today.

Previously, I was sceptical also, and appreciated the isolation of the certification board and other association activities. However, after watching the CFA Institute (which itself has absolutely superb wealth management curriculum, ethical standards, and CE), I’m increasingly convinced the isolation is not serving practicing financial planners well.

For a glimpse of what could be, the Institute is a clear example of effective fiduciary and client standards enforcement, rigorous education and examination requirements, public awareness campaigning, and ethical standards enforcement, all under one roof.

I believe this consolidation has been effective as ensuring very high quality educational content (they aggregate academic writings with guest authors, chapter-by-chapter, which are themselves selected by elected officers) for a standardized minimum body of knowledge, provide optional (and high quality) CE resources (but do not crowd out others from providing such CE as well), and effectively maintain an engaged local association, because every certificant also is automatically made a member of the local chapter.

Therefore, in my view, I believe any forward progress the CFP Board is seeking towards these ends would be leaps-and-bounds better for our fellow financial planner practitioners. You’re undoubtedly warranted in your scepticism of changes, but advancements at the CFP Board that coincide with strong governance rules and policies may be the best path forward for all of us, starting with ending the isolation of the FPA/CFP Board.

I am considering starting a UTBCFP program as in Used To Be a CFP. First they doubled the fee and now another increase with an operating surplus and $20,000,000 portfolio? We got a DJ commercial…fandamtastic. My UTBCFP organization would roll back the annual cost, keep the same CE requirement. Board membership would be voluntary by vote and require 10 year tenure and actual be run by people in our business… The non-profit world is another bubble that needs to be popped….reading their 2015 990, where are they spending $440,000 in professional dues? Why are we paying the CEO almost $1,200,000 in salary and benefits? A total of 6 people over $250,000 a year. I am not getting the value in an organization being run by non CFP’s…it needs to change fast…

As to the $250k per top people, that’s DC for you. The $1.2 million follows the outlandish salary of the head of FINRA. Who’s going to stop either one — no one.

Its really not correct to compare the salary of a Self Regulatory Organization (SRO) executive (FINRA) to the salary of a marketing organization that the judge in the Camarda Case (against the CFP Board of Standards) has compared to a private club. Further, in the worst case, FINRA can regulate a Registered Representative out of business for “bad behavior” while the CFPBS can only remove the right to use the trademark. Its just not a correct comparison in so many ways.

However, if you compare the pay of the head of the SRO regulated by the SEC to the pay of the head of the SEC, you’re in for a shocker! No small wonder that the current President left the SEC in favor of FINRA. Is it reasonable for the head of a quasi-government regulatory agency to be paid 3x what the President of the Executive Branch makes, or as a subset of the SEC regulatory environs, to be paid 4-5x what that head makes?

My original response was to suggest that FINRA’s pay levels are unreasonable. The reason FINRA instituted member bonds, and upped other fees recently was to increase revenue and offset revenue reductions in complaints coming in for arbitration.

Further, until the recent agreement by DOJ to junk class action in BICE agreements, taking the industry and the consumer back to the much lower costs of arbitration — FINRA was no doubt seriously concerned how it’s bottom line would be impacted.

Of course, this naturally leads us to a spin-off discussion about 1) FINRA’s future and their desired oversight of stand alone RIA’s which they desperately want to build their empire. 2) Which also leads us to a spin-off on if Financial Planning should be industry regulated. 3) Then there’s the DOL and Obama officials who confuse financial planning with retirement planning which is just a small segment of financial planning. 4) And then another discussion on why the SEC and FINRA competes with each other on auditing broker dealers, which is a travesty in and of itself. And finally 5) Why shouldn’t the Dodd – Frank rule be amended in order to provide protection to purchasers of Securities Indexed Annuities?

Hey M Kitches, perhaps you’d like to have some fun with these topics in the next few months?

I am constantly amazed that disclosure and transparency are diluted the further up the ladder you go in an organization, from the CFP BOS, to the broker dealers to FINRA. With that said, having served on a non-profit volunteer board @ a credit union, I believe it makes sense to have folks “Not in the business” on the board to keep things impartial, but also and in conjunction with, there should be a board seat(s) for one or two CFP certificants as members “At Large” to ensure accountability. How long those terms are or should be is debatable, but I would suggest two to three years maximum. Enough time to learn and be effective, but not overly burdensome and short enough to not get caught up in the rhetoric. As for the increase in “Dues”, that needs to be explained, period.

Great comments, and gripping analysis by MK. One point overlooked by MK, of which he probably isn’t aware — the costs passed to FPA Chapters by the CFP Board of Standards. As I recall, just prior to the previous increase in CFP renewal fees, the CFP Board of Standards started charging chapters to submit CE for approval. As a Chapter Pres, but non-CFP, I was pretty ticked off. They have since increased the fees. A chapter either has to increase chapter dues, or charge for chapter meetings or in our chapter’s case, make it up with more sponsors at the annual symposium and start charging non-members. While that may make sense from a financial perspective – the net effect is to increase costs on the 10% of advisors who seek to be more professional in their approach. The hidden lining for the CFP organization in the fiduciary rule is to increase the CFP trademark as a value to attract more CFP professionals (certificants is a monumentally stupid description) , at the same time charging for more and eventually make the CFP Board as the place to go.

As to the advertising component for using only CFP’s, let me point out that the initial ad push was limited in scope, and followup advertising has reduced considerably. One wonders where the value of the additional surcharge for advertising if advertising has become limited. FPA has long sponsored a lookup for CFP’s by practice. Can you name the website that the CFP Board developed to compete with FPA? 5…4…3…2…1…time’s up. If you can’t, you just underscored my point.

Carson Wealth Management Group Financial Planning Company is an Omaha, Nebraska-based autonomous individual budgetary warning firm with nothing to offer. We are paid just by our customers and in light of just their interests. Meet with a Certified Financial Planner™ proficient in Nebraska. http://carson-wealth.business.site/