Executive Summary

Building strong client relationships is a high priority for all financial advisors, and one of the most effective tools for establishing and strengthening relationships is good communication skills. Yet, for many financial advisors, actively designing a good communication strategy to put to use with clients is not always an obvious exercise topping their task lists. The importance of this should not be overlooked, though, as a recent YCharts survey found that a majority of financial planning clients felt their advisor contacted them infrequently or very infrequently.

In this guest post, Sean Brown – CEO and President of investment research platform YCharts – shares the results of the recent YCharts Advisor-Client Communication Report, surveying over 650 financial planning clients about the frequency of advisor communication they receive, how they prefer to receive it, and the impact that communication has on whether or not to choose to stay with their financial advisors. In addition to the majority of clients indicating they had infrequent contact from their advisors, a majority of clients, especially those under 50, also expressed that they preferred to receive information from their advisors regarding their portfolio holdings, and 85% of clients said that their advisors’ communication style and frequency mattered when deciding whether to retain their services or to refer the advisor to a family member or friend.

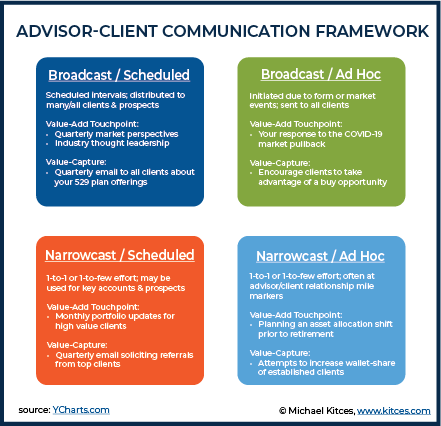

Accordingly, creating a communication strategy can be a helpful way to stay in touch with clients on a regular basis. A 2x2 Advisor-Client Communication Framework can organize communication efforts by cadence (scheduled and ad hoc) and by audience (narrowcast and broadcast), resulting in four ‘quadrants’ of communication style, each with a purpose that can apply to unique situations. These quadrants consist of “Broadcast/Scheduled” communication efforts that occur at regular intervals distributed to many (or all) clients (e.g., quarterly market perspectives), “Broadcast/Ad Hoc” communication initiated due to firm or market events and broadly distributed to clients (e.g., announcements regarding changes in firm personnel, or the firm’s response to recent market events), “Narrowcast/Scheduled” communication that is more individualized and used for key accounts (e.g., monthly portfolio updates), and “Narrowcast/Ad Hoc” communication that is used primarily at important times in the advisor-client relationship (e.g., responses to client inquiries, notice of an asset allocation shift prior to a client’s retirement).

This structure can help advisors identify what they may already be using on a regular basis, and other potentially useful practices they may not yet have leveraged. Furthermore, clients can be segmented into the framework by considering different factors such as their impact on the practice, portfolio strategy, life stage, and relationship status (e.g., new clients, clients at risk of moving elsewhere, etc.).

Ultimately, the key point is that an effective communication strategy can be helpful for financial advisors to stay connected with their clients on a regular basis. By assessing different communication strategies to use for their own unique client segments, advisors can strengthen relationships and, at the same time, add value to the lives of their clients.

People hire a financial advisor because they’re worried about their financial well-being when they don’t want to be.

Put another way, an advisor’s ultimate value-add is to help clients achieve their financial goals, while helping to relieve the stresses and concerns (or at least, being an outlet for them) brought on by money and an uncertain future. But beyond the more tangible work of being an advisor – evaluating goals and needs, building financial plans, constructing portfolios, etc. – how can clients be guided to think, “My advisor’s got it covered,” whenever a question or concern pops into their head?

To stay top-of-mind, reinforce to clients the value you provide, and build stronger relationships, frequent and consistent communication is a necessity.

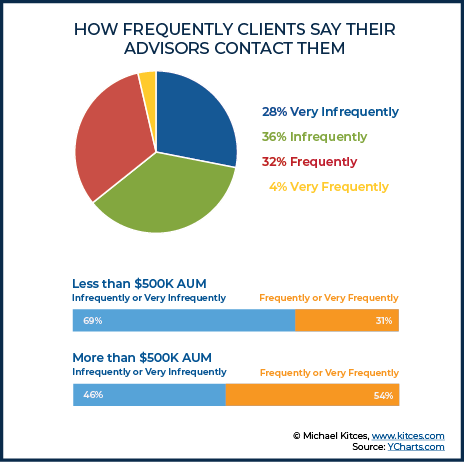

In our recent Advisor-Client Communication Report, which surveyed more than 650 individuals employing a financial advisor, YCharts found evidence that suggests advisors should be doing a lot more when it comes to client communication. In fact, 64% of respondents said their advisor contacts them infrequently or very infrequently, implying that many financial advisors may be proactively engaging and communicating with a subset of their (likely top) clients, but are not consistently and systematically engaging with the majority of their clients.

These shortcomings in communications may have been partially masked (or forgiven) in recent years by an 11-year bull market. However, the emerging downturn is suddenly shining a bright spotlight on such deficiencies.

Of course, the very label “communicate” encompasses a wide range of potential advisor-client interactions, from one-to-many (e.g., newsletters) to one-to-few (client events) and one-to-one (client meetings). To better categorize the many ways in which advisors and clients interact, YCharts developed the Advisor-Client Communication Framework – a tool that helps advisors evaluate their communication strategy and adjust or augment their efforts, ultimately in pursuit of building and maintaining even stronger client relationships.

This Communication Framework can provide an organized way to build a strategy and create valuable touchpoints that are more relevant to each client, engaging not just top clients that tend to receive the majority of the focus, but all clients (even and especially those who may feel less frequently contacted). And by implementing some actionable recommendations that address issues brought to light by the Advisor-Client Communications survey, a new or improved communications strategy can be developed to help make clients’ lives better, and the advisor’s book of business more secure, through valuable touchpoints.

Financial Advisor Communication (Or Lack Thereof!) Influences A Clients’ Decision To Stay With The Advisor And To Make Referrals

To grasp how clients view communication efforts from their financial advisors, the survey in our Advisor-Client Communications Report asked end-consumers about the actual (and desired) frequency that their financial advisor contacted them regarding their financial plan and progress toward their financial goals.

The responses led us to three key insights about the advisor-client dynamic: there are many clients who don’t feel engaged with their advisors, clients want personalized communications from their advisors related to their portfolios, and communication style (and frequency) matter to clients when deciding whether to stay with their advisor and make referrals to friends and family.

Insight #1: Many Clients Do Not Feel Engaged

The majority of survey respondents said they hear from their advisor infrequently, and more than a quarter feel that their advisor contacts them “very infrequently.” And while not surprising, advisors evidenced more proactive communication with their more affluent clients. Nearly half of the clients with $500,000 or more in AUM still responded that they are contacted “infrequently” or “very infrequently” by their financial advisor!

While these figures may seem surprising, just think about the often-referenced Pareto principle, or 80/20 rule. Of all the time an advisor spends communicating with clients, it’s likely that about 80% of that effort is directed at just 20% of all clients!

And that doesn’t mean that efforts are misplaced... the 20% of clients with whom advisors communicate most are likely the largest, most important clients, and also the advisor’s biggest advocates.

Still, though, neglecting literally a majority of an advisor’s clients – according to our own data – can create significant potential ‘cracks’ in the health of the advisory firm’s relationship to its clients.

Of course, time itself is limited to engage in individual one-to-one meetings and phone calls with every client throughout the year. However, as discussed later, one-to-one is just one of many ways to maintain advisor-client communication.

Insight #2: Clients Want Personalized Communications

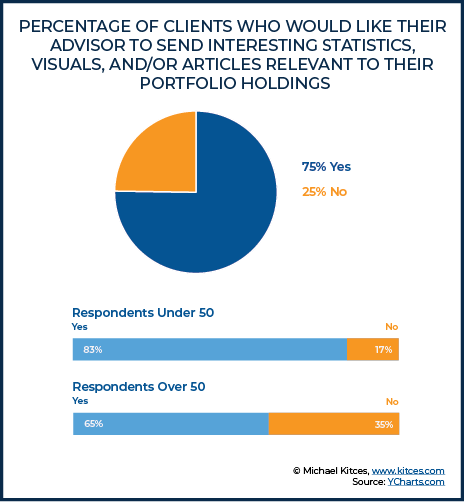

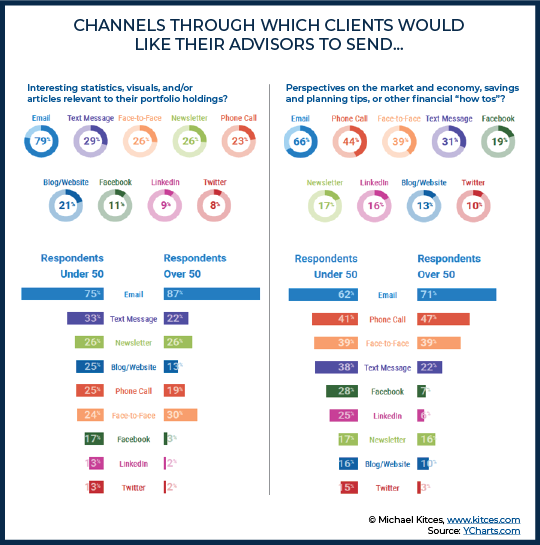

In today’s world of unsolicited spam and overly broad message blasts, when clients hear from their advisors, they want content that is hyper-relevant to them. In fact, 75% of clients indicated that they want their advisor to send news articles, statistics, or visuals… as long as they’re relevant to the client’s own portfolios.

When bifurcating clients by age – those younger than 50, and those 50 or older – there was a clear preference for younger clients in particular to receive proactive article-sharing and similar communication from their financial advisors, with four out of five clients in the younger group showing a strong desire to receive personalized information. Though even amongst older clients, the majority – nearly two out of three clients over 50 – felt the same way.

Of course, the obvious caveat is that ‘personalizing’ communication can take even more time (especially when applied across an entire client base). Though as discussed later, communication – including personalized communication – can still be executed in many forms (beyond just the traditional one-to-one client meeting or phone call).

Insight #3: Success Can Be Directly Impacted By Your Communications Strategy

While clients’ desires to hear from their financial advisors should be taken seriously at face value, the question remains of whether client communications can really impact an advisor’s bottom line.

In other words, is there a tangible return on investment for time and effort put into communications?

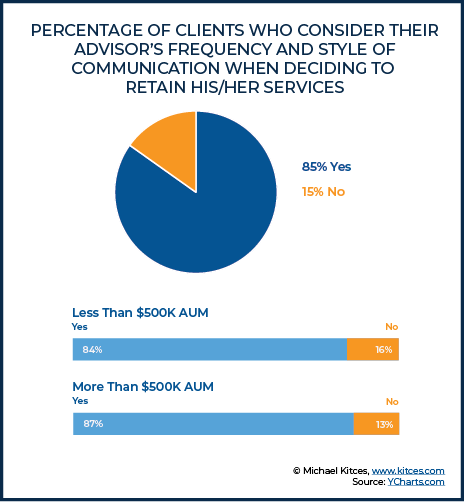

When asked if communication style and frequency would impact a decision to retain their advisor, 85% of clients answered a resounding “yes.” And that number was slightly higher still for clients with $500,000 or more in AUM, who have greater expectations of communication for their advisors given the amount of their fees paid!

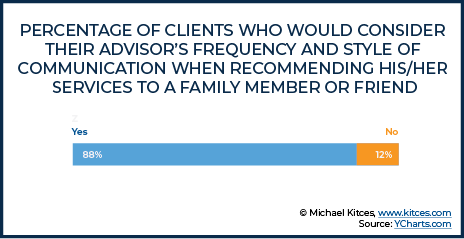

Similarly, this trend of more-communication-equals-more-business holds with client referrals as well. Nearly 9 out of 10 respondents said they would consider communication style and frequency when referring their advisor to family and friends (or not!).

In summary, the Advisor-Client Communications Survey told us that most advisors have limited reach when communicating beyond a subset of their (ostensibly most affluent) clients. Additionally, clients’ desires for personalized touchpoints, together with an emerging bull-market reversal, is creating a potential watershed moment of opportunity for advisors to set up a communications strategy to use with their clients.

It may feel natural to respond to the clients calling today, but in the long run, clients’ satisfaction, retention, and referrals may all be compromised when communication is narrowed to just a small subset of clients. Which makes it even more crucial to leverage tools and technology available today to expand the advisor’s client-communication capabilities.

Key Communication Touchpoints For An Effective Communication Strategy

Before detailing the Advisor-Client Communication Framework we developed from our research, it’s important to understand that there are two different kinds of key communication touchpoints:

- Value-Add Touchpoints. An encounter between an advisor and client(s) where the advisor’s sole motivation is providing value to the client (e.g., an informational blog, some recommended articles, or even a happy birthday text).

- Value-Capture Touchpoints. An encounter between an advisor or client(s) where the advisor’s motivations include their own interests, though hopefully mutually beneficial (e.g., soliciting referrals, proposing new investments to increase wallet share, or pitching a prospect to open an account).

Both Value-Add and Value-Capture Touchpoints have a vital place in an advisor’s client communication process. And notably, there’s nothing bad or evil about Value-Capture touchpoints – not everything has to always be a free Value-Add – but they become much more effective (and possibly less annoying for clients) when paired with the right number of Value-Add Touchpoints as well.

By analogy, think of what it takes to grow tomatoes.

Every day a gardener waters the plant, makes sure it’s getting sunlight, and pulls any weeds nearby. Even after some time, they might only see some small, green, rock-hard tomatoes on the vine. The gardener shouldn’t be discouraged and shouldn’t pick them. They’re not ready… yet!

But after weeks and weeks of watering, weeding, and pounding in stakes to help the vines grow, those tiny green buds turn into big, round, red tomatoes. Now they’re ready. Now they can be picked and cashed in for all the effort that’s been put into them.

Just like growing tomatoes, better client communication starts with adding value to clients’ lives. Once financial advisors have done that adequately, capturing value becomes much easier.

Client Touchpoints Can Be Organized By Timing Cadence and Target Audience

So considering the survey results and the insights it provided, we can explore how valuable touchpoints with clients might be added from using a strategic approach to client communications.

We found that every touchpoint between advisors and clients can be defined by two cadences: Scheduled and Ad Hoc, where Scheduled communications are initiated on a regular, periodic basis; and Ad Hoc communications are only initiated as needed, such as announcements made in response to unplanned circumstances. Furthermore, touchpoints can also be defined by two audiences: Narrowcast and Broadcast, where Narrowcast audiences target one client, or just a few clients, and Broadcast audiences target broader groups (e.g., all clients, all prospects, all firm stakeholders, etc.).

This led us to the Advisor-Client Communication Framework.

Defined with examples below, the Framework combines the cadence and audience factors into a 2x2 matrix that organizes the advisor’s efforts and identifies gaps in how they engage with clients. This tool can help advisors close in on that optimal mix of Value-Add and Value-Capture Touchpoints.

Broadcast/Scheduled communication occurs at regular intervals, contains broadly relevant information, and is sent to all, or many, of the advisor’s clients and prospects. For example, writing a quarterly blog with your perspectives on the economy and sharing it with clients via email or LinkedIn.

Broadcast/Ad Hoc communication is sent to all or many clients and prospects, but instead of being planned, they occur when needed or in response to other events. For example, the market takes an unexpected turn for the worse, so the advisor proactively reaches out to clients and assures them they’re prepared.

Narrowcast/Scheduled communication is used when reaching out to one or a few clients in a regular or pre-defined cadence. For example, a client or group of clients own a concentrated stock position from their employer and the advisor emails them at milestone intervals to reduce the position over time.

Narrowcast/Ad Hoc communication occurs when advisors interact directly with one or a few clients, either before or in response to events affecting only that defined group. For example, when preparing a prospect proposal, any presentation or recommendations made to that individual are Narrowcast/Ad Hoc.

An Advisor-Client Communication Framework For Building And Evaluating Communications Strategies

Now that we’ve reviewed the 2x2 Communications Framework, here are two ways that it can be used to organize Value-Add and Value-Capture touchpoints through an assessment of timing cadence and target audience.

Exercise #1: Evaluate Communications Strategies For Gaps To Fill With (More) Valuable Touch Points

A blank Framework template can be downloaded and used to identify current communication strategies. Within each quadrant on the template, touchpoints can be identified as either Value-Add or Value-Capture.

Which quadrants are empty? Which are crowded? Depending on specific communications goals, the ideal balance may skew toward certain quadrants. But care should be taken not to fall into the natural ‘trap’ of relying too much on personalized meetings and eschewing broadcast altogether, or to rely too much on ad hoc opportunities (e.g., waiting for market events or clients calls to respond to) over scheduled and systematized communication (which takes some time to plan up front, but can ultimately become very efficient to maintain). And as always, the value of each opportunity should be considered versus the effort they require.

Assessing the balance of existing Value-Add and Value-Capture touchpoints can be a useful way to help brainstorm how additional touchpoints can be added to lay the groundwork for stronger client relationships.

Exercise #2: Segment Clients By Different Factors, And Map Them To The Framework

If, after the first exercise, advisors don’t see any clear and obvious areas for improvement, that’s great! They are in rarified air with a well-built communications strategy.

To take it up a notch and build a truly next-level strategy, though, clients can be segmented with different qualitative and quantitative factors. Here are a few ideas to get started:

- Impact To The Practice. Create several impact buckets (e.g., high AUM, propensity to refer new clients, influential in key target markets); it makes sense to spend more time and effort communicating with clients who are identified as most impactful to the practice. (But again, that doesn’t necessarily just mean more one-to-one personalized communication; it could mean incorporating them into more systematized broadcast communication, too!)

- Portfolio Strategy. If model portfolios are used, clients can be segmented by the model they’re invested in, and the securities held in those models (and the same can be done for portfolio sleeves for advisors who use them).

- Life Stage. Depending on their financial progress, clients might have different questions and priorities; are they a new investor, new home-owner, or pre- or post-retiree? For instance, when it comes to market volatility, younger investors might need a broadcast message to encourage them to view it as a buying opportunity, but retired clients may need a different type of communication about how to manage the volatility or adjust their spending from a sequence-of-return-risk perspective!

- Relationship Status (not talking about Facebook here!). Which clients are new relationships? Which are at risk of transferring elsewhere? Which are prospects that barely got away?

Framework quadrants (and the strategies within each quadrant) can be designed strategically around the nature of the advisor’s book of business, with each client segment the advisor identifies assigned to the appropriate quadrant and strategy.

For example, the high-AUM retiree group might greatly benefit from Narrowcast/Scheduled messaging about personal finance beyond their working years. Or a Broadcast/Scheduled strategy can be implemented with a series of blogs and videos that educate young clients on such topics as budgeting, starting a 529 savings plan, and getting a mortgage.

When clients are segmented and Value-Add Touchpoints are tailored to the groups in which they are placed, they have a better experience and are further reminded that advisors are thinking about their specific situation and goals.

Warning: While it may be tempting to over-segment clients, it’s important to stick to a simple segmentation; otherwise, it can become hard to justify the extra effort (to communicate, or just to manage the communication) for only a handful of clients. Each firm and each advisor is unique; accordingly, the set of segments they create will be different and should make sense for who their clients are.

Financial Advisor Communication Strategies Should Align With The Advisor’s Primary Value-Add

A financial advisor’s primary value-add is to eliminate financial worries from their clients’ minds and help them achieve their goals. As such, all of the functional value an advisor provides – building plans, managing portfolios, being a confidante or friend – rolls up to their total wealth of expertise in adding value to clients’ lives.

It stands to reason that the ways in which they communicate with clients should reflect the value they provide. The following sections offer some actionable recommendations to help advisors build out a robust communication strategy to use with clients.

Start Small, Send A Few Articles Every Week

One way to add a touch of personalization with limited effort is to compile a list of helpful or interesting news articles each week, add your own thoughts or opinions as to why the articles are relevant, then send them in an email to all clients. While the email isn’t personalized to each specific client, it is personalized by the advisor sending it to direct their clients’ attention and showing them that their advisor is a knowledgeable resource should they have questions. (Akin to how Nerd’s Eye View sends out its Friday round-up of Weekend Reading articles!)

There’s no need to ask for anything in return when sending out this type of value-add communication; it’s just about pointing out to clients some helpful information they might be interested in. This tactic is an excellent way to start small in building out an effective communication strategy.

Further benefits of the email-of-articles include quick and easy roll-out, creating a one-to-many communications channel, and even if clients don’t read every email they’re sent, they get the message that their advisor is doing what they hired them to do – to guide them away from worry and toward their financial goals, and that the advisor is reading all the relevant information and is on top of the market situation.

Invest In Email Automation Software

An email automation tool is a worthwhile investment, especially for advisors who pursue segmenting clients for communication purposes (like we outlined above).

These software programs help to scale personalized communications, manage segmented client lists, and send emails in bulk. They also provide invaluable data like open rates and click rates so advisors can continually optimize their value-add touchpoints.

Some tools worth looking into include MailChimp, GetResponse, ActiveCampaign, AWeber, Snappy Kraken and LeadPilot.

One email-marketing company, Moosend, created a super-helpful comparison of different email automation providers, all under $20 a month, and advisors can see more industry-specific digital marketing tools on this landscape map of advisor technology solutions.

Explore New And Non-Traditional Communication Channels

Another consideration for client communications is where the advisor is interacting with their clients. Our Advisor-Client Communications Survey identified several channels that clients identified as preferred means of receiving information. And despite the common lamentation about the overwhelm of spam, the top was still ‘good old-fashioned’ email!

Perhaps not surprisingly, several emerging communication channels, namely text messaging and social media, are more popular with younger clients. (Notably, some of the email automation software programs mentioned above also have texting features!)

More than a third said they would communicate with their advisor via text, and Facebook and LinkedIn were the most popular social media channels. Though for both those over- and under 50, email remained dominant, and phone calls and face-to-face meetings also remained strong (particularly for more personally applicable information beyond just basic statistics or shared articles).

For advisors that give their clients a few options for their preferred means of contact, it may be worth expanding those options to include text message, in addition to phone and email. Additionally, encouraging clients to follow or friend your firm’s social media accounts (on Facebook, LinkedIn, Twitter, or YouTube) gives advisors more opportunities to create Value-Add Touchpoints by (virtually) meeting your clients where they’re spending their time online.

Advisors are facing a critical juncture. During the past decade-plus, a historic bull market with limited drawdowns may have led to some very happy clients, but it may have also caused some advisors to lower their guard. The challenge has been accentuated with the recent market turmoil as clients who felt out of touch with their advisors have suddenly expressed far more anxiousness.

However, forces like fee compression, zero-commission trading, and increasingly complex investor demands that face advisors today make client satisfaction, retention, and referrals more important than ever.

Accordingly, an effective communications framework can provide a holistic way for advisors to break down different communication types, so that they can focus on covering a breadth of outreach methods, rebalancing areas that may be overconcentrated or not used at all. Additionally, a well-organized framework can make it easier to identify the tools and solutions that can help support and improve any gaps or weak areas an advisor may identify in their existing communication strategies.