Executive Summary

With a market decline of nearly 30% in just a few weeks as the coronavirus pandemic expands and amidst eye-popping daily market volatility, most financial advisors today are simply trying to help clients to remain calm, stay the course, and not engage in panic-selling. As while it’s relatively ‘easy’ to keep clients focused on the long-term and to stick to their established plans when their retirement accounts are marching steadily higher, it’s a different story when a major disruption occurs. Yet, in practice, following the advice to “do nothing” in the face of historic volatility is challenging, as it’s human nature to want to do something – whether to fight or flee – in the face of a dangerous threat.

However, just because advisors may be guiding clients to “do nothing” when it comes to selling out of their portfolio, it doesn’t mean that nothing can be done. Instead, recent market volatility does present a number of other financial and tax planning opportunities, from the more ‘obvious’ topics, like rebalancing and tax-loss harvesting, to other potentially necessary adjustments, and even opportunities, that might not be readily apparent mid-crisis.

As a starting point, advisors should re-run clients’ retirement projections, which could mean communicating some not-so-pleasant news (such as having to adjust the plans they’ve made for their retirements and/or even their current lifestyle). But knowing whether their path has changed (or in some cases, not!), and by how much the plan will need to be adjusted (often far less than what clients fear) will go a long way towards mitigating their current stress levels.

Advisors can also help clients effectively adjust their budgets as needed. While many have likely already changed some of their spending habits (if only because they are constrained by social distancing from many of their usual activities), some will need to make longer-term adjustments. And while severe (but shorter-term) spending restrictions might seem like the immediate 'best' option to follow, oftentimes smaller (but permanent) cuts can be far easier to adapt to (and can actually be more effective in the long run!).

From another budgeting perspective, making contingency plans for next-in-line sources of cash, should a client deplete their emergency fund, is an important step. While such an event may not seem very likely at the moment, game planning for such an event can at least provide peace of mind, especially since some of those options (such as using a home as a source of funds) take time to secure.

Other potential planning opportunities include reducing loan payments to lenders making special accommodations for those affected by COVID-19, using the once-in-a-lifetime option to transfer funds out of an IRA and into an HSA, fixing “asset-location” problems that have (up to this point) been impractical from a tax perspective, and reviewing (and maybe revising) healthcare proxies, living wills, and advance directives to account for current travel restrictions and the healthcare implications, should a client contract COVID-19.

Ultimately, the key point is that financial advisors are uniquely positioned to help clients – almost all of whom are under an unusually high amount of stress at the moment – by making mid-course adjustments to their plans, staying focused on the bigger picture, creating contingency plans, and generally providing them with some peace of mind in these highly uncertain times. And more generally, doing something – with respect to the financial plan – can help clients feel like they are more in control (even as advisors guide clients not to panic-sell from their portfolios). As with everything, this too shall pass, but the important thing is for clients to take steps to control those things that are in their power to control.

*** Author's Note: Due to the fluid nature of this legislation, some information below (particularly some of the provisions around student loans) has changed since this article was published.

On February 19, 2020, the S&P 500 reached its highest point since a more-than-decade-long bull market run began on March 9, 2009. In the ensuing weeks, a pandemic, the likes of which the world has not seen in generations, has led to an unprecedented pullback in the markets and an even more drastic change in the way most Americans live.

While no one would wish for times like these, it is during these very moments when advisors can provide clients with the greatest amount of value, keeping them focused on the long-term and taking advantage of opportunities that may not otherwise be immediately clear. Certainly, advisors should not ignore ‘obvious’ investment strategies, such as capital-loss harvesting and rebalancing, but there are a variety of other discussions that can, and perhaps should, be had as well.

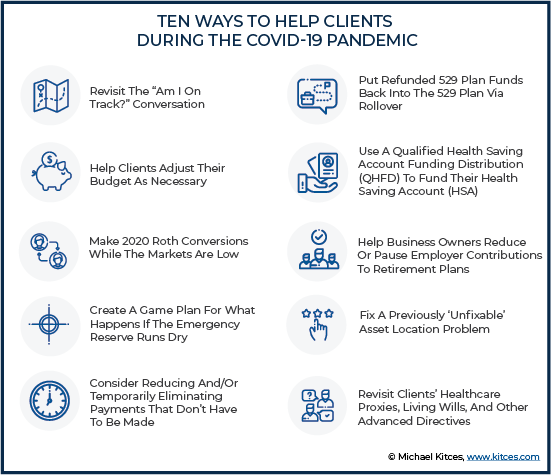

With that in mind, here are ten conversations to consider having with clients during these difficult times to add value, remain top of mind, and make the best of what has become a truly global problem.

#1: Revisit The “Am I On Track?” Conversation

No one enjoys seeing their hard-earned savings ‘evaporate’ before their eyes. But as painful as it may be to see (rapidly) declining balances, the bigger pain point for people is often a forced change to a previously agreed-upon plan.

For younger families, that might be the difference between being able to pay for two years of a child’s college education instead of four years. For those close to retirement, it might mean working an additional year or two beyond the existing target. And for those already in retirement, it may mean an adjustment to discretionary spending.

In some cases, however, clients may have accumulated a buffer significant enough to withstand a substantial market pullback, such as the one we are currently experiencing, to avoid any changes to their plan. Other scenarios may require clients to make certain changes, but those changes may be nowhere near the level that they are envisioning.

With all this in mind, one of the most impactful things that advisors can do right now is to reevaluate, rerun, re-whatever-you-want-to-call-it clients’ plans to be able to give them the answer to the all-important question, “Am I on track?”

Although the impact of recent events will certainly vary from one client to the next (and possibly for the same client with respect to different goals), there is a nearly universal benefit to simply knowing where one stands. Whether the news is good (relatively speaking, of course) or bad, the ‘knowing’ has the potential to reduce anxiety and stress.

Of course, a single advisor may easily be responsible for one hundred or more client relationships, and thus, a prioritization plan for client contact should be created. Advisors should consider prioritizing:

- Clients who have historically expressed greater concern during market pullbacks; and

- Clients who are close to significant goal-based events, such as retirement, a child’s college, etc.

#2: Help Clients Adjust Their Budget (Effectively) As Necessary

For those clients whose plans are materially impacted by the current economic crisis and market pullback, perhaps one of the most valuable services an advisor can provide is to help the client to review their monthly/annual spending to make adjustments, as necessary, to make the plan work again. More specifically, there are two key functions an advisor can play in this role.

First, advisors can help clients to adjust spending in financially effective (and realistic) ways. For instance, many individuals believe that the best way to mitigate a market pullback is to substantially reduce spending – say by 25% or more – for a few years, until the market “recovers”. The reality, though, is that such cuts in spending are not only very painful, but are often not as effective in managing long-term safe withdrawal rates as other less severe, but more elongated spending changes.

Advisors looking to guide clients through the ‘tightening-the-belt’ process should consider encouraging clients to consider much smaller – call it around 3% – but permanent changes to annual spending, instead of recommending very steep short-term cuts. Clients are unlikely to feel anywhere near the pain otherwise caused by changes in shorter-term multi-year spending cuts of 20+%.

And just as important (if not more so), there is ample evidence to suggest that such changes are actually far more effective at dealing with market pullbacks than shorter, bigger spending cuts in the first place!

Second, advisors can serve as a sounding board to help clients talk through and make potentially difficult decisions. Whether a client is 85 or 35, making cuts to existing spending can be difficult. In some cases, the expense(s) to go may be obvious, but other times, it may be more challenging, particularly in situations where spouses disagree on what should be cut. Advisors can help clients to remain focused on the things which are most important to them and to serve as impartial arbiters when/if desired.

#3: Make 2020 Roth Conversions While The Markets Are Low

The decision of whether to make a Roth conversion – or not – is primarily a tax decision, which comes down to answering the question “Would I rather pay tax on this money at my income tax rate today, or at my income tax rate in the future?” with “My income tax rate today.” But once the decision to make a Roth IRA conversion has been made, leveraging the timing of that conversion can add a valuable boost.

More specifically, making a Roth conversion during a market dip can be a particularly opportune time. For those who believe that there is much more ‘pain’ to come – or are at least reasonably fearful of the possibility – there are a couple of potential options to consider.

One such option is to engage in some Roth-Conversion-Cost-Averaging. Simply put, instead of making one large Roth conversion now, spread out the conversion into smaller increments throughout the year. For example, instead of converting $100,000 all at once, do four Roth conversions of $25,000 each month for the next four months.

Another (riskier) option, but one that potentially comes with a higher upside, is to use the 60-day rollover window to try and recreate the recharacterization option that was eliminated by the Tax Cuts and Jobs Act (TCJA) back in December of 2017, effective for 2018.

As advisors will recall, prior to 2018, Roth IRA conversions could be recharacterized (undone) up until October 15th of the year after the conversion. The TCJA eliminated that option, though, thus resulting in a situation where taxpayers are now ‘stuck’ with their Roth conversions, for better or worse.

Or are they?

There is, in fact, a way for some clients to have what amounts to a short window of opportunity to decide whether they want to keep a conversion… or not. It’s not particularly complicated, but, as noted above, it does come with a fair amount of risk, as it raises both potential once-per-year rollover and 60-day rollover concerns. But for those willing to take the leap, here’s how it works:

Step #1: Take a distribution, in-kind, of IRA investments, and put them in a taxable account.

Step #2: Decide whether or not to keep the conversion:

- If you decide to keep the conversion, complete the conversion by transferring the assets IN-KIND to a Roth IRA before the end of the 60+-day rollover window; or

- If you decide NOT to keep the conversion, complete a 'regular' rollover by transferring the assets IN-KIND to a Traditional IRA, thereby 'artificially recharacterizing' the (not-actually-a-)'conversion' before the end of the 60-day rollover window.

To reiterate, before attempting this strategy, be sure that you have a solid understanding of the once-per-year rollover rule, the same-property rule, and the 60-day rollover rule.

#4: Create A Game Plan For What Happens If The Emergency Reserve Runs Dry

Financial Planning 101 says to “create an emergency fund for a rainy day” that typically consists of at least 3-6 months’ worth of expenses in cash, or liquid cash alternatives. Right now, the U.S. is only about one month into the COVID-19 crisis (though the first known U.S. case of COVID-19 precedes that date by about an additional month) but there’s no telling how long it will take until either the virus ‘runs its course’ or an effective therapy or vaccine is found, allowing life to return to some semblance of normalcy.

While the pending emergency relief package expected to be passed by the U.S. Senate later today may blunt some of the typical effects, several analysts have projected the unemployment rate to rise to 30% or higher in the near future, which would be higher than peak unemployment during even the Great Depression (and more than three times the peak unemployment during the 2008 Financial Crisis/Great Recession). If that happens, there’s no telling how long it will take, particularly in hard-hit areas, for some people to get back to work and avoid living off of their savings.

Given this dynamic, advisors should consider helping clients to establish the next-in-line source of cash to use after the emergency reserve runs dry. Notably, although clients may still be months away from running low on emergency funds, it’s important to identify the next source of cash now, as it can provide both psychological benefits (e.g., peace of mind) for clients, as well as practical benefits as some options to consider may take weeks or longer to establish.

One logical place to turn once cash assets have been exhausted is taxable brokerage accounts. Using assets inside such accounts to fund living expenses has several advantages, including that it’s quick, simple, and, depending on the assets liquidated (as well as whether there are existing carry-forward losses to offset any gains), there may not be any tax consequences.

On the flip side, though, using taxable brokerage assets may require selling positions at depreciated values. Furthermore, long-held positions may still have a significant gain, even after the market pullback, resulting in capital gains tax being owed.

For those who lack other adequate options, but who wish to avoid liquidating taxable investments at substantially depressed values, a securities-based loan may be worth looking into. Such loans are offered by certain custodians, using the securities held within their accounts as collateral. Interest rates are generally significantly lower than the margin rates offered by the same institutions, while actually dollars available as a loan will vary based on the types of securities held within the account. Typically, however, if a loan is available, it will be for at least 50% of the market value of the securities within the account.

Of course, many individuals don’t have substantial savings in taxable accounts, because they have accumulated most of their non-emergency-fund savings in tax-favored accounts, such as IRAs, 401(k)s and other employer-sponsored retirement plans. For individuals with employer plans, one potential source of liquidity is to see if the plan offers a loan provision.

Meanwhile, IRA owners and participants in plans without loan features may wish to simply take a distribution of retirement assets. Distributions of pre-tax assets will still be taxable, but up to $100,000 should be available without a penalty, assuming the COVID-19 relief bill negotiated in the Senate is passed into law, as expected.

Still, for other clients, the best source of capital will be from what may be their single largest asset… their home. Notably, there are a variety of ways in which homeowners may be able to unlock some of the equity in their homes. For instance, spurred on by research, including that conducted by Wade Pfau, some planners have encouraged eligible clients to secure line-of-credit style reverse mortgages on their home to help mitigate sequence-of-return risk and to avoid selling assets during significant market drops (like this one!).

Those who have secured such mortgages should certainly consider beginning to draw on some of their available loan proceeds, potentially with the mindset of paying the loan down with proceeds of the sale of other investments once asset prices have rebounded.

For others who either don’t qualify for a reverse mortgage, or simply don’t want one, a home equity line of credit (HELOC) offers another potential option. However, given today’s low-interest-rate environment and the relatively strong housing market of the last decade, an even more attractive option may be to use a cash-out mortgage. While rates for such mortgages are generally higher than their non-cash-out conventional mortgage counterparts, they can give homeowners access to potentially large amounts of cash at a fixed rate for (typically) as long as 30 years (whereas most HELOCs are issued with variable interest rates).

#5: Consider Reducing And/Or Temporarily Eliminating Payments That Don’t Have To Be Made

Many individuals’ cashflows are impacted by the current COVID-19 crisis. Meanwhile, others may be fortunate enough to be relatively unaffected in this regard, yet the uncertain future of the economy and markets warrants caution, especially where defensive actions can be taken with little to no downside or additional cost.

To that end, advisors can help clients to understand the types of payments that can (or should) currently be considered for reduction. In particular:

- Federal Student Loan Payments. Last week, the Department of Education announced that the interest rate on all Federally-provided student loans will automatically drop to 0% for a period of at least 60 days (pending further guidance). Borrowers have also been given the right to suspend payments for at least two months (pending further guidance). Notably, the reduction in the interest rate is automatic, but the loan payments will only stop if a forbearance is requested (or, in some cases, automatically if the borrower is late on payments). Thus, individuals who wish to stop payments must generally take proactive measures to do so. Borrowers can call 1-800-4-FED-AID, or visit their loan servicers website to make the change.

- Mortgage Payments. In some states, such as New York, a mortgage ‘holiday’ may be available to clients who have seen disruptions in income due to the COVID-19 crisis. While the exact terms will vary between jurisdictions, the general idea of such a provision is to automatically allow impacted borrowers to defer payments without incurring additional costs and/or impacting their credit scores. In states where such relief is not available, mortgage companies may work with borrowers to defer certain payments without incurring late fees or other additional charges. Notably, for clients with mortgages, ongoing payments likely represent the single largest monthly expense so getting any relief in this area could make a substantial difference when cashflow has been impaired.

- Credit Card Payments. Perhaps somewhat surprisingly, many credit card companies have ‘stepped up to the plate’ and voluntarily offered cardholders varying degrees of relief during the COVID-19 crisis. The potential relief offered by some companies includes reduced or delayed monthly payments, reduced interest rates, and abated late and other fees. The available relief is rapidly changing, so clients should be encouraged to reach out to their individual credit card companies, or to visit applicable companies’ COVID-19 relief pages.

#6: Put Refunded 529 Plan Funds Back Into The 529 Plan Via Rollover

While the extent of the COVID-19 epidemic has led many institutions of higher learning to transition from live, in-person courses to online distance learning, some classes have simply been canceled, leading to the academic institution refunding all or a portion of previously paid amounts. In other situations, students may have chosen to temporarily leave school to the same effect, receiving tuition refunds.

Where tuition and/or other qualifying educational expenses that are now being refunded were paid with 529 plan funds, strong consideration should be given to replacing such funds into a 529 plan. As a result of a change made by the Protecting Americans from Tax Hikes (PATH) Act of 2015, and as further explained by the IRS in Notice 2018-58, individuals receiving such refunds can roll them back into the student’s 529 plan within 60 days of receipt. Refunds rolled back into a 529 plan do not count towards the plan’s contribution limit.

Absent the completion of such a rollover, the taxable portion of the refund would be includable in income, and potentially subject to penalties. And to make matters worse, although the IRS has stated that it intends to release regulations to simplify this calculation, no such regulations are available to date.

Thus, for the time being, it would appear as though the refunded amount would have to be treated as a proportionate amount of basis and earnings as the 529 plan distribution that was used to pay the expenses in the first place. Notably, this can get particularly complicated where multiple payments to a single institution, and for a single academic period, were made via multiple 529 plan distributions that spanned multiple calendar years (thus resulting in different basis-to-earnings ratios!).

Sound complicated? Then there’s an easy fix. Encourage clients to complete the 529 plan rollover within 60 days of receiving the refund, and you won’t have to worry about any of that!

#7: Use A Qualified Health Saving Account (HSA) Funding Distribution (QHFD) To Fund Health Saving Accounts

In general, it is best to try and reserve amounts in retirement accounts for their intended purpose… retirement. Sometimes, however, life gets in the way of even the best of intentions and plans. For some clients, that time may be now.

For those clients with cashflow problems who need to pay medical bills or can’t otherwise fund Health Saving Account (HSA),), one potential (partial) solution would be to use the little-known Qualified HSA Funding Distribution (QHFD). A QHFD is a once-in-a-lifetime (quite literally, as in an individual is only permitted to make one QHFD during their lifetime) option to move money directly from an IRA to an HSA. The amount that can be transferred is limited to the maximum HSA contribution that the individual is eligible to make during a given year.

For 2020 the maximum HSA contribution is $3,550 for individuals with self-only coverage and $7,100 for individuals with family coverage. Individuals 55 and older by the end of the year may contribute an additional $1,000 catch-up contribution.

For those who would otherwise be unable to make their 2020 HSA contributions, but who have available IRA dollars, there are two reasons why a QHFD should be strongly considered. First, if funds are tight enough that the HSA contribution can’t be made, it likely means that if what seems-to-be-inevitable medical costs arise, there won’t be a ‘good’ source of funds from which to pay them (and being HSA-eligible means an individual has a high-deductible health plan (HDHP), which means, at least initially, insurance will be no help either).

Certainly, a distribution from an IRA could be used to pay such an expense, but that distribution would be taxable, and potentially subject to a 10% penalty as well (note that the 10% exception for medical expenses only exempts expenses in excess of 7.5% of AGI for 2020). By contrast, making a QHFD first, and then taking a distribution from the HSA to pay the same expense would be both tax- and penalty-free.

Second, even for those who do not have imminent expenses, if there aren’t enough available funds to cover making a full HSA contribution, then the QHFD should be strongly considered. Notably, HSAs are generally higher on the hierarchy of tax-preferenced accounts for most individuals. Thus, if the choice is to have dollars in a Traditional IRA or to have the same dollars in an HSA account, it generally pays to have those dollars ‘live’ inside the HSA.

#8: Help Business Owners To Reduce Or Pause Employer Contributions To Retirement Plans

Many small businesses, and small business owners, have been particularly impacted by the current COVID-19 pandemic. Current lockdown and/or social distancing policies have resulted in business revenues dramatically being reduced, or in some cases, eliminated altogether. During these turbulent times, many business owners are doing everything to keep their businesses afloat and to hang on to as many employees for as long as possible.

In some cases, those goals may be advanced by eliminating and/or reducing normally required retirement plan contributions. Many small business owners, for example, have incorporated either nonelective or matching safe harbor provisions into their 401(k) plans to allow themselves (and other highly compensated individuals) to contribute the maximum amount of salary into the plan annually, without worrying about testing. While such contributions are generally not a ‘choice’ on the part of the owner, if the plan’s safe harbor notice includes language that allows the employer to reduce or eliminate the safe harbor (which is generally a good practice in times such as this), then the safe harbor contributions can be suspended or reduced. In addition, IRC Section 412(c)(2)(A) allows a company to suspend such contributions, even if such language was not included in the safe harbor notice, when the company is operating under an economic loss for the year (which clearly may be the case right now).

Advisors working with clients who would like to consider making such changes should be encouraged to speak with a TPA, as the plan will need to be amended. In addition, other procedural requirements must be fulfilled, such as providing notice to employees of the change (which can’t actually go into effect until at least 30 days after employees have received the notice) and giving employees an opportunity to change their own salary deferral elections.

It should be noted, though, that by making such a change, the plan is no longer operating using a safe harbor, and thus, would be subject to annual testing.

Employers using SIMPLE IRAs may also wish to revisit their employer contributions. However, changes to employer contributions to SIMPLE IRA plans cannot be adjusted mid-year. Rather, they can only be adjusted prospectively for future years.

Nevertheless, employers with SIMPLE IRA plans who are struggling now may wish to look forward to 2021 to ‘recover’ some of their losses by reduced SIMPLE IRA matching contributions. While employees’ contributions are generally required to be matched up to 3% of their salary, the 3% rate can be reduced to as low as 1% in up to two out of five years.

#9: Fix A Previously ‘Unfixable’ Asset Location Problem

While gross returns certainly matter, at the end of the day, what really counts for clients is after-tax returns. How much money did the client make that they can actually spend? Certainly, generating tax-efficient returns can be bolstered in any number of ways, such as maximizing tried-and-true strategies like tax-loss harvesting, or simply by using tax-efficient investments in the first place.

But another significant and often ignored way to generate additional tax alpha is by properly locating the ‘right’ assets in the ‘right’ type of account. For instance, if a client has Traditional IRA assets, Roth IRA assets, and assets in a taxable account, in which account are the bonds placed? Where does the stock go? REITs? And so on and so forth.

For example, as a general rule of thumb, it makes sense to have your highest long-term expected-return assets located inside a Roth account, where they can grow tax-free. But what if your client’s highest long-term expected return asset consists of growth stock, which they’ve historically been holding inside a taxable brokerage account? While it might make sense, in a vacuum, to have those assets located inside a Roth account, the cost of making a corrective change (i.e., the capital gains tax that would be owed when liquidating appreciated assets in the taxable account) may have been too big to make such a change worthwhile. Or, in other cases, simply too big for a client to stomach.

Thankfully(ish?), as a result of the recent market pullback, that may no longer be an obstacle. As such, advisors who have been contemplating repositioning clients’ assets and adjusting the asset location plan should review accounts as quickly as possible to determine if such a move is now a viable option.

It’s worth noting that we’ve had historical levels of volatility recently, with both huge swings to the downside, as well as huge swings to the upside. With that in mind, while almost unimaginable in more normal times, given the current market environment, the difference of a single day’s performance may literally dictate whether such changes make sense.

The window may be limited, and changes may need to be made fast to capitalize on the current environment. As such, advisors should both identify clients for whom they’d like to make such changes and, if such changes don’t make sense yet, identify the potential market levels where such analysis should be revisited (as they could come sooner than expected!).

#10: Revisit Clients’ Healthcare Proxies, Living Wills, And Advance Directives

Estate planning is often the last item to be checked off clients’ lists, as the thought of contemplating one’s demise is often too uncomfortable to deal with. In other situations, clients may not feel like they need an estate plan, because either they don’t feel they have ‘enough’ money, or because most or all of their assets will pass outside of probate.

Estate planning, of course, covers more than just the financial bases. A critical element of estate planning is the planning for what has traditionally been viewed as end-of-life care, making sure clients wishes regarding things like “Do you want to be kept alive through the use of artificial machines?” and “Do you wish to be an organ donor?” have been properly addressed.

For individuals who have not yet engaged in this sort of planning, the current COVID-19 crisis may be just the ‘kick in the pants’ they need to get moving. And while face-to-face meetings with an attorney may not currently be possible, most of the estate planning process (save for the actual signing and/or notarization of documents) can be addressed virtually or over the phone.

Even clients who have existing healthcare proxies, living wills, and advance directives may wish to reconsider some of the terms or language therein. For example, some clients may have named an individual who lives far away as a healthcare proxy because they assumed that if things got bad, that person would be there for them. Current travel restrictions may make that difficult, though, if not impossible; thus, it may be helpful to name an alternate person to fulfill that role, even if only as a back-up.

Other issues that advisors may wish to discuss with clients include the terms by which they would like to be kept alive. As most people are now aware, COVID-19 is a respiratory disease that attacks the lungs. And while most cases are (thankfully) not severe, those that require hospitalization often require the use of a ventilator in order to ensure that blood supply remains adequately oxygenated.

Notably, a ventilator is a means of artificial life support. It is a machine that is doing the work of the lungs. Accordingly, if a client’s living will or healthcare directive provides that they do not wish to be kept alive via artificial means, this would potentially include the use of a ventilator… even if recovery is still possible, or even likely. Given the COVID-19 crisis, and the increased likelihood that such a measure may ultimately be needed, advisors should encourage clients with existing directives to review them to ensure they accurately reflect their wishes.

For example, should the directive say that “No means of artificial life support should be used”, or should it read more along the lines of “No means of artificial life support should be used once doctors have determined that a return of normal brain function is unlikely”?

Finally, once clients are satisfied that their legal documents read as desired and reflect their current wishes, advisors can assist by storing copies of the documents for clients, and by helping to facilitate discussions about what they want with clients’ healthcare agents and/or other persons relevant to their planning.

With any luck, the COVID-19 virus will peter out on its own, or the combination of science and social distancing will allow us to arrive at the same result. It’s all but certain that we will get through this crisis. What is less certain, however, is when.

In the meantime, advisors can continue to do what they do best. Help clients keep things in perspective. Encourage clients to avoid making emotionally driven decisions. Use the current situation to your advantage as best as possible.

In short… control what you can control. The rest usually falls into place.

Thank you for a thorough and informative article. While I’m pretty sure it is wishful thinking, does the IRS by any chance keep a tally of the QHFD? If clients — or myself for that matter — can say with reasonable confidence that they have not applied the QHFD option in the past few years but are not certain that they have _never_ made a QHFD contribution to their HSA, does there happen to be a reasonably convenient way to verify that the QHFD is still available? Clients may switch their accountant (CPA) or tax software over the years. Or does the confirmation essentially involve reviewing every single income tax return (since first opening an HSA)?

Can the QHFD be done in addition to a yearly contribution? Or is it simply to replace it? This is not limited to this year, but open in any year? Thanks and very helpful tips.

The QHFD would simply replace all or a portion of the annual contribution limit. It’s usually not a ‘big deal’ from a planning perspective, which is why so many people have never even heard of it. But during times like this, it can prove a valuable little tool 🙂

What drives the need to see if they are still on track while we’re in the middle of the fire? Reviewing the article from 10/1/14 (Understanding Sequence of Returns Risk … Bear Market Crashes…) a quick bear market has limited impact on long-term results. It seems too early to re-run a plan right now and suggest a spending cut.

#5 is now even more applicable since federal student loan payments (assuming they are not FFEL loans) and their corresponding interest are completely suspended for 6 months! And, those 6 months still count towards loan forgiveness options that the individual may be on.

If you need any kind of Loan, financial advice/ Monetary empowerment, kindly contact us now via Email: [email protected]

We can help you finance/loan (project funding) your business dreams through Commercial Lending for Asset Based Lending, Equipment Leasing, Commercial Real Estate Loans, Business Loans, Import & Export Finance, Capital Goods Financing & Leasing, Finance for import duties, Project Loans, Working Capital, Debt Consolidation.

Mr. Apna M B +918099362729

https://www.mbfinanceservice.com

E-mail: [email protected]