Executive Summary

Financial advisors who work with couples (or families) may generally find that their clients often require a special set of communication skills not just to avoid moments of alienation but also to help the couple or family experience a sense of unity as they consider their financial goals. Yet, given the current state of evolving financial planning curricula, these communication skills are not generally included in training provided to financial planners. While advisors may be taught technical skills such as helping clients set savings and retirement goals and creating tax and investment strategies for those clients, they aren't taught how to get two (or more) different individuals in a relationship or family unit to agree on those goals and to successfully execute them together.

Fortunately, there are resources for advisors to learn, develop, and hone relationship and financial therapy skills that can help them communicate effectively with their clients. For instance, researchers James Grubman and Dennis Jaffe created a hypothetical curriculum for individual financial advisors and financial planning firms to use that helps them to identify the most relevant and useful communication skills for their practices and also to design and implement strategies to use with their client couples and families. Additionally, a variety of case studies can be used by advisors to think through the communication needs of their clients, especially when helping them work through financial goals that elicit sensitive and emotional relationship challenges.

Ultimately, the key point is that working with client couples and families presents unique challenges that often require special communication skills to be solved effectively. And while most traditional financial planning curricula do not address financial therapy or relationship skills to prepare advisors to face these challenges, there are resources available for advisors to identify, develop, and practice the skills needed to work proficiently with these clients. Honing the communication skills to address the needs of client couples and families can improve not just the dynamics and flow of client meetings but also the relationship between the advisor and clients, as well!

Working With Clients Who Are Couples As Couples – Instead Of Only As Separate Individuals – Has Unique Challenges

When an advisor works with married clients or partners, helping them to formulate financial goals is not the only objective; many clients also need help finding a way to walk the chosen path to achieve those goals together – including a strategy that works for both of them. And this is no small feat, especially when each may have different (and even conflicting) priorities and motivation levels for the other's priorities.

Further, because very few of us actually take the time to think about how we feel, what we have learned, and what we aspire to do when it comes to spending our money, we tend to lack a good understanding of the deeper role that money plays in our lives. Although this is a very normal and common phenomenon, it does tend to make the financial advisor's job more difficult (although perhaps much more interesting!), as the challenge of helping client couples with their finances is compounded when the individuals themselves never fully identify (let alone articulate!) their future financial goals.

Nerd Note:

The fact that many humans tend to have a hard time thinking about the future is not because we lack intelligence or rationality. Our brains are simply better programmed to think about the immediate here and now, in contrast to more abstract concepts such as aspirations and emotions. Moreover, the difficulty that humans have with connecting themselves to versions of their future selves is completely normal. Certainly, because of our inherent intelligence and creativity, we can get better at knowing ourselves, but not without taking the time and effort to engage with these questions, ideas, and beliefs.

Accordingly, when working with client couples, advisors will find that it is often very common that neither person has a full understanding of their own relationship with money, not to mention any knowledge of the other person's relationship with money. And this is often the case with partners and spouses.

Example 1: Cliff and Clara are happily married and are expecting their first baby. They currently live in a small apartment and will need more space once their baby arrives, so they have decided to look into buying a new home.

Clara grew up wealthy and never had to worry about money. Although she is not irresponsible with money, she has always had the freedom to turn to her family for help whenever she needed it. Clara has always been able to get what she wanted and has never been overly concerned about budgets.

On the other hand, her husband Cliff was raised by a single parent who sometimes struggled to make ends meet. While his family wasn't necessarily poor, Cliff has always worked from a budget, and he hates spending on what he considers 'frivolous' or 'excess' expenses. Debt makes him very nervous.

Cliff and Clara come to their financial advisor, Lola, to talk about their changing financial goals and next steps.

Their conversation goes a bit like this:

Lola: Congratulations! Yeah, baby! I am so pleased for both of you. New house, huh? Tell me, what sort of house are we thinking about?

Cliff: Hmmm…well….

[Clara jumps in and cuts Cliff off]

Clara: We are going to buy raw land and build a new home on it so that we have exactly what we want. I want a big, beautiful kitchen and a backyard with lots of mature trees. When I was a kid, we had acres of land; it was the best.

Cliff: Uh, well. I don't know about that.

Clara: You are no fun! Cliff is always worried about budgets. I am proud that he is good with money, but I really want to build my dream home. I have looked for homes on the market, and I just do not want those.

Cliff: It is not that I am trying to be no fun or that I don't want our dream home – I do. And I love your creativity for those things and how you help me think bigger. Yet, as you said, I just want a budget, and I want to stick to it. I forever hear about the woes of building – I mean, sheesh, have you seen the price of lumber lately!

[Lola, the advisor, interrupts and is very careful trying not to sound judgmental as she summarizes the situation]

Lola: If I may, a quick summary just to make sure I am on the same page with both of you. Clara, you are already picking out your kitchen, and your version of a budget is: find all the things you may want, add them up, and then be prepared and fine with simply spending more. Cliff, you want to spend too – enjoy the nice things that Clara picks out, but you want to know how much you will spend and put a stopgap on anything further.

[Cliff and Clara nod their heads in agreement]

Lola: Well then, I think we are in for some compromises.

In the above example, neither Cliff nor Clara is probably aware of how potentially difficult it will be to find a compromise based on what they each want and how their upbringings have shaped their personal views on money. Thankfully, Cliff and Clara do see value in each other's differences – Clara complimented Cliff on the fact that he is budget-oriented, and Cliff likes the fact that Clara is creative and dreams big. Yet, when push comes to shove, their house goals could potentially and quickly elicit heated arguments. And while Lola recognizes that compromise will be needed, she is not certain how much her clients' backgrounds will influence how they make decisions, not only individually but as a couple as well.

Additionally, while Lola, the advisor, was able to summarize the situation in a non-biased manner, she may not always be able to do that so easily. Lola herself was raised in a single-family household, and although she works with lots of clients with multi-million-dollar homes, she has always (silently) considered their lifestyles to be extravagant.

Accordingly, if Lola intends to help her clients compromise, she may need to recognize her own bias as a potential obstacle with how to best serve the client as a couple, respecting and speaking to their collective need to find a workable path to their goals, and without siding with one individual over the other. This takes very special communication skills that most people do not possess without being taught.

As illustrated in the example below, without yet recognizing the bias created by her own background, Lola continues the discussion as follows:

Example 2: Continuing the conversation in Example 1 between Lola and her clients, Cliff and Clara, who have different ideas about the future home they would like to buy…

Lola: Tell me, if you were to ballpark an estimate, how much do you think you would spend?

Cliff: No more than $450,000, maybe $500,000.

Clara: Uh, I am thinking of a budget quite a bit higher. I was thinking that closer to $750,000 sounds about right.

[Lola notes the wide gap between the two estimates and, even though she likes Clara, she thinks that Clara needs to be more realistic.]

Lola: Okay, so we are not exactly on the same page. Clara, tell me, why are you aiming for such a high budget?

[Clara feels a bit attacked, and that she is the odd person out in the conversation.]

Clara: Well, as I said…I have looked at lots of houses online. I know the neighborhood, the size of the house, and the details that I want. I know how much it will cost to build and to get close to what I am looking for.

Lola: I hear you that building is important to you and that you want the best. Yet, do you think there are ways you could cut back and get closer to $500,000?

Lola is not intentionally siding with Cliff and asking Clara to compromise; it is happening subconsciously. Because of her own family upbringing and personal views of what 'extravagant' housing looks like, she thinks that Clara's price range is a bit unrealistic. Unfortunately, though, Clara feels attacked and uncomfortable. The way Clara sees it, Lola has just taken sides with Cliff, and she can feel it. It does not feel good.

Lola has subconsciously focused on only the individuals within the couple, and in doing so, Lola has also inadvertently neglected the couple as a unit that the individuals themselves make up!

Client Couples Need To Be Heard As Individuals Yet Served As A Couple

In the last two examples, the advisor unintentionally sided with one spouse of a married client because of her own ingrained biases from her personal experience. The advisor didn't realize she was doing this, and she certainly didn't do it on purpose. As mentioned before, working with client couples takes special communication skills that are not easy to master.

Notably, even Marriage and Family Therapists (MFTs), who work with couples and larger families, are trained specifically to work with couples and groups. They are taught to understand the specialized nature of communicating with couples and the importance of learning those communication skills in the work that they do. While financial advisors are not taught these skills, learning how to use these skills is still critically important to their work with client couples (and larger families).

So what do Marriage and Family Therapists learn that advisors can benefit from, too?

To begin, advisors can do a bit of what Lola did, in Example 1 above, and make time to hear from both members of the couple. Again, Lola asked questions of the individual spouses and held space for them to answer, even though Clara did a lot of interrupting. Lola listened to both sides and even effectively repeated back the two somewhat opposing views that she heard.

Yet, where Lola erred, in Example 2, was when she started serving just Cliff, or conversely when she started questioning just Clara, instead of keeping with the same flow of soliciting information from both parties. Basically, as demonstrated in Example 2, if the advisor happens to befriend only one member of the couple (even though it might happen inadvertently) – the other member is left feeling alienated, and they may both end out moving away from the advisor's services. In other words, even if it does not happen immediately, Clara may get frustrated by being the only one ever asked to compromise and may decide to persuade Cliff to switch advisors, or she may simply outlive Cliff; in either case, Lola will lose her client.

Moreover, instead of selecting a single spouse or partner to focus on, an advisor can instead focus on serving the couple as a unit over the individual spouse or partners. This is important for two reasons. The first reason is to ensure that progress can be made by both people; if the advisor inadvertently fails to help clients create goals as a couple, fighting or disagreement amongst the couple may slow or even end progress. The second reason is to minimize distrust of the advisor and to prevent antagonistic behavior not just between the client themselves but also between the client and advisor.

Example 3: Continuing the conversation in Example 2, above, between Lola, the advisor, and Cliff and Clara, her client couple, where Lola has inadvertently taken Cliff's side over Clara's…

Clara [very annoyed]: Look, if this is just going to turn into a Clara-shaming party, I am out! Compromise means that both people should be working at something. And so far, I am the only one who is being asked to do anything – so do you mean "compromise", or do you mean "acquiesce"?

Cliff [calmly, but beginning to feel overwhelmed]: Hey, hey. Maybe Lola has a point. We are far apart, and I am willing to maybe set a budget at $550,000, but really. Come on, $750,000? That is just too much. I can't. I really feel like I am stretching already.

Clara [still very annoyed]: Oh, whatever, Cliff. You always feel that way. Lighten up. Whose team are you on anyway?

Neither Clara, nor Cliff, nor Lola will be walking out of this meeting today unscathed or with any forward momentum. Clara is angry at both Cliff and Lola and feels very defensive. Cliff is stressed and overwhelmed, not only by the money and the anxiety over incurring so much debt but also by the fact that his wife is now mad at him.

Lola has totally lost control of the meeting and has landed herself in hot water. Even if she does manage to eventually repair trust over time with Clara, this is not going to be forgotten anytime soon.

If Lola could go back in time, it would behoove her not just to serve the couple (over the individual spouses) but also to focus on remaining a neutral third party. This won't necessarily ensure that the members of the couple don't fight with each other, but it will at least keep Lola out of hot water (although it is not impossible that one or both members of the couple could become upset that you won't take their side). Regardless, neutrality is key.

Example 4: Lola, because she reads the Kitces blog, has immediately realized what has gone wrong in her conversation with Clara and Cliff in the previous examples. She can't necessarily go back in time and start again, but she can apologize and re-organize her approach.

Lola: I'm sorry. If I may interrupt…

[Cliff is looking for any help, and Clara simply gives Lola a death stare]

Lola: You are right Clara, I hear you when you say that what I was asking for was not a compromise. I assure you that was not my intention. Please forgive me. I am here to serve both you and Cliff and your life together as a couple. If you don't mind, let's have some tea and try again.

[Cliff, Clara, and Lola take a short walk and get tea. Lola knows, thanks to a previous Nerd's Eye View article, taking a walk can de-escalate a tense situation.]

Lola [back in the office]: Thank you both, Cliff and Clara. It is hard to find a compromise, and I think I can do a lot better facilitating some common ground. Over the next 30 minutes or so, I would like for our goal to be to create a list of things we agree on when it comes to the new home. Cliff, please tell me, what are five important factors you want in the house?

Cliff: I want to agree on a budget. I do want a nice kitchen…both indoors and outdoors. Clara's family has an outdoor kitchen, and I love going to their house for those BBQs. I want the same thing for us.

[Clara smiles.]

Cliff: That is three, hmm. I would like a man cave. And I would like for our master bedroom to have really nice, well-organized closets. I despise clutter.

Clara: I want nice closets, too! And I agree with having a nice indoor and outdoor kitchen. I want trees; that may sound silly, but we have had a city life for a while, and I want some green space. And I want a really nice master bath.

Lola: Great, so it seems we agree on closets and indoor and outdoor kitchens. And correct me if I'm wrong, but neither of you necessarily disagree with each other's other two points: the budget and man cave for Cliff and the trees and the master bath for Clara.

Cliff: No, I think Clara is on to something with the trees and the bath; that sounds nice.

Clara: Yeah, a man cave… or maybe a family movie area. And I am okay with a budget. I will agree that $750,000 is high. It is the high end of my budget. I don't need to spend that much. I just want to be able to talk through my options.

Lola: Great. As I said, part of my job is to listen to you individually and also to serve you as a unit. Cliff and Clara, tell me, do either of you have ideas for how to best start building out what will be our agreed-upon budget?

[Cliff and Clara look at each other, smile, and both start to answer]

The above example might be a bit romanticized, but it can happen like that; Cliff and Clara really care for each other, and both want to build a dream house. Lola has facilitated serving the couple, giving both individuals the opportunity to talk, share, agree (or disagree), and then still pushed for ways that help the couple – as a unit – win without favoring one member over the other.

Had Clara or Cliff disagreed – perhaps Clara hated the idea of a man cave or, because of Cliff's seasonal allergies, he rejects the idea of adding trees – the important thing would have been for Lola to remain neutral and avoid taking sides.

Lola can consider information from each individual and add it to the growing collection of ideas from which the couple will ultimately make a decision together, but she is not the one to decide which choices trump others. Instead, those decisions need to come from Cliff or Clara, and Lola can facilitate helping them make those decisions by asking open-ended questions and going deeper into the whys and motivations behind the client's choices.

As an example, Cliff shared a bit about why he liked the idea of the outdoor kitchen when he shared his fond memories of visiting Clara's parents' home and enjoying their backyard barbecue area. Clara also shared some of her deeper 'why' when she mentioned how she loved growing up with a lot of green space as a kid.

Clara and Cliff are actually sharing meaningful information, although they may be doing so inadvertently, through what feels like part of a simple conversation. Yet, if Lola is paying attention, she can pick up on the clues that reveal what is really important to each spouse and to both as a unit, repeat them back to the client, and get them – both individually and as a couple – to come to a deeper understanding of themselves and what they want their life will look like together.

How Advisors Can Develop Communication Skills That Work With Couple Clients (and Larger Client Units)

From the examples above, we can see that Lola, the advisor, is clearly a fast learner, and she was able to switch gears in the heat of the moment with her client couple. While it may be useful to develop these same skills, it can be a challenge to identify which skills to develop and how to practice them before getting in front of clients.

So how might an advisor practice these skills, and how would they generate ideas about handling communication with couples (or larger family groups) as a single client unit?

A Communication Skills Framework Can Help Advisors Identify How To Improve Communication With Couples And Larger Groups

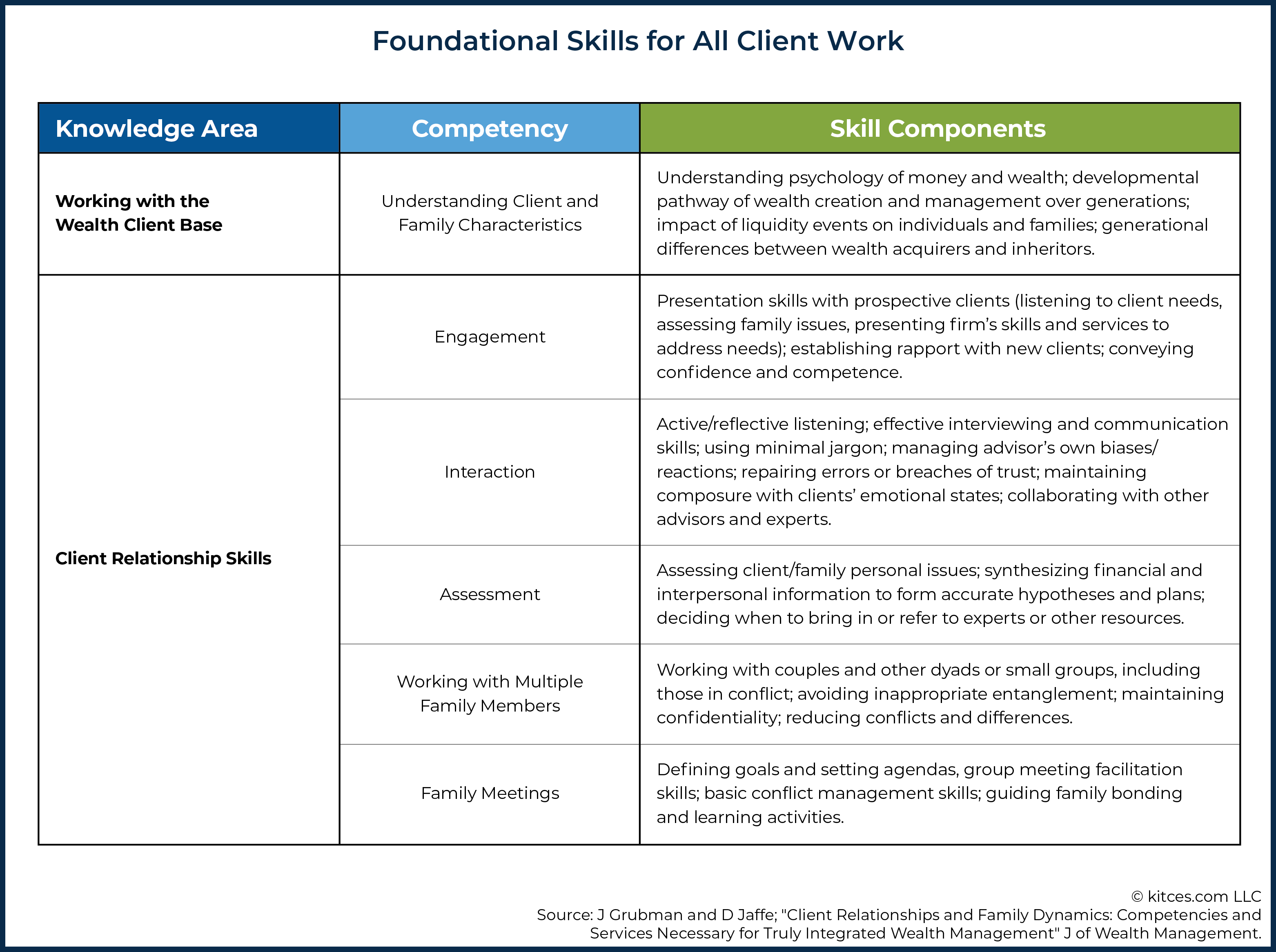

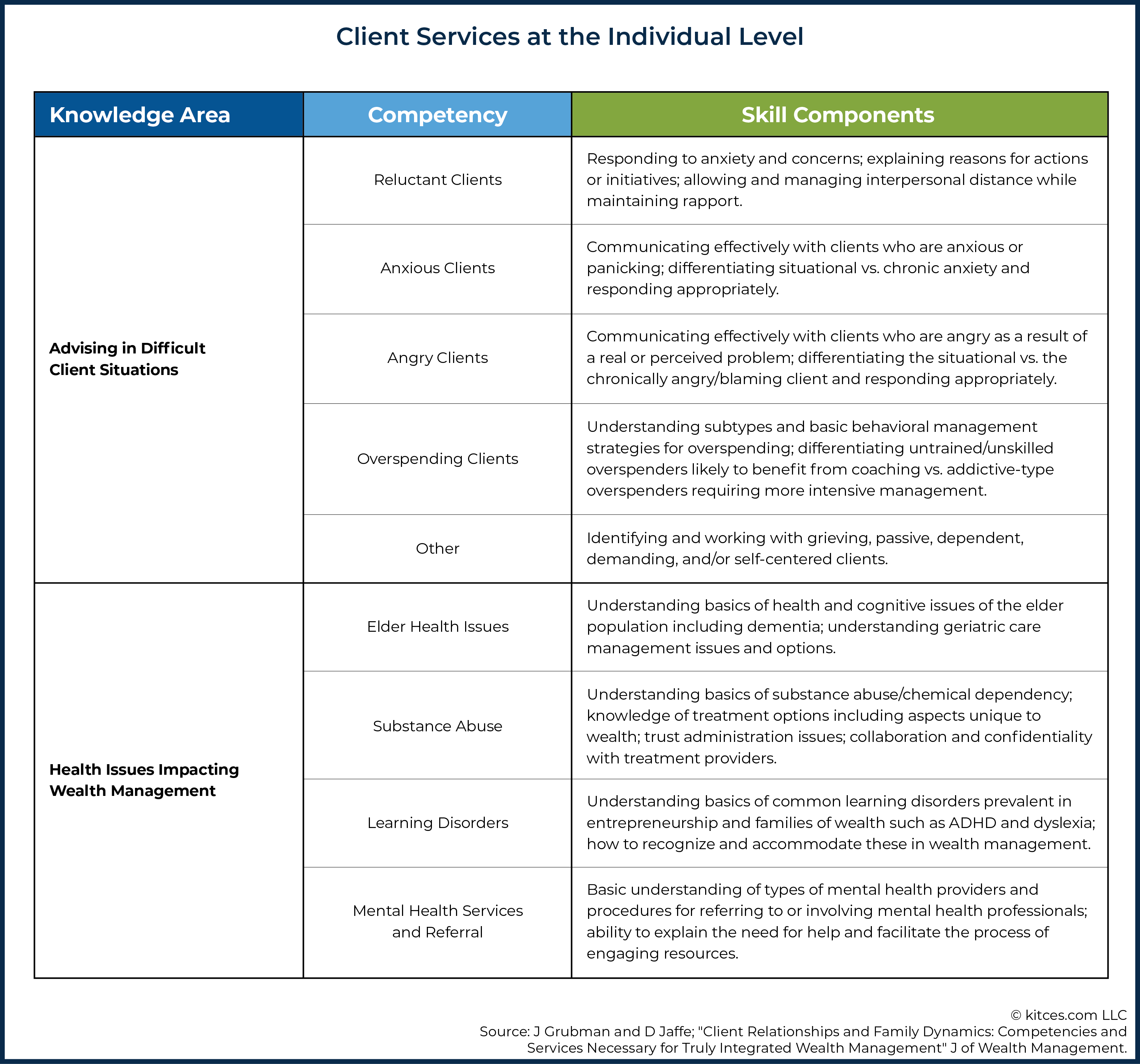

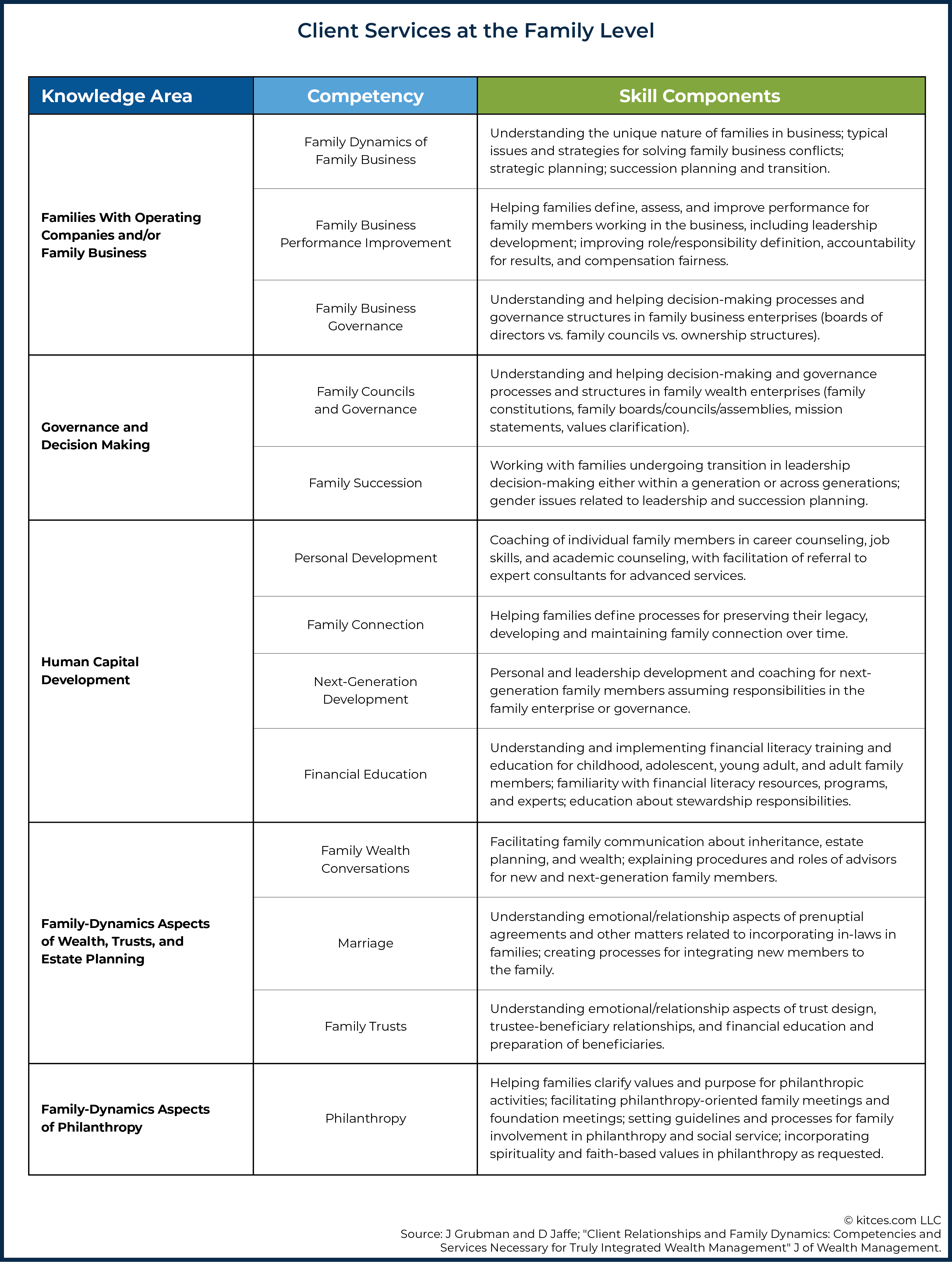

Psychologist James Grubman and Professor of Organizational Systems Dennis Jaffe, researchers who both specialize in wealth and family dynamics, have written about the skills needed to work with individuals, couples, and families. They created a sample curriculum that can help advisors understand how to delineate important communication skills that can be most useful with individuals and larger units.

The chart below breaks down these skills into specific Knowledge Areas that apply to all client work in general, as well as to topics relevant to working with individual clients and clients at the family level. Each of the Knowledge Areas includes Competencies that highlight important communication skills needed in each area and specific Skill Components for each Competency. The Skill Components for each Competency outline important considerations for situations or dynamics that can arise in their respective Knowledge Area (and that can provide valuable teaching opportunities).

Advisors can use this curriculum to identify specific Knowledge Areas or Competencies that are most relevant to them, their practice, and their clients. Then, by focusing attention on how the firm applies the outlined Skill Components, they can find areas that might need improvement, practice the skills that need honing, and even look for additional training if the resources are not immediately available in some form through the work environment.

For example, an advisor who works for a firm that does a lot of work involving intergenerational wealth might consider examining the Knowledge Area that examines "Client Relationship Skills" (in the Foundational Skills For All Client Work group) and focus on the Competency "Family Meetings" and "Working With Multiple Family Members". At the Family Level, they may decide to examine the Knowledge Area examining "Families With Operating Companies And/Or Family Businesses" because many of their clients are business owners.

Once specific Competencies are chosen, the advisor can then confirm whether they have mastered the specific Skill Components that relate to them and work on improving areas where they identify weaknesses. For instance, the advisor whose firm specializes in intergenerational wealth may recognize that while they excel at the Skill Components related to Family Dynamics of Family Business and Family Business Performance Improvement, they may not feel quite as strong in dealing with Family Business Governance. As a result, they decide to further research how different governance structures can benefit their particular clients.

The table can serve as a powerful tool for advisors to assess areas where they might need to improve and to create training resources for themselves. Working with a client that consists of more than one person tends to get more difficult and complex as more people are included. And because remembering how to use new skills in the heat of a client meeting can often be quite challenging, using tools to practice skills, role play, and even develop cheat sheets and sample agendas for how ideal meetings can go can make a huge difference – not only for the advisor's confidence but also in improving the dynamics and flow of the meeting with actual clients!

Case Studies As Tools To Practice And Improve Communicating With Multi-Person Clients

Developing and discussing case studies can provide a valuable opportunity for advisors to practice speaking to the individuals and the client couple or family. Case study ideas can be designed around relevant Skill Competencies in the sample curriculum presented above, or advisors can generate a list of existing couple and/or family goals they have seen in their office for more context and ideas.

The examples presented earlier, with Cliff and Clara, can be used as a potential case study as a starting point, but advisors might also consider other cases that involve couples who do not get along quite so well with one another.

For example:

Lydia and Thomas need help. While Thomas wants a new home, Lydia is content where they are in their current home.

The couple actively fights about the house, which they have been discussing for 4 years, and tension between the couple has really risen lately. Their children (a son and daughter) are both fully grown and live on their own. Thomas has little sentimental connection to the house, but Lydia still feels deeply tied to it.

Additionally, Lydia is fearful of taking on any housing debt at this stage in their life. She has never worked and is quite conservative about money and budgets. Thomas, on the other hand, earns all the money for the household and really wants to spend it how he sees fit.

Lydia feels bullied and controlled financially by Thomas. Thomas feels manipulated by Lydia and how she uses her emotional attachment to the house as a reason to stay.

How might an advisor help Lydia and Thomas to find common ground and discuss their issues and concerns?

Case studies like these can help advisors develop methods to use in sensitive client situations, such as how they might deal with clients when they are angry or how the firm chooses to work with client couples who split up and even divorce. Identifying when and how to incorporate a discussion around financial education and personal development, facilitating conversations that help clients respect each other's values, and finding the resources to help guide clients to conduct their own family meeting are all positive ways that advisors can strengthen their skills to work with client couples and families.

Below is another sample case study that can be used to examine a common area of disagreement, which focuses on when individuals in a marriage or partnership should retire:

Carla and Harold are married and are thinking about when they will retire. Carla is 63 years old and is a successful pediatrician with her own practice that she built from the ground up. Harold is 71 years old and is an architect.

They both love their jobs, but Harold also loves traveling. He wants to retire soon so they can spend time traveling before they are too old to be able to enjoy it, but Carla isn't ready to retire. She and Harold often fight about this topic.

It is not so much that Carla is opposed to the idea of retirement, but she has been a doctor her whole life and is having trouble imagining herself not being a doctor. It is who she is and how she defines herself, so for Carla, retirement would mean giving up her identity. Additionally, Carla worries about who will take care of her patients when she retires – she feels attached to the children she treats and isn't certain that other pediatricians would care for them as much as she does.

Harold, on the other hand, likes his job and has enjoyed his work for many years, but being an architect has never fully defined him. For instance, he is also a bass-fishing enthusiast, a woodcarver, and a whiskey aficionado. He has had many interests outside of work and can't wait to do more of those things.

Carla understandably has some deep anxiety about letting go of her work and feels that Harold just does not understand her. Harold feels like Carla does not want to spend time with him when she says she just can't retire, and it hurts. They both feel a rift has been created in their marriage because of these opposing views.

How would an advisor help Carla and Harold to reconcile their retirement goals and to communicate their deeper needs and fears to each other?

Advisors can use case studies to practice and role-play various responses, playing all the different characters. The fact that these scenarios represent very difficult situations does not suggest they are less likely to happen in real life. The more advisors can prepare to have conversations with clients experiencing serious challenges and to practice how to respond to such circumstances as a firm, the better off advisors – and clients! – will be.

For financial advisors who want deeper financial therapy training to work with client couples and their unique relationship needs, there are ample learning opportunities available. Several programs are designed for advisors to practice communicating not just with individuals but also with couples and larger groups. The Financial Therapy Association and Financial Psychology Institute offer training programs and continuing education courses around these topics, and the Accredited Financial Counselor (AFC) training programs also have modules that address serving couples and individuals.

It is very common for advisors to work with couples as clients and, depending on the firm, maybe even with entire families. And as more individuals are included in a meeting, the more difficult the job of the financial advisor becomes as structural relationships of the family unit become increasingly complex. While the tasks involved in attending to each individual in the couple or family are important, they must simultaneously be carried out while being mindful of the couple or family itself as a whole.

Accordingly, communicating with couples and families as a unit – instead of with the individuals within the unit – is not something that advisors normally receive training on, but that does not mean that it is unimportant or not useful. On the contrary, because training isn't formally offered, it's more important for advisors to continually work on improving their communication skills with couples to best serve their clients who are partnered or married.

Just as with all skills, practice makes perfect. Practicing with friends, children, and colleagues can be an easy way to get comfortable with these communication skills before actually meeting with a client. There are also lots of associations that offer training in this area, where advisors can get additional support.

Leave a Reply