Executive Summary

With the average age of a financial advisor over 50 and nearly 1/3rd of all financial advisors projected to retire in the next 10 years, there is a rapidly rising demand for next-generation talent to replace them. And the demand is only further amplified by the ongoing shift of the advisory industry from commission-based compensation to (recurring) AUM fees, which for the first time make it viable for advisory firms to hire a deep bench of Support and Service advisors to retain existing clients without any need to be responsible (or successful) at finding their own new clients.

Unfortunately, though, the past two decades of a rising movement of independent advisors amongst both the independent broker-dealer and independent RIA channels has drastically reduced incentives for firms to develop their own talent. Creating a prospective next-generation talent shortage at the exact moment it’s needed most.

And the rising talent shortage is increasingly evident in the latest industry benchmarking data of the 2018 InvestmentNews Compensation and Staffing study, which shows that advisory firms are being forced to hire Service advisors from outside the industry and poach Lead advisors from competing firms just to fulfill their talent needs, due to the lack of up-and-coming next-generation Support advisors. And the shortfall is especially evident amongst the largest independent advisory firms that are experiencing the fastest growth rates and are overwhelmingly seeking to hire Support and Service advisors to deepen their bench.

Fortunately, though, the model of gaining “professional leverage” by using support professionals to improve the efficiencies (and economics) of partners is well entrenched in most professional services firms, from doctors (that typically have several nurses per doctor), to accounting firms (that have as many as 10 employees per partner), and law firms (which sometimes have as many as 25 employees per partner). Which suggests that, as advisory firms continue to transition to recurring revenue advice models, there is still ample room for further hiring and talent development to occur, especially in a world where 76% of advisory firms still have more Lead advisors and Partners than Support and Service advisors to work with them. Nonetheless, the apparent rise of a talent shortage means that the advisory industry may witness substantial upward pressure on advisor compensation in the coming years until it can attract enough next-generation advisors to fulfill the demand!

Hiring And Promotion Trends In Financial Advisory Firms

Being an effective financial advisor requires a substantial amount of training, education, and experience in various skill domains, resulting in career paths that often have years or even a decade of “paying your dues” before either reaching a healthy level of advisor income as an independent, or a senior advisor position as an employee. Which means for advisory firms, even after finding great future advisor talent, it takes a long time to groom and develop it to be ready for Lead advisor responsibilities with clients.

However, the ongoing growth of the advisory industry, and especially the rise of the fee-based model at both broker-dealers and RIAs, is creating a rapidly growing demand for advisor talent. Because one of the most unique aspects of the fee-based model is that, once an advisory firm develops a substantial client base, it needs advisors who can service those clients, retaining their ongoing fee revenue while freeing up “room” for the founders/partners to go out and get more clients. As contrasted with the traditional commission-based model, where every year, the advisor wakes up with zero or near-zero revenue, which means the pressure is not on hiring advisors who can service clients, but those who can find new ones to do business with.

And in the latest InvestmentNews Compensation and Staffing Study for 2018, the data reveals that fee-based advisory firms are beginning to grow and compound so rapidly, that a shortage is emerging for support- and service-level advisor talent, especially amongst the largest advisory firms that are growing the fastest and hiring the most positions!

And in the latest InvestmentNews Compensation and Staffing Study for 2018, the data reveals that fee-based advisory firms are beginning to grow and compound so rapidly, that a shortage is emerging for support- and service-level advisor talent, especially amongst the largest advisory firms that are growing the fastest and hiring the most positions!

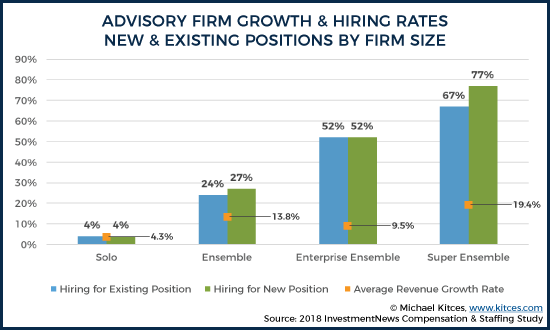

As the results reveal, the largest advisory firms – the “Super Ensembles” that have $10M or more in annual revenue – are growing the fastest and doing the most hiring, while Enterprise Ensembles ($5M to $10M in revenue) and Ensembles (multi-advisor with <$5M in revenue) are hiring substantially as well. The trend is especially pronounced when recognizing that the larger firms are not only enjoying higher growth rates but are also growing on a larger base of existing assets and revenue in the first place. After all, a $10M+ revenue firm that grows at 19.4% adds nearly $2M of new revenue, likely requiring the hiring of several advisors, while an average Enterprise Ensemble with $7.5M of revenue growing at 9.5% still adds nearly $700k of revenue (requiring another advisor hire every year), and an Ensemble firm averaging $3M of revenue and growing at 13.8% adds just over $400k of revenue and may hire an advisor every 18 months.

And in point of fact, the InvestmentNews data shows that a whopping 74% of Super Ensembles chose to hire a Support advisor in 2017, along with 58% of Enterprise Ensembles. Overall, 62% of advisory firms added a Support advisor in 2017, 43% added a Service advisor, 22% added a Lead Advisor, and nearly 8% added a partner.

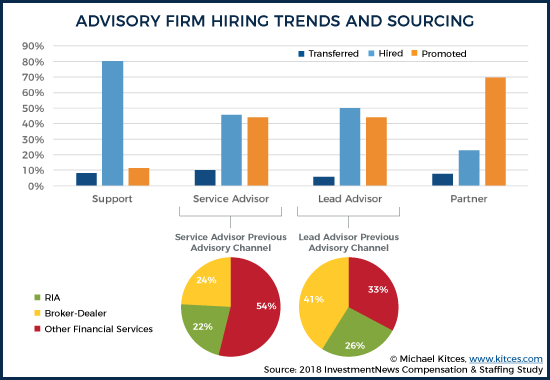

However, the sources of that talent varied greatly. Perhaps not surprisingly, most Support advisors were hired from externally as an “entry-level” job into financial planning. Though, notably, this suggests that few advisory firms have an effective career path to transition their Operations and Client Service team into Support advisors. Forcing them to hire from outside the firm to find talent.

By contrast, Service advisors were more likely to be transferred or promoted internally within the firm, as more advisory businesses have begun to develop and train Support advisors (to have people to promote) in recent years, rather than solely hire externally. However, amongst those that were hired, 27% were not simply recruited as experienced advisors from another firm but were hired from elsewhere in financial services, and another 27% were hired from outside the industry altogether! Which suggests that there is still a shortage of Support advisor talent in the aggregate, driving firms that haven’t already developed their own to seek alternative paths to get the more experienced talent they need!

Similarly, amongst Lead advisors, firms were even more driven to hire from outside their firm. However, since Lead advisors require substantial experience to be capable of both being fully responsible for client relationships, and often for at least some business development as well, advisory firms that hired Lead advisors were far more likely to do so by poaching advisors from other firms, including other RIAs, as well as independent broker-dealers, wirehouses, and elsewhere in the financial services industry. Suggesting that advisory firms haven’t hired enough Support and Service advisors in the past to have a sufficient pool of talent from which to hire and promote!

In fact, the only position where the majority of advisors were added from “in-house” developed talent was at the Partner level, where nearly 80% of the advisors who became partners did so as an internal promotion or transfer rather than being hired/recruited externally.

The Emerging Shortage Of (Real) Financial Planner Talent

The reason these trends of advisory firms looking outside their firms – or outside the industry altogether – to find advisor talent is that, demographically, the industry is still only on the front end of a multi-year generational transition that is looming. As data from Cerulli Associates suggests that the average age of a financial advisor is over 50 now, and just over 1/3rd of all advisors (about 110,000 in total) are expected to retire in the next 10 years and must be replaced.

Which suggests that when advisory firms already must hire the majority of their Lead advisor talent from other firms, and must seek the majority of their Service advisor hires from outside the traditional advisor channels altogether, the struggles to attract and retain next-generation advisor talent may soon go from bad to worse.

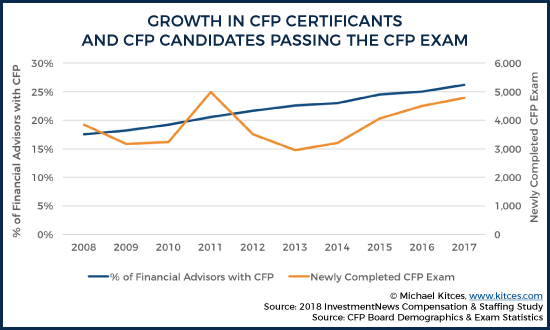

In fact, the InvestmentNews Staffing data shows that when promoting Lead advisors, they had a median of 11 years of experience and 65% of candidates had their CFP certification. By contrast, externally-hired Lead advisors had 15 years of experience (which as a result tend to be more expensive for the firm), and only 47% had their CFP certification. And given that overall, fewer than 30% of all financial advisors have CFP certification, firms may soon struggle even more to find financial-planning-centric talent (for which even the recent increases in the number of CFP exam takers may not be sufficient to meet the demand).

The shortage of experienced CFP talent is further accentuated by the fact that Super Ensembles that conduct the most hiring showed a whopping 28% of positions remaining unfilled at the end of the year, and that even amongst Service advisors being hired, the average years of experience has declined from 9 to 6 as firms must dig deeper to find any experienced talent at all!

Next-Generation Hiring, Talent Development, And Operational Leverage

The fact that the advisory industry is facing a shortage of next-generation talent isn’t entirely surprising. It’s a function of how the financial advisor channels themselves have evolved over the past 20 years.

In the early years of financial advisors, it was “standard” for large firms to hire and train their advisor talent, with a combination of sales training (in how to attract and retain clients) and product training (in the various solutions that advisors of the time would implement with their clients). While industry attrition was high – given the challenges of attracting and retaining clients, even with training – advisors who were successful with their firms tended to stick with those firms for the long run, providing a Return On Investment (ROI) to the firm for its training.

However, the rapid rise of the independent broker-dealer model in the 1990s and 2000s, alongside the rise of the independent RIA in the 2000s and 2010s, created substantial new alternatives for existing advisors to switch firms, after being trained, to obtain better payouts and total compensation by being recruited as an “experienced” advisor. The end result: as advisors became more independent and more prone to switching broker-dealer platforms or switching channels altogether (to becoming an independent RIA), many large financial services firms began to scale back the depth of their training programs and talent development, and instead focused more on simply hiring away the best-experienced talent to their platform. Or stated more simply, financial services firms didn’t want to spend their resources to train and develop advisors who would just be recruited away by the competition once they became more experienced anyway – especially since new advisors typically generate very little revenue while they’re still establishing their client base.

Yet as noted earlier, the shift from commissions to the fee-based AUM model is fundamentally beginning to change the math of advisor hiring and talent development. Because with a recurring revenue model, advisory firms that have an existing client base can hire Service and Support advisors to retain that client revenue at a lower cost than traditional advisors due to the lack of any business development responsibilities. Thus why, in the latest advisor salary benchmarking data, the typical Service advisor makes $94,000/year, but the average compensation of Lead advisors is $165,000 (for their additional business development responsibilities).

Which is important as a business, because it allows the advisory firm owners themselves to shift from merely being another well-compensated “Lead” advisor who profits from the work they do for their clients, to business owners that profit from the ongoing revenue clients pay in excess of what it costs for employee advisors to service them. And when the clients are the clients of the firm and given to the advisor to manage, they are more likely to remain with the firm even if the advisor decides to leave.

Yet as the InvestmentNews Staffing study notes, advisory firms are somewhat unique amongst professional services firms in that they typically have “only” 1 partner for every 2-3 advisors and other employees. By contrast, in accounting firms, it’s not uncommon to find a ratio of 1 partner for every 10 employees, and law firms sometimes have as many as 25 employees for each partner.

In fact, the benchmarking data suggests that only 24% of advisory firms have more Service and Support advisors than Lead Advisors and Partners (but when was the last time you saw a hospital where the doctors outnumbered the nurses!?). And even amongst the firms that do have such high professional leverage – at least relative to other advisory firms – they are still struggling to drive shareholder value from it, with no material difference in operating margins between those firms and the other 76% that have even less favorable ratios of Lead to Support advisors.

Nonetheless, the existence of substantial professional leverage in other professional services businesses suggests that, despite the next-generation talent shortage already beginning to emerge, advisory firms may still be in the very early stages of substantially deepening their bench of Support and Service level advisors, and that the struggle to attract and retain talent may only get worse from here. Of course, the caveat is that this approach to scaling a professional services firm – including an advisory firm – only works if the firm has a sustainable marketing and business development process to continue to get more new clients to be serviced by Support and Service advisors.

Yet given that the InvestmentNews Staffing study shows that the largest advisory firms are managing to scale their marketing and have the highest growth rates, with the average Super Ensemble added more than $2M of new revenue last year alone, suggests that in the coming years the largest independent advisory firms may become the primary competitors for next-generation talent. Although with a general shortage of talent in the industry, there may be many more years of rapidly-rising Support and Service advisor compensation… until the industry can attract more next-generation financial advisors in the first place!?

Yet given that the InvestmentNews Staffing study shows that the largest advisory firms are managing to scale their marketing and have the highest growth rates, with the average Super Ensemble added more than $2M of new revenue last year alone, suggests that in the coming years the largest independent advisory firms may become the primary competitors for next-generation talent. Although with a general shortage of talent in the industry, there may be many more years of rapidly-rising Support and Service advisor compensation… until the industry can attract more next-generation financial advisors in the first place!?

So what do you think? Has your firm felt the pinch of not being able to find enough talent to service existing clients? Are you looking to build your bench of Service and Support advisors? If so, where are they coming from? Let us know in the comments below.

I remember getting interviewed for a financial advisor job out of college. They deserve their shortage. “Oh you can make great money, but it’s all commission based and you start from scratch.” “oh well…how do i make money in the beginning?” “Well you build your client base. You might start at 20k or 30k a year for a while.” “Oh I”m not interested have a nice day.” “May I ask why” “Um…I’m not interested at the CHANCE of making 20k to start. I have bills now. Bye have a nice day.”