Executive Summary

For most workers, employer retirement plan limits are what they are, with a salary deferral cap of $18,500 (in 2018), and the opportunity for employers to add even more on top in the form of matching, profit-sharing, and similar contributions (up to an aggregate limit of $55,000 in 2018). The general rule typically boils down to “save as much as you can, and be certain to capture any matching contributions at a minimum.”

However, for a subset of workers, there is a possibility of being covered by two (or more) different defined contribution plans at the same time. Either for those who have an employee job with two different businesses (each of which provides a 401(k) or similar defined contribution plan). Or because they have a “side hustle” in the gig economy that allows them to create their own “employer” retirement plan as a self-employed individual. Which raises the question of how to coordinate between the two (or more) plans.

The first limitation on employer retirement plan contributions, under IRC Section 402(g), is the salary deferral limit of $18,500/year, plus a catch-up contribution of up to $6,000. This limit applies once per taxpayer across any/all plans they’re involved with (except for 457(b) plans, which are counted separately, and IRAs, which have their own standalone contribution limits).

The second limitation is known as the 415(c) overall limit, which is the (currently $55,000, plus any catch-up contributions) cap on the aggregate total of all contributions that go into the plan (including both salary deferral contributions by the employee, after-tax employee contributions, and any/all contributions from employers, from profit-sharing to matching contributions). However, unlike the 402(g) limit which applies once across all plans, the 415(c) overall limit applies separately for each plan.

The caveat to the overall limit, though, is that if the employers are “related” to each other (either as a parent-subsidiary or brother-sister controlled group, some combination thereof, or an affiliated service group), the overall limit (along with other employer retirement plan testing rules and requirements) is applied once across all plans as well.

Which means that while individuals who work two employee jobs at independent companies can receive contributions from each, and employees who have their own side hustle can still create their own self-employed retirement plan with its own overall limit, entrepreneurs who own multiple businesses must be cautious not to run afoul of the controlled group requirements that would require them to aggregate all their businesses together and not “double-dip” by trying to reach the overall limit across multiple retirement plans from each separate-but-not-really-separate business!

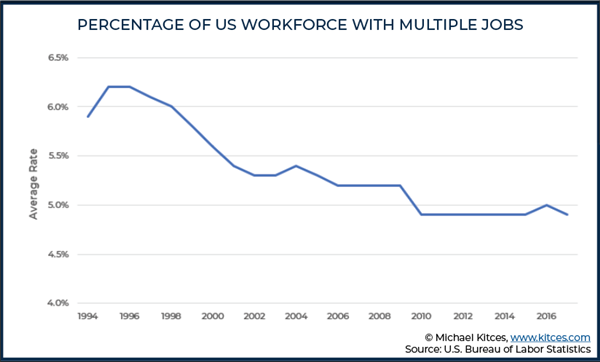

Last night, Alexandria Ocasio-Cortez was elected to represent New York’s 14 Congressional District in Congress. It was a history-making night for the young woman, who at just 29 years of age, is the youngest woman ever to be elected to Congress. Earlier this year, however, Ocasio-Cortes found herself in a bit of hot water after somewhat infamously stating during an interview on PBS’ “Firing Line” that, "Unemployment is low because everyone has two jobs.”

The statement, which went on to say, “Unemployment is low because people are working 60, 70, 80 hours a week and can barely feed their family," received Politifact’s dubious “Pants on Fire” rating, but it did raise the question… how many people do work two jobs? According to the U.S. Department of Labor’s Bureau of Labor Statistics, which keeps track of such things, the answer, at least for 2017, was roughly 5% of all workers, and it’s been declining for two decades.

However, there’s ample reason to suspect, and many believe, that the Bureau’s numbers might be off. For example, some people may work second jobs for which they are paid “under the table.” Others cite issues with the BLS’s methodology. And some even speculate that there are a substantial number of people who don’t even realize that they technically have two jobs… an idea that could have some merit, particularly as the “gig economy” continues to grow.

Nevertheless, even if we take the BLS’s statistics at face value, that still means that millions of workers have multiple jobs, and therefore, have the potential to contribute to multiple retirement plans on an ongoing basis. And that’s to say nothing of those workers who switch employers during the year and may have access to both plans at some point during the same calendar year! Or those who create their own “side hustle” job that effectively makes them a Schedule C self-employed individual on top of being an employee for another business as well.

With that in mind, it’s become increasingly important for advisors to understand the rules for situations in which a client can set up and/or contribute to more than one retirement plan at a time.

Breaking Down The “Basic” Defined Contribution Plan Contribution Limits

When it comes to retirement plans, there are two basic limits of which retirement savers must be aware; the salary (elective) deferral limit, sometimes referred to as the 402(g) limit, and the “overall limit,” or “annual additional limit," sometimes also referred to as the 415(c) limit, after the IRC code sections under which they can be found.

402(g) Elective Salary Deferral Limits

The limit on salary deferrals for most retirement plans that savers are familiar with, such as 401(k)s, 403(b)s, and the Thrift Savings Plan (that allow salary deferrals as part of the plan), have an annual salary deferral limit of $18,500 in 2018 ($19,000 for 2019). The annual salary deferral limit is a per taxpayer limit across all plans in which he/she participates.

Notably, though, 457(b) plans also have the same ($18,500 in 2018) dollar amount limit, as outlined under IRC Section 457(b)(2), but their salary deferral limit is counted separately from other plans.

In 2018 (and 2019), each of these plans also allows savers 50 or older by the end of the year to contribute an additional $6,000 as a “catch-up contribution.” Furthermore, these limits apply to both amounts deferred into the “traditional” side of such plans, as well as deferrals to designated Roth accounts (DRAs), such as a Roth 401(k), maintained by the same plan.

(Note: 403(b) and 457(b) plans may offer participants additional catch-up contribution opportunities.)

SIMPLE IRAs (and the almost-never-used SIMPLE 401k) also offer savers the ability to defer salary, but limit “regular” deferrals to $12,500 in 2018 ($13,000 for 2019). Similarly, these plans allow savers 50 or older by the end of 2018 (unchanged for 2019) to contribute an additional $3,000 as a catch-up contribution.

In addition, it’s notable that the annual IRA contribution limit (to traditional and Roth IRAs) is entirely separate from the salary deferral limits for employer retirement plans. Thus, an individual with a 401(k) plan can contribute $5,500 (for 2018) to an IRA plus $18,500 to a 401(k) plan (in addition to any catch-up contributions to each), though the traditional IRA contribution may not be deductible.

415(c) Overall Defined Contribution Plan Limit

The second limit, commonly known as the “overall limit,” which applies to 401(k)s, 403(b)s, SEP IRAs, and Thrift Savings Plans participants, is $55,000 for 2018 ($56,000 in 2019).

The overall 415(c) limit is a cap on all contributions made to a single plan on behalf of a participant for a given year (and thus is applied on a plan-by-plan basis). Such amounts include salary deferrals (as discussed above), as well as all employer contributions, such as matching contributions, non-elective contributions, and profit-sharing contributions. The overall limit also includes any after-tax contributions made to a plan by a participant during the year (e.g., as part of a “mega-backdoor Roth” contribution).

(Note: SIMPLE plans [both SIMPLE IRAs and SIMPLE 401(k)s] are not impacted by the overall limit. The annual limit on total SIMPLE plans is a function of the employee’s salary deferral, plus the required employer matching/non-elective contribution).

In the event that an employee is 50 or older by the end of the year and takes advantage of the opportunity to make a catch-up contribution, the overall 415(c) limit is increased by the amount of the catch-up contribution (from $55,000 to $61,000 in 2018, or $56,000 + $6,000 = $62,000 in 2019). Notably, though, merely being 50 or older by the end of the year does not by itself increase the overall limit; the actual catch-up contribution must be made to count towards the higher limit.

Example #1: Elizabeth is 55 years old and defers $20,500 into her 401(k) plan in 2018. Thus, she has made a catch-up contribution of $2,000 (as the “regular” salary deferral limit is $18,500, the excess $2,000 to reach a $20,500 total deferral is a catch-up contribution). As a result, Elizabeth’s overall limit for contributions made to that 401(k) for 2018 are $57,000 ($55,000 “regular” 401(k) limit + $2,000 catch-up contribution = $57,000). Which means Elizabeth could receive another $57,000 - $20,500 = $36,500 in various employer contributions (e.g., matching and profit-sharing contributions).

Example #2: Price is 58 years old and defers $10,000 into his 401(k) during 2018. Thus, he has not made any catch-up contribution (as his total deferrals do not exceed $18,500), and his overall limit remains at $55,000, allowing for up to another $45,000 in employer contributions.

Coordinating The 402(g) Salary Deferral Limits When Participating In Multiple Employer-Sponsored Plans

As noted earlier, the 402(g) salary deferral limit is a per-taxpayer limit, which means it applies once in the aggregate to an individual across all their employer retirement plans.

Thus, regardless of how many plans in which a client participates, they can only defer a maximum of $18,500 in 2018 ($19,000 in 2019), or $24,500 if they are 50 or older by the end of the year ($25,000 in 2019). This coordination applies when a client has access to multiple 401(k)s, multiple 403(b)s, multiple Thrift Savings Plans, multiple SIMPLE IRAs, or any combination of these plans. Which means in essence, when a retirement saver has access to more than one retirement plan, they must coordinate their salary deferral limit across/between the various plans.

Again, though, 457(b) plans are not included in this list of coordinated plans. Thus, clients who have access to both a plan on this list and a 457(b) plan, are eligible to defer up to $18,500 in 2018 ($19,000 in 2019) into each plan, or $24,500 into each plan in 2018 if they are 50 or older by the end of the year ($25,000 in 2019).

Coordinating The 415(c) Overall Limit When Participating in Multiple Employer-Sponsored Plans

Coordinating 402(g) salary deferral limits between multiple employer-sponsored retirement plans is fairly easy. Coordinating the overall 415(c) limit between multiple plans, on the other hand, can get a bit more complicated. That’s because there’s an additional level of analysis that must be performed.

When evaluating how the overall limit applies to multiple employer plans, it’s first necessary to determine if there is a relationship between the employers offering the plans that would cause them to be considered part of a “controlled group” or a member of an “affiliated service group,” as discussed in further depth below. For simplicity, we will continue to refer to the combination of these groups as “related employers.”

When a saver participates in multiple plans sponsored by related employers, the plans are treated as a single plan for contribution purposes (and also for any other rules/requirements, including vesting, non-discrimination, ACP/ADP testing, and top-heavy rules). Thus, if someone is an employee of two related employers, each of whom offers a 401(k), the maximum amount that can be contributed to both plans, combined, between employer and employee contributions, would be $55,000 for 2018.

If two plans are offered by unrelated employers, then the overall 415(c) limit applies separately to each plan. Thus, for example, if a young (under 50) saver works for two separate employers in 2018, and both employers offer a 401(k) that include employer contributions, they can theoretically receive a total of $110,000 between the two plans, so long as the total salary deferred to both plans, combined, is no more than $18,500.

Notably, while the overall limit is applied separately to each plan sponsored by an unrelated employer, the still-combined salary deferral limit between those plans effectively means that in order to “max-out” multiple retirement plans, it takes a substantial amount of employer contributions. As with a single plan, it takes “just” $55,000 - $18,500 = $36,500 of employer contributions to reach the maximum limit, but with two plans it takes $110,000 - $18,500 = $91,500 of employer contributions to reach the two-plan limit. Thus, it is often easiest to take true advantage of (i.e., to max out) multiple retirement plans when a client controls one of the unrelated businesses and can establish (and fully fund) a plan for themselves in the manner that is most efficient (on top of what the other unrelated business provides).

Identifying Related Employer Controlled Groups For Contribution Plan Limits

IRC Section 1563 defines three types of controlled groups; parent-subsidiary controlled groups, brother-sister controlled groups, and combination controlled groups.

Generally speaking, these types of related employers are “easy” to spot because they have definitions that are largely rules-based.

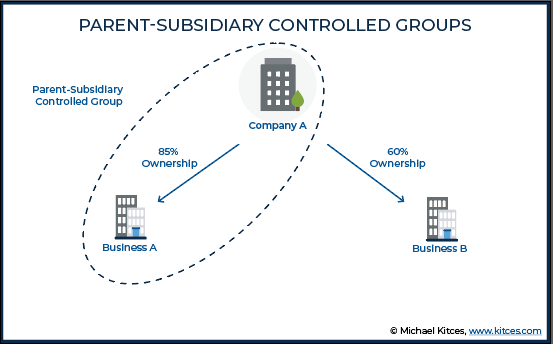

Parent-Subsidiary Controlled Groups

Parent-subsidiary controlled groups, as described in IRC Section 1563(a)(1), and further explained in Treasury Regulation 1.414(c)-2(b), are generally defined as scenarios where a parent company owns 80% or more of a subsidiary company. In the event that one or more of the subsidiaries of the parent also has a controlling (80+%) interest in a company, that downstream company would be considered part of the controlled group as well.

Brother-Sister Controlled Groups

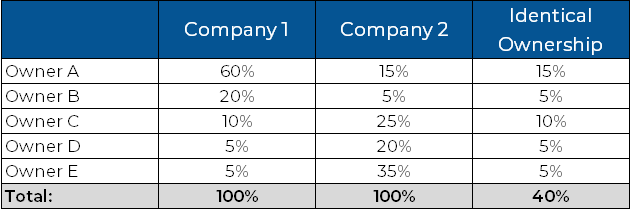

Brother-sister controlled groups, as described in IRC Section 1563(a)(2), and further explained in Treasury Regulation 1.414(c)-2(c)(1), are generally defined as scenarios where five or fewer persons who are individuals, trusts and/or estates have a collective controlling interest (80+%) in more than one entity and where those five or fewer owners also have “effective control” over the companies. “Effective control” is defined as having more than 50% total identical ownership between the companies in which the group has a controlling interest.

Example #3: Consider the following scenario, in which four persons collectively have a controlling interest in two companies:

Note that the total identical ownership – the total percentage of ownership that each person has in both companies – is “only” 40% across the two companies. Thus, even though the four owners collectively own more than 80% of both businesses, this is not a brother-sister controlled group before there is no more-than-50% “effective control” block, and the two companies would be treated as separate and unrelated employers.

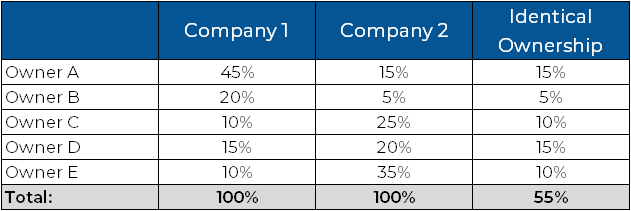

Example #4: In contrast to the prior example, suppose that a similar group of individuals has the following controlling interest in two companies:

Here, the total identical ownership between the two companies is 55%. Thus, the group of owners not only has a controlling interest in the company, but they also have effective control. As a result, this would constitute a brother-sister controlled group scenario, resulting in the two businesses being treated as a single employer for purposes of the overall 415(c) limit (and any other employer retirement plan testing rules).

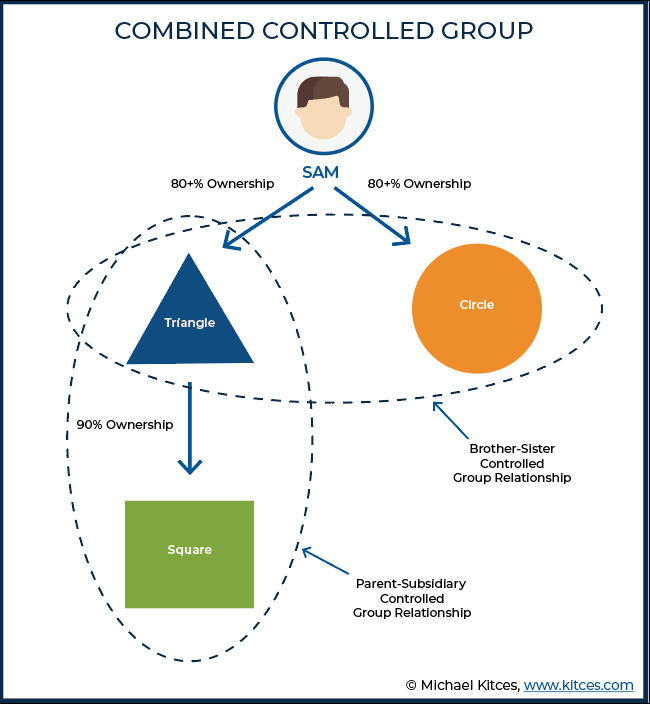

Combined Controlled Groups

Combined controlled groups, as described in IRC Section 1563(a)(3) and Treasury Regulation 1.414(c)-2(d), are scenarios in which each entity of the group is a member of either a parent-subsidiary or a brother-sister-controlled group, and at least one of the entities is the common parent of a parent-subsidiary group, and that same company is also a member of a brother-sister group.

For instance, consider the following chart of companies:

Here, Sam has a controlling interest (80+%) ownership in both Triangle and Circle. Further, Triangle owns 90% of Square. Thus, all three companies are part of the same combined controlled group, where Triangle and Circle are part of a brother-sister controlled group, and Square is also a part of the controlled group because it is a subsidiary of controlled-group-participant Triangle.

Affiliated Service Groups

In contrast to the relatively straightforward, mostly-rules-based factors that go into the determination of what constitutes a controlled group, the determination of what constitutes an affiliated service group, as outlined in IRC Section 414(m), and proposed regulation 1.414(m)-1, is often far more complex, owing to its more principals-based factors. No doubt, this complexity is part of the reason why the proposed regulations, which were initially promulgated back in 1983, still have yet to be finalized!

The need for these more complicated affiliated service group rules became apparent after a pair of Tax Court decisions from the late 1970s. In both the 1978 decision in Kiddie v. Commissioner, and the decision in Garland v. Commissioner during the following year, the Tax Court ruled that even though there were some common ownership and related business activities between a number of entities, a controlled group did not exist because the rigid, rules-based control percentages had not been met. Even though on its face, the businesses seemed very “related” due to their in-depth affiliations with each other.

Congress, concerned that businesses would be able to exploit these court decisions further by dividing their workforce between entities that work closely together weren’t a “controlled group” due to a carefully crafted ownership structure, created the initial affiliated service groups rules of IRC Section 414(m) in 1980. While a complete discussion of the affiliated service group rules is beyond the scope of this article (you can read much more about them here, if you’re so inclined), the basic “gist” of the rules is to treat multiple entities that are essentially running one or more businesses together, as a single entity.

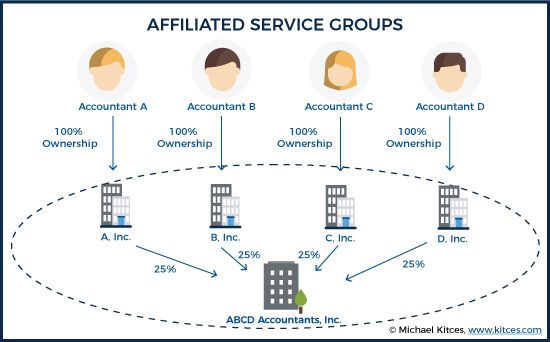

Example #5: To see how the affiliated service group rules might collapse multiple entities into a single employer for retirement plan purposes, consider the following:

Note that accountants A through D each own 100% of Accountant A, Inc. through Accountant D, Inc., respectively. Furthermore, note that each corporation only owns 25% of the total interest of ABCD Accountants, Inc. Thus, there is no parent-subsidiary control group, and no brother-sister control group.

Now suppose that ABCD Accountants, Inc., employs clerical staff, staff accountants, etc., and that it also does all the billing for accounting services provided. Then, after paying relevant expenses, ABCD Accountants, Inc. distributes profits to four separate corporations, each wholly-owned by one of the four principals of the firm.

Absent the affiliated service group rules, each of the middle-men corporations would be able to establish its own retirement plan, benefiting only its sole owner, while simultaneously excluding all of the employees of ABCD Accountants, Inc. In essence, the accountants would be able to create retirement plans for themselves, without any obligation to offer the plan for their downstream employees (who are firewalled off behind ABCD Accountants). Well, that wouldn’t be very fair, now would it?! And so with that in mind, the affiliated service group rules would collapse the five companies together so that employees of each company would be considered employees of a single employer, recognizing the actual substance of the arrangement.

Maximizing “Free Money” Employer Matching Contributions When Participating in Multiple Retirement Plans

It’s often said that, in life, nothing is free. That may be true, but employer matching contributions on salary deferrals for 401(k) and similar plans might be about as close as it gets. As such, it’s almost always a good idea to try and contribute as much salary as is necessary to secure an employer’s maximum matching contribution. (While this might seem obvious, research shows that roughly one-third of all plan participants still fail to take this simple step!)

Owing to the safe harbor rules, it’s common for many employers to match employee salary deferrals dollar-for-dollar on the first 3% of salary deferred, plus an additional 50% match on the next 2% of salary deferred. This is sometimes referred to as a “basic match.” In such situations, deferring 5% of one’s salary into such a plan results in an immediate 80% return on investment (receiving an instant 4% match on the 5% contribution)!

But what happens when two employers each offer a matching contribution? How should savers allocate their funds? Clearly, if a saver is able to contribute enough to both plans – taking into consideration both their budget and the coordinated salary deferral limits – to secure the maximum match from both employers, that’s the optimal path. Often, however, either due to budget constraints or the salary deferral limits, choices will have to be made that will impact the amount of employer matching contributions a saver can make.

Example #6: Heather is a 45-year-old emergency room physician who works for two different hospitals that each pay her a salary of $250,000 per year ($500,000 total).

Each hospital offers the “basic match” for 401(k) contributions (the safe harbor contribution of matching 100% of the first 3% of contributions, plus a 50% match on the next 2%). In order to get the maximum matching contribution from each employer, though, Heather must contribute $12,500 to each 401(k)… Except that Heather can’t do that! That would be a total of $25,000 in salary deferrals across the two plans, and the maximum Heather can defer into the two plans, combined, is $18,500.

Here, the optimal strategy is likely for Heather to contribute at least 3% of her salary to each of the plans. Since both plans will match those contributions dollar-for-dollar, those amounts are worth more than the next 2% deferred into either plan.

Thus, Heather should make sure to defer at least $7,500 (250,000 x 3% = $7,500) into each of the 401(k) plans ($15,000 total) in order to get a “full” $15,000 match. She could then defer an additional $3,500 to either plan – or a combination of the plans – in order to “fill up” her available 50%-matching salary deferrals to get the remaining $1,750 of matching contributions.

Maximizing Tax Benefits By Choosing The Right Company Retirement Plan for A Saver’s Own Business

As noted above, it’s often easiest to maximize the tax benefits of multiple retirement plans when one of those plans is the client’s “own” plan, either under a sole proprietorship (e.g., for a consulting business or other side hustle), or even as the owner of an outside business over which they exercise enough control so as to dictate the type of plan selected and the nature of its funding (beyond being an employee in another business as well).

Conveniently, due to the demands of working for more than one employer, many clients with two or more jobs have a “day job” and a “side gig.” It’s not entirely uncommon, however, to find clients with a “side gig” that is nearly as profitable as their “day job,” and in some cases, even more so! Which opens up the potential for substantial second-retirement-plan savings opportunities!

Example #7: Matt is a 45-year-old non-owner employee of Best Contractors, Inc. As an employee, he earns a salary of $231,250 and participates in the company’s 401(k) plan. In addition, Matt also has a side hustle as a residential architect on nights and weekends, and generates $100,000 of net profit via his sole proprietorship.

Here, Matt has two unrelated employers (as he owns 100% of his sole proprietorship but isn’t an owner of Best Contractors at all), and thus, in a best-case scenario, he can receive up to $110,000 of total contributions for 2018. The determination of what the best plan for Matt’s sole proprietorship will be largely driven by the nature of his Best Contractors plan. To illustrate this point, let’s consider two extremes.

First, let’s suppose that the Best Contractors 401(k) plan offers an employer match on up to 8% of salary. In such a circumstance, Matt would obviously want to get the maximum match, so he would defer $18,500 ($231,250 x 8% = $18,500). As such, there is no salary deferral room left for him in any plan he would create for his sole proprietorship. Thus, a SEP IRA, which is easy to set up and is all employer funded, would likely represent the best choice for Matt, and allow him to reduce his taxable income by another $18,587 ([$100,000 profit - $7,065 deduction for one-half of self-employment tax on the 92.35% of net earnings for self-employment purposes] x 20% = $18,587 max SEP contribution).

Suppose, however, that Matt’s employer does not offer any matching contributions to its 401(k), but does offer a 20% profit sharing contribution. As a result, Matt would receive a $46,250 ($231,250 x 20% = $46,250) profit-sharing contribution in 2018, leaving him only enough room in the plan to defer $8,750 ($55,000 - $46,250 = $8,750). Here, adopting a 401(k) as the retirement plan for Matt’s sole proprietorship might make the best choice, because in addition to allowing him to make a profit-sharing contribution of $18,587 (the same as a SEP IRA contribution), it would also allow him to defer an additional $9,750… the difference between the $8,750 he could defer into the Best Contractor 401(k) and the $18,500 limit for 2018.

Alternatively, Matt might not defer anything into his Best Contractor 401(k) – leaving just the annual profit sharing contribution there – and contribute an additional $37,087 to his solo-401(k), which would represent the maximum profit-sharing contribution to that plan, plus an additional $18,500 deferral amount. In either case, though, the combination of plans would allow Matt to receive up to $83,337 in contributions for 2018… far in excess of the $55,000 overall limit for a single plan (or multiple plans of related employers).

Ultimately, the key point is that salary deferral limits for individuals apply once across all plans, while employer contributions are limited on a per-plan basis… unless the plans themselves are related employers under the controlled group or affiliated service companies that aggregate that limit back into one as well.

Which means business owners that are involved in multiple businesses need to be cautious not to over-contribute to employer retirement plans by failing to consider them on an aggregated basis (as a controlled group). But those who are simply employees of multiple businesses can receive employer contributions to each… even though they’re only able to make salary deferrals up to one limit across all plans (and may need to coordinate to maximize their matching contributions). Fortunately, though, individuals who have their own “side business” (while being a non-owner or at least having a non-controlling interest in another business) do still have room to create their own separate retirement plan for their outside business to contribute to… and can choose proactively from SEP and (individual) 401(k) plan options to maximize their employer contributions and/or the remainder of any salary deferral limits as well!

Hey Jeff, thanks as always for this useful information to reference. I’m getting hung up on a very specific part of your Example #7 I’m hoping you can clarify. Since Matt and his employer already paid the full Social Security tax for the year with his $231,250 salary, can he then reduce his self employment tax owed?? ([$100,000 profit – $2,678 deduction for one-half of self-employment tax (Medicare only?!) on the 92.35% of net earnings for self-employment purposes] x 20% = $19,464

If a public employer has a 401 and 457 (employee voluntary deferrals only), do the 457 deferrals count against the 415(c) annual additions limit?

Hi Jeff, How might one correct for an individual who participated in two different employer plans and inadvertently made excess contributions in prior years? Can you use the IRS 5329 form, or does the employer/plan administrator have to be involved? Is there a statute of limitations?

can you contribute to two seperate 457 plans if sponsored by different employers?

Jeff, thanks for covering all this info. I’ve read other articles, but all seem silent on an overlapping issue. For someone under 50, is it possible for a self employed individual to contribute $61K (for 2022) to 401k/profit sharing and also make a non-deductible ira contribution of $6000?