Executive Summary

Since the merger of the IAFP and the ICFP over 14 years ago, the FPA has faced trying times. Amidst a backdrop of aging advisor demographics, a growing tide of retirees, and a declining total headcount of financial advisors, the FPA has never managed to grow materially beyond its peak membership on the day it was born, and since the 2008 recession was suffered from a 17% decline in membership and a 36% decline in revenue.

Yet the reality is that notwithstanding the difficult environment, the number of CFP certificants has nearly doubled since 2000, and the FPA’s failure to grow actually marks a drastic decline from having over 50% of all CFP certificants as members to under 25% of them, leading in turn to a significant loss in its power and standing as an organization. The FPA’s "mysterious" inability to grow despite the tremendous growth of its target market seems to stem from a battle between the legacy of the IAFP and ICFP that still rages on, with the FPA moving close enough to the ICFP’s "CFP-centric" worldview to alienate non-CFPs, yet not close enough to be a beacon of advocacy and success for CFP professionals either. The end result: while 10 years ago the FPA still had enough strength and momentum to sue the SEC and win in pursuit of its advocacy goals for financial planning, now the FPA’s power has waned to the point that it defers to the CFP Board on key issues to certificants and when the CFP Board launches a career center to compete with the FPA’s own Job Board the FPA congratulations the CFP Board for the competitive victory!

Ultimately, the FPA’s inability to honor its own bylaws and its founding Memorandum of Intent, and the organization's struggle to focus effectively to champion and advocate on behalf of CFP certificants – or even control their own advocacy efforts and messaging amongst the leadership and the chapters – raises the fundamental question of why it’s even necessary to have a standalone membership association separate from the CFP Board that grants the marks. Would CFP certificants be better served by going from paying two organizations to only one, and simply having the CFP Board function as both the credentialing body for CFP professionals and their membership organization as well, as is done in many other countries around the world?

Of course, longstanding CFP certificants have witnessed the CFP Board engage in many of its own blunders over the years, and an outside membership association for CFP certificants can be an effective (and even crucial) form of checks-and-balances against the CFP Board. Yet the FPA has increasingly failed to execute this key role, and the FPA’s ongoing loss in power has been the CFP Board’s gain. As the FPA becomes weaker, is the CFP Board becoming increasingly aggressive in trying to chip away at the FPA’s sources of members and revenue and professional impact, potentially accelerating the FPA’s demise? Will the FPA be able to step up and grow its “market share” of CFP certificants to regain its former power before it’s too late, or has the FPA already lost too much focus and momentum, and made itself too irrelevant for too many CFP certificants?

What Is The Membership Association For CFP Certificants?

If you ask the average CFP certificant “as a CFP professional, what is the membership association that represents you and advocates on your behalf” you’d be surprisingly hard pressed to find a clear and consistent answer.

Many might respond the CFP Board, though in point of fact the CFP Board is not actually a 501(c)(6) membership association, but a 501(c)(3) charitable organization whose mission and purpose is to benefit the public by granting the CFP marks and maintaining their standards; the CFP Board grants the CFP certification and is the owner of the associated trademark, but functions closer to a “regulator” of CFP certificants (as an overseer of the use of the CFP trademark) than a membership association representing them. In fact, given some of the CFP Board’s recent enforcement actions, arguably the whole point of having a membership association for CFP certificants would be to specifically represent the interests of CFP professionals against the CFP Board when its policies go awry!

If it’s not the CFP Board, the next logical answer for the membership association for CFP certificants might be the Financial Planning Association (FPA), which came forth from the merger in 2000 of the former International Association of Financial Planning (IAFP), and the Institute for Certified Financial Planners (ICFP), where the latter really was effectively the membership association for CFP certificants, and the former was a broader organization open to anyone who wished to do or support financial planning (regardless of designation). The merger was intended to bring some of the size and capabilities (and dollars) of the IAFP, to the profession-building focus of the ICFP, consolidating their power, dollars, and numbers to advocate on behalf of the profession, and also simplifying the number of membership organizations to which financial planners belonged. At the time of the merger, the FPA was nearly 30,000 members strong.

Yet over the past 14 years, despite a clear Memorandum of Intent created to facilitate the merger and endow the subsequent direction and vision of the organization, the FPA has failed stunningly to live into its role as the membership association for CFP certificants and those who support them.

The FPA’s Declining Market Share Of CFP Professionals (And Total Membership, Too)

Since the merger, the FPA’s total membership headcount declined, from a peak at the merger of almost 30,000, to only about 23,000 currently. On the one hand, this might be “forgiveable” given that the overall number of financial advisors has declined a little over 10% (as estimated by Cerulli) over that time period as well.

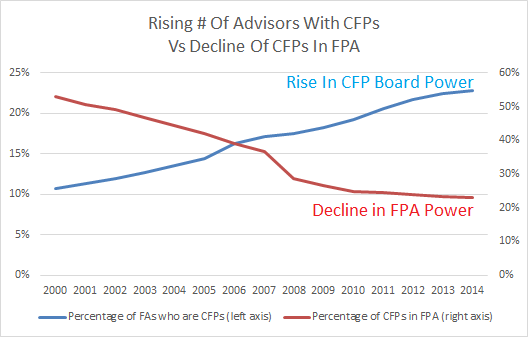

Yet this decline in the FPA’s membership count has also come during a time period where the number of CFP certificants has nearly doubled (from about 36,000 to over 70,000), and the percentage of financial advisors who have CFP certification has more-than-doubled (from about 11% to 23%, as the count of CFP certificants is up even as the total number of financial advisors has declined).

As a result of these shifts, the FPA’s estimated market share of the CFP certificants it purportedly represents, which should be its core membership, has plummeted from 50% to under 25%. As of now, it’s estimated that only about 17,500 of its 23,000 members have their CFP certification today (the rest being students, international members, affiliated professionals, and a small number of non-CFP financial advisors), out of a total of more than 70,000 CFP professionals.

By contrast, if the FPA had merely maintained its market-share-percentage of CFP certificants since the merger, and did no more than hitch its wagon to the CFP Board’s growth engine for the past 14 years, the association would/should be more than double its current size, with upwards of 50,000 members in total! To be merely flat in membership since 2000 would actually indicate a significant loss of market share, and the actual decline in membership since 2000 represents a dramatic step backwards in the power of the organization since the merger!

Where Did The FPA Go Wrong Since The IAFP & ICFP Merger?

So given what appeared to be a relatively clear focus for the FPA at the time of the merger, what happened?

In the early years, the FPA (and especially its board) maintained a strong ICFP focus, notably spinning off the old IAFP broker-dealer division into the newly spawned Financial Services Institute in 2003 so the FPA could focus ever more on financial planning issues. The FPA’s early momentum culminated in 2004 when it sued the SEC over the broker-dealer exemption for fee-based accounts (colloquially known as the “Merrill Lynch” rule), and industry articles at the time were declaring that the ICFP’s profession-building CFP-centric focus were winning the contest for the FPA’s soul.

The FPA’s lawsuit turned out to be a resounding victory, as the organization not only sued the SEC... it won the lawsuit 3 years later! In turn, this forced broker-dealers that wanted their advisors to get paid investment management fees while providing ongoing advice to actually become registered as investment advisers, preventing broker-dealers from charging fiduciary-like fees without any fiduciary duty, and spawning the explosive rise in hybrid B-D/RIAs over the past decade or so.

Yet in the midst of its incredible forward momentum in being the membership association for CFP certificants as a burgeoning profession, the FPA started to come under criticism. Some suggested that the board of directors was becoming too RIA- (and former ICFP-member) centric, and needed to be less ICFP-homogeneous. Others raised the question of whether the FPA’s CFP-centric focus was preventing its growth (as total membership had remained stagnant for several years, though arguably that was inevitable early on as the merged organization found its footing), and whether the FPA needed to do a better job drawing in non-CFPs and other various allied/affiliated professionals.

As a result, the composition of the FPA board of directors began to shift, the organization began to adopt a more IAFP-style “big tent” philosophy (anyone who values financial planning is welcome under the big tent, with less focus specifically on CFP certificants), with the unfortunate outcome that even as the FPA won the lawsuit with the SEC, the victory may have marked the zenith of FPA’s power (and its membership count), both of which have been waning ever since as its focus has wandered.

The problem with this “swinging of the pendulum” back towards the IAFP in the mid-2000s is that it left the FPA in a deadly “no-man’s land” for membership; the organization was too CFP-centric to attract non-CFP financial advisors who didn't feel welcome (which today are estimated at only about 5% of total membership), but backed too far away from its CFP-centric messaging to be a beacon for CFP certificants either who were often turned off by the low bar necessary to become a member (driving down CFP market share from over 50% to under 25%). The end result: by trying to adjust its membership requirements to the lowest common denominator, the FPA has simultaneously become less appealing for CFP certificants and non-CFPs as well, and thus membership has been in decline, despite the fact that it was intended to be the membership association for a base of CFP certificants that has doubled over the same time period (and while some have suggested that FPA’s fiduciary positioning may have also “cost” it some members, it’s difficult to see how given that the CFP Board adopted its own fiduciary standard in 2008 and has continued to grow throughout!)!

FPA Bylaws And A Return To CFP Centricity... In Name Only?

In a seeming acknowledgement of its problem – and how far the pendulum had swung in the wrong direction – the FPA “recommitted” in 2012 to its ICFP roots, and ICFP-founder P. Kemp Fain’s vision of “one profession, one designation”, as incoming CEO Lauren Schadle took the reins.

One the one hand, the fact that the FPA had to “recommit” to this vision at all is somewhat stunning, as part of the legacy of the merger Memorandum of Intent was the ICFP’s codification of the FPA’s CFP-centricity into the bylaws of the organization itself. Accordingly, Article II of the FPA’s bylaws state (and have since the merger):

Article II – Purposes

Section 2.1. The purposes of the Association shall be to serve the needs of its members and to establish the value of financial planning and the success of the financial planning profession. This Association is organized exclusively for one or more of the purposes as specified in Section 501(c)(6) of the Internal Revenue Code of 1986.

Section 2.1.1. The thrust of FPA’s message to the public will be that everyone needs objective advice to make smart financial decisions and that when seeking the advice of a financial planner, the planner should be a CFP licensee.

Section 2.1.2. The thrust of FPA’s message to the financial services industry will be that all those who support the financial planning process are valued equally as members in FPA and that anyone holding themselves out as a financial planner should seek the attainment of the CFP mark. FPA will commit to assisting financial planners who are interested in pursuing the CFP designation.

Section 2.1.3. FPA will proactively advocate the legislative, regulatory and other interests of financial planning and of CFP licensees. FPA will encourage input from all of its members in developing its advocacy agenda. It is the intent of FPA not to take a legislative or regulatory advocacy position that is in conflict with the interests of CFP licensees who hold themselves out to the public as financial planners.

Notably, this FPA focus – “that anyone holding themselves out as a financial planner should seek the attainment of the CFP mark” while also allowing as members anyone else who supports the financial planning process – was not only written into the bylaws, but would be almost impossible to change, as Section 17.1 of the bylaws states: “…any amendment or repeal of the Organization’s purposes, as outlined in Article II, shall require ratification through an affirmative vote of at least a majority of the individual members of the FPA…” In other words, to the extent that the FPA in the mid-2000s wanted to become less CFP-centric in its focus, it was operating in violation of its own bylaws by shifting its focus without securing a majority vote of the membership!

Yet despite the FPA’s recommitment to what its bylaws already said it was, and a partial rebranding of the FPA towards a “One FPA” theme (One Profession, One Designation), since Schadle’s announcement of the FPA’s renewed focus upon becoming CEO in 2012 (and a rather negative “blasting” response from American College CEO Larry Barton), the FPA has taken virtually no public positions and statements declaring itself to be the primary membership association for CFP certificants, and taken no significant public positions advocating on their behalf to the CFP Board. Their “CFP centric” return appears to be reflected on only its own website, and is far more difficult to observe in its deeds and public advocacy beyond what may be discussed internally at its home office and board meetings.

In fact, in its recent “Advocacy Day In Washington DC”, the FPA focused all of its efforts lobbying legislators on Capitol Hill, and embarrassingly forgot to include the DC-based CFP Board itself on the list of organizations to visit regarding advocacy in Washington, despite the ongoing challenges for CFP certificants regarding compensation disclosures! In other words, the FPA has declared that it is an advocacy organization on behalf of CFP certificants, but apparently saw no need to advocate the very organization that oversees their CFP marks (despite plenty of recent CFP Board challenges and issues to advocate about!)!

The FPA And The CFP Board – Checks And Balances

The fact that the FPA has not viewed the CFP Board as an organization to which it should lobby and advocate raises a crucial fundamental question about its very reason for being – after all, what’s the point of having two organizations, the FPA and the CFP Board, if it’s not so they can serve as a system of checks and balances against each other? Couldn’t the profession have more efficiency, and generate more political clout on behalf of the profession to legislators and (other) regulators – not to mention, being less expensive for CFP certificants who don’t have to pay two fees to two organizations – if the roles were simply merged into one?

For instance, in Australia, the “FPA” actually fulfills both roles (there is no separation of membership and credentialing), allowing the organization to advocate directly to regulators as both the credentialing organization and the membership association – a key lobbying role it has been playing over the past several years as Australian regulators have rolled out their “Future of Financial Advice” (FoFA) reforms.

For members of the financial planning community here in the US, the answer to the question “why not just merge the FPA and CFP Board into one organization” quickly comes back to the fact that the CFP Board has a long and unfortunate history of engaging in “blunders” from time to time, for which the FPA (and its predecessor organizations) can sometimes play a key advocacy role in getting the CFP Board back on the right track. Yet when the FPA refuses to take a public position on key issues to represent CFP certificants to the CFP Board, it raises the question of whether the FPA is simply making itself irrelevant and is becoming redundant as a membership association.

The FPA’s Waning Power As An Advocate For CFP Professionals

To some extent, it’s not entirely surprising that the FPA has been less willing to push the CFP Board on advocacy issues pertaining to CFP certificants – because it doesn’t actually have a lot of power to advocate with as the FPA’s own clout has been waning dramatically while its share of CFP certificants declines. If the FPA had kept pace with the growth in CFP certificants itself, and had 40,000-50,000 of them as members (and likely well over 50,000 total members at that point), it would be hard for the CFP Board to ignore. As the FPA has failed to take up the mantle for CFP certificants and its market share has fallen to fewer than 25% of CFP certificants as members, its role as a check-and-balance to the CFP Board is coming undone, and the balance of power is shifting to the CFP Board.

The rapid decline in FPA’s power has been astonishing, especially given the recent compensation issues of the CFP Board. While the FPA could have taken the situation as a renewed opportunity to reassert itself as being relevant in representing CFP certificants to the CFP Board and embolden its CFP advocacy brand – especially on behalf of its members working at broker-dealers who may have been slighted by the compensation disclosure debacle but are not comfortable confronting the CFP Board directly – yet instead the FPA deferred entirely to the CFP Board about when to have "the talk” about its recent compensation disclosure issues (and given that the CFP Board has insisted there is no problem to talk about, is tantamount to the FPA just looking the other away and ignoring the issue altogether). In other words, in the span of under 10 years the FPA has gone from successfully suing the SEC to defend the interests of fiduciary financial advisors and commanding significant political clout, to not even being willing to publicly call out the CFP Board on the blatant flaws in its compensation disclosure rules at all.

In the meantime, the FPA’s waning power seems to be not only external; it is also struggling to keep itself focused and on message internally as well. For instance, despite trying to work collaboratively with the Financial Planning Coalition, an FPA board member recently raised the question of whether financial planning should be state regulated (while a reasonable consideration, the Coalition has not publicly agreed to pursue such a course), and there are rumors that the FPA of Florida statewide organization is exploring whether it could actually implement some kind of state licensing for financial planners without necessarily advocating for the CFP marks that are central to the FPA’s mission. Though FPA chapters are technically separate and standalone legal entities from the national organization, the conflict highlights the fact that the FPA still hasn’t fully obtained the buy-in of even its own chapters to the organization’s CFP-centric focus and bylaws, even 14 years after the merger.

And the FPA’s inability to stay on-message and coordinated with the Financial Planning Coalition raises the question of why the CFP Board would want to engage the FPA in the Coalition at all, as there’s little purpose to having the FPA in the Coalition if it will not (or cannot) support the whole purpose of a “coalition” which is to maintain a unified advocacy front! The FPA’s uncoordinated role in the Coalition is especially problematic since the primary asset the FPA brings to the Coalition – its state chapter system and potential to help drive a grassroots effort for state regulation (should the Coalition actually decide to pursue state regulation in a concentrated and coordinated manner) – isn’t much of an asset if the FPA can’t steer and coordinate its own chapters in the first place! Yet the possibility that the FPA may be making itself more of a liability than an asset to the Coalition is a dangerous position, given that the FPA needs the Coalition for advocacy clout far more than the Coalition needs the FPA (as the CFP Board already has more dollars, greater numbers, and stronger connections given its Washington DC base); if the FPA undermines its own role in the Coalition, its advocacy power and relevance to the profession just wanes even further.

The Rising Power Of The CFP Board Is Further Undermining The FPA

Of course, what is a decline in the power of the FPA also represents a rise in the power of the CFP Board, a transition in the balance of power that the CFP Board seems intent to accelerate and capitalize upon to advance its own goals. As noted earlier, the shift in the profession’s balance of power has allowed the CFP Board to control the issues, including not only quieting FPA amidst the CFP Board's refusal to acknowledge a problem with its compensation disclosure rules, but forcing NAPFA to abdicate its own leadership of the “fee-only” definition and capitulate to the CFP Board’s position despite the fact that NAPFA originated the fee-only definition and movement!

However, over the past two years the CFP Board has gone beyond just trying to drive and control the issues, and appears to be proactively trying to undermine the FPA - a potential “silent war” assaulting the FPA’s role in the profession and even its financial viability. First there was the CFP Board’s attempt to begin to offer CFP CE credit, effectively going into competition with the FPA (and other CE providers), which could have damaged attendance at FPA (and NAPFA) conferences that are still a key revenue generator to fund the organization’s annual operating budget; the FPA fought hard and repelled the CFP Board’s attempt (along with NAPFA which was similarly threatened), but only after engaging with a fervor that seemed to signal that the FPA recognized that its own life was on the line.

Then earlier this spring, the FPA announced its partnership with the Academy of Financial Services (AFS), including the decision to co-host an academic track at the FPA BE conference and for FPA to co-publish their Financial Services Review journal; not to be outdone, the CFP Board co-opted the FPA’s announcement with AFS by declaring its own new initiatives just weeks before the FPA/AFS partnership became public, including announcing the CFP Board’s new academic financial planning journal to compete against the FPA’s Journal of Financial Planning (and the AFS’ Financial Services Review), and a new Center for Financial Planning to support academic research. The CFP Board’s announcement of the initiatives – which seemed premature given that they still haven’t been implemented more than 6 months later – was rumored to have come specifically to pre-empt the FPA announcement once the CFP Board had failed in its own attempt to partner with AFS.

More recently, the CFP Board struck against the FPA again, announcing the launch of a new career center in 2015 that would be a “one stop shop” for guides on how to “bridge the gap” from student to financial planner, job and internship listings, and other career management content, a rather direct dig at the FPA’s own Job Board and its now-defunct “Bridge The Gap” program which have not lived up to the task and could now be trumped entirely by the CFP Board’s new initiative (as the CFP Board appears to have far more capabilities to reach students with messaging about its career center as they enroll themselves for the CFP exam in the first place). This presents not only financial implications to the FPA – as their Job Board is a(n admittedly not huge) source of non-dues revenue for the organization – but also potentially cuts off the FPA’s lifeline to students as future members. After all, the biggest issue a graduating financial planning student faces is trying to find a first job and enter the profession, and if the CFP Board is perceived as the go-to source for that solution, the FPA is potentially written out of the student’s awareness altogether.

And the FPA’s battle-weary response to the CFP Board’s latest initiative? The FPA not only declined to fight the issue (now so weak that it has to choose which battles to fight and which it will just concede), but it embarrassingly applauded the CFP Board’s victorious effort at implicitly highlighting the FPA’s failures and making the FPA less relevant to new students in the future.

Will The FPA Survive The Next Recession?

Ultimately, the risk to the FPA is that if the CFP Board manages to chip away at enough of the FPA’s supports – from its pipeline to students, to its non-dues revenue channels with the Journal (which generates advertising revenue) and the Job Board (for which firms pay to have job listings), to its conference attendance and offering of CE credits – the FPA itself could financially topple.

As is, the FPA’s revenue is down 36% from 2008, and it has been forced to trim staff and services accordingly, despite the fact that the markets, economy, and financial advisors are all seeing record highs for income and growth. If the FPA is off 36% in revenues despite the economic recovery of the past 5 years (and down 17% in members despite the fact that the number of CFP certificants is up 20%), then what happens when the next recession comes along and things get really tight, and more advisors choose not to renew while prospective sponsors also cut back their advertising budgets? Can the organization survive another recession after failing to recover from the last one, when it’s now down to only $2M in net assets (on a $10.6M operating budget)?

Acknowledged or not, it seems that the FPA is in a fight for its very survival right now, and it’s a fight the FPA may not win. A loss of the FPA would leave a gaping void in the profession, as it’s simply not feasible to have a group of 70,000+ CFP professionals who do not have their own dedicated professional membership association.

Which, in point of fact, may be exactly what the CFP Board is waiting for – to either facilitate a takeover/assimilation of the FPA, or simply replace it with a new membership organization. While the CFP Board can’t literally be the membership association for CFP certificants – it is legally structured as a 501(c)(3) charity, not a 501(c)(6) membership association, which limits its ability to directly deploy its assets and income as a membership organization – it’s not difficult to imagine ways the CFP Board could still facilitate the process. For instance, while it’s not clear whether the organization could legally use its some of its own $23M war chest of net assets on its balance sheet (according to its 2012 Form 990) to fund a new membership organization spin-off, it might use its relationships to leverage sponsors that could “seed” a new replacement membership organization, and then establish a tight integration between the CFP Board and the new association to rapidly accelerate its growth (for instance, by doing marketing directly to its list of CFP certificants to encourage them to join the new organization). In fact, I would go so far as to say the CFP Board and its Board of Directors would be remiss if they haven’t at least been exploring potential paths to supporting/sponsoring/spawning their own membership association if the FPA takes itself out of the picture.

Of course, the reality is that the FPA has become weak enough that the CFP Board could potentially launch a competing membership organization now, and just further accelerate the decline of the FPA. But realistically, the CFP Board likely would prefer to see the FPA fold (or become desperate in a manner where the CFP Board controls the terms of a merger or wind-down), so that the CFP Board can try to take over the one unique asset the FPA has that the CFP Board wants – its state chapter system and capabilities to do grassroots lobbying at the state level for state regulation, should it be decided that’s the ultimate regulatory path to pursue to advance the financial planning profession (with the CFP Board obviously advocating for the CFP marks as the minimum professional standard).

Where Should The FPA Go From Here?

So given all these challenges, where should the FPA go from here? At the most basic level, the FPA has to focus on one simple reality if it is going to survive: the only way to defend itself against the CFP Board is to have as many CFP certificants as possible, who support the FPA for its advocacy efforts on their behalf (including against the CFP Board) and keep the FPA relevant as a separate membership organization from the CFP Board. The FPA leadership should make “market share of CFP certificants” its one crucial Key Performance Indicator for the coming years when evaluating the success of its staff, programs, and efforts. Just growing membership isn’t enough (not that the FPA has even been succeeding in that regard); if the FPA isn’t gaining in total share of CFP professionals, too, it’s still losing ground in its power struggle with the CFP Board.

After all, the reality is that with 70,000 CFP certificants and the numbers still growing, there are too many CFP professionals to not have a clear membership association loudly and publicly advocating on their behalf and helping to make them more successful. If the FPA cannot take on that role – whether due to its fuzzy and meandering focus, lack of clear messaging, or simply poor execution – then some other organization will eventually fill the void (CFP-Board-driven or otherwise), and at the point a true competing membership association crops up to challenge the FPA, its demise may only be further hastened (as it cannot afford to lose what core CFP certificant membership base it has left). Which means, once again, the FPA either truly lives into its CFP-centric mission, or it must figure out an astonishing pivot that could keep itself relevant as a membership and advocacy organization competing against another CFP-centric membership group (and given the existence of FSI, NAIFA, and others, it’s not really clear what other role the FPA could realistically fulfill).

In other words, the FPA really has no choice at this point but to embrace its CFP-centricity – or better yet, clarify its position to be “one profession, one minimum designation” so it can support the CFP marks as a pathway to the financial planning profession without undermining its relationship with post-CFP educational providers – because any other path just makes the FPA “yet another financial advisor membership association” (a tactic that has clearly done it no favors for the past decade), and the less it attracts CFP certificants, the less beholden the CFP Board must be to the FPA, and the more opportunity the CFP Board has to try to undermine and replace the FPA. In other words, if the FPA doesn’t live into the vision of the ICFP, the CFP Board or some new competitor will take over the role themselves and make the FPA irrelevant to the future of the financial planning profession. There are too many CFP certificants to be so under-represented.

Notably, though, the FPA (finally) fully embracing its CFP centricity and (loudly and publicly) taking up its mantle as the membership association for CFP certificants and advocating on behalf of the CFP Marks does not mean acquiescing or subjugating itself to the CFP Board in the process. The FPA already takes lobbying issues to the SEC and FINRA, even though its members are RIAs and registered representatives; the fact that the FPA lobbies against certain policies of the regulators doesn’t change the fact that members are still expected to be registered with those regulators, and the same would be true of encouraging financial planners to be CFP certificants while advocating on their behalf against the CFP Board when apporpriate. In fact, the whole point of embracing CFP centricity is that by having more CFP certificants the FPA shifts the balance of power back into its favor, to be able to hold its own against the CFP Board and advocate even more effectively, because in advocacy the reality is that numbers = power. The Financial Services Institute recognized this, rapidly gained power in lobbying to FINRA because it has gathered nearly 37,000 registered representatives as members, and so too can the FPA (re-)gain power by trying to rapidly add more CFP certificants to its ranks in order to represent them.

Of course, it’s worth noting again that from the perspective of a CFP certificant, if the FPA cannot step up to the task and ultimately topples, the loss of the FPA isn’t necessarily a bad thing. A potential consolidation of the credentialing body and the membership association allows for a better pooling of resources, more coordinated advocacy and lobbying efforts, likely lower costs for CFP certificants who are FPA members and can just pay one fee instead of two, and the unification of the two could actually become a superior CFP-centric membership association than what the ICFP was and what the FPA was intended to be.

Again, though, the greatest caveat to the elimination of the FPA and a consolidation of the profession’s power within/behind the CFP Board is the fact that with the FPA out of the way, it becomes increasingly difficult for CFP certificants to push back against the CFP Board in an organized and coherent manner when the CFP board does something objectionable, as it has been wont to do from time to time over the years. Which means that ultimately, the FPA’s best path to survival at this point may be to explicitly capitalize on the collective nervousness of the CFP certificant community about what happens when the CFP Board goes “unchecked” for too long, and solicit members on the basis of being that organization which can advocate for their interests against the CFP Board when necessary (while also striving to help their members be successful in other ways as well, and advancing the CFP marks as the center of the financial planning profession in accordance with the FPA bylaws).

But the bottom line, though, is simply this: with the ongoing growth in CFP certificants, it is simply impossible for 70,000+ professionals to not have a membership and advocacy association dedicated solely and entirely to their needs. The FPA is at a crossroads about whether to step up and fully embrace the vision of the IAFP and ICFP merger – to loudly, proudly, and publicly be the membership association of CFP certificants and those who support the financial planning profession with the CFP certification at its center – and justify why CFP certificants should pay for both the CFP marks and a separate membership association to represent them, or risk being made irrelevant as its financial resources continue to dwindle and its power continues to wane, until eventually the CFP Board or some other competitor steps up to fill the CFP certificant membership void on its own terms.

Great post Michael. I have a difficult time paying all dues lately, I don’t see any value in having our leaders battle to demand regulation and legislation. I would suggest they have had success that could easily be their niche again… they are the one place that once upon a time had great consumer outreach; seminars, blogs, events… but no longer. I’ve been a part of several projects over the last decade that aren’t seen through to completion, or just left to die. There’s no leadership. Over the last year I spent maybe twenty hours providing them work for a project… I should have guessed what would come of it – nothing. Why start a consumer project if you don’t know what it will take to complete? I valued their opposition to CFP Board on CE, so I do see they have some potential value, which is why I’ve stuck around when I know so many who haven’t. However, they need to drop pretending to be something they’re not ready to be in the maker of legislation, and focus on their core value. CFP Board and NAPFA have a little more room to think they can upset members by not focusing on their value proposition to members, but even they IMHO aren’t doing all they can. FPA could easily stake claim to the place for consumers, press, and members to go for financial planning knowledge; they just seem like they aren’t willing. If I had advice, it would be get out of this coalition and spend all energy on consumer outreach through your members. Won’t happen as long as they have all of these attorneys killing our associations with their lobbying on the payrolls.

BillyBob,

In point of fact, FPA trimmed its budget on lobbying after the revenue decline in 2008; it shut down its Washington office altogether, replacing it with an outsourced lobbying firm (ostensibly also narrowing the scope of how much they would lobby on) at a significantly lower cost.

Being part of the discussion of the future of regulation for financial planning is a crucial part, but that’s the whole point of being part of the Financial Planning Coalition and its purpose – as you note, FPA certainly can’t be the maker of legislation on its own.

Having FPA more involved in communicating financial planning to the public is something that could also be better coordinated with the CFP Board – especially given CFP Board’s ongoing spending in public awareness already – although I have to admit I wish the FPA would spend far more time helping advisors figure out how to get paid for their services, and less time helping advisors figure out how to give more of their services away for free (i.e., pro bono). I’m certainly not against pro bono work at all, but I hear far more advisors struggling to grow their businesses than advisors struggling to figure out how to spend less time getting paid and more time doing pro bono instead…

Sorry to hear of your time and efforts spent on a project ‘that went nowhere’ though. It hurts for any volunteer to see that kind of outcome (or lack thereof). 🙁

– Michael

All true. My feeling on the lobbying in total is it is not how the profession grew into existence, and it isn’t how it will continue to, no reason to get into that, however I do feel they need to spend their time focused on their strengths, which lobbying clearly is not one, or not an efficient one they are structured to take on. Joining a coalition with a partner who is destroying your value as an organization I see as a weakness. You lay out the idea behind promoting the CFP, which is fine, but I also always saw FPA as uniquely situated to be the group that brought together specialists in attorneys, accountants, 401(k), insurance specialists, etc., the CFP and non-CFP. In our area these individuals have disappeared from membership. CFP Board has changed it’s mission clearly, maybe FPA should do the same. I valued FPA conferences and journals due to depth of experts more so than elsewhere.

I’ll also share, I enjoyed the pro-bono aspect, but in this part of the world that’s been dead a long time, my guess is they’ve lost the relationships and capital they had there. IMHO that’s one way the profession gains public credibility, not through legislation, I enjoyed the opportunity, and no, it’s not for those starting out. It was an asset they built, however aside from that volunteer work I mentioned I haven’t received a pro-bono request in years.

Thanks for the chance to rant about it ! Hope someone’s paying attention.

Excellent post!

Thanks Lee! 🙂

Great post. The CFP Board needs checks and balances and their recent survey built on the premise CFP’s need another regulatory body is case in point. We don’t need more regulators we need someone who will stand up and loudly proclaim to the public the benefits of working with a CFP.

Tim,

To be fair, it’s worth noting that part of the point of the recent Coalition study was not that planners need more regulators, but that they need BETTER regulators and a regulatory effort focused on what we do.

Imagine a world where financial planners are NOT subject to as many as half a dozen different regulators (SEC, FINRA, state securities, state insurance, etc.) based on every possible type of product being implemented… they’re just subject to ONE regulator that oversees them AS financial planners. And the only people under that regulator are the ones who really practice as financial planners, and are the only ones who can hold out to the public as such. That’s the point they’re getting at with the study.

– Michael

I’m sure there are central planners with intentions like yours Michael, but that’s not the nature of government, it isn’t what those who make decisions actually implement, nor do they have the ability to keep up with changing businesses. The nature of government is to fail and to demand more power and money. If you have government employees as clients, they know this. I hear it all of the time.

Regulatory capture puts us even more under the thumb of those with the money, and when that one is an insurance giant, be careful what you wish for. It’s against how government operates to have less regulators; and it just doesn’t happen. Look at the banking industry, many banks don’t even know who their regulator is, and many regulators don’t know what banks they are responsible for. And… yet… those regulators won’t ever lose their jobs or pensions, and their budgets will never decrease, nor will their employment numbers.

State insurance regulators are in place for one reason – protect the business of domiciled insurers, and the federal government is willing to have that protected. I wonder how much declining membership is due to how many of us believe these battles are not worth fighting, and it’s better for our survival as a profession to not take them on.

Financial Planners providing financial planning advice have no regulation by government entities. Don’t “loudly proclaim” too loudly if a CPA-PFS is around. Although I’m fond of and embracing both, take a look at the educational requirements including CPE/CEU of the CPA-PFS. Like me, you may get a wake-up call!

Michael,

CPAs can get a CFP. Non-CPAs cannot get a PFS.

If PFS were to become the standardized marks of the profession, you would exclude… what, 95% of current practitioners who can’t get the PFS without going back to college for auditing classes? How does that possibly advance the profession of financial planning by attaching it to accounting requirements that have no relationship to financial planning?

If CPAs want to be financial planners – for which I’m actually a huge supporter, and think the AICPA PFP section has some great people – what’s wrong with having them simply become CPA, CFP, and join in the efforts to advance a single UNIFIED profession… since, again, “their” mark is actually MORE exclusionary of non-CPAs than anything else around!

– Michael

Amen!!

At this point I am disappointed with both organizations as they look more and more dysfunctional at the top as time goes on. I think of another professional mark called Certified Public Accountants. They have great public awareness of who they are and what they do. They don’t have the drama that CFPS’s have to put up with.

Tim,

To be fair, the accounting profession does have a bit of a head start. The AICPA was founded in 1887 and has been at it for a very long time.

I suspect if you go back to their first few decades of the AICPA, you’d see a whole lot of inner turmoil to the emerging profession as well. That’s just the reality of how professions emerge; it’s never easy.

– Michael

I have often been asked why, as a CFP since 2007, I am not a member of the FPA. In my case, it comes down to my experiences with the local chapter when I was first starting in the business.

Long story short, in several conversations it was clear to me that my employment with an insurance B/D (even though I was a CFP and doing comprehensive financial planning) was seen as inferior to the “fee-only” planners doing “real” planning (one quote that stuck was “well, I guess everybody has to start somewhere”). That attitude of superiority, and even condescension, has kept me from returning for 7 years (who knows if it has changed).

Even now, as someone who is a fee-only, stand-alone adviser without a B/D, I was so put off by that attitude that it would take some serious convincing that things have changed in the organization and that there was value beyond the magazine before I would consider joining.

-Elliott Weir

Thanks Michael for your thoroughness.

Interesting that Elliott and I seem to both be turned off by the FPA, but for opposite reasons. Elliott feels that the FPA looks down on commission advisors and I think the FPA should be more fee-only centric as I don’t think commissions are compatible with a fiduciary standard of care.

I used to be a commission broker and agent, and switched because fee-only substantially reduces conflicts of interest- it’s just much easier to be a fiduciary without commissions. While I think it’s fine for the FSI to claim that a fiduciary standard isn’t necessary, I do not think it’s helpful to our profession for any of our professional organizations to suggest that commissions and fees are equally compatible with a fiduciary standard of care.

We actually discussed whether to renew FPA last week, and I basically said that I hated to bail on them because they have at least seemed to try to move towards fiduciary care, but it has been in fits and starts. The FPA knows they’ll lose members if they advocate for fee-only, and they don’t know how many members they’d pick up since NAPFA already has the fee-only ground.

Perhaps the FSI and NAPFA are the natural membership organizations as long as we have two forms of compensation.

Bill,

It’s worth noting that commissions by their nature don’t HAVE TO be an unmanageable conflict of interest that violates the fiduciary standard (though many of today’s extreme commission products would clearly fail the test). For instance, term insurance is a product that is so standardized in pricing and structure already, with compensation that is still modest, it’s not hard to imagine how it could fit in with fiduciary advice. Ultimately, fiduciary outcomes are judged by the process by which the advice was crafted and rendered, not merely/solely the compensation.

It is worth noting, though, that the FPA actually has far MORE fee-only advisors than NAPFA does, as ironically the NAPFA culture is so strong that it even turns off many fee-only advisors (though clearly it attracts others). And officially, both FPA (and CFP Board itself) are “compensation-neutral”, though in practice the experience for FPA varies a lot from one chapter to the next (as Elliott noted).

Personally, I think the ultimate path should be much MORE about focusing on fiduciary and LESS about pure compensation models – including how to establish a fiduciary process that MIGHT allow SOME commissions, under appropriate standards (which a good fiduciary rulemaking process should establish and clarify).

Part of the problem for FPA – and the CFP Board as well to a large extent – is that they have preached a fiduciary standard, remained “compensation neutral” in allowing commissions, and done nothing to provide guidance to practitioners about how to reconcile those two positions. :/

– Michael

The reality is that financial advisors are often acting in a fiduciary

capacity regardless of those who claim otherwise. Clients seek us out

because they lack knowledge- which all by itself establishes the

relationship as fiduciary.

In fiduciary relationships there will always be conflicts of interest and unfortunately the common belief is that disclosure addresses the problem. It turns out that this is a terrible approach because disclosure actually causes worse outcomes when advisors are faced with bad compensation incentives- which can more than overwhelm processes intended to produce unbiased advice.

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=480121

So disclosure really looks like an abdication of fiduciary responsibility,

The approach that will result in best fiduciary practices is to minimize conflicts and the existence of commissions simply makes it harder for the profession to act in a fiduciary capacity.

I believe that the existence of commissions is also preventing the development of fee only services that would be accessible by middle and lower income consumers. If we provide plans for true middle income consumers (household income $50k), we can do it for $500 if we don’t have to spend extra marketing effort and time to explain why they are better off paying us $500 then getting recommendations for purchasing financial products that don’t have any fees (but result in $1000 in commissions that they don’t see).

Bill,

As a brief follow-on, this does also continue the point I made in the article, that by trying to forever choose the middle ground, the FPA often ends out alienating BOTH sides. It’s too-fee-only for many commission-based advisors, not fee-only-enough for many fee-only advisors, too-CFP-centric for non-CFPs, but not-CFP-centric-enough to attract CFP certificants en masse.

Ironically, the FPA is basically suffering from the same large-scale problem that many advisors are struggling with as well – the total loss of differentiation by trying to be a generalist that appeals to everyone, and in the process doesn’t actually appeal to anyone. :/ http://www.kitces.com/blog/are-financial-planners-experiencing-a-crisis-of-differentiation/

– Michael

Michael, thank you for a comprehensive history lesson. I appreciate it because its good to know what has gone on in order to learn. Two things are important to me: First: the “financial planning association” has always been “financial planning” and not exclusive to financial planners, financial advisors, certificants, charterholders or trademarkers. The beauty of associating with like-minded professionals has always related to business building and boy, as you mentioned your preference of striving to be more successful, we need that focus. Second, although I always embrace professional (referring to CFP Board, American College, Kaplan, Zahn, etc) and university education, the government licensing of Financial Planners will be the single greatest Public Awareness event for the protection of consumers and the success of financial planners since the creation of financial planning in the 1970’s. It will also be a “Game Changer” for the CFP Board and the FPA. Thanks again, Michael!

Michael,

The point is not really to “just” be about CFPs per se, but to

be about financial planning.

The caveat is that if FPA really believes in pushing forth

financial planning AS A PROFESSION, the hallmark of a profession is that it MUST have a minimum threshold for competency and a means to delineate “real” financial planners from the rest.

And while the CFP Board has its own issues, I don’t see anything

remotely as well positioned to be that minimum competency standard for

professionals besides the CFP marks. So if it’s going to be “something” – and

HAS TO be something to meet the requirements for a profession – the CFP marks

is the best horse we’ve got in this race.

So we either encourage and support that horse – INCLUDING

having FPA play a role shaping its future – or we abdicate the role, and let the CFP

Board entirely control its own future. And as I noted in the article, I think it’s healthier for the emerging profession – given the CFP Board’s own history of issues – to have the FPA serve as a check-and-balance system, rather than simply leave the CFP Board completely free to do whatever it wishes with limited means of accountability from the CFP certificants themselves!

– Michael

When I read you write, “So if it’s going to be “something”

– and HAS TO be something to meet the requirements for a profession – the CFP

marks is the best horse we’ve got in this race,” I knew that my experience

working with the State of Florida regulators gives me a different point of view

and a much more hopeful one, too. I’m not in favor of one or the other when

discussing CFP Board or American College or Boards of Accountancy, etc. But the

state regulators will make their own requirements for licensing of financial

planners and we’ll like it because it gives the public clarity, something to

trust.

Just one quick example, the CFP Board couldn’t

get past the minimum requirement of 30 CE’s every two years while the CPA has 80

every two years. Heck Michael, even the RFC requires 40 per year. 18 college

level hours, 15 CE’s/year doesn’t even compare to CPA-PFS.

Can we open our eyes to this because it is a new

horse race? And licensing will make it even better for all of us including the consumer.

Michael,

I’m not saying licensing of financial planning is bad. I’m simply saying that having regulators create YET ANOTHER REGULATORY STANDARD is just more regulatory redundancy in an already-badly-regulated industry.

And the CFP Board’s decision to not implement the increase in CE hours was primarily about the dearth of quality CE providers educating advisors in the first place. The clear trend of the comment responses to the proposal was not against more CE, per se, but against requiring more CE when the current CE already does such a bad job teaching relevant/new content. Thus why the CFP Board has spent the past two years trying to improve CE quality, changing requirements for CE sponsors, etc. – an area which I’ve also covered in depth on this blog in the past, see http://www.kitces.com/blog/strategies-for-cfp-board-to-improve-the-quality-of-cfp-continuing-education-ce-credit/

– Michael

Seriously, Michael. I’m beginning to think that you have cloned yourself. I don’t know how you put out so much good content as quickly as you do.

Anyway, I dropped FPA after a few years in the business. As a fee-only planner, I simply can’t back a member organization that doesn’t hold its members to the fee-only and fiduciary standard.

NAPFA is far from perfect, but it’s my go-to member organization for now. I’ve wondered why we need separate fee-only organizations such as Garrett, Cambridge, and now XY. Couldn’t NAPFA carve out areas of focus by niche or fee model? I get that smaller organizations can be more nimble, but isn’t there also strength and efficiencies in numbers?

Keep up the great work!

Rob,

I think the distinction is that Garret, Cambridge, and now XYPN are not merely “fee-only membership” groups. They are entire platforms for executing a particular (albeit fee-only) financial planning business model. I call them “TFPPs” (like TAMPs, but for financial planning – see http://www.kitces.com/blog/forget-the-tamp-its-time-for-the-tfpp/ ) and the role of a TFPP is fundamentally different than a membership association.

In point of fact, XYPN actually pays for all of its members to ALSO be members of NAPFA, as we believe that even with the services that XYPN provides to its advisors, there is value to being in a membership association like NAPFA, too!

– Michael

Great article! I really think long term the planning profession needs it’s own professional designation and it’s own professional organization.

Impressive article Michael. Well researched, thoughtful, and articulate.

Michael,

I am a financial planner and a volunteer board member of my local FPA chapter. They have worked hard for years to try and build up our chapter. I have heard the numbers that you presented before, but your blog seems to predict the end of the FPA and you do support that prediction with facts. I do not have a national perspective, so I defer to yours, but I am disappointed with the implications of your article. It makes me question if any such organizations can succeed- as there is always a great deal of different agendas AND money in this field? I am a fairly new planner so I am not defending FPA- just concerned about hearing negative feedback about so many organizations.

Kevin,

It’s worth noting that ultimately, the chapters are separate and distinct entities from the national organization. So chapters can survive – in some manner or another? – even as national FPA has woes, though building and just administering membership would be difficult without national to assist. But even “without” the FPA, people still have a need to come together for community!

In point of fact, I believe that the chapters are one of the greatest assets of the FPA all around, but the challenges of membership building at the national level do unfortunately translate down to the chapter level as well. :/

– Michael

Great analysis Michael thank you. We debate keeping FPA memberships in my office, and I dropped mine years ago. The journal is great, the discussion board options nice, but I don’t see a lot of value from the other offerings especially when professional dialogue is so readily available if you want it.

Although, we are frugal and have cut cable and the home phone too, so perhaps that trend is also part of the shift… I am happy to pay the CFP board extra money for educating the public.

Michael,

As so often in the past, you have done a great service by “stirring the pot” and stimulating a badly needed discussion about the future of the FPA. Still, I have to wonder whether the time has not come to leave the designation wars of the ’90s behind us (the CFP mark won so let’s move on) and to finally seize the opportunity created by the merger that created the FPA. Rather than endlessly focusing on whether the merger was a hostile takeover by the IAFP of the ICFP to create “The community of those who support the Financial Planning Process” (Whatever that meant), or a hostile takeover of the IAFP by the ICFP with the aim of reincarnating the ICFP, isn’t it time that we recognize that what the merger created was and is the Principal Professional Organization for Financial Planners?

I have taught CFP courses for 15 years and assure you that with the compensation paid as adjunct faculty, it hasn’t been for the money. While I have differences with the CFP Board (the only one I never disagree with is my wife) I still support the CFP mark, its ethical and educational requirements. I am not advocating any disavowal of the CFP mark by the FPA, but if the FPA is to be nothing more than the “booster club” for the CFP Board, it does indeed become irrelevant. Even more, the FPA’s support for the CFP mark is simply redundant if the FPA is nothing more than the an organization of and for CFPs.

Isn’t it time that we seize the opportunity created by the merger and finally become what we have been ever since; the Principal Professional Organization for Financial Planners? We can continue to support the CFP mark as called for in the memorandum and do so, not because we are required to, but because it still serves as the “gold standard” for the financial planning profession. We can also then insist that the CFP Board live up to that standard. It would also enable the FPA to reach out to the AICPA in a collaborative fashion rather than pretending that the PFS were somehow hostile territory.

Finally, and as a practical matter, if Financial Planning is ever to become a profession in its own right, rather than just being something that investment professionals or insurance professionals do, it is going to need some kind of regulatory standards. I would suggest that we may want to think long and hard as to whether we really want to contemplate having the CFP Board serve as our FINRA. Much as FINRA may like to maintain that it is an independent regulatory body, it is ultimately a “self regulatory body” and the “selves” there are the broker dealers and is accountable to them. As of now, the CFP Board is accountable only to the extent that it depends on certificants valuing the mark, seeking it and continuing to renew. If they are even given true regulatory authority, they would be totally unaccountable. Is that really what we want?

What the financial planning profession desperately needs is a professional organization that advocates on its behalf — whether that advocating be on the national level, on the state level, or towards the CFP Board. It is a mystery to me why the FPA has, since its inception, been so consumed by its past that it refuses to pick up that mantle. I am optimistic that, despite those still seeking to reconstitute the old ICFP, the FPA is groping in that direction. Hopefully, the discussion you are stimulating here will help to move it there before it is too late.

David,

Thanks for your comments!

What you’re saying here is virtually identical to the point I’m trying to express as well. It’s not merely that the FPA be “the booster club for the CFP marks” – it’s that the FPA focus on advancing the profession, which includes backing a competency standard that can become a credible minimum standard for the profession, for which as you note the CFP marks have already been the winner and the designations wars are over.

In fact, the whole POINT of having the FPA support the CFP marks while being separate from the CFP Board is to serve as that advocate for the profession – including having the CFP marks as its minimum standard – and that may include advocating AGAINST the CFP Board when appropriate.

For some reason, the FPA seems to have allowed itself to become so intimidated by the CFP Board, that it has become afraid to support the marks and backed away from them for years… not recognizing that the less the FPA backs the marks, the less the FPA has any voice in what the CFP Board does or the direction of the profession itself…

– Michael

Michael,

Part of the issue may well be that, as I have been told by “usually highly reliable sources” the FPA can date its declining membership to the day when the CFP Board stopped sharing its list of new certificants.

David,

What business gets a free list of qualified prospects just handed to it on an ongoing basis?

Sure, I suppose it was a nice free ride for the FPA in the early years as long as it lasted. But the fact that the FPA doesn’t get a free list of prospective members from the CFP Board is hardly a legitimate reason to blame for a decade’s worth of declining membership.

That was a reasonable excuse for why FPA’s growth might have paused for a year or two, way back when the list got cut off. If FPA has failed to grow for a decade and still blames the end of getting the list a decade ago, then shame on the FPA for not coming up with a single other new way to get members for all the time that’s passed since then.

You, I, and all of us who run businesses, recognize that getting new clients/members requires effort to market and build awareness of our businesses and the value that we provide. Why should FPA be any different?

– Michael

That is certainly true, and yet if the FPA is to support the CFP mark, would it be so strange for the CFP Board to continue being supportive of that effort rather than to pull the rug out from under it?

There is no question that the FPA could have and should have done a much better job of adapting once it happened, but it does raise the question as to whether the membership decline was due to the FPA drifting away from its support of the mark, so much as its failure to adapt to the CFP Board casting it adrift.

David,

But the FPA has not consistently supported the CFP marks. It has wavered back and forth for a decade about whether to be the “big tent” for all people supporting financial planning, or whether to specifically focus on the CFP marks as the core designation for the emerging financial planning profession.

When the FPA continues to waver its focus back and forth every few years, is it any wonder the CFP Board is less-than-enthusiastic to support them in return? Especially since the reality remains that the CFP Board is having no trouble growing ITS ranks even without the FPA’s support, and the weaker the FPA is, the more the CFP Board can do as it pleases with less accountability?

– Michael

Michael,

I am not quite sure how the timing on this worked, but if the FPA precipitated the cut off, that certainly was a major strategic error. Perhaps, now that the pendulum has swung back the CFP Board can be convinced to reconsider.

Still, I am not sure they will be much more enthusiastic about a CFP practitioner organization that stands up to them, than one they have been for one that they perceive as wavering in its support. If not, as you point out, that leaves only a more effective marketing program for FPA.

David,

FPA didn’t precipitate the cut-off, the CFP Board did. Sharing the list was recognized to be a potential violation of their own privacy policy for CFP certificants (though realistically, they could have come up with a workaround if they really wanted to).

The point is simply “If the FPA’s existence as an advocacy organization is contingent on being handed a list of potential members from the very group they’re advocating towards, something is VERY broken.” The FSI doesn’t get handed a list of registered reps from FINRA so that FSI can recruit them to lobby against FINRA. The state insurance regulators don’t hand lists of new insurance agents to NAIFA. Every other advocacy organization does the work of going out to get members; if FPA was getting a nice easy ride from the CFP Board for a while, that’s great, and I can appreciate losing that list was a disruption for a short while.

But if we’re still talking about it a decade later, something is very wrong. It’s no excuse to STILL not be growing this many years later!

– Michael

Michael,

I would think that your points here are beyond dispute. In fairness, I know that there are many at & in FPA who share these concerns, but you have done a tremendous service by stimulating this much broader discussion. Thank you, thank you, thank you.

David

I do believe we need an advocate with the CFP when, not if, they go rouge. I have always looked to the FPA to do just that but I am beginning to wonder after reading this post if the battle is too far gone and we need to prepare ourselves for another regulating organization with little in the way of promoting the CFP standards to the public. I have always viewed the CFP board as power hungry at the expense of their members and this does nothing to alleviate those fears.

Michael,

This is nothing short of a tour de force — an inarticulate manifesto. This all needs saying; I appreciate that you have said it thoroughly, forcefully and articulately. Many thanks.

One thing. As thorough as you have been, I think you have missed a major issue, namely the role that the financial services institutions have played and continue to play in the governance and public perceptions about the proper practices of our work. Financial planning continues to be conflated with investment management first and then financial products in general. CFP Board contributes to the confusion by Its continued reliance on 1972 categories; both inhibit the appropriate evolution of the profession.

I must admit I have a thing about financial services companies acting like they’re the ones that do the financial planning, not individuals. That said, I don’t think we have done much analysis of the impact of these companies on the development of what is now being called the financial planning profession.

May I suggest posting it on FPA Connects? Again, thanks for this articulate contribution to an important conversation.

Dick Wagner

Oops the first line should read ” an articulate.” Thanks Dictate 4.0.

Dick,

Thanks for clarifying. I was thinking that seemed to be an awfully backhanded compliment. 😉

– Michael

Dick,

Thanks for the kind words.

You have some interesting points here about the role that (product) companies play in this process. I’m not sure I’m convinced it’s been what has shaped the FPA in particular, but I concur with your comment that it has shaped some of the other conversations around the emerging profession.

Regarding FPA Connect, you (or anyone) is welcome to post there a link to this article for those who want to come and read. (I’m always wary to not post my own content there, for fear of being deemed ‘self-promotion’ even when that’s not the intent.)

– Michael

As always, great insight. I’m ready to support Michael in leading a coup against both the CFP board and the FPA (I’m belong to both). I would gladly double or triple my dues to both organizations if I thought either one of them was really taking our profession to the next level.

P.S. Michael your blog really is good enough to warrant a subscription fee. Perhaps you should consider adapting a Nick Murray business model with a newsletter and spot coaching service.

Michael,

Your main tenant here, that FPA should shed it’s confusion and identity crisis and fully embrace its CFP-centric core value, may be like pushing mud with a boulder up hill. FPA has grappled with what it actually stands for ever since the merger. The fact is that IAFP grew and flourished as a membership association, embracing all financial services professionals and providing educational content and networking opportunity for all. (Advocacy wasn’t a big issue before the merger.) Then CFP-centric became the standard, and that was fine, too. When Lauren was taking over, Ithere was a town hall meeting at the Chapter Leadership Conference (2011, I believe) in which David Brand as spokesperson for FPA leadershp shared that FPA was assertively now CFP-centric. I reacted with dismay, as I felt that FPA’s stakeholder base was further narrowing. The problem I saw was that the words were CFP-centric, but the message I heard was CFP-exclusive. In looking at my notes this morning from that meeting, I see that I wrote “Financial planning-centricity YES! But the messaging coming from leadership feels like exclusivity.” (I raised this point at the meeting, but it was essentially ignored. I also wrote “service lines confusion: you can’t successfully have a “one profession” position inside an organization which purports to be a broader, all embracing industry association.” I had a serious foreboding for the future then.

I joined IAFP in 1979 and have always been an active member. As a past president of my Chapter and on the front lines, I ignored the messaging so as not to alienate what few allied professionals who embraced the financial planning process that we had as members. It was impossible to recruit what should have been this low hanging fruit with out any support on this front from FPA. In many conversations with FPA leadership, I have raised these red flags over and over; but, I don’t believe we can see the forest for the trees.

Two very tangible realities before I end this (too) long comment: 1)the membership fees for two organizations are substantial, only one is necessary to a CFP practitioner’s practice, While the other may be desireable, it may not be easily affordable. I’m sure choices are being made out there. 2)The value and importance of a pure membership organization (FPA) is not as obvious as the necessity of paying the CFP Board’s dues, even though they frankly offer less overt value other than the license itself. 3) I know that FPA’s covert CFP-exclusive advocacy has alienated MANY professionals who otherwise either practice or embrace the financial planning process from joining, and these are the very professionals who could make FPA relevant and healthy again.

Michael, you are so valuable to this profession. Thanks for being there and doing your thing.

Eric Bruck, CFP

Michael,

Your main tenant here, that FPA should shed it’s confusion and

identity crisis and fully embrace its CFP-centric core value, may be like

pushing mud with a boulder up hill. FPA has grappled with what it

actually stands for ever since the merger. The fact is that IAFP grew and

flourished as a membership association, embracing all financial services

professionals and providing educational content and networking opportunity for

all. (Advocacy wasn’t a big issue before the merger.) Then CFP-centric

became the standard, and that was fine, too. When Lauren was taking over,

Ithere was a town hall meeting at the Chapter Leadership Conference (2011, I

believe) in which David Brand as spokesperson for FPA leadershp shared that FPA

was assertively now CFP-centric. I reacted with dismay, as I felt that

FPA’s stakeholder base was further narrowing. The problem I saw was that the

words were CFP-centric, but the message I heard was CFP-exclusive. In looking

at my notes this morning from that meeting, I see that I wrote “Financial

planning-centricity YES! But the messaging coming from leadership feels

like exclusivity.” (I raised this point at the meeting, but it was

essentially ignored. I also wrote “service lines confusion: you

can’t successfully have a “one profession” position inside an

organization which purports to be a broader, all embracing industry

association.” I had a serious foreboding for the future then.

I joined IAFP in 1979 and have always been an active member. As

a past president of my Chapter and on the front lines, I ignored the messaging

so as not to alienate what few allied professionals who embraced the financial

planning process that we had as members. It was impossible to recruit

what should have been this low hanging fruit with out any support on this front

from FPA. In many conversations with FPA leadership, I have raised these

red flags over and over; but, I don’t believe we can see the forest for the trees.

BTW, The language of the “Memorandum of Intent…” you posted was pretty much spot on for attracting our “fellow travelers”. We coulda shoulda stuck to its letter and intent. Excerpts”

“…The new organization will create an environment where financial planners hold the CFP license and will encourage and facilitate attainment of the CFP mark by financial planning professionals, so that ultimately the CFP mark is synonymous with financial planner…

a. The thrust of FPA’s message to the financial services industry will be that all

those who support the financial planning process are valued equally as members

in FPA and that anyone holding themselves out as a financial planner should

seek the attainment of the CFP mark. FPA

will commit to assisting financial planners who are interested in pursuing the

CFP designation….

a. Any individual or entity that supports financial planning will be valued equally as

a member of FPA.”

Two very tangible realities before I end this (too) long

comment: 1)the membership fees for two organizations are substantial,

only one is necessary to a CFP practitioner’s practice, While the other may be

desireable, it may not be easily affordable. I’m sure choices are being

made out there. 2)The value and importance of a pure membership organization

(FPA) is not as obvious as the necessity of paying the CFP Board’s dues, even

though they frankly offer less overt value other than the license itself. 3) I

know that FPA’s covert CFP-exclusive advocacy has alienated MANY professionals

who otherwise either practice or embrace the financial planning process from

joining, and these are the very professionals who could make FPA relevant and

healthy again.

Michael, you are so valuable to this profession. Thanks for being there and doing your thing.

(I hope that this didn’t post twice. It disappeared when I came back to add a bit.)

Eric Bruck, CFP

I am going to devote mere minutes to responding to this post. Yes, FPA lost its way in the late 2000s. It has rededicated itself to its initial purpose and is making great strides in the right direction. Other than that, this blog is filled with inaccuracies, old news, rehashed dialogs and the appearance of much greater knowledge, experience of the past and insight than is actually there. Among other things, it hugely overstates competition between FPA and CFP Board and hugely understates the groundedness of FPA’s decisions regarding and interactions with CFP Board about their initiatives (I can’t imagine how congratulating an organization on an exceptional effort at important work can be interpreted as weakness). The fact is, whatever number of CFP professionals belong to FPA, they are the most passionate, dedicated and profession-focused CFP professionals. The goal of increasing membership is what led to the muddy focus in the late 2000s. The current focus on CFP centricity and helping us all be the best financial planners and business owners we can be is the right focus, and one that will lead to however many members are interested in that. And, as has been the case for all time, those passionate, dedicated and profession-focused CFP professionals will carry the full weight of building this profession. Others will benefit, but those who participate will know the impact their dedication has had – and it will matter. If you want to build the profession of financial planning, hold and revere your CFP certification and be an active, dedicated member of FPA.

Elissa,

If the current FPA is really as laser-focused on helping dedicated and profession-focused CFP professionals, then that’s fantastic. That’s all I’m really asking and suggesting here in the first place.

But I have to admit that I don’t feel like that’s what I’m seeing in the public actions of FPA over the past few years. It still feels like an organization that is afraid to take on that mantle, and defers to the CFP Board on issues that it should be pushing the CFP Board on instead if the FPA is going to be the one that drives the profession forward.

– Michael