Executive Summary

The compounding growth of computing power suggests it’s only a matter of time before computers have the same “brainpower” as a human being. In fact, if Moore’s Law – that computing power doubles every 18-24 months – continues to hold, the crossover point where computers are smarter than humans might not even be all that far away. Which has troubling implications for a wide range of knowledge-based professions, from doctors, to lawyers, to financial planners who might someday be replaced by a “robo-planner” instead.

Yet research shows that our brains are hard-wired to process information differently when received from human beings rather than computers. We evolved as social animals – a trait that was vital to our survival in the early years – which means even if a robo-planner could deliver the same advice as a human, we might be less likely to take it.

In turn, this implies that the key trait for financial planners in the future will be the one skill that our brains are not programmed to receive from a computer: empathy. Because we need to feel that we are heard and understood before we’re willing to take someone’s advice about how to change our behavior, and those feelings of connectedness are an exclusively human-to-human domain.

Unfortunately, though, in today’s environment, there’s remarkably little in the way of “empathy training” for financial planners. But the good news is that empathy training is possible, and is actually on the rise in a number of other professions, from medicine to law and even to the military and the police. Which suggests it may only be a matter of time until it’s more readily available for financial advisors as well.

Still, though, with the onward marching of computing power, our transition from being “knowledge workers” to “relationship workers” may be here sooner than we realize. The good news is that means “robo-planning” will not be the end of human financial planners. But it remains to be seen whether or how many of us will be ready if and when the moment of change comes?

The Exponential Growth Of Technology And The Threat Of Robo-Planning

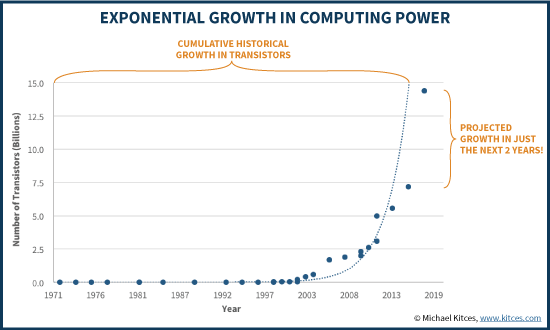

The capabilities of technology are increasing at an exponential rate. In the context of computers, the phenomenon has been dubbed “Moore’s Law”, after Intel co-founder Gordon Moore, who observed that the number of transistors on a computer chip (and therefore its computing power) were doubling every 18-24 months.

In the early years of Moore’s Law, this meant the number of transistors were going from 5 to 10, and then from 1,000 to 2,000. Now, however, it’s about going from 1 billion to 2 billion, to 4B and then to 8B. Which means the absolute increase in each doubling – e.g., from 4 billion to 8 billion – is now an astounding magnitude. After all, a doubling every 2 years means we’ll add as many new transistors to a microprocessor in the next 24 months, as we figured out how to add over the past 50 years cumulatively since we created the first computer!

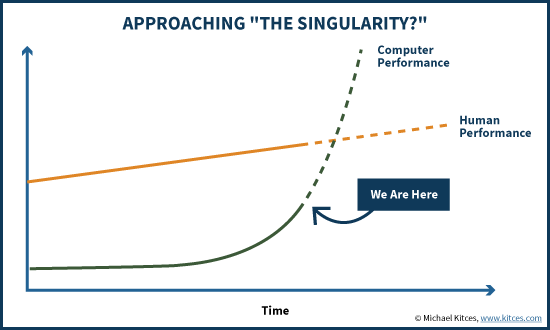

From the perspective of a financial advisor – or any human being – this is troubling, because as humans we may still be learning and advancing, but we’re not getting smarter at a pace that can possibly keep up with the growth in technology. In other words, the computers are getting smarter at a faster pace than humans…

For some, this has raised the question of whether we’ll reach a point that has been dubbed “the Singularity” – the moment at which technological/artificial intelligence actually surpasses human intelligence, beyond which it’s unclear whether or how the human race would co-exist with even-smarter computers. And given the pace of exponential compounding, computers could “catch up” quickly, even though right now they’re still quite far behind.

Even if we act to stop this eventuality – or perhaps the pace of Moore’s Law begins to break down before we get there, simply due to the laws of physics – the challenge remains that the rapid growth of technology could potentially have a dramatic impact on the role of financial advisors. While today’s “robo-advisors” are really just operating as “robo-allocators” – providing a focused asset allocation service, and not holistic financial advice – it’s only a matter of time before the technology expands, all potential financial planning recommendations are mapped into a decision tree, and the rise of true “robo-planning” begins.

“Robo-Planning” Will Change Advisors, Not Replace Them

Notably, though, the potential rise of “robo-planning” still doesn’t necessarily mean an end to financial advisors. After all, the original story of the Luddites – now a colloquial term for those who fear and oppose new technology – was that they were self-employed weavers in 19th century England who feared the end of their trade when new technology (i.e., stocking frames and power looms) was introduced, and culminated in the Luddites actually destroying the new weaving machinery… but in the end, the technology just created new and different jobs (including those who would operate the new stocking frame and power loom technology tools), and did not result in “technological unemployment”.

Nonetheless, the looming threat of ever-advancing technology – especially when it grows at a compounding, exponential rate – does raise the fundamental question:

What is the role of the human financial advisor in the future, if/when the computers become as smart as we are?

Because the compounding growth of computing power suggests it’s only a matter of time.

Yet as Colvin points out, the missing element in the equation is the way our brains are hard wired – we are “social animals”, having evolved that way to survive by working together. And as a result, we are programmed to relate uniquely to other human beings. In fact, recent research has found that when human beings talk to each other face to face, the electrical activity in their brains literally begins to synchronize. Just shaking another person’s hard also causes an electrical experience in the brain… and afterwards, we judge the people as being more trustworthy and competent, simply because we shook their hand.

What all this implies is that in the long run, it may not be a matter of what computers can do in lieu of humans. Instead, it’s about the fact that there are some things we may always prefer to get or do by engaging with other humans. Because that’s the way our brains are built to operate: to have relationships with other human beings.

From Knowledge Workers To Relationship Workers

For the second half of the 20th century, economic and productivity growth were driven heavily by “knowledge workers”, a term coined by management guru Peter Drucker in the 1950s to describe how the primary asset of workers was no longer their ability to do physical/manual labor, and instead was their ability to learn and apply their knowledge.

Yet the irony of this rise of the knowledge worker is that one of its primary creations was the computer. Early on, this piece of technology helped to make us more efficient. But now it threatens to “do” knowledge work better than knowledge workers themselves. For instance, IBM’s Watson supercomputer recently diagnosed in 10 minutes a case of rare leukemia that had stumped doctors in Tokyo for months. And computers are getting better at doing a lot of legal work (e.g., combing through discovery documents) than the lawyers themselves. In other words, knowledge workers may have created the tool that ultimately makes them irrelevant.

Yet as Colvin notes, this still doesn’t mean that all the work humans do will be made irrelevant. Instead, it simply implies there may be a shift – just as in the past, when we went from physical labor workers to knowledge workers, in the coming decades we may transition again, from knowledge workers to relationship workers.

The key distinction of being a relationship worker is that even if the computer knows all the “facts” and “information”, we just don’t relate to and take in the information in the same way when it comes from a computer. In other words, even if the computer can make the diagnosis, we want to hear it from another human being. Whether it’s regarding a health problem, or a financial one.

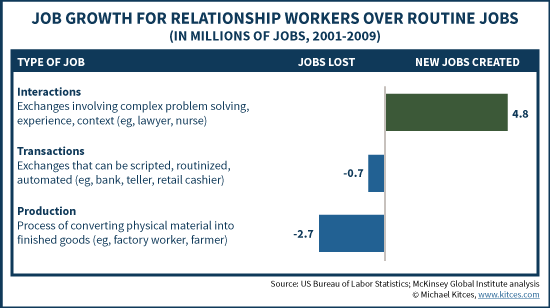

In fact, research from McKinsey on “The Future Of Work” is already finding that while technology is replacing production jobs from factories, and increasingly is replacing routine transactional tasks, job growth continues to be robust in jobs that involve interpersonal human relationships.

In addition, the reality is that, when it comes to financial planning in particular, one of the greatest challenges in helping clients to achieve their goals is that they don’t even know what their goals are in the first place, and may not even be capable of visioning how their needs and desires may differ in the future. And even if and when goals are determined, “life happens” and our needs change, which means goals are often dynamic. Furthermore, sometimes our greatest challenges are the unstated ones – the client who has a “spending problem” where the spending is really about a desire for social status or a way to cope with other emotional issues, or the one who insists on keeping a concentrated investment in a single stock that was inherited from a parent because selling the stock would mean severing the last remaining connection with his deceased father.

In other words, in real life our financial problems and goals are constantly changing, and in not always rational ways, which means sometimes it’s not actually a “solvable” problem in the first place. It’s hard for a computer to answer the question when the client doesn’t even know what the right question is to ask. The role of the financial planner is to help the client change their behaviors if/when/as necessary to navigate the (emotional) journey.

Training Empathy And Relationship Workers

In a world where the value of a financial advisor is increasingly about the uniquely-human relationship – and not just the expert financial knowledge that a computer can replicate – the skill of empathy becomes crucial.

Empathy is the ability to discern what someone else is thinking and feeling, and then respond in an appropriate way. It’s about being able to put ourselves in someone else’s shoes, and consider from their perspective what they must be thinking and feeling, in order to formulate the right response.

Research in the world of medicine – another domain of knowledge workers who are increasingly becoming relationship workers – is already finding that empathy plays a crucial real-world role. One study found that patients are more likely to follow through on a doctor’s recommendation when the physician exhibits greater empathy, while another discovered that doctors with low empathy are more likely to make errors (ostensibly because they miss important information by failing to understand the patient’s perspective), and subsequently are also more likely to be sued for malpractice after bad medical outcomes.

And despite the conventional view that some people are simply born more or less empathetic than others, it turns out that empathy can be trained. The medical industry has been practicing empathy training for years, where doctors role-play patient scenarios, are required to focus on what the patient is likely thinking and feeling, and then receive constructive feedback about how they did.

This core template for teaching empathy – explain how something should be done, show it done well, ask trainees to do it (in ‘pretend’ patient/client situations), and then provide feedback – is being applied in a wide range of industries.

Colvin points out that even the military is recognizing the importance of empathy training, where wars in the future aren’t just about killing people, but being able to win the hearts and minds of the population… which is all about human skills. In fact, the origin of the famous Navy Fighter Weapons School (also known as “Top Gun”) was an empathy-training-style program of putting pilots through intense life-like situations, recording everything that happened, and giving candid feedback, teaching the fighter pilots how to better understand the enemy’s perspective in order to anticipate and respond appropriately. Training in empathy is also becoming a keystone of police academy training.

The Future Of Financial Advisors And Financial Advisor Empathy Training

Unfortunately, while financial planning has increasingly been establishing the technical competency foundation of what it takes to be a professional – e.g., by completing the CFP educational requirement and passing the CFP exam – there is remarkably little education or training for the active listening and empathy skills that should build on top.

Historically, this wasn’t necessarily a “problem” because most financial advisors started out as salespeople, and if their empathy skillsets were poor and they couldn’t develop rapport with clients, they “failed out” of the business in the first year or two. The natural survivorship bias meant that most experienced financial advisors already had a natural empathy skillset, and later they went back to school to build up their technical competency and earn their CFP marks. But financial advisors never had to “practice” the relationship and empathy side of financial planning.

Now, however, students can graduate from college having already completed their CFP education, work for several years as a paraplanner, and then find to move up, they must learn the relationship skill of empathy and also how to do sales and business development. Except there’s a dearth of training in how to do this. There are at least some programs that offer sales training for financial advisors, but almost none for empathy training. And while some advisors end out learning “on the job” as associate advisors, not all senior advisors are very good at teaching and giving feedback (especially when survivorship bias means empathy skills were probably natural for them to begin with). And ironically, the recent CFP Board changes to water down the experience requirement means it’s even less likely that the typical advisor will have had the opportunity to learn or develop empathy skills from real-world experience, either.

Nonetheless, the ongoing forward march of computing power and what computers can do – and the way it’s already rippling through other professions like law and medicine – suggests that it’s only a matter of time before true “robo-planning” arrives, and just being able to recommend financial strategies and tactics to clients won’t be enough. Financial planning will shift from being about delivering expert information and solutions, to a focus on empathy skills and being a “relationship worker” instead.

Notably, a baseline level of technical knowledge will still be relevant – as it’s difficult to apply empathy if you don’t also understand how the financial rules and mechanics work – but will simply be what clients expect, not what they pay a premium for. Instead, our relevance will be the ability to truly show empathy, to connect to clients, because that’s the part the computer cannot replace, whether it’s helping people assess ever-changing goals and desires, or assist them in changing their behavior to actually achieve them.

So what do you think? Is robo-financial-planning so far away it’s not worth considering? Or an inevitability? Will the rise of robo-planning made financial planners irrelevant, or just shift their role from knowledge workers to relationship workers instead? Please share your thoughts in the comments below!

The future is relationship workers. Earlier today I read a quote from Nick Murray. He says that “behavior modification ought to be, in and of itself, an advisor’s value proposition, because great behavioral advice is — at critical moments in an investor’s lifetime — worth so much more”. Today and tomorrow it will be difficult for a computer to get people to change behavior “at critical moments” in a person’s life. To change behavior based on the advice of a human or a computer requires trust. Just like we insist on a pilot in a plane, we will insist on a human behind the machine for a few decades yet. In the most serious of matters, we still trust humans more than computers.

What a remarkably thought provoking and illuminating article. Thanks Michael for articulating that which we may have already known, but needed to hear it aloud.

This is certainly a fear of mine. I have 30+ years of career left and I need to make sure I remain relevant. Since I’m currently more on the technical side of things (plan creation for someone else to present), the need for my work could evaporate within a handful of years. It seems that I’ll either need to move to the relationship side of the business very soon or need to start looking for exit strategies to migrate to other industries. I’d much rather take the former, but it’d be good to evaluate all my options.

Thanks for the great article, Michael. As WiseOwl said, these are thoughts most of us have had, but it’s something that needs to be discussed out in the open.

We also need to work with clients who value a trusted relationship. If all they care about are costs, or investment returns, they won’t be clients for long. “Just say no” to the wrong type of clients.

Some good thoughts here Michael. It amazes me how people write off the threat of robo-advice without truly understanding the way it will impact our industry. I recently read Rise Of The Robots and there’s a great line in there that says something like “What is outsourced today will be automated in the future”.

So many things that advisers spend lots of time on today will be automated in the future. This actually represents a huge opportunity for advisers to reposition their businesses to deliver the things that their clients really need.

My big concern around this is the lack of training in the area of empathy and other related skills. Our system develops planners with good technical skills, but doesn’t look at their people skills. And that’s just not an American thing, it’s the same here in Australia.

Great article, Michael. Thanks! It would be great if some of the major conferences started offering sessions on empathy training, or if one of our industry coaches started making courses available that companies could send employees to.

Great article Michael! Your McKinsey chart seems to show it all. Assuming that trend is continuing for this decade, one can see that the transaction and calculating part of our work is fast being replaced by automation. My 50 years of successful financial advising on a fiduciary basis tells me that the hand-holding and the trust part is our real value. Let’s keep automating the other stuff!

Great article Michael. As an old saying goes, client’s don’t care how much you know until they know how much you care.

We are boiled down to empathy as our last remaining advantage, and yet we still want our full 1% of AUM fee!

There seems to be a backlash against empathy. Of course, the criticized version defines it as entirely emotional. And we know it’s rational, as well. https://www.nytimes.com/2016/12/30/books/review/against-empathy-paul-bloom.html