Executive Summary

Over the years, study after study has shown wealthy families are often worried about passing along their wealth to children, and the risk that those children may end out being “spoiled”, overly concerned about material things, and generally naïve about the value of money. Which is understandable given the extensive research into the correlation between negative (and sometimes tragic) outcomes and so-called “affluenza” (a lack of motivation and sense of isolation often seen in young individuals who are very wealthy). Compounding these worries, families often have difficulty discussing wealth and money with their children - often out of fear that pointing out the size of a potential inheritance will just amplify the problem – even though this lack of communication may just leave their children with “surprise” large inheritances that they have no idea how to handle.

Financial advisors, however, are in a unique position to help their wealthy clients in such situations by showing them how to have conversations about money with their families. Because while families may be uncomfortable and uninformed about how to talk about money, financial advisors talk about money for a living and often thrive on having these conversations! Moreover, helping clients improve their money communication skills not only serves to strengthen relationships within the family between family members themselves, but it also strengthens the relationship the advisor has with the family as a whole. Which is important when dealing with clients who are planning for wealth transfers, as it is very common for heirs to leave their family’s original advisor once they come into their wealth (and similarly is very common for surviving spouses to switch advisors after their spouses pass away).

When creating a process to help clients with money conversations, advisors can start by focusing on three core components: purpose, practice, and people. Money mission statements are a particularly effective way for clients to crystallize their purpose around money, as they are essentially declarations of the family’s long-term goals, attitudes, and beliefs about money. They can serve as powerful tools offering a framework for families to structure conversations around money and wealth with each other, ideally lasting through future generations. Meanwhile, money mission statements also help families practice not just talking about money, but also using it (and teaching children to use it) in ways that are consistent with the values they identified in their mission statements. Finally, involving the right people into the process – family members and relevant professionals across disciplines, such as tax professionals, estate planners, and financial therapists and/or psychologists – can ensure that support is available in all areas where it is needed.

Some considerations that advisors can take into account when creating a process to use with their clients include: 1) how to structure the actual process – how frequently will meetings with clients be held, at what cost, and which professionals will be included in the meetings; 2) how to market the process – will open client appreciation events be held to facilitate money conversations between families or will the process involve only private family meetings, and what channels will be used to advertise the new services; and 3) how to network with other professionals – which professional associations and resources can be leveraged for expertise and support, and what types of training opportunities might offer relevant experience?

Ultimately, the key point is that helping clients identify their values and beliefs around wealth is an essential starting point for advisors to guide their clients through the anxiety they may have around money conversations. By becoming comfortable with and gaining confidence in talking about money with other family members, families will have an easier time imparting core values to future generations slated to inherit wealth and preparing them to use their own assets responsibly and with purpose.

According to a report by United Income released in 2019, an estimated $36 trillion will move from the current generation to the next over the next 30 years. Research using the Federal Reserve’s Survey of Consumer Finances has found the median inheritance was $69,000 (the average was $707,291); for trust funds, the median wealth transfer was $285,000 (the average was $4,062,918) in 2016. No matter how you look at it, there are a lot of individuals that will be inheriting a lot of money – but are the givers and the receivers prepared?

The question is rhetorical; financial planners know that regardless of the size of the inheritance, transferring wealth is a complex process. Those passing on the wealth have their own desires for how their wealth will ultimately be used, while those receiving the wealth may often times have other goals.

What is more, a 2016 research article presented by Kathleen Rehl, Carolyn Moor, Linda Leits, and John Grable report from 2018 cites that “70 percent of widows fire their financial advisor after their spouse dies.” Further, various studies have found that 90 to 95 percent of heirs switch advisors after they receive their inheritance. Essentially… when wealth moves…so do the clients. It is common for individuals (widows and surviving heirs) to seek out a new financial advisor, suggesting that the original relationship the advisor had developed with the family may not always be inclusive of (or favored by, or relevant to) all family members or the next generation.

In light of these struggles with wealth transfers and the behavioral dynamics that come with them, it is even more important for financial advisors to embrace their power to help clients (and their own financial planning firms) by working with the family as a whole, versus just one member of the family, and discussing three key ideas:

- Purpose – without any purpose, an heir may feel aimless and lack motivation, which may put them at potential risk to squander their inheritance;

- Practice – simply because someone has a lot of money does not necessarily mean can manage it effectively (and is often why lottery winners run out of money); and

- People – an heir with a purpose and the knowledge to realize their goals will likely benefit from having other people, which may include a professional advisor or family member, to help them spread and grow their mission.

By maintaining focus on these three areas, financial advisors can assist their clients in developing effective communication strategies to talk about money, designing a game plan to better prepare heirs for imminent wealth, and creating a genuine mission statement that is relevant to the family’s goals and core values.

These are services that might also help to retain clients during and after a wealth transition. While one might argue that keeping the family wealth within the firm would be reason enough for advisors to offer these services no matter what, these ‘services’ can also be offered as separate or add-on client experiences or even as client-appreciation-style events. Alternatively, designing and offering family meetings as a separate program can demonstrate to the client that this is an important process, but beyond the scope of traditional financial planning services.

Either way, it is important for the advisor and the client to acknowledge from the get-go that these conversations will take time and require expertise. Financial advisors interested in expanding into this area for the sake of their own firm’s longevity, because it is an additional service to offer (and charge for), or simply because it is interesting, will be better prepared if they take the time to consider how they might deliver these services as part of a current structure or, more likely, as part of a new service offering with additional fees.

Why Parents Worry About Too Much Inheritance, And Why Impact Is More Important Than Amount

All parents worry about their kids. As a new mom, I can attest to the fact that the word “worry” does little to fully explain my concerns. One common concern shared by many affluent parents is how their wealth transition will impact their children’s lives and aspirations.

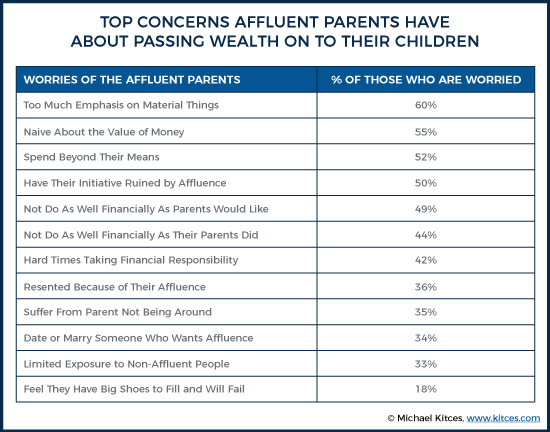

For example, in the 2007 XXVI US Trust Survey of Affluent Americans, which included individuals with an investable net worth greater than $5 million (excluding their primary residence), researchers found that 53% of the families surveyed were concerned about their wealth having a negative impact on their kids. A more recent study conducted by Withers LLP and Scorpio Partnership in 2014, which surveyed 3,000 families from around the world who were asked, “What is your greatest fear regarding your wealth and your family in the future?”, similarly found that families with net worth of $10 million or more expressed their largest fear, only second to health, was that their children would lack drive and ambition to get ahead.

In their book, “Preparing Heirs – Five Steps to a Successful Transition of Family Wealth and Values”, authors Roy Williams and Vic Preisser present data from the 2000 XIX US Trust Survey of Affluent Americans, noting that such fears were often based on over-emphasizing material things, not understanding the value of money, and relationships or expectations surrounding money.

Research has also made it very clear that these fears are real, and that excessive wealth really can be associated with unhappy and sometimes even tragic circumstances (even ending in suicide). One survey of wealthy individuals found that respondents were “generally dissatisfied” with their lives, often admitting that they had difficulty enjoying their wealth, and sometimes tended to take an excessive risk without the knowledge or know-how to handle the risk (e.g., entering into business ventures when they know nothing about running a business). Another research study examining middle school and high school students in wealthy families found higher tendencies for depression, substance abuse, and sexual promiscuity. Finally, wealth has also been correlated with high rates of eating disorders, cheating, and stealing among teens.

And research supports this idea that “affluenza”, in which young, wealthy people suffer from a lack of motivation and a sense of isolation, is associated with too many options that lead to “paralysis by analysis”.

“A very rich person should leave his kids enough to do anything but not enough to do nothing.” – Warren Buffett

“It’s not a favor to kids to have them have huge sums of wealth. It distorts anything they might do, creating their own path.” – Bill Gates

So is the answer, then, that a lot of wealth is good, just okay, or does it simply screw us up?

Leaning on work from the book Wealth in Families by Charles Collier, a famous researcher in the area of estate planning and wealth transfers, the answer appears to depend heavily on the manner in which families do (or do not) talk about money with their kids, the messages actually sent (and whether the communication is through words or inadvertently modeled through behaviors), and when they have these conversations.

In other words, in spite of these studies about the adverse effects of inheriting significant wealth, parents need not fear leaving an inheritance for their children, as research also shows that transferring wealth can be a positive experience if done correctly (which does not necessarily mean avoiding the transfer altogether or limiting the amount that is given). In fact, the “problems” of wealth seem to have less to do with the amount given, but more so from how the amount might impact motivation and aspiration… if the heirs aren’t prepared properly in advance.

For example, some families may discuss wealth with their future inheritors early on, where others may choose to wait until their children have the opportunity to “make it on their own first” before revealing the wealth they intend to bequeath – mirroring many of the fears uncovered by the 2000 XIX US Trust Survey of Affluent Americans.

Another example that Collier presents is how entrepreneurs and first-generation wealth-owners tend to give less to their children than old-wealth families because they wanted to “keep their kids hungry”. Others still, talk about wealth as a means to stop working. Which may sound like a luxury to some, but people with and without wealth alike ultimately need purpose, and many individuals find great purpose in their work – i.e. the opposite of affluenza.

Ultimately, the point is that the messages families send, and the manner in which they send them, have a large impact on children (potentially more so than the impact of the wealth itself). This is mirrored in a more recent vintage of the US Trust Surveys from 2016 that found how parents spoke to their kids about achievement, financial discipline, and work, sowed the seeds for success.

Wealth Transitions Fail From Poor Communication, Inadequate Preparation Of Heirs, And Lack Of Family Mission Statements

Even though we know that talking about money is good, we also know that actually having conversations about money is hard.

In fact, research by Roy Williams and Vic Preisser, who interviewed over 3,000 wealthy families in order to examine wealth transitions and how “unstructured” wealth transfers can have a potentially damaging impact on inheritors, found that just talking about wealth within families is very hard for most. Their work finds that wealth transitions generally fail (i.e., there is a loss of control over how assets are used, such as by heirs squandering the money), because of poor communication and trust, inadequately preparing heirs (also about communication), incorrectly understanding the impact of taxes and laws (communication about technical issues), and the lack of a (family) mission statement (more family communication).

Communication & Trust – It Starts At Home

According to Williams and Preisser, 60% of transition failures are a result of a breakdown in communication and trust between family members about their wealth. Yet, regardless of when or how families have conversations about money and wealth, it is undeniable that the place in which we learn about money, in large part, is at home.

People teach their children about money both directly, and often times more so, indirectly. Research on money scripts, the beliefs we have about money, and the financial practices we use is based on what we learn about money early on from our parents at home. Money scripts are, by definition, learned in childhood, passed down from generation to generation, and are typically subconscious. Moreover, breakdowns in communication in the home may stem from a person not being ready to hear, learn, or talk about their wealth, whether due to (lack of) age or maturity. Communication breakdowns may also stem from the parents simply not knowing how or when to talk about wealth.

Families included in Williams and Preisser’s research believed that they could speak directly and technically about wealth once a child reached ages 25 to 30. However, as financial planners know, this is often when many individuals unexpectedly gain access to their trusts or their inheritance for the first time (i.e., when parents reach the age that they are materially more likely to unexpectedly pass away). As such, by waiting until their children are older, families may lose the opportunity for the “good conversations” they intended to have to prepare their children for managing wealth.

Enter the first place advisors can help – parents are often scared to talk about money, but financial planners do it for a living! A client-appreciation-style event that is actually a class for parents about how to talk to their kids about money can be an enjoyable and effective way to introduce families to having money conversations. There can be games, food, family fun, and togetherness where parents and their children of varying ages can come together to talk about and interact with money in a non-threatening, non-stressful way.

Helping parents to learn how to talk to their kids, and even what to talk to their kids about, can give them the confidence they need to teach their kids about budgeting and developing good habits over time to manage money responsibly, as it is hard to budget effectively if you have never had to budget your entire life. In other words, even though there may not technically be a need to budget, the process can help young people understand the value of allocating resources responsibly.

Starting these conversations early also provides parents with the opportunity to model the behavior they wish for their children to emulate. Again, as part of a game-night, or money for the family event, financial advisors can help families individually or as a group practice healthy money habits. And this is important, because when families wait to have wealth conversations until their children are much older (e.g., in their 20s or 30s), children may perceive a disconnect between what their parents say they want them to do, and the behaviors they may (perhaps inaccurately) recall observing throughout their childhood, which can ultimately lead to financial distrust and dysfunction in the family.

Thus, financial advisors can be a great resource for their clients (even all of their clients at one time if structured as a client appreciation event) by creating an environment where the financial advisor (and even additional team members together) can demonstrate what it means to have healthy financial conversations.

As while the intention is not to suggest that a client is somehow messing up their kids’ futures or to imply anything about how they might be raising their children to be healthy stewards of wealth, normalizing and demonstrating healthy money conversations can be an easy way for advisors to get the ball rolling, perhaps even “sell” the other family meeting services and begin to open this door with clients, as those that show up to these events are probably prime candidates to try the family meeting services.

Preparing Heirs For Wealth And The Special Problems With “Sudden Money”

The second-largest roadblock to successful wealth transfers is having inadequately prepared the heir(s) to receive that wealth. William and Preisser’s study found that 25% of transition failures stemmed from poor preparation of heirs; in many of these instances, the issues were a direct extension of the prior poor communication and a lack of trust issues. Additionally, poorly formed estate documents or an incorrectly filed federal estate tax return may leave a wealthy family at a major loss.

Essentially, developing the knowledge and skill it takes to be a steward of one’s wealth is an ongoing process that takes a long time. Many wealthy parents (especially if they are first-generation wealthy) have spent a lifetime growing, learning, struggling, failing, learning more, and struggling again to get to where they are, and while their kids won’t necessarily have to face the same gauntlet, they also lose out on those lifetime opportunities to learn such lessons, and consequently may need additional coaching to learn how to manage their wealth successfully.

Moreover, preparing a child to receive an inheritance can often be planned; it is what happens once the inheritance is suddenly received that is often more difficult… where the time for heirs to learn those money lessons is compressed down to no time at all. Thus, those who do suddenly receive money do not always have the knowledge, and often the emotional understanding, to handle their new wealth in the most appropriate ways.

For example, stories about lottery winners or famous athletes going broke, losing vast sums of money, are common headlines in the news. In fact, this phenomenon of receiving wealth suddenly, and the slew of problems that comes with it, is so common that the term “sudden wealth syndrome” has been used to describe the situation. Within the field of financial planning, training programs like those offered by the Sudden Money Institute have been created to specifically address issues such as the emotional stress that may accompany the sudden transition into having wealth, and the new knowledge needed to actually manage the money.

Money Mission Statements – Words Matter

The third issue that can play a vital role in a successful wealth transfers has to do with words, where family mission statements can have a potentially tremendous impact on the success of a wealth transfer. Essentially, the motto provided by family mission statements gives families a way to talk about money, offering a touchstone to build trust, communicate, and establish methods to educate heirs about wealth.

This is supported by Williams and Preisser, whose work emphasizes the importance of having a family mission statement specific to wealth. In their work, they found that families with mission statements were more likely to retain control of assets within the family.

However, developing a money mission statement isn’t that simple – it’s not just simply penning something like, “Our money will be for the good of the world”. Instead, Williams and Preisser describe a money mission statement as “not just a goal…it is a declaration of the family…A mission is the long-term target, the goal, and the destination”. Here is one of many money mission statement examples offered in their book:

To strengthen our family and use its assets wisely; to enable our family and others to realize their fullest potential; to value and encourage love, work, self-sufficiency, and cooperation within the family and the larger community.

Ultimately, a successful family mission statement will take plenty of discussion, thoughtfulness, honesty, and time for a family to develop together, and also offers unique opportunities for advisors to provide a valuable service to their clients.

How Advisors Bring Value To Clients (And Their Own Practices) By Creating Money Missions (And Other Structures)

Summarizing work by Collier and again by Williams and Preisser, wealth appears to need three things if it is going to be transferred in a healthy and productive manner avoiding the issues of bad communication, inadequate preparation, and poor planning: Purpose, Practice, and People. All of which are areas where financial advisors can play an important role!

Wealth Needs A Purpose

In the 2018 Insights on Wealth and Worth Study, a study of 892 high net worth individuals (with $3 million or more in investable assets, not including their primary residence), found that only 47% of those interviewed had identified a Purpose for their wealth. Which could arguably suggest that roughly half of a given financial advisor’s clients may not have thought about the Purpose of their own wealth and how it will survive them, nor about the long-term impact they want their wealth to have on the world.

And perhaps not surprisingly, 49% of the interviewees also reported that they had not taken steps to use their wealth as they intended, supporting the findings of Williams and Preisser relating to the power of a mission statement and further suggesting the likelihood that many people have not thought at all, or at least not much, about putting together a money mission of their own.

So how might financial advisors develop new services for clients around wealth transitions? One way they can help clients identify the purpose of their wealth is through developing a money mission statement. This conversation is likely very easy to start if the firm has already started to provide “money conversation” training via client appreciation events. If they haven’t, advisors can still frame the conversation within a traditional financial planning meeting.

For example, an advisor meets with their client, John and Jane, and identifies that they are able (and wish) to leave an inheritance for their three children. The advisor asks, “Do you have a money mission statement?” It should come as no surprise if the client answers with one of the following responses: 1) We have no idea; 2) What is a money mission statement?; or 3) We have thoughts about what we want our kids to do with the money (e.g., education, financial freedom) but are not sure how to communicate these goals.

These responses are very common. Advisors can reassure their clients that their answers are normal, and that while parents often don’t know how to go about gifting wealth to their kids or having the discussion, there are strategies the advisor can help them implement to set up a good money mission statement.

How a financial advisor helps their client may vary (e.g., style, timing, outside resources), but there are some key elements identified in work by both Collier and by Williams and Preisser that advisors can consider:

- The meetings should (eventually) include everyone – sitting across from John and Jane talking about their money, the conversation and need for a mission will start with them, but you will eventually invite the whole family;

- The goals of the mission should focus on happiness for the family, but also each member individually;

- The outcomes of the mission should provide structure and tasks for the family, but also each member; and

- The moral of the mission should tell the world about this family, but also provide individual meaning.

In other words, the resulting mission and the meetings you have with the family (maybe yearly) related to the mission should elevate the family as a group, but also provide individual involvement.

Wealth Needs Practice

A mission statement can provide a valuable opportunity for family members to practice communicating about wealth, underscoring the idea that each individual matters – just as much as the family as a whole – to the mission.

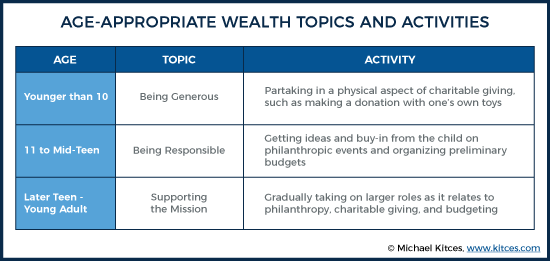

For instance, having set up the mission with the family, the financial advisor can facilitate ongoing healthy, age-appropriate conversations about wealth each year with the family. Some topic and activity examples are provided in the timetable below.

Money mission statements can also prompt family members to practice using wealth. For example, both Collier and Williams and Preisser mention the benefits for wealthy families of either starting a charity or participating in a charity by helping form and manage a budget related to the charity’s financial needs and situation.

Not surprisingly, because the problem identified with inherited wealth is usually more about the psychological and motivational aspects and less about actually using or running out of assets, basic financial skills are rarely taught to heirs-to-be. However, while some might argue that a wealthy beneficiary won’t really need to worry about saving the traditional 10% of their salary given their large inheritance, it is actually beneficial for children to see their money working for the causes identified in their money mission statements, and to learn about budgeting and the value of the dollar. So even if they don’t need to budget for themselves (because they’re not actually “financially constrained”), they can still learn how to budget for a charitable organization (that the family might help to establish and manage).

Perhaps most importantly is the opportunity for children to learn how to communicate about money with other people, so that by the time they come into their wealth, having practiced using money in a measured and thoughtful way, beneficiaries may be less likely to spend erratically or regret their wealth – two common fears and often realities of wealthy families.

The age-appropriate financial topics and activities mentioned above provide a safe and constructive outline for discussing money and practicing money management. For instance, a mid-teen involved with philanthropic events or charity work could be encouraged to research a new passion project, present that project to the board (including at least a rough budget), and then receive feedback and ideas from other family members and the financial advisor.

In these environments it is okay to make mistakes or not fully understand the proposed budget or actionable tasks – the point of these meetings is to encourage learning, which is very different from actually executing the project. Children are exposed to their wealth, get to interact with their wealth in a purposeful way, and practice communicating and using their wealth as it pertains to the family mission – not just to self-interests.

Wealth Needs People

Finally, managing and using wealth responsibly is easier with the help of other people. Referring back to the 2018 Insights on Wealth and Worth Study, the interviewees who had actually made (or felt they had made) greater progress toward their goals were often the ones working with a financial advisor!

In the 2007 US Trust study of Affluent Americans, interviewees were asked what or who they relied on to teach their kids about money – 27% answered financial advisors, ranking in 4th place. Though of the rest, 71% reported they taught their children themselves (which we know might not be so great), 53% said college (where personal finance is actually rarely taught outside of a finance degree), and 46% answered that they learned on their own (which is also probably not so great).

Moreover, even though the role of the financial advisor ranked 4th, the potential and opportunity for financial advisors in the development of a client’s financial skills and financial knowledge cannot be understated. Clients trust their advisor and need their guidance in these areas. While financial planners obviously know to introduce their clients to other trusted professionals as needed, this isn’t always obvious to the client.

In other words, recommendations and introductions by the financial planner matter a great deal, not just for the knowledge, but for the relational and emotional needs such as confidence that comes from a trusted recommendation. Just like referring a client to a CPA or estate planning attorney for their tax and estate plan needs, advisors can also refer clients to financial therapists or financial psychologists who can offer support with their family communication and emotional needs.

Before balking at that last statement about financial therapists and financial psychologists as a potentially uncomfortable recommendation for advisors, consider the following. When sitting in front of the client, again discussing the pros, cons, benefits, and costs of all the additional services that may be of value to the client, a list of recommended professionals can be presented to the client, which could include estate planners, CPAs, financial therapists, financial psychologists and legal mediators. Having each of these professionals included on the list and going through the list is one way to normalize the offer of bringing a financial therapist/psychologist to the meeting, giving the advisor a chance to explain what each of the different professionals do, the expenses of this type of professional, and why one or more by be beneficial at different times, at different meetings, working through different financial concerns.

In summary, regardless of who participates in the money mission meetings, it is critical to do two things. One, have a process for discussions and services that you want to offer (this first step will take some initial homework on the advisor’s part). Two, normalize the process and the offering. Again, clients might get nervous at the mention of “therapist”, “psychologist”, or even “attorney”, but if you let them know it is common and helpful to have these professionals involved as part of the process, explaining the purpose and role of each one, much of the worry about why they are in the room can fall away.

Creating A Money Mission Statement Process For Clients – Action Checklist and Resources

Here is a list of action items and considerations for creating a process for clients to develop a Money Mission Statement, normalizing it so they are comfortable doing it (with the advisor’s support!), and getting to know other relevant professionals who can assist in the process.

Step 1 – Creating a Money Mission Statement Process

- How many meetings each year would you want to have?

- 1 to 3 in the first year to get the mission established

- 1 to 2 a year moving forward to keep the mission alive and grow the roles of individual family members

- Note: The initial years will often rely heavily on the financial planner and other professionals to facilitate, teach, and run the meetings. However, as the family becomes accustomed to their roles, the meetings, and talking about/using their wealth in accordance with their mission statement, the financial advisor and other professionals may do less work as family members step up to take larger roles over time.

- What is the cost?

- Do you want to sell an all-expenses included experience?

- You know the cost of your services and the hourly rates of other professionals; a flat-fee can be offered to cover your expenses and those of other professionals involved.

- Do you want to list out separate charges for varying professionals?

- Clients might like the opportunity to pick and choose different professionals (and see their associated fees) as needed throughout the process, “a-la-carte” style.

- Do you want to sell an all-expenses included experience?

Step 2 – Marketing the Process

- Do you want to put on a client event or two structured around the idea of facilitating money conversations within the family?

- Do you want to design a one-page brochure that reviews the new offering and bring it up at all future annual meetings already on the books?

- Do you want to do both client events and develop a piece of marketing material?

Step 3 – Networking With Other Professionals

- If you haven’t already, attend a local meeting of the National Association of Estate Planners and Councils.

- This organization has a membership base of approximately 30,000 members, and oversees the Estate Law Specialist Board, accredited by the American Bar Association, and certifies attorneys as Estate Planning Law Specialists. You can meet Accredited Estate Planners and Estate Planning Law Specialists to find attorneys who are interested in doing this deeper, often more creative work.

- If you haven’t already, attend the Financial Therapy Association (FTA) conference and meet some financial therapists (in 2020 FTA will be co-locating with XYPN’s conference in Denver, CO – come check them out!)

- If you don’t have time for a conference, visit the website and find a financial therapist in your area on the Find an FT link.

- Interview a few FTs and find one that is into working in this area.

- If you can’t find any financial therapists in your area, you can also visit your state’s registry of mental health professionals and start making phone calls to meet with the ones who have relevant experience.

- Relevant experience may include: family counseling, financial coaching, mediation, couple’s counseling, group therapy, solution-focused therapy

- Get some training for yourself – some relevant certifications and training programs:

- Certified Financial Transitionist – Financial Transitionist Institute (training division of the Sudden Money Institute for financial professionals)

- Certified Financial Behavior Specialist – Financial Psychology Institute

- Accredited Estate Planners – National Association of Estate Planners and Councils

Advisors should take time in designing their process and keep in mind that, with more or varied individuals in the room, financial advisors themselves do not have to be the knower or the doer of all things. Advisors can let other professionals help with the heavy-lifting in areas where those professionals are most comfortable, leaving advisors to do what they do best.

There is no doubt that coordinating the logistics of a large inheritance for one’s children can be a stressful and complex process. However, advisors have the ability (and trust of their clients) to create a process that can actually alleviate their clients’ anxiety, potentially avoid financial transition failures, and prevent the loss of clients to a wealth transition in the first place.

What is more, thoughtfully and methodically designing wealth transition services, such as supporting clients in developing a money mission statement, not only sets an advisor’s firm aside (as these are not commonly seen services), it also allows the advisor to develop a plan that is, from a compensation standpoint, doable as well as profitable. Affluent clients in particular need their financial planners to do work in this area, and a plan that helps them establish an open dialogue about money with their family members will in turn help to create a structured environment under which they can more comfortably prepare children to receive their inheritance.

Advisors can guide their clients through the process of creating a money mission statement by addressing the key issues of purpose, practice, and people, and they can play a central role in their clients’ financial lives by helping them identify the core values and goals for their wealth that the entire family agrees upon. Furthermore, money mission statements and family meetings will serve as a valuable tool providing a long-term (and possibly even an inter-generational) framework for healthy communication habits about money and a basis for establishing sound money management practices that parents can model and teach to their children.

Summary of Resources

The following is a summary of resources that may be useful for advisors interested in developing money mission statement meetings with their clients:

- Professional Organizations (Networking, Training)

- Financial Transitionist Institute website – the training division of Sudden Money Institute, offers training for professionals working with clients going through major life events and issues the Certified Financial Transitionist (CeFT) designation.

- National Association of Estate Planners and Councils – offers specialization programs for attorneys to become Estate Planning Law Specialists (EPLS), or individuals in other disciplines (including financial planning, insurance, trust services, and accounting) to become Accredited Estate Planners (AEPs).

- Financial Therapy Association – consists of professionals from a variety of a disciplines aiming to grow the financial therapy profession, shape practice standards, and to promote academic research in financial therapy.

- Financial Psychology Institute – offers a training program for the Certified Financial Behavior Specialist designation, to help “financial and mental health professionals to work more effectively with clients.”

- Books

- Wealth in Families by Charles W. Collier – book that discusses intergenerational wealth transfers and the role of philanthropy in wealth planning.

- Preparing Heirs by Roy Williams and Vic Preisser – book that discusses family wealth transfers based on research by the authors on 3,250 wealthy families, organized around a five-step wealth transition plan.

- Previous Nerd’s Eye View Blog Posts

- Finding Your Own Money Story To Better Communicate With Clients

- Managing And Nurturing Clients Through The Lifecycle Of The Advisor-Client Relationship

- How The Human-to-Human Connection Helps Facilitate Positive Behavior Change

- Helping Clients To Switch Behavior By Directing The Rider, Motivating The Elephant, And Shaping The Path

- It’s Not Just About Telling Clients What To Do, It’s About Motivating Them To Do It!

If you’re a passionate closet writer who wants to be published but can’t find a way to do so, make each keystroke your way to wealth by penning your own blog. Starting a blog doesn’t require extensive technical skills but it’s important that you have expertise in the field you are writing on. This will attract visitors to your site. Building a large following will enable you to earn profit by luring advertisers, writing paid reviews or getting commissions for promoting other people’s products.

Great article! I’ll use part of this with the Legacy Lifeprint work I’m doing with donors/members of three nonprofits I’m assisting.

Fantastic and comprehensive article on this very important topic. I really appreciated the perspective that it is not the amount of wealth transferred but the impact that matters, and that has a lot to do with preparation of heirs. Much appreciated.

Very insightful, will take my time to read and learn from this. Thank you.

Thank you for this piece. What a great way to start 2020. A timely, visionary, practical, with applicable elements to bring to our clients. Love the idea of a monetary mission statement!