Executive Summary

Last fall, the Bipartisan Budget Act of 2015 changed the rules to eliminate two popular Social Security claiming strategies for married couples: File-and-Suspend, and Restricted Application.

Fortunately, the new rules didn’t take effect immediately, but the first transition – the elimination of File-and-Suspend – will apply for anyone who first requests for a voluntary suspension of benefits on April 30 or later. As a result, anyone who wants to be “grandfathered” under the old (current, and more favorable) rules has less than two weeks to complete their Social Security application and suspension request by the April 29 deadline!

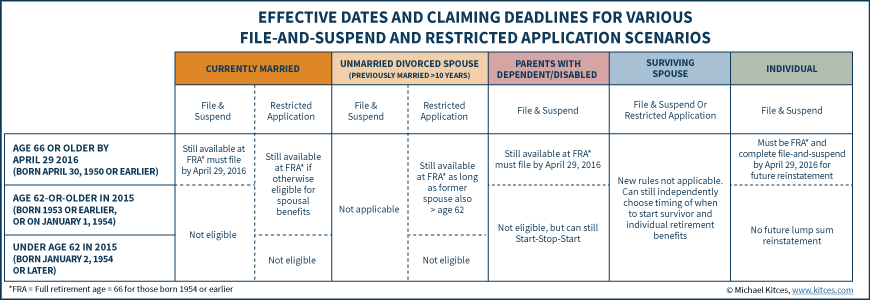

As a result, anyone who has at least met the full retirement age of 66, and is not yet age 70, should be considering whether to submit a file-and-suspend request by April 29. Notably, the tactic is a moot point for anyone who has already claimed benefits, or who doesn’t plan to delay benefits going forward. Nor is file-and-suspend relevant for widows (who don’t need file-and-suspend to coordinate between retirement and survivor benefits), nor for divorcees (who rely on the Restricted Application strategy instead, which remains available after April 29 for anyone who was born in 1953 or prior).

Nonetheless, for married couples (and some parents with children) who are in the age 66-70 window and have not yet claimed their benefits, but where one person could activate a spousal or dependent child benefit for someone else while delaying their own benefit, only a small time window remains to submit a File-and-Suspend request before the rules are changed forever! And arguably, anyone who is single and doesn’t care about spousal benefits, but simply wants to preserve the right to “undo” and reinstate their delay decision in the next few years, may want to consider submitting a request to File-and-Suspend by April 29 as well!

Understanding The Soon-To-End File-And-Suspend Rules

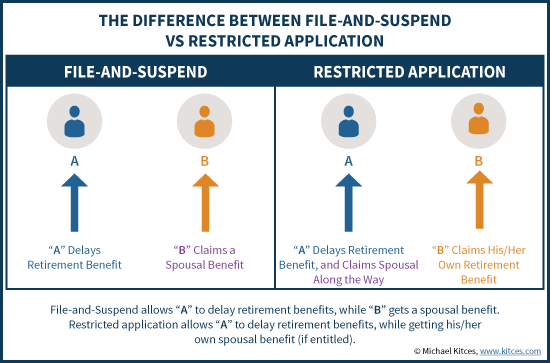

In order for a spouse to be entitled to Social Security spousal benefits, the primary worker – upon whose earnings that spousal benefit will be calculated – must himself/herself have filed for benefits as well. In the ‘traditional’ family unit, this meant that the wife couldn’t get access to her spousal benefit until her husband actually filed for his own. When he got his retirement benefits, she became entitled to spousal benefits based on his record (which she could then claim if she was eligible based on her own age).

This ‘unification’ of retirement and spousal benefits – where couples cannot get either until the primary worker files for benefits – was the case for most of Social Security’s history… up until the Senior Citizens Freedom To Work Act in 2000. This legislation introduced, for the first time, the concept of “voluntary suspension”, where someone could file for benefits, and then later choose to suspend them (after reaching full retirement age) in order to accrue delayed retirement credits from suspension until the maximum age 70.

While the original vision of voluntary suspension was for a worker who had started benefits early (e.g., at age 62) to change their mind later and stop benefits in order to go back to work (thus the “Freedom To Work” Act), in the years after the rule was enacted, commentators observed that voluntary suspension could happen immediately after someone filed, too. Of course, doing so would simply mean the worker would never get a single benefit check, but the advantage was that by filing, a spouse could become entitled to spousal benefits, while by immediately suspending, the original worker could still earn the maximum delayed retirement credits as well. It was a form of “have your cake, and eat it, too”.

However, Congress viewed this File-And-Suspend Social Security tactic as an unintended consequence and a “loophole” of the voluntary suspension rule, given that in the system’s original framework, which had existed for decades, entitlement to spousal benefits was always supposed to coincide with the workers’ own retirement benefit (not be a scenario where you can get one while delaying the other).

Accordingly, in the fall of 2015, Congress enacted as a part of the Bipartisan Budget Act of 2015 a new rule to effectively “kill” the File-And-Suspend strategy, by stating that effective April 30 of 2016, a worker’s decision to suspend retirement benefits will suspend all benefits based on that individual’s earnings history, including spousal (and dependent) benefits. While voluntary suspension remains, this change renders the File-And-Suspend tactic totally useless, as now suspending really will be the equivalent of just having not filed at all.

Notably, though, the new voluntary suspension rules under the Bipartisan Budget Act of 2015 apply only for those who try to (file-and-)suspend on or after April 30 of 2016. Which means there’s under two weeks remaining for anyone who wants to take advantage of the “old” rules to act, now, before it’s gone forever.

Who Should Consider File-And-Suspend By The Deadline?

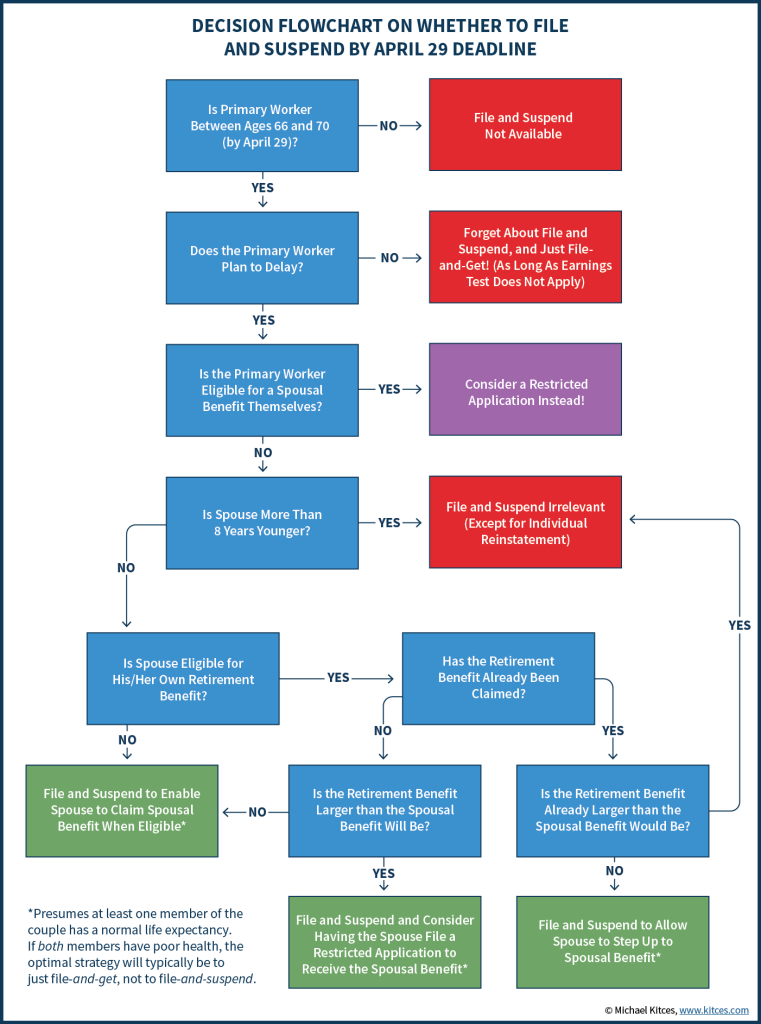

First and foremost, it’s crucial to recognize that file-and-suspend (or voluntary suspension in general) is only available for those who are full retirement age (currently age 66). Which means if the retiree isn’t already 66 (and/or won’t be turning 66 by April 29), then file-and-suspend is off the table anyway. Last year’s rule change took the option away before it was ever a chance.

Similarly, because the decision to file and suspend benefits is all about earning delayed retirement credits until age 70, it’s a moot point for anyone who is already age 70 or older (and would have started benefits already). In other words, the consideration of whether to engage in file-and-suspend by the deadline is only possibly relevant for those who are precisely between the ages of 66 and 70. (Notably, since Social Security allows a request for benefits to be filed up to 3 months ahead of when they will begin, there is some debate about whether an individual who turns 66 by July 29 could file and suspend by April 29th and be eligible under the “old” rules, since the filing happened in time, even though full retirement age hasn’t yet been reached. Given that the Social Security Administration has provided no guidance on this issue, it remains unclear what the outcome will be for anyone who tries this tactic by the deadline.)

In addition, the reality is that considering whether to file-and-suspend is only relevant for those who actually plan to delay benefits (and haven’t started already!), as otherwise the strategy is not to File-and-Suspend, but simply to File-and-Get benefits (which also makes the spouse entitled to any available spousal benefits, too), or to file a Restricted Application to claim their own spousal benefit (if the spouse already filed, themselves).

Nonetheless, for those who are between ages 66 and 70, have not started benefits, and plan to delay (and not claim a spousal benefit via a Restricted Application along the way), the opportunity to file and suspend before the April 29 should be considered, as there are several planning scenarios where it remains appealing.

Navigating The File-And-Suspend Deadline For Couples (And Parents)

To the extent that file-and-suspend is primarily about making a spouse (or dependent child) entitled to Social Security’s spousal or dependent benefits, married couples (and/or parents of minor children) have the most to gain by engaging in the file-and-suspend strategy before the deadline.

To actually be beneficial, though, at least one spouse needs to actually be in the age-66-to-age-70 window (where he/she could file and suspend in the first place), and the other spouse (who would claim the spousal benefit) needs to have a reason to claim a spousal benefit in the first place.

For instance, if the spouse had already claimed his/her own retirement benefits, that are higher than the spousal benefit, no spousal benefit will be paid either way, so there is no reason for a file-and-suspend (except to potentially preserve an individual reinstatement, as discussed in the next section). More generally, for file-and-suspend to be useful, the spouse needs to either not be eligible for his/her own retirement benefit, the retirement benefit needs to be smaller than the spousal benefit (such that accessing a spousal benefit would at least be a step up in benefits), or the spouse who has not-yet-filed needs to utilize the restricted application tactic themselves (filing for his/her spousal benefits at full retirement age, and switching to individual retirement benefits later).

Notably, the latter tactic is also irrelevant if the spouse is more than 4 years older, as by then he/she would have filed for individual retirement benefits anyway (making the opportunity for a restricted application a moot point). Similarly, if the spouse is more than 8 years younger, then file and suspend is also irrelevant to maximize a couple’s benefit, because by the time the spouse is eligible for a spousal benefit, the primary worker would have just filed for benefits already (even if delayed to age 70).

Beyond spousal benefits, file-and-suspend also remains relevant for a parent at full retirement age who has minor (or disabled) children in the household, and may be eligible for a dependent benefit as well as (or instead of) a spousal benefit. Once the (youngest) child reaches age 18, though, a dependent child’s benefit is no longer relevant (unless the child is permanently disabled).

In all these cases, though, it’s important to recognize that file-and-suspend is only appealing for a couple who otherwise wants to delay the primary worker’s Social Security benefit to age 70 in the first place, either to maximize his/her own benefit, or the survivor’s benefit. In a scenario where both spouses are unhealthy and are not likely to reach normal life expectancy, the optimal scenario is typically for both spouses to claim their own benefits as early as possible (which means the primary worker doesn’t file-and-suspend, he/she just files-and-gets benefits instead!).

File-And-Suspend For Individuals To Preserve Retroactive Reinstatement

While file-and-suspend is primarily about maximizing benefits for a couple, another indirect benefit of file-and-suspend is the opportunity for someone to change their mind after delaying and reinstatement benefits retroactively back to full retirement age.

The key to this strategy is that under the “normal” rules for Social Security, a request for retroactive benefits can only go backwards for up to 6 months’ worth of benefits. However, for someone who has previously filed-and-suspended, a request to reinstate benefits can go all the way back to the original date of suspension.

Thus, for instance, someone who was delayed Social Security benefits and then, at age 68, got news of an unfavorable health condition that would significantly curtail life expectancy (such that it was no longer beneficial to have delayed), a request for retroactive benefits could only claim the prior 6 months, but someone who had filed-and-suspended at full retirement age could request 24 months (2 years) of benefits in this case, going all the way back to that original age 66 suspension date.

As a result, individuals who don’t even have a spouse or dependent children may still wish to consider engaging in file-and-suspend before the April 29 deadline, just to preserve this option. Notably, though, doing so is only relevant if the person plans to delay benefits in the first place, and is between the ages of 66 and 70 (as age 66 is required to be eligible for file and suspend in the first place, and someone who is already beyond age 70 will have already filed for benefits anyway).

For those in the age window, though, this strategy remains relevant whether as an individual, or as a married couple where file-and-suspend is irrelevant. However, those considering the strategy should be aware of two caveats: 1) for a couple, engaging in file-and-suspend will also make that person ineligible to do their own restricted application for the other spouse’s benefit (which may actually be more appealing instead); and 2) for an individual or couple, the act of filing (to file-and-suspend) will enroll that person in Medicare Part A, which renders him/her ineligible to make any future contributions to a Health Savings Account (in the case that he/she was a participant in a high-deductible health plan and was otherwise eligible to begin with).

To take advantage of the tactic, though, it’s necessary to file and suspend by the April 29, 2016 deadline. For any file-and-suspend that occurs on April 30, 2016 or later, the subsequent opportunity for retroactive reinstatement is eliminated, under the new rules of the Bipartisan Budget Act of 2015. In other words, to preserve the ability to retroactively reinstate after the deadline, it’s necessary for the file-and-suspend to have occurred before the deadline.

File-And-Suspend Still Irrelevant For Those Who Are Divorced and/or Widowed

Because file-and-suspend is primarily about activating spousal benefits (or in certain cases, preserving the ability for a retroactive reinstatement of benefits), the strategy is generally irrelevant for those who are divorced or widowed.

Instead, the planning opportunity for widows is simply to coordinate the timing of individual retirement benefits and survivor benefits, which can already be done independently of one another. In general, the optimal strategy will simply be to claim the lower benefit as early as possible, and delay the larger benefit as late as possible (unless in poor health, and then the widow should simply claim any/every benefit as soon as they are eligible and won’t face a reduction due to the Earnings Test).

For divorcees, file-and-suspend also remains irrelevant, though restricted application is relevant, for those who want to claim an ex-spouse’s spousal benefit at full retirement age, and switch to their own benefit later. However, in the case of a restricted application, the changes under the Bipartisan Budget Act of 2015 are different; restricted application is automatically grandfathered for those born in 1953 or earlier (or on January 1st of 1954). As a result, anyone who is eligible based on their birth date will remain eligible going forward; the April 29 deadline is irrelevant.

Completing The File-And-Suspend Process Online By The April 29 Deadline

Notably, for those who do want to file-and-suspend by the April 29 deadline, there’s also the non-trivial matter of just executing the actual file-and-suspend claim in time. For many, this has proven to be more difficult than expected, due to widespread reports that local Social Security Administration offices are confused, and staff are undertrained, about how to process the requests. In some cases, those who are eligible for file-and-suspend being outright (and incorrectly) told they’re ineligible, despite a recent Social Security ‘emergency release’ trying to clarify the situation.

In addition, a potential glut of Social Security claiming requests, with the April 29 deadline looming, may also make it difficult for many retirees to even get a meeting in their local Social Security office in time.

Fortunately, though, it is possible to complete the file-and-suspend process using Social Security’s online system, which some are suggesting is the best course of action at this point, both to avoid the hassle of trying to schedule a local meeting, and the risk that the local Social Security Administration employee will be undertrained and unable to properly process the request in a timely manner.

To begin the process of filing online, go to the Social Security Administration’s “Retire Online” portal to submit the Social Security claim. The SSA even provides a 2-page visual guide on how to complete the application.

Unfortunately, though, while the application process to request to start of Social Security benefits is straightforward (and there is a box to check for those who want to file a restricted application for just spousal benefits), there is nothing in the online application process to indicate how to request the benefits be suspended (the key second part of a “file-and-suspend” strategy!). In order to make the request, Mary Beth Franklin advises to add a comment in the “Remarks” section towards the end of the online application, stating “I want to suspend my benefits”, and when the Social Security Administration’s main office processes the application, they will follow up by telephone to confirm the (immediate) voluntary suspension of benefits that completes the file-and-suspend process.

Alternatively, some advisory firms have partnered with third-party services that help to facilitate the online filing process, such as the $100 "Virtual Filing Service" provided by Social Security Advisors (which might be paid by the client, or offered as an add-on service by the financial advisor themselves!). In addition, those having trouble scheduling an appointment in time for the filing deadline can instead file a Form 795 - a Protective Filing Statement - to indicate their intention and (unsuccessful) attempt get an appointment in order to file-and-suspend by the April 29 deadline.

So what do you think? Are you doing any "last minute" File-and-Suspend applications for clients before the April 29 deadline? What planning and claiming scenarios have come up with your clients?