Executive Summary

Launching a financial planning firm is difficult. Not merely because of the cost and complexities of founding the business, and the challenge of getting new clients, but the opportunity cost of foregone income when you’re trying to build a practice and don’t have enough clients to be sustainable yet. In fact, for most advisors the “income gap” from when a practice is launched until it pays a livable wage can be many times the pure startup costs alone!

In the past, financial planners often bridged the gap by selling financial services products and taking the significant upfront commissions to round out their income in the early years. Yet in today’s environment, and especially in an advice-centric business, selling products for large commissions simply isn’t feasible or desirable… yet the lack of commissions and rising focus on fee-only firms ironically makes it even harder to bridge the gap successfully!

Fortunately, there are solutions, from doing hourly planning and offering standalone financial plans, to actually providing a limited amount of commission-based insurance solutions that clients actually need (and would have to pay for anyway), to easing into a practice by getting a job as an associate planner first or even getting a “side gig” to help make ends meet in the meantime. While these income gap fillers won’t necessarily fully resolve the issue – especially since the greatest challenge may simply be finding and getting clients in the first place – they can go a long way to at least partially bridging the gap and making it easier to survive the launch of a new firm!

The Opportunity Cost Of Foregone Salary When Starting Out As A Financial Planner

For a financial planner starting a firm, “the gap” is that space between when you start out as a financial planner, and when you actually have enough clients paying for (ongoing) financial planning to sustain yourself that way. And with most types of recurring revenue models, from Assets Under Management (AUM) to annual or monthly retainers, it can take several years to accumulate enough clients to achieve a stable base of business revenue, which means “the gap” can exist for years. In fact, for most new advisors, the gap is by far the single greatest “cost” in starting an advisory firm in the first place; startup costs for setting up an RIA can be as little as $10,000 or less, but the opportunity cost of years’ worth of foregone income (by not working in some other job/profession with more stable ongoing wages) can be huge, amounting to tens or even a few hundred thousand dollars!

The gap exists due to time it takes to build expertise, build trust, build relationships, build actual business, and accumulate sufficient number of clients, to actually get paid (and paid enough) for what you do. And while the gap has existed as long as financial planning itself, it’s notable that today’s financial planners are compelled to fill the gap in a very different manner than the founding generation of financial planners. For instance, in 1980 the average front-end load an investor paid for a mutual fund was 5.6%, and while costs started coming down since then by 1990 the average front-end load actually paid by an investor was still 3.9%. Which means in decades past, an investor with “just” $100,000 in investible assets would generate a roughly $4,000 - $5,000 commission, payable immediately and in full. By contrast, an advisor in today’s world operating as an RIA and charging a 1% AUM fee will generate a quarter fee of $250, and the first payment of that fee might not occur for another month or two until the next quarterly billing period!

Of course, it’s worth noting that the advisor of the past who was focused primarily on selling A-share upfront-commission mutual funds wasn’t necessarily trying to be a financial planner in the first place. And that’s actually part of the point; most of the first generation of financial planners didn’t actually start out as financial planners. They started out as insurance agents or mutual fund sales representatives, who sold their financial services products to make a living for many years. At some point down the road, either to deeper their business, expand their services, or simply to move away from a product-centric focus, they sought out education as a financial planner and began to adopt a more planner- and advice-centric approach to working with their clients.

Which means while today’s financial planners may be the second generation of planners, they are the first ones to enter financial services and try to start a financial planning practice from scratch on day 1. And in an environment where the large upfront commissions of old just aren’t feasible nor practical when delivering an advice-centric solution, today’s financial planners require entirely different approaches in trying to solve the income gap as a new financial planner starting out!

Side Hustles, Upfront Planning Fees, And Other Ways To Bridge The Income Gap

So how can a new financial planner bridge “the gap” when starting an advice-centric firm, where it’s not viable (nor desirable) to take on a product-centric focus? There are a few options…

Hourly Fees. If selling small ad-hoc financial services products as needed for upfront commissions was the gap-filler for the last generation of financial planners, selling ad-hoc hourly financial advice may be the primary gap-filler for the current generation. While long-term relationship-based clients (that generate recurring revenue) are important for the long-term health of most advisory businesses, not every consumer wants and needs a comprehensive relationship, and providing hourly as-needed advice fills a void for consumers and an income gap for new advisors.

Project Planning Fees. For some people, their needs go beyond “just” an hour or few of advice, and require a full comprehensive plan. Doing standalone plans for a $1,000 - $3,000 fee can go a long way to bridging the income gap. Such plans might be offered as an expanded solution for clients who need more than “just” an hourly solution, or as an additional (and separately priced) upfront service for clients who will eventually work with you on an ongoing basis (e.g., every AUM client will pay ongoing AUM fees, but also a $2,000 upfront planning fee, though be cautious that your upfront fees aren’t so high they discourage clients who would have more long-term value to the business by not charging so much upfront!).

Insurance Commissions. Notwithstanding the industry’s current swing towards fee-only financial planning, and the goal of starting an advice-centric firm, the reality is that many clients really do need various forms of insurance products, including term life insurance, disability income insurance, long-term care insurance, and even health insurance. Whether you intend to receive a commission or not, the end cost to the client is typically exactly the same, because these products are built with “distribution costs” (i.e., commissions) already embedded into the premium. So you can give your clients the insurance advice for free (or for a separate fee) and then send them to TermInsurance.com to buy it, or you can help them implement it directly. The cost to the client is the same, the only difference is whether you’re paid to help the client implement, or if you help them implement the solution and send the commission to TermInsurance.com. While some larger and established advisory firms decide “it’s not worth the trouble” to go this route, for a newer planner aiming to bridge the income gap (or even to sustain as part of an ongoing business model), that’s a non-trivial amount of business revenue to have the client purchase something they already need and that you were recommending to them anyway!

Start As A Paraplanner. Another option to bridge the income gap of starting a practice is simply to not actually start one from scratch right away in the first place; instead, check the job listings for a role as a paraplanner/associate planner in an existing firm and aim to do that for a period of years. With the job as a base, you can then either seek to build a client base in parallel to your job, or simply start to establish your professional network and build relationships with potential referrers who can send you clients in the future. A crucial caveat to this process: be certain the firm that hires you is on board with the plan! This is not only because working with “outside” clients must be disclosed to and generally overseen by the firm (for compliance purposes), but also because it’s important that your expectations about establishing clients is consistent with the goals of the firm. Some advisory firms are more than happy to have associate planners begin establishing their own clients and bring in revenue; other firms welcome all planners to get clients, but may impose the firm’s minimums (which could make getting new client impossible in practice); and a few firms specifically design their associate planner positions assuming the planner is fully committed to the firm and will not be doing outside activity as well. Better to get everything out in the open up front about what your long-term plans and intentions are and ensure there’s alignment with the firm, than follow a path that’s almost certain to burn a bridge in the future.

Get (Or Keep) A Side Hustle. For those who can’t find work as a paraplanner to make ends meet, the next alternative is to find some other work - a "side hustle" - to help bridge the income gap. Some will use skills from their prior profession on a freelance basis, or even keep an “old” job as they transition into financial planning (especially helpful sometimes for transitioning as a career changer into financial planning). The biggest caveat to this approach of getting a side hustle as a new financial advisor is that ultimately, it takes a lot of work to learn the skills, build the networks and relationships, and establish yourself as a financial planner, and this can be even harder if the job filling the income gap has no connection to financial services to at least be a partial stepping stone. Thus, ideally the “gap job” would/should be something related to financial planning and financial services in the first place, from consulting with other advisors, to providing outsourced support work or even doing intern work (something is better than nothing!), to doing freelance writing on financial planning/personal finance topics.

Of course, the caveat to almost all of these approaches is that you still need a process to get clients in the first place. The good news is that there are many paths, including lead-generation networks like NAPFA, Garrett Planning Network, or XY Planning Network (if your business model fits one of those platforms). For many of these gap-filling approaches, one of the best paths to new clients is simply building relationships with other (local) advisors whose businesses are bigger and may not be interested in working with “smaller” clients but are happy to refer it out to a trustworthy fellow advisor… especially one for whom those clients would be great for bridging the income gap and getting the business going.

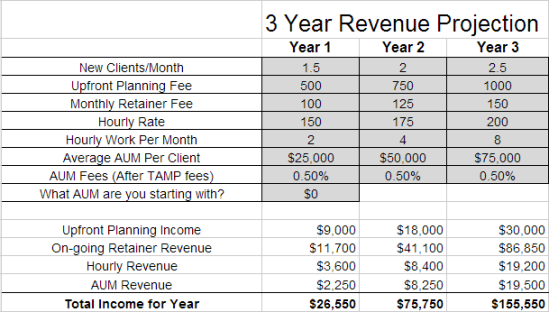

Ultimately, the reality is that most of these income-gap-filler strategies will only go “so far”, especially in the first year or two, because even with some lead generation and client referral opportunities, there are just only so many clients a new advisor can get. Nonetheless, building on this systematically over just a few years can quickly close the gap; for instance, just working with 1-2 new clients per month for a small monthly retainer fee and a modest upfront planning fee, and doing another 2 hours of hourly planning on the side, can quickly compound to more than $150,000/year of revenue in just 3 years (though obviously take-home income after business expenses will be lower), and the upfront and hourly "gap-filler" revenue can be as much as 20%-40% of revenue in the early years!

The bottom line, though, is simply this – if you’re looking to start a financial planning firm, recognize the challenge of the income gap early on, the opportunity cost it represents, and have a plan to tackle it. While the biggest constraint may simply be the pace at which new clients can be found, having a means to generate some additional revenue by finding more finite ways to work with clients in a limited engagement and get paid for it can go a long way to bridging the gap and growing the business to the point that it sustains itself.

So what do you think? How did you manage the income gap when you launched your advisory firm? If you’re still thinking about launching your firm, what’s your strategy to bridge the gap?

A couple of things I would point out for would be firm starters reading this. First, depending on location, 2 clients a month would be an amazing result by year two. Unless you have a a great network in place, do not underestimate the difficulty of getting clients. There is a reason why the insurance companies and wirehouses want you to have a list of 200 people before they would offer you a job. It is tough.

Secondly, even if you hit these projection targets, as Michael correctly points out, those figures are total income, not your net income. Don’t think, “Hey, I will be making $150k by year three.” Managing your cash flow and your expectations may be the diffrence between whether you “make it” or not as a new firm owner.

Finally, if you are considering your own firm. Keep reading this blog. It is a treasure to the financial planning community. Thanks Michael.

Scott,

Yes indeed, I’ve actually had many debates with Alan Moore about the feasibility of these new client numbers for newer advisors. I’m VERY cognizant of the challenges that new (and even experienced) advisors face getting an ongoing stream of “just” 1 client per month!

The caveat – and reason I think they’re feasible – is that for younger planners WHO AIM TO SERVE THEIR PEERS, there is SUCH an unmet need, so the market opportunity is enormous. We really do see members of our XY Planning Network drawing in this kind of client volume, through a combination of all the tools mentioned here – Find-An-Advisor tools like NAPFA, building relationships with other larger/established advisory firms who refer out “smaller” clients, etc.

This is certainly NOT a path to working with millionaires at this pace. But the under-age-45 moderate-to-high-income-but-no-assets group is astonishingly large and underserved. It will be harder to grow like this in another 5-10 years when more advisors are serving them and it’s more competitive!

– Michael

Having worked with dozens of start up firms now, bringing in 1-2 clients per month is about the average. Scott, I would agree with you if the firms are going after million dollar clients, and therefore have a lot of competition for their clients. The difference here is firms working with younger clients (.ie XY Planning Network members) means they are working with clients VERY few advisors are interested in. This also means the price point is lower (small clients) so the 1-2/month is necessary to get rolling.

So basically I’m just agreeing with Michael here… Or maybe he is just agreeing with me on this one 🙂

Hi guys! Decided to jump in on this 1-2 clients a month debate. After my first year in business I was at 17 ongoing clients plus 6 people that I had done projects work for or worked with them for a one time flat fee. To be fair, when I started my fees were WAY TOO LOW, but I knew that after my first 10 clients they would go up (I raised them after 5 clients). I knew that I would learn a ton from working with my first 10 clients and I have learned a ton! I have raised my fees multiple times in the last year and a half and I would say that Michael’s year 1 projection is actually eerily similar to how much money I actually grossed in year 1. (I’m hoping that year 2 looks similar as well!)

I would say that I’ve been surprised how much I’ve been able to earn from other income streams (side hustles as I like to call them) in additional to planning fees and AUM. I made a few thousand dollars my first year in freelance writing gigs. I also set up an account on https://clarity.fm/sophiabera after writing a guest post for you 🙂 because so many planners were reaching out to me about starting their own RIA. So now they can set up a call through Clarity and I’ve already made over $1,500 in 2014 just from that. (I owe you a beer, Michael).

Anyway, there are millions of upper middle class Americans that are making six figures and can afford to pay $100-$200 a month for a financial planner they just don’t know that we exist yet. They think they need $500k in an investment account before anyone will work with them. I think finding 1-2 of those people per month is doable.

My tips to find them are: get quoted in the media, start a blog, start a newsletter and send it out regularly, write guest posts, and network with other planners so that they can send you your ideal clients. Most of these tips are what everyone else has been doing online for years, as financial planners we’re just a little slow to catch on.

Hi There!

I couldn’t help but jump in here. Michael, this is a fabulous post that really hits the need to be creative with your practice from day one when starting out.

I’ve just officially wrapped on year 1 of Workable Wealth and similar to Sophia, have averaged 1.5 ongoing clients / month, have additional recurring revenue from writing, and other project income for media and speaking engagements, plus consulting on the side.

When I launched in 2013, I was actually completely candid with my then employer and phased out of my position at a local financial planning firm over 4 months which helped me to learn to really balance my priorities and time while supplementing my income.

My income numbers are unique because I’ve chosen not to do AUM, but have taken on additional project work. I’d say my client rate is similar to year one, fees have been bumped up over the past 12 months to those that Michael has listed in year 3, and the biggest lesson I’ve learned is how to guide prospects and clients through the thought process on making this investment of their time and money into a process that will give them clarity and peace of mind. (So the whole spend money to save money topic).

I agree with Sophia on tips to get the ball rolling when you’re focusing on building your practice: Establish a niche, use websites like HARO to get quoted, leverage forums like this one and XYPN to connect with other advisors, write a blog (consistently), send out a newsletter (consistently), and most of all – don’t be afraid to be different. Also, have an opt-in on your website. You want to capture the people who are landing on your homepage. No opt-ins = lost opportunity. Create a guide, e-book, checklist or some sort of paper that will provide value and prompt sign-ups.

Scott, I would agree with you. As I’m going into my second year of running my RIA, and having spoken with dozens of other planners in a similar situation, pulling in 1-2 clients per month in the first two years is definitely not the norm – some firms are struggling to have 2-4 clients by the end of their first year.

To be more realistic, I think the first year net income should be a break even at best, with a gradually increasing revenue stream. While some planners are achieving this income model, I don’t think it’s prudent to show this being the norm.

Having extra income streams definitely helps as it relieves a huge financial stress, and it can either be tapered off over time, or used to build a portfolio of income streams.

I concur that 1-2 for a new advisor may be high — especially if they don’t start business with a large network or think they don’t have a large network.

I also agree that it’s very good to keep another job while you’re starting out and that the job helps you or leads you to future clients.

What I see at times, is new advisors who start their business with a nest egg they’ve saved from other jobs. I’ve also seen those who don’t have a nest egg, start saving like crazy so that as they move towards their dream job as an advisor.

There is also a “needy vibe” that shines it’s head so clearly, when money has becomes a need. It happens whether we like it or not, whether we know it or not. Prospects feel the vibe because it comes out strong when speaking with them and causes them to run away.

There are other reasons, I noticed, when I used to work with new advisors and business owners, that holds them back from bringing in clients each month or at least each quarter — all things that can be rectified.

a) Wear too many hats: willing to let some tasks to be outsourced or managed by another.

b) Create a larger network: Many people don’t think they have a large network to call upon. Thomas Leonard, CFP, created a process called the Team 100. Write a list of all the professionals and business people you do know (and use), along with all family members. Use that list as a starting place.

c) Stop learning: Take what you know and use that in your business. If you’re going to learn, read various books on how million dollar financial advisors and consultants start and grow their businesses

d) Give prospecting time: Giving prospects the time they need to eventually turn into clients. Create a client engagement process and if you don’t have one, check out 7 Figure Advisors.

e) Create a niche: It’s probable that within that niche you won’t yet know who your ideal client is. But start out with a niche, based on who enjoy being around, a segment of the population who can afford you, and what you have in common with them and/or the services you really enjoy doing. (3 P’s: population, passion, product/service)

f) Take advice: Read the top people in your industry regarding investing, planning, and business management.

g) Follow your business and marketing plan: that’ helps advisors to pick 3-4 ways to market consistently and stops the usual spaghetti marketing taking place

h) Invest in the right things for your firm: Software, business cards, even a website on one page will help you manage your business and give you a heads up on marketing. Don’t spend money on like fancy new office furniture, expensive websites, etc.

I) Choose the name of your company wisely. Don’t name companies after yourself. That advice comes from the business brokers I’ve spoken to. I find that business owners in general change the name of their firm either in year 2 or 5 to align the business better with it’s consistent vision and mission.

Maria you say, “There is also a “needy vibe” that shines it’s head so clearly, when

money has becomes a need. It happens whether we like it or not, whether

we know it or not. Prospects feel the vibe because it comes out

strong when speaking with them and causes them to run away.”

Desperate people have desperate ways. I think that many in your industry would admit that once they do a bad thing and get away it, then giving in to the siren song gets easier and easier, i.e., doing bad things to get/collect (not earn) more and more money becomes the norm, and of course, those in the next cubicle/office or at the next desk get the virus too and away go the scruples. I suppose that it eventually infects the whole firm.

It is my hope that “the unsuspecting, inexperienced prospects” feel the vibe more often than they do now and become absolute runaways.

Fortunately I know not to answer people who hide behind photo’s and who don’t use their own names.

Agreed Maria. Any response we give this (?) simply validates his existence.

I find that rather comical, as you work in an industry where wolves masquerade as sheep and prey on those who they pretend to nurture and care about. From what I’ve read in financial “services” industry publications the financial “services” industry is one of the most opaque industries in the world.

I’ve given this some thought. I liken your industry to three other dark industries–the tobacco industry, the Catholic Church and the league of denial–the National Football League.

DAT,

If you feel this negatively about the industry, you’re welcome to move along, as it seems you don’t really have any interest in partaking in a productive conversation on this blog.

That aside, if you look around at the ongoing content and posts on this blog, I think you’ll find that what is espoused here is almost as negative on the “traditional” financial services industry as you are…

– Michael

And to that, Michael, I will say if you are not part of the solution, you are part of the problem. I strongly feel that if the out-of-sight, out-of-mind fee collection for financial advisors(ers)/brokers/1st,2nd,3rd,senior vice presidents/money managers/wealth managers/financial planners/financial counselors or whatever the latest word is for them were changed to an hourly wage with an itemized invoice, you would immediately eliminate many of the rotten apples from your industry.

Let me guess, you’re one of those “do-it-yourself” types? Hey, I’m happy for you. But realize that there are millions of Americans who need advice from a trusted financial planner/advisor and are willing to pay for it. Imagine that, we should actually be PAID for what we do, just like you pay to have your house painted or your plumbing fixed. Your posts reek of sour grapes and frankly they’re being aired on a forum for perhaps some of the industry’s best advisors who take the time to read Michael’s blog because we care for our clients and want to do the right thing. As an advisor who left a big firm with a salary and started my own practice, trust me, Michael’s blog on this topic is spot-on. I’m currently growing my practice and it’s not easy, yet I go to work every day thinking about how to work towards my client’s best interests. There are many times when I could take the easy road and sell some high commissioned product, but I don’t. I’ve sacrificed the higher payout for the good of my client relationships. I’ve done this all while having to rely largely on my wife’s income while I work my tail off to help support our young family. Your comments are honestly pretty offensive and are clearly written coming from the perspective of someone who doesn’t have a clue what he’s talking about, despite how long you’ve “researched” our industry.

To the contrary, I think and feel that I am spot on, as the information that I am reading is written by those in your industry. They are writing about themselves. I have come to believe like Jane Bryant Quinn–the only people that should have a “financial advisor” are very experienced, very sophisticated investors. There’s less asymmetrical information in that relationship. Of course, there may be a lot of “fake it until you make it” going on in your industry, but how is an inexperienced person supposed to figure that out. Once you figure one thing out, the industry has come up with something else to fool you. It’s the whack a mole thing. Unsuspecting, inexperienced folks must stay away, as trustworthiness in your “i can’t resist the siren song” industry is very, very hard to come by and the risk of having one’s lifelong, hard-earned savings used as a “financial advisor’s” piggy-bank is too great. You might say it’s a double whammy risk–risking one’s savings in the markets and risking one’s savings in the hands of a “can you trust him/her or not financial advisor.” And maybe you can trust him today, but what about tomorrow? What about after a financial meltdown when his salary is cut in half, but his expenses–mortgage, private school for several kids, keep up with the Jones’ lifestyle–stay the same or increase? Will he be able to resist the siren song? Desperate people have desperate ways.

The only fix for this huge trustworthiness problem, as I see it, is no more out-of-sight, out-of-mind fee collection. Fiduciary duty for brokers (RRs at B/Ds) isn’t going to cut it, as it doesn’t work for IARs at RIAs. The change must be in payment collection. It must be via 110% transparency–hourly wage, itemized invoice (show me what you did every 15 minutes just like an attorney) and payment via check, money order or credit card. If you aren’t comfortable telling your client/customer that information out loud and on an itemized invoice, then you haven’t earned it. I have no problem with people getting paid for the service rendered, but I want to see/experience the service and know the hourly wage. That way I can determine if it’s worth it or not.

You say, “I’m currently growing my practice and it’s not easy, yet I go to work

every day thinking about how to work towards my client’s best interests.” You have to think about how to work in your clients’ best interests? Is that not something that you just know?

You say, “There are many times when I could take the easy road and sell some

high commissioned product, but I don’t.” That is *never* okay for anyone in your industry to do. That’s the easy money. That’s the stealing from one’s so-called clients/customers. That’s the deception. That’s the client/customer working for you and not you for him/her. That’s the “I work in my best interest and what happens to my client/customer and his/her money doesn’t matter, because I need/want that money.”

You say, “I’ve sacrificed the higher

payout for the good of my client relationships. I’ve done this all

while having to rely largely on my wife’s income while I work my tail

off to help support our young family.” Everyone on the outside of your industry is doing this too. Your are not alone. Making a living, planning and supporting a family, saving money, starting a business–none of those things are easy for anyone, but one does it, and those with integrity do it without robbing one’s customers/clients. I can’t imagine anyone who would want a “financial advisor” who lacked integrity. I, however, feel that there is a huge shortage of integrity in the so-called financial “services” industry–Wall Street, banks–investment and commercial, firms, the whole shebang.

your complaints aren’t without merit. The problem is, you seem to be barking up the wrong tree. I’m a CFP professional, so I’m legally bound as a fiduciary to act within my clients’ best interests. The other thing you seem to be doing is assuming there aren’t bad people in every service industry. There are unscrupulous lawyers, doctors, plumbers, electricians, etc. Billing by the hour, invoicing every minute isn’t feasible for various reasons. First and foremost, I never want my clients to feel they don’t want to pick up the phone and call me because they’ll be billed. That’s largely how clients of lawyers and accountants tend to feel. Our profession is a bit of an art and science and a good portion of our job is to console clients in bad markets or during personal struggles they encounter – ie., divorce, death in the family, tragedy, etc. If a client calls me to share a concern about how they might fund their child’s college education after losing a spouse, should I send them a bill for the 45 minutes I spent with them on the phone?

I don’t have time to make this pretty, but I appreciate your reply and want to share what I think.

I don’t feel that there is any wrong tree. A local CFP went to a nursing home, picked up his client who suffers from dementia, took him to Best Buy, bought him a laptop computer, took him back to the nursing home, set him up for e-delivery (need I explain anymore) and then proceeded to excessively trade in his account(s) from 2005 until 2010. Unfortunately CFP has nothing, absolutely nothing to do with character. Will others who are unsuspecting and inexperienced realize that the CFP behind someone’s name may just be a disguise? That’s one of those whack a mole things. Bernie Madoff may have been a CFP or a CFA or a CPA but would that have mattered? No, the man was first and foremost a narcissistic sociopath. In terms of character what’s behind your name does not matter; it’s what is in your head–the connections in your brain–that matters. Unfortunately your industry does not keep (or may not even attract) Mother Teresa-types, and when you are dealing with people’s lifelong, hard-earned savings (which cannot be replaced–there is no second chance for those workers–they can’t work another 40 years to re-save that money) a Mother Teresa-type is exactly what people need and if you asked them, I believe that that is what they would say that they want. And I mean in terms of character–loads of integrity and very sincere and unquestionably trustworthy.

Yes, there are bad boys and girls in other industries and in professions, but your industry is *extremely* unique. In terms of RRs/BDs it is self-regulated via FINRA (per Larry Doyle’s In Bed With Wall Street FINRA arbitration is a kangaroo court) and in terms of IAR/RIAs it is purposefully under-regulated via the SEC (and Wall Street-Washington DC revolving door problem is massive here). You take bad plumbers, electricians, doctors, lawyers to court and that becomes public record. That’s huge. That’s transparent. Your industry locks things up tight and places them in the dark never to see the light of day again. That CFP that I spoke of at the beginning of this reply is still working. He is still touching people’s lifelong, hard-earned savings. Sure if you understand that brokercheck.org is where you go to look up your caring, nurturing, trusted “financial advisor,” you can see that he has a customer dispute that it was settled and that the firm paid $xxx,xxx. What you can’t find, however, is what he did, and that’s really what you need to know. You need to know what his character is. Is he a good boy or a bad boy? In this case, he’s a rotten boy with CFP behind his name. Rotten boys can get that CFP designation too. I feel, however, that the CFP board should be able to rip that CFP designation away from him. Maybe they did. I certainly hope so.

Also plumbers, electricians,and lawyers are compensated differently than so-called financial advisors/ers. They are compensated on a fee for service basis or an hourly basis. Doctors are paid differently, but it’s still they perform a service and then are paid a fee usually, but not always, via insurance. If one has no health insurance he/she may not go to the doctor when he/she should, but that is his/her decision to make.

Transparency is key. No out-of-sight, out-of-mind fee collection. NONE. Cut an invoice and show what you did every 15-20 minutes. Client sees the invoice, decides if the juice is worth the squeeze and pays via check, money order or credit card. Just making this change could save millions of investors from being harmed by their so-called financial advisor/er and his/her firm.

You are consoling clients to convince them to let you keep their money, because you are compensated based on assets under management. The amount of money you take home to pay bills and support your lifestyle is dependent upon the amount of assets they have with you. Correct? That is a huge conflict of interest, and believe it or not, your client may not comprehend that especially when you have developed a very caring, nurturing relationship with them. That’s a very dangerous position for a client. Very dangerous. Very vulnerable. Do I hear the siren song? Does the so-called financial advisor/er hear the siren song? Can he/she resist the siren song? The so-called financial advisor/ers ability to resist the siren song is dependent on many things–number of bills to pay, number of children, child support, alimony, mortgages, FA living above or below his/her means–where’s the yacht, the economy, financial “services” industry created/manufactured financial meltdown, etc., etc., etc.

I understand that you want to help your clients through divorces, deaths, etc., but do you have bona fide counseling skills? Have you been trained as a counselor? Again, I see this as a very, very dangerous thing. I do not feel that one’s so-called financial advisor/er, especially when collecting out-of-sight, out-of-mind fees, is the one to help one through a tragedy. Red flags are popping up in my head, but unfortunately red flags will NOT be popping up in your clients’ heads during times of tragedy. Clients will be in a very, very vulnerable state. I, again, hear the siren song. The so-called financial advisor/er will hear it too. Can he/she resist it this time? What’s going on in his/her life?

In answer to this question:

If a client calls me to share a concern about how they might fund their

child’s college education after losing a spouse, should I send them a

bill for the 45 minutes I spent with them on the phone?

Yes, you should send him/her a bill so that they know what they are paying for that service. Then, they can decide if the service was worth it. That’s how hourly rates works. It must be transparent.

You want to collect money for that 45 minute phone call via out-of-sight, out-of-mind fee collection. How does that client know what he/she paid for that 45 minute call? Does he/she not deserve to know what he/she paid for that 45 minute call? Counselors charge by the hour. Why should it be any different for “financial” counselors? Why do you want to hide the amount that you will collect for that 45 minute call? Are you wanting that client to think that you did that for free? That may just be what he/she will think and that is *wrong.* That’s just another way of cementing that trusting/caring relationship that you have with him/her. Client thinks: “Wow, he called me and talked to me for 45 minutes and didn’t charge me a thing for it. He’s wonderful.” I hear the siren song again.

We started in 2006 with eight client relationships, and added about six to eight clients a year thereafter. This year (2014) we have added more than ten, which is momentum, but that after eight years. It wasn’t until 2013 that we hit the revenue stability which Angie Herbers talks about in her white papers. My wife returned to work after the children were grown so I could do this. But, it has worked out well, we are grateful, and the two of us are headed into the best season of our lives.

Great article Michael. The very topic I’ve been debating about the past few weeks . Gives me lots to think about as an aspiring planner looking to transition from a FT corporate role.

Are these people incapable of getting a loan? That’s what other small business people do. And if one is unable to get a loan, one asks family members for help–you know, like Mom and Dad. And then there’s getting a second or even third job. Or then there’s putting the spouse or older children to work. Why is it that the so-called financial advisory/ery industry thinks that their slaves–oops I mean their so-called customers/client should fund all their expenses?

Pretty sure where the blog says “if you’re looking to start a financial planning firm, recognize the

challenge of the income gap early on, the opportunity cost it

represents, and have a plan to tackle it”, that getting a loan could be one of the steps in the plan. That said, how is getting a loan and paying it back through revenue generated from services provided to clients any different than what you’re miffed about? How is it different than any other start up business generating revenues with or without debt funding?

Transparency. Out-of-sight; out-of-mind fee collection. Do you *earn* it or do you just *collect* it? Do you understand what I’m getting at here? I have been reading about/studying your industry for about one year now, and I am flabbergasted.

And I think many, many, many others on the outside would be flabbergasted as well.

From a practical perspective, it’s often difficult to get bank financing for a startup advisory firm. Most of the “cost” for career changers coming into financial planning is foregone salary during the startup phase; the actual “hard cost” to start a firm is much more modest (see http://www.kitces.com/blog/setting-up-an-ria-and-starting-a-new-financial-planning-practice-on-less-than-10000/ ).

So when there’s no client base, no physical assets, and no other collateral, it’s pretty hard to get a startup loan. The only ones who can qualify for one generally have enough other income/assets to qualify for the loan, they don’t actually need it. :/

And one has to wonder how they got that money. Maybe their previous “clients/customers” should be considered shareholders of the new firm. You think?

From reading these comments you folks certainly must be a “I must live high on the hog” bunch. Others from the outside could certainly learn a lot from reading your industry’s blogs, publications, tweets, etc., but doing so also makes one want to puke.

0% credit cards. I’m serious. Finishing my first year as an RIA, on a great trajectory, and I’m happy to take banks’ money at 0% for personal expenses and also for business. My practice will be cash flow positive in calendar year 2014, and I reasonably expect income to continue to rise. I also had clients to bring with me from my previous job at another RIA (albeit with significant payments for the first two years under a noncompete). I must emphasize that the use of credit cards is something I planned very carefully and would not be for everyone. I have enough Roth money in retirement savings to pay off all my debt if I want to (with no tax or penalty as it would all be a return of contributions). I’d just rather use 0% money than withdraw from Roth and give up that tax-free growth.

Michael/Alan

Thanks to both you for the post & subsequent comments. Very informative and timely as I am in the process of making the very same difficult decisions. Even for someone who has been in the industry for a long time (non-producer capacity), I find it difficult to get a handle on how many of my existing clients will chose to follow me. Never mind getting the word out and begin acquiring brand new clients. I use an “industry” ratio of 10-3-1 in my projections. 10 contacts, 3 prospects, 1 client. Sounds reasonable?

Michael,

The 10-3-1 rule has been around for a very long time.

It’s still a pretty ‘decent’ rule of thumb, with the caveat that it’s usually 10 MEETINGS with people who could legitimate do business with you, for 3 bona fide prospects and 1 full client. Not merely 10 random contacts. Because if they’re loose connections and don’t tie to your business or target market, you can have 100 useless contacts and 0 prospects!

– Michael

Michael, this topic is very much on point for me. I am not currently in my own firm, but I am working for an existing firm which is not charging me rent, but taking a significant percentage of any income. That would be fine, but the existing RIA has not given me ANY marketing support. I am not even on the web site. I have to laugh at even 1 new client per month. And while I have sufficient means to not only deal with this, but even spend money on marketing, the issue is that I would be spending my money on marketing the RIA which benefits the owner much more than me. AND, I am trying to gain the work experience to use the CFP mark, so I am stuck for another few months.

Meanwhile, I am teaching in the CFP program at a local college and working with existing clients and attempting to attract some new ones. If I had to rely on my income, there is no way I could do it. But ultimately, when I can use the CFP mark in my marketing and deal with the marketing the firm situation, I am sure I will grow a decent practice. But if someone were to ask me how long it takes to be able to live on the income, I am now going to guess 5 to 7 years. Its just too long!

Hi David,

Five to seven years is about right. Have you considered venturing out on your own? Sounds as if you have, and are waiting to complete your experience qualifier for the CFP marks. Wishing you well.

Hi Randy,

Yes I have been thinking about what I will do when I can use the CFP Mark and starting my own RIA is something I’m thinking about. But then I will miss working with other people and while I am very knowledgeable, I would like to work somewhere there can be give and take with others in the office. People who have different expertise than myself and together we can provide clients a better experience.

David – this may be seen as a plug, but I’ll put it here anyway 🙂

As I finished the first year of running my RIA, I put together a book of what it was like. It reads like a diary and goes through various experiences of a new owner. You can get a sample here before you think about if you want to buy it: http://financeforteachers.com/freebook

Nothing like going through the experience without any of the risk?!

Hi David,

Perhaps you could team up with another CFP or two, and start your own firm. If I can help, or you simply want to talk shop, you are welcome to email or call.

Warm regards,

Randy

Thanks. I may take you up on that after February!

You are welcome to. Office number is 770.817.0525. Email is [email protected].

David – I was worried about the same thing when I launched by firm since I had always worked in offices with at least a few other advisors. Joining Garrett, ACP, or XYPN (depending on preferred business model) can provide a community of advisors that are working under a similar business model and it can really help make up for a lack of advisor interaction on a day-to-day basis. You can also form a study group of like-minded advisors, and that can give you the people to call when you need help, or just need some words of encouragement. As Seth Godin would say, you just need to find your Tribe.

I’d be curious to hear more about how prospects respond to a upfront fee and a monthly retainer. It seems a lot of prospects are still averse to paying a fee when they can get it done for “free” somewhere else. It’s going to take time for this shift in thinking to occur.

In my experience, the 45 and under crowd gives more push-back. Even the ones who have the means to pay.

We charge a planning fee as well as AUM. We don’t have a minimum asset level and some clients do not choose to have us manage their assets. The planning fee acts as a barrier to entry where we generally do not get clients with very low asset levels. But it is a struggle to get clients to pay the planning fee, although frankly the planning fee is not enough to pay for the time in doing the comprehensive plan. I work very hard on a comprehensive plan and I have to hope that I will have a chance to manage a client’s assets once the plan is completed.

Hi Daniel,

We charge an upfront fee, or planning fee, when onboarding new clients. We don’t refer to it as a planning fee, but rather an onboarding fee, which does include comprehensive planning. There is significant work involved getting a client set up in our systems, doing the planning work, coordinating details with other professionals, etc. Average age of client base is 52, though we have several clients in their 30’s and 40’s. So far, no push back from them. However, we do have fairly stringent guidelines for new clients, which guidelines aren’t related to income or assets.

Thanks, Michael. Agreed! Although I strongly suspect my definition of a “qualified prospect” will change over time as I am able to focus more and more on the “ideal” client for my practice. As everyone stated, the name of the game is to survive the first 18-24 months.

Michael, as a leader in your industry, I would like to see you lead the charge to end out-of-sight, out-of-mind fee collection. Are you up for that challenge? I honestly believe that that one change could save millions of investors from being harmed by their so-called financial advisors/ers. It’s not the total solution, but it is a huge start. Huge. I think that it would drive many of the bad and rotten apples out of the industry. They might go on to become fund managers, but from what I’m reading that bunch is a dying breed. Hallelujah.

It’s ironic how much financial planning needs to go into the inception of a financial planning firm. Still, it’s a useful skill and a valuable service. Your clients will probably appreciate how much financial planning it took just to get your business started. It’s a testament unto itself.

http://www.maddernfinancial.com.au

Michael, I started my fee-only firm in 2001 with 0 clients. There are a few of us who were fee-only from day 1, even back in the late 90’s. I bridged the gap by working for $25 / hour for an accounting firm doing taxes and doing comprehensive financial plans for $2k-$4k, as the first step in a long term planning relationship. It took about 1-2 years to get back to my prior wage income. I also had about 2 years of living expenses in savings, but I didn’t use it. With the current model of charging a monthly fee for planning, I think it’s a viable option if you combine that with a “side hussle,” as you call it. Personally, I think that doing tax returns was a great way to learn taxes and make some side money, and there are plenty of CPA firms that need help during tax season!

Great article. you explained it very well. Thank you for sharing. Please keep sharing more about Financial Goals For A Business!