Executive Summary

Major tax reform typically only occurs once every decade or few. But after a tumultuous series of negotiations in both the House and Senate, a final reconciled version of the Tax Cuts and Jobs Act of 2017 appears to be heading shortly to President Trump for signature.

The legislation will result in substantive tax reform for corporations, with the elimination of the AMT and consolidation down to a single 21% tax rate, all of which are permanent. However, when it comes to individuals, the new legislation is more of a series of cuts and tweaks, which arguably introduce more tax planning complexity for many, and will be subject to a(nother) infamous sunset provision after the year 2025.

Nonetheless, the new tax laws have a lot to like for individual households, almost all of whom will see a reduction of taxes in the coming years (though not after the 2025 sunset). While 7 tax brackets remain, most are decreased by a few percentage points (to a top rate of 37%), along with the repeal of the Pease limitation. The AMT remains, but its exemption is widened. Most common deductions remain, though they are more limited, and an expanded standard deduction means fewer will likely claim itemized deductions at all in the future. There is a new crackdown on the Kiddie Tax (subjected to trust tax rates instead of parents' tax rates), but a much wider range of families will benefit from a great expanded Child Tax Credit (with drastically higher income phaseouts). And a doubling of the estate tax exemption amount – to $11.2M for individuals, and $22.4M for couples with portability, will make estate tax planning irrelevant in 2018 and beyond for all but the wealthiest of ultra-HNW clients.

Of particular interest for financial advisors are a number of key provisions. The controversial rule that would have eliminated individual lot identification, and required all investors to use FIFO accounting, is out and not included in the final legislation. However, also out is the ability to deduct any miscellaneous itemized deductions subject to the 2% of AGI floor – which means all investment advisory fees will no longer be deductible starting in 2018. In addition, several popular Roth strategies will be curtailed by the repeal of recharacterizations of Roth conversions (although the backdoor Roth rules remain). And while the deduction for pass-through businesses remains in place in the final legislation, and may be appealing for “smaller” advisors whose total income is under the $157,500 for individuals (and $315,000 for married couples) threshold. Although for larger advisory firms, the service business treatment is so unappealing, that large RIAs may soon all convert to C corporations (or at least, become LLCs and partnerships taxed as corporations under the “Check The Box” rules).

Ultimately, the new tax rules are actually complex enough that it will likely take months or even years for all of the new tax strategies to emerge, from when it will (or won’t) make sense to convert to a pass-through business, to navigating the new tax brackets, and the emergence of strategies like “charitable lumping” to navigate a higher standard deduction. In the near term, though, most are simply focused on taking advantage of end-of-year tax planning… especially taking advantage of deductions in the next two weeks that may not be available after 2017 once the Tax Cuts and Jobs Act is signed into law.

On the “plus” side, though, at least ongoing tax complexity means there will continue to be value for tax planning advice?

For the original documentation of the Tax Cuts and Jobs Act:

- Final legislative text as enacted and supporting Conference Committee notes

- Legislative text of prior Senate GOP proposal

- Legislative text of prior House GOP proposal

GOP Tax Plan Summary Of TCJA

Over the past month, both the House GOP and Senate have put forth their respective proposals for tax reform – each of which passed with relatively narrow margins in their respective chambers, and both of which generated substantial controversy around key provisions. Leaving just a few weeks before the end of the year to reconcile the two in an effort to have President Trump sign the Tax Cuts and Jobs Act into law in 2017.

On Friday, December 15th, the final version of the legislative text was released, along with the supporting Conference Committee notes. In general, the final legislation followed the Senate’s version of the bill, incorporating a few of the House proposals, and often splitting the difference where there were gaps between the two.

Many of the most controversial provisions – such as the repeal of medical expense deductions – were left behind, but so were a number of areas of simplification (e.g., the House GOP’s consolidation of the various education tax credits).

Ultimately, the final legislation is still the most substantive layer of tax reform since President Bush’s tax cuts of 2001 and 2003. And similar to the last round of major tax law changes, includes a “sunset” provision that all of the individual tax law changes will lapse after the year 2025 (although the corporate tax law changes are permanent, as are the shift to using chained CPI for indexing tax brackets, and the repeal of the individual mandate). The sunset provision was necessary to meet the Byrd Rule requirement that only allows Senate legislation to be passed with a simple majority if it does not result in net tax cuts beyond a 10-year period (otherwise, it requires 60 votes to prevent a legislation-stopping filibuster).

Whether the legislation actually sunsets after 2025 or not remains anyone’s guess at this point. Republicans anticipate that they will eventually be able to make the rules permanent, if only because when the sunset is nigh, the “fiscal cliff” it creates may compel legislators to act at the time (which is how the sunset provisions of President Bush’s tax cuts were ultimately made permanent).

In the meantime, though, we have a new tax environment to deal with… albeit one that was not quite as “tax reformed” and simplified as originally hoped (particularly for individuals, which were more of ‘tax tweaks’ and less of ‘tax reform’ than the corporate side where AMT was repealed and the tax bracket was collapsed to a single 21% rate). Individuals will still face 7 tax brackets, on top of the Alternative Minimum Tax (AMT), and will still be able to claim most of their common deductions – although many deductions are more limited now, and with a higher standard deduction, far fewer will itemize at all.

In fact, the introduction of a 20% deduction for pass-through businesses arguably makes our tax future more complex than the past, as employees will be incentivized to shift to becoming independent contractor service businesses, even as larger service businesses do not benefit from the new rules at all and may feel compelled to convert to C corporations (or at least become partnerships or LLCs taxed as corporations).

In this summary of the GOP tax plan, we focus primarily on the new tax rules as they pertain to individuals and small business owners, from a discussion of the new tax brackets and rates, adjustments to deductions, reforms to AMT, the new deduction for pass-through businesses, and the expanded exemption of the estate tax.

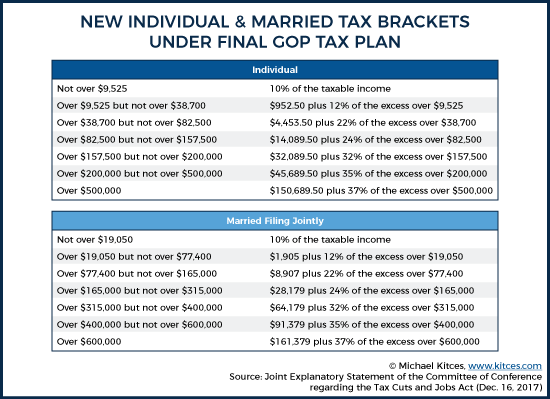

TCJA Tax Brackets Under The GOP Tax Plan

The original version of President Trump’s proposed tax brackets from the campaign trail in 2016 would have reduced our current 7 tax bracket structure down to only 3 brackets (12%, 25%, and 33%), while the House GOP Tax Plan would have come down to a 4-bracket structure with rates of 12%, 25%, 35%, and 39.6% (albeit with a 5th phase-out bracket of 45.6% for upper income individuals).

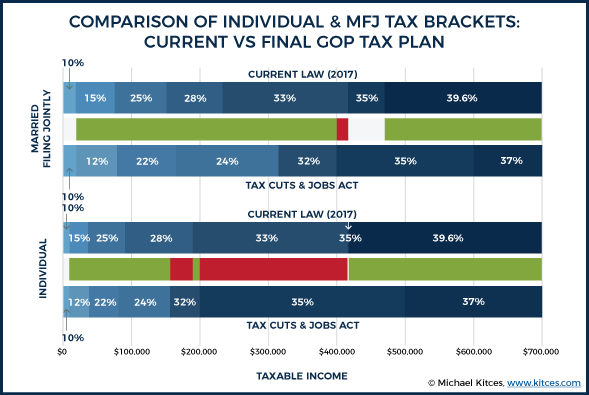

The final tax brackets under the GOP Tax Plan, though, followed the original Senate proposal, which retained our existing 7 tax brackets, and simply trimmed (most of) the tax brackets by a few points. In the end, the TCJA tax brackets will be 10%, 12%, 22%, 24%, 32%, 35%, and a top rate of 37%, and will remain in place until the end of 2025, when they will sunset.

The good news for most is that, relative to today’s tax brackets, the new TCJA tax brackets will produce at least a small reduction in marginal tax brackets for virtually all taxpayers, as while the 10% and 35% brackets remain as is, the other 5 tax brackets all received a 1% to 4% reduction in rates.

In the future, these tax brackets will continue to be adjusted for inflation, but after being set at these levels in 2018, adjustments occurring in 2019 and thereafter will use chained-CPI (also known as C-CPI-U), which many believe is a more accurate representation of inflation, but also tends to be slightly lower, and therefore would result in slightly lower inflation adjustments to the tax brackets in the future. In point of fact, this shift – that tax brackets in the future will adjust for chained-CPI instead of traditional CPI – is the primary reason why TCJA is projected to show a relative tax increase for individuals by 2027 (as by then, the new favorable tax brackets will have lapsed, but the new chained-CPI remains with lower tax bracket thresholds remains).

Pease Limitation Repealed

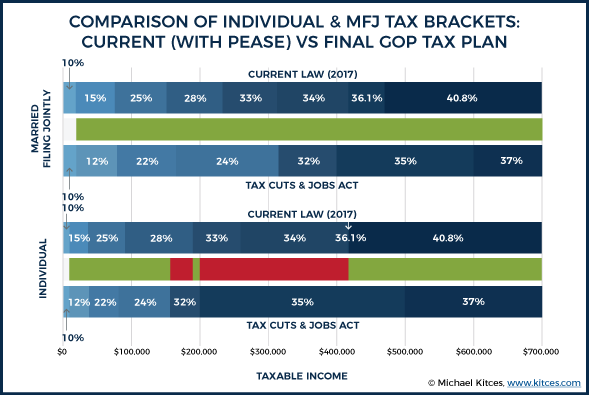

Beyond changes to just the tax brackets themselves, Section 11046 of TCJA repeals IRC Section 68, commonly known as the Pease limitation (named for the Senator who originated the rule). The Pease limitation phased out 3% of a taxpayer’s itemized deductions once income crossed a certain threshold (in 2017, those with more than $261,500 of AGI as individuals, or $313,800 as married couples).

Notably, while the Pease limitation was literally a phaseout of itemized deductions, because the magnitude of the phaseout was based on an individual’s income (not their deductions, as it was based on the amount of income over the threshold), the Pease limitation was effectively a 1% to 1.2% surtax for upper income individuals. Accordingly, the removal of the Pease limitation effectively provides a further reduction in marginal tax rates for upper-income individuals.

As with the individual tax brackets, the repeal of the Pease limitation sunsets after 2025 (i.e., the Pease limitation is scheduled to return in 2026).

Marriage Penalty For High-Income Couples

It’s also notable that while the earlier version of the Senate proposal would have eliminated the so-called “marriage penalty” by making all tax brackets for married couples double the threshold for individuals (to avoid the “penalty” of two high-income individuals paying more in taxes as a married couple than they would have as individuals), the final TCJA tax brackets bring back the marriage penalty for upper income individuals, by making the top 37% tax bracket kick in at $500k for individuals, but “only” $600k for married couples.

Example. Bradley and Angie each expect to have $500,000 of income (after all deductions) in 2018, and are planning on getting married. As individuals, neither of them would be in the top 37% tax bracket (which begins right at $500,000), and instead would have their income taxed at a blend of 10%, 12%, 22%, 24%, 32%, and slightly over half at 35%, producing a tax liability of $150,689.50 each (or $301,379 in taxes for their combined $1,000,000 of income). However, as a married couple, their joint income of $1,000,000 is subject to the new joint tax brackets, where everything above 37% is subject to 37% tax taxes, producing a tax liability of $309,379, or $8,000 higher than what the couple would have paid as two individuals.

The “good” news, at least, is that because all the lower brackets still have marriage penalty relief, and the new 35% tax bracket is so wide (for individuals, everything from $200,000 to $500,000 of income), the net impact of the upper-income marriage penalty is “just” shifting a large segment of income at the end that would have been taxed at 35% into the 37% bracket instead. Thus, even in the “worst case” scenario above, the net impact of the marriage penalty is only $8,000 (which is the last $400,000 of income [$200,000 each] between $600,000 and $1,000,000 of total couple’s income getting taxed at 37% instead of 35%).

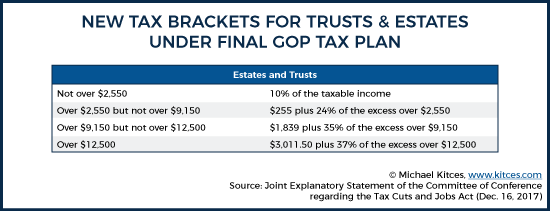

Simplified (And Lower) Tax Brackets For Estates And Trusts

While the final TCJA legislation kept the existing 7 tax bracket structure for individuals and couples, in the case of trusts and estates, the number of tax brackets actually is reduced (from the current 5 trust tax brackets, to just 4): 10%, 24%, 35%, and a top rate of 37%.

Of course, in practice the lower tax brackets for a trust or estate have limited impact, as the brackets are very “compressed” – it only takes $12,500 of income to reach the top 37% tax bracket, anyway. Which means for most trusts, the net result is simply a small tax cut of 2.6% (from 39.6% down to 37%) on the majority of trust income.

Kiddie Tax Now Subject To Trust Tax Rates

One significant but rarely discussed provision of the House GOP tax plan was a significant revamp of the Kiddie Tax rules, which were retained in the final version of TCJA.

Under current law, children (generally, those under age 19, or full-time students under age 24) are taxed at their own individual tax brackets for any earned income (i.e., from wages or self-employment), but their unearned income (i.e., portfolio income) above a modest threshold of just $2,100 (in 2017) is stacked on top of their parents’ income as reported on their own tax return (effectively taxing the child’s unearned income at their parents’ top marginal tax rates).

Under TCJA, though, the “allocable parental tax” (the additional taxes the child pays based on adding their income to their parents’ top marginal tax rates) is restructured. Instead of adding the child’s income to their parents’ tax brackets, the Kiddie Tax will instead be calculated by subjecting the child’s unearned income to the trust tax brackets – which, as noted earlier, have a top tax bracket of 37% on any income over $12,500.

For high-income individuals, this change will have little or no impact, as couples that had more than $400,000 of income were already in the 35% tax bracket (where the application of trust tax rates is only a 2% difference), and couples with more than $600,000 of income were already in the 37% bracket anyway.

However, for lower and middle income couples, the change may be more significant, as in the past a couple earning $120,000/year would have applied the Kiddie tax at their 25% tax bracket (which is only 22% under the new rules), but will now have all of the child’s unearned income over $12,500 taxed at 37%. On the other hand, it’s worth noting that, at today’s low interest rates, it actually takes a substantial portfolio (or perhaps a sizable inherited IRA, as post-death RMDs from an inherited IRA are also unearned income) to generate $12,500 of unearned income.

At an average yield of 3%, the child would need a portfolio of more than $400,000 to generate such income. For children with more modest levels of income, the new Kiddie Tax rules could actually result in a tax saving, as the first $2,550 of unearned income (over the initial $2,100 threshold) is taxed at just 10%, and the next $6,600 of income is taxed at only 24%. (Although significant capital gains would quickly be taxed at 20%, which is the top rate that applies to trusts over the $12,500 income threshold.)

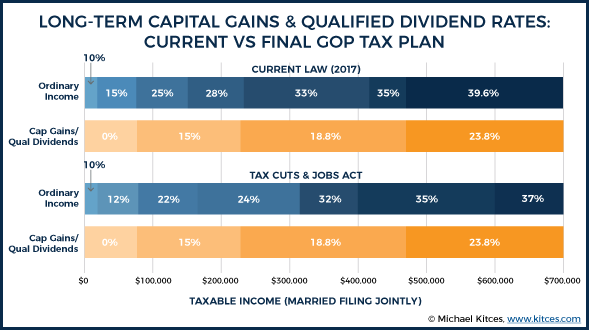

Capital Gains And Qualified Dividends Retain Old Thresholds Under TCJA

Under current (soon-to-be-prior) law, the thresholds for the 0%, 15%, and 20% long-term capital gains (and qualified dividend) rates are based on the thresholds for the individual tax brackets: those who fall in the 10% and 15% ordinary income brackets get 0% rates, while income in the 25%, 28%, 33%, or 35% brackets gets the 15% capital gains rate, and income in the top 39.6% bracket gets the 20% preferential rate. (In addition, the 3.8% Medicare surtax on Net Investment Income applies on top, producing a maximum capital gains rate of 23.8%.)

However, while the new TCJA rules introduce new tax brackets, and slightly re-draw the tax bracket thresholds, preferential rates for long-term capital gains and qualified dividends will continue to use the old thresholds. As a result, preferential capital gains and qualified dividend rates will no longer line up cleanly with the ordinary income tax brackets.

Instead, the 0% capital gains rate will end at $38,600 for individuals (and $77,200 for married couples), even though the bottom two tax brackets end at $38,700 and $77,400 (although it’s possible a future Technical Corrections act will re-align these).

More significantly, though, the transition from 15% to 20% capital gains rates will also continue to use the “old” top tax bracket thresholds of $425,800 for individuals and $479,000 for married couples – which would now fall in the middle of the new 35% brackets, rather than being aligned to the top 37% brackets. Even as the 3.8% Medicare surtax on net investment income will also continue to apply with its own not-indexed-for-inflation thresholds of $200,000 of AGI for individuals ($250,000 for married couples).

Merging Personal Exemptions Into An Expanded Standard Deduction

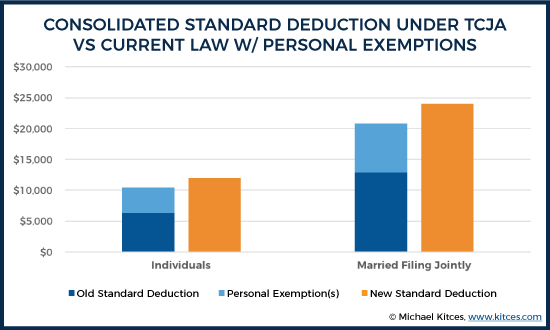

A key aspect of the tax reform proposals, going all the way back to President Trump’s proposals on the campaign trail, was a consolidation and expansion of the Standard Deduction and Personal Exemptions into a single, larger standard deduction. The final version of the GOP Tax Plan retains this proposed consolidation, by repealing Personal Exemptions (and thus the Personal Exemption Phaseout income surtax along with it) and increasing the Standard Deduction.

Under the new rules, the Standard Deduction will be $12,000 for individuals and $24,000 for married couples, as compared to just $6,350 for individuals and $12,700 for married couples under current law (in 2017). And the “additional standard deduction” amount (an extra $1,250 for a blind individual, or one over age 65) will continue to apply as well (although it would have been removed under the House GOP plan).

Notably, though, while these new Standard Deductions are higher, under current law individuals also received a $4,050 personal exemption (and married couples could claim $8,100) on top of their standard deduction, which means the new consolidated standard deduction is only a slight net increase, from $6,350 + $4,050 = $10,400 for individuals up to $12,000, and from $12,700 + $8,100 = $20,800 to $24,000 for married couples.

In fact, the expanded standard deduction alone won’t even be enough to make up for the loss of personal exemptions for families, which could have previously claimed a $4,050 (in 2017) personal exemption per family member. Which means a family of 5 would have had 5 x $4,050 = $20,250 of personal exemptions, plus a $12,700 standard deduction, for a total of $32,950 in deductions. Under the new law, the new standard deduction remains at just $24,000. In fact, even just adding one child – such that the family could have claimed 3 personal exemptions – leaves the family with a smaller deduction under the new rules than existed under prior/current law.

Expanded Child Tax Credit And Qualifying Dependent Credit

While the consolidated standard deduction may add up to less than the “old” standard deduction plus personal exemptions for families, in practice a related expansion of the Child Tax Credit will more than make up for this in most cases.

Specifically, under the new rules, the Child Tax Credit is expanded from $1,000 per qualifying child under the age of 17 (the proposal to increase the age threshold to under-18 did not survive in the final legislation), up to a Child Tax Credit of $2,000 per qualifying child (of which $1,400 is a refundable credit for those whose net tax liabilities would be more than zeroed out by the credit).

In addition, the income phaseout rules for the Child Tax Credit are dramatically increased, from the current thresholds of $75,000 for individuals and $110,000 for married couples, up to $200,000 for individuals and $400,000 for married couples. Although these thresholds are not indexed for inflation.

The net result of these new rules – especially given that the Child Tax Credit is a dollar-for-dollar credit – is a significant tax savings compared to the “losses” of not claiming additional Personal Exemptions.

Example. Raymond and Debra have two children, and a joint income of $150,000. Under current law, they are able to claim a $12,700 standard deduction, plus 4 personal exemptions (for Ray, Debra, and each child), providing a total deduction of $28,900, which they can claim against their 25% tax bracket, for a total tax savings of $7,225. However, they do not receive the Child Tax Credit at all, as it is already phased out at their income levels.

Under the new rules, the couple’s joint Standard Deduction would be “just” $24,000, instead of $28,900. However, the couple will now be eligible for 2 x $2,000 = $4,000 of child tax credits, which are not phased out at their income level. As a result, while they may pay $1,225 in additional taxes due to the loss of $4,900 of deductions (at their prior 25% rate), the addition of $4,000 in new child tax credits means their net tax liability is still reduced by $2,775!

Of course, for high-income families that are over $400,000 of AGI (for couples, or $200,000 for individuals), the Child Tax Credit is phased out. However, such high-income taxpayers were already mostly or fully phasing our their Personal Exemptions under current law, and as a result may still benefit from the expanded Standard Deduction (and eliminated personal exemptions).

Notably, the new rules also include a new $500 (nonrefundable) credit for dependents who are not “qualifying” children (i.e., dependents under age 17). This may include older (e.g., college-aged) children who are still claimed as dependents, and even dependent parents who are being cared for in the home. The new $500 qualifying dependent credit is also subject to the same (higher) income phaseout rules.

The expanded Child Tax Credit, along with the new $500 qualifying dependent credit, will sunset after 2025.

Limitations And Reforms To (Miscellaneous) Itemized Deductions

One of the most controversial aspects of the proposed tax reforms, especially the original House GOP version of the legislation, was the potential curtailment of a wide range of individual itemized deductions.

Notably, the reality is that technically itemized deductions are only used by a moderate subset of taxpayers – approximately 30%, according to the available IRS data. However, for those who do claim itemized deductions, they can be very substantial, both for high-income individuals (who claim significant deductions for state income taxes in particular), as well as those facing unusual and often unfortunate circumstances (from casualty losses to major medical expenses).

Ultimately, the final version of the GOP Tax Plan did not eliminate as many itemized deductions as first feared, but did curtail them more than some high-income (or at least, high-deduction) taxpayers may have hoped. In fact, when the more limited itemized deductions are combined with the expanded standard deduction, it’s anticipated that only a very small percentage of households will itemize deductions at all in the future.

Nonetheless, itemized deductions do remain – albeit subject to a series of new rules, which are discussed below.

$10,000 Cap On State & Local Income Tax & Property Tax Deductions

The original proposals for tax reform would have completely eliminated any deductions for taxes paid to a state or local government, including both state and local income taxes and local property taxes.

Given the wide range of income and property tax rates from state to state, the relative impact of this “State And Local Tax” (SALT) provision varied, and controversially was projected to have a disproportionate impact on “blue” Democrat states (as certain Democrat states like New York, California, and Maryland have some of the highest state income tax rates, and therefore the higher state income tax deductions). Which was objected to by not only Democrats from those states, but also Republicans from the subset of Republican counties in those states. As a result, the House GOP tax plan ultimately proposed a repeal of just the state income tax deduction, while retaining an up-to-$10,000 deduction for local property taxes.

In the final version of the Tax Cuts and Jobs Act of 2017, households will be given the option to deduct their combined state and local property and income taxes, but only up to a cap of $10,000. (Notably, it is a $10,000 limit on the combined total of property and income taxes, not $10,000 each!) The $10,000 limit applies for both individuals and married couples (an indirect marriage penalty for high-income couples), and is reduced to $5,000 for those who are married filing separately.

In addition, to prevent households from attempting to maximize their state and local tax deductions in 2017 (before the cap takes effect in 2018), the new rules explicitly stipulate that any 2018 state income taxes paid by the end of 2017 are not deductible in 2017 (and instead will be treated as having been paid at the end of 2018). However, this restriction applies only to the prepayment of income taxes (not to property taxes), and applies only to actual 2018 tax liabilities, which means it is still permissible to pay 4th quarter 2017 estimated taxes by the end of 2017 (and not in early January of 2018) to obtain the 2017 deduction. (And in point of fact, there wasn’t much existing authority to support deducting prepayments of income taxes for a future tax year, anyway.)

Mortgage Deduction Limited To $750,000 Of Principal & No Home Equity Indebtedness

The tax deduction for mortgage interest has been one of the most controversial in recent years. On the one hand, the tax deduction is viewed as an essential policy tool to make housing – and the dream of homeownership more affordable. On the other hand, the fact that it is a deduction means those who benefit the most are the highest income individuals (who claim the deduction at the highest marginal tax rates), while lower-income individuals most in need of assistance may not even itemize (and therefore get no benefit at all). Consequently, a recent NBER study found that mortgage interest deductions may have no net impact on homeownership rates in the long run (and at best just artificially increase housing prices).

Nonetheless, the mortgage interest deduction remains so popular, that curtailing it is very difficult. The original House GOP proposal would have limited the mortgage interest deduction to only the interest on the first $500,000 of debt principal (down from the current limit of $1,000,000), while eliminating the deduction for interest on home equity indebtedness.

The final Tax Cuts and Jobs Cut splits the difference, placing a new cap on mortgage interest deductibility on the first $750,000 of debt principal (so-called “acquisition indebtedness” used to acquire, build, or substantially improve a primary residence or designated second home). Notably, though, the lower limitation only applies to new mortgages taken out after December 15th of 2017; any existing mortgages retain their deductibility of interest on the first $1,000,000 of debt principal, and a refinance of such mortgages in the future will retain their $1,000,000 debt limit (but only for the remaining debt balance, and not any additional debt). In addition, any houses that were under a binding written contract by December 15th to close on a principal residence purchased by January 1st of 2018 (and actually close by April 1st) will also be grandfathered. The original House GOP proposal to limit mortgage interest deductibility to only the primary residence was not retained in the final legislation; instead, the rules continue to apply to both a primary residence and a designated second home.

On the other hand, the final GOP Tax Plan did retain the decision to eliminate deductibility for any home equity indebtedness altogether, and without any grandfathering for existing home equity indebtedness. After 2017, interest on home equity indebtedness simply will no longer be deductible, period.

Though it’s important to note that “home equity indebtedness” under IRC Section 163(h) is not based on whether the loan is actually a “home equity loan” or “home equity line of credit”. Instead, the determination of “home equity indebtedness” vs “acquisition indebtedness” is based on how the mortgage proceeds are used.

Specifically, “acquisition indebtedness” is a mortgage used to acquire, build, or substantially improve the primary residence; “home equity indebtedness” is money used for any other purpose (e.g., for personal spending, refinancing credit cards, paying for college, buying a car, etc.). Thus, a HELOC that is used to build an expansion on a house is still treated as acquisition indebtedness (as it was used for a substantial improvement), while a cash-out refinance of a traditional 30-year mortgage used to repay credit cards will be “home equity indebtedness” for the cash-out portion.

(Public) Charitable Contribution Limits Expanded

The standard rules for charitable contributions limit the deduction for cash donations to public charities (and private operating foundations) at 50% of the taxpayer’s AGI. However, under the Tax Cuts and Jobs Act of 2017, this 50% limit is expanded to 60%. Notably, this increase will not only make it easier for those who make substantial charitable contributions to claim a full deduction, but for those who previously made substantial gifts, may help to “release” existing carryforward deductions under the new higher limit.

On the other hand, it’s notable that TCJA will continue to require substantial documentation in order to claim deductions going forward. Specifically, current law generally requires that a charity provide (and the donor obtain) contemporaneous written acknowledgement of a charity for any donation of $250 or more (to substantiate not only the value of the donation, but also whether the charity provided any goods or services in return that would reduce the value of the deduction). A recent proposal under IRC Section 170(f)(8)(D) would have eliminated this requirement if the donee (i.e., charity) included documentation of donations when filing its own tax return, but the Treasury never issued final regulations on this provision, and TCJA repeals it. Thus, contemporaneous written documentation for gifts over $250 will continue to be required in the future.

Notably, a proposal under the House GOP plan that would have increased the charitable mileage rate was not included in the final legislation.

Temporarily Expanded Medical Expense Deductions For 2017 And 2018

One of the more controversial proposed limitations on itemized deductions under the House GOP legislation was the potential repeal of medical expense deductions, as part of the general overhaul of curtailing itemized deductions.

In the end, though, not only was the medical expense deduction not repealed or limited, it was actually temporarily expanded. Under the final Tax Cuts and Jobs Act, the 10%-of-AGI threshold for medical expense deductions is reduced to just 7.5% of AGI, both retroactively for the now-ending 2017 tax year, and the upcoming 2018 tax year. In addition, the medical expense threshold is adjusted to 7.5%-of-AGI for AMT purposes in 2017 and 2018 as well, ensuring that even AMT’ed taxpayer receive the benefit.

After 2018, the medical expense deduction reverts back to the 10%-of-AGI threshold.

Casualty Losses Now Limited To Federal Disaster Relief Areas

Under the existing IRC Section 165(c)(3), households may claim a deduction for major losses arising from fire, storm, shipwreck, theft, or similar casualties – with the caveats that deductible losses are only those in excess of $100 per casualty/theft, the losses are only deductible to the extent they are not compensated by insurance, and the losses overall are only deductible to the extent they exceed 10% of AGI. Nonetheless, for those who have major personal losses – e.g., the destruction of a home, car, or other personal property in a natural disaster – the casualty loss can provide material relief.

Under the Tax Cuts and Jobs Act, though, these deductions for “personal casualty losses” will be deductible only if the losses are attributable to a declared national disaster (under the terms of Section 401 of the Stafford Disaster Relief and Emergency Assistance Act), as occurred in situations like Hurricanes Katrina, Sandy, and Harvey. For those who are not in a Federal disaster area, though, casualty losses will no longer be deductible.

Investment Advisory Fee & Other Miscellaneous Itemized Deductions Repealed

When it comes to miscellaneous itemized deductions (particularly those subject to the 2%-of-AGI floor), the original House GOP proposal had proposed a crackdown on several common “miscellaneous itemized deductions”, including tax preparer (or tax prep software) expenses, and unreimbursed employee business expenses, while other popular deductions – most notably for financial advisors, the ability to deduct investment advisory fees – remained intact. By contrast, the Senate legislation proposed a simpler – but far harsher – change of simply repealing the category of miscellaneous itemized deductions entirely.

Ultimately, the Tax Cuts and Jobs Act went with the Senate proposal, repealing all miscellaneous itemized deductions that are otherwise subject to the 2%-of-AGI floor under IRC Section 67. This includes all tax preparation expenses, various unreimbursed employee business expenses (including the home office deduction), losses on a variable annuity (or losses below the non-deductible “basis” portion of an IRA or Roth IRA), and a wide range of “expense for the production of income” – including trustee’s and other fees paid on behalf of an IRA, safety deposit box fees, depreciation of home computers used for investments… and the deduction for investment advisory fees.

Notably, any expenses properly attributable to a bona fide business – either a business entity, or a sole proprietorship claimed on Schedule C – will remain deductible there, including everything from investment advisory fees (and tax preparation fees) attributable to business accounts, and the home office deduction (that is actually tied to a bona fide business the individual owns, and not just as an unreimbursed employee business expense).

Planning For 2017 & 2018 Investment Advisory Fees

For financial advisors in particular, the loss of the deduction for investment advisory fees will make it substantially more appealing to have IRAs and other retirement accounts pay their own advisory fees, as fees paid by an IRA are still permissible Section 212 expenses of the IRA, and fees paid from a pre-tax IRA are by definition 100% pre-tax (the equivalent of making those fees a deductible expense). However, it’s important to bear in mind the limitations of paying advisory fees from IRAs – in particular, that only investment advisory fees can be paid from an IRA (not financial planning fees), and that an IRA should only pay its own advisory fees (and not the fees for any other accounts, which can be treated as a taxable distribution or even a prohibited transaction). And of course, it will still be preferable to use outside dollars to pay the advisory fees for a Roth IRA (given that it’s not pre-tax money, which means there’s no tax benefit to using Roth dollars to pay fees).

As the 2017 tax year comes to a close, some financial advisors may also wish to accelerate invoicing and billing of advisory fees before the end of the year, specifically to allow clients to deduct their investment advisory fees in 2017 while still permitted. Notably, though, accelerating payments is a moot point for clients already subject to the AMT (or who will become subject to the AMT with a significant increase in investment advisory fee deductions). In addition, if a client prepays more than $1,200 in advisory fees more than 6 months in advance, the advisor is must make additional custody disclosures and provide an audited balance sheet of the business with Part 2 of Form ADV; as a result, even for financial advisors who wish to bill clients in advance before the end of the year, it will not likely be feasible or practical to bill more than the upcoming quarter or perhaps 1st half 2018 fees. And doing so will still require a plan and process to "true up" the actual advisory fee (based on those final quarter ends) versus the prepaid fee in advance, and may be challenging for most advisory firms simply because such in-advance billing would violate their existing advisory agreements (and a mass update of advisory agreements would be challenging before the end of the year).

On the other hand, it’s notable that going forward, financial advisor compensation paid via commissions – for which the cost is subtracted directly from the mutual fund, annuity, or other product’s internal expense ratios – effectively remains a pre-tax payment for clients, as those costs are netted directly against any taxable gains before commission-based products are liquidated or make distributions.

In other words, the repeal of the investment advisory fee deduction effectively puts RIAs at a tax disadvantage to commission-based advisors when working with clients. Will the loss of the investment advisory fee deduction set the stage for a future lobbying effort by financial advisors to make a unified tax deduction for investment advisory and financial planning fees (and/or finally permit both types to be paid directly from a retirement account)? Or alternatively, will advisory firms begin to create their own mutual fund or ETF products to manage their own strategies on a pooled basis, just to obtain the more favorable tax treatment for the deductibility of investment management fees?

Changes To 529 College Savings Plans & Other TCJA Educational Reforms

The original House GOP tax plan proposed a substantive overhaul of educational tax incentives, including the repeal of the Hope Scholarship and Lifetime Learning Credits (which would be consolidated into a slightly expanded American Opportunity Tax Credit), the end of new contributions to Coverdell Education Savings Accounts (which would be permitted to roll into 529 college savings plans), along with a repeal of the student loan interest deduction and the Savings Bond interest exclusion for higher education expenses. At the same time, the Senate version of TCJA would have eliminated the tax exclusion of tuition assistance for graduate and Ph.D. students, effectively making their tuition discounts taxable income.

Ultimately, the final version of the Tax Cuts and Jobs Act included none of these provisions. Instead, only a small subset of educational tax reforms remained in place, such as a provision stipulating that student loans discharged due to death or disability will no longer be treated as taxable income (although discharged student debt that is forgiven under other Federal programs like Income-Based Repayment [IBR], PAYE, or REPAYE remains taxable).

529 Plans For Private Schools & Homeschooling

While most of the originally proposed educational reforms under TCJA were not included in the final legislation, the new rules do change 529 college savings plan in several important ways.

First and foremost, 529 plan distributions can now be used tax-free for private elementary and secondary school expenses (for up to $10,000 in distributions per student each year), and includes both public, private, or religious schools.

In addition, tax-free 529 plan distributions will now be permitted to cover homeschooling expenses as well. Specifically, the following homeschooling-related expenses will now be treated as eligible education expenses: curriculum and curricular materials; books or other instructional materials; online educational materials; tuition for (non-related) tutors or educational classes outside the home; dual enrollment in an institution of higher education; and educational therapies for students with disabilities. Notably, the $10,000-per-student annual limit will also apply to homeschooling expenses. (Michael's Note: After initial agreement on the "final" legislation, an adjustment due to the Byrd Rule resulted in the homeschooling provision being eliminated from the Tax Cuts and Jobs Act. As a result, only the expansion of 529 plan distributions for private elementary and secondary school expenses remains.)

Ultimately, these changes to 529 college savings plans make them even more competitive as an alternative to Coverdell Education Savings Accounts. In the past, the decision of Coverdell vs 529 plan was primarily about funding college (529 plan) vs elementary/secondary school (Coverdell), but this is largely a moot point under the new rules. Technically 529 plans are still more limited for elementary/secondary school expenses due to the $10,000 annual limit for a student, but Coverdell accounts often can’t fund much more than this anyway due to their $2,000 upfront contribution limit.

On the other hand, it’s also worth noting that because the new IRC Section 529(c)(7) redefines “qualified higher education expenses” to include homeschooling expenses, and IRC Section 530(b)(2)(A)(i) stipulates that tax-free Coverdell distributions are available for “qualified higher education expenses” as defined in IRC Section 529, the new homeschooling provisions effectively apply to Coverdell accounts as well. Which may be appealing for parents who already have dollars in Coverdell Education Savings Accounts that haven’t been used because they decided to homeschool their children.

Refinements To 529A ABLE Accounts

In addition to the changes to 529 college savings plans, the final TCJA legislation also makes a few adjustments to 529A plans – also known as ABLE accounts, which provide tax-free distributions for disabled beneficiaries.

Specifically, the new rules permit money in a 529 plan to be rolled over to a 529A ABLE account (without any non-qualified distribution penalties), as long as the 529A beneficiary is the same person (or a member of the same family) as the original 529 plan account.

However, even rollovers from 529 plans to 529A ABLE accounts will still be restricted to (and count towards) the annual contribution limit for ABLE accounts, which is the annual gift exclusion (rising to $15,000/year in 2018). Thus, large 529 plan balances may take years (or even decades) to slowly siphon off to a 529A plan if the child becomes disabled after accumulating significant college savings. And rollovers from a 529 plan to a 529A ABLE account will cap out the contribution limit for the beneficiary (effectively blocking anyone else from adding further dollars to the account that year).

On the other hand, even if the annual contribution limit to the 529A ABLE account is capped out, the designated beneficiary themselves may be able to make an additional contribution, under a separate new provision of TCJA. Specifically, the new rules stipulate that the beneficiary may contribute to their 529A account, above and beyond the normal contribution limit, if they have earned income from employment. The maximum amount of employment income that can be contributed is the lesser of 100% of their compensation, or the Federal poverty line threshold for a one-person household (which is $12,060 in 2018). In addition, the beneficiary must not also be contributing to an employer retirement plan (e.g., a 401(k), 403(b), or 457(b) plan) to be permitted to contribute their income to a 529A plan.

In addition, if the designated beneficiary of the ABLE Account themselves is the one who actually makes the contributions, he/she will now be able to claim the Saver’s Credit as well (which is normally only available for contributions to retirement accounts, but is being expanded to ABLE accounts).

Alternative Minimum Tax Exposure Reduced With Expanded AMT Exemption Amount

One of the big goals from the earliest stages of tax reform – going back to President Trump’s tax proposals, and the original GOP reform template from 2016 – was the repeal of the Alternative Minimum Tax. Although in practice, the primary means of accomplishing AMT “repeal” under most reform proposals was simply to eliminate most common deductions, and reduce the tax brackets (the original top rate would have been only 33%) – effectively making the regular tax system so similar to the AMT, there would be no more AMT.

However, given that the final TCJA legislation ended out keeping a substantial number of individual deductions (some of which are currently AMT adjustments), and did not reduce the tax brackets nearly as far as first proposed. As a result, the AMT was not quashed out automatically in the changes, and given the pressure on keeping the legislation within its budget target, the AMT was not able to be fully repealed.

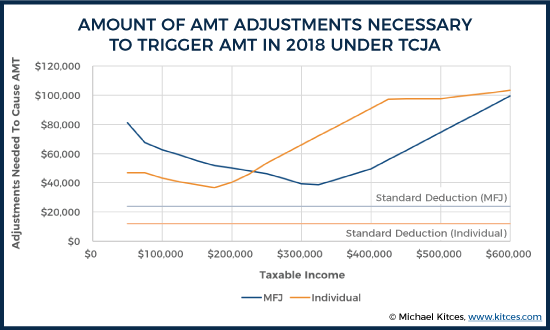

Nonetheless, the scope of the AMT was dramatically altered under the final legislation. Specifically, the new rules increase the AMT exemption from what would have been $55,400 for individuals and $86,200 for married couples, up to $70,300 and $109,400, respectively. In addition, the phaseout of the AMT exemption – which effectively creates a “bump zone” where the otherwise-top-AMT-rate of 28% rises as high as 35% - is also adjusted substantially higher, from a threshold of $123,100 for individuals and $164,100 for married couples, up to a whopping $500,000 for individuals and $1,000,000 for married couples.

The end result of these changes – an increased threshold for the AMT exemption phaseout, along with a higher AMT exemption amount itself – is that while today the AMT commonly impacted those around $150,000 to $600,000 of income, in the future AMT exposure will be much smaller, and it will be extremely difficult to be impacted at all, especially given more limited deductions.

For instance, the chart below shows the amount of AMT adjustment items that individuals and/or married couples would have to have, in order to be subject to the AMT. Notably, the standard deduction – which is not deductible for AMT purposes – is only $12,000 for individuals and $24,000 for married couples, which is far less than what it would take to trigger the AMT. Similarly, for those who itemize, a $10,000 cap on state and local tax deductions means no more than $10,000 of AMT adjustments, and the loss of miscellaneous itemized deductions means those cannot be added back for AMT purposes, either. In essence, short of very large AMT adjustments – e.g., the bargain element of an Incentive Stock Option – it will be difficult for virtually anyone to be subject to the AMT in the future.

An added benefit of the expanded AMT exemption (when combined with the higher AMT exemption phaseouts) is that many people who in the past were impacted by the AMT and generated a Minimum Tax Credit (e.g., for exercising Incentive Stock Options) but couldn’t actually use the MTC (because they continued to be subject to the AMT every year) will finally be able to use most/all of their AMT credits. Because a higher AMT exemption – and a bigger gap between the household’s regular and AMT tax liabilities – provides more room to claim those carryforward MTCs.

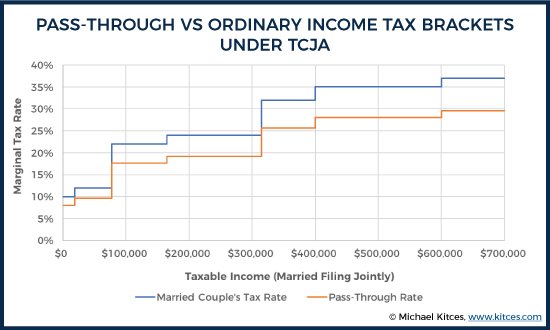

New “Qualified Business Income” 20% Deduction For Pass-Through Entities

One of the most controversial provisions of the new Tax Cuts and Jobs Act is the rule that will allow pass-through business entities (e.g., partnerships, LLCs, or S corporations) to benefit from a lower tax rate. The original house GOP version would have simply taxed pass-through income at a maximum rate of just 25% (as opposed to top ordinary income tax brackets). The Senate version was different, and instead granted a 23% deduction against pass-through business income, essentially reducing the marginal tax rate by 23% of its rate. Thus, the top tax rate on business income is 37% but would be reduced by 23% of 37%, which amounts to a 28.5% rate. Lower tax brackets would have been similarly reduced by the deduction.

The final legislation adopted the Senate version in a new IRC Section 199A, but adjusted the deduction to 20% (down from 23%) for so-called “Qualified Business Income” (QBI). Which means in practice pass-through businesses will be taxed on only 80% of their pass-through income (or alternatively, will effectively be taxed at only 80% of the normal tax bracket rate on all their business income).

Notably, “pass-through businesses” include partnerships and LLCs, S corporations, and sole proprietorships filing Schedule C. And while the deduction is claimed for pass-through business income, it will be claimed on the individual’s personal tax return. However, the final legislation explicitly notes that the deduction will not be an above-the-line deduction in computing AGI, and instead will be a below-the-line deduction (though also not an itemized deduction, so it can be claimed even for those who claim the standard deduction).

However, the new rules permitting deductions for pass-through businesses have a number of restrictions in place, intended to prevent business owners who do substantive work in the business from reclassifying their wages (i.e., labor income) as business income eligible for the pass-through rate. The restrictions are also intended to limit the appeal of employees trying to leave their firms, and then contract back to their prior companies via a pass-through entity, in an effort to reclassify their wage income as pass-through business income.

First and foremost, the rules explicitly state that any type of investment income from a pass-through business is not eligible for the Qualified Business Income deduction (nor is any income attributable to foreign business activity). In addition, Qualified Business Income (eligible for the deduction) does not include “reasonable compensation” to an S corporation owner-employee (which, similar to the rules for FICA taxes on S corp owner-employees, prevents them from under-paying themselves on salary in an effort to minimize their tax liabilities). Similarly, QBI does not include any guarantee payment for services in a partnership or LLC.

Second, the rules limit the QBI deduction to the lesser of 20% of its business income or 50% of the total wages paid by the business to its employees. Thus, a high-income business that has very few employees (e.g., a firm making $5M of revenue and $3M of profits that pays only $1M to a handful of employees) might have its deduction limited to only 50% of its payroll (in this case, a $500k deduction for 50% of payroll, instead of a $600k deduction for 20% of its profits). For capital-intensive businesses with very few employees (e.g., real estate investors, factory/machinery-intensive businesses), a last-minute addition to the final legislation (which was not included in either the original House or Senate versions) gives an alternative wage limit, which is 25% of W-2 wages plus 2.5% of the unadjusted basis of depreciable property (e.g., equipment and machinery, or even real estate). Notably, though, these wage limits to the QBI deduction apply only if the taxpayer’s own taxable income (not AGI, but taxable income after deductions) exceeds a threshold of $157,500 for individuals or $315,000 for married couples (which is down from $250,000 and $500,000, respectively, in the original Senate version, and now aligns to the top of the new 24% tax brackets).

Third, and of importance for financial advisors in particular, the QBI deduction does not apply to “specified service” businesses – which under IRC Section 1202(e)(3)(A) includes those performing services in various professional fields, including health, law, accounting, actuarial sciences, performing arts, consulting, athletics, financial services, or any other trade or business where the principal asset of the business is the reputation or skill of 1 or more of its employees. (Notably, a last-minute change to the legislation explicitly excluded engineers and architects from these limitations, preserving the QBI deduction for those professional fields.) Similar to the W-2 wage limits, the specified service business limit will only apply to those whose taxable income exceeds the thresholds ($157,500 for individuals, and $315,000 for married couples). Service business owners whose income rises above the thresholds will phase out the QBI deduction over the next $50,000 of income (for individuals, or $100,000 for married couples), which means the pass-through deduction under IRC Section 199A will be completely gone by income levels of $207,500 for individuals and $415,000 for married couples (and the threshold amounts will be adjusted for inflation in future years).

Notably, for partnerships, LLCs, and S corporations, these income threshold limitations – where the W-2 wages limitation and the specified service business limitation kick in – are calculated individually (based on each partner/owner share of all income, deductions, W-2 wage allocations, etc.). Which means “lower income” partners and owner-employees might still be eligible for the QBI deduction on a service business, even as higher-income partners/owners are not. Which may introduce a number of new family business planning opportunities for pass-through businesses by distributing ownership to multiple family members who are all below the threshold.

Planning Issues And Complications For The Section 199A Pass-Through Business Deduction

For many pass-through businesses (and sole proprietors), the new IRC Section 199A pass-through deduction on Qualified Business Income will be material (or at least modest) tax relief. As a 20% deduction against all QBI, the deduction itself will scale to the size of the business. A company earning $100,000 of income will obtain a $20,000 deduction (worth $4,400 in the new 22% tax bracket); a company earning $10,000,000 of income will obtain a $2,000,000 deduction (worth $740,000 at the new 37% top tax bracket). And given that each partner/owner calculates their own deduction based on their own income, the value of the QBI deduction itself will vary from one partner to the next.

The greatest tax planning opportunity – and potential challenge for many existing businesses – will lie in the fact that, for the first time ever, self-employed individuals (either as sole proprietors, or as owners of partnerships, LLCs, or S corporations) will have a lower tax rate than employees doing substantively similar work, thanks to the 20% QBI deduction. For many workers, this will introduce a temptation to recharacterize their working relationship from employee to independent contractor, or otherwise form separate business entities that contract back to their employer for their prior work. Which will further amplify what are already active battles that the IRS has with businesses that improperly characterize employees as independent contractors for FICA tax purposes and to avoid employee benefits obligations (as now the employees themselves will want to be characterized as independent contractors for the tax break, too).

Notably, though, the path for most employees to recharacterize themselves as independent contractors only “works” to the extent that they stay under the income thresholds. Because virtually all independent contractor work, including all types of “consulting”, would likely be characterized as a specified service business. Which means the benefits of being independent will start to phase out at $157,500 for individuals and $315,000 for married couples, and will fully phase out by $207,500 and $415,000, respectively. And those phase-outs are based on taxable income – which means all income, including other non-business income (and even capital gains, or Roth conversions) would apply when determining whether the service business phase-out threshold has been breached.

On the other hand, very large service businesses with substantial income will find the new specified service business limitations to be especially problematic. Because once owner-employees are past the income thresholds (e.g., a multi-billion-dollar RIA, or a large accounting or law firm), owners (and especially concentrated owners, such as founders) will obtain no benefit from the QBI deduction, even as they face a top ordinary income tax rate of 37%. Meanwhile, the top corporate tax rate is now only 21% under the Tax Cuts and Jobs Act. Which means a lot of large service businesses may end out converting to C corporations under the new rules (dragging their smaller partners along), or at least revoke their S elections (as S corporations) or choose to have their partnership/LLC taxed as a corporation (which is permitted under the “Check The Box” rules as long as there are at least 2 partners/members). Expect to see a lot more discussion in the coming year about large service businesses reclassifying (unless Congress creates a Large Service Business exemption under a future Technical Corrections Act to the legislation).

Estate & Gift Tax Exemptions Doubled (But Not Repealed!)

While the early buzz from the House GOP legislation was that the estate tax might be repealed (after 2024), the final Tax Cuts and Jobs Act legislation did not repeal the estate tax (not now, nor in the future).

However, the final GOP Tax Plan legislation does double the unified estate and gift tax exemption amounts from their current levels, which turns the otherwise-scheduled-to-be-$5.6M exemption in 2018 into an $11.2M individual estate tax exemption (or $22.4M for married couples with portability). The increased exemption is not retroactive, though, and only applies to those who pass away after December 31st of 2017. No other changes are enacted, though; step-up in basis remains, as does the top 40% tax rate on gifts and estates, and the other existing rules on generation-skipping taxes.

Ultimately, the expansion of the estate tax exemption will go even further to reduce exposure to what has already been a drastic narrowing of the estate tax over the past 15 years. Even under current law, the number of estates subject to Federal estate tax has fallen by nearly 95% since 2001, and is now estimated to be under 5,000 estates per year. The further narrowing of the estate tax with higher exemption amounts will further reduce the relevance of estate tax planning (which increasing is shifting to the income tax planning opportunities at death), and will also make it easier for the IRS to audit virtually every estate that is subject to the estate tax (and spot any questionable strategies and abuses). Expect a further crackdown on advanced estate tax strategies in the coming years – especially GRATs, which are already on Congress’ radar – as the IRS becomes even more targeted.

For many, though, the further expansion of the Federal estate tax exemption shifts estate taxes to primarily be a state problem, at least for the 15 states that still have a state level estate tax. In recent years, a number of states had “recoupled” to the Federal estate tax exemption, which means their state level exemptions will immediately increase in 2018 as well. For other states, though, their exemptions remain much lower – in some cases, still fixed at $1M from the “old” state estate tax credit rules prior to 2001 – and in those states, there will be additional pressure to fix the fact that state estate taxes can often be avoided entirely with deathbed gifts (given the lack of state estate taxes, or the backstop of a Federal gift tax now that the Federal exemption has risen even further).

The bottom line, though, is that the estate tax – at least and especially at the Federal level – will be a very uncommon financial planning need in the future. Albeit still very high stakes for the small subset of ultra-high-net-worth families who are over the $11.2M exemption (or $22.4M for couples).

Miscellaneous TCJA Tax Provisions Of Note

Beyond the high level “headline” provisions of the Tax Cuts and Jobs Act, the final legislation included a wide range of miscellaneous “crackdowns” and “loophole” closers.

Of note to financial advisors is that the controversial investment provision that would have required FIFO treatment for all investments (and eliminated the ability identify specific shares being sold) was not included in the final legislation. Although given that there have been proposals to eliminate specific share identification and require FIFO as far back as 2013 means the potential FIFO rule may return again in the future.

Other notable – and at times, controversial – loophole closers that did not make the final cut (and therefore all remain intact) include:

- Elderly and Dependent Care credit

- Tax credit for plug-in electric vehicle

- $250 schoolteacher deduction

- Adoption Assistance tax credit

- Tax preferences for private activity bonds

In addition, the proposal that would have significantly curtailed the IRC Section 121 exclusion of up to $500,000 of capital gains on the sale of a primary residence was not included in the final legislation. The proposal would have changed the lived-and-used in 2-of-the-last-5-years requirements to a 5-of-the-last-8 years instead, and would have imposed a phaseout of the capital gains exclusion for couples with more than $500,000 of AGI (or $250,000 AGI for individuals). Yet despite being included in both the House and Senate versions of TCJA, the final legislation did not include the proposal.

On the other hand, a number of notable provisions were included in the final legislation, including:

- Individual Mandate Repealed. After being proposed mid-way through the drafting process, the final TCJA legislation does repeal the individual mandate for health insurance. Notably, though, the individual mandate (and the potential tax penalty) does remain in place for the 2018 tax year. The repeal will not take place until 2019.

- Alimony Treatment Is Reversed. Under existing law, alimony payments are deductible to the individual paying the alimony (usually higher income), and reported as taxable income to the alimony recipient (usually lower income), unless the divorce decree or separation agreement stipulated otherwise. Under the TCJA legislation, alimony payments would no longer be deductible by payors, nor reportable by recipients, effectively eliminating the tax bracket arbitrage between the two. However, this provision will only apply to divorce agreements after December 31st of 2018 (or for prior agreements that are explicitly modified to adopt this provision in 2019 and beyond).

- 1031 Exchanges Limited To Real Estate. Most financial advisors know IRC Section 1031 as the rules that allow a “1031 exchange” of like-kind real estate for other real estate. However, 1031 exchanges are not exclusive to just real estate, and have been used for other types of “investment property” such as classic cars or airplanes or boats. Under the new rules, though, 1031 exchanges (occurring after 12/31 of 2017) will apply only to real estate.

- Moving Expense Deductions & Exclusions Repealed. Under current law, households can claim an above-the-line deduction for moving expenses (as long as certain distance provisions are met). However, TCJA repeals the moving expense deduction (except for certain moving expenses for active duty military) beginning in 2018. In addition, the ability of employers to pay for moving expenses tax-free (i.e., reimbursement of moving expenses were excluded from income) is also repealed (except for certain active military), which means in 2018 and beyond, reimbursed moving expenses will be taxable income to employees.

- Increased Depreciation For Business Cars. Claiming vehicles as business expenses has long been a controversial area, and led years ago to the creation of IRC Section 280F that explicitly limits the deductibility of “luxury automobile mobiles”. However, a provision in the Senate version of TCJA, which was adopted in the final form, significantly increases the deductibility for business cars beginning in 2018, and may even make buying a new automobile in the business more appealing than leasing (as is commonly done today given the 280F limitations).

- Crackdown On Business Entertainment Expenses. Current law permits businesses to claim deductions for 50% of entertainment expenses directly related to the business (e.g., meals and entertainment for people the business may be doing business with). However, TCJA will limit these rules starting in 2018 by barring any deduction for “an activity generally considered to be entertainment, amusement, or recreation” (even if they directly relate to or are associated with the business). Although the 50% deduction for food and beverage expenses associated with the business remains.

- Flexibility To Roll Over 401(k) Loans After Termination. One of the big “risks” of taking a loan from a 401(k) plan is that many plans require that the loan be immediately repaid if the employee separates from service (or face adverse tax consequences). And may even require repayment if the plan terminates (e.g., the employer goes out of business). Under TCJA, though, a “qualified plan loan offset” amount for a terminated 401(k) loan is eligible for rollover within 60 days, essentially providing an (ex-)employee more time to repay the loan (directly into a rollover IRA) to avoid the tax consequences of non-repayment.

- Employer Tax Credit For Paid FMLA. Under the Family & Medical Leave Act, employers must provide certain employees with the option for up to 12 weeks of unpaid, job-protected leave per year (and must maintain group health benefits during the leave). To incentivize employers to further support FMLA, though, the TCJA legislation provides employers a business credit equal to 12.5% of wages paid to employees during leave (as long as the employee is paid at least 50% of their normal wages), and the credit phases in to as much as 25% of wages if the employer provides 100% continuing wages (up to the 12-week maximum).

-

Crackdown on Deferred Compensation. A proposal from the House GOP plan that remained in the final TCJA legislation will crack down on nonqualified deferred compensation plans, triggering taxation as soon as there is “no substantial risk of forfeiture” (i.e., when it becomes vested, regardless of when it is paid). And the new rules would extend to a wider range of stock options and stock appreciation rights under new “Qualified Equity Grant” rules. Expect to see a lot of revising to various deferred compensation plans in the coming year.(Non-qualified deferred compensation crackdown was not included in the final TCJA legislation.)- Crackdown on Equity Grants For Private Companies. Income deferred for equity grants will only be "qualified" in limited circumstances where grants are connected to employment services and a minimum percentage of company employees participate in the grants. And income deferral will be further limited for the most highly compensated employees of the company.

- Sexual Harassment Settlements Not Deductible If Subject To An NDA. An interesting addition to the final Tax Cuts and Jobs Act legislation is a Senate provision that denies a business any tax deduction for any settlement, payout, or attorney fees related to a sexual harassment or sexual abuse claim, if the payments are subject to a nondisclosure agreement. Which effectively means that businesses will now have to choose whether to require an NDA, or receive a tax deduction for the costs associated with a sexual harassment or abuse lawsuit… an interesting way to apply tax leverage against businesses that try to hide such settlements in the future?

Beyond the provisions above, two other notable rules for at least some financial advisors are new scrutiny on life settlements transactions, and a crackdown on Roth recharacterization strategies.

New Reporting Requirements For Life Settlement Transactions

A “life settlement” transaction is one where the policyowner of a life insurance policy sells the policy to a third party. The appeal of such transactions is that, where the original policyowner has had an adverse change in health since the policy was originally issued, a third-party buyer may be willing to pay more for the policy – and hold it until the death of the original insured – than the insurance company is willing to offer as a cash surrender value. For instance, a surviving spouse who is in declining health but no longer has a need for a $1M insurance policy with a $150,000 cash value might find a third-party buyer who would pay $200,000 in cash (which the spouse might prefer to enjoy while she’s alive, especially if she has no heirs who need the death benefit anymore).

From a tax perspective, the significance of life settlements transactions is that they trigger the “transfer for value” rules, that cause the death benefit to be taxable to the new owner (rather than the usual tax-free treatment for life insurance death benefits under IRC Section 101). However, because a life settlements transaction itself – the purchase and change in ownership – are not themselves reportable events, the IRS has struggled to track whether buyers of life settlements transactions are properly reporting their taxable death benefits (or not).

To close this gap, the new rules stipulate that when a “reportable policy sale” occurs – which is “the acquisition of a life insurance contract, directly or indirectly, if the acquirer has no substantial family, business, or financial relationship with the insured” – the buyer must report information about the purchase to the IRS, the insurance company that issued the policy, and the seller, including the buyer’s and seller’s information (name, address, and taxpayer ID number), the date of the sale, the name of the insurer, and the amount of the payment (although the payment amount doesn’t have to be reported to the insurer, just the IRS).

In turn, when an insurer receives notice of a reportable policy sale, the insurer must in turn report to the IRS and the seller the policy number and the basis in the contract. And when the insured ultimately passes away, the insurer is again required to provide reporting – to both the buyer/policyowner, and the IRS – including the death benefit payment, and (again) the estimated basis of the policy.

On the plus side, though, the new life settlements rules explicitly state that the cost basis of an insurance policy (for the purposes of determining life settlement gains) will not include any adjustment for mortality and expense or other cost of insurance charges (which reverses IRS Revenue Ruling 2009-13 that cost of insurance charges reduced the seller’s basis in the policy).

Roth Recharacterizations Of Prior Conversions Repealed

The original rules for Roth contributions and Roth conversions contained a provision that allows for such contributions or conversions to be “recharacterized” – effectively an “undo” button that would permit a Roth contribution to be switched back to a traditional IRA, or a Roth conversion to be switched back to its original source IRA.

The primary purpose of these recharacterization rules was to provide a means to unwind Roth contributions or conversions for those who were over the income limits – as under the original 1997 rules, both Roth contributions and conversions had income limits. In essence, if the individual contributed or converted, and then later discovered he/she was over the income limits, there was a way to undo the contribution or conversion that should have never happened in the first place.

A key aspect of the rules, though, was that in order to “true up” a Roth recharacterization, the taxpayer was required to undo not only the original contribution or conversion, but also the pro-rata share of any gains (or losses) that had occurred in the account during the interim. The rule was meant to ensure that if someone contributed (or converted) and the account went up, that the contribution (or conversion) and the growth had to be returned (otherwise, taxpayers could just keep making impermissible contributions/conversions, taking them back, and leaving the growth behind inside the Roth IRA every year).

Yet an indirect side effect of these rules was that they could be used proactively as well. As not only did gains have to be recharacterized, but losses had to be recharacterized as well. And since recharacterizations occurred on an account-by-account basis, it was possible to actually convert multiple investments into multiple accounts, let them run for the up-to-21-month recharacterization period, and then be able to cherry-pick the winners and recharacterize the losers (ensuring that all Roth conversions “always” go up in the first 21 months!).

Early on, this potential abuse was an inevitable side effect of the fact that Roth conversions needed a way to recharacterize, in case the household discovered (after the end of the year) that they were over the Roth conversion income limits. Except the Roth conversion income limits were repealed in 2010, as a part of the Pension Protection Act. Which means under current law, the only remaining purpose of a Roth recharacterization is various abuse strategies (or perhaps those who simply have a change of mind/heart after the fact).

Accordingly, the Tax Cuts and Jobs Act repeals the rules permitting recharacterizations of Roth conversions, effective starting in 2018. Notably, though, the rule only limits recharacterizations of Roth conversions (and not of Roth contributions), permitting those who mistakenly make a new Roth contribution and later discover they’re over the income limits to recharacterize it back to a traditional IRA. But Roth conversions cannot be recharacterized anymore.

The bad news of these new rules is that the popular multiple-account-Roth-conversion strategy is nullified going forward. Nor is it safe to fill lower tax brackets by doing “excess” partial Roth conversions and then recharacterizing the excess after the fact (instead, the “correct” amount for a partial Roth conversion needs to be determined before the end of the year, to ensure the correct amount is converted). In addition, advisors should be wary that even “accidental” Roth conversions that turn out to be larger than desired cannot be unwound after the fact anymore!

Fortunately, though, the new limit on Roth recharacterizations applies only for taxable years beginning after 12/31 of 2017 (i.e., the 2018 tax year and beyond). Which means existing already-completed 2017 Roth conversions should still be eligible to recharacterize in 2018 (since it would be recharacterizing a conversion for the 2017 tax year, while the new rules only apply in the 2018-and-beyond tax years). Although notably, the timing of the effective date for 2018 recharacterizations of 2017 conversion (i.e., whether they will be permitted or not) is still being debated by many tax commentators.

Notably, this provision should not affect the ability to make so-called “backdoor Roth” contributions. With the caveat that once the IRA contribution is converted, that conversion can no longer be undone.

2017 End Of Year Planning For The GOP Tax Plan

As a major piece of tax legislation, the Tax Cuts and Jobs Act is likely to be with us for many years to come. Its massive corporate tax reforms are now permanent, and while the individual tax law changes are nearly all scheduled to sunset, the lapse won’t come until after the year 2025. Which leaves a lot of time for lawmakers to potentially make the rules permanent (as ultimately happened to the 10-year sunset provisions for President Bush’s 2001 and 2003 tax cuts).

As a result, there will be time to adapt to the new tax laws. And many provisions – especially the new rules for pass-through businesses – will likely take months to fully digest, as new tax planning strategies are developed.

Nonetheless, with the legislation anticipated to pass both houses of Congress and be signed into law by President Trump this week – less than two weeks before the end of the tax year – raises questions about what can or should be done before the end of the year to take advantage of the new rules (or to dodge next year’s “loophole closers”).

In general, the thrust of the new legislation is to reduce income tax brackets, and also more significantly limit deductions. As a result, advisors and their clients should generally be looking to defer income into the new lower tax brackets in 2018 (beyond, perhaps, still filling the lowest tax brackets for partial Roth conversions if available), while it will be more appealing to accelerate deductions (especially those that may not even be available next year).

In fact, most end-of-year tax planning will likely focus on maximizing the deductions that are going away, particularly with respect to the cap on State And Local Tax (SALT) deductions, and the loss of miscellaneous itemized. As while the new law does limit the ability to prepay 2018 state tax liabilities in 2017 just to obtain the deduction, it is still possible to pay 4th quarter (or the full year’s) 2017 state taxes by December 31st in order to obtain the deduction this year. And some advisors may even wish to collect 4th quarter advisory fees before the end of the year (if their systems can accommodate). Though bear in mind that these items are also AMT adjustment amounts under current law, which means lumping them into 2017 may still result in little or no tax benefits if they trigger AMT (and especially for those already over the AMT line).