Executive Summary

In the early years of financial planning, the reality was that most advisors only needed one skill to be “successful”: the ability to sell, and get clients. After all, when advisors are solely compensated by commissions, if you can’t keep finding new prospective clients to sell to – and actually sell something to them – your income will quickly go to zero.

As financial advisors have shifted to the AUM model though, and the recurring revenue it supports, the requisite entry level skillset has shifted. Now for many advisors, the key abilities are technical competency to give the right advice, and empathy skills to form and deepen the client relationship. Sales and business development comes later, if at all.

And as advisory firms have grown, for many the emerging skills gap is in the area of management, from training and developing other staff members, to the overall execution of the business.

From the career track perspective, what this means is that for financial advisors to progress in their own careers, it becomes necessary to expand their expertise across more and more of the domains – generally at least three of the four. And for advisory firms themselves, the four skill domains may provide a helpful roadmap to consider where the firm should invest resources to improve the team for the future!

The Original Skills Progression For “Financial Advisors”

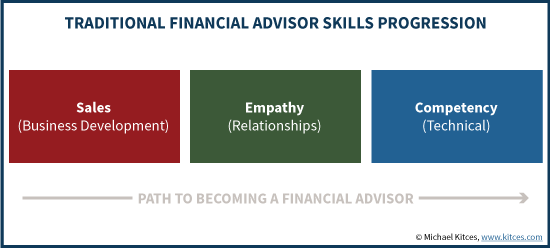

In the early years of “financial advisors”, the reality is that almost no one was actually a financial advisor paid for financial advice. Instead, they were sellers of financial services products, from (door-to-door-sold) insurance policies in the 60s and 70s to tax shelters in the 70s and 80s to stocks and then mutual funds in the 80s and 90s.

As a result, the primary skill that someone needed to survive in the early years was the ability to sell. If you couldn’t do business development, prospecting for potential clients and then closing them as clients, you didn’t make any money, you couldn’t validate your (sales) employment contract, and you were out of the business. Financial services firms had extensive “financial advisor training” programs that were really just about (product) sales training.

For the subset of salespeople who were successful enough at cold selling – in an era where most sales were driven by cold-knocking door-to-door and later with the telephone by following a cold calling script – eventually they had the opportunity to form deeper relationships. The virtue of deepening a relationship was that it turned someone from a mere sales opportunity into a potential referral source, in a world where we only refer and do business with people we know, like, and trust.

The caveat, however, is that the skillset to form strong relationships with clients and centers of influence is different than just the ability to sell. It requires the key skill of empathy – an ability to be aware of and cognizant of the feelings of other people, so that you can adjust your communication style and approach in order to connect with them. While some people are naturally born with this talent – they have a high “emotional intelligence” – for others, it’s a new skill to learn and be trained in.

For those who did have the crucial good empathy and active listening skills – either naturally or learned – it became possible to build a steadier income from repeat/recurring business with existing clients, and the referrals that were generated from those clients and other centers of influence or strategic alliances. In turn, this freed up time for the financial salespeople to no longer spend all their time worrying about where the next client was going to come from, and instead to take the final step of skills development to actually become a financial advisor: learning the technical competency skills necessary to actually give bona fide financial advice.

After all, the reality is that it’s not really possible to be a true “financial advisor” until you have the training and education to know what the correct advice is to provide in the first place. Otherwise the “advisor” may give well-intentioned recommendations, but the advice may be factually incorrect! Learning the technical knowledge required for competency – e.g., by earning the CFP certification – was the last step to becoming a full-fledged financial advisor. (And of course, the competency to give more sophisticated advice didn’t hurt as a sales differentiator, either!)

How The AUM Model Has Changed Financial Advisor Training

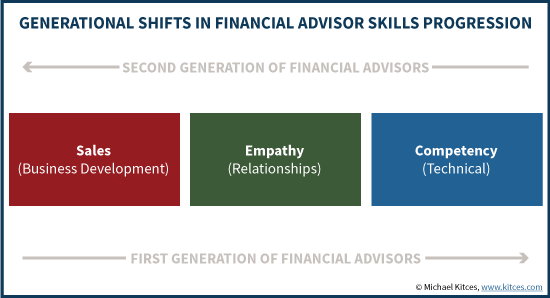

The early roots of financial advisors were all about the skills progression from sales to empathy to technical competency, which was borne out of necessity – because if the financial advisor couldn’t first and foremost get clients, there was no one to whom services would be delivered and from whom payment could be received. Financial services firms didn’t just have a list of clients to hand out.

However, the growth of the AUM model and its recurring advice provided in exchange for recurring revenue, fundamentally changed this equation. Suddenly, the problem for many rapidly growing advisory firms was that the founders responsible for sales and business development were running out of the capacity necessary to service a growing volume of existing clients. Yet because those existing clients generated recurring revenue – in the form of AUM fees – it was feasible to pay a highly skilled financial advisor to service them.

However, since the firm already had the clients, the traditional skills progression for their financial advisors were different. It was no longer necessary to start with sales and business development, because the firm already had that covered. Instead, the need was for advisors who had the technical competency to deliver advice (unsupervised), and the empathy to be able to establish a relationship with a client (and be able to retain them in the future).

Ironically, the rise of these employee financial advisors has now led to a unique new challenge for many firms – their financial advisors are highly skilled in technical competency and empathy relationship-building, but have no training or experience doing sales and business development!

In other words, the evolution of advisory firms has turned financial advisor skills development around 180 degrees: while the first generation of financial advisors started with learning (or naturally having) sales skills and then developed their empathy and technical competency, today’s generation of financial advisors starts with technical competency and empathy and must learn to develop their sales skills!

The Management Skills Gap In Financial Advisory Firms

As recurring-revenue AUM firms have continued to grow from a median size of just $25M of AUM and just 1 staff member 15 years ago, to $100M of AUM and several staff members in 2008, and now $200M+ of AUM and a dozen staff members today, an emerging challenge has been the need for dedicated management just to handle the size of the firms.

Unfortunately, though, the reality is that management skills are really an entirely different domain than sales, empathy, or technical competency skills. In fact, given the self-selection of most experienced advisors – who were (and had to be) sales people first and foremost just to survive – arguably management skills are actually the biggest skills gap for most advisory firms today.

Accordingly, demand for Chief Operating Officer (COO) positions in advisory firms over the past 6 years has driven a whopping 7% per year growth rate in the average COO compensation, and practice management guru (and Pershing Advisor Solutions CEO) Mark Tibergien has suggested that the industry’s ongoing struggles in bringing in Millennial financial advisors may be more of an advisory firm management problem than a Millennial attitude problem. Major RIA custodians like Schwab and Fidelity have also tried to step up with leadership development programs to fill the void.

After all, the reality is that whether you’re a “first” generation advisor who went from sales to empathy to technical competency training, or a “second” generation advisor who went the other direction, neither necessarily have any management training as a part of their personal career and skills development! At best, some who have a natural talent in this area have risen to the top, and in the rest of the cases advisory firms have had to hire outside talent to fill the management gap (explaining, again, the rapid growth of COO compensation in advisory firms!).

The Four Skill Domains Of Financial Advisor Mastery

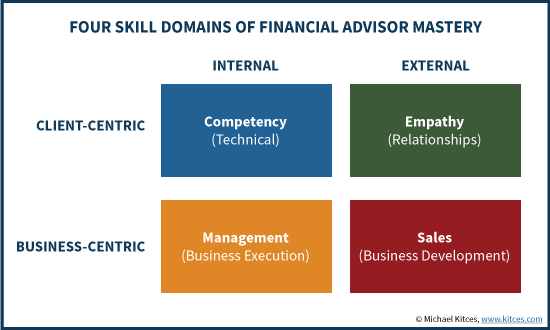

Given these dynamics, it appears that ultimately there are four domains in which financial advisors may seek to improve their skills to advance their careers: competency (technical), empathy (relationships), sales (business development), and management (business execution).

Notably, there is a significant difference in the focal areas of each of the skills domain. Developing the advisor’s competency and empathy are ultimately client-centric skillsets – they’re about actually delivering better and more effective financial planning advice, and retaining financial planning relationships. By contrast, the domains of sales and management are more business-centric – they’re ultimately about building the business itself and growing the value of the business. Or viewed another way, competency and empathy are about working in the business, while sales and management are about working on the business.

In addition, the skill domains can also be differentiated by their internal versus external orientation. The competency of the advisor, and the management of the business, are both internally focused back towards the advisor and the business. By contrast, empathy and sales skills are externally focused on the client, or bringing in clients to grow the business. In theory, I suspect that those financial advisors who are naturally more introverted may be naturally more inclined towards the internal skills, while extroverts may have more natural skillsets in the external domain. And given that historically financial advisors had to be first-and-foremost successful at sales, it’s perhaps no surprise that experienced financial advisors seem to disproportionately be hard-wired extroverts!

In fact, the reality that most people have a natural inclination towards one domain or another means most advisors will struggle to master all four domains. Most will start out with an innate skillset for one (a natural aptitude for sales, or technical competency), expand into a second to advance their career (improve sales or empathy/communication skills or advance their technical competency), and a few may cross over to a third in the later stages of their career (e.g., moving from traditional financial advising into the manager of a financial advisory firm, or someone in a management position who decides to shift into a client-facing advisory position). The number who can master all four will be relatively few – but those are also the ones who will likely rise to the top of the largest and most successful firms!

Charting The Course Of Your Financial Advisor Career Track Advancement

As financial advisory firms continue to grow, the roles within firms are becoming more and more specialized. The benefit of this shift is that it provides an opportunity for financial advisors (and all employees) to move into the role that is best suited to their natural talents. The challenge is that it may make them so comfortable in their current role that they never learn to improve their skillsets in the other domains – which, ultimately, will limit their upside.

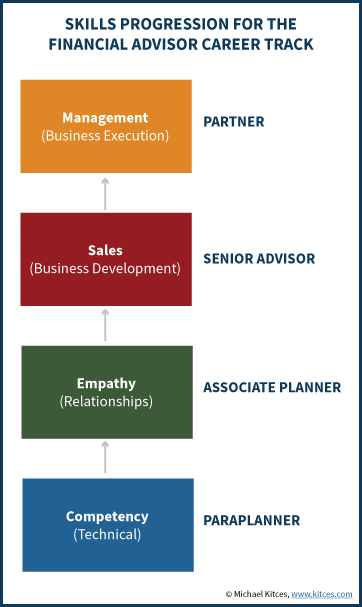

In fact, viewed from the opposite direction, it’s the expansion of mastery into other skillsets that is increasingly defining the financial advisor career track itself. It starts with obtaining mastery of the technical competencies of knowledge as a paraplanner, then proceeds to developing empathy skills as an associate planner, and then to doing business development for the firm as a senior advisor, with the potential for ownership (or “making partner”) by taking on management responsibilities as well.

In fact, viewed from the opposite direction, it’s the expansion of mastery into other skillsets that is increasingly defining the financial advisor career track itself. It starts with obtaining mastery of the technical competencies of knowledge as a paraplanner, then proceeds to developing empathy skills as an associate planner, and then to doing business development for the firm as a senior advisor, with the potential for ownership (or “making partner”) by taking on management responsibilities as well.

In other words, adding new domains of mastery is actually the key to progressing down the financial advisor career track! And the fact that for many, it is very difficult to become “good” in so many different areas is perhaps why, in the end, fewer and fewer financial advisors are ultimately becoming partners/owners of advisory firms (not that you can’t earn a very good compensation “just” by being a great financial advisor who works with clients!).

Ultimately, though, the bottom line is simply this: progressing through the entire financial advisor career track requires mastery in a number of different skill domains. For firms looking to develop talent, they would be well suited to consider how they are helping to develop their employees in each of these domains. And for financial advisors looking to advance their own careers, recognize that if you want to eventually move to the next tier, you will likely have to push your limits by trying to master a “new” skill domain!

So what do you think? Does this seem like an appropriate conceptual framework for how financial advisors can progress in their careers? Do you think there’s anything missing? Please share your thoughts in the comments below!

I would make it “Sales / Marketing”, at least for independent RIAs. There are lots of opportunities, and many more than before. And at lower cost. But marketing is problematic for employee advisors and broker dealer affiliated advisors.

Seems to parallel the consulting world…. or COULD parallel the consulting world. When I started they gave you some technical knowledge but mostly said “SELL”!

I agree JRB about the consulting world skills. Actually business management skills in general are helpful.

Back in 2007 I started asking my advisor client to read books that consultants would read to grow their firms. Seems to me that is the way the industry is moving for some and consulting skills has proved to be very helpful .

Michael, conceptually I agree with you. I think to some extent the “system” is still stacked against those who fall in G2 of your article. Although there are some attempts to change training programs, most new “financial advisors” are in reality nothing more than asset gatherers. This is because most larger firms are still in the business of selling product, AUM these days, rather than intellectual capital of their advisors. So the system forces advisors to sell in order to survive. 9 out 10 do not. Those who survive and make it to the top and become managers may or may not have managerial skills. In fairness, the same dynamic can be seen in law and accounting. Partner in a law firm may be a great technician but have no people skills. I hope the DOL ruling, possibly followed by the SEC, will force the industry at large into developing advisors with more rounded skill set. From a personal experience, I am struggling with operating skills of my nascent financial planning firm simply because I never had to worry about the ops having worked at large organizations. Either I will have to develop these additional skills or eventually hire someone if and when the firm gets large enough.

Michael, I really like this article, I think you are spot on. I think the challenging part of the hiring process for junior employees is to figure their natural level of empathy as this is a skill very difficult to develop if you don’t have any to begin with. Since keeping a client is easier than getting a new one and hard skills are easier to teach than soft skills, I would definitely start at the empathy level.

Good article Michael. If there is anything missing it is resources or recommendations for how an advisor can develop the ‘new’ management skillset.

Something for me to cover in the future! 🙂

– Michael

Extremely helpful article. Thank you. If we take the old (tongue-in-cheek) adage that, “those who can’t do- teach” and expand it with, “those who do extremely well- build”; then can we consider that there might be a fifth skill domain for Advisory Leadership? This is a role primarily involved in coaching and oversight of other advisors. I think of my firm and the people I’d want for leadership are those who have obtained a level of mastery in the areas you mentioned, but also have skills in leading others. Interested in your thoughts. Thank you for all you do for our industry.