Executive Summary

In an increasingly competitive landscape, most financial advisors have succeeded by providing quality service that retains their existing clients, with the average financial advisor retention rate at 94%.

Yet the challenge is that while offering great service may keep clients on board, it’s incredibly difficult to use “great service” as a differentiator. In fact, according to one recent study, 72% of all advisors differentiate on client service. And by definition, when the majority of advisors differentiate on the same point, it’s not differentiating anymore!

In addition, differentiating on service is also difficult because there’s no clear and consistent definition of what “great service” even is. Especially since what is great service to one client may not be to another. What constitutes “great” is truly in the eye of the beholder.

Which means at a minimum, for advisors who do want to differentiate on great service, it’s necessary to truly articulate what “great” really means (and for whom). For instance, advisors might craft a “Client Service Standards” document that explicitly states what “great service” really means, at least from the advisory firm’s perspective in trying to serve its ideal clients. Of course, then it’s also crucial to affirm that what the advisor thinks is great service is really perceived that way by the clients themselves. And if you commit to it, be certain you’re really ready to deliver it, too!

The Undifferentiated Service Differentiator Of Most Financial Advisors

As part of the work for its ongoing Research and Practice Institute, the Financial Planning Association recently released a new study, entitled “Defining and Communicating Your Value”. The research aimed to help understand how advisors define their value for clients, and differentiate from other advisors. And the results weren’t pretty.

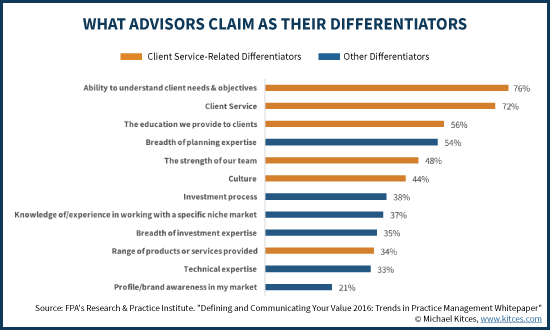

In fact, when asked “Which of the following sets you apart from other advisers… [and] differentiates your business from others” the surveyed advisors responded as follows:

The key distinction of this chart – colored for additional clarity – is that almost half of it (colored in orange) relates directly to the firm’s client service (and the people who deliver it)… with terms/labels that are almost impossible to actually differentiate with. In particular, nearly 3/4ths of all advisors say that their top two differentiators are “client service” and “the ability to understand client needs and objectives”!

But what does that really mean? How exactly is an advisor’s service superior through better understanding a client’s needs and objectives than other advisors? Are you really staking the future of your business on “I’m more understanding” and “I have a better data gathering process”? And when was the last time you ever heard a prospective client say “I left my former advisor because he/she sucked at data gathering and didn’t understand my objectives”?

More generally, what does it mean to say that you “differentiate on service”? Does that mean you’re faster at transferring accounts than other advisors? Is it because you spend more time in meetings than other advisors (and is that good service, or just bad productivity and an inefficient meeting!?)? Do you return phone calls and reply to emails faster than other advisors? How would you even know? And how would your clients know how to compare you, when they can’t even evaluate something “invisible” like your client service until after they’re already a client?

Notably, advisors working with affluent clients have extremely high retention rates (one PriceMetrix study pegged industry-wide advisor retention rates at around 94%, with top advisors maintaining 98% annual retention), suggesting that most advisors are in fact likely delivering solid service for their clients. Except, again, with an industry average retention rate of 94%, this suggests that virtually all advisors are meeting or exceeding their clients’ expectations in this regard. In other words, these aren’t differentiators; they are necessary components to serve and retain clients in the first place, and every advisor does it.

Great Service Is In The Eye Of The Beholder

One of the greatest challenges in defining “great service” is that what even constitutes “great” will depend on the person receiving the service, and their own circumstances and expectations.

For instance, if you’re working with a retired client, “great service” might reference your willingness to meet during the day at a convenient time to them. But if you’re working with a client who is still employed, “great service” might mean your willingness to meet at night, since it’s inconvenient for them to take time off from work during the day! And if the reality is that your office isn’t really at a very convenient location in the first place, “great service” might mean you never meet at your office at all, and instead go to the client to meet at their home or office instead!

Similarly, the length and frequency of meetings that constitute “great service” may vary by client. For some, a “great” meeting is one that happens quickly and gets done promptly. For others, “great service” means that the meeting is productive and has some social enjoyment as well (e.g., meeting over a meal or at an event). For those with busy lives where meetings are a hassle, having 4 meetings a year may be an onerous scheduling burden, where “great service” is figuring out how to get it all done in 2 meetings. For other clients who prefer more frequent contact, “great service” could mean monthly in-person meetings and quarterly meetings is too sparse!

Even determining the nature of service-related communication can be a challenge in determining what constitutes “great” service, with significant generational divides. For busy Gen X clients still working, effective email communication is valued more as a “great service” than in-person meetings! For Baby Boomer and Millennials clients, “great service” is more likely to mean an in-person meeting, but Boomers have a strong preference for formal meetings at the advisor’s office, while Millennials are more likely to prefer an informal “catch-up” at a third-party location to view the service as “great”.

And the differences amongst client expectations varies across the full spectrum of “service”. For some, great service means receiving communication regarding every step of the process. For others, it’s about minimizing the communication and only connecting when it really matters. For some, a great service response requires a returned email or phone call within the hour. For others, it might be any response the same day. Or by the close of the following day.

Simply put, the definition of “great service” is in the eye of the beholder, and will vary significantly depending on who the target clientele is in the first place! Which means when an advisor says they offer “great service”, the expectation they’re creating in the mind of the client will vary greatly from one to the next!

Crafting Great Service Requires Knowing Who You Serve

Ultimately, defining “great service” requires first defining who the firm is providing the service for, since for instance working with affluent Gen X business owners will be very different than retired Baby Boomer clients (which in turn will vary further still based on their wealth, their affluence, what they really want from their advisor, etc.).

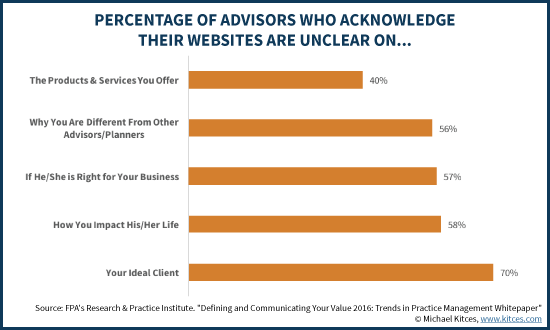

Unfortunately, though, the FPA’s RPI Study on Communicating Value reveals that most advisors also have no clear definition on who they serve in the first place, and therefore cannot define it in their marketing materials, either. For example, the study found that when asked “if a prospective client came to your website, to what extent would he/she understand…” what differentiates you, who your ideal client is, and how you impact their lives, the majority of advisors acknowledged their own websites are unclear!

In fact, in perhaps the ultimate of ironies, the earlier chart regarding how advisors differentiate showed that advisors are more likely to differentiate by the breadth of their expertise than by the depth of technical expertise or a particular niche. In other words, the majority of advisors report that being an undifferentiated generalist is their differentiation (except it can’t be if a majority of advisors differentiate the same way!).

Accordingly, then, it is perhaps not surprising that most advisors struggle to differentiate on “great service” – because they haven’t defined who they serve, and therefore cannot articulate what “great service” would even mean to that particular type of client!

Defining “Great Service” By Crafting Clear Service Standards

Ultimately, the decision of who to serve and how to find a niche to specialize in is beyond the scope of today’s article. But for those who do have a clearly defined ideal client – and perhaps even for those who don’t – differentiating on “great service” still means, at a minimum, defining what “great service” really means (hopefully in a manner that is relevant to your [target] clientele).

One path to defining great service is to actually create a “Client Service Standards” document, that could be used both internally with your staff/team to create proper expectations of client service (as what is “great service” to you may be higher or lower than what the rest of your team thinks is necessary!), and also to communicate service expectations directly to clients and prospects.

For instance, a Client Service Standards document might include service details like:

- How quickly do you pick up the phone? 3 rings? 1 ring?

- Will you always pick up calls during office hours, or allow it to roll to voicemail if no one is currently available?

- What is your timeliness in returning phone calls: Same hour? Same day? Next day?

- If the client calls, will they always get you, or another member of your team, or just anyone in the firm?

- What is your timeliness in returning emails: Same as phone calls?

- If clients have to leave a message, will those messages always be returned by the advisor, or just by anyone on the team?

- How quickly will you analyze a financial planning question? Do you provide turnaround on financial issues in a day? Two days? A week? Two weeks?

- What is the frequency of meetings? Annual? Semi-annual? Quarterly? Monthly?

- What is the duration of meetings? 1 hour meetings? 2 hour meetings?

- Where will meetings be held/located? At the advisor’s office, the client’s home, or elsewhere? By video conference or in-person?

- What is the timing to schedule meetings? How quickly can a client schedule a meeting?

- What communication will be provided to clients between meetings? From whom? About what?

- Will you offer a statement of service commitment? What are the consequences to the team/firm if someone doesn’t deliver on the service as expected? Will you provide a refund (e.g., for a month’s worth of fees) to demonstrate your service commitment?

Ultimately, this kind of Client Service Standards document could be presented directly to current clients to reinforce your service commitment, to prospective clients to demonstrate what “good service” really means and how you intend to fulfill it, and could even be included in your marketing materials and as a part of the design of your financial advisor website for prospects to learn for themselves how serious the firm really is about delivering “great” service.

Of course, a key step to the process should be vetting your intended service standards against your existing (or target) clients. After all, you may not necessarily need to have the “highest possible” service commitment in each area... because again, what’s “great” to you may be unnecessary (or even overkill) for your clients. Accordingly, it’s crucial to show your clients a draft version of your new Client Service Standards document. Does the client/prospect agree that this is good service to them? Is it not enough, or too much? Are there differences of opinion amongst the clients? What do they really expect? And are you prepared to deliver it? (And if not, think twice about trying to differentiate on “great service” if you’re not ready to follow through!)

In the end, though, the bottom line is simply this: “great service” is for most advisors something they already deliver – at least enough to retain their current clients – but is both too common and too vague to be a real differentiator. Which means in the end, it still needs to be done to keep your clients, but probably shouldn’t be relied upon as a differentiator to get them.

But for those who do want to truly differentiate on service, consider crafting a “Client Service Standards” document that clearly articulates what “great service” really is, in a manner that can resonate with clients and differentiate you with prospects (from all the other advisors who haven’t defined their own service standards). Just remember, though, that if you define and commit to this kind of “great service” you’d better be ready to deliver on it!

So what do you think? Have you ever tried to articulate for your firm what “great service” really means? Does it mean the same thing to your clients as it does to you? Would you find a “Client Service Standards” document helpful to explain your value to your prospective clients? Please share your thoughts in the comments below!