Executive Summary

The explosive growth of technology has made it possible for individual financial advisors to be more personally productive than ever before, from software to automate key tasks to the use of (virtual) assistants to even further leverage the advisor’s time.

However, the reality is that every financial advisor eventually hits some personal productivity wall – the point at which there just aren’t any hours left in the day to serve more clients, even with the assistance of a technology and a team of support. In some cases, it’s the time to manage the team itself that becomes the biggest barrier to growing further.

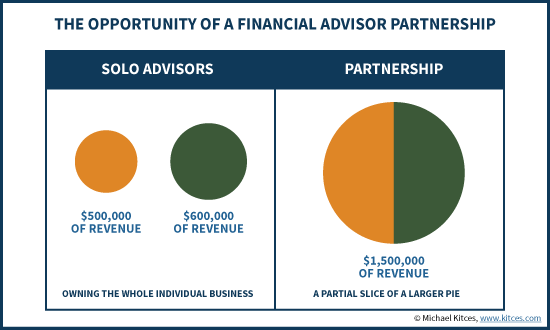

At that point, the opportunity for growth shifts to the need to add a financial advisor partner, where the advisor has the potential to earn a smaller slice of a much-larger pie. And in this context, the ideal of usually not just to combine together two already-successful financial advisors, but to actually find advisors who have different and complementary skillsets, which enhances the potential for the new whole to be worth more than just the sum of the individual parts.

Unfortunately, though, for many advisors the biggest challenge in adding a financial advisor partner is simply finding one in the first place. For most, the path seems to be through financial advisor conferences and events related to their platform, where it’s most feasible to find like-minded individuals. And fortunately, the availability of third-party “financial advisor compatibility assessment” tools can help to ensure that the partners will likely be able to formulate a shared vision for the future growth of their new joint business!

The Limits Of Personal Productivity As A Financial Advisor

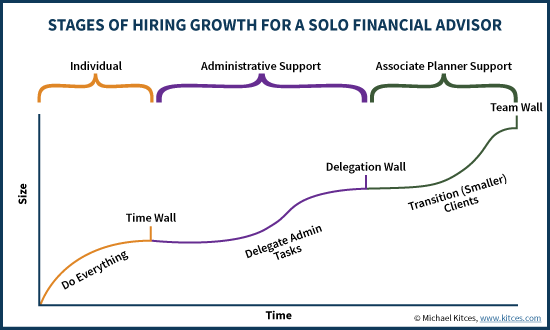

In the early days as a financial advisor, there is a lot of time, but not (yet) a lot of clients to serve. This leaves the advisor with time to market to prospects, build the business itself, and serve the few new clients who come on board.

As the number of clients grows, though, the available time begins to dwindle. What was once “free time” between marketing efforts and prospect meetings is now filled with actual client meetings, and the ongoing service demands to keep those clients happy. The advisor’s schedule begins to fill up.

As growth continues, eventually the financial advisor simply hits a time wall. All the available time is consumed by serving existing clients, there’s no more time to market the business and meet with prospects. Growth grinds to a halt. It’s time to hire.

The good news of hiring is that it gives the advisor an opportunity to free up some otherwise-fully-consumed time. It typically starts with (either in-person or virtual) administrative staff support, with a focus on delegating any tasks that don’t really require the advisor themselves to be executed, and allowing the advisor to focus more on interacting directly with current clients, and continuing to grow the business.

Eventually though, all the client service work that can be delegated has been delegated, and the advisor’s time is just consumed by the sheer number of hours it can take to meet and communicate with 100+ active clients. At that point, the advisor has hit the delegation wall, and it’s necessary to hire again – now searching out an associate financial planner – to whom a subset of the (smaller) clients themselves can be shifted.

Once again, this frees up the advisor’s time, but for the advisor who continues to grow, eventually an aggregate team wall is reached, where the advisor can simply no longer bring in a large enough number of new clients to keep an ever-growing team of associate planners busy. Not to mention that the time demands for managing the business itself become more complex with a growing number of team members to manage!

Finding A Partner To Make The (Shared) Pie Bigger

While a solo financial advisor with a core team of staff support can grow an incredibly profitable personal practice, the reality is that at some point the advisor’s personal productivity just cannot be leveraged any further. The advisor’s time is consumed by a combination of serving a subset of existing clients, and managing the staff team that serves the rest. And while a very healthy income may result, it’s ultimately not even really a “business” in the truest sense of the word, because it’s still entirely dependent on the advisor’s own efforts, and would quickly vanish without the advisor’s involvement. And there’s certainly no time left to make the pie any bigger.

This becomes the classic point of transitioning to find and add a partner to the bsuiness. Because ultimately, the opportunity of having a partner is that having just a slice of a larger pie can still result in a bigger business that generates more income – particularly as it truly expands into a real business, that can survive beyond its dependency on any one person.

The key distinction of partnership businesses is the opportunity for the whole to be worth more than the sum of the parts – in other words, that two advisors together can build a larger combined business than either could alone.

To some extent, this is feasible simply by leveraging the available economies of scale in an advisory firm. Resources necessary to manage a growing team, from an Operations manager and HR functions, to procuring physical office space and technology support, are often more cost-efficient for larger firms than smaller firms (since many key supporting jobs don’t require twice the management to manage twice the people).

In other scenarios, partnership allows the joint business to grow larger than either would have been individually because the partners can each focus on what they do best, further amplifying their productivity. The partner who really thrives on business development can delegate all management tasks to the other partner who prefers to manage and develop the internal team, and the partner who prefers to manage the team can focus there without being ‘burdened’ by business development responsibilities that are not a core strength anyway.

Ultimately, though, the fundamental point is simply that partnerships survive and thrive when the shared pie is bigger than what any one partner could have produced alone. When the pie isn’t growing, adding a partner simply feels like a step backwards in income. When the pie is growing, partnership simply allows each partner to enjoy their share of the larger (and still growing) pie.

Complementary Advisor Skills To Make The Pie Bigger

A key distinction for advisors looking at potential partnership is to recognize that ultimately, while often advisors with strong business development skills and growth like to partner with other advisors who have strong business development skills, in many cases complementary skillsets (rather than identical/matching ones) can do even more to support the growth of the business and ensure business compatibility.

The reason is that as advisory firms grow and hire more employee advisors to support the partners/founders, the blocking point for future growth eventually shifts from being able to get clients and having the capacity to serve them, and instead is about the infrastructure necessary to manage that ever-growing team. And navigating this growth phase – which typically strikes as firms cross the $100M to $200M of AUM phase, and can continue all the way up to $1B of AUM or more – requires a substantively different set of skills, focused on management and the development of people, along with the building of systems and processes.

In other words, just bringing together multiple partners who are all good at business development may allow the firm to be somewhat larger than what either partner could do individually, but will eventually suffer if not further supported by a key employee – or increasingly often, a partner – who is skilled at the building of the business infrastructure and the managing of people. The partners must have compatible long-term goals for their complementary skillsets to work together, but the best partnerships are usually not ones where all the partners are good at the same thing(s).

And in point of fact, in many of the largest advisory firms, this structure is quite common, where one partner is the external “face” of and visionary for the firm (heavily responsible for business development), and another is the internal “integrator” that focuses on the building of the business.

Notably, the coming together of complementary skillsets is not only a phenomenon of larger firms that have hit a wall, either. In many cases, advisory partnerships are founded by those who have complementary skillsets in the first place. Whether it’s the business developer paired with a service-minded advisor to “do” the planner, or a financial planner partnered with someone who prefers to focus on portfolio management (where the combination of the two is a holistic wealth management offering), or a business visionary paired with an integrator to help implement it all, complementary partnership skillsets are often the most effective at rapidly building successful advisory businesses, by allowing each to focus on what they do best, from day 1.

Where To Find A Potential Business Partner?

For advisors who have hit “the wall” and are realizing they need a partner to climb over it, or perhaps are launching an advisory firm and wish to find a partner with a complementary skillset to grow more effectively from the start, there’s still one key question: how do you find the “right” partner in the first place?

In practice, I find that most advisors seem to find partners from their existing personal and professional networks – most commonly fellow advisors from their existing platform (e.g., at their current custodian or broker-dealer), or via a shared group affiliation (e.g., fellow advisors from the Financial Planning Association or NAPFA).

In turn, this implies that one significant virtue of going to financial advisor conferences is the opportunity to meet and “network” with other advisors, who may someday become business partners. Not because the advisor necessarily goes to the conference to find a partner, per se, but because the professional connections made there often turn into partnerships later as needs and circumstances change. Anecdotally, I find that most partnerships come about from advisors who have “known each other for years” and ultimately decided to either merge their practices, or form a new business together, because there was finally an alignment of goals and interests at a time that was mutually beneficial for both to pursue the effort.

Of course, an important caveat to coming together with another advisor as a partner is that it’s still crucial to assess the business compatibility of the partnership. The mere fact that both advisors were success individually does not mean they will be effective at working together in a common business, whether because their personality styles are too different to effectively communicate and make decisions, or because their underlying personal drivers and motivations are too different to formulate a shared and common vision. Fortunately, there are at least some “financial advisor partnership compatibility” tools to help make that assessment up front, but more generally potential partners should recognize that compatibility is not automatic just because each individual was successful.

The bottom line, though, is simply that while financial advisors can leverage themselves with technology and staff support, there is a real limit to how large virtually any advisory firm can grow before it becomes necessary for more owners to contribute to the common business good. The upside is that doing so makes it possible for the partners collectively to build a business larger than what any could have created alone. But doing so successfully requires that the partners actually be able to craft a shared vision and effectively make decisions to work towards it; merely being successful individuals is not enough to ensure that it will be even better to work together!

So what do you think? Are you considering whether to add a financial advisor partner? Where have you looked to find one? Were you a solo advisor who added a partner, and was able to grow the business even larger? Have you ever been a partner in a partnership that didn’t work out, and have some ‘lessons learned’ to share?