Executive Summary

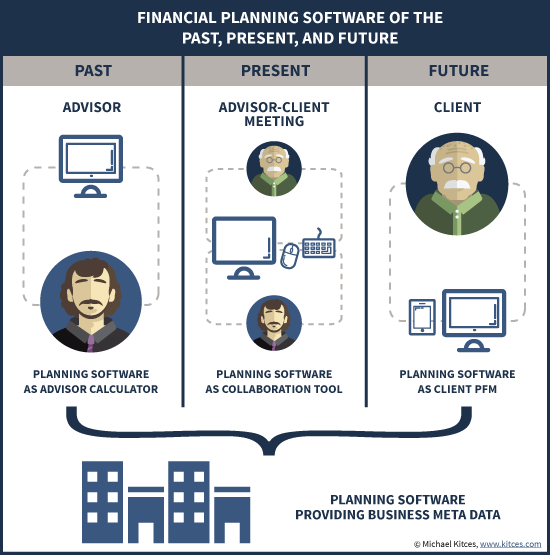

For much of its history, financial planning software was basically just an elaborate calculator. Advisors could gather client data, feed it as input to the calculator tool, and the software would spit out the projected results… which were then used to facilitate the sale of a product.

As financial planning has evolved to be primarily about the delivery of advice itself – not just for the sake of a product sale – so too has the software evolved, from a calculator to illustrate the outcome of a product or strategy recommendation, to a collaborative tool that can be used to formulate the client’s plan itself. After all, given the complexity of an uncertain future, it’s hard to really understand what path to pursue, until the client first analyzes a range of scenarios to understand the opportunities. Accordingly, financial planning software has increasingly become a tool for real-time collaborative scenario planning.

In the future, though, financial planning software can and will progress further, from a tool that supports collaboration at a single point in time, to one that truly supports continuous planning for the reality of continuous change we face in our lives. Imagine a holistic personal financial management (PFM) solution for clients, that simultaneously operates as financial planning software for the advisor, all continuously updated from external data flows, making it feasible for the advisor and client to see the milestones and recommendations that have already been accomplished, and whether the client is on track in progressing towards goals of the future.

Financial Planning Software Of The Past – The Advisor’s Calculator

Answering long-term questions like “am I on track for retirement” requires long-term projections, to understand whether someone’s current trajectory of spending and saving will get them to the desired goal. And between cash flow fluctuations (e.g., retirement savings are disrupted by college goals, but supplemented later by the sale of a business), different types of accounts with different tax status (taxable accounts, traditional retirement accounts, Roth retirement accounts, deferred annuities, 529 plans, and more), and the complexity of the tax system, it was generally easier to use a packaged financial planning software solution than build your own in Excel (though many advisors still do).

The efficiency and value-add of financial planning software was that it allowed advisors to input client data and facts, and get an output with the projected results, that could then be shared with clients. Such projections were too complex for most clients to do on their own, and again a packaged solution was generally still faster (and more accurate) than the advisor trying to do his/her own projections from scratch.

From the client’s perspective, the output of the planning software became a guidepost about whether the plan was “on track” or not, and whether the advisor could recommend any changes to improve the situation. Given that early on advisors were compensated primarily for the sale of (insurance and investment) products, financial planning software solutions effectively became a sales tool and part of the sales process.

Thus, the advisor Established a relationship with the client, Gathered data, Analyzed the data and various alternatives, Developed the plan recommendations, Implemented them with the client, and then Monitored for changes. This EGADIM (Establish, Gather, Analyze, Develop, Implement, Monitor) approach is still enshrined in the formal financial planning process, and financial planning software was the essential tool of the Analyze phase that could then drive forward to Developing the (product) recommendations. When the advisor said “Save this much more (in my fund solution), and here’s how your retirement improves” or “Fail to buy insurance and here’s how your spouse’s retirement and kids’ college plans will fall short,” the financial plan output was the analytical output to validate the advisor’s recommendation.

In its context of a calculator tool to facilitate doing projections that would support the sale of a product – a blend of financial educational and product/solution illustration – financial planning software worked reasonably well. However, as financial planning has increasingly evolved towards the advice itself being the value of the advisor-client relationship, the financial planning software of the past no longer addresses the needs of the present.

Financial Planning Software Of The Present – Real-Time Collaboration Tool

While the financial planning software of the past worked well enough to make a point or illustrate a specific concrete problem – and its potential (product-based) solution – it’s far more problematic to use as an actual planning tool with clients. The reason is that if the goal is to actually formulate a plan of what to do in the future, given a range of possible outcomes and the real-world uncertainty of life, it’s necessary to examine lots of different potential scenarios of how the future might play out.

In other words, if you’re just trying to just analyze the outcome of a particular path, you need a calculator to do the complicated math; but if you’re trying to formulate a plan amongst a complex range of multiple different potential paths, you need to simulate the potential outcomes of each path to understand the ramifications of proceeding in one directly versus another. In this role, the function of the financial planner is not to do the analysis (i.e., to provide the results of the software calculations), but to work collaboratively with the client to understand and interpret the results to come to a conclusion about how to move forward.

Source: Scenario Selling: Technology and the Future of Professional Selling by Sullivan & Lazenby

Of course, if the intention is to look at lots of different possible scenarios to formulate a plan for the future, it’s not very effective for the advisor to have to keep running back to his/her office to run a new “what if” alternative in the planning software and print it out. Instead, if planning software is going to be used to look at lots of different scenarios, it’s far more productive to bring the software into the conference room, and engage the process in real time with clients.

In turn, this shift of planning software from being “behind the scenes” to being face-to-face with clients has begun to drive a change in how planning software itself is being designed. Output is shifting from ledger-style tables into visual graphics. The interface is being modified so the plan inputs can be easily adjusted “on the fly” to illustrate alternative scenarios live and in real time, where the advisor – or even the client – can grab the mouse, and drag sliders to show how the plan outcomes shift as the assumptions are adjusted.

For instance, in recent years MoneyGuidePro launched its PlayZone, eMoneyAdvisor added its EMX Decision Center, and Advicent acquired Figlo to bring their more interactive financial planning tools to the US. In addition, Envestnet recently acquired FinanceLogix, an early leader in designing planning software with sliders that update in real time to be used interactively with clients.

While arguably some of these tools still have a bit of room for improvement, the financial planning software of today has clearly evolved from its roots of the past – from a planning calculator towards a truly collaborative planning tool.

Financial Planning Software Of The Future – A Continuous Planning Tool

While collaborative tools at the time of doing “the plan” is a good start, financial planning software is still lacking in the ongoing tools to facilitate ongoing collaborative planning.

In the context of the history of financial planning, this isn’t entirely surprising. The roots of planning – and the use of planning software – were in working towards a product sale. Planning occurred at a finite moment in time, drove towards a product to be implemented, and was “done”. At least, until the next finite moment to do a new/updated plan, and find a new opportunity for something to implement.

In reality, though, planning and goals are constantly evolving and changing. We are constantly progressing towards or away from goals, updating and changing those goals as our needs and priorities change, while looking back at the milestones that have been accomplished. Which means we need a better means to facilitate that monitoring and continuous planning process.

Some ways that financial planning software of the future may evolve to accommodate this include:

- Continuous Data Updates. Just as the idea of quarterly performance statements has slowly and steadily given way to client portals where account values and results are available 24 hours a day, 7 days a week, 365 days a year, so too will financial planning software soon progress to the point where advisors (and clients!) can log in 24/7/365 and see exactly where the current plan stands. The end result is that there will be no more “financial plan update” meetings, as planning software will always be updated, allowing it to support more fruitful ongoing planning conversations instead!

- Planning Software As Client PFM. From the advisor’s perspective, planning software is a calculation and collaboration tool. From the client’s perspective, it’s a Personal Financial Management (PFM) tool, helping clients be able to see at any time where they stand financially – everything from income to debt and savings to net worth – and be able to understand their progress towards goals and achieve significant milestones. The days of the financial advisor as the “gatekeeper” to the information in the financial plan is gone. The planning software is the client’s direct portal to that information, and the advisor helps the client on that journey.

- Tracking Plan Progression And Implementation Over Time. When planning software continuously tracks and updates, it also truly becomes possible to track the progression of a plan over time, including the implementation of the plan. After all, if clients will log into their planning software as their central PFM dashboard to keep track of their financial lives, that’s exactly where they should also get the gentle nudges and reminders of the plan recommendations they still need to implement. In addition, as plan recommendations are completed and checked off over time, the planning software can again become a living library of all the planning that has been done (which also helps advisors reinforce their value proposition by being able to show all that the client has achieved in their work together!).

- Cash Flow Tracking. A key opportunity for financial planning software of the future is cash flow tracking, where the continuous import of financial data makes it possible to actually get a handle on a household’s expenditures. Historically, many advisors have shied away from giving advice on cash flow and budgeting, due in no small part to the difficulty that clients have in tracking that information in the first place. When cash flow tracking becomes automatic, a whole new productive area of giving advice on managing household cash flow becomes feasible.

- Advisor Alerts. A key shift that will occur when planning software is continuously updated is that instead of advisors regularly contacting clients to “check in” just to see if anything has changed, they will instead be able to rely on their planning software to know if anything has changed (financially) and spot opportunities in advance of client communication. For instance, planning software might notify an advisor if a market decline has pulled a certain client’s ongoing retirement spending to a dangerous level, or if interest rates have declined enough that another client should refinance, or whether a client is ahead or behind on a savings goal. This allows for advisors to have more meaningful points of contact with clients, either to reinforce success, encourage an adjustment, or come to the table with an immediate planning opportunity. Notably, the ability for advisors to track and monitor automatically also creates a second layer of protection for oversight as well; for instance, imagine an advisor who spots questionable large transfers out of an elderly client’s checking account, and identifies that perhaps a family member is engaging in financial abuse or fraud.

- Client Alerts. In addition to planning software that alerts the advisor of planning opportunities or concerns, the software can also provide alerts directly to clients. This might be to warn a client that is going off track, or to reinforce client success. Proactive planning software alerts create the possibility for “gamification” of financial planning, where the software automatically gives rewards for successfully achieving goals (“Congratulations, you successfully stayed on budget for the third month in a row!”) that are so crucial to maintaining (financial) behavior change.

Beyond these enhancements, it’s also notable that a major opportunity for financial planning software of the future is to better allow financial plans to be built modularly over time, until they come together into the financial planning whole. Especially given that ultimately, most clients will seek out a financial planning for a specific solution to a specific problem – e.g., a “modular planning” issue – and only later broaden it to a more comprehensive relationship. Imagine planning software that can help deliver a college planning analysis on a standalone basis, but then be expanded to include a retirement plan projection, and then analyze cash flow and savings, and then support tax planning, etc. This allows financial plans to be built incrementally, over time, at a pace comfortable for a client, rather than forcing clients to do “everything” at once even if they’re not prepared to do so.

Given where we were not long ago, where financial planning software was primarily a behind-the-scenes calculator to analyze complicated problems and deliver a “recommendation” that would assist in the sale of a product, we’ve come a long way. Planning software is increasingly able to be used as a collaborative tool to facilitate real-time planning discussions. But there’s still ample room for further improvement to fully transform planning software into the continuous planning tool of the future that will truly support an ongoing financial planning relationship!

So what do you think? Are there other areas where you think financial planning software can/should improve? Would a solution that allows clients to continuously access their planning information make it easier to do planning with them, or threaten to replace the advisor altogether?